Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

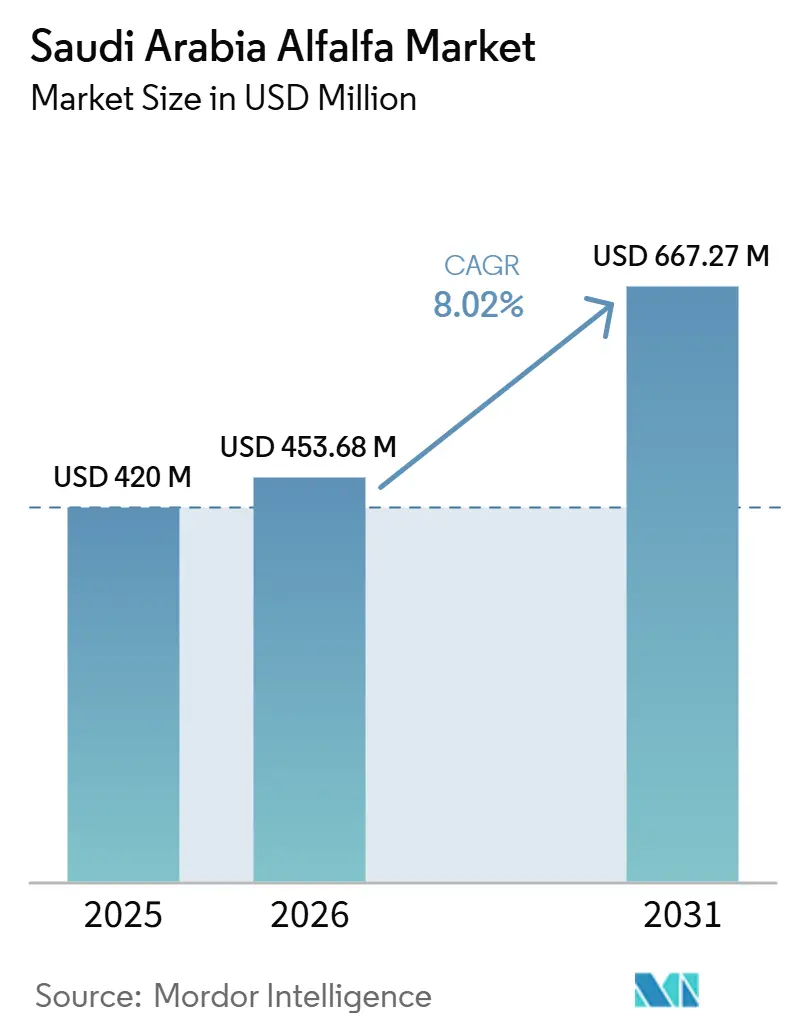

| Base Year Market Size (2025) | USD 420 Million |

| Market Size (2026) | USD 453.68 Million |

| Market Size (2031) | USD 667.27 Million |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Alfalfa Market Analysis by Mordor Intelligence

The Saudi Arabia alfalfa market was valued at USD 420 million in 2025 and is forecast to grow from USD 453.68 million in 2026 to USD 667.27 million by 2031, at a CAGR of 8.02% during the forecast period from 2026 to 2031. The phaseout of perennial forage cultivation by the Ministry of Environment, Water and Agriculture has made import dependence a structural feature of the market, as large operators no longer have a viable domestic alternative for commercial-scale forage supply. Import subsidies for alfalfa hay and pellets continue to support purchase economics for dairy farms and feed processors, allowing the market to absorb supplier shifts without a sharp demand reset. Demand remains anchored in industrial dairy systems, while rising camel and equine feed demand is broadening the premium forage base and supporting product diversification. Competition in the market is increasingly shaped by origin diversification, contract security, product specifications, and delivery reliability rather than price alone, as buyers place high value on supply continuity and nutritional consistency. Freight disruption risk in 2026 has also strengthened the case for multi-origin sourcing, flexible port routing, and tighter inventory planning across the market.

Key Report Takeaways

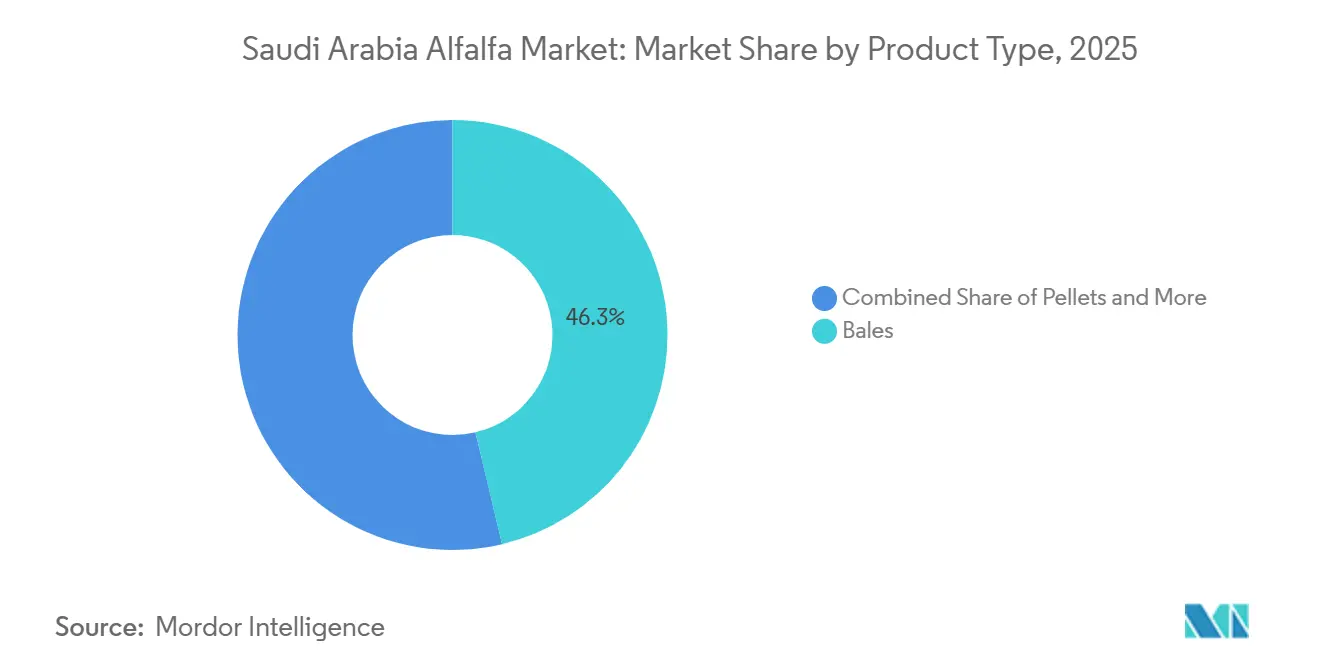

- By product type, bales were the largest segment and held 46.3% of the market share in 2025, while pellets are the fastest growing segment and are anticipated to expand at a 10.3% CAGR between 2026 and 2031.

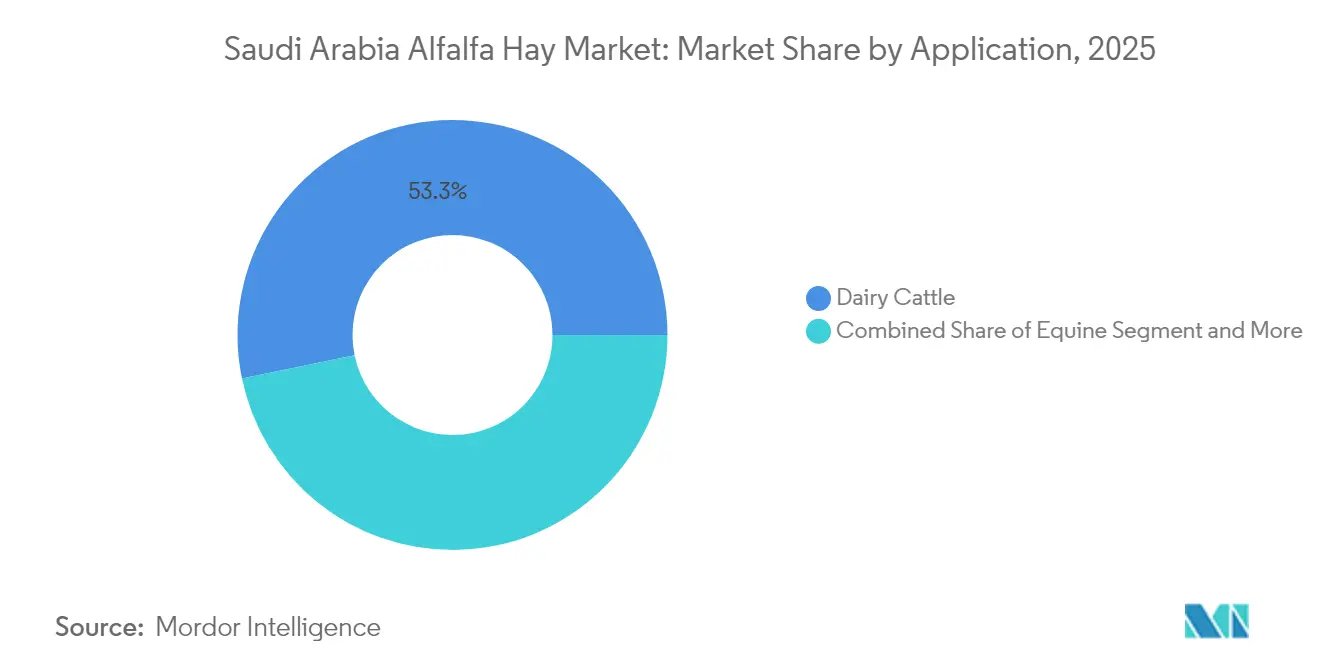

- By application, dairy cattle feed was the largest segment and accounted for 53.2% of the market size in 2025, while equine feed is the fastest growing segment and is anticipated to expand at an 10.0% CAGR between 2026 and 2031.

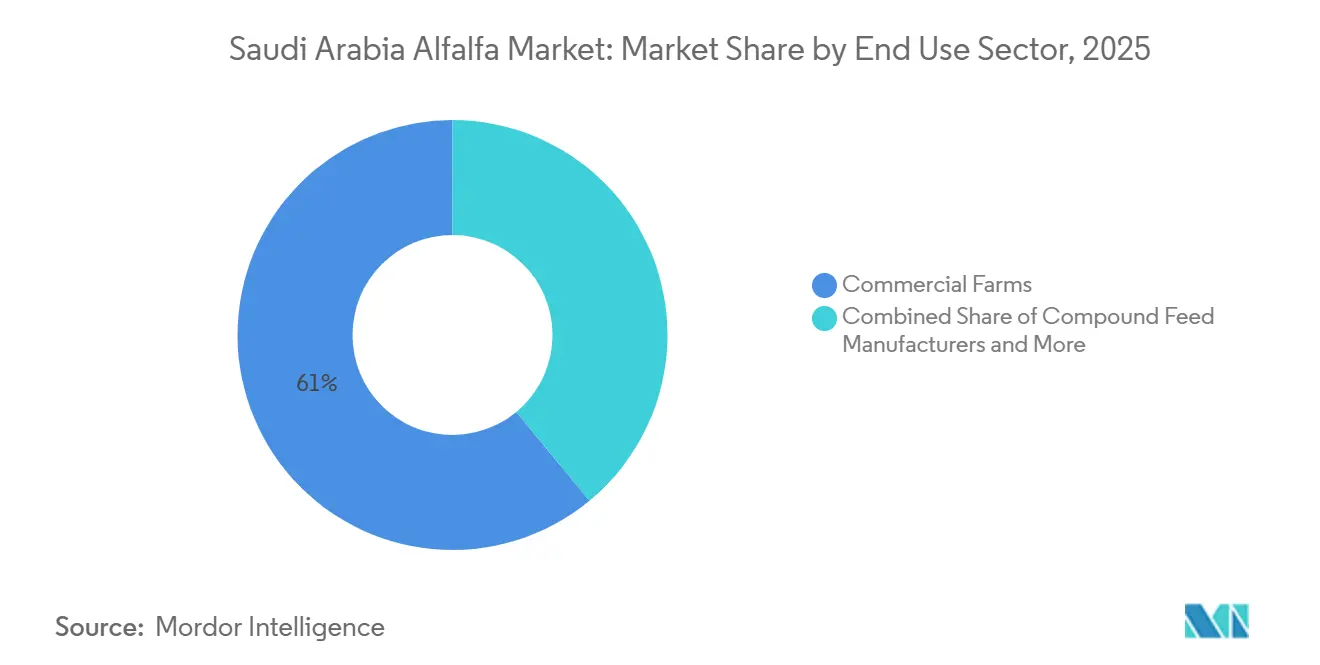

- By end use sector, commercial farms were the largest segment and captured 61.0% of the market share in 2025, while household and hobby animal owners are the fastest growing segment and are anticipated to expand at a 9.4% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of commercial dairy herds and forage intensity | +2.3% | National, concentrated in Riyadh and Eastern Region dairy corridors | Long term (≥ 4 years) |

| Rising camel and equine feed demand for premium forage | +1.8% | National, with highest intensity in Riyadh, Hail, and Tabuk regions | Medium term (2-4 years) |

| Import reliance on high quality baled forage | +1.5% | Global supply converging at Jeddah Islamic Port and Dammam | Long term (≥ 4 years) |

| Feed security priorities for large integrated livestock operators | +1.2% | National, driven by large integrated scale operations | Medium term (2-4 years) |

| Growth of contracted supply models between importers and end users | +0.9% | National, with early gains in Jeddah import corridor and Eastern Province hubs | Medium term (2-4 years) |

| Low water forage positioning versus alternative roughage sources | +0.6% | National, especially relevant in Tabuk and Al-Jouf | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Commercial Dairy Herds and Forage Intensity

Saudi Arabia's commercial dairy sector remains the largest source of alfalfa demand in the country. Almarai reported 189,000 dairy cows in 2025 across its 8 integrated dairy farms, while National Agricultural Development Company (NADEC) is another large-scale buyer with dairy and livestock operations that keep forage procurement central to feed planning[1]Source: Annual Report, “Integrated Annual Report 2025,” almarai.com. Once perennial forage cultivation is fully removed from commercial farming, these operators must rely on imports, overseas farmland, or contracted supply networks rather than domestic sources. This shift ties dairy feed demand closely to international alfalfa availability, making herd scale a direct driver of the Saudi Arabia alfalfa market. It also supports longer contracting cycles, as high-output dairy operations cannot tolerate disruptions in forage quality or delivery timing.

Rising Camel and Equine Feed Demand for Premium Forage

Camel and equine demand adds a distinct premium layer to the Saudi Arabia alfalfa market that differs from standard dairy procurement. According to the Saudi Press Agency, Saudi Arabia's camel population reached 2.24 million head in 2024, confirming the size of the addressable base for premium forage products in this segment. According to data from the Spanish Association of Dehydrated Alfalfa Manufacturers (AEFA), Spanish exporters reported strong Saudi demand for dehydrated alfalfa pellets and other premium formats in 2025, including 38,608 metric tons of pellets, indicating sustained demand from quality-conscious and specification-driven buyers. Tabuk Agricultural Development Company (TADCO) positions its alfalfa products on feed quality parameters that align with high-performance livestock applications, reinforcing the market preference for reliable fiber characteristics over bulk volume. As a result, premium demand growth in the Saudi Arabia alfalfa market is linked to quality assurance, handling performance, and lower spoilage risk in hot climate storage.

Import Reliance on High-Quality Baled Forage

Import dependence in the Saudi Arabia alfalfa market is not a temporary condition, as policy and water constraints have already restructured the supply base. According to World Integrated Trade Solution data, Saudi Arabia ranked as the second largest global importer of alfalfa meal and pellets in 2024 by volume, importing 112,021 metric tons, indicating that value-added product formats already represent a material share of the Saudi Arabia alfalfa market[2]Source: World Integrated Trade Solution, “Lucerne (alfalfa) meal and pellets imports by country in 2024,” wits.worldbank.org. Ministry of Environment, Water and Agriculture (MEWA) subsidy framework for imported alfalfa and pellets reduces the cost gap for commercial users and maintains the commercial viability of imported supply even when freight conditions move against buyers. This sustains supplier competition within the Saudi Arabia alfalfa market, but does not reduce the underlying dependence on imported high-quality forage.

Feed Security Priorities for Large Integrated Livestock Operators

Feed security planning has become a core competitive factor in the Saudi Arabia alfalfa market for large integrated buyers. Almarai's 2025 annual report disclosed 27 owned overseas farms across 27,486 hectares that produced 257,784 metric tons of feed inputs, confirming that self-supply functions as a hedge rather than a secondary activity. The same report indicated that certification and sustainability controls now feature alongside price and volume in procurement planning, reflecting a more formalized sourcing model in the Saudi Arabia alfalfa market. Large operators are therefore better positioned to manage port disruptions, contract slippage, and spot market shortages. This leaves smaller commercial buyers more exposed when freight delays or origin concentration reduce available traded supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water stress and irrigation limits for domestic forage production | -1.8% | National, most acute in Tabuk, Al-Jouf, and Qassim groundwater basins | Long term (≥ 4 years) |

| Freight cost volatility on long haul imported hay and pellets | -1.4% | Global, with concentrated impact on Jeddah Islamic Port and Dammam corridors | Short term (≤ 2 years) |

| Quality variability and spoilage risk in hot climate storage and handling | -0.8% | National, amplified in interior regions away from port intake points | Medium term (2-4 years) |

| Policy pressure to reduce water intensive feed cultivation | -0.8% | National, with spillover implications for overseas sourcing and future forage substitution | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Water Stress and Irrigation Limits for Domestic Forage Production

Water stress remains the most significant structural constraint on the Saudi Arabia alfalfa market. The United States Department of Agriculture (USDA) noted that Saudi Arabia formally restricted alfalfa seed imports and domestic production, confirming that a commercial-scale local recovery is not a near-term option. As a result, supply shortages cannot be addressed by expanding local acreage when imported volumes become expensive or delayed. Water policy has therefore transformed what was once a domestic production base into a long-term import dependency for the Saudi Arabia alfalfa market.

Freight Cost Volatility on Long-Haul Imported Hay and Pellets

Freight volatility directly restrains costs because the Saudi Arabia alfalfa market depends on seaborne supply for commercial-grade products. Maersk is anticipated to activate emergency freight surcharges in March 2026 on cargo moving to and from Dammam and Jubail, highlighting how quickly logistics costs can change for Saudi buyers. Alfalfa hay and pellets are bulky and have relatively low value per unit of weight, so freight rate changes have a larger impact on landed costs than they do for many other imported goods. This cost pressure becomes more visible when buyers rely on limited origin corridors or operate with short inventory cycles. It also pushes the Saudi Arabia alfalfa market toward larger contracts, more diversified origin mixes, and stronger port-side planning to reduce disruption risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pellets Gaining Ground on Bale-Led Volumes

Bales account for 46.3% of the Saudi Arabia alfalfa market share in 2025, indicating that long-stem forage remains central to commercial feeding programs. This position reflects large dairy buyers’ continued preference for field-cut products that support rumen function and reliable intake behavior. TADCO markets its alfalfa based on quality characteristics aligned with high-performance dairy applications, supporting the view that bale demand remains closely tied to nutritional outcomes rather than handling convenience alone. Spanish Association of Dehydrated Alfalfa Manufacturers (AEFA) also reported that Saudi Arabia absorbed 121,122 metric tons of Spanish dehydrated alfalfa bales during the 2024/25 campaign, confirming the scale of bale procurement directed to the Saudi Arabia alfalfa market.

Pellets are forecast to record the fastest product growth, with a CAGR of 10.3% from 2026 to 2031, as they improve freight efficiency and reduce handling losses. Spain supplied 84% of that pellet value, indicating that the Saudi Arabia alfalfa market relies on a narrow supplier base for processed products. Cubes and compressed bales remain smaller niches, but they serve premium camel, equine, and retail channels, where ease of handling and lower storage losses matter more than scale. The product mix is therefore shifting gradually, although bales retain a structural advantage in the Saudi Arabia alfalfa market because dairy remains the largest demand center.

By Application: Dairy Cattle Dominance Challenged by Equine Growth

Dairy cattle feed accounted for 53.2% of the Saudi Arabia alfalfa market in 2025, reflecting the continued dominance of commercial milk production in defining overall demand. This share is driven by large integrated operators such as Almarai and NADEC, whose herd sizes and processing operations require consistent, year-round forage procurement. Poultry, beef cattle, and small ruminant applications remain relevant but secondary, with much of that demand met through compound feed channels rather than direct premium forage procurement. Dairy cattle feed therefore continues to anchor the Saudi Arabia alfalfa market even as the overall user base expands.

Equine feed is the fastest-growing application segment, anticipated to expand at a 10.0% CAGR between 2026 and 2031. Demand is supported by Saudi Arabia's Jockey Club and the broader equine hospitality sector, where buyers require premium-quality alfalfa with consistent nutritional specifications. This makes equine feed less sensitive to cost pressures compared to more price-driven livestock categories. Camelids and other livestock feed also represents a strong growth application, supported by Saudi Arabia's camel population, which sustains demand for certified, specification-controlled alfalfa products that command premiums over standard dairy-grade hay. A 2026 Ministry of Environment, Water and Agriculture-Food and Agriculture Organization (MEWA-FAO) study noted that an expanded Farm Service Delivery Model for small ruminants could generate SAR 18 billion (USD 4.8 billion) in additional meat and dairy production over five years, indicating a broader demand base beyond large commercial dairy operations.

By End Use Sector: Commercial Farms Dominate, Household Segment Accelerates

Commercial farms accounted for 61.0% of the Saudi Arabia alfalfa market in 2025, reflecting the concentration of livestock demand within large integrated operations. Almarai's overseas feed production and sourcing structure demonstrates how large buyers combine owned supply, contracted supply, and inventory planning to manage forage procurement at scale. NADEC's integrated livestock and feed strategy also supports institutional demand for alfalfa products, as larger agribusiness groups increasingly manage nutrition inputs across multiple animal categories. Compound feed manufacturers form a secondary end-use layer, particularly for poultry, sheep, and goats, where alfalfa meal or pellet fractions support balanced feed formulations. This structure keeps pricing power and procurement discipline centered on a relatively small number of commercial buyers within the Saudi Arabia alfalfa market.

The household and hobby animal owners segment is forecast to grow at a 9.4% CAGR from 2026 to 2031, making it the fastest-growing end-use segment. This group includes small ruminant keepers, backyard poultry owners, and individual camel and horse buyers who access the Saudi Arabia alfalfa market through retail stores, cooperatives, and smaller distributors. The USDA has documented monthly support payments for small livestock holders, which helps sustain purchasing power for forage even when retail unit prices remain above commercial bulk rates. GASTAT's (General Authority for Statistics) livestock data also supports the breadth of this user base, as animal ownership is distributed across multiple categories beyond commercial dairy. While this segment is smaller in absolute value, it is contributing to a wider channel structure in the Saudi Arabia alfalfa market beyond large farm procurement.

Geography Analysis

Saudi Arabia is a single-country market, but the Saudi Arabia alfalfa market shows clear regional differences across production history, import handling, and end-use concentration. Tabuk and Al-Jouf were historically central to licensed domestic forage cultivation. TADCO remains the most visible commercial alfalfa operator in Tabuk, while Al-Jouf Agricultural Development has maintained alfalfa as a key forage crop in its portfolio. MEWA's restricted cultivation framework means these northern regions are no longer growth areas for large-scale field expansion. Their role is now more closely tied to residual licensed activity, transitional production, and legacy expertise than to broad domestic supply growth.

The western and eastern port corridors are more important to the current Saudi Arabia alfalfa market than inland cultivation zones. Jeddah Islamic Port serves as a major intake point for product arriving from Spain, the United States, and Argentina, particularly for buyers serving central demand clusters. According to General Authority for Statistics, Riyadh remained the largest raw milk producing region in 2024 at 1.6 billion liters, which explains why western port inflows and inland distribution to central Saudi Arabia carry strategic value [3]Source: General Authority for Statistics, “Livestock Statistics 2024,” stats.gov.sa. The Eastern Province also matters, as Dammam supports industrial dairy and livestock flows connected to the eastern side of the Kingdom.

Interior regions such as Riyadh, Hail, and Al-Qassim function mainly as consumption hubs rather than supply origins in the Saudi Arabia alfalfa market. Riyadh's dairy concentration keeps it at the center of forage demand, while Hail and other interior zones add poultry, small ruminant, and mixed livestock consumption. Limited port-side storage and long inland movements can increase handling complexity for these regions, particularly when imported supply is delayed. This makes route reliability and warehouse quality more important than regional production potential for current market performance. PIF's support for arid climate agricultural technologies suggests that regional feed systems may become more efficient over time, but this does not reduce the near-term import dependence of large dairy and livestock operators. The geography of the Saudi Arabia alfalfa market is therefore defined by ports, inland logistics, and livestock concentration rather than by domestic growing areas.

Competitive Landscape

The Saudi Arabia alfalfa market is moderately concentrated, with the top five players holding a major share of revenue. Competition centers on supply reliability, product form, nutritional consistency, and landed cost control rather than price discounting. Companies compete in a buyer environment where commercial farms prioritize stable quality and predictable deliveries over occasional low spot prices. This makes the Saudi Arabia alfalfa market more relationship-driven than many other agricultural commodity markets with shorter contracting cycles.

Almarai's strategy illustrates how large buyers are shaping the Saudi Arabia alfalfa market. Its five-year investment program and overseas farm base reduced reliance on external spot purchases, while feed output from owned farms provided a hedge against disruptions in traded volumes. Al Dahra offers a second example, as its integrated feed business structure supports larger supply commitments and gives Saudi customers access to a broader sourcing and logistics platform. TADCO represents a third strategic approach, where product positioning is tied to forage quality characteristics and premium livestock performance rather than bulk volume sales alone. These approaches indicate that leading participants in the Saudi Arabia alfalfa market are using supply chain control, technical quality, and operating scale to maintain their positions.

The competitive gap between large and small participants is further widened by compliance and sourcing requirements in the Saudi Arabia alfalfa market. Import approvals, product quality checks, and feed specification standards create entry barriers for new suppliers that lack a documented operating history. Buyers also favor suppliers that can support multi-origin diversification when one supply corridor becomes more expensive or less reliable. This is particularly relevant following 2026 freight disruptions, as supplier resilience is now assessed by contract performance under stress, not only by quoted price. The faster growth of household and hobby channels may create opportunities for smaller pack sizes and retail-focused distribution, but the main profit pool in the Saudi Arabia alfalfa market remains with institutional buyers and large import programs. As a result, the market remains open to competition, but durable advantage is concentrated among participants that can combine logistics strength, quality assurance, and commercial scale.

Saudi Arabia Alfalfa Industry Leaders

Alfeed

Al Dahra ACX Global Inc.

Alfalfa Monegros S.L.

Border Valley Trading, LLC

Bailey Farms International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: NADEC launched a SAR 2 billion (USD 533 million) livestock project in Hail, supported by SAR 1.1 billion (USD 293 million) in government-backed financing from the Agricultural Development Fund. The facility targets an annual production capacity of 1 million sheep by 2030, which is anticipated to significantly expand mixed-forage feed demand in the northern interior of Saudi Arabia, including alfalfa, and directly support Vision 2030 food security targets.

- May 2025: TADCO obtained a two-year winter fodder seed production license from MEWA under the ministry's updated licensing framework. The license positions TADCO among the few licensed domestic forage producers under the restricted-cultivation regime, aiding the market.

- February 2025: Balady Poultry unveiled a five-year growth plan including USD 304 million investment to build new slaughterhouse, processing facility, and hatcheries, funded through the Saudi Agricultural Development Fund and commercial loans, directly impacting the alfalfa demand in the country.

Saudi Arabia Alfalfa Market Report Scope

Alfalfa hay is obtained from the alfalfa plant, also known as lucerne and Medicago sativa. It is cultivated as an important forage crop and is widely used in animal nutrition because of its high protein content and forage value.

The Saudi Arabia Alfalfa Market is Segmented by Product Type (Bales, Pellets, Cubes, and Compressed Bales), by Application (Dairy Cattle Feed, Beef Cattle Feed, Poultry Feed, Equine Feed, Small Ruminant Feed, Camelids and Other Livestock Feed), and by End Use Sector (Commercial Farms, Compound Feed Manufacturers, Household And Hobby Animal Owners, and Pet Food and Specialty Nutrition). The Market Size and Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition |

Key Questions Answered in the Report

What is the forecasted value of the Saudi Arabia alfalfa market by 2031?

The Saudi Arabia alfalfa market is forecasted to reach USD 667.27 million by 2031, rising from USD 453.68 million in 2026 at an 8.0% CAGR.

Why is Saudi Arabia so dependent on imported alfalfa?

MEWA’s phaseout of perennial forage cultivation and water stress constraints have made imports and overseas sourced forage the main supply base for commercial users.

Which product type leads demand in Saudi Arabia?

Bales led the market in 2025 with a 46.35% share because large dairy farms still need long stem forage in regular feeding programs.

What are the main risks for suppliers and buyers?

The main risks are freight volatility, origin concentration, hot climate storage losses, and long term policy pressure to shift away from water intensive feed systems.

Page last updated on: