Saudi Arabia Full Service Restaurants Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

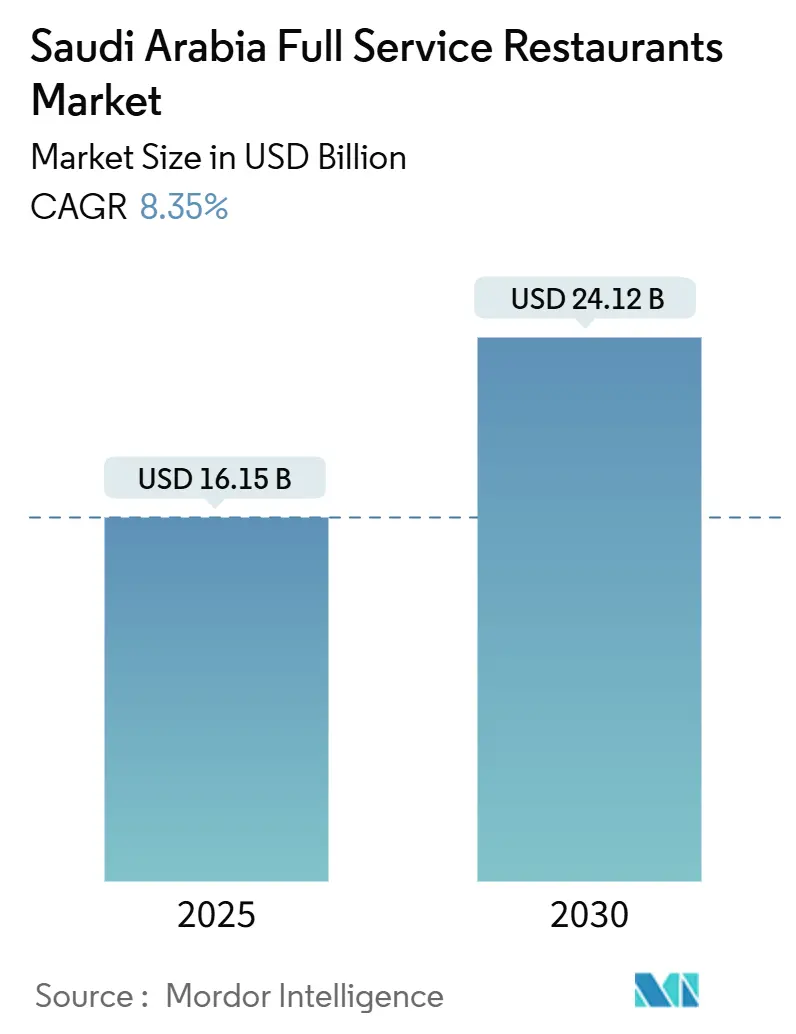

| Market Size (2025) | USD 16.15 Billion |

| Market Size (2030) | USD 24.12 Billion |

| Growth Rate (2025 - 2030) | 8.35% CAGR |

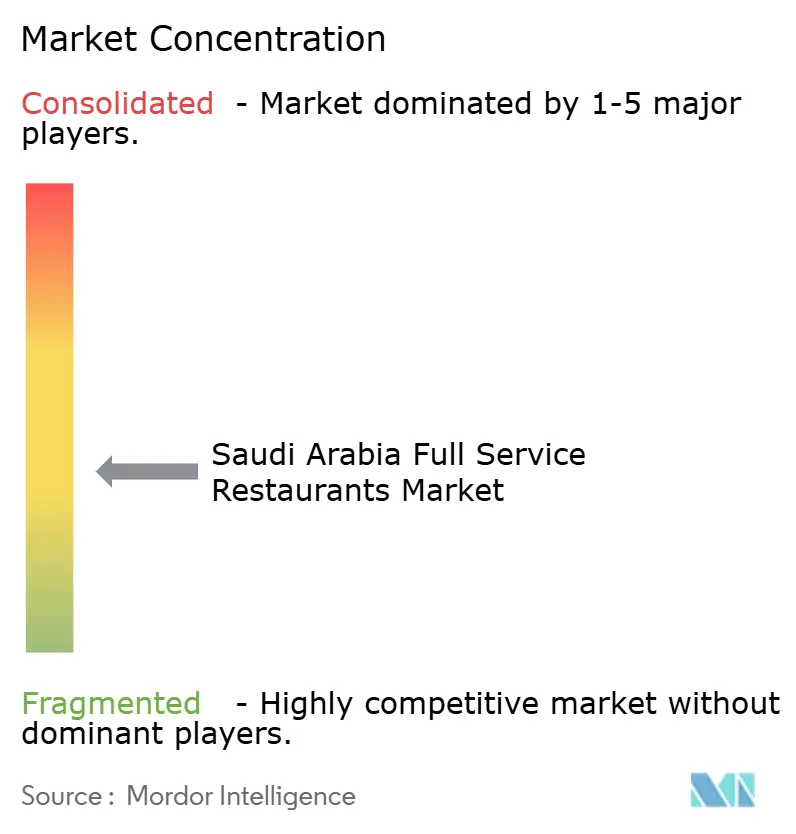

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Full Service Restaurants Market Analysis by Mordor Intelligence

The Saudi Arabia full-service restaurants market is projected to reach USD 16.15 billion in 2025 and is expected to grow to USD 24.12 billion by 2030, registering a CAGR of 8.35% during the forecast period. Key growth drivers include the development of tourism under Vision 2030, a growing middle-income population, and supportive franchise regulations. These factors are driving higher average check values and the expansion of outlets in major cities. Significant investments in infrastructure, including destination projects and the addition of new hotel rooms, are expected to sustain demand from both domestic and international visitors. Additionally, the increasing adoption of digital payments, as seen in restaurant POS transactions in August 2024, is improving revenue visibility and enabling data-driven menu optimization. Operators who effectively integrate dine-in, takeaway, and delivery channels are capturing additional sales while keeping fixed costs under control, thereby enhancing profit margins over the medium term. According to the International Trade Administration, the country recorded substantial tourist arrivals in 2023, with combined domestic and international tourism spending reaching significant levels. The government aims to increase tourism’s direct GDP contribution from its current level to 10% by 2030[1]Source: Saudi Arabian Monetary Authority, “POS Transactions Data,” sama.gov.sa.

Key Report Takeaways

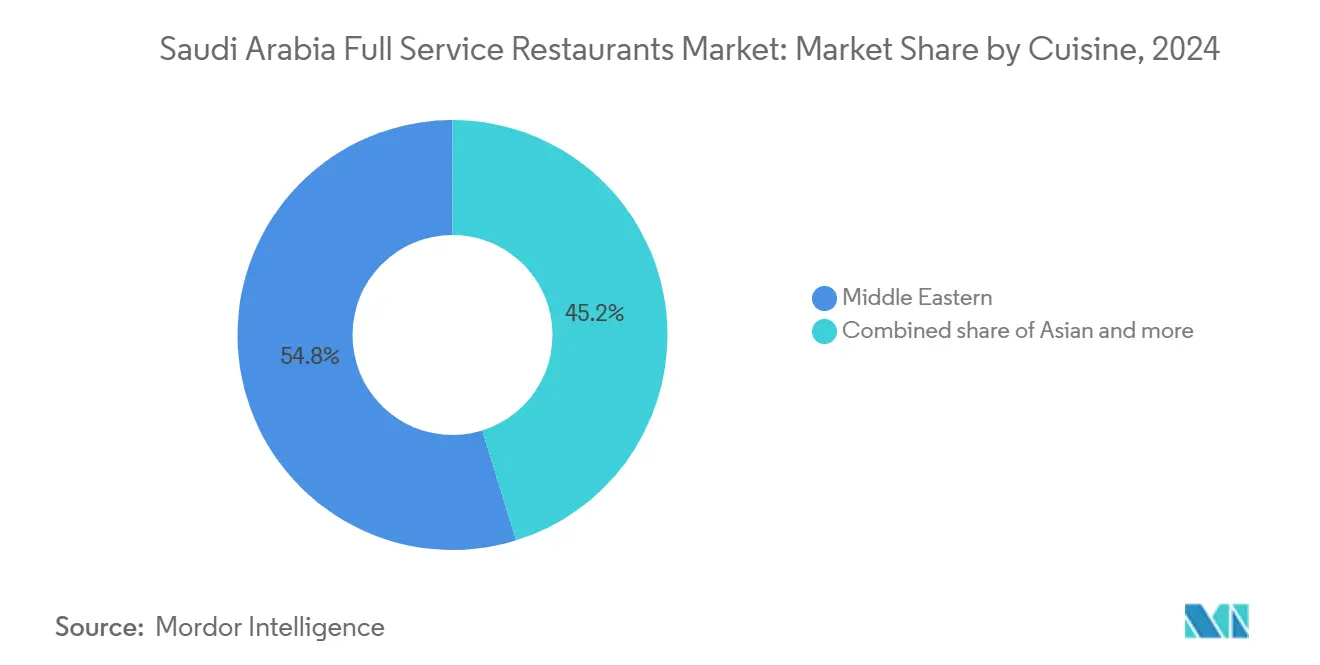

- By cuisine, Middle Eastern concepts led with 45.23% of the Saudi Arabia full service restaurants market share in 2024; Latin American outlets are projected to expand at a 10.43% CAGR to 2030.

- By outlet type, chained outlets captured 55.93% revenue share in 2024, while independent venues are expected to post a 7.81% CAGR as consumer appetite for niche dining experiences rises.

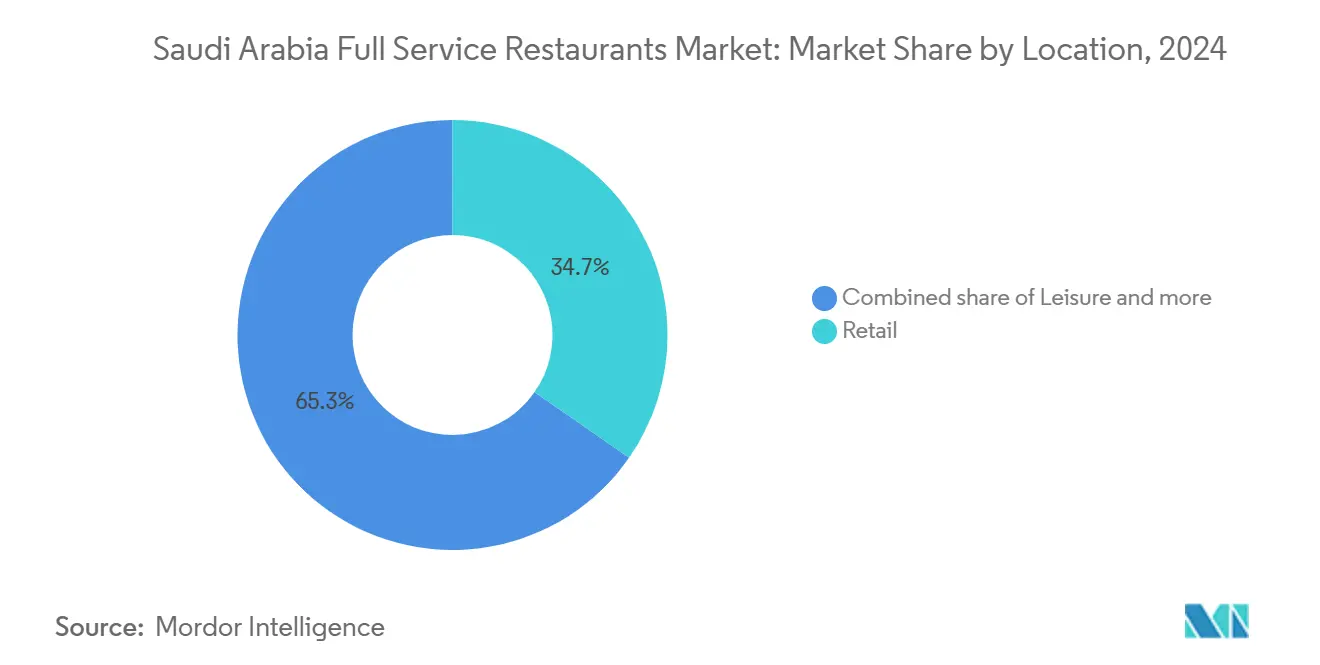

- By location, retail settings commanded 39.24% of 2024 sales; the same format is poised to grow at a 9.21% CAGR through 2030.

- By service type, dine-in held 65.29% of spending in 2024, whereas takeaway is advancing at a 9.01% CAGR on the back of mobile ordering adoption.

Saudi Arabia Full Service Restaurants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural emphasis on family and group dining | +1.5% | National, concentrated in Riyadh, Makkah, Eastern Province | Long term (≥ 4 years) |

| Boom in international chain restaurant entries | +0.8% | Major cities: Riyadh, Jeddah, Dammam, with spillover to secondary markets | Medium term (2-4 years) |

| Rise of specialty and niche cuisines | +1.2% | Urban centers with high disposable income, tourist destinations | Medium term (2-4 years) |

| Increased focus on health-conscious options | +0.9% | National, early adoption in affluent districts | Short term (≤ 2 years) |

| Expanding leisure and entertainment sector | +1.8% | NEOM, Red Sea, Qiddiya, Diriyah, major urban entertainment districts | Long term (≥ 4 years) |

| Online food ordering/delivery integration for FSRs | +1.1% | Metropolitan areas with high smartphone penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cultural emphasis on family and group dining

Saudi Arabia's family-centric culture sustains demand for full-service restaurants that cater to large group gatherings and extended dining experiences. The traditional majlis-style socializing fosters a preference for spacious venues with private dining areas, resulting in higher average check sizes compared to the individual dining patterns common in Western markets. Regional food preferences vary significantly, with Najdi cuisine dominating the central regions and Hejazi flavors prevailing in the western provinces. This creates opportunities for restaurants to authentically represent local culinary traditions. The cultural practice of hosting extended family during religious holidays and social occasions drives predictable demand spikes, with restaurants experiencing 40-60% higher revenues during Ramadan and Eid periods. Additionally, government initiatives under Vision 2030, aimed at promoting cultural heritage, further support traditional dining customs, positioning family-oriented full-service restaurants as key beneficiaries of this cultural preservation effort.

Boom in international chain restaurant entries

The Kingdom's franchise market has witnessed remarkable growth by Q3 2024, driven by the removal of regulatory barriers and the introduction of streamlined approval processes that have significantly reduced the time required for market entry. Monsha'at's Franchise Center has played a pivotal role in this expansion, supporting a substantial number of brands ready for franchising, with the accommodation and food services sectors dominating registrations. International operators have gained from substantial financing agreements dedicated to franchise expansion, while master franchise agreements have enabled swift multi-city rollouts across the Kingdom's primary urban centers. The 2024 Franchise Expo underscored this momentum, with numerous franchise agreements signed, reflecting a rapid proliferation of brands that is set to enhance competitive dynamics and broaden consumer options. Geographically, the focus remains on high-density markets such as Riyadh, Makkah, and the Eastern Province, indicating a strategic approach by international chains to establish a strong presence in major urban areas before targeting secondary cities.

Rise of specialty and niche cuisines

Consumer sophistication and increased international exposure through travel and digital media consumption are driving demand for authentic specialty cuisines beyond traditional offerings. The impressive growth of Latin American cuisine highlights this trend, supported by the successful market entry of concepts like Maido and other Peruvian establishments that appeal to affluent demographics seeking unique dining experiences. The Saudi Food and Drug Authority's mandatory nutrition labeling requirements, effective from 2024, provide an opportunity for specialty cuisine operators to differentiate themselves by emphasizing transparency in ingredient sourcing and preparation methods[2]Source: Saudi Food and Drug Authority, “Menu Nutrition Labeling Regulations,” sfda.gov.sa. This transparency resonates with consumers who value knowing the origins and preparation of their food. Niche positioning enables smaller operators to command premium pricing while avoiding direct competition with established mainstream chains. Additionally, NEOM's food security initiatives, which focus on novel proteins and sustainable aquaculture, create supply chain opportunities for specialty restaurants aiming to source locally and align with evolving consumer preferences for environmentally-conscious ingredients.

Increased Focus on Health-Conscious Options

The Saudi Food and Drug Authority's introduction of comprehensive nutrition labeling regulations in 2024 is driving increased menu transparency, aligning with the growing demand from health-conscious consumers. Flexitarian dining trends, supported by research indicating a rise in plant-based food adoption among Saudi consumers, present opportunities for full-service restaurants to diversify their protein offerings beyond traditional meat-focused menus. Additionally, NEOM's investments in controlled-environment agriculture and novel protein development provide local sourcing options for restaurants aiming to position themselves as health-focused establishments. The alignment of regulatory requirements with evolving consumer preferences offers competitive advantages to operators who adopt clean-label ingredients and provide transparent nutritional information. Furthermore, rising disposable income among younger, urban demographics supports a willingness to pay premium prices for health-oriented dining, enabling sustainable business models centered on wellness-focused concepts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition from quick-service and delivery-only models | -0.7% | Urban centers with high delivery penetration | Short term (≤ 2 years) |

| Strict food safety, licensing, and labor regulations | -0.5% | National, stricter enforcement in major cities | Medium term (2-4 years) |

| Rising operating costs | -0.8% | National, acute in prime real estate locations | Short term (≤ 2 years) |

| Pressure on maintaining uniform quality across chains | -0.6% | Chain operators with multiple locations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High competition from quick-service and delivery-only models

Cloud kitchens and delivery-only concepts take advantage of structural cost benefits by removing front-of-house expenses, high rents for prime locations, and the need for extensive service staff. This enables them to offer competitive pricing while maintaining better profit margins compared to traditional full-service establishments. The growing online food delivery market fosters platform-dependent ecosystems, allowing delivery-only operators to quickly test market demand and scale successful concepts without the significant capital investment required for full-service restaurant buildouts. Consolidation within the delivery sector has concentrated market power among platform operators, which may lead to higher commission rates and reduced profitability for full-service restaurants reliant on third-party delivery channels. Changes in consumer behavior, accelerated by pandemic-era dining restrictions, have normalized delivery and takeaway consumption, reducing the frequency of dine-in occasions that are critical for full-service restaurants to maximize revenue. Competitive pressures are particularly pronounced in urban markets where delivery infrastructure is highly developed, pushing full-service operators to invest in technology integration and improve operational efficiency to maintain their market share against more agile, delivery-focused competitors.

Rising operating costs

Labor cost inflation, driven by Saudization requirements, continues to exert pressure on full-service restaurants, which typically operate with higher staff-to-revenue ratios compared to quick-service alternatives. Financial disclosures from major operators indicate margin compression, with some reporting profit declines despite revenue growth, primarily due to higher selling and administrative expenses. Real estate costs in prime locations are escalating as Vision 2030 infrastructure projects drive demand for commercial space, particularly in entertainment districts and tourism zones where full-service restaurants aim to secure optimal locations. Additionally, commodity price volatility impacts ingredient costs, while supply chain disruptions compel restaurants to maintain higher inventory levels or source from premium suppliers, both of which negatively affect profitability. The Saudi Arabian Monetary Authority's interest rate environment further influences financing costs for expansion and working capital, adding financial strain on operators looking to scale their businesses[3]Source: International Trade Administration, “Saudi Arabia Tourism Industry Expansion,” trade.gov. Although energy and utility costs remain subsidized, gradual rationalization under economic diversification policies increases the cumulative cost burden. Full-service restaurants must either absorb these costs or pass them on to consumers through menu price adjustments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine: Middle Eastern Dominance Faces Diversification

Middle Eastern cuisine is set to hold a significant market share of 45.23% in 2024, driven by its deep cultural roots and established supply chains for traditional ingredients. Latin American cuisine is expected to grow at a robust compound annual growth rate (CAGR) of 10.43% through 2030, as consumers increasingly seek authentic international dining experiences. Asian cuisine continues to benefit from the growing expatriate population and business travel, particularly in the oil industry hubs of the Eastern Province. European cuisine concepts remain focused on luxury hotels and upscale shopping districts, catering to premium dining preferences. Meanwhile, North American franchise chains rely on their strong brand recognition and operational systems but face rising competition from regional Middle Eastern concepts that better align with local tastes and dining customs.

Other full-service restaurant (FSR) cuisines, including fusion and contemporary options, are carving out market share by offering unique dining experiences. These concepts leverage social media-driven marketing to attract younger consumers looking for visually appealing and memorable dining occasions. Furthermore, the Saudi Food and Drug Authority's nutrition labeling requirements create opportunities for cuisines that emphasize fresh ingredients and transparent preparation methods. This trend particularly benefits Mediterranean and contemporary healthy dining concepts, which align with consumer preferences for health-conscious and high-quality meals.

By Outlet: Chained Operations Drive Market Evolution

Chained outlets are anticipated to capture 55.93% of the market share in 2024, with a robust growth rate of 9.55% CAGR. This impressive growth is largely attributed to the establishment of a comprehensive franchise support system, which has significantly shortened market entry timelines from the earlier 8-12 months to just 2 months. By streamlining regulatory processes, this system has enabled chained outlets to expand their operations more efficiently, allowing them to seize growth opportunities and strengthen their market presence. The structured approach not only accelerates expansion but also ensures consistency in operations, which is critical for maintaining brand standards and customer trust.

Independent outlets, meanwhile, are navigating increasing competitive pressures from their chained counterparts. However, they continue to hold a unique position in the market by capitalizing on their inherent strengths. These include greater menu flexibility, the ability to adapt to local market preferences, and an authentic cultural appeal that resonates with consumers seeking personalized and unique dining experiences. Furthermore, the development of the franchise ecosystem, supported by Monsha'at's SAR 2.4 billion financing program, has provided a significant boost to the industry. This initiative not only facilitates the rapid geographic expansion of successful concepts but also offers operational guidance, which plays a crucial role in improving the success rates of new entrants in the market.

By Location: Retail Integration Transforms Dining Patterns

Retail locations are projected to account for 39.24% of the market share in 2024, with a growth rate of 9.21% CAGR. This growth reflects the successful integration of dining and shopping experiences, which enhance consumer dwell times and boost per-visit spending in mixed-use developments. Standalone locations continue to hold a significant presence but face challenges due to rising real estate costs in prime areas. These challenges are further intensified by Vision 2030 infrastructure projects, which are increasing demand for commercial space in entertainment and tourism zones.

Leisure locations benefit from growing investments in the entertainment sector. For instance, SEVEN's USD 13 billion program aims to develop 21 destinations, creating captive audiences for co-located dining venues. Lodging-based restaurants are supported by the expansion of the hotel pipeline, which is expected to reach 315,000 rooms by 2030. However, these establishments face seasonal fluctuations influenced by pilgrimage and business travel patterns. Travel locations, such as airports and transportation hubs, are experiencing steady growth driven by increased connectivity and rising passenger traffic.

By Service Type: Traditional Dine-In Adapts to Digital Integration

Dine-in services are expected to maintain a 65.29% market share in 2024, underscoring the enduring appeal of social dining experiences and the personalized hospitality offered by full-service restaurants. This preference highlights the value customers place on the ambiance and service quality that come with dining out. Meanwhile, takeaway services are projected to grow at a robust CAGR of 9.01%, fueled by advancements in digital integration. These innovations enable full-service restaurants to extend their reach, catering to customer demand beyond the constraints of traditional operating hours and seating capacity, thereby unlocking new revenue streams.

Delivery services are poised to benefit from the rapidly growing online food delivery market, which is forecasted to reach USD 13.5 billion by 2030. However, full-service operators face challenges in maintaining profitability due to commission structures and the operational complexities associated with delivery, which differ significantly from the higher-margin dine-in transactions they are accustomed to. To address these challenges, many operators are investing in sophisticated technology infrastructure. The implementation of unified POS systems has become critical, allowing seamless synchronization of inventory, pricing, and order management across dine-in, takeaway, and delivery channels, ensuring operational efficiency and a consistent customer experience.

Geography Analysis

Saudi Arabia's full-service restaurant market is primarily concentrated in key urban areas. Riyadh leads the market, accounting for 34% of restaurant point-of-sale activity, driven by its high population density, elevated disposable income levels, and advanced infrastructure that supports a thriving dining ecosystem. Jeddah follows with 14% of activity, reflecting similar urban dynamics. The Eastern Province, anchored by cities like Dammam and Al Khobar, benefits from its oil industry workforce and international business presence, which fuel demand for premium dining experiences. This region also serves as a testing ground for international restaurant concepts before their broader rollout across the Kingdom.

Secondary markets, including Medina, Taif, and Abha, are emerging as the fastest-growing segments. These areas are gaining traction due to infrastructure development and tourism initiatives under Vision 2030, which are enhancing accessibility and driving economic activity. As these regions become more connected and economically vibrant, they present significant opportunities for restaurant operators to tap into underserved markets.

Vision 2030 mega-projects and other tourism infrastructure investments are creating additional growth opportunities across the country. Projects like NEOM's Sindalah Island, which plans 38 fine-dining establishments, and The Red Sea project, with its 50 resorts across 22 islands, are reshaping market dynamics. Qiddiya's entertainment city, targeting 48 million annual visitors by 2030, is expected to generate concentrated dining demand. With USD 800 billion allocated to tourism infrastructure across multiple regions, the market is expanding beyond traditional urban centers to purpose-built destinations requiring full-service dining options aligned with luxury tourism goals.

Competitive Landscape

The Saudi Arabia full-service restaurant market is moderately fragmented, fostering a competitive environment where established players coexist with emerging concepts and international entrants. Strategic approaches in this market can be categorized into three primary areas: international franchise expansion leveraging established operational systems, local concept development emphasizing cultural authenticity, and hybrid models that combine international brand recognition with regional menu adaptations. The adoption of technology is a key differentiator for successful operators, with integrated POS systems, delivery platform connectivity, and customer relationship management tools enabling data-driven decision-making and operational efficiency improvements.

Alamar Foods' recent performance underscores market volatility, with a revenue decline followed by significant net profit growth in Q4 2024, driven by operational optimization and strategic positioning. White-space opportunities are emerging around mega-project developments, offering first-mover advantages to operators willing to invest in purpose-built destinations before market saturation occurs. Disruptive trends include delivery-only concepts that challenge traditional cost structures, health-focused establishments benefiting from regulatory transparency requirements, and experiential dining venues incorporating entertainment elements to justify premium pricing.

The franchise ecosystem is expanding rapidly, with registrations reaching a notable level by Q3 2024. This growth intensifies competition while creating opportunities for scalable concepts. However, regulatory compliance, particularly with Saudi Food and Drug Authority nutrition labeling requirements, adds operational complexity. This dynamic favors well-capitalized operators with advanced supply chain management capabilities, as smaller independent establishments may lack the resources to implement comprehensive compliance programs.

Saudi Arabia Full Service Restaurants Industry Leaders

Al Faisaliah Group

Americana Restaurants Intl PLC

Saleh Y Naghi (Naghi & Sons)

Bloomin' Brands Inc.

Landmark Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Michael Mina has launched his first Saudi restaurant, Taleed by Michael Mina, in Riyadh’s Diriyah. The venue blends Mina’s Middle Eastern heritage with Mina Group’s culinary expertise, offering innovative dishes influenced by traditional Saudi flavors, a significant addition to the Kingdom’s rapidly evolving culinary scene.

- November 2024: Dog Haus, the fast-casual hot dog and burger brand with 50 locations in the US, debuted in Saudi Arabia to strong local enthusiasm. Recently partnering with Jake Paul, the brand made headlines and continues international expansion, though the specific Saudi launch site remains undisclosed.

- August 2024: Epik Foods has opened its first brick-and-mortar restaurant, Healthy & Co, in Riyadh, Saudi Arabia. This launch marks their expansion from delivery-only kitchens to physical dining, targeting the growing demand for healthy food. Further openings in Jeddah and Khobar are planned, solidifying Epik Foods’ regional presence.

Saudi Arabia Full Service Restaurants Market Report Scope

| Asian |

| European |

| Latin American |

| Middle Eastern |

| North American |

| Other FSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-In |

| Takeaway |

| Delivery |

| By Cuisine | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| By Outlet | Chained Outlets |

| Independent Outlets | |

| By Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel | |

| By Service Type | Dine-In |

| Takeaway | |

| Delivery |

Key Questions Answered in the Report

What revenue figure do full-service restaurants record in 2025 and how fast will they expand through 2030?

Sales reach USD 16.15 billion in 2025 and are forecast to climb to USD 24.12 billion, implying an 8.35% CAGR over the period.

Which cuisine line shows the strongest upside over the next five years?

Latin American concepts lead with a projected 10.43% CAGR, benefitting from rising demand for novel, chef-driven experiences.

How will Vision 2030 mega-projects affect outlet placement strategies?

New demand clusters at NEOM, the Red Sea resorts, and Qiddiya will favor first-mover operators that secure fine-dining pads inside these developments.

Which technology upgrades deliver the quickest payback for operators?

Cloud-based POS systems that synchronize dine-in, takeaway, and delivery channels reduce idle kitchen capacity below 5% and curb order-to-pickup times to under 12 minutes.

How do chained and independent outlets compare on growth trajectories?

Chains hold 55.93% of 2024 sales and grow at 9.55% CAGR thanks to franchise financing, while independents retain agility and are expected to expand at 7.81% CAGR by focusing on niche concepts.

Page last updated on: