Saudi Arabia Health Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.83 Billion |

| Market Size (2026) | USD 3.03 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Health Drinks Market Analysis by Mordor Intelligence

The Saudi Arabia health drinks market size is expected to reach USD 2.83 billion in 2025 and USD 4.49 billion by 2031, registering a CAGR of 8.2% during 2026-2031. The market is growing as consumers spend more on wellness, fitness, and convenient nutrition. Higher gym participation is increasing demand for hydration, energy, and recovery drinks, while rising disposable incomes support premium functional beverages. Vision 2030 continues to promote healthier lifestyles, sports participation, and better nutrition standards. Stricter labeling rules are also pushing brands to improve product claims, formulations, and compliance, making credibility and distribution strength key to growth.

Key Report Takeaways

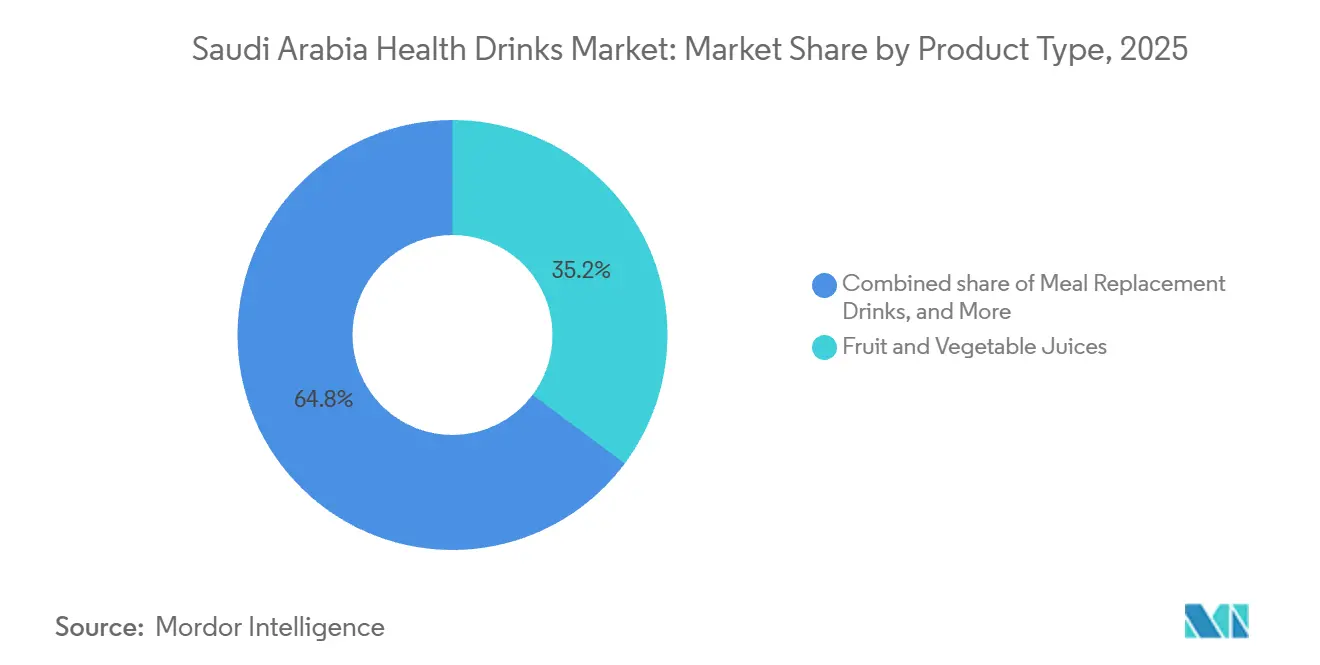

- By product type, fruit and vegetable juices led with 35.2% of the Saudi Arabia health drinks market share in 2025, while herbal and adaptogenic drinks are forecast to expand at a 9.2% CAGR through 2031.

- By packaging type, bottles accounted for 41.2% of the Saudi Arabia health drinks market size in 2025, while Tetra Packs are projected to grow at an 8.8% CAGR through 2031.

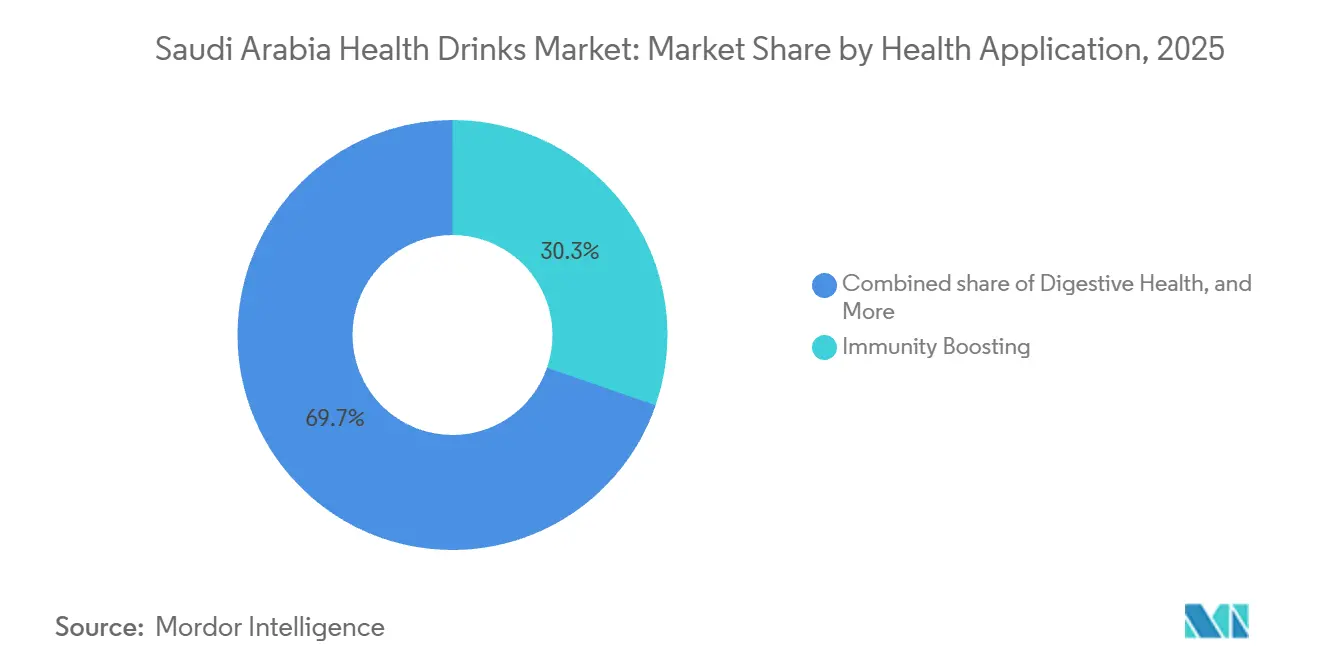

- By health application, immunity boosting held a 30.3% share of the Saudi Arabia health drinks market size in 2025, while digestive health is advancing at a 10.7% CAGR through 2031.

- By distribution channel, hypermarkets and supermarkets captured 42.7% of the Saudi Arabia health drinks market share in 2025, while specialty stores are forecast to record a 9.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Health Drinks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health Consciousness | +1.2% | National, strongest in Riyadh and Jeddah urban corridors | Medium term (2-4 years) |

| Growing Demand for Functional Beverages | +1.0% | Global, most concentrated in KSA urban markets | Medium term (2-4 years) |

| Busy And Active Lifestyles | +0.7% | Urban KSA, especially Riyadh, Jeddah, and Dammam | Short term (≤ 2 years) |

| Increasing Fitness And Sports Participation | +0.6% | National, with notable acceleration in the 18-29 age group | Medium term (2-4 years) |

| Influence Of Social Media And Digital Marketing | +0.5% | National, with early gains in Gen Z and millennial demographics | Short term (≤ 2 years) |

| Product Innovation And Flavor Variety | +0.4% | Global, with localization gains in Saudi Arabia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness

Health awareness in Saudi Arabia is now shaping beverage choices in a more direct and sustained way across age groups. The General Authority for Statistics survey cited by the Saudi Sports for All Federation showed that 59.1% of Saudi adults aged 18 and above completed at least 150 minutes of physical activity per week in 2025, up from 13% in 2018. The 18-29 age group recorded the highest participation rate at 71.2%, which matters because younger consumers are also more open to trying new hydration and recovery formats. This change supports the Saudi Arabia health drinks market because consumers who exercise regularly tend to pay closer attention to ingredient labels, sugar levels, and functional claims. It also strengthens repeat demand rather than one-time trial, since beverages linked to hydration, energy, and recovery fit more easily into weekly routines. The Saudi Arabia health drinks market therefore benefits not only from broader awareness, but from a more regular pattern of health-focused consumption.

Growing Demand for Functional Beverages

The Saudi Arabia health drinks market is also being lifted by stronger demand for beverages that offer a clear use case, such as immunity support, digestive comfort, hydration, or energy. Consumers are moving beyond plain refreshment and are increasingly looking for products that fit a personal routine or a specific physical need. This shift gives functional beverages a stronger shelf position because purchase decisions are becoming more purpose-led than impulse-led in several urban channels. Brands that can explain what the product does, how it fits daily wellness, and why the formulation is credible are gaining a clearer path to relevance. The result is a category mix that is gradually tilting toward beverages with defined benefits instead of broad lifestyle messaging alone. That transition supports the Saudi Arabia health drinks market because it raises both product value perception and the willingness to pay for differentiated formats.

Increasing Fitness and Sports Participation

Fitness participation has become a practical demand driver for the Saudi Arabia health drinks market rather than a broad lifestyle theme. The same national activity data showed strong momentum among women as well as younger consumers, which widens the addressable base for sports hydration, herbal energy, and recovery beverages. This matters because categories once centered on a narrower male consumer set are now reaching a broader range of buyers with different routines and purchase occasions. Rising participation also helps specialized beverages enter more parts of the day, including pre-workout, post-workout, and general hydration use. As activity levels become more normalized, retail buyers have greater reason to expand assortment in sports and functional drink shelves. That makes the Saudi Arabia health drinks market more resilient because demand is tied to habit formation rather than short-lived novelty.

Influence of Social Media and Digital Marketing

Digital platforms are shaping product discovery and brand credibility across the Saudi Arabia health drinks market. The Saudi Center for Opinion Polling reported in 2025 that 99% of Saudis actively use social media, which gives health beverage brands a very large and highly connected audience for education, trial, and community building. This matters more in health drinks than in many beverage categories because ingredient transparency and functional benefits can be explained quickly through short videos and influencer-led demonstrations. It also lowers the entry barrier for emerging brands that do not have the trade spending power of larger multinational companies. Social media can therefore shorten the time between product launch and consumer recognition, especially in herbal, probiotic, and premium wellness categories. The Saudi Arabia health drinks market gains from this because awareness, aspiration, and purchase intent can now move faster than traditional shelf-based discovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Environment | -0.9% | National, with early compliance pressure in Riyadh and Jeddah | Medium term (2-4 years) |

| High Scrutiny Of Health Claims | -0.7% | National, with international alignment across EFSA, FDA, and Codex references | Long term (≥ 4 years) |

| Competition From Established Beverage Categories | -0.5% | National, across urban and semi-urban markets | Short term (≤ 2 years) |

| Short Product Shelf-Life In Some Categories | -0.3% | National, most acute beyond major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Environment

The Saudi Arabia health drinks market is facing a tougher compliance environment that improves quality standards but also slows some launches and raises execution costs. The Saudi Food and Drug Authority stated in its annual report that it issued more than 60 new laws and guidelines across food, drug, and medical device sectors in 2024. This pace of rulemaking shows that regulation is becoming more active and more detailed at the same time[1]Source: Saudi Food and Drug Authority, “SFDA Annual Report January 2025”, sfda.gov.sa. For health drink brands, that means formulation, labeling, documentation, and market entry planning need to be aligned much earlier in the product cycle. It also creates a stronger advantage for companies that already have regulatory teams, testing resources, and experience handling structured approval processes. The Saudi Arabia health drinks market therefore remains attractive, but the path from concept to shelf is becoming more demanding for smaller and less prepared operators.

High Scrutiny of Health Claims

Health claim scrutiny is another meaningful restraint across the Saudi Arabia health drinks market, especially in categories built around herbal, probiotic, or adaptogenic positioning. Claims linked to immunity, digestion, stress relief, or performance can attract attention quickly, but they also face closer review when supporting evidence is weak or inconsistently presented. This raises the cost of commercialization because brands need stronger documentation, cleaner messaging, and clearer boundaries between wellness language and therapeutic implication. The challenge is more visible in fast-growing subcategories where the pace of innovation can run ahead of the pace of claim validation. Larger multinational and well-funded regional players are better placed to manage this because they can spread regulatory costs across broader portfolios. As a result, the Saudi Arabia health drinks market is growing, but health-positioned differentiation cannot rely on marketing language alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Juices Hold Ground While Herbal Formats Accelerate

Fruit and vegetable juices are expected to account for 35.2% of the Saudi Arabia health drinks market in 2025, remaining the largest product type by value. Their lead reflects strong consumer familiarity, wide modern retail distribution, and daily use in households before functional beverages expanded the category. Consumers also find juices easy to understand, compare, and repurchase, especially from brands with a strong local presence and steady shelf visibility. In the Saudi Arabia health drinks market, traditional juices connect routine consumption with health positioning without requiring major behavior change. As a result, they remain the volume anchor for mainstream retail, while newer formats scale from a smaller base.

Herbal and adaptogenic drinks are forecast to grow at a CAGR of 9.2% from 2026 to 2031, making them the fastest-growing product format in this segmentation and a key growth area in the Saudi Arabia health drinks market. Growth reflects rising interest in targeted wellness, natural ingredients, and convenient ready-to-drink formats. Culturally familiar ingredients can gain commercial relevance when brands position them as premium and functional options. This growth will not replace traditional juice demand soon, but it is changing innovation priorities. Established formats still lead on reach and familiarity, while herbal products gain traction through specificity, premiumization, and consumer curiosity.

By Packaging Type: Bottles Lead but Tetra Packs Reshape Ambient Access

Bottles are expected to account for 41.2% of market value in 2025, making them the leading packaging format in the Saudi Arabia health drinks market. Their strength comes from portability, resealability, and a clear link with convenience and premium presentation. These features support demand in sports drinks, premium juices, and energy beverages, where consumers often buy for on-the-go use. Bottle formats also match urban consumption patterns in Saudi Arabia, especially among commuters, gym users, and consumers seeking immediate consumption. As modern retail, convenience stores, and foodservice channels expand, bottles are expected to retain the largest value share, even as alternative formats become more cost-efficient.

Tetra Packs are forecast to grow at a CAGR of 8.8% from 2026 to 2031, ahead of the broader packaging mix. Their growth is supported by shelf stability, easy handling in ambient conditions, and better suitability for distribution beyond major cities. These benefits matter in the Saudi Arabia health drinks market because climate, logistics, and cold-chain availability vary across regions. Aseptic carton packaging can help brands reach areas where refrigerated juice or dairy drinks face practical limits. This makes packaging a strategic growth lever, not just an operational choice. SADAFCO is expected to sign an agreement in September 2025 to deploy the Tetra Pak E3/Speed Hyper aseptic filling line in Saudi Arabia. The system is designed to produce 40,000 packages per hour while reducing water, energy, and chemical use compared to conventional lines, signaling confidence in efficient, high-throughput carton packaging.

By Health Application: Immunity Dominates While Digestive Health Outpaces All

Immunity boosting is expected to account for a 30.3% share in 2025, making it the largest health application in the Saudi Arabia health drinks market. This leadership shows that immunity remains the most established wellness claim in the category. Its broad household appeal, premium positioning, and strong consumer familiarity help retailers give immunity-led products stable shelf space. These beverages are easy to understand and need limited education at purchase. This makes them suitable for pharmacies, modern trade, and general wellness channels. As a result, immunity remains the clearest link between everyday beverage purchases and functional health positioning.

Digestive health is forecast to register a 10.7% CAGR from 2026 to 2031, making it the fastest-growing application across the Saudi Arabia health drinks market. A 2024 cross-sectional study published in Frontiers in Immunology found that 84.1% of Saudi adult participants believed probiotics support digestion and gut health, while 72.5% associated probiotics with immune support. These findings show that consumers already understand the benefits, reducing the education burden for brands[2]Source: Frontiers Editorial Office, “Awareness, Knowledge, and Beliefs About Probiotics and Prebiotics Among Saudi Adults, A Cross-Sectional Study”, frontiersin.org. With familiar product claims and rising interest in gut health, trial can turn into repeat consumption faster. This supports digestive health’s faster growth than the broader market.

By Distribution Channel: Hypermarkets Lead but Specialty Stores Disrupt

Hypermarkets and supermarkets are expected to account for 42.7% of the Saudi Arabia health drinks market in 2025, making them the largest distribution channel by value. Their lead reflects wide product ranges, chilled display space, high footfall, loyalty programs, and in-store promotions that drive repeat purchases. These stores remain the main channel for mass-market juices, energy drinks, and dairy-based health beverages. They also give brands the scale to improve visibility, use shelf adjacency, and reach routine grocery shoppers. This makes modern trade important for companies targeting volume rather than niche positioning. As long as households continue shopping mainly in large organized chains, hypermarkets and supermarkets will retain their advantage.

Specialty stores are forecast to grow at a 9.7% CAGR from 2026 to 2031, which makes them the fastest-growing channel in the Saudi Arabia health drinks market. Their momentum reflects a deeper split between mainstream grocery demand and a more deliberate wellness purchasing journey. Dedicated health outlets, gym nutrition stores, and pharmacy chains can support products that need explanation, ingredient storytelling, or staff guidance before conversion. That advantage is especially relevant for herbal, probiotic, and premium wellness drinks that may struggle to stand out in broad grocery aisles. As a result, specialty retail is becoming a launch pad for brands that cannot secure wide hypermarket space at the start.

Geography Analysis

The Saudi Arabia health drinks market remains concentrated in major urban centers, with Riyadh and Jeddah serving as the primary demand hubs for new launches and established sales. Riyadh benefits from its role as the administrative center and its strong base of wellness, retail, and corporate activity, which supports trials of premium beverages. Jeddah adds scale through dense consumer traffic, higher exposure to international brands, and its position as a major commercial gateway. The Eastern Province, led by Dammam and Khobar, also generates meaningful demand, as higher-income consumers support spending on premium health drinks. Together, these three areas act as the main testing grounds for new products before brands consider wider rollout across the Saudi Arabia health drinks market.

Urban concentration shapes how companies plan investment. Brands typically build visibility, gather consumer data, and secure shelf space in Riyadh, Jeddah, and the Eastern Province before entering secondary cities. This approach is especially important for products that need cold-chain handling, in-store education, or premium pricing. As a result, the Saudi Arabia health drinks market functions as an urban-first category, where strong execution in a few metropolitan areas can matter more than limited presence across many locations. This pattern does not restrict future expansion, but it affects how quickly product types can scale. Products with easier handling, longer shelf life, and wider price accessibility tend to move beyond the main cities faster than premium or refrigerated formats.

Secondary cities such as Mecca, Medina, Abha, and Taif remain important because they represent underpenetrated demand rather than marginal demand. Their opportunity is strongest where ambient distribution, value positioning, and simple product communication can offset infrastructure gaps. This is why packaging choices play a critical role in the Saudi Arabia health drinks market, particularly as ambient-shelf formats can reach stores that are less suited to sensitive refrigerated products. Seasonal movement during Hajj and Umrah also creates spikes in demand for hydration, immunity, and energy drinks, adding a supply and distribution planning requirement for brands. These seasonal demand pulses do not change the national market structure, but they create demand periods that reward strong execution. Saudi Arabia is also gaining a broader regional role in standards and production. Tetra Pak Arabia stated in 2024 that its Jeddah facility exported 40% of its output to 11 Middle Eastern countries, showing that beverage-related manufacturing in the Kingdom connects with regional supply flows. This matters for the Saudi Arabia health drinks market because domestic compliance and production capabilities can support broader Gulf reach over time. It also means formats and packaging systems proven in Saudi Arabia can gain relevance beyond the local market.

Competitive Landscape

The Saudi Arabia health drinks market remains moderately fragmented, with global beverage companies and domestic dairy and juice players competing across several subcategories. PepsiCo, The Coca-Cola Company, Nestlé, Red Bull, and Monster Beverage hold strong positions where international branding, sports links, and wide distribution matter. Almarai, NADEC, SADAFCO, and Al Rabie remain important due to their local retail knowledge, customer trust, and ability to adapt products to Saudi consumption habits. Rising demand for hydration, functional beverages, low-sugar options, and convenient formats keeps competition active. No player controls the full category, and leadership varies by format, channel, and price point. As a result, scale alone does not ensure an advantage across the market.

Financial strength and execution capacity continue to matter. Almarai is expected to report net revenue of SAR 22 billion in 2025, up 5% year over year, while its beverage-related categories are likely to benefit from portfolio expansion and long-term investment planning. Large domestic operators can protect market share through distribution, plant investment, brand support, and category depth. In the Saudi Arabia health drinks market, companies must support core volume segments and newer wellness-led niches. This gives leading players more room to test products than smaller challengers and explains why incumbents remain influential as newer formats grow faster.

Recent strategic moves show how companies are preparing for the next stage of competition. In June 2025, Almarai is expected to complete the acquisition of Pure Beverages Industry Company, expanding into bottled water and strengthening its position in hydration-linked categories. In September 2025, SADAFCO is expected to sign an agreement with Tetra Pak to install a high-speed aseptic filling line in Saudi Arabia, showing continued investment in packaging efficiency and production scale. These moves indicate that portfolio breadth, operating capability, route-to-market readiness, and advertising are shaping competition. Larger companies are improving reach and flexibility, increasing pressure on smaller brands that depend on one product theme or channel.

Saudi Arabia Health Drinks Industry Leaders

Almarai Company

PepsiCo, Inc.

The Coca-Cola Company

Nestlé S.A.

Danone S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SFDA began enforcement of food transparency regulations including SFDA.FD 5023, mandating caffeine-content disclosure per 100 ml, high-sodium icons, calorie burn-time indicators, and full nutritional panels across all Saudi food establishments, restaurants, cafes, and online delivery platforms.

- June 2025: Almarai completed the acquisition of Pure Beverages Industry Company,/ owner of the Ival and Oska bottled water brands, for SAR 1.04 billion (USD 277 million), extending its beverage portfolio into premium hydration and positioning the combined entity to capitalise on rising functional water demand.

- April 2025: iPRO strengthened its presence in Saudi Arabia through a strategic distribution partnership with Al Rabie Saudi Foods Co. Ltd. The collaboration aims to expand the availability of iPRO's functional hydration beverages across modern retail, convenience stores, and other key sales channels in the Kingdom.

Saudi Arabia Health Drinks Market Report Scope

| Fruit and Vegetable Juices |

| Sports and Energy Drinks |

| Herbal and Adaptogenic Drinks |

| Meal Replacement Drinks |

| Dairy and Plant-based Drinks |

| Other Product Types |

| Bottles |

| Cans |

| Tetra Packs |

| Others |

| Immunity Boosting |

| Digestive Health |

| Hydration and Recovery |

| Other Applications |

| Hypermarkets / Supermarkets |

| Specialty Stores |

| Online Retail Stores |

| Convenience Stores |

| Other Channels |

| By Product Type | Fruit and Vegetable Juices |

| Sports and Energy Drinks | |

| Herbal and Adaptogenic Drinks | |

| Meal Replacement Drinks | |

| Dairy and Plant-based Drinks | |

| Other Product Types | |

| By Packaging Type | Bottles |

| Cans | |

| Tetra Packs | |

| Others | |

| By Health Application | Immunity Boosting |

| Digestive Health | |

| Hydration and Recovery | |

| Other Applications | |

| By Distribution Channel | Hypermarkets / Supermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Convenience Stores | |

| Other Channels |

Key Questions Answered in the Report

What is the projected value of the Saudi Arabia health drinks market by 2031?

The Saudi Arabia health drinks market is projected to reach USD 4.49 billion by 2031, rising from USD 2.83 billion in 2025 at an 8.2% CAGR from 2026 to 2031.

Which product type leads sales in Saudi Arabia health drinks?

Fruit and vegetable juices held the largest product type share at 35.2% in 2025, supported by broad retail availability and familiar daily use.

Which segment is growing fastest in Saudi Arabia health drinks?

Digestive health is the fastest-growing application, with a forecast CAGR of 10.7% through 2031, helped by strong consumer belief in probiotic benefits.

Why are specialty stores growing faster than hypermarkets in this space?

Specialty stores are projected to grow at a 9.7% CAGR because they provide more education, curation, and staff support for premium and functional beverages.

Page last updated on: