Saudi Arabia AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

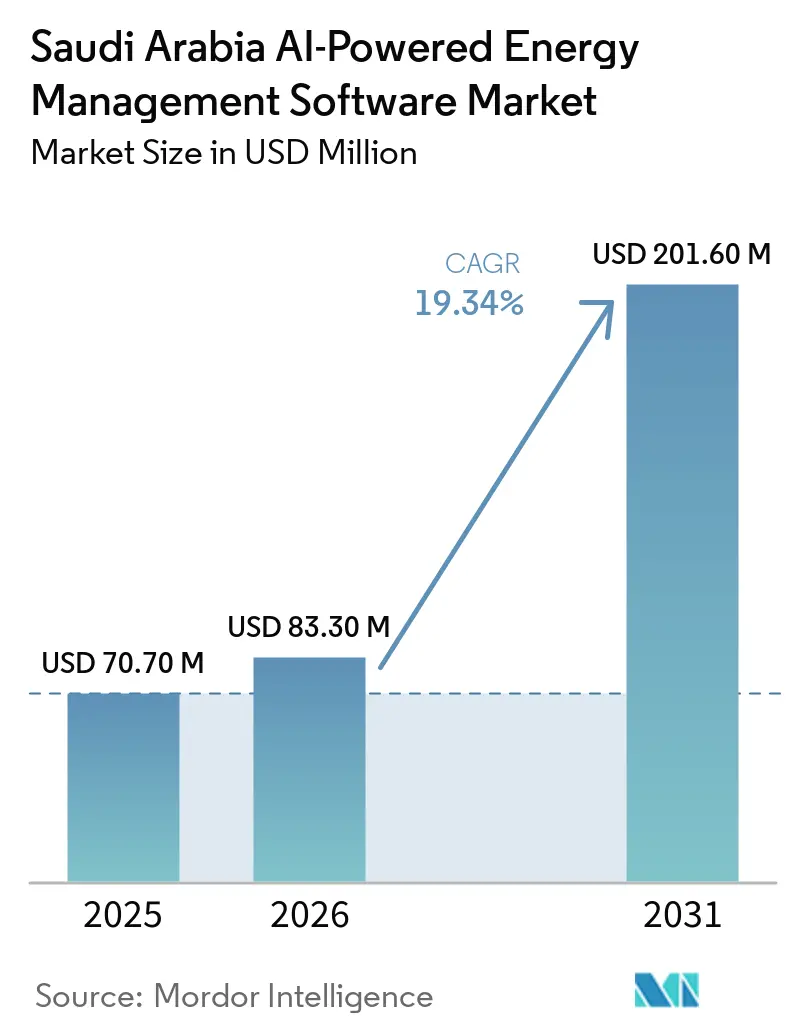

| Base Year Market Size (2025) | USD 70.70 Million |

| Market Size (2026) | USD 83.30 Million |

| Market Size (2031) | USD 201.60 Million |

| Growth Rate (2026 - 2031) | 19.34% CAGR |

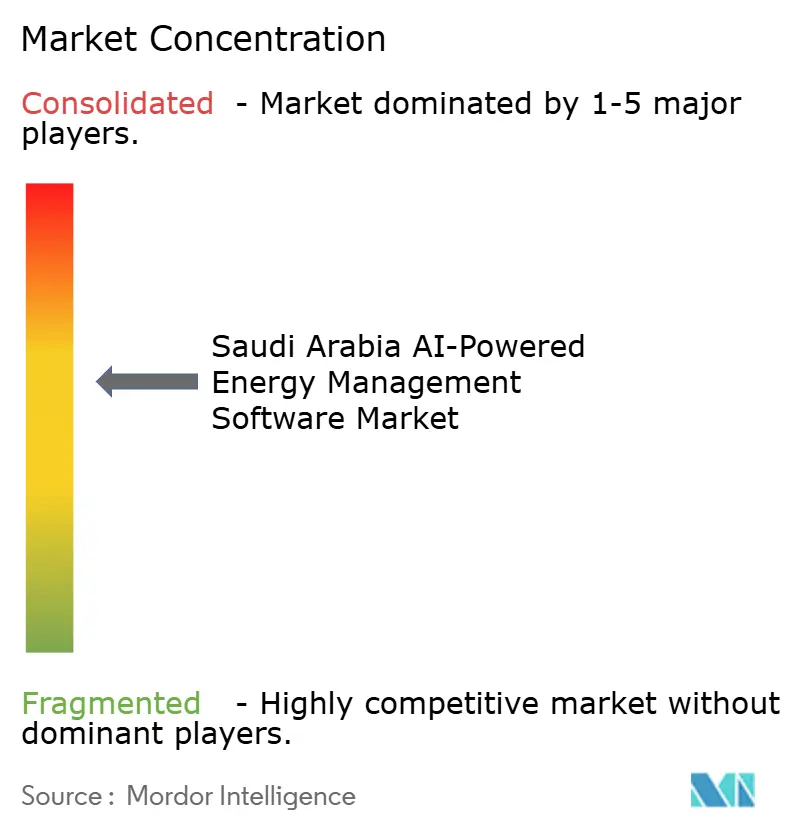

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Saudi Arabia AI-powered energy management software market size was valued at USD 70.7 million in 2025 and estimated to grow from USD 83.3 million in 2026 to reach USD 201.6 million by 2031, at a CAGR of 19.34% during the forecast period 2026-2031. The Saudi Arabia AI-powered energy management software market is being shaped by the country’s push to raise renewable power generation, improve grid performance, and lower emissions under Vision 2030. Demand is also rising because utilities, large campuses, and industrial operators now need software that can respond to changing load patterns, rising cooling demand, and more complex operating conditions. Buyers are paying closer attention to platforms that can connect with existing meters, sensors, and control systems without requiring a full replacement of older infrastructure. Competition centers on vendors that can combine software depth, local delivery support, cybersecurity readiness, and integration capabilities across utility and industrial settings. Growth opportunities remain strongest where digital energy control has moved from reporting usage to actively forecasting demand, balancing loads, and supporting renewable integration.

Key Report Takeaways

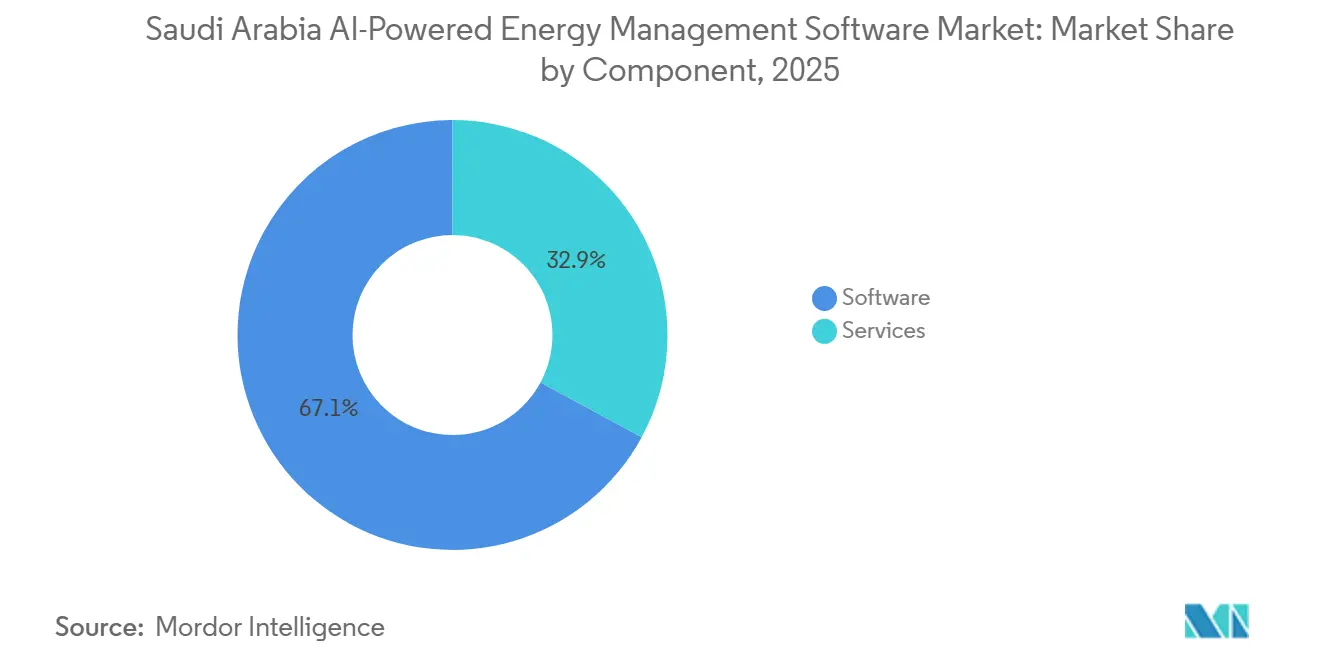

- By component, software held 67.12% of revenue in 2025, while services are projected to expand at a 20.41% CAGR through 2031.

- By deployment mode, cloud-based led with 57.18% of revenue in 2025, while hybrid is projected to record the highest CAGR of 20.53% through 2031 in the Saudi Arabia AI-powered energy management software market.

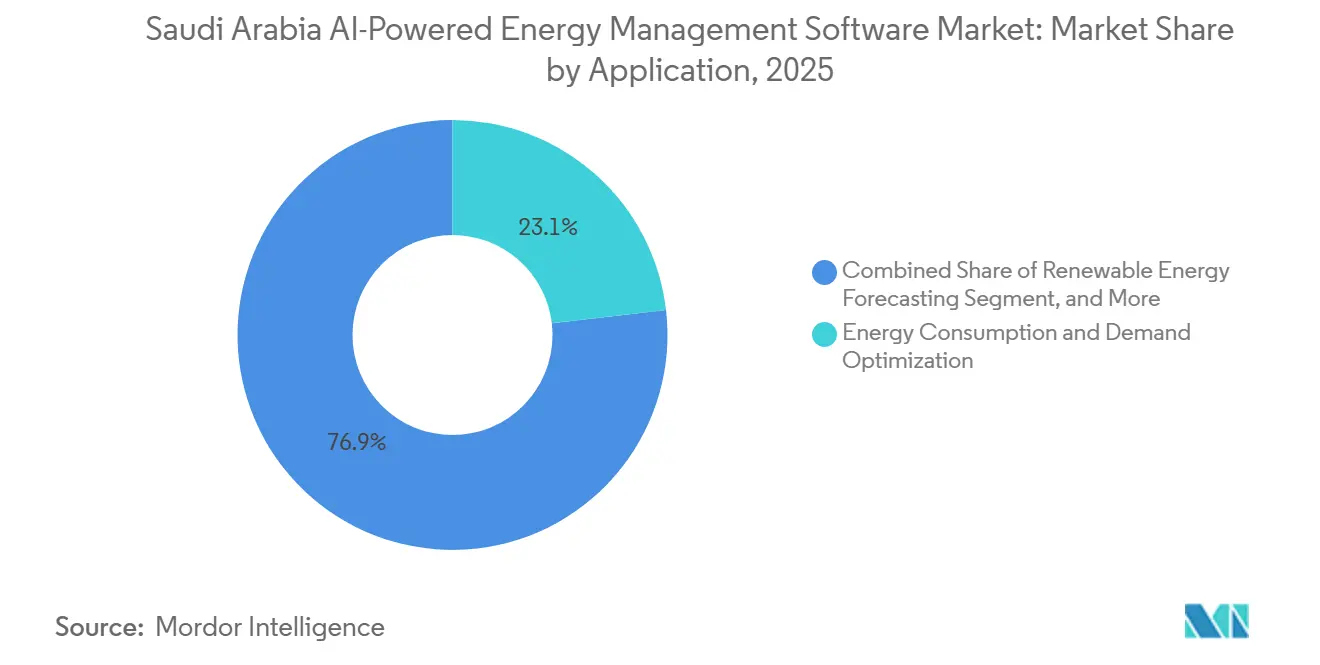

- By application, energy consumption and demand optimization accounted for 23.14% in 2025, while renewable energy forecasting and integration are projected to grow at a 20.64% CAGR through 2031.

- By end user, utilities held 34.19% of the Saudi Arabia AI-powered energy management software market share in 2025, while industrial facilities are projected to expand at a 20.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Utility Demand Response Integration Across Commercial Buildings | +4.5% | Kingdom-wide, concentrated in Riyadh, Jeddah, and Eastern Province commercial zones | Short term (≤ 2 years) |

| Accelerated Net Zero Building Retrofits in Vision 2030 Projects | +4.0% | National, with early gains in Diriyah, NEOM, Red Sea Project, and Qiddiya | Short term (≤ 2 years) |

| Expanding Industrial IoT Connectivity in Energy-Intensive Facilities | +3.5% | Eastern Province, NEOM Oxagon, and SPARK | Medium term (2-4 years) |

| AI-Based Load Forecasting Adoption in Large Campus Operations | +2.5% | Riyadh and Jeddah commercial districts, university and hospital campuses | Medium term (2-4 years) |

| Multisite Energy Benchmarking Demand From Enterprise Facilities Teams | +2.0% | Riyadh, Jeddah, and Dammam | Medium term (2-4 years) |

| Localization of Energy Optimization Workflows For Arabic-First Operations | +1.5% | Kingdom-wide, with early traction in government and semi-government entities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Utility Demand Response Integration Across Commercial Buildings

Cooling demand remains the largest load issue in commercial buildings, as HVAC systems account for over 70% of building energy use in Saudi Arabia.[1]Saudi Energy Efficiency Center, “Buildings Sector,” Saudi Energy Efficiency Center, seec.gov.sa This makes demand response more important in the Saudi Arabia AI-powered energy management software market because utilities need faster control over building loads during peak conditions. The value of these platforms increases further when software can automate changes across HVAC, lighting, and process equipment, rather than relying on manual action. The Saudi Arabia AI-powered energy management software market is therefore moving toward platforms that can receive utility signals and translate them into immediate building-level responses. Vendors that can connect cleanly with utility systems and existing building controls are in a stronger position, as buyers want less disruption during deployment. That preference also favors providers with proven local integration capability, since large building portfolios often include multiple control systems and different retrofit histories.

Accelerated Net-Zero Building Retrofits in Vision 2030 Projects

Vision 2030 has created a broad pipeline of new developments and retrofits that must show stronger energy performance from the start.[2]Saudi Vision 2030, “King Salman Energy Park,” Saudi Vision 2030, vision2030.gov.sa This has elevated the role of AI-powered energy management software in Saudi Arabia, as project owners need software for metering, monitoring, reporting, and optimization as part of routine delivery. The pressure is not limited to flagship projects, as older commercial assets also face stronger expectations for efficiency and cost control. In practice, that means the Saudi Arabia AI-powered energy management software market benefits from both new construction and the large installed base of buildings that still run on older energy systems. Software becomes more attractive when it can turn compliance work into measurable savings, especially in buildings with high cooling loads and long operating hours. Vendors that tailor reporting and workflows to local project standards are likely to keep customers longer because the platform remains useful after initial commissioning.

Expanding Industrial IoT Connectivity in Energy-Intensive Facilities

Industrial digitalization is becoming a major driver of demand as large facilities connect more equipment, sensors, and edge systems into a common operating environment. IBM and Aramco announced in May 2026 that they intended to collaborate on industrial AI, agentic AI, automation, and materials science across Saudi Arabia’s energy systems.[3]IBM Newsroom, “IBM and Aramco Explore Collaboration to Accelerate AI and Innovation Across Saudi Arabia,” IBM Newsroom, mediaroom.com The Saudi Arabia AI-powered energy management software market benefits from this shift, as connected industrial sites require continuous monitoring, dispatch support, and performance optimization across power-intensive assets. The Saudi Arabia AI-powered energy management software industry also becomes harder for late entrants because plants that generate their own operating data tend to stay with the platform that already understands site behavior. NEOM adds to this effect because its development model depends on advanced digital infrastructure and large-scale energy orchestration. Vendors with industrial connectors, local support, and strong cybersecurity posture are better positioned, as buyers do not want to test unproven systems in production environments.

AI-Based Load Forecasting Adoption in Large Campus Operations

Large campuses are becoming an important demand pocket because they combine heavy cooling loads, long operating schedules, and measurable savings potential. Research published in 2025 showed that hybrid deep learning models applied to Saudi grid load data delivered lower forecasting error than conventional statistical models.[4]Sajeh Zairi and Mushira Freihat, “Electric Load Forecasting Using Machine Learning for Peak Demand Management in Smart Grids,” Engineering, Technology and Applied Science Research, etasr.com That finding supports the Saudi Arabia AI-powered energy management software market because hospitals, universities, and public campuses need better short-term planning and more accurate load scheduling. Buyers also see value in forecasting tools that support participation in demand response programs and internal cost control. The Saudi Arabia AI-powered energy management software market is likely to see faster adoption among this group because campus operators typically manage large, centralized facilities and can measure results sooner. Vendors that present forecasting as an operating tool rather than a reporting feature are more likely to win because the return is easier for buyers to evaluate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Building Management Systems | -3.5% | Kingdom-wide, most acute in pre-2015 commercial real estate stock in Riyadh and Jeddah | Medium term (2-4 years) |

| Cybersecurity Concerns Around Cloud-Connected Energy Platforms | -2.5% | National, especially critical infrastructure, oil and gas, and utility OT environments | Medium term (2-4 years) |

| Limited Availability Of High-Quality Real-Time Energy Data | -1.5% | Secondary urban and industrial zones, less acute in Riyadh and Eastern Province | Long term (≥ 4 years) |

| Slow Change Management In Asset-Heavy Industrial Organizations | -1.0% | Eastern Province industrial clusters and legacy petrochemical and desalination facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Concerns Around Cloud-Connected Energy Platforms

Cybersecurity remains a significant constraint because energy platforms increasingly connect operational systems to cloud analytics and remote software layers. Saudi buyers in utilities, oil and gas, and heavy industry place high weight on security controls, local hosting readiness, and compliance with strict operational requirements. That underscores the advantage of larger vendors, as they usually have more resources for secure architecture, certification work, and local delivery support. The result is a Saudi Arabia AI-powered energy management software market where procurement cycles can lengthen when the platform touches critical assets or sensitive operational data. Hybrid deployment becomes more attractive in this environment because it allows local processing for control data while still using cloud tools for broader analytics. Vendors that treat cybersecurity as part of product design rather than an add-on are more likely to pass screening and remain in the final bidding rounds.

Fragmented Legacy Building Management Systems

A major barrier in the Saudi Arabia AI-powered energy management software market is the split between new AI-ready assets and older buildings that still run on isolated control systems. Many pre-2015 commercial properties were built around proprietary building management systems with limited data exchange and weak integration options. That slows software adoption because vendors often need extra hardware, protocol conversion, and manual data mapping before the platform can work properly. It also raises project costs, which can weaken the savings case for owners of mid-sized properties and older commercial portfolios. The Saudi Arabia AI-powered energy management software market therefore favors vendors and local partners that already understand mixed BMS environments and can shorten integration timelines. Without that local integration depth, even a strong software platform can struggle to move past pilot stages in the retrofit segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Early Adoption While Services Gain Depth

Software held 67.12% of the Saudi Arabia AI-powered energy management software market share in 2025, which shows that buyers still prefer to start with analytics, monitoring, and optimization platforms before expanding service scope. In the early phase of deployment, customers often want visibility into load behavior, energy waste, and system inefficiencies before committing to broader managed programs. That has helped software-first vendors win initial contracts across utilities, campuses, and large commercial assets. The Saudi Arabia AI-powered energy management software market also rewards modular platforms because customers often want to add forecasting, reporting, and demand response functions in stages. This buying pattern keeps software in the lead because it gives users more control over budgets, deployment timing, and internal approval steps.

Services are projected to expand at a 20.41% CAGR through 2031, underscoring the importance of implementation and continuous optimization after the first deployment wave. The Saudi Arabia AI-powered energy management software industry is moving toward longer customer relationships because AI tools need model tuning, workflow changes, and ongoing performance reviews under local operating conditions. That is especially relevant in Saudi Arabia, where cooling intensity, tariff reform, and mixed infrastructure create site-specific requirements that generic settings cannot always handle. IBM’s planned collaboration with Aramco in industrial AI supports that shift by pointing to stronger demand for advisory, integration, and operational AI support in the energy system. Service demand also rises when owners need Arabic-language workflows, benchmark reporting, and local technical support for daily use. Over time, that narrows the gap with software, as customers increasingly judge value by sustained performance rather than platform access alone.

By Deployment Mode: Cloud-Based Leads While Hybrid Gains Strategic Weight

Cloud-based deployment accounted for 57.18% of revenue in 2025, reflecting the appeal of centralized software updates, easier scaling, and broader data visibility across multiple sites. This lead fits the needs of commercial groups, enterprise headquarters, and public organizations that want faster software rollout without building large in-house infrastructure. Cloud models also support easier integration with smart meters, sensor networks, and enterprise reporting tools, helping the Saudi Arabia AI-powered energy management software market expand beyond stand-alone monitoring. For many users, cloud deployment remains the simplest route to launch because it reduces the initial technical burden and speeds up dashboard access across teams. That explains why cloud-based systems still set the baseline for mainstream adoption, even as more advanced buyers ask for deeper control options.

Hybrid deployment is projected to rise at a 20.53% CAGR through 2031, making it the fastest-growing mode in the Saudi Arabia AI-powered energy management software market. Growth is being driven by buyers who want cloud analytics but still need local control over sensitive operational data and fast response at the site level. This matters most in industrial settings, where delays or external dependency can create risk for power-intensive operations and continuous processes. The Saudi Arabia AI-powered energy management software industry is therefore shifting toward architectures that split workloads between local infrastructure and broader cloud tools. Hybrid models also help vendors address cybersecurity concerns without abandoning advanced forecasting and optimization features. That balance is likely to become a stronger buying requirement as software moves deeper into utility operations, industrial campuses, and critical infrastructure environments.

By Application: Demand Optimization Leads Revenue While Renewables Integration Gains Speed

Energy consumption and demand optimization accounted for 23.14% of the Saudi Arabia AI-powered energy management software market in 2025, indicating that customers still enter the category through cost-control and load-management use cases. These tools are easier to justify because buyers can link them directly to power bills, operating schedules, and visible efficiency gains. They also fit well with the needs of buildings and campuses that want to cut peak demand without redesigning core systems. In the Saudi Arabia AI-powered energy management software market, this application remains the most practical starting point because it produces measurable operational value early in deployment. Once organizations gain confidence in baseline monitoring and optimization, they are more willing to add predictive maintenance, distributed energy management, and advanced control functions.

Renewable energy forecasting and integration is projected to expand at a 20.64% CAGR through 2031, making it the fastest-growing application area. Saudi Arabia’s renewable power push underscores the need for better forecasting and dispatch support, as greater solar and wind penetration adds greater variability to system operations. The Ministry of Energy’s renewable energy program and related national initiatives show the scale of that transition. KAPSARC reported in 2025 that AI-based dynamic line rating in the Saudi power system could reduce renewable curtailment by up to 46% under a 2030 scenario and lower annual variable electricity costs by up to 3%. This makes forecasting and integration more than a niche function because it directly supports grid stability, renewable uptake, and better system economics. The Saudi Arabia AI-powered energy management software market is likely to place more value on vendors that can move from forecast generation to dispatch support as renewable penetration increases.

By End User: Utilities Lead While Industrial Facilities Expand Fastest

Utilities held 34.19% of the Saudi Arabia AI-powered energy management software market share in 2025, which reflects their central role in metering, grid analytics, and system-wide load management. Utility demand tends to be larger in scale and more visible because projects often touch many assets, broader data flows, and large customer bases. That keeps utilities at the center of the Saudi Arabia AI-powered energy management software market, especially where digital grid programs require new monitoring and planning tools. Wipro’s July 2025 smart grid contract with Saudi Electric Company’s National Grid SA showed that utility buyers are still investing in data management and forecasting capability at scale. Utility projects also influence later adoption across other segments by shaping data standards, signaling structures, and interoperability expectations.

Industrial facilities are projected to grow at a 20.75% CAGR through 2031, making them the fastest-expanding end-user group in the Saudi Arabia AI-powered energy management software market. This growth comes from large sites that need tighter coordination across power use, production continuity, asset health, and emissions visibility. NEOM and SPARK support that direction because both are tied to advanced industrial development and modern digital infrastructure in the Kingdom. Industrial operators also create greater demand for high-reliability architecture because energy software must work alongside production systems rather than in parallel. That raises the value of vendors with industrial integration experience, local engineering support, and strong control over security design. As a result, the Saudi Arabia AI-powered energy management software market is likely to see more product differentiation in industrial settings than in standard commercial deployments.

Geography Analysis

The Eastern Province remains the most intensive operating zone for the Saudi Arabia AI-powered energy management software market because it combines oil and gas activity, large industrial clusters, and energy technology investment. SPARK adds to that role by supporting a concentrated base for energy-related manufacturing, services, and project activity in the Kingdom. The area also benefits from close links between industrial assets, utility infrastructure, and technical service providers, which makes software deployment more practical at scale. Demand in this geography is less about stand-alone dashboards and more about integrating forecasting, dispatch, and operational performance into everyday plant and network management. That makes the Eastern Province one of the clearest indicators of how the Saudi Arabia AI-powered energy management software market is shifting toward heavier industrial use.

Riyadh is the main commercial and institutional hub because it houses ministries, corporate headquarters, universities, hospitals, and large public facilities. This gives the Saudi Arabia AI-powered energy management software market a strong base in campus operations, enterprise software procurement, and city-scale building portfolios. Demand in Riyadh is also helped by the need to manage energy use across large mixed-use assets with long operating hours and high cooling loads. Jeddah presents a different pattern because its logistics, hospitality, healthcare, and port-linked assets create a broader mid-market opportunity. In that setting, multisite benchmarking, centralized reporting, and load forecasting can be more attractive than highly customized industrial platforms. Together, Riyadh and Jeddah expand the Saudi Arabia AI-powered energy management software market beyond utility-led demand and make commercial building software a more active part of growth.

NEOM stands out as a distinct demand environment because its development model relies on advanced digital coordination, large-scale renewable energy, and tightly managed infrastructure. NEOM describes itself as a new regional model built around innovation, infrastructure, and future-focused systems. That makes it highly relevant to the Saudi Arabia AI-powered energy management software market because it pushes technical expectations beyond standard building automation or simple reporting. Requirements shaped in mega-project settings are likely to influence future requests in other parts of the country, especially for edge processing, forecasting accuracy, and coordinated control across distributed assets. The result is that geography in this market is not only about where demand is highest, but also about where software requirements become more advanced first.

Competitive Landscape

The Saudi Arabia AI-powered energy management software market is moderately concentrated around large global automation and building technology firms, while enterprise software groups and specialist AI vendors compete for higher-value use cases. Incumbents benefit from installed hardware bases, local partner networks, and years of work in utility and industrial accounts. That gives them an advantage when customers want one provider to handle software, controls, service support, and compliance documentation. The Saudi Arabia AI-powered energy management software market also remains difficult for small stand-alone vendors because buyers often favor proven integration capability over narrow feature depth. This is especially true in critical environments where a platform must work with existing operational systems and pass strict internal screening.

ERP and enterprise software providers add pressure from another angle because they can embed energy functions into systems that customers already use for assets, maintenance, and operations. IBM’s May 2026 collaboration with Aramco showed how enterprise AI suppliers are moving deeper into industrial environments that were once led mainly by operational technology vendors. Wipro’s utility contract in 2025 also showed that software-led service firms can win important positions in smart grid and data management programs. These moves matter because they broaden the competitive field beyond traditional building and industrial controls. The Saudi Arabia AI-powered energy management software market is therefore seeing more overlap between OT vendors, enterprise platforms, and specialized digital service providers.

Pure-play AI companies still have room to compete, but they need a clearer edge in accuracy, transparency, or speed of deployment to justify separate adoption. C3.ai’s June 2026 expansion with Shell across more than 13,000 pieces of equipment strengthened its industrial credibility and showed how specialist AI vendors can scale in asset-heavy settings. GridPoint’s March 2026 report that it was nearing USD 1.5 billion in cumulative customer energy savings across more than 20,000 commercial building deployments also reinforced the case for software-driven efficiency at portfolio scale. The best opening for newer entrants in the Saudi Arabia AI-powered energy management software market may lie in localized workflows, Arabic-first interfaces, and faster integration into mixed infrastructure environments. Where incumbents are broad but slower, focused providers can still gain ground if they solve specific operating problems more directly.

Saudi Arabia AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: C3.ai and Shell signed a new multi-year agreement extending C3.ai's predictive maintenance and AI agent-based root cause analysis platform across Shell's global operations, covering more than 13,000 pieces of equipment. The expansion substantiates pure-play AI platform credentials for large-scale industrial energy asset management.

- May 2026: Aramco and IBM announced an intended collaboration to advance industrial AI, agentic AI, automation, and materials science across Saudi Arabia's energy systems, announced at IBM THINK Boston. The collaboration combines IBM's enterprise AI platforms with Aramco's operational datasets across mission-critical energy environments.

- March 2026: GridPoint announced it was approaching USD 1.5 billion in cumulative energy savings across 20,000+ commercial building deployments as US electricity prices hit decade highs, reinforcing the financial case for AI-driven commercial building energy management.

- July 2025: Wipro won a multi-year strategic contract from Saudi Electric Company - National Grid SA to implement a Smart Meter Data Management system enabling intelligent forecasting, reporting, and improved grid planning across the Kingdom's transmission network.

Saudi Arabia AI-Powered Energy Management Software Market Report Scope

The Saudi Arabia AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Saudi Arabia AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

How large is the Saudi Arabia AI-powered energy management software market in 2026?

The Saudi Arabia AI-powered energy management software market stands at USD 83.3 million in 2026 and is projected to reach USD 201.6 million by 2031 at a 19.34% CAGR.

What is driving demand for AI-powered energy management software in Saudi Arabia?

Demand is rising because utilities, campuses, buildings, and industrial sites need better demand control, forecasting, and renewable integration under Vision 2030 energy goals.

Which application generates the most revenue in this space?

Energy consumption and demand optimization led with a 23.14% revenue share in 2025 because buyers still prioritize cost control and load management first.

Which end-user group is growing the fastest in Saudi Arabia?

Industrial facilities are projected to grow at a 20.75% CAGR through 2031, supported by large digital and industrial development projects such as NEOM and SPARK.

Why is hybrid deployment gaining traction over time?

Hybrid models balance cloud analytics with local control, which helps users address cybersecurity, data handling, and response-time needs in critical environments.

Who are the main competitors active in this category?

The field includes global automation and building technology leaders, enterprise software companies, and specialist AI vendors, with competition shaped by integration depth, service capability, and local execution.

Page last updated on: