Scoring Balloon Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 487.35 Million |

| Market Size (2031) | USD 726.08 Million |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

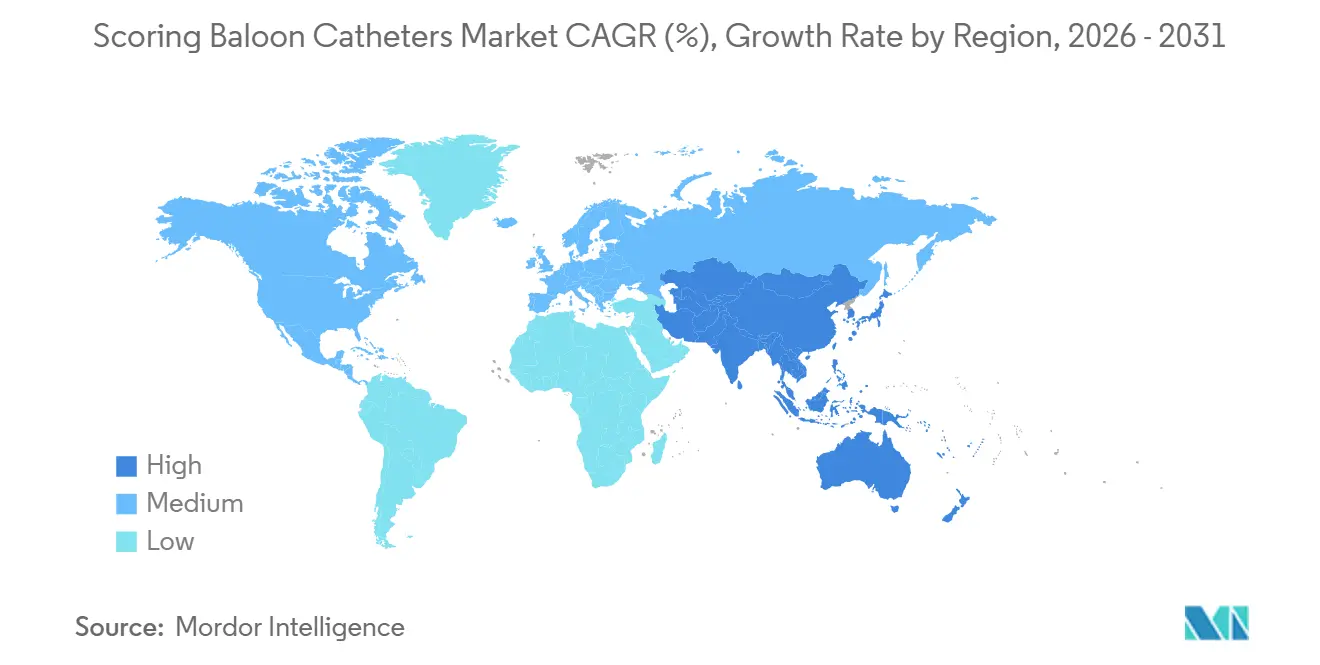

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

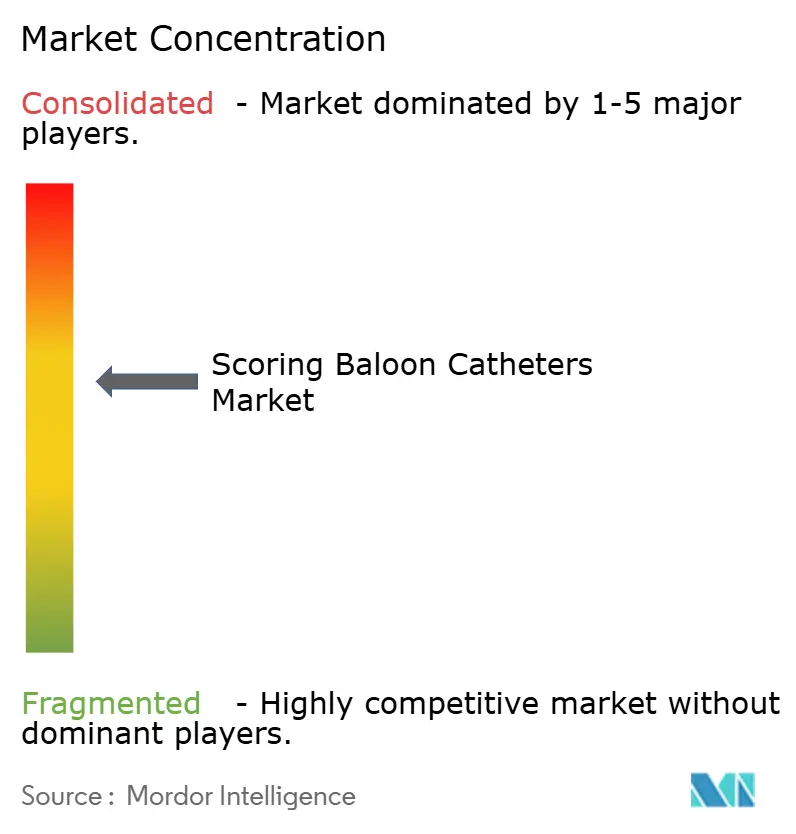

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Scoring Balloon Catheters Market Analysis by Mordor Intelligence

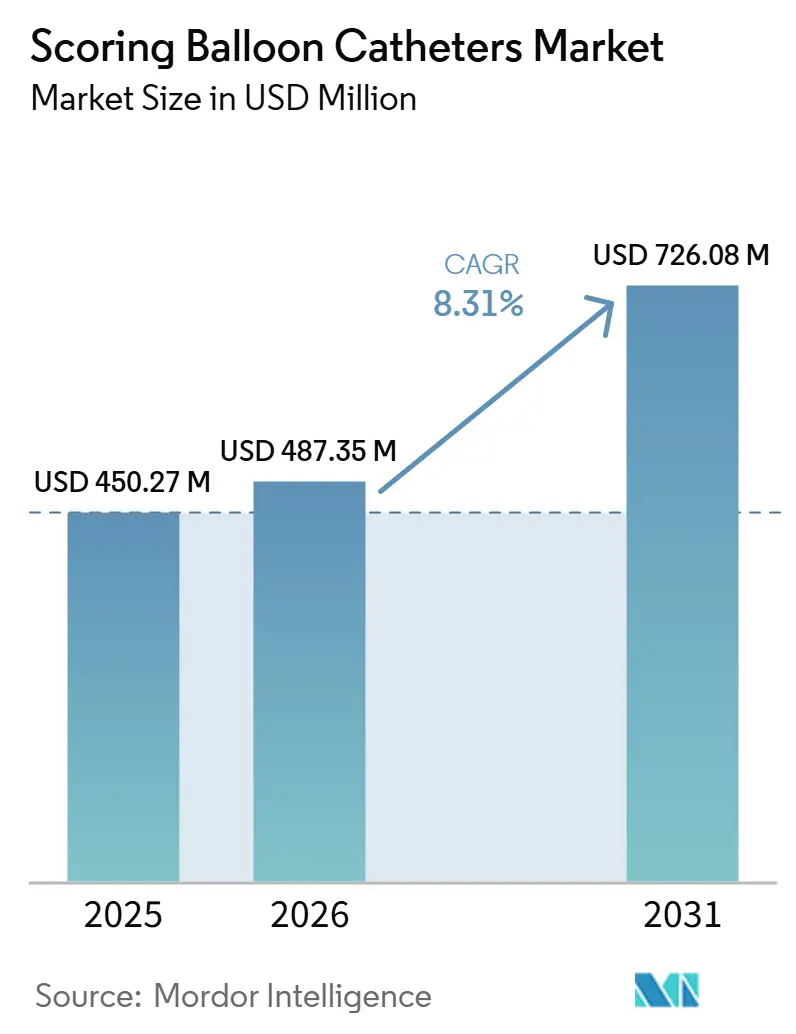

The Scoring Balloon Catheters Market size is expected to grow from USD 450.27 million in 2025 to USD 487.35 million in 2026 and is forecast to reach USD 726.08 million by 2031 at 8.31% CAGR over 2026-2031.

The scoring balloon catheters market is moving on the back of higher procedure volumes in both coronary and peripheral interventions, while calcified coronary lesions are becoming a more common challenge in PCI and are harder to manage with plain balloon angioplasty alone. The scoring balloon catheters market also benefits from a wider clinical shift toward more predictable lesion preparation before stenting, because physicians want more reliable stent expansion and fewer corrective steps later in the same procedure. Another layer of support comes from the expansion of PCI-capable cath labs and ambulatory settings, where interventional teams often prefer devices with familiar handling and shorter learning curves than atherectomy systems. The scoring balloon catheters market remains moderately concentrated, with established companies using integrated cath lab relationships, broad product portfolios, and ongoing product development to protect their position, while smaller players continue to widen the peripheral opportunity set. The main pressure on the scoring balloon catheters market comes from intravascular lithotripsy, yet randomized and trial-linked data support a meaningful cost advantage for balloon-based calcium modification at many hospitals.

Key Report Takeaways

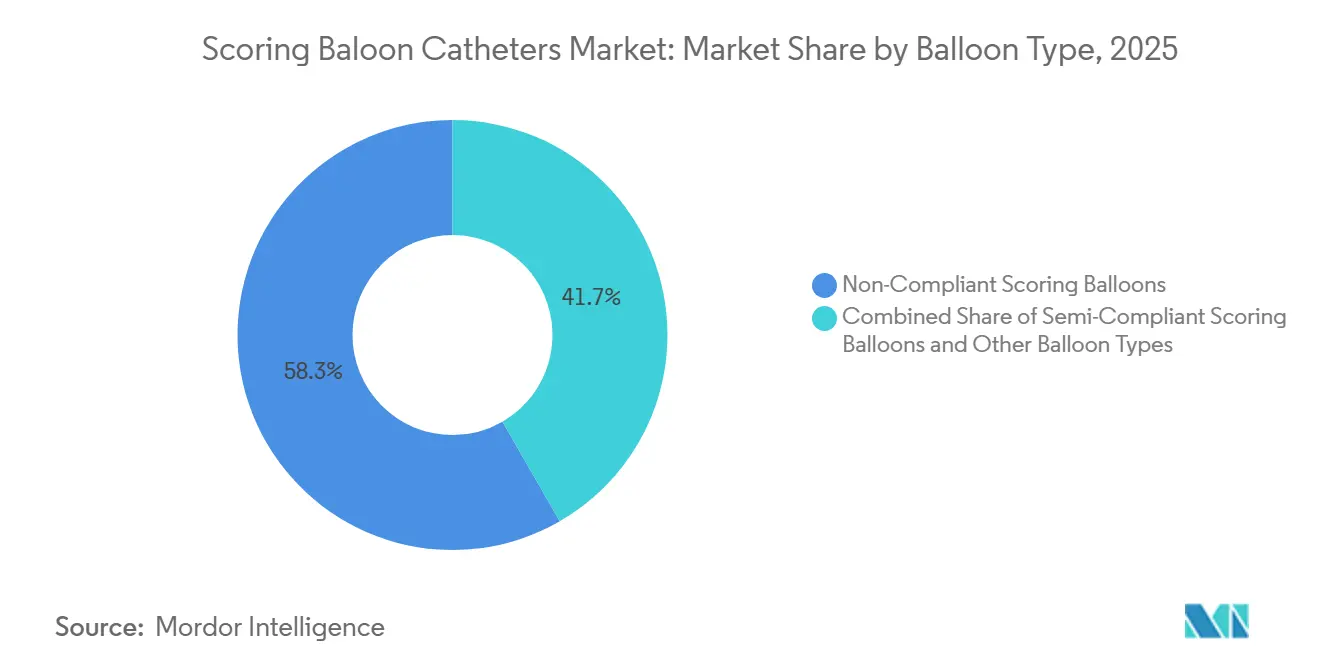

- By balloon type, non-compliant scoring balloons held 58.32% share in 2025 and are forecasted to expand at an 8.53% CAGR through 2031.

- By material, nylon held 52.19% share in 2025, while PET is forecasted to expand at an 8.60% CAGR through 2031.

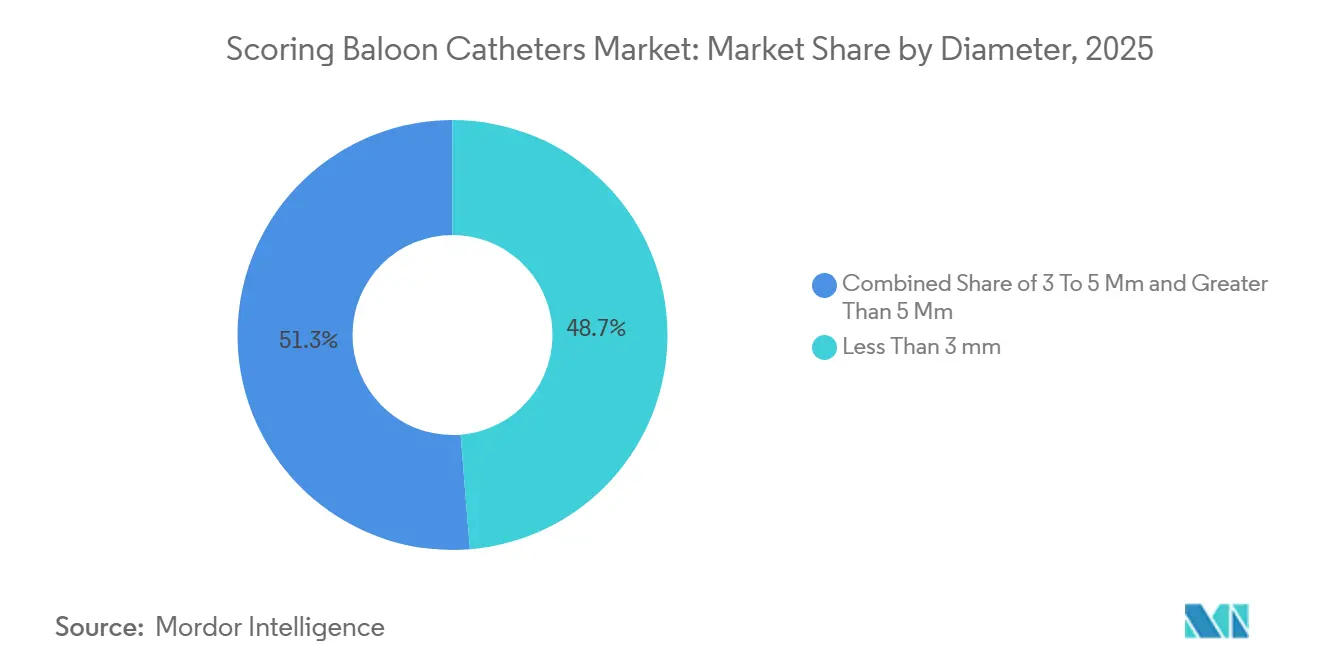

- By diameter, balloons less than 3 mm accounted for 48.71% share in 2025 is forecasted to expand at an 8.23% CAGR through 2031.

- By application, coronary accounted for 35.21% of the scoring balloon catheters market size in 2025, while peripheral is forecast to expand at an 8.47% CAGR through 2031.

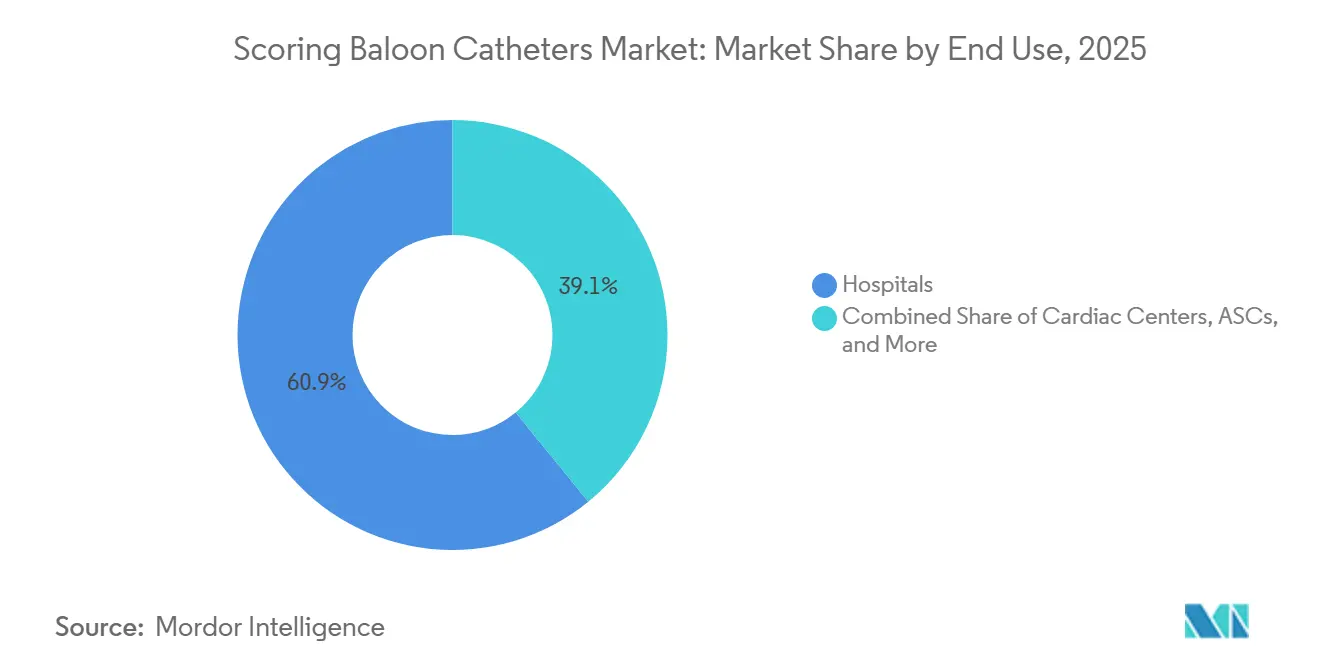

- By end use, hospitals held 62.10% of the scoring balloon catheters market share in 2025, while ambulatory surgical centers are projected to grow at a 9.56% CAGR through 2031.

- By geography, North America accounted for 38.10% of the scoring balloon catheters market size in 2025, while Asia-Pacific is projected to expand at a 9.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Scoring Balloon Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Calcified Coronary Lesions | +2.3% | Global, highest in North America, Europe, and Japan where aging populations overlap with high diabetes and CKD prevalence | Long term (≥ 4 years) |

| Shift Toward More Predictable Lesion Preparation Before Stenting | +1.7% | North America and Europe, with spillover to high-volume APAC centers | Medium term (2-4 years) |

| Expansion Of PCI-Capable Cath Labs And Ambulatory Settings | +1.4% | North America, APAC core, with spillover to MEA | Short term (≤ 2 years) |

| Clinical Preference For Lower Dissection And Better Stent Expansion Outcomes | +1.1% | North America and Europe, especially academic and regional hospitals | Medium term (2-4 years) |

| Underused Intravascular Imaging Supporting Precision Scoring | +0.7% | North America, with growing uptake in APAC and Europe | Long term (≥ 4 years) |

| Catheter Shaft Refinements Improving Trackability | +0.3% | Global, with fastest adoption in high-volume coronary centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden Of Calcified Coronary Lesions

Calcified coronary disease is becoming harder to ignore because published evidence shows calcium in 25% to 30% of patients presenting for PCI, and that burden rises with older age, diabetes, chronic kidney disease, and dyslipidemia. The scoring balloon catheters market gains from this pattern because rigid lesions often do not respond well to plain balloon dilation and require more controlled focal force before stent placement. It is also noted that severely calcified lesions were associated with a 62% higher risk of 1-year adverse outcomes after PCI, which makes lesion preparation more central to routine procedural planning[1]Source: National Center for Biotechnology Information, “Calcified Lesion Outcomes After PCI,” PubMed Central, pmc.ncbi.nlm.nih.gov. Intravascular ultrasound adds to the demand picture because it reveals more calcium than angiography alone, and the rising IVUS-guided PCI use in Medicare cases leads to stronger recognition of lesions that need specialized preparation. The scoring balloon catheters market, therefore, benefits not only from a larger disease burden but also from better detection of lesion complexity during case planning.

Shift Toward More Predictable Lesion Preparation Before Stenting

Physicians are placing more value on a more predictable preparation step because inadequate lesion modification remains one of the clearest causes of stent underexpansion, restenosis, and thrombosis in complex coronary work. The scoring balloon catheters market is supported by the meta-analysis, which found a 33% lower target lesion revascularization risk for cutting and scoring balloons versus conventional balloons in native coronary disease[2]Source: REC Interventional Cardiology, “Naviscore First-In-Man Study,” REC Interventional Cardiology, recintervcardiol.org. That pattern matters at the hospital level because operators increasingly want the lesion addressed well before the stent is placed, rather than relying on a bailout step after suboptimal stent expansion is already visible. Naviscore first-in-man study across 10 European centers, where 85 patients recorded a 94% procedural success rate and 7.50% residual stenosis after stent implantation, with no in-hospital major adverse cardiac events. The scoring balloon catheters market, therefore, gains when hospitals and physicians judge lesion preparation by total case efficiency and final implant quality, not only by the acquisition cost of the balloon.

Expansion Of PCI-Capable Cath Labs And Ambulatory Settings

The scoring balloon catheters market is also tied to the expansion of procedural capacity, especially where selected cardiovascular interventions are shifting from inpatient settings into ambulatory sites. CMS added hundreds of cardiovascular procedure codes to the ASC Covered Procedures List in January 2026, and that change broadened the procedural settings where coronary and peripheral work can be performed. The announcement of a dedicated cardiovascular ASC in Delaware with two cardiac catheterization and electrophysiology labs for coronary and peripheral vascular interventions. This shift matters for the scoring balloon catheters market because ASC-based teams often prefer devices that are familiar, straightforward to use, and less operationally demanding than atherectomy systems. The scoring balloon catheters market is therefore well-positioned in care settings that want controlled lesion preparation without the added complexity of capital-intensive plaque modification platforms.

Clinical Preference For Lower Dissection And Better Stent Expansion Outcomes

The scoring balloon catheters market is also supported by a clinical preference for lower dissection risk and more reliable stent expansion, especially in lesions where vessel injury can change the final result. The University of East Anglia single-center study found scoring balloon pre-dilation was an independent predictor of better angiographic outcomes and was associated with a lower risk of severe dissection than conventional balloons in drug-coated balloon angioplasty. It is also cited randomized data on the Wedge NC scoring balloon, which confirmed non-inferiority versus conventional balloon angioplasty and showed superior stent expansion. That matters for the scoring balloon catheters market because operators are increasingly unwilling to accept vessel preparation that raises the chance of poor stent geometry or downstream corrective work. The scoring balloon catheters market gains when physicians view scoring pre-dilation as a consistent step in calcified or difficult lesions rather than as an occasional add-on.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Per-Procedure Cost Versus Conventional Balloons | -1.3% | Global, most pronounced in cost-sensitive settings in APAC, MEA, and South America where plain balloons are the default | Medium term (2-4 years) |

| Competition From Intravascular Lithotripsy And Atherectomy Platforms | -1.0% | North America and Europe, where IVL uptake is accelerating in hospitals with complex calcium case volumes | Long term (≥ 4 years) |

| Limited Operator Familiarity In Lower-Volume Centers | -0.6% | APAC periphery, MEA, and South America, especially rural or tier 3 hospitals | Long term (≥ 4 years) |

| Reimbursement Pressure For Adjunctive Plaque Modification Devices | -0.5% | North America and Western Europe, where device bundling can constrain separate billing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Per-Procedure Cost Versus Conventional Balloons

The scoring balloon catheters market still faces a clear pricing hurdle because scoring balloons carry a premium over standard PTCA balloons, and that difference matters in systems operating under fixed or tightly managed reimbursement. This pressure is sharper in hospitals that do not handle large calcified case volumes, because procurement teams may default to plain balloons unless clinical protocols clearly define when scoring devices are necessary. China’s procurement environment as structurally tougher for imported devices, with domestic alternatives such as MicroPort’s FireFalcon adding pricing pressure in coronary intervention. That makes premium positioning harder to defend, even when multinational products have established clinical familiarity or broader global brand recognition. The scoring balloon catheters market, therefore, needs hospitals to see a clear procedural value in better lesion preparation if suppliers want to hold pricing above conventional balloon levels.

Competition From Intravascular Lithotripsy And Atherectomy Platforms

The most direct product challenge to the scoring balloon catheters market comes from intravascular lithotripsy, which offers a simple method for cracking superficial and deep calcium with a limited learning curve. Boston Scientific’s SEISMIQ 4CE coronary IVL catheter met its primary safety and effectiveness endpoints at EuroPCR 2026, with 93.30% freedom from MACE and 93.70% procedural success, which supports a future U.S. regulatory filing. That progress raises pressure on the scoring balloon catheters market in heavily calcified lesions, where hospitals may compare several plaque-modification options side by side. At the same time, the Short-CUT randomized trial presented at TCT 2025, where cutting balloons were non-inferior to IVL and carried a USD 3,632 lower cost per procedure. The scoring balloon catheters market, therefore, remains competitive, but it still has a strong value argument in settings where hospitals must balance procedural outcome with device cost

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Balloon Type: Non-Compliant Design Dominates Lesion Preparation Workflow

Non-compliant scoring balloons held 58.32% of the market by balloon type in 2025, which kept this format at the center of current lesion preparation practice. The scoring balloon catheters market continues to favor non-compliant designs because they are better suited to the precise, high-pressure inflation cycles needed to crack dense coronary calcium without overstretching the vessel wall. Abbott’s Scoreflex NC, as a practical example, has a rated burst pressure of 20atm and a crossing profile of 0.0343 inches, which reflects the category’s focus on controlled expansion and deliverability. Its external nitinol scoring wires are designed to generate focal stress that fractures calcium at lower nominal pressures than a plain non-compliant balloon while maintaining dimensional control.

The scoring balloon catheters market still leaves room for semi-compliant designs, but their role remains narrower and more selective. Their position in lesions where some controlled vessel compliance is preferred, especially in bifurcation disease or sequential vessel engagement strategies. That niche matters, but it has not displaced the stronger physician preference for rigid, predictable inflation in dense calcified disease. The scoring balloon catheters market therefore remains anchored in non-compliant formats because operator familiarity and cath lab protocols still support that design as the default for difficult coronary preparation. This concentration in one balloon type also gives established suppliers a durable advantage, because once a design is embedded in routine workflow, switching behavior tends to slow unless a clearly better outcome or cost profile appears.

By Material: PET Gaining Ground As Precision Requirement Rises

Nylon accounted for 52.19% of the material segment in 2025, which kept it in the lead across the present installed product base. The scoring balloon catheters market has relied on nylon because it offers a useful balance between trackability in tortuous coronary anatomy and radial strength that remains suitable for many coronary scoring applications. That balance matters because many operators still judge a balloon first by how well it crosses the lesion and follows the wire through tight anatomy. Nylon also fits the current coronary-heavy volume pattern in the scoring balloon catheters market, where deliverability often decides whether a device is practical in real cases. For those reasons, nylon continues to hold a large share even as material preferences evolve around tighter dimensional behavior.

PET is the fastest-growing material segment and is projected to expand at an 8.60% CAGR through 2031, which reflects the rising value of dimensional precision in high-pressure use. Growth to a greater need for balloons that resist deformation and hold a more exact profile during inflation, especially in complex calcified lesions. This shift matters in the scoring balloon catheters market because more demanding lesion preparation leaves less tolerance for shape drift at peak pressure. It is also noted that ISO 10555-1 and related standards are pushing manufacturers toward more traceable performance certification, which can raise the qualification bar for newer entrants while favoring suppliers with validated polymer systems. Polyurethane and other materials still remain relevant in more flexible peripheral or smaller-gauge catheter designs, but the scoring balloon catheters market is clearly giving more attention to materials that support tighter control under demanding inflation conditions.

By Diameter: Less Than 3mm Segment Anchors Volume Across Coronary Applications

The less than 3mm diameter segment accounted for 48.71% of the market in 2025, which shows how strongly current demand remains tied to coronary lesion treatment. The scoring balloon catheters market depends heavily on this size range because many calcified coronary lesions appear in vessels where oversizing quickly raises the risk of dissection and poor final vessel geometry. Small-vessel intervention also leaves little room for inflation error, which makes controlled plaque modification more valuable before a drug-eluting stent is placed. This is why the scoring balloon catheters market continues to draw a large share of its procedural volume from devices built for small coronary diameters.

A 2025 optical coherence tomography study across 3 Japanese hospitals was conducted, where calcium fracture was achieved in 5 of 7 cases treated with a novel scoring balloon in severely calcified lesions with substantial calcium arc. That finding supports the importance of small-diameter scoring devices in lesions where both vessel size and calcium burden complicate treatment. The 3mm to 5mm segment serves larger coronary vessels and part of the proximal peripheral opportunity, while devices above 5mm remain more closely tied to peripheral interventions such as iliac and femoropopliteal work. Even with peripheral expansion, the scoring balloon catheters market still tells a predominantly coronary volume story when diameter demand is examined in detail. This sizing pattern also explains why companies continue to focus product development on trackability and crossing performance in the less than 3mm range.

By Application: Peripheral Growth Accelerates As Device Portfolio Expands

Coronary accounted for 35.21% of the scoring balloon catheters market size in 2025, which kept it as the leading application segment even as the category broadened into more vascular beds. The scoring balloon catheters market remains rooted in coronary procedures because calcified coronary lesions continue to drive the need for focal plaque modification before stent deployment. Coronary use also has the strongest link to intravascular imaging, stent optimization, and large hospital purchasing patterns, which gives it a central role in product validation and physician familiarity. That said, the conventional PTCA balloons still dominate first-pass pre-dilation at many centers outside the calcified lesion subset. This means the scoring balloon catheters market still has room to deepen coronary penetration even before considering new peripheral opportunities.

Peripheral is the fastest-growing application and is projected to expand at an 8.47% CAGR through 2031, as endovascular-first treatment approaches extend scoring balloon use across carotid, lower limb, and renal indications. The FDA clearance for DK Medical Technology’s D-Kutting LL peripheral scoring balloon in April 2025 and Goodman Co.’s Aperta NSE PTA Balloon Dilatation Catheter in April 2025, which together expanded the cleared peripheral device set. That wider choice set matters because peripheral specialists need more variation in length, diameter, and lesion approach than standard coronary workflows require. Cagent Vascular’s POINT FORCE registry, which was initiated in January 2025 to generate real-world evidence for the Serranator serration balloon catheter in complex peripheral artery disease. The scoring balloon catheters market therefore has a stronger second growth engine in peripheral intervention than it did even a few years ago, and new clearances are helping make that expansion more durable.

By End Use: Hospitals Anchor Volume While ASCs Drive The Growth Narrative

Hospitals accounted for 62.10% of the end-use market in 2025, which made them the clear anchor for present procedural volume. The scoring balloon catheters market still depends on hospitals because complex PCI capabilities, catheterization labs, cardiac surgery backup, and higher-acuity patient handling have historically remained concentrated in inpatient environments. Cardiac centers form the next layer of demand because they capture specialist coronary volume that often exceeds the capacity or experience of smaller community hospitals. That structure gives the scoring balloon catheters market a stable core, since the most difficult calcified cases are still more likely to be handled in larger institutions with deeper interventional support. It also means that leading suppliers can protect their share through long-standing hospital relationships and broader cath lab coverage rather than through standalone device selling alone.

Ambulatory surgical centers are the fastest-growing end-use segment and are projected to expand at a 9.56% CAGR through 2031. The scoring balloon catheters market is well aligned with that shift because ASC procurement teams often prefer solutions that balance procedural effectiveness with operational simplicity and lower equipment burden. This trend to the 2026 CMS expansion of cardiovascular ASC codes and to the broader move of lower-acuity coronary and peripheral interventions away from full hospital settings[3]Source: Ambulatory Surgery Center Association, “ASC Covered Procedures List Updates,” Ambulatory Surgery Center Association, ascassociation.org. It also cited ChristianaCare’s 2026 cardiovascular ASC announcement, which provides a direct example of how future procedure capacity is being built in this setting. As a result, the scoring balloon catheters market is positioned to benefit when outpatient cardiovascular sites look for lesion preparation devices that are effective, familiar, and easier to integrate into a high-throughput workflow.

Geography Analysis

North America held 38.10% of the scoring balloon catheters market share in 2025, which made it the largest regional segment by value. The scoring balloon catheters market in North America is anchored by the United States, where PCI volumes remain high and private hospital infrastructure is dense across leading interventional networks. Another important support comes from reimbursement and site-of-care policy, because CMS added hundreds of cardiovascular procedure codes to the ASC Covered Procedures List in January 2026, which widened the settings where scoring balloons can be used. It is pointed to BD’s UltraScore clearance in February 2026, and the 30-day FDA review cycle suggested rising regulatory familiarity with this device class for iterative product improvement.

Europe remains the second-largest regional market, and the scoring balloon catheters market there is supported by countries such as Germany, the United Kingdom, France, Italy, and Spain. Procedure demand is linked to established statutory coverage for coronary and peripheral interventions, while regulatory expectations under the EU Medical Device Regulation keep evidence standards high for new device entry. That creates a market structure that favors companies with stronger clinical data packages and broader post-market support. The Naviscore first-in-man study across 10 centers in Spain and Portugal, which added regional clinical evidence for a next-generation axial scoring design and can influence hospital procurement thinking in Europe.

Asia-Pacific is the fastest-growing region at a 9.91% CAGR through 2031, and the scoring balloon catheters market is benefiting there from larger procedure volumes, expanding hospital capacity, and a wider mix of domestic and imported devices. China supports that growth through a dual-track structure where premium imported devices serve major urban centers, while domestically approved products move more aggressively into provincial hospitals. MicroPort’s FireFalcon coronary scoring balloon approval in November 2024 as a clear example of how domestic offerings are expanding in the Chinese market. Japan remains important because device uptake there depends heavily on local evidence and physician confidence in specialized coronary tools. India and South Korea also add to the scoring balloon catheters market through hospital expansion and technology-ready cath lab infrastructure in high-growth urban systems. The Middle East and Africa remain smaller in absolute terms, but GCC investment in advanced cardiac intervention capacity gives the region strategic importance. South America is improving from a lower base, though the reimbursement and economic pressure as limits on faster movement away from conventional balloons in public hospital networks.

Competitive Landscape

The scoring balloon catheters market operates with moderate concentration at the global level, and Boston Scientific, Medtronic, and Abbott Laboratories are the leading manufacturers shaping the pace through integrated cath lab platforms, broad product portfolios, and meaningful R&D depth. The scoring balloon catheters market favors these companies because interventional customers often buy across a full procedural ecosystem rather than around one device line in isolation. Large suppliers also benefit from deeper relationships with high-volume hospital accounts, stronger distribution coverage, and the ability to support both coronary and peripheral practice patterns. That makes competitive entry difficult for smaller companies unless they offer a clear advantage in niche performance, pricing, or indication coverage.

Boston Scientific’s position illustrates how the market is evolving on two fronts at once. On one side, the company remains part of the established scoring balloon competitive set through its broader interventional footprint in high-volume cath labs. On the other side, Boston Scientific is also raising pressure on the scoring balloon catheters market through the progress of its SEISMIQ 4CE coronary IVL catheter, which met key endpoints at EuroPCR 2026 and supports a future U.S. filing. Abbott remains relevant through established coronary intervention products such as Scoreflex NC, while Medtronic benefits from scale and broader cardiovascular relationships that keep it visible in hospital purchasing decisions.

The next layer of competition comes from specialist and regional companies that are widening product choice in parts of the market where the largest groups are not yet dominant. MicroPort stands out because of its strategy to both domestic Chinese calcium modification breadth and wider U.S. coronary portfolio expansion through the April 2026 FDA clearance of Firefighter Pro. Goodman Co. and DK Medical Technology have added peripheral scoring options through FDA clearances that expand the addressed lesion set outside standard coronary use. Cagent Vascular is using the POINT FORCE registry to build the real-world evidence base around its serration balloon platform in complex peripheral artery disease. The scoring balloon catheters market is therefore likely to see the strongest competitive moves around sub-3mm coronary trackability, evidence-backed peripheral adoption, and the ability to defend value against IVL rather than on simple device breadth alone.

Scoring Balloon Catheters Industry Leaders

Boston Scientific Corporation

Medtronic Plc

Abbott Laboratories

Cardinal Health, Inc.

Cook Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: BD's Bard Peripheral Vascular Receives FDA Clearance for UltraScore Focused Force PTA Balloon. The FDA cleared the UltraScore under K260012 in 30 days, which reflected substantial equivalence to predicate scoring balloons and signaled regulatory maturity in this device class. The clearance expands BD's peripheral scoring balloon presence in the U.S. ambulatory and hospital market

- April 2025: BD's Bard Peripheral Vascular Receives FDA Clearance for UltraScore Focused Force PTA Balloon. The FDA cleared the UltraScore under K260012 in 30 days, which reflected substantial equivalence to predicate scoring balloons and signaled regulatory maturity in this device class. The clearance expands BD's peripheral scoring balloon presence in the U.S. ambulatory and hospital market

Global Scoring Balloon Catheters Market Report Scope

As per the scope of the report, scoring balloon catheters are specialized angioplasty devices used in endovascular and percutaneous coronary interventions to modify atherosclerotic plaque and prepare lesions prior to balloon angioplasty, stent implantation, or other vascular interventions. These catheters incorporate scoring elements, such as wires, struts, or scoring structures, on the balloon surface that create controlled focal force during inflation, facilitating plaque fracture while minimizing vessel trauma and balloon slippage. Scoring balloon catheters are designed to improve lesion preparation, optimize vessel expansion, enhance procedural outcomes, and support the treatment of complex, calcified, and resistant vascular lesions.

The scoring balloon catheters market is segmented by balloon type into semi-compliant scoring balloons, non-compliant scoring balloons, and other balloon types; by material into nylon, polyethylene terephthalate (PET), polyurethane, and other materials; by diameter into less than 3 mm, 3 to 5 mm, and greater than 5 mm; by application into coronary and peripheral applications, with peripheral further segmented into carotid, lower limb, renal, and other peripheral applications; and by end use into hospitals, cardiac centers, ambulatory surgical centers, and other end users; and by geography into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Semi-Compliant Scoring Balloons |

| Non-Compliant Scoring Balloons |

| Other Balloon Types |

| Nylon |

| Polyethylene Terephthalate |

| Polyurethane |

| Other Material |

| Less Than 3 Mm |

| 3 To 5 Mm |

| Greater Than 5 Mm |

| Coronary | |

| Peripheral | Carotid |

| Lower Limb | |

| Renal | |

| Others |

| Hospitals |

| Cardiac Centers |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Balloon Type | Semi-Compliant Scoring Balloons | |

| Non-Compliant Scoring Balloons | ||

| Other Balloon Types | ||

| By Material | Nylon | |

| Polyethylene Terephthalate | ||

| Polyurethane | ||

| Other Material | ||

| By Diameter | Less Than 3 Mm | |

| 3 To 5 Mm | ||

| Greater Than 5 Mm | ||

| By Application | Coronary | |

| Peripheral | Carotid | |

| Lower Limb | ||

| Renal | ||

| Others | ||

| By End Use | Hospitals | |

| Cardiac Centers | ||

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in scoring balloon catheters through 2031?

Growth is tied to more calcified coronary lesions, wider use of structured lesion preparation before stenting, and expansion of PCI-capable hospital and ASC settings.

How large is the scoring balloon catheters space in 2026 and 2031?

The scoring balloon catheters market size stands at USD 487.35 million in 2026 and is projected to reach USD 726.08 million by 2031 at an 8.31% CAGR.

Which application area remains the largest today?

Coronary led applications with 35.21% share in 2025, reflecting the category's strong role in calcified coronary lesion preparation before stent placement.

Which end-user group is growing the fastest?

Ambulatory surgical centers are expanding the fastest with a 9.56% CAGR through 2031, supported by the 2026 expansion of cardiovascular ASC procedure codes.

Why do non-compliant scoring balloons lead the product mix?

They held 58.32% share in 2025 because operators value their precise, high-pressure inflation behavior in dense calcified lesions.

What is the biggest competitive threat to this category?

Intravascular lithotripsy is the clearest product threat, although a USD 3,632 per-procedure cost advantage for balloon-based options in a key randomized comparison.

Page last updated on: