Saudi Arabia Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

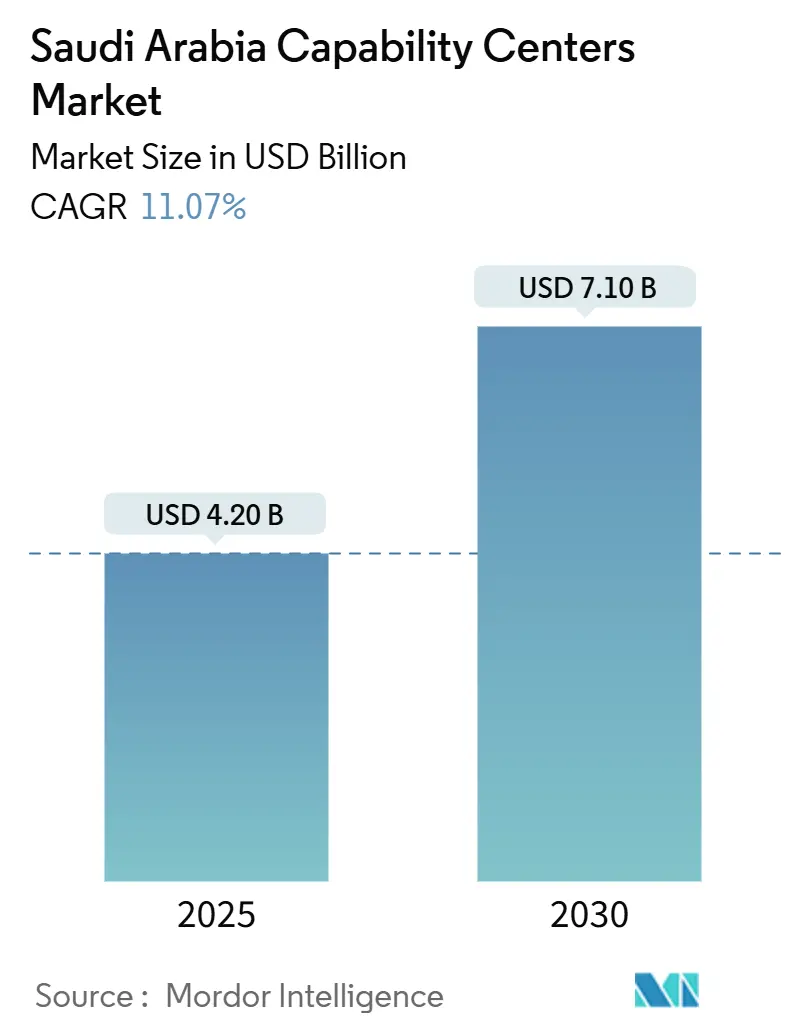

| Market Size (2025) | USD 4.20 Billion |

| Market Size (2030) | USD 7.10 Billion |

| Growth Rate (2025 - 2030) | 11.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Global Capability Centers Market Analysis by Mordor Intelligence

The Saudi Arabia global capability centers market size is estimated at USD 4.2 billion in 2025 and is projected to reach USD 7.1 billion by 2030, representing a 11.07% CAGR over the forecast period. This performance confirms the kingdom’s emergence as the preferred location for multinational captive hubs across the Middle East and North Africa. Aggressive investment incentives, a rapidly expanding hyperscale data center network, and Vision 2030 digital-first mandates are converging to pull high-value engineering, analytics, and business-support work onshore. Early movers secure proximity to Saudi Arabia’s USD 833 billion domestic economy, unparalleled 30-year tax holidays, and a strategic time-zone bridge between Europe, Asia, and Africa. Competitive tactics, therefore, revolve less around labor-arbitrage pricing and more around securing bilingual talent, maintaining regulatory compliance, and aligning with government localization rules.

Key Report Takeaways

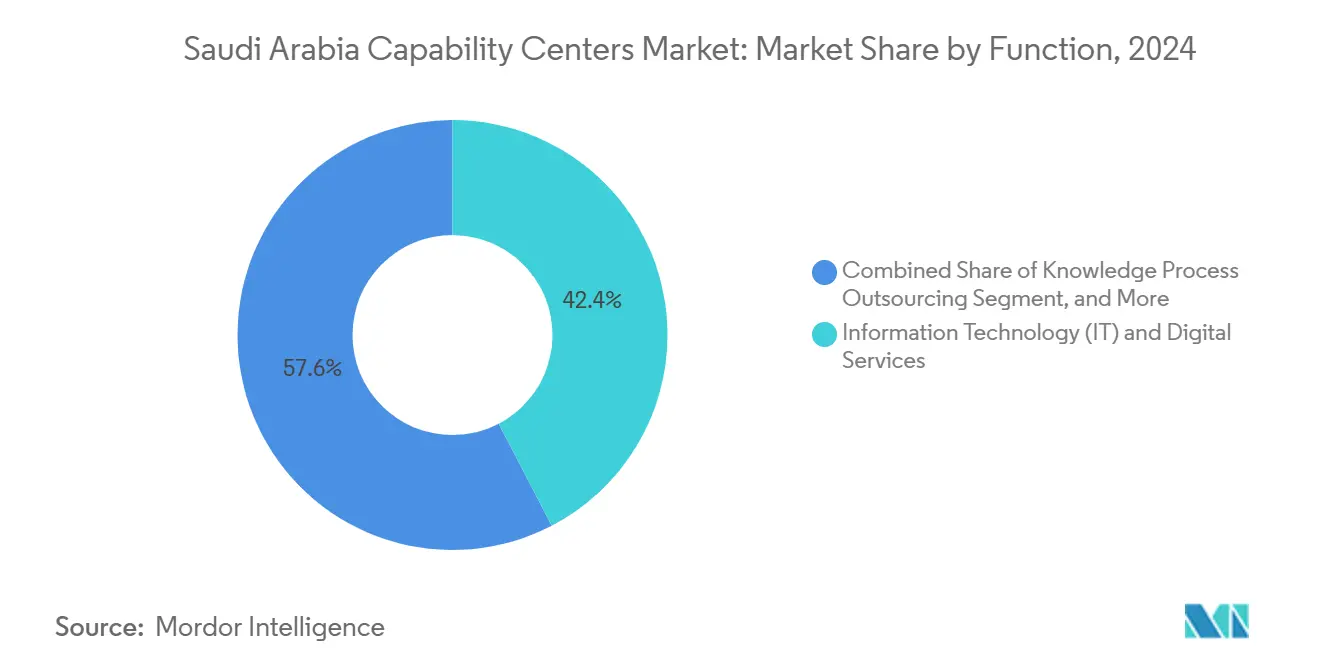

- By function, information technology and digital services held a 42.36% revenue share of the Saudi Arabia global capability centers market in 2024; the healthcare and life sciences sector is expected to advance at an 11.85% CAGR through 2030.

- By engagement model, captive centers commanded 57.88% of Saudi Arabia's global capability centers market share in 2024, while build-operate-transfer structures are expected to expand at a 12.16% CAGR through 2030.

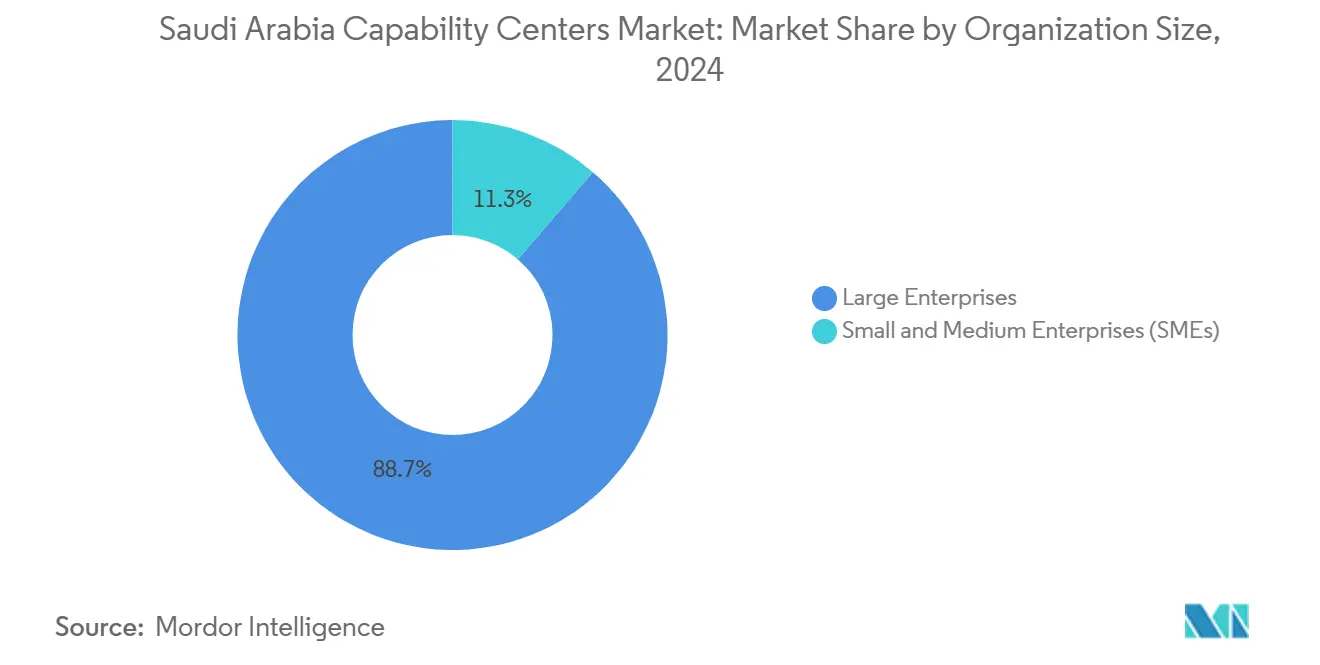

- By organization size, large enterprises contributed 88.68% to the Saudi Arabia global capability centers market size in 2024, while small and medium enterprises are projected to rise at a 12.97% CAGR through 2030.

- By industry vertical, banking, financial services, and insurance captured 33.52% of the Saudi Arabia global capability centers market in 2024; healthcare and life sciences are projected to grow at the fastest CAGR of 11.85% to 2030.

Saudi Arabia Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 digital-first mandates accelerate captive tech demand | +2.8% | National – Riyadh, Jeddah, NEOM | Medium term (2-4 years) |

| Generous headquarters incentive program (0% corporate tax up to 50 years) | +3.2% | National – Riyadh Financial District | Long term (≥4 years) |

| Double-digit growth in national ICT spending 2024-2030 | +2.1% | National with spillover to the Global Capability Center | Medium term (2-4 years) |

| Expanding the Saudi STEM graduate pool through scholarship repatriation | +1.9% | Major urban centers | Long term (≥4 years) |

| PIF-backed hyperscale data-center cluster attracts co-located Global Capability Centers | +2.3% | Riyadh, Jeddah, NEOM zones | Short term (≤2 years) |

| Local-content quotas in public contracts push MNC on-shore delivery | +1.8% | National, all procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Digital-First Mandates Accelerate Captive Tech Demand

Saudi ministries aim to achieve 50% digital-service penetration by 2030, compelling foreign corporations to embed engineering and analytics capabilities within the kingdom rather than relying on external outsourcers. Twenty-three government entities initiated major AI, blockchain, and cloud programs in 2024, and each project requires secure development environments with tight data-residency adherence.[1]Saudi Vision 2030, “Digital Government Program,” vision2030.gov.sa The resulting funnel of large transformation contracts gives the Saudi Arabia global capability centers market a durable five-year demand runway.

Generous Headquarters Incentive Program Creates Compelling Unit Economics

The Regional Headquarters Program grants 0% corporate tax for 30 years, 100% foreign ownership, and expedited work visas, trimming delivered cost per full-time equivalent by 25-30% against traditional offshore destinations. Forty-seven approvals in 2024 underscore how the policy tilts capital-allocation models in the kingdom’s favor. Corporations also commit to hiring Saudi nationals, reinforcing local talent pipelines and long-term ecosystem depth.

Double-Digit Growth in National ICT Spending Drives Service Demand

Saudi ICT expenditure reached USD 28.4 billion in 2024, marking a 14.2% year-over-year growth that significantly exceeds the average for the wider Middle East.[2]Communications, Space and Technology Commission, “National Strategy for Data and AI,” cst.gov.sa The National Strategy for Data and Artificial Intelligence earmarks an additional USD 20 billion through 2030, ensuring a multi-year pipeline of platform migrations, analytics deployments, and cybersecurity rollouts. Government entities account for 42% of this incremental spend as ministries rush to meet Vision 2030 digital service targets. State-owned enterprises are mirroring the trend, injecting demand for cloud-native ERP, predictive maintenance analytics, and real-time supply chain dashboards. These projects require on-shore development to satisfy data-residency and local-content rules, channeling workloads directly into captive centers. As budgets continue to expand at a rate above GDP growth, service providers can project steady utilization rates and premium billing for advanced skills.

Expanding Saudi STEM Graduate Pool Through Scholarship Repatriation

More than 200,000 scholarship-funded STEM graduates have returned to Saudi Arabia since 2020, enriching the bilingual engineering base with global best practices.[3]Ministry of Education, “STEM Education Statistics 2024,” moe.gov.sa Saudi universities produced 47,000 additional STEM graduates in 2024, a 23% increase from 2020. Notably, 35% of computer-science degrees are now awarded to women, following policy changes that mandate 40% female participation. Fifteen new AI and data-science programs, delivered in partnership with global tech firms, accelerate specialization in machine learning, natural-language processing, and robotics. King Abdullah University of Science and Technology alone has added 1,200 patents since 2020, showcasing commercializable research that pairs well with industry R&D centers. Capability-center operators benefit from reduced relocation costs and quicker cultural alignment versus expatriate hiring. The growing domestic pipeline also eases Saudization quota pressures, stabilizing long-term talent supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Salary inflation for bilingual tech talent | -1.8% | Riyadh and Jeddah | Short term (≤2 years) |

| Shallow niche engineering skill depth versus India and the Philippines | -1.2% | National | Medium term (2-4 years) |

| Restrictive data-residency and cross-border transfer laws | -0.9% | National | Long term (≥4 years) |

| Cultural assimilation strain on imported corporate processes | -0.7% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Salary Inflation for Bilingual Tech Talent Pressures Cost Models

Senior software engineers in Riyadh and Jeddah now command USD 80,000-120,000 annual salaries, versus USD 25,000-40,000 in mature offshore hubs, creating a material jump in fully loaded cost per seat. Wage bills have increased by 15-20% each year since 2024 as firms rush to meet the 70% local-hire mandate for technology roles.[4]Ministry of Human Resources and Social Development, “Saudization Requirements Technology Sector,” hrsd.gov.sa Specialist positions in AI, cloud architecture, and cybersecurity offer signing bonuses exceeding USD 15,000 and relocation packages that align with Silicon Valley benchmarks. The Personal Data Protection Law further restricts supply because only Saudi nationals are eligible to hold designated data governance posts. Vendors offset pressure through tiered career ladders, automation of routine tasks, and internal academies that cross-skill junior staff. While salaries will remain structurally higher than those in legacy offshore markets, rapid productivity gains from cloud tooling and process digitization can help preserve margin targets.

Shallow Niche Engineering Skill Depth Versus Established Markets

Despite rapid expansion, Saudi talent pools still lack density in semiconductor design, advanced manufacturing automation, and deep pharmaceutical research. Corporations often run dual-hub models, retaining sites in India or the Philippines for niche workloads, while Saudi teams handle customer-facing and compliance-sensitive tasks. University programs are scaling, yet the 4-6-year gestation for doctoral-level specialists means near-term shortages persist. The Saudi Arabian Monetary Authority’s fintech sandbox comprises 87 participants; however, many still outsource blockchain or quantitative-trading code to external centers due to a lack of local expertise. Government grants encourage universities to launch micro-credential courses, though industry feedback notes variable curriculum quality. Providers, therefore, invest in expatriate mentors and structured knowledge-transfer cycles to deepen technical bench strength while broader educational reforms take hold.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: IT Services Maintain Leadership amid Engineering Upswing

Information technology and digital services accounted for 42.36% of the Saudi Arabia global capability centers market in 2024, driven by public-sector cloud migrations and private-sector fintech rollouts. The segment is forecast to post an 11.58% CAGR through 2030 as ministries demand robust cybersecurity, analytics, and citizen services platforms. Engineering and research hubs are smaller in absolute value, yet their double-digit expansion rate benefits from NEOM’s USD 500 billion smart-city construction and the Saudi Green Initiative’s USD 187 billion renewables pipeline.

Support functions such as business process management and knowledge process outsourcing complement core development teams by handling finance, procurement, and compliance analytics. Banks leverage knowledge centers for Basel III stress-testing while energy firms outsource reservoir-simulation data crunching. This service layering enables new entrants to establish low-risk BPO contracts before scaling into high-value engineering workloads, a pattern observed across the Saudi Arabia global capability centers industry.

By Engagement Model: Captives Dominate while BOT Gains Traction

Captive entities held 57.88% of Saudi Arabia's global capability centers market in 2024, reflecting a multinational appetite for intellectual property security and close alignment with local regulators. The regional headquarters tax holiday strengthens that appeal, ensuring full financial control without partner profit shares. Build-operate-transfer models, growing at a 12.16% CAGR, appeal to firms seeking local expertise during setup but ultimately require operational control. Government one-stop licensing has reduced the BOT transition from 18-24 months to 12-15 months, compressing the time-to-benefit.

Traditional third-party outsourcing continues to support non-sensitive tasks, yet data-residency statutes and content quotas limit its relative share. Hybrid BOT structures increasingly handle health-tech and fintech workloads where regulatory oversight is intense, signaling a nuanced segmentation within the Saudi Arabia global capability centers market.

By Organization Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises accounted for 88.68% of 2024 demand, as conglomerates such as Saudi Aramco and SABIC consolidated their global digital operations within the kingdom. These corporations manage portfolios of analytics, R&D, and shared-service functions, justifying the need for dedicated campuses. Meanwhile, small and medium-sized enterprises expand at the fastest rate, with a 12.97% CAGR. Monsha’at’s USD 2.1 billion financing program enables startups to tap into shared cloud platforms instead of building proprietary infrastructure, bringing plug-and-play SaaS development to the Saudi Arabia global capability centers market size for the first time.

Emerging fintech and e-commerce players also leverage pay-as-you-grow arrangements with hyperscale cloud providers. As venture funding surpassed USD 1.2 billion in 2024, many seed-stage companies are now graduating to Series B with pre-configured engineering pods hosted within larger service providers’ centers, illustrating a maturing pipeline beneath the enterprise tier.

By Industry Vertical: BFSI Retains Primacy, Healthcare Gains Momentum

Banking, financial services, and insurance contributed 33.52% of 2024 revenue, nurtured by the Saudi Central Bank’s push toward digital banking and open-API ecosystems. Complex regulatory checks favor onshore development, where compliance officers and developers sit side by side. Healthcare and life sciences grow fastest at 11.85% CAGR, powered by tele-health rollouts, electronic health record integration, and NEOM’s biotech ambitions.

Manufacturing, automotive, and industrial verticals gather pace as Lucid Motors, Aramco, and hydrogen-economy projects demand advanced automation coding and battery-management analytics. Retail, consumer goods, and telecom add incremental volumes, each adopting omnichannel and 5G-enabled use cases. This widening sectoral base underpins the long-term addressable ceiling for the Saudi Arabia global capability centers market.

Geography Analysis

Riyadh accounts for roughly 45% of current center footprints, supported by federal ministries, sovereign-wealth projects, and the Regional Headquarters Program’s 30-year tax holiday. Multinationals cluster inside the Riyadh Financial District, where Class-A offices, Tier-IV data centers, and a new metro grid compress commute times for a growing bilingual workforce. The city’s King Salman International Airport, slated to handle 120 million passengers annually, is expected to reduce executive travel cycles across Europe, Asia, and Africa by 2028. Local regulators offer single-window licensing, reducing setup periods to weeks, giving early movers a speed advantage. These factors anchor Riyadh as the primary hub for the Saudi Arabia global capability centers market.

Jeddah has emerged as a secondary node, thanks to its Red Sea port, long-standing commercial heritage, and proximity to King Abdullah Medical City. Healthcare and life sciences capability centers are drawn here to support the Ministry of Health's digital projects and the expanding medical tourism industry. Logistics advantages also attract retail and fast-moving consumer goods players who need same-day import-export clearance through Jeddah Islamic Port upgrades funded under the USD 147 billion National Transport and Logistics Strategy. NEOM, although still under construction, already hosts pilot labs focused on robotics, renewable energy, and smart-city operating systems that require on-site R&D teams.

Specialized economic zones, including King Abdullah Economic City and the Jazan Economic City, round out the geographic spread. Each zone offers 100% foreign ownership, dedicated fiber backbones, and customs-free corridors, allowing for hardware prototyping alongside software development. Co-location with heavy-industry tenants lets engineering centers iterate quickly on industrial IoT and advanced manufacturing projects. National data-governance standards issued by the Saudi Data and AI Authority ensure uniform compliance rules, allowing companies to shift workloads across sites without requiring new legal reviews. Combined, these zones extend the service radius of capability centers while maintaining a competitive total cost of ownership.

Competitive Landscape

The competitive field is moderately fragmented, with the top five vendors accounting for a significant share of the total revenue. Tata Consultancy Services, Infosys, Wipro, HCLTech, and Tech Mahindra maintain legacy enterprise contracts; however, they are now aggressively hiring Saudi nationals to meet 70% localization quotas. Direct captives from Oracle, Microsoft, Lucid Motors, and Saudi Aramco compete on proprietary IP and industry-specific depth, reshaping the traditional labor-arbitrage equation.

Regional specialists differentiate themselves through Arabic-language AI, Islamic finance compliance engines, and interoperability frameworks for health data. These boutiques often partner with universities for joint research, then monetize the output through managed-service agreements. Their cultural alignment and regulatory fluency enable them to win bids that global outsourcers have historically dominated, particularly in the banking and healthcare sectors.

Infrastructure alliances with Google Cloud, Oracle Cloud, and Microsoft Azure underpin many engagements, offering low-latency zones and built-in data-residency controls. Vendors also invest in in-house academies to curb wage inflation and reduce talent churn. The strategic focus is shifting from price to delivery resilience, cybersecurity maturity, and environmental, social, and governance (ESG) credentials. As multinationals pursue specialized partners instead of single mega-providers, the Saudi Arabia global capability centers market rewards firms that blend deep domain knowledge with strict local compliance.

Saudi Arabia Global Capability Centers Industry Leaders

Accenture plc

Capgemini SE

IBM Corporation

Tata Consultancy Services Ltd

Cognizant Technology Solutions Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Oracle confirmed a USD 1.5 billion expansion that adds three new Riyadh and Jeddah data centers, each fitted with AI accelerators and low-latency zones for co-located capability centers.

- September 2025: Lucid Motors completed its USD 3.4 billion King Abdullah Economic City complex, employing 2,500 staff in electric-vehicle engineering and battery technologies.

- August 2025: Microsoft launched a USD 800 million AI research hub in NEOM with King Abdullah University of Science and Technology, targeting Arabic language models and smart-city solutions.

- July 2025: Saudi Aramco opened a USD 2.1 billion global technology center in Dhahran, focusing on carbon-capture analytics and renewable energy integration.

Saudi Arabia Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the 2025 value of the Saudi Arabia global capability centers market?

The market is valued at USD 4.2 billion in 2025.

How fast is the sector expected to grow through 2030?

It is forecast to register an 11.07% CAGR between 2025 and 2030.

Which functional area holds the largest share?

Information technology and digital services lead with a 42.36% share in 2024.

Why are captive centers preferred over outsourcing models?

Captives secure intellectual-property control and satisfy strict data-residency rules better than third-party arrangements.

Which vertical is expanding the fastest?

The healthcare and life sciences sector is projected to grow at an 11.85% CAGR through 2030.

What is driving salary inflation in Saudi capability centers?

Intense demand for bilingual tech talent and 70% Saudization quotas have pushed senior-engineer pay up by 15-20% annually.

Page last updated on: