Saudi Arabia Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

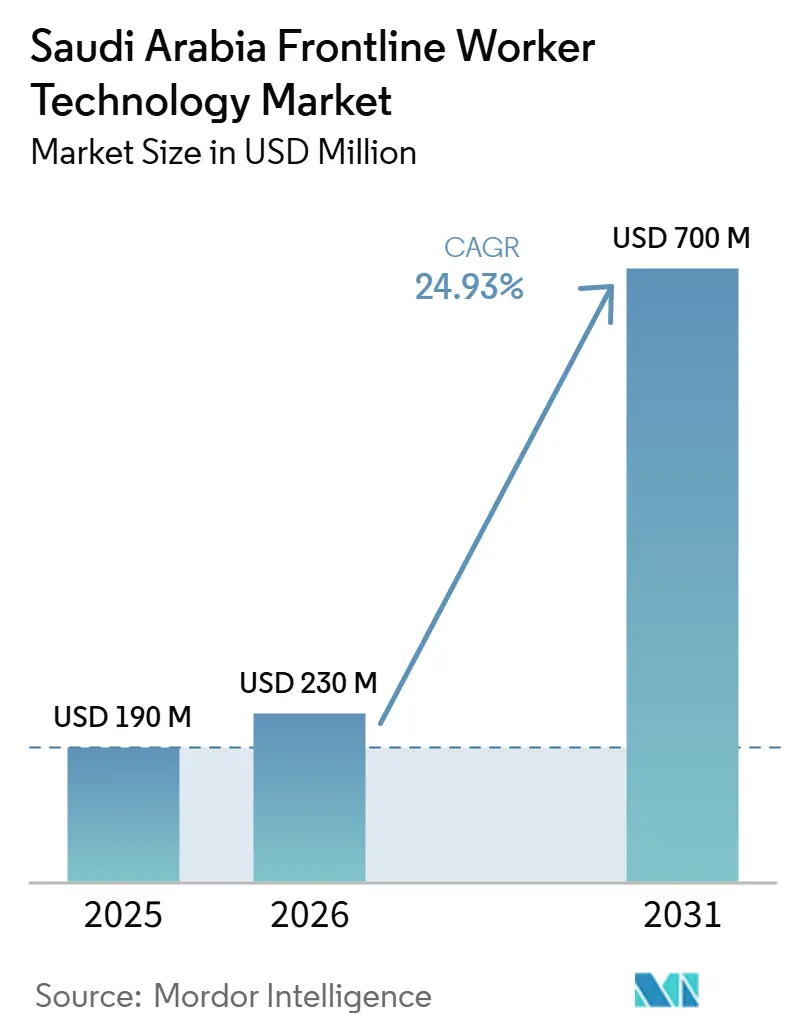

| Base Year Market Size (2025) | USD 190 Million |

| Market Size (2026) | USD 230 Million |

| Market Size (2031) | USD 700 Million |

| Growth Rate (2026 - 2031) | 24.93% CAGR |

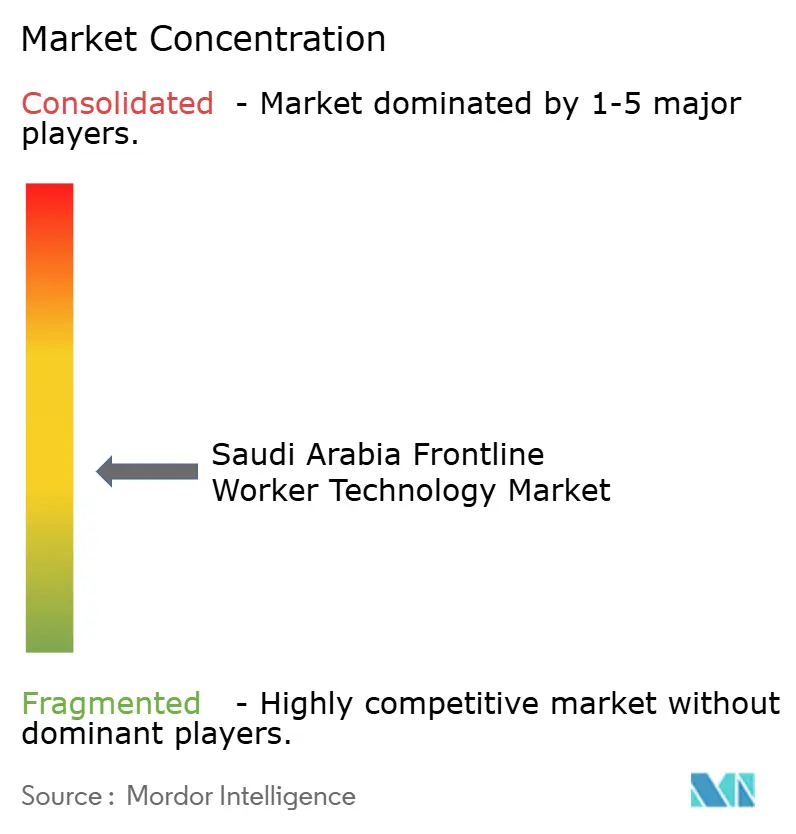

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Frontline Worker Technology Market Analysis by Mordor Intelligence

The Saudi Arabia frontline worker technology market size was valued at USD 190 million in 2025 and estimated to grow from USD 230 million in 2026 to reach USD 700 million by 2031, at a CAGR of 24.93% during the forecast period (2026-2031). Growth is being shaped by the large project pipeline under Vision 2030, which is consolidating workers, contractors, and safety obligations across construction, industrial, logistics, and public operations. Regulatory tightening has also moved digital safety management closer to a business requirement, as contractors now need stronger documentation, audit-readiness, and workforce traceability to remain eligible for major work packages. The market is also benefiting from stronger local technology presence, improved industrial connectivity, and greater acceptance of platforms that combine field communication, compliance workflows, and operational data in a single system. Competition is widening as global software vendors, rugged device makers, wearable specialists, and localizing providers all target the same enterprise accounts and project ecosystems. Budget constraints among subcontractors and uneven interoperability across mixed-vendor environments still slow adoption, but the direction of the Saudi Arabia frontline worker technology market remains firmly upward as buyers shift from isolated tools to broader frontline operating systems.

Key Report Takeaways

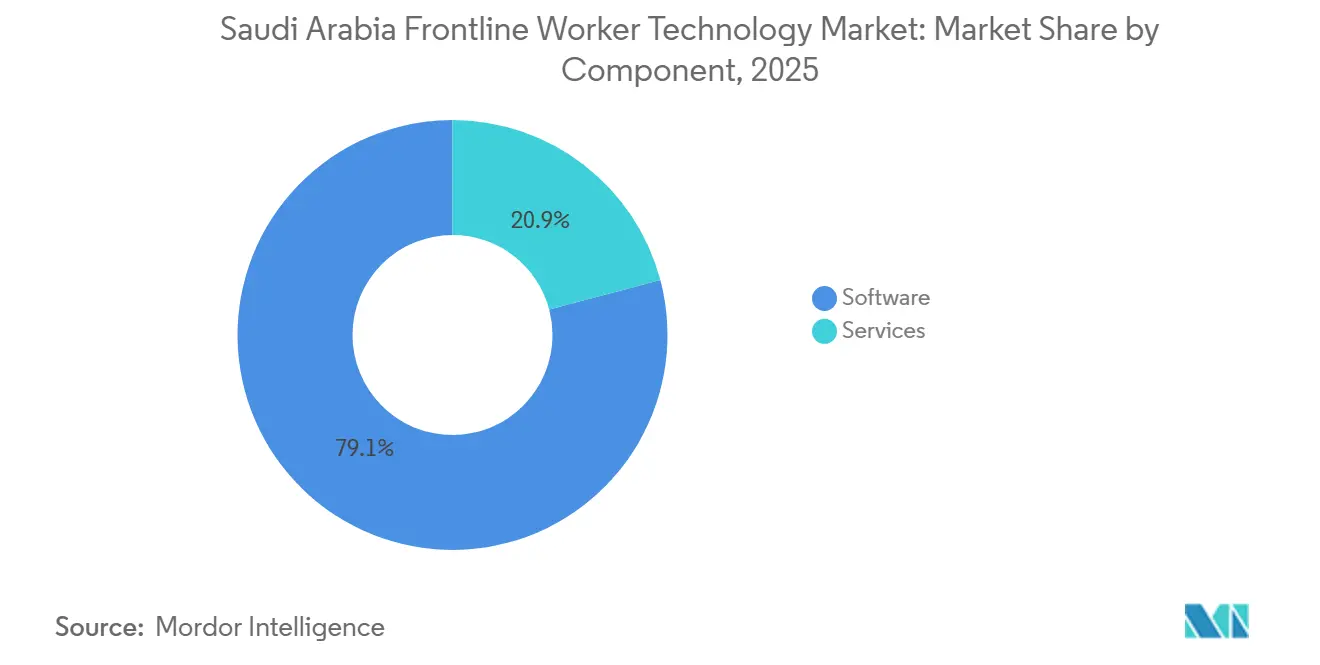

- By component, software held 79.11% of the Saudi Arabia frontline worker technology market share in 2025, while services are projected to expand at a 26.14% CAGR through 2031.

- By deployment, cloud-based platforms accounted for 74.61% of the Saudi Arabia frontline worker technology market size in 2025 and are expected to grow at a 27.33% CAGR through 2031.

- By organization size, large enterprises captured 73.61% share in 2025, while small and medium enterprises are projected to record the fastest CAGR of 28.89% through 2031.

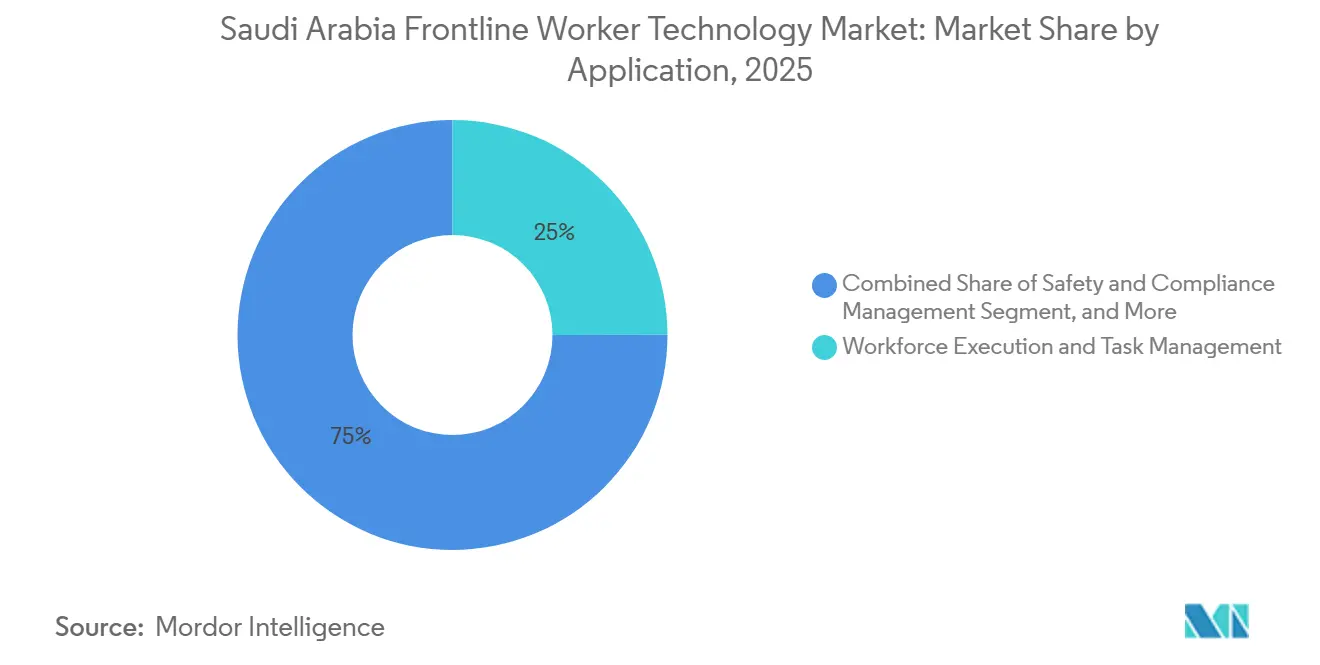

- By application, Workforce Execution and Task Management held a 24.99% share in 2025, while Safety and Compliance Management is projected to advance at a 29.41% CAGR through 2031.

- By end-user industry, construction accounted for 28.11% of the market share in 2025, while Government and Public Administration is projected to expand at a 31.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Worker Safety Digitization Across Hazard-Heavy Industries | +5.5% | National, led by major construction, industrial, and energy sites | Short term (≤ 2 years) |

| Tightening Occupational Safety Compliance in High-Risk Worksites | +4.8% | National, with stronger relevance in construction, petroleum, gas, electricity, and manufacturing | Short term (≤ 2 years) |

| Faster Adoption of Connected Wearables for Real-Time Hazard Detection | +3.9% | National, strongest across construction, industrial, and remote field operations | Medium term (2-4 years) |

| Expansion of Private 5G, LTE, and Industrial IoT Coverage at Industrial Sites | +3.2% | National industrial zones, especially energy, logistics, and manufacturing corridors | Medium term (2-4 years) |

| Aramco-Led Digital Safety Procurement Standards | +2.6% | Saudi Arabia and GCC supplier ecosystems linked to Aramco requirements | Medium term (2-4 years) |

| Heat Stress Analytics Demand in Outdoor Workforces | +1.8% | Saudi Arabia and other GCC outdoor labor environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Worker Safety Digitization Across Hazard-Heavy Industries

Worker safety digitization has moved closer to core operations in the Saudi Arabia frontline worker technology market, as large worksites now need faster reporting, tighter coordination, and clearer accountability across multiple contractor layers. The 2024 occupational safety framework from the Ministry of Human Resources and Social Development required establishments with 50 or more workers in high-risk sectors to implement an occupational health and safety management system aligned with ISO 45001.[1]Ministry of Human Resources and Social Development, “Occupational Safety and Health Management Regulation,” Ministry of Human Resources and Social Development, hrsd.gov.sa That requirement raised the value of software that can record incidents, manage corrective actions, and preserve a reliable audit trail over time. Cority’s 2026 launch in Saudi Arabia with in-Kingdom cloud hosting showed that vendors now see local deployment and local compliance support as necessary for serious participation in the Saudi Arabia frontline worker technology market. As a result, buyers are increasingly treating digital frontline systems as operating infrastructure rather than optional support tools.

Tightening Occupational Safety Compliance in High-Risk Worksites

Compliance pressure has become a direct growth driver in the Saudi Arabia frontline worker technology market because safety requirements now shape procurement decisions earlier in the project cycle. The Ministry of Human Resources and Social Development stated that health and safety in the work environment must be supported through formal rules, protective measures, and employer responsibility across Saudi workplaces.[2]Ministry of Human Resources and Social Development, “Health and Safety in the Work Environment,” Ministry of Human Resources and Social Development, hrsd.gov.sa. The detailed OSH regulation also required larger establishments in high-risk fields to formalize systems and assign qualified responsibility for occupational health and safety management. Saudi Aramco’s third-party cybersecurity compliance program added another screening layer for vendors that want to supply connected systems into Aramco-linked environments. This has shortened the path for suppliers, enabling them to combine compliance workflows, security controls, and enterprise deployment support into a single offer.[3]Aramco Digital, Armada, and Microsoft, “Aramco Digital, Armada, and Microsoft Collaborate to Deploy World’s First Industrial Distributed Cloud,” PR Newswire, prnewswire.co.uk.

Faster Adoption of Connected Wearables for Real-Time Hazard Detection

Connected wearables are gaining ground in the Saudi Arabia frontline worker technology market because employers want more continuous visibility into worker location, exposure, and field conditions. A 2025 study in Buildings found that awareness and adoption of IoT and wearable tools in the Saudi construction sector remained uneven, suggesting the runway for expansion remains significant as training and incentives improve. Blackline Safety launched the G8 wearable in January 2026, combining gas detection, lone worker protection, and communication in a rugged device, reflecting broader demand for fewer devices with greater field capability. Qualcomm and Aramco Digital also announced work on an AI-enabled industrial 5G smartphone with native 450 MHz support, signaling a broader move toward smarter field endpoints for frontline teams. The Saudi Arabia frontline worker technology market is therefore moving toward bundled hardware, software, and analytics instead of isolated devices bought one at a time.

Expansion of Private 5G, LTE, nd Industrial IoT Coverage at Industrial Sites

Better industrial connectivity is supporting the Saudi Arabia frontline worker technology market because connected safety and workflow systems only deliver full value when they operate reliably across large, remote sites. Qualcomm and Aramco Digital announced in 2025 that they were collaborating on an industrial 5G smartphone supporting the 450 MHz band, directly linking frontline devices to industrial IoT use cases. Aramco Digital, Armada, and Microsoft also announced a collaboration to accelerate real-world AI and digital transformation in industrial settings through a distributed cloud. These moves matter because they improve the conditions for live data exchange, remote oversight, and faster application response times in the field. The result is a stronger base for cloud platforms, mobile workflow tools, and connected worker applications across the Saudi Arabia frontline worker technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Sensitivity Among Mid-Tier Contractors and Subcontractors | -2.8% | National, strongest among mid-sized contractors and labor-heavy subcontractors | Short term (≤ 2 years) |

| Workforce Adoption Friction for Always-On Monitoring and Wearable Usage | -1.6% | National, especially in labor-intensive project settings with mixed workforce profiles | Medium term (2-4 years) |

| Cybersecurity and Data Governance Concerns for Worker Location and Biometric Data | -1.2% | National, especially in security-sensitive industrial and energy environments | Medium term (2-4 years) |

| Device Interoperability Gaps Across Multi-Vendor Safety Stacks | -0.7% | National, strongest on large sites using multiple hardware and software vendors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Sensitivity Among Mid-Tier Contractors and Subcontractors

Budget pressure remains the clearest structural restraint in the Saudi Arabia frontline worker technology market, as labor-intensive subcontractors often operate on tight margins while still facing rising compliance demands. A 2025 Springer Nature study on cloud adoption barriers in Saudi construction found that security concerns and connectivity issues ranked among the most significant challenges, while cost and expertise limits also shaped adoption outcomes. These constraints matter because smaller contractors usually have fewer internal resources to manage implementation, training, and system support after the first purchase. The result is slower conversion from interest to deployment, even when project owners favor more digital oversight. Vendors that lower the first-step burden through subscriptions, managed setup, and simpler reporting formats are better positioned to widen adoption in this part of the Saudi Arabia frontline worker technology market.

Workforce Adoption Friction for Always-on Monitoring and Wearable Usage

Worker adoption still slows parts of the Saudi Arabia frontline worker technology market because the value of connected tools depends on consistent daily use in the field. The 2025 Buildings study on IoT and wearable adoption in Saudi construction reported low awareness among site workers and highlighted the need for better engagement and support for Construction 4.0 tools.[4]MDPI, “Barriers, Enablers, and Adoption Patterns of IoT and Wearable Devices in the Saudi Construction Industry, Survey Evidence,” Buildings, mdpi.com This challenge is sharper for always-on devices that workers may view as intrusive or uncomfortable during long shifts. It is less severe for tools that deliver an immediate worker benefit, such as safety alerts, faster communication, or easier task guidance. Adoption will improve, but the Saudi Arabia frontline worker technology market still needs stronger training design and clearer worker-facing value to drive sustained usage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue While Services Scale With Implementation Needs

Software held 79.11% of the Saudi Arabia frontline worker technology market in 2025, indicating that buyers still allocate most spending to platforms that organize frontline work, safety reporting, and communication. This lead reflects the way large organizations prefer recurring systems that can be rolled out across sites instead of stand-alone tools with narrow use cases. The Saudi Arabia frontline worker technology market size for software remains closely tied to enterprise demand for documentation, workflow control, and audit readiness across complex contractor environments. Cority’s Saudi launch in 2026, with local cloud hosting and regulatory alignment, reinforced that software suppliers now compete on localization and deployment depth as much as on features.

Services are the fastest-growing component, with a 26.14% CAGR through 2031, because many buyers need support well beyond the initial software license. Implementation, systems integration, user training, and ongoing program support all become more important when deployments span multiple sites and contractor groups. The Ministry of Human Resources and Social Development's requirement for structured occupational health and safety management also supports ongoing advisory and process support around digital systems. SAP’s January 2026 workforce system deployment for the National Center for Non-Profit Sector Development, which processed more than 22,000 employee requests and 9 payroll cycles on an integrated system, showed how services-led execution can accelerate digital workforce transformation in Saudi organizations.

By Deployment: Cloud Platforms Lead Current Demand And Future Growth

Cloud-based deployment held a 74.61% share in 2025 and is projected to record a 27.33% CAGR through 2031, indicating that the Saudi Arabia frontline worker technology market is moving most strongly toward centrally managed, scalable operating models. Large project footprints and remote sites make centralized updates, mobile access, and data availability more practical in the cloud than in isolated local environments. The Saudi Arabia frontline worker technology market share for cloud platforms is also supported by the need to standardize workflows across supervisors, field teams, and contractors without rebuilding local systems at every site. Cority’s Saudi platform is hosted on Google Cloud within the Kingdom, which shows that local cloud presence now matters to enterprise buyers and regulators alike.

Hybrid deployment still holds relevance in cases where some operational data is kept under tighter internal control while other workflows move to shared platforms. On-premises systems remain present in narrower environments where data sensitivity, legacy architecture, or internal policy slows migration. At the same time, Saudi Aramco’s supplier cybersecurity compliance requirements make secure architecture a basic condition for connected technology providers in critical environments. That mix still favors cloud growth because security, residency, and scalability are increasingly being addressed within localized enterprise-grade hosting models rather than through fully separate installations.

By Organization Size: Large Enterprises Hold The Base While SMEs Lift The Growth Rate

Large enterprises captured 73.61% of the Saudi Arabia frontline worker technology market in 2025, reflecting their stronger budgets, wider project footprints, and greater ability to absorb implementation complexity. This group includes large industrial operators, major project developers, public institutions, and prime contractors that need unified platforms across many workers and locations. Their spending has an outsized influence on the Saudi Arabia frontline worker technology market because enterprise deals often combine software, rugged devices, integration, and long support commitments in a single procurement cycle. Saudi Aramco’s third-party cybersecurity compliance program also favors better-resourced vendors and buyers that can meet higher technical and governance standards.

Small and medium enterprises are projected to grow at a 28.89% CAGR through 2031, indicating that adoption is spreading down the contractor pyramid, even though the revenue base remains concentrated higher up. The push is practical because smaller firms need auditable records, safer field processes, and better labor coordination to stay competitive in large project ecosystems. The 2025 Springer Nature study on Saudi construction barriers showed why this segment still moves more slowly: security concerns, connectivity limitations, and internal capability gaps remain significant obstacles. Even so, the Saudi Arabia frontline worker technology industry is opening up more space for mobile-first, lower-complexity solutions that better fit subcontractor budgets than full enterprise suites.

By Application: Task Management Leads Today While Safety Compliance Expands Fastest

Workforce Execution and Task Management held the largest 2025 share at 24.99%, while Safety and Compliance Management is projected to grow at a 29.41% CAGR through 2031. The first pattern reflects the daily need to assign tasks, manage handoffs, track completion, and coordinate crews across labor-intensive sites. The second pattern reflects tighter legal and procurement standards that place more value on digital records, incident management, and documented compliance actions. The Saudi Arabia frontline worker technology market for compliance applications is benefiting from the Ministry of Human Resources and Social Development framework, which requires larger, high-risk establishments to implement structured safety management aligned with ISO 45001.

The rest of the application mix is also becoming more connected rather than remaining in separate silos. Employee communication tools matter because multilingual and shift-based workforces need consistent updates and fast issue escalation. Learning and knowledge tools are gaining importance as organizations try to improve field readiness without slowing site activity. Aramco’s Yanbu refinery's digital transformation demonstrated how virtual reality training can support safer, more efficient learning delivery in industrial operations. TeamViewer also demonstrated in 2025 how augmented reality and SAP-linked guidance can support inspection, assembly, and maintenance workflows, which fits the broader move toward application convergence in the Saudi Arabia frontline worker technology market.

By End-User Industry: Construction Holds The Largest Base While Government Expands Fastest

Construction accounted for 28.11% share in 2025, while Government and Public Administration is projected to record the fastest CAGR of 31.66% through 2031. Construction remains the largest base because the Saudi Arabia frontline worker technology market is closely tied to large sites where labor coordination, safety tracking, and contractor oversight all need stronger digital support. The sector also benefits from the availability of rugged devices and industrial localization, as shown by Honeywell’s October 2025 production line in Dhahran for frontline-worker handheld computers. Qualcomm’s 2025 collaboration with Aramco Digital on an AI-enabled industrial 5G smartphone also supports the construction case by expanding the kind of connected mobile equipment available to field teams.

Government and Public Administration are rising faster because public bodies are investing in digital workforce systems, integrated processes, and stronger service execution. SAP’s January 2026 deployment for the National Center for Non-Profit Sector Development showed that large public-sector workforce management programs are already moving on integrated enterprise platforms. Industrial manufacturing, transportation and logistics, healthcare and life sciences, hospitality, and retail also contribute to the Saudi Arabia frontline worker technology market as they digitize shift operations, coordination, and field compliance. The Saudi Arabia frontline worker technology industry is therefore broadening beyond its original construction and energy base, even though those sectors still shape current demand.

Geography Analysis

The Saudi Arabia frontline worker technology market is geographically concentrated in areas of the Kingdom where industrial density, project scale, and institutional demand are strongest. The Eastern Province remains the most established adoption cluster because it combines oil and gas operations, industrial infrastructure, and a large frontline labor base. Honeywell expanded its Dhahran facility in October 2025 with a production line for frontline-worker handheld computers, which supports the region’s role as a practical hardware base for connected field operations. The region also aligns well with Saudi Aramco’s cybersecurity compliance framework, which influences vendor readiness for connected solutions in critical industrial settings. This makes the Eastern Province especially important for software, rugged mobility, connected safety, and the adoption of industrial workflows.

Riyadh is emerging as the main center for administrative digitization, enterprise workforce systems, and national compliance workflows within the Saudi Arabia frontline worker technology market. The Ministry of Human Resources and Social Development has set the policy direction for workplace safety and formal safety management, which gives the capital a central role in shaping adoption priorities. Public-sector platform deployments also support Riyadh’s role, as seen in SAP’s January 2026 implementation for the National Center for Non-Profit Sector Development. Vendors that want to scale in the Saudi Arabia frontline worker technology market, therefore, need a strong fit with both field operations and policy-driven process requirements centered in Riyadh.

The Tabuk region, led by NEOM activity, has become one of the most technology-intensive work environments in the Kingdom, even though buyer requirements there are still evolving across project phases. That makes it an important proving ground for digital permits, connected worker tools, site communication, and live monitoring across large and remote worksites. Jeddah and its nearby economic zones add another layer of demand through logistics, hospitality, commercial services, and urban infrastructure. Together, these regional differences mean the Saudi Arabia frontline worker technology market does not expand evenly, because adoption depth depends on how closely each area is tied to industrial operations, public digitization, or large-scale development programs.

Competitive Landscape

The Saudi Arabia frontline worker technology market is moderately fragmented, with global software vendors, rugged hardware providers, wearable specialists, and localizing service partners competing across overlapping use cases. No single vendor type defines the market, because buyer demand spans safety, communication, mobility, analytics, compliance, and workflow execution. Large international suppliers still hold an advantage in enterprise credibility, product breadth, and prior relationships with industrial customers. At the same time, local fit has become more important, which is why the Saudi Arabia frontline worker technology market increasingly rewards Arabic support, in-Kingdom hosting, and alignment with local procurement and compliance expectations. This combination keeps the competitive field open even when large global brands remain visible.

One clear strategic pattern is the expansion of local presence. Cority launched its Saudi Arabia operations in January 2026 and positioned the country as its MENA regional headquarters, with Google Cloud hosting inside the Kingdom to support local deployment expectations. Another pattern is local manufacturing and field-device readiness, as Honeywell added handheld computer production in Dhahran in October 2025 to support frontline operations more directly from within Saudi Arabia. These moves matter because they reduce the distance between product supply, support capability, and customer requirements in the Saudi Arabia frontline worker technology market.

A third pattern is product convergence around fewer but smarter devices and tighter platform integration. Blackline Safety introduced the G8 wearable in January 2026, combining gas detection, lone worker protection, and communication in a single device, reflecting demand for broader functionality in a smaller field kit. Qualcomm and Aramco Digital’s 2025 collaboration on an AI-enabled industrial 5G smartphone points in the same direction, with field hardware designed for connected industrial work rather than general-purpose mobile use. Motorola Solutions also expanded its AI-powered safety and security capabilities in early 2026, adding to the broader push toward more intelligent and integrated frontline environments. The Saudi Arabia frontline worker technology market still offers room for more localized compliance tools, simpler SME-focused products, and stronger interoperability across mixed vendor stacks.

Saudi Arabia Frontline Worker Technology Industry Leaders

Blackline Safety Corp.

Honeywell International Inc.

Motorola Solutions, Inc.

SoloProtect Ltd.

Everbridge, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Cority launched its Saudi Arabia operations as its MENA regional headquarters, with cloud hosting on Google Cloud within the Kingdom and AI-powered EHS capabilities aligned to giga-project compliance demands.

- January 2026: Motorola Solutions showcased expanded AI-powered safety and security solutions at Intersec Dubai, demonstrating visual alert systems designed for oil and gas, construction, and healthcare sectors in the Middle East.

- January 2026: Blackline Safety launched the G8 wearable safety device, combining gas detection, lone worker protection, and radio-quality communication in a single rugged platform, with first shipments initiated in February 2026.

- January 2026: Saudi Arabia's National Center for Non-Profit Sector Development completed one of the fastest ERP implementations in the Saudi public sector, deploying SAP S/4HANA and SAP SuccessFactors and processing more than 22,000 employee requests through fully automated workforce management systems.

Saudi Arabia Frontline Worker Technology Market Report Scope

The Saudi Arabia frontline worker technology market encompasses the ecosystem of software and services designed to empower non-desk employees who primarily execute their duties away from a traditional office setting. This includes tools that facilitate employee communication, task management, scheduling, knowledge sharing, and performance tracking across sectors such as retail, manufacturing, healthcare, and logistics. The market features cloud-based, on-premises, and hybrid deployment models tailored to the operational and digital transformation needs of organizations of varying sizes, aiming to improve operational efficiency, safety compliance, and real-time decision-making at the edge of business operations within Saudi Arabia.

The Saudi Arabia Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises. and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for Saudi Arabia frontline worker technology?

The Saudi Arabia frontline worker technology market was estimated at USD 230 million in 2026 and is forecast to reach USD 700 million by 2031, growing at a 24.93% CAGR.

Which component contributes the most revenue in this space?

Software led the market with a 79.11% share in 2025 because buyers prioritize platforms for compliance, task execution, communication, and audit trails.

Why is cloud deployment growing so quickly in Saudi frontline operations?

Cloud-based deployment held 74.61% share in 2025 and is projected to grow at a 27.33% CAGR because large and remote worksites need centralized access, updates, and scalable control.

Which buyer group is creating the fastest expansion opportunity?

Small and medium enterprises are projected to grow at a 28.89% CAGR through 2031 as subcontractors adopt digital tools to remain eligible for larger project ecosystems.

Which application area is expanding the fastest?

Safety and Compliance Management is projected to grow at a 29.41% CAGR through 2031 because regulatory requirements and enterprise audit needs are becoming more formal and more digital.

Which end-user segment is rising fastest in Saudi Arabia?

Government and Public Administration is projected to post the highest CAGR of 31.66% through 2031, while construction remained the largest end-user segment in 2025 with 28.11% share.

Page last updated on: