Saudi Arabia Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

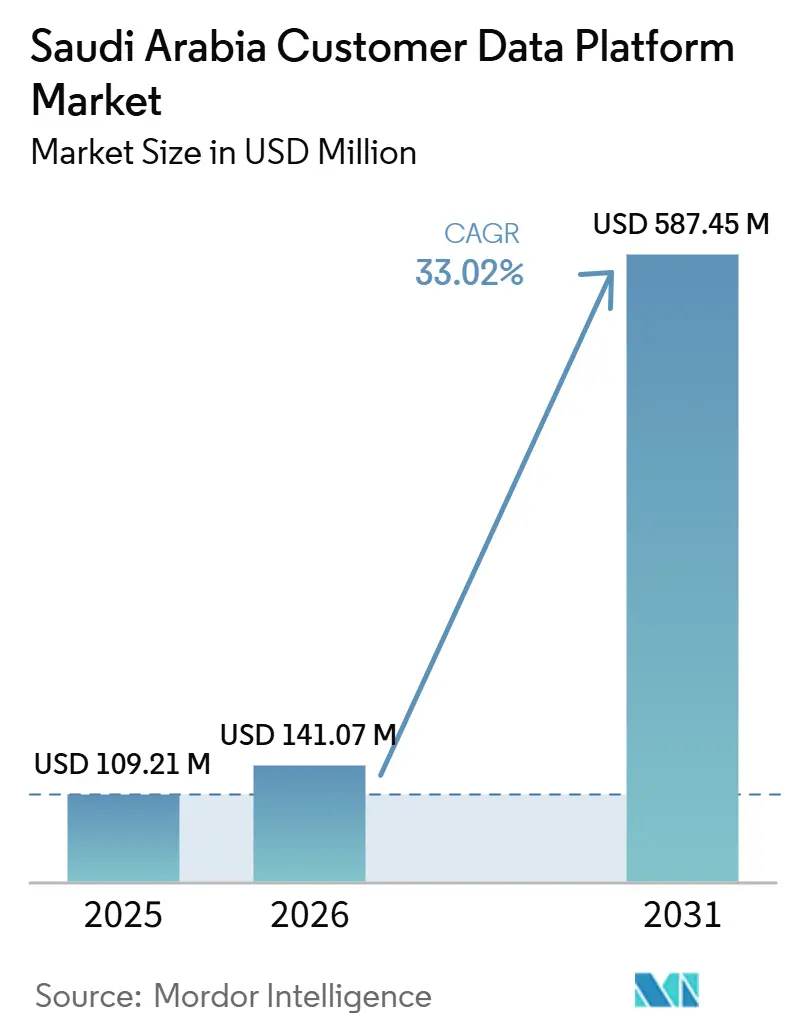

| Base Year Market Size (2025) | USD 109.21 Million |

| Market Size (2026) | USD 141.07 Million |

| Market Size (2031) | USD 587.45 Million |

| Growth Rate (2026 - 2031) | 33.02% CAGR |

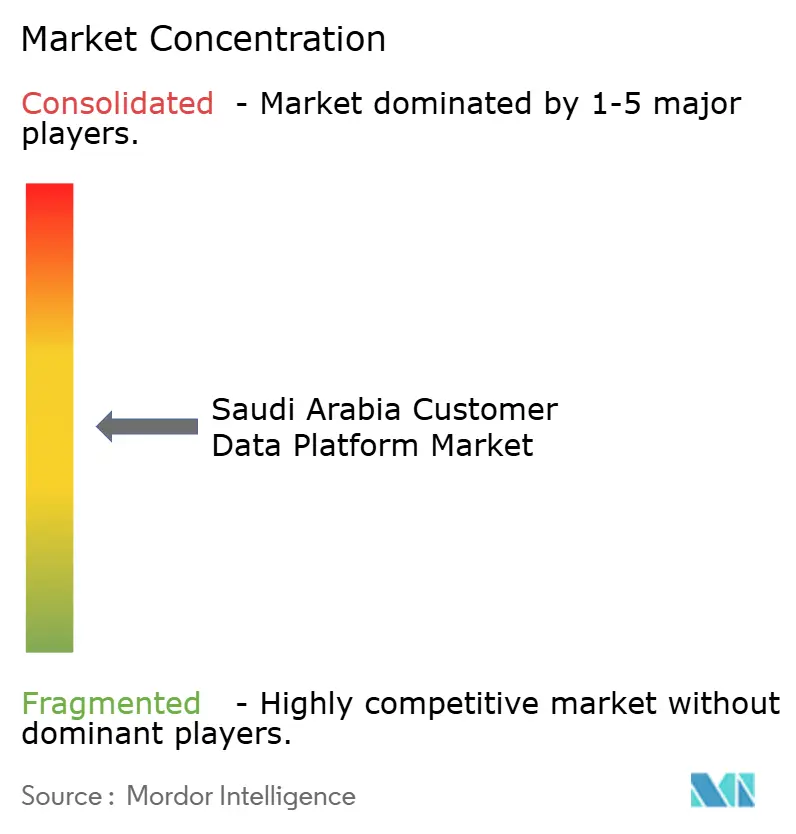

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Customer Data Platform Market Analysis by Mordor Intelligence

The Saudi Arabia customer data platform market size was valued at USD 109.21 million in 2025 and estimated to grow from USD 141.07 million in 2026 to reach USD 587.45 million by 2031, at a CAGR of 33.02% during the forecast period 2026-2031. The Saudi Arabia customer data platform market is advancing as enterprise buyers face three linked pressures: stricter personal data rules, broader cloud adoption, and a reduced reliance on third-party tracking for customer acquisition. Demand is also rising because enterprises are no longer treating customer data unification as a limited marketing tool; they are now using it as a shared layer for compliance, personalization, analytics, and customer journey management across business functions. Vendor strategy in the Saudi Arabia customer data platform market is becoming more localized, as global platforms are building in-country support capacity, aligning more closely with sovereign data expectations, and positioning their products as enterprise infrastructure rather than optional software overlays. The next stage of expansion is likely to depend less on awareness and more on implementation depth, because buyers already understand the use case and now need systems that can connect older records, support consent controls, and activate data in real time. That mix keeps the Saudi Arabia customer data platform market in a rapid buildout phase, where purchasing decisions are increasingly shaped by execution readiness, regulatory fit, and the ability to show commercial value from unified customer records.

Key Report Takeaways

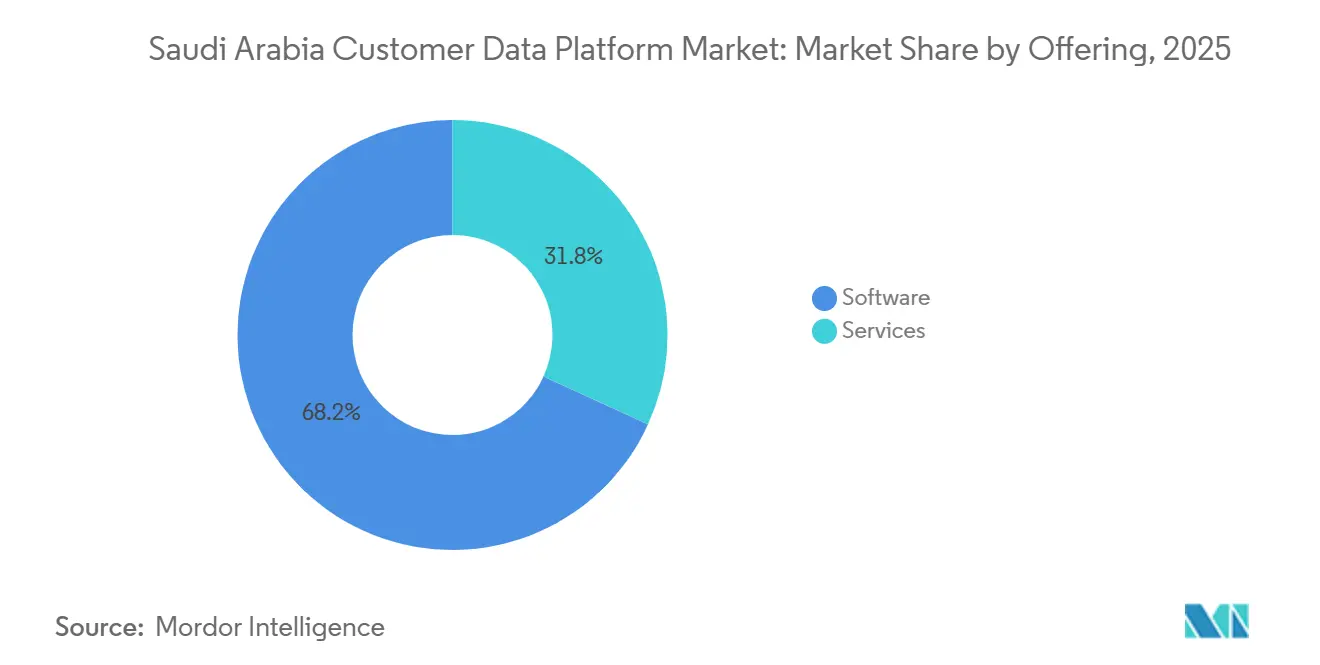

- By offering, software held 68.19% of the Saudi Arabia customer data platform market share in 2025, while services are projected to expand at a 35.92% CAGR through 2031.

- By deployment mode, cloud accounted for 64.13% of the Saudi Arabia customer data platform market size in 2025 and is projected to advance at a 34.97% CAGR through 2031.

- By organization size, large enterprises held 71.23% of the Saudi Arabia customer data platform market share in 2025, while SMEs are projected to record the highest CAGR at 35.41% through 2031.

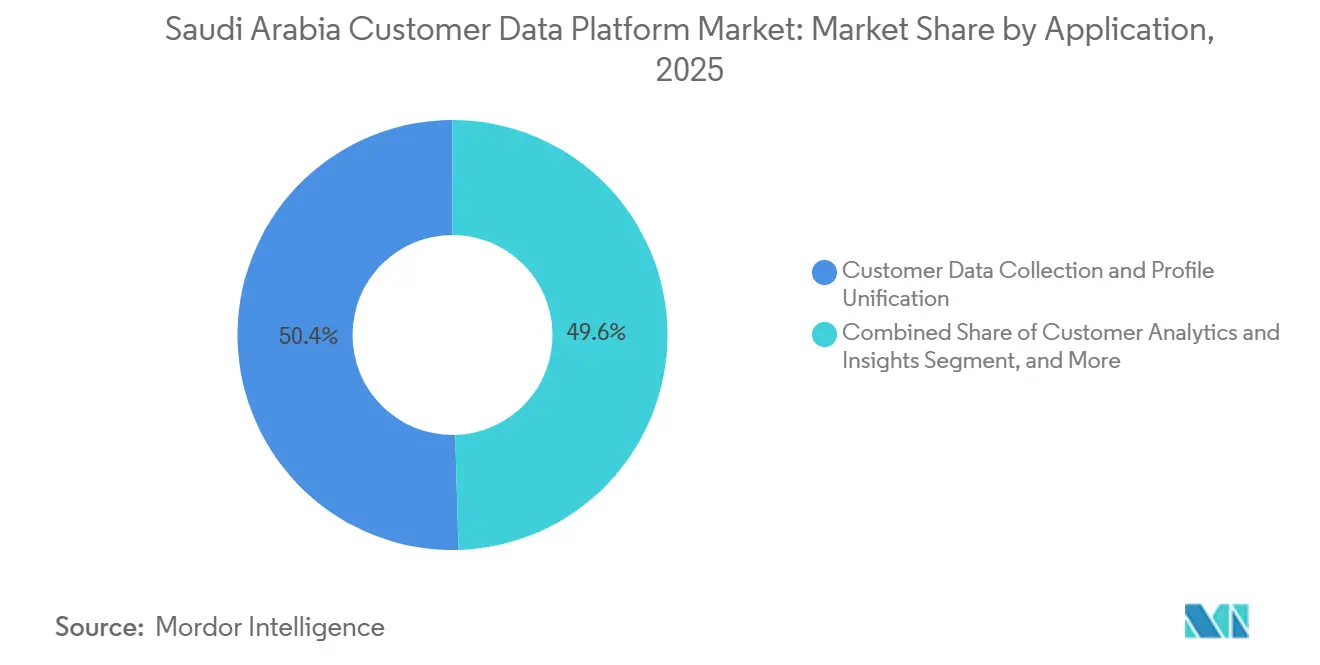

- By application, customer data collection and profile unification accounted for 50.44% of the Saudi Arabia customer data platform market share in 2025, while audience segmentation and personalization are projected to grow at a 34.68% CAGR through 2031.

- By end-user industry, retail and e-commerce held 29.14% share in 2025, while BFSI is projected to expand at a 34.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital Commerce and Omnichannel Customer Journeys | +8.2% | National, with early gains in Riyadh, Jeddah, and Dammam | Short term (≤ 2 years) |

| PDPL-Driven Consent and Data Governance Requirements | +7.1% | National | Short term (≤ 2 years) |

| Vision 2030 Led Enterprise Cloud Modernization | +6.3% | National, with spill-over to GCC peers | Medium term (2-4 years) |

| First-Party Data Priority as Third-Party Cookies Decline | +4.8% | Global, with concentrated impact on Saudi digital commerce | Medium term (2-4 years) |

| Real-Time Identity Resolution for Telecom Subscriber Monetization | +3.2% | National, concentrated in stc, Zain KSA, and Mobily subscriber bases | Medium term (2-4 years) |

| Composable CDPs Lowering Data Movement and Storage Costs | +2.1% | Global, relevant to Saudi enterprise data teams | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Commerce and Omnichannel Customer Journeys

Saudi e-commerce spending reached USD 27.96 billion in 2025, which means brands now manage a much larger volume of customer interactions across marketplaces, social channels, apps, websites, and physical locations than they did only a few years earlier. Smartphone penetration exceeded 98%, and national 5G coverage reached 78%, supporting near-constant consumer connectivity and creating a steady flow of event data that enterprises need to unify before it can be used effectively. In that setting, the Saudi Arabia customer data platform market benefits because retailers, travel operators, and consumer brands cannot rely on separate campaign tools or isolated channel reports when customer behavior spans storefronts, messaging apps, and checkout systems within the same journey. The operational issue is not simply data volume; it is the cost of acting on partial records, because fragmented profiles weaken targeting, limit attribution, and reduce the value of media spending, which is already rising across digital commerce environments. This is why the Saudi Arabia customer data platform market continues to attract enterprise spending as enterprises seek a cleaner link between customer acquisition, retention, and measurable commercial outcomes.

PDPL-Driven Consent and Data Governance Requirements

The Personal Data Protection Law has changed technology priorities in Saudi Arabia, as consent capture, storage, use controls, and audit readiness now sit closer to core enterprise systems than before. The Saudi Arabia customer data platform market is benefiting from that shift because a CDP can serve as a practical layer for managing customer permissions, profile history, and activation rules in a single place rather than across disconnected systems. This matters for enterprise buyers because compliance work becomes more difficult when customer information moves across CRM, loyalty, e-commerce, and service platforms without a unified view of what the customer has authorized. PDPL requirements also support demand for tools that document data flows, separate identity resolution from activation rights, and help internal teams prove that customer data is being processed within approved boundaries. As a result, the Saudi Arabia customer data platform market is supported not only by revenue goals but also by the need for defensible governance practices that can withstand internal review and formal oversight.

Vision 2030 Led Enterprise Cloud Modernization

Cloud modernization under Vision 2030 has created an environment where the Saudi Arabia customer data platform market can scale faster because the surrounding architecture is becoming more compatible with real-time data tools. A SAP and YouGov survey released at LEAP 2025 found that 75% of Saudi enterprises had already moved core business processes to the cloud, while another 22% planned to migrate within 15 months, which sharply expands the install base for cloud-delivered customer data applications. Oracle reinforced that trend with a USD 14 billion commitment to Saudi cloud and AI infrastructure in May 2025, and Salesforce later operationalized its USD 500 million commitment through a Riyadh regional headquarters, which shows that major vendors are matching demand with local execution capacity. These moves matter because CDP projects depend on scalable compute, API access, and better cloud connectivity across marketing, commerce, service, and analytics systems, all of which become easier to support as enterprise cloud maturity improves. The Saudi Arabia customer data platform market, therefore, sits within a broader infrastructure cycle where software selection, implementation economics, and vendor support models are improving together rather than in isolation.

First-Party Data Priority as Third-Party Cookies Decline

The decline of third-party tracking is pushing Saudi enterprises to treat consented first-party data as a long-term operating asset rather than a campaign input housed within a single business unit. That change favors the Saudi Arabia customer data platform market because CDPs are designed to collect, unify, govern, and activate first-party records across multiple systems without losing control of identity and permissions. The shift is especially important in a market where commerce is digital, mobile use is widespread, and customer journeys often move across brand websites, social channels, marketplaces, and offline touchpoints within a short time window. Once third-party identifiers weaken, the value of owned customer history rises, and the commercial gap between enterprises with strong consented data foundations and those without them widens. This keeps the Saudi Arabia customer data platform market closely tied to broader enterprise efforts to improve data quality, make audience building more dependable, and reduce wasted spend caused by incomplete customer context.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity across Legacy CRM, ERP, and Loyalty Stacks | -3.2% | National, concentrated in large enterprise and government verticals | Short term (≤ 2 years) |

| Data Residency and Cross-Border Transfer Constraints | -2.4% | National, with heightened impact for multinationals operating in Saudi Arabia | Medium term (2-4 years) |

| Shortage of CDP and Reverse-ETL Talent | -1.6% | National, APAC spill-over | Medium term (2-4 years) |

| Vendor Lock-In Concerns in Large-Scale Enterprise Deployments | -1.0% | Global, concentrated in Saudi large enterprise segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across Legacy CRM, ERP, and Loyalty Stacks

Integration remains a real brake on the Saudi Arabia customer data platform market because many large organizations still operate older enterprise systems that were not built for unified, real-time customer data flows. SAP and YouGov found that 42% of Saudi enterprises viewed integration with existing systems as a primary AI and data implementation challenge, a finding that reflects the same kind of friction CDP projects face when they try to connect source systems with different identifiers and inconsistent data logic. The problem becomes harder when loyalty databases, service applications, and transactional systems were deployed at different times and were never designed to maintain one persistent customer profile across departments. It also slows early returns, because a project may spend its first phase cleaning data and aligning records before marketing or service teams can use the platform meaningfully. For the Saudi Arabia customer data platform market, this means growth remains strong, but execution quality and systems integration capacity still decide how quickly value can be realized after purchase.

Data Residency and Cross-Border Transfer Constraints

Data residency rules create another restraint because multinational vendors and multinational buyers often need to adapt standard deployment models before they can move customer information across borders or store it outside the Kingdom.[1]Saudi Data and Artificial Intelligence Authority, “Personal Data Protection Law,” National Data Governance Platform, sdaia.gov.sa The Saudi Arabia customer data platform market is therefore shaped not only by product capability, but also by where data is hosted, how transfers are documented, and whether legal and technical teams can approve the final architecture. That gives an advantage to vendors that have already committed capital to local infrastructure and in-country delivery, because they can reduce uncertainty during procurement and shorten compliance review cycles. The same issue can delay adoption for enterprises that operate across the GCC and want one customer data layer across markets, since legal requirements do not always align neatly from one jurisdiction to another. This keeps architecture decisions in the Saudi Arabia customer data platform market closely tied to sovereignty, governance, and vendor footprint rather than solely to product features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads While Services Deepens Delivery Needs

Software held 68.19% of the market in 2025, while services are projected to grow at a 35.92% CAGR through 2031, which shows that platform licensing still anchors spending even as implementation work rises quickly. In the early stages of enterprise adoption, buyers often start with the core platform because they first need a stable way to ingest data, manage identities, and connect customer records across operational systems. That pattern supports a strong software base in the Saudi Arabia customer data platform market, since the initial buying decision often centers on integration breadth, governance functions, audience management, and compatibility with the wider enterprise stack. The leading position of software also reflects the fact that many enterprises want a central system of record for customer profiles before they expand into more advanced orchestration and activation workflows. Once that base is selected, procurement often moves to implementation planning, partner support, and managed delivery, which then pulls the services layer into a larger role.

Services are expanding faster because many buyers need outside help mapping data sources, defining consent logic, configuring connectors, and training business teams that will rely on the platform after launch. SAP and YouGov reported that 47% of Saudi enterprises identified a lack of skilled personnel as a key AI and data implementation challenge, which helps explain why managed support and systems integration are becoming more important in live customer data projects. Services demand in the Saudi Arabia customer data platform industry is also strengthened by the need for Arabic-language enablement, consent mapping, and deployment designs that fit PDPL expectations without delaying business use cases. Salesforce added another signal when it said it plans to upskill 30,000 Saudi citizens in AI by 2030, because a stronger local talent base would gradually support more in-country delivery and reduce dependence on imported specialist support over time. The result is a segment structure where software maintains the largest revenue base, but services capture a greater share of the execution burden as deployments move from evaluation to operational use across the Saudi Arabia customer data platform market.

By Deployment Mode: Cloud Anchors Demand While Hybrid Stays Relevant

Cloud captured 64.13% of the market in 2025 and is projected to grow at a 34.97% CAGR through 2031, indicating that the current largest share of demand is also the fastest-growing part of future demand. This pattern is logical because customer data platforms work best when enterprises have elastic compute, broad API connectivity, and easier access to surrounding systems for ingestion, analytics, and activation. The Saudi Arabia customer data platform market has therefore aligned strongly with the wider national cloud cycle, where enterprise migration is no longer limited to experimentation and is now part of operating model change. SAP and YouGov found that 75% of Saudi enterprises had already moved core processes to the cloud, and another 22% planned to migrate within 15 months, supporting a broad deployment base for cloud CDP tools. Oracle and Salesforce have also expanded their local presence, reducing implementation friction for buyers who want enterprise-grade cloud services delivered with stronger in-country support.

Hybrid still holds strategic relevance because some regulated workloads cannot move as freely as less sensitive marketing or analytics processes, even when organizations want a unified customer layer. In practice, this means enterprises may keep some records or processing activities closer to local or private environments while using cloud layers for orchestration, segmentation, and activation. The Saudi Arabia customer data platform market supports that balance because buyers do not always choose between full cloud and full on-premises, but instead seek architectures that meet sovereignty requirements without sacrificing speed. Data transfer and hosting obligations under Saudi data governance rules make this especially important for banking, healthcare, the public sector, and other tightly governed environments. That is why cloud leads, but hybrid remains meaningful as enterprises try to balance scalability with tighter control over sensitive customer information.

By Organization Size: Large Enterprises Lead While SMEs Expand the Base

Large enterprises held 71.23% of the market in 2025, while SMEs are projected to grow at a 35.41% CAGR through 2031, indicating that current spending remains concentrated at the top even as the next wave broadens the buyer pool. Large organizations naturally lead because they manage higher data volumes, more channels, more business units, and stronger compliance exposure, which makes the need for unified customer records easier to justify. They also have larger budgets and a greater ability to absorb multistage implementation work, which matters in a market where integration quality still affects time to value. In the Saudi Arabia customer data platform market, large enterprises lead across financial services, telecom, retail, and large diversified private groups with many brands and operating entities. Their demand is also reinforced by internal pressure to connect the marketing, commerce, service, and analytics teams around a single, governed customer view rather than separate local databases.

SMEs are growing faster because SaaS delivery has lowered the minimum cost and reduced the operational burden that once made CDP adoption harder for smaller teams. The Saudi Arabia customer data platform market is seeing this shift as mid-sized companies improve their digital channels, invest more in owned customer relationships, and seek packaged deployments that do not require a large in-house engineering bench. This is especially relevant in business groups where several smaller brands or operating units want one practical view of the customer without building an enterprise-scale architecture from the ground up. Vendors are likely to respond with simpler onboarding models, shorter implementation programs, and more prescriptive use cases that help SMEs reach value faster. That keeps the market’s long-term expansion tied not only to large enterprise upgrades but also to the widening accessibility of customer data tools for smaller Saudi businesses seeking to improve retention, conversion, and cross-brand visibility.

By Application: Profile Unification Holds Scale While Personalization Builds Faster

Customer data collection and profile unification accounted for 50.44% of the market in 2025, while audience segmentation and personalization are projected to grow at a 34.68% CAGR through 2031, which shows a clear difference between the foundational layer and the fastest-expanding commercial use case. The large share of profile unification reflects the simple fact that no downstream workflow works properly until the enterprise can recognize the same customer across systems, channels, and transaction histories. That is why this application still anchors the Saudi Arabia customer data platform market, even when buyers talk more publicly about AI, campaign optimization, or real-time personalization. A unified record remains the starting point for consent controls, analytics, orchestration, and service interactions, so enterprises continue to fund this layer first before they scale more visible use cases. The opening phase of many projects, therefore, centers on data ingestion, identifier cleanup, and profile governance rather than immediate campaign activation.

Audience segmentation and personalization are growing faster because once a reliable profile base is established, business teams can finally use data more directly and measurably across acquisition, retention, loyalty, and service workflows. PDPL makes this more important because enterprises need a clearer line between what a customer has agreed to and how that information can be used for targeting or journey design. Marketing campaign orchestration, analytics, and consent management continue to hold significant market share, but their expansion is closely linked to the maturity of the unification layer beneath them. The Saudi Arabia customer data platform market size for customer data collection and profile unification remained the largest application base in 2025, while the fastest pace now sits with personalization-focused workflows that can turn governed data into direct commercial actions. This creates a market structure where foundational data work still accounts for a large share of spending, but value perception increasingly comes from the business use cases that sit on top of that core layer.

By End-User Industry: Retail Holds the Largest Base While BFSI Grows Fastest

Retail and e-commerce held 29.14% of the market in 2025, while BFSI is projected to expand at a 34.29% CAGR through 2031, creating a clear split between the segment with the broadest installed base and the one with the strongest forward momentum. Retail led because Saudi Arabia’s digital commerce activity is already large, customer journeys are highly channel-driven, and brands need cleaner identity resolution across storefronts, marketplaces, mobile apps, social platforms, and loyalty systems.[2]U.S. International Trade Administration, “Saudi Arabia - eCommerce,” U.S. Department of Commerce, trade.gov Smartphone penetration above 98% and 5G coverage at 78% add to that pattern because shoppers generate frequent behavioral signals that can be captured, linked, and activated when the data architecture is strong enough. The Saudi Arabia customer data platform market, therefore, finds a natural base in retail, where conversion, repeat purchase, and omnichannel measurement are closely tied to customer profile quality. Travel, leisure, and consumer-facing service categories connected to the retail ecosystem also support this demand because they rely on many of the same cross-channel engagement practices.

BFSI is advancing fastest because banks and financial institutions are modernizing customer engagement while strengthening data governance, service quality, and personalization. Finastra reported in 2026 that 93% of Saudi financial institutions planned to increase spending on customer experience and personalization, while 87% planned broader modernization investments, pointing to a strong near-term demand outlook for customer data tools. Healthcare and life sciences, information technology and telecom, media and entertainment, industrial manufacturing, and government and public administration continue to make up the remaining addressable base. Telecom remains particularly relevant because subscriber-scale data environments create a strong use case for real-time identity resolution, offer management, and service personalization when enterprise systems can process live events well. The Saudi Arabia customer data platform market share remains highest in retail today, but its next major concentration of strategic investment is likely to come from BFSI as modernization and customer experience programs move deeper into execution.

Geography Analysis

Demand in the Saudi Arabia customer data platform market is concentrated first in Riyadh, then in Jeddah and the Eastern Province, because those locations carry the largest mix of enterprise headquarters, regulated institutions, large consumer brands, and complex service operations. Riyadh leads because it combines government presence, financial decision-making, major corporate offices, and a high density of enterprise technology spending that naturally supports earlier CDP adoption. Jeddah shows a different demand pattern, as retail, tourism, hospitality, and leisure activities create a stronger need for cross-channel customer visibility and more consistent personalization across physical and digital touchpoints. The Eastern Province adds a more operational profile, where large industrial and energy-linked organizations can apply customer data tools to B2B relationship management, service workflows, and partner-facing analytics. This city-level pattern does not change the national nature of the market, but it does shape where pilots start, where partner ecosystems grow fastest, and where vendors can build the strongest commercial references.

The infrastructure picture supports wider geographic adoption because the country already has high digital readiness for real-time customer engagement use cases. Smartphone penetration exceeded 98%, and 5G coverage reached 78%, enabling cloud-connected platforms to process behavioral signals and support live activation across the main urban centers. The Saudi Arabia customer data platform market, therefore, benefits from a strong digital base that supports omnichannel business models rather than simple web or app interactions. As enterprises outside the largest commercial hubs continue to digitize, demand is likely to shift from headquarters-led deployments toward broader national rollouts.

Within the GCC, Saudi Arabia stands out because it combines large domestic scale, strong compliance pressure, and a deeper current wave of cloud and AI investment than nearby markets. Oracle committed USD 14 billion to Saudi cloud and AI infrastructure, and Salesforce operationalized its USD 500 million national commitment through a Riyadh regional base, which underlines how vendor capital is being directed specifically toward the Kingdom rather than treated as a general regional allocation.[3]Oracle, “Oracle's Commitment to Saudi Arabia and President Trump's Vision for Global Prosperity,” Oracle, oracle.com That combination keeps Saudi Arabia at the center of regional reference demand, because large enterprises expanding across the GCC are likely to make architecture decisions in the Kingdom first and then adapt those choices to adjacent markets. The Saudi Arabia customer data platform market is, therefore, not only the main domestic opportunity in this field, but also the regional benchmark for how governed, cloud-linked customer data systems are likely to be deployed across the wider Gulf.

Competitive Landscape

The competitive structure of the Saudi Arabia customer data platform market shows a stronger top tier and a broader specialist layer beneath it. Large suite vendors such as Salesforce, Adobe, Oracle, and SAP hold an advantage with major enterprises because they can combine customer data functions with adjacent applications in marketing, commerce, service, ERP, and analytics. That positioning matters in Saudi Arabia because many buyers prefer platforms that integrate with existing enterprise software environments rather than adding another isolated point solution. At the same time, the market is not closed, as specialists such as Tealium, Twilio Segment, Bloomreach, Amperity, mParticle, and Treasure Data continue to compete on flexibility, real-time activation, composable design, and identity depth. This keeps the Saudi Arabia customer data platform market moderately concentrated at the top, but still open enough for focused vendors that can better address clear implementation or architecture gaps than the broad suites.

Recent strategy moves show how vendors are trying to sharpen those positions in practical ways. Oracle announced role-based AI agents inside Oracle Fusion Cloud CX in February 2026, built on Oracle Unity Data Platform profiles, which strengthened its message around unified data and embedded activation across marketing, sales, and service. Salesforce had already reinforced its local commitment in November 2025 by opening a Riyadh regional headquarters, which supported in-country delivery, partner growth, and product relevance for Saudi enterprise buyers.[4]Salesforce, “Salesforce Saudi Arabia Launches, Operationalizing USD 500 Million Commitment to Kingdom's Digital Transformation,” Salesforce, salesforce.com SAP also added weight to the local compliance argument when it made SAP Business Technology Platform available on Google Cloud in Saudi Arabia for regulated customers, providing SAP-linked enterprises with a more practical route for sovereign deployment planning. These moves matter because buyers are not only comparing product features; they are also comparing vendor readiness in terms of sovereignty, support, adjacent integration, and the speed at which value can be delivered after purchase.

Specialists are responding by connecting more directly to warehouse, AI, and activation workflows rather than trying to outmatch the suite vendors on breadth alone. Twilio Segment released Advanced Audiences features in April 2026, which helped marketers build warehouse-native audiences with less dependence on data teams and made the platform more relevant in talent-constrained deployment settings. Bloomreach deepened its Databricks partnership in June 2026, reflecting the wider push toward AI-driven activation built on unified customer data rather than separate campaign systems. In the Saudi Arabia customer data platform market, vendor competition is increasingly defined by three tests: local compliance credibility, ease of integration with the existing stack, and the ability to turn customer data into live action without forcing enterprises into slow, resource-heavy operating models.

Saudi Arabia Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Bloomreach deepened its partnership with Databricks as a launch partner for Databricks CustomerLake, an agentic CDP that extends Bloomreach's Loomi AI personalization engine across email, the web, and other engagement channels, using unified data from the Databricks platform.

- April 2026: Twilio Segment released Advanced Audiences features in its Linked Audiences product, enabling marketers to build warehouse-native audiences and activate them without manual requests from the data team, reducing the 15-to-30-hour weekly data team burden for audience management.

- February 2025: Oracle announced new role-based AI agents embedded within Oracle Fusion Cloud CX for marketing, sales, and service workflows, built on Oracle Unity Data Platform's unified customer profiles to drive personalization at scale.

- November 2025: Salesforce formally operationalized its USD 500 million Saudi Arabia commitment by establishing a regional headquarters in Riyadh, showcasing CDP and Agentforce deployments at Red Sea Global, Almosafer, and Cenomi on its inaugural Innovation Day.

Saudi Arabia Customer Data Platform Market Report Scope

The Saudi Arabia Customer Data Platform Market comprises software platforms and services that enable organizations to collect, integrate, manage, and activate customer data across multiple channels and business systems. These platforms support advanced customer segmentation, campaign optimization, personalization, consent management, and customer analytics. The Kingdom's digital transformation programs, expanding e-commerce ecosystem, and growing adoption of customer-centric business strategies support the market. CDPs help enterprises deliver personalized customer experiences while improving marketing efficiency and customer retention.

The Saudi Arabia Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the Saudi Arabia customer data platform market?

The Saudi Arabia customer data platform market was valued at USD 109.21 million in 2025, stands at USD 141.07 million in 2026, and is forecast to reach USD 587.45 million by 2031 at a 33.02% CAGR.

Which deployment model leads customer data platform adoption in Saudi Arabia?

Cloud leads with 64.13% share in 2025 and is also the fastest-growing deployment mode, with a projected 34.97% CAGR through 2031.

Which end-user sector drives the largest demand in Saudi Arabia?

Retail and e-commerce held the largest share at 29.14% in 2025 because omnichannel commerce creates heavy demand for profile unification and activation.

Why is BFSI becoming important for customer data platform vendors in Saudi Arabia?

BFSI is projected to grow at a 34.29% CAGR through 2031, supported by rising spending on customer experience, personalization, and broader modernization programs.

What is the main regulatory factor shaping platform adoption in Saudi Arabia?

PDPL is the central regulatory driver because it makes consent management, audit readiness, and governed customer data usage more important in enterprise system design.

What is the biggest execution challenge for customer data platform projects in Saudi Arabia?

Integration remains the biggest challenge because older CRM, ERP, and loyalty systems often hold fragmented identifiers and slow the creation of unified customer profiles.

Page last updated on: