Saudi Arabia Galvanizing Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

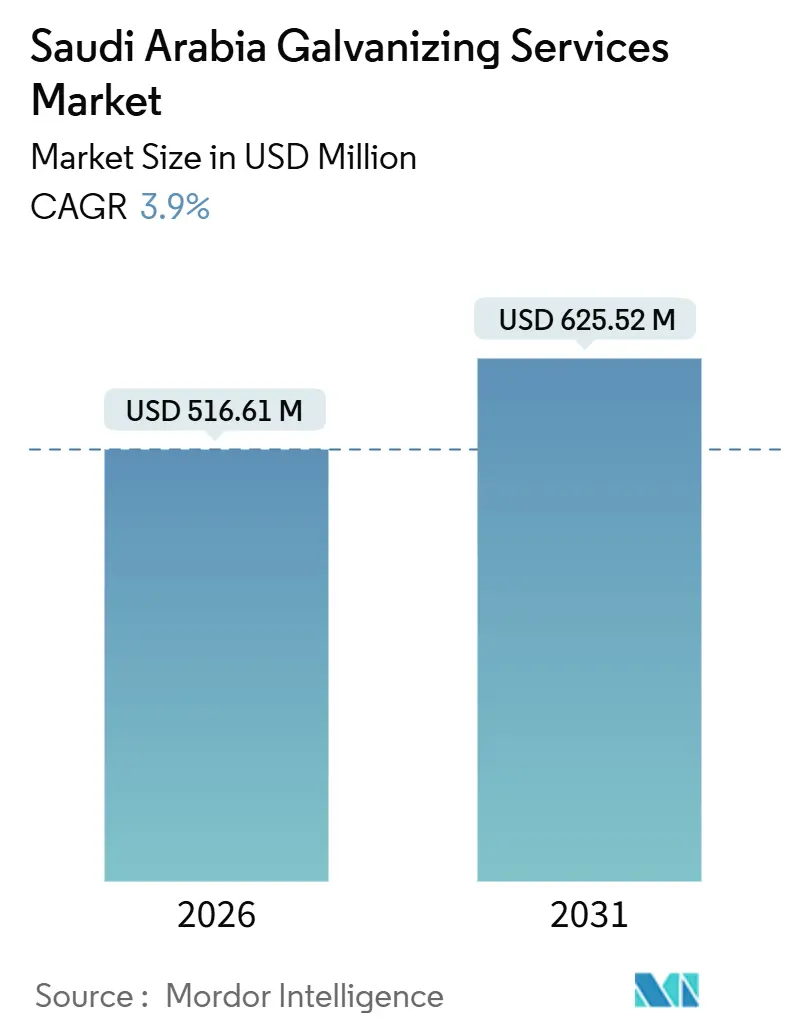

| Market Size (2026) | USD 516.61 Million |

| Market Size (2031) | USD 625.52 Million |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

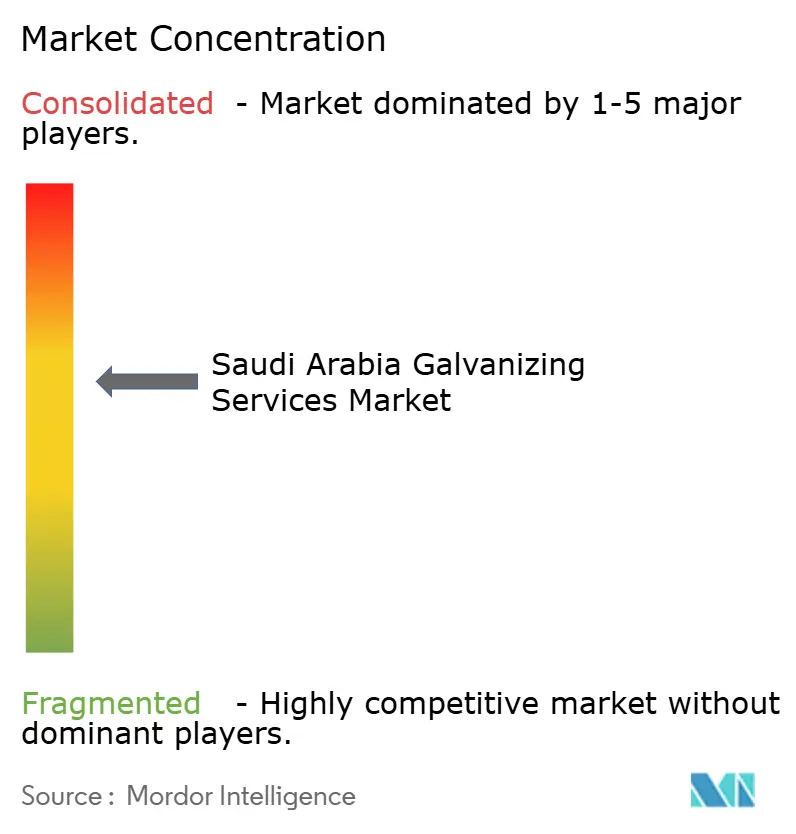

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Galvanizing Services Market Analysis by Mordor Intelligence

The Saudi Arabia Galvanizing Services Market size is estimated at USD 516.61 million in 2026, and is expected to reach USD 625.52 million by 2031, at a CAGR of 3.9% during the forecast period (2026-2031). A measured trajectory stems from giga-project steel demand still being in design phases, legacy hot-dip capacity that cannot handle thin-gauge modules, and zinc-price swings that compress galvanizer margins. Transmission-tower retrofits, solar-tracker frames, and bridge-deck replacements continue to anchor demand because they require thick, uniform coatings that only immersion kettles deliver. Meanwhile, renewable-energy developers and new automotive OEMs are signaling the need for faster, lighter, and more precise coatings, a specification gap that existing lines cannot yet satisfy. Tightening environmental rules and the SABER Technical Regulation for traceability are raising compliance costs, yet they also favor operators with in-house testing, ISO-compliant labs, and zinc-recovery systems. Overall, the Saudi Arabia galvanizing services market remains moderately fragmented, with five operators controlling the bulk of capacity, although none has moved decisively into electro-galvanizing, leaving a strategic opening for technology-focused entrants.

Key Report Takeaways

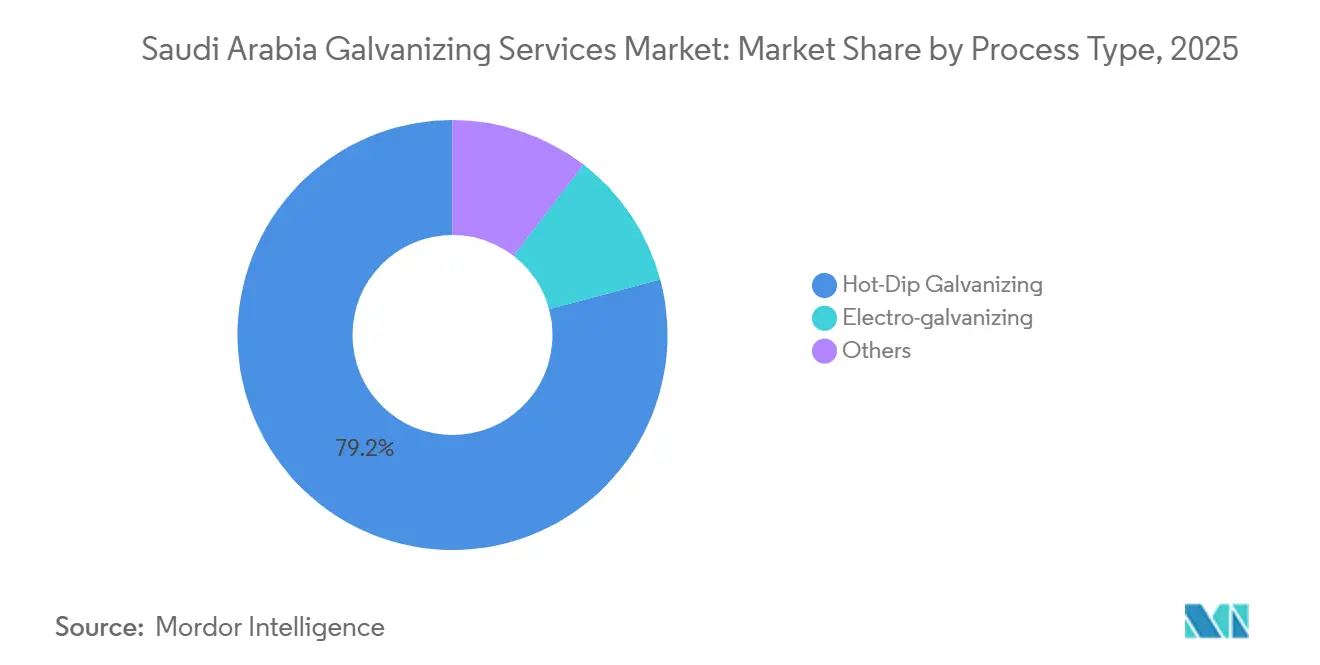

- By process type, hot-dip galvanizing led with 79.17% revenue share in 2025 and is forecast to expand at a 4.04% CAGR through 2031, slightly above the Saudi Arabia galvanizing services market average.

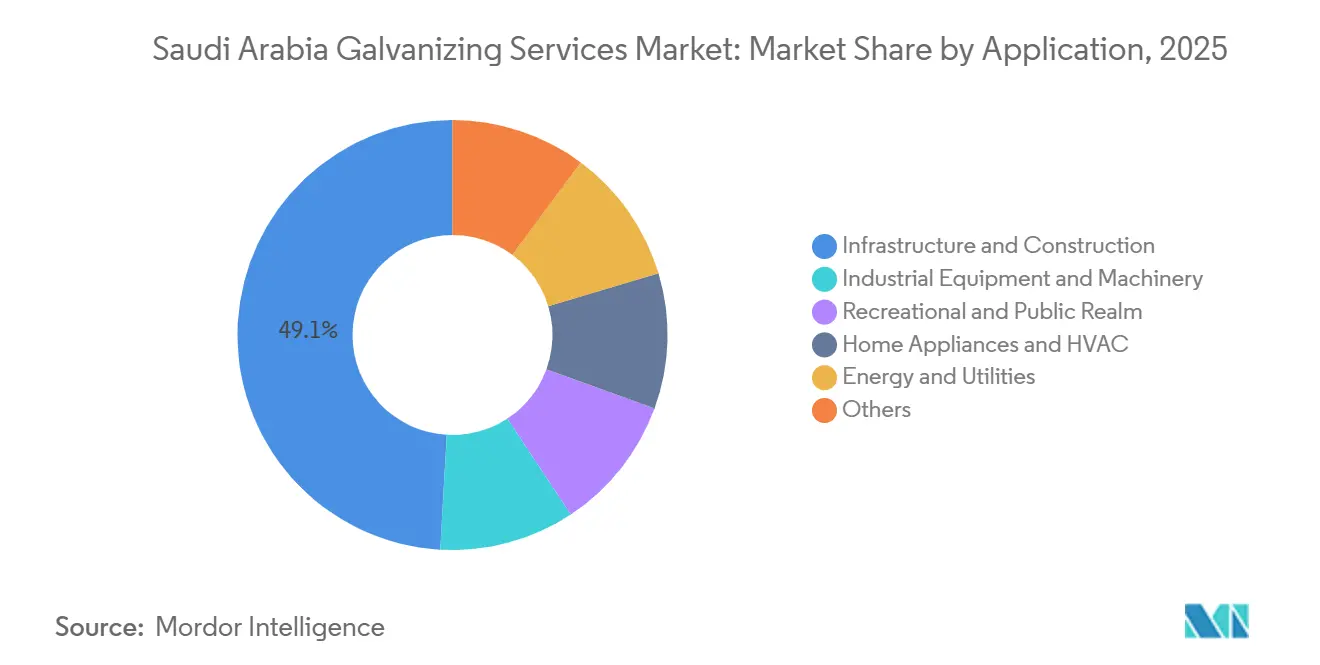

- By application, infrastructure and construction captured a 49.09% share of the Saudi Arabia galvanizing services market size in 2025, while energy and utilities are advancing at a 7.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Galvanizing Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from construction and infrastructure projects | +1.2% | National, concentrated in Riyadh, Jeddah, NEOM, Qiddiya | Medium term (2-4 years) |

| Increasing use in automotive manufacturing for corrosion resistance | +0.6% | National, with early gains in King Abdullah Economic City | Long term (≥4 years) |

| Rising investments in energy infrastructure | +0.8% | National, spill-over to Northern Borders and Tabuk regions | Short term (≤2 years) |

| Rapid uptake of lightweight galvanized modules in off-site and modular housing | +0.5% | National, pilot zones in Riyadh and Eastern Province | Medium term (2-4 years) |

| Localization incentives under Saudi Vision 2030 expanding domestic capacity | +0.7% | National, manufacturing clusters in Jubail and Yanbu | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Construction and Infrastructure Projects

Saudi Arabia's ambitious giga-projects have created an unprecedented backlog in structural-steel orders. However, operators are holding off on capital commitments, waiting for definitive EPC awards, leading to a lag in galvanizing capacity additions. Construction contracts saw a significant increase, with steel-intensive projects like bridges, elevated rail, and cable-stayed spans comprising a notable portion of this total. As a result, peak demand for galvanized coatings is anticipated around 2027-2028. This timeline presents producers with a tight window to either expand their kettles or strike tolling deals with underutilized lines in Bahrain and the UAE. Adhering to GSO ISO 1461:2013 standards mandates a minimum 85-micron coating for structural members in industrial settings[1]ISO 1461 Hot-Dip Galvanized Coatings, Gulf Standardization Organization, gso.org.sa. Unfortunately, older kettles often struggle to consistently meet this specification. Without an increase in capacity, rejection rates could soar, leading to expensive reworks and delays for contractors involved in bridges and rail projects.

Increasing Use in Automotive Manufacturing for Corrosion Resistance

Lucid Motors launched trial production in late 2024, while Ceer has set its sights on producing units each year by 2030. , but both OEMs still import electro-galvanized coil because no domestic line can meet the ISO 9227 salt-spray standards of 720 hours. Despite incurring a premium on landed costs due to import reliance, the practice persists. This is largely because setting up a single electro-galvanizing line demands significant investment and a lengthy commissioning period. HVAC and white-goods producers face a similar gap; Shaker Group’s partnership with LG Electronics aims to localize compressor production, but coils remain imported, eroding Vision 2030 localization targets. A domestic electro-galvanizing facility would unlock contracts across automotive and HVAC segments, making it the highest-return brownfield investment in the metals value chain.

Rising Investments in Energy Infrastructure

In 2024, the Saudi Electricity Company allocated significant funds for grid reinforcement, aiming to integrate renewable capacity, either under construction or already signed. Transmission networks have upped their standards, now mandating hot-dip coatings for desert and coastal towers. This requirement is double that of temperate-climate norms, leading to a reduction in kettle throughput and a tightening of supply. Renewable developers are in need of mounting structures for their solar and wind projects, translating to an annual demand surge of galvanized steel. Additionally, lead times for custom lattice towers have stretched, nudging some developers to consider alternatives like powder-coated or weathering-steel towers, which, despite their higher lifecycle costs, offer shorter delivery windows.

Rapid Uptake of Lightweight Galvanized Modules in Off-Site and Modular Housing

By 2030, ROSHN aims to roll out housing units, with a significant portion being constructed off-site using light-gauge steel frames. The Saudi Green Building Forum advocates for the use of pre-galvanized coils in modular construction, citing benefits like the elimination of on-site welding fumes and a reduction in assembly time. However, with only two domestic galvanizers slitting pre-galvanized coils, modular fabricators find themselves importing from China and India, incurring a price premium. In late 2024, disruptions in Red Sea shipping extended the transit time from Shanghai to Jeddah, putting project schedules at risk. A domestic line for pre-galvanized coils, equipped with cut-to-length capabilities, could command a price premium. Yet, given ROSHN's ambitious pipeline and the Ministry of Housing's annual target, the investment promises a payback within a few years.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in zinc prices affecting input costs | -0.4% | National | Short term (≤2 years) |

| Stringent environmental regulations on pickling waste and fume emissions | -0.3% | National | Medium term (2-4 years) |

| High energy-consumption intensity for hot-dip processes | -0.2% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Zinc Prices Affecting Input Costs

London Metal Exchange zinc futures fluctuated significantly before stabilizing, compressing galvanizer margins. Smaller operators without hedging programs saw raw-material costs rise, forcing them to reject low-margin bridge-deck orders. Price swings deter kettle expansion because project IRRs drop below hurdle rates unless developers pre-commit to off-take contracts.

Stringent Environmental Regulations on Pickling Waste and Fume Emissions

In 2024, the National Center for Environmental Compliance slashed the permissible limit of hexavalent chromium in rinse water to 0.05 mg/L. They also mandated continuous opacity monitoring, enforcing penalties of 30-90 day shutdowns for non-compliance[2]Revised Industrial Emissions Standards 2024, National Center for Environmental Compliance, ncec.gov.sa. Retrofits represent months of profit for a mid-sized plant. Additionally, the SABER Technical Regulation's laboratory traceability requirement adds costs per sample and extends lead times by four to six weeks. As a result, fabricators are now consolidating their orders with a select few galvanizers that possess ISO 17025 labs, putting pressure on smaller players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Hot-Dip Dominance Reflects Infrastructure Legacy

Hot-dip galvanizing accounted for 79.17% of 2025 revenue and is forecast to grow at 4.04% through 2031, faster than the overall Saudi Arabia galvanizing services market. In contrast, electro-galvanizing and other methods face challenges in achieving significant growth, primarily due to the absence of a domestic continuous-processing line. The market size for hot-dip galvanizing services in Saudi Arabia highlights a significant dependence on traditional legacy kettles. Furthermore, the dominance of hot-dip processes signals a structural inertia, with most operational lines having been installed between 1985 and 2005.

Large hot-dip plants, equipped with ISO-compliant labs, benefit from shortened batch-testing cycles. This advantage is crucial, especially since SABER mandates third-party verification. While electro-galvanizing offers precision, its potential remains largely untapped. Notably, companies continue to import coils, even with a two-week shipping delay that makes them vulnerable to disruptions in the Red Sea. Mechanical galvanizing caters to the transmission network with supplies of bolts and nuts. However, its growth has plateaued, especially as newer tower designs demand fewer fasteners.

By Application: Energy Segment Outpaces Construction Despite Smaller Base

Infrastructure and construction delivered 49.09% of 2025 revenue. Meanwhile, the energy and utilities sector is witnessing the fastest growth among all segments, expanding at a 7.72% CAGR. The market for galvanizing services in Saudi Arabia, specifically for energy applications, is set to surge over the forecast period. This growth trajectory is largely driven by the procurement of lattice towers and tracker frames for utility-scale solar and wind projects.

While industrial equipment and machinery enjoy steady growth, buoyed by petrochemical expansions in Jubail and Yanbu, they grapple with a substitution risk from stainless-steel and FRP alternatives. Demand from recreational and public sectors is poised for a significant uptick post-2026. This surge is attributed to Saudi Arabia's preparations for the 2034 FIFA World Cup, which involves the construction of multiple stadiums. The event is projected to consume a substantial amount of structural steel, with a significant portion earmarked for galvanizing. Home appliances and HVAC systems command a notable market share, bolstered by the Shaker Group’s expansion. However, the market continues to rely on domestic coil imports until the debut of a new electro-galvanizing line.

Geography Analysis

Saudi Arabia's galvanizing services market is primarily centered around three key industrial corridors. The Central Region, led by Riyadh, accounts for a significant portion of the market's revenue. This region enjoys a strategic advantage due to its closeness to major giga-project headquarters and fabrication yards. Notably, NEOM’s rebar-automation facility and Qiddiya’s entertainment complex both procure steel from nearby plants, benefiting from either captive galvanizing or tolling agreements. Demand in this region is projected to grow steadily through 2031, outpacing the national average.

The Eastern Province, contributing a substantial share of the market's revenue, is bolstered by Zamil Steel’s impressive fabrication capacity and UNICOIL’s galvanized-coil line. Given that the coastal humidity in summer exceeds 70%, zinc oxidation is accelerated. As a result, specifications mandate 610 g/m² coatings. While these coatings reduce kettle throughput, they also extend delivery schedules. The region sees a dominance of energy and utilities orders, thanks to upstream petrochemical projects in Jubail and Ras Tanura, which necessitate galvanized cable trays and support structures.

Although the Western Region constitutes a smaller portion of Saudi Arabia's galvanizing services market, it boasts the fastest growth rate. Developments in Red Sea tourism, port infrastructure, and desalination plants fuel this surge. A notable challenge is the absence of large-scale galvanizing facilities west of Jeddah, resulting in an additional 400-600 km haulage. This not only inflates logistics costs but also extends lead times. While Tabuk Steel’s plant addresses some of the demand for NEOM's grid extensions, its shallow kettle poses limitations, particularly for bridge girders. The Northern Borders and southern provinces, tied to renewable projects in Tabuk and transmission extensions into Najran and Jizan, round out the market. Developers in these regions occasionally opt for powder-coated or weathering-steel alternatives. This choice, made to sidestep the three-week round-trip to galvanizers in the Eastern Province, does elevate lifecycle costs but ensures timely construction.

Competitive Landscape

The Saudi Arabia galvanizing services market is moderately consolidated. Technology adoption remains conservative; no operator has publicly disclosed plans for inline pickling automation or closed-loop zinc-recovery systems despite tighter NCEC limits on hexavalent chromium. White-space opportunities cluster in electro-galvanizing for automotive and HVAC, pre-galvanized coil slitting for modular housing, and mobile galvanizing units deployable at remote giga-project sites.

Saudi Arabia Galvanizing Services Industry Leaders

Energya

UNICOIL (Universal Metal Coating Company)

Hidada

AIC Steel

Al Yamamah Steel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Xuzhou RITMAN Equipment and HITECH signed a deal to supply an automatic hot-dip galvanizing centrifugal coating line in Saudi Arabia.

- June 2024: Salem Balhamer Holding modernized 70% of the AL-JUBAIL HIT Steel Fabrication & Galvanizing Factory, integrating cutting-edge equipment.

Saudi Arabia Galvanizing Services Market Report Scope

Galvanizing services are defined as the process of applying a protective zinc coating to iron or steel to prevent rust and extend the lifespan of metal products. This involves methods like hot-dip galvanizing, where metals are cleaned and immersed in molten zinc, creating a durable, corrosion-resistant layer that is metallurgically bonded. The galvanizing services market represents the total revenue generated from galvanizing activities, including both third-party services and in-house operations. These estimates exclude costs related to steel material and its procurement.

The galvanized steel market is segmented by process type and application. By process type, the market is segmented into hot-dip galvanizing, electro-galvanizing, and others. By application, the market is segmented into infrastructure and construction (including bridges, rail, roads, and structural steel), industrial equipment and machinery, recreational and public realm (such as stadia, parks, street furniture, and signage), home appliances and HVAC, energy and utilities (covering transmission towers, solar, and wind), and others (including agriculture, fencing, etc.). For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Hot-Dip Galvanizing |

| Electro-galvanizing |

| Others |

| Infrastructure and Construction (bridges, rail, roads, structural steel) |

| Industrial Equipment and Machinery |

| Recreational and Public Realm (stadia, parks, street furniture, signage) |

| Home Appliances and HVAC |

| Energy and Utilities (transmission towers, solar, wind) |

| Others (Agriculture, Fencing, etc.) |

| By Process Type | Hot-Dip Galvanizing |

| Electro-galvanizing | |

| Others | |

| By Application | Infrastructure and Construction (bridges, rail, roads, structural steel) |

| Industrial Equipment and Machinery | |

| Recreational and Public Realm (stadia, parks, street furniture, signage) | |

| Home Appliances and HVAC | |

| Energy and Utilities (transmission towers, solar, wind) | |

| Others (Agriculture, Fencing, etc.) |

Key Questions Answered in the Report

How fast is the Saudi Arabia galvanizing services market expected to grow through 2031?

It is forecast to expand at a 3.90% CAGR, reaching USD 625.52 million by 2031, from USD 516.61 million in 2026.

Which process type currently dominates demand?

Hot-dip galvanizing commands 79.17% of revenue due to infrastructure and transmission-tower needs.

What drives the fastest application growth?

Energy and utilities advance at 7.72% CAGR as grid reinforcement and renewable projects accelerate.

What major risk affects galvanizers’ margins?

Zinc-price volatility on the London Metal Exchange can swing margins for operators without hedging.

Page last updated on: