Robotics CNC Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.5 Billion |

| Market Size (2031) | USD 4.30 Billion |

| Growth Rate (2026 - 2031) | 11.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotics CNC Turning Centers Market Analysis by Mordor Intelligence

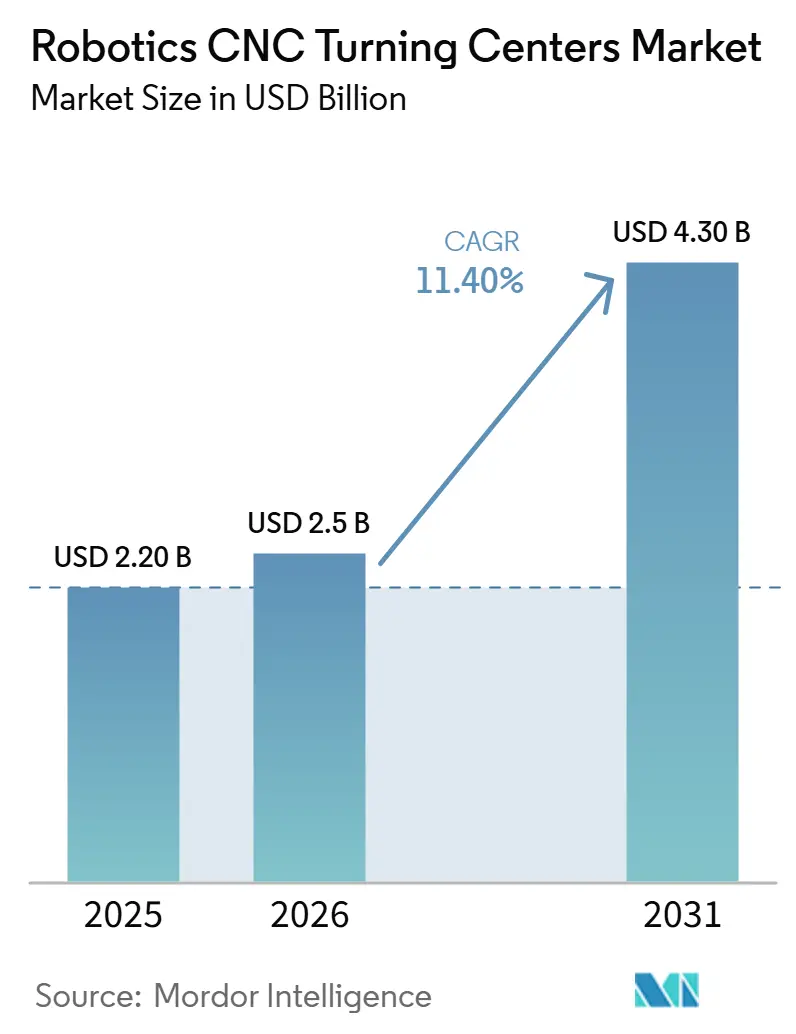

The Robotics CNC Turning Centers Market size is expected to grow from USD 2.20 billion in 2025 to USD 2.5 billion in 2026 and is forecast to reach USD 4.30 billion by 2031 at 11.40% CAGR over 2026-2031.

The robotics CNC turning centers market is undergoing structural growth because manufacturers are facing rising labor costs, persistent gaps in skilled shop-floor staffing, and a growing need to maintain steady output across multiple shifts without adding similar levels of labor. Industrial robot deployment remained strong in 2024, with 542,000 units installed worldwide, indicating that automation demand across machine tending and material handling remained firm even in a mixed macro setting. China accounted for 295,000 of those installations in 2024, or 54% of the global total, which helps explain why the Asia-Pacific continues to account for the largest share of the robotics CNC turning centers market. Europe and North America remain important for advanced turning cells used in high-mix and low-volume production, where flexibility, software depth, and fast changeovers matter as much as raw throughput. The robotics CNC turning centers market also continues to benefit from aerospace production ramp-ups and reshoring programs, even as high upfront cell costs, interface gaps between robots and CNC systems, and cybersecurity exposure keep adoption decisions selective in smaller plants.

Key Report Takeaways

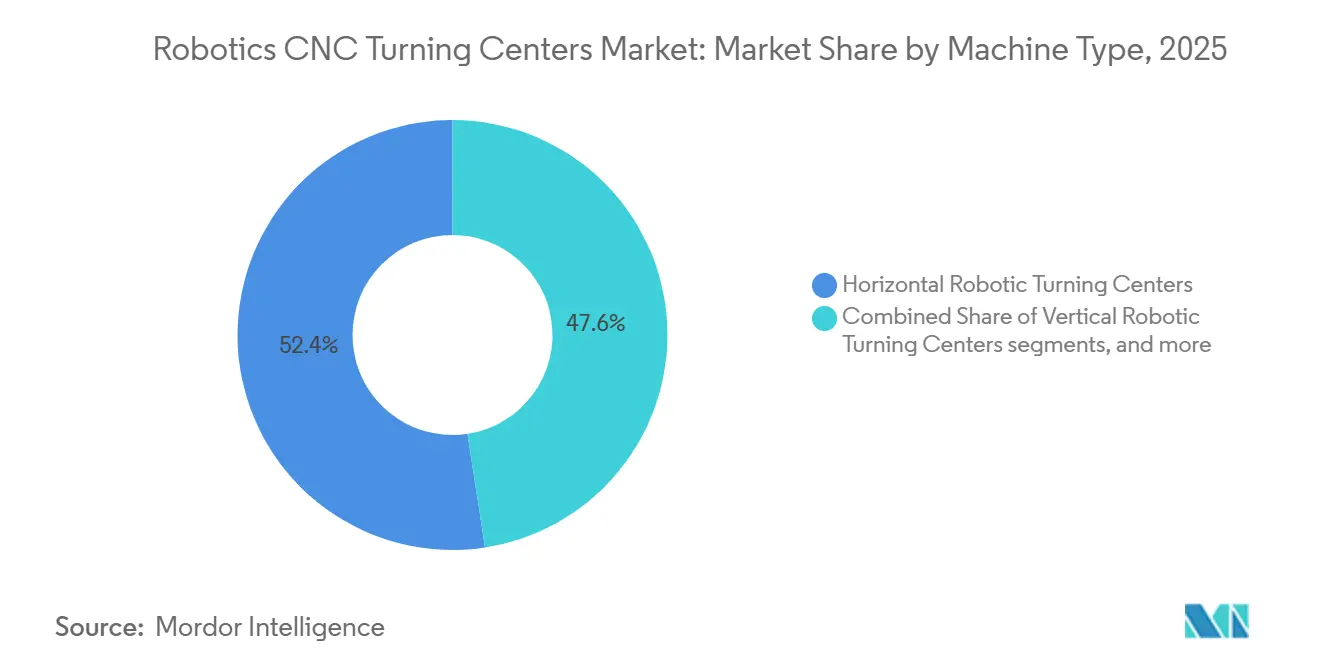

- By machine type, horizontal robotic turning centers accounted for 52.41% of the robotics CNC turning centers market size in 2025, while multi-tasking robotic turning centers are forecast to expand at a 17.1% CAGR through 2031.

- By robot type, articulated robots accounted for 54.62% of the market share in 2025, while collaborative robots are projected to record the fastest growth at a 18% CAGR through 2031.

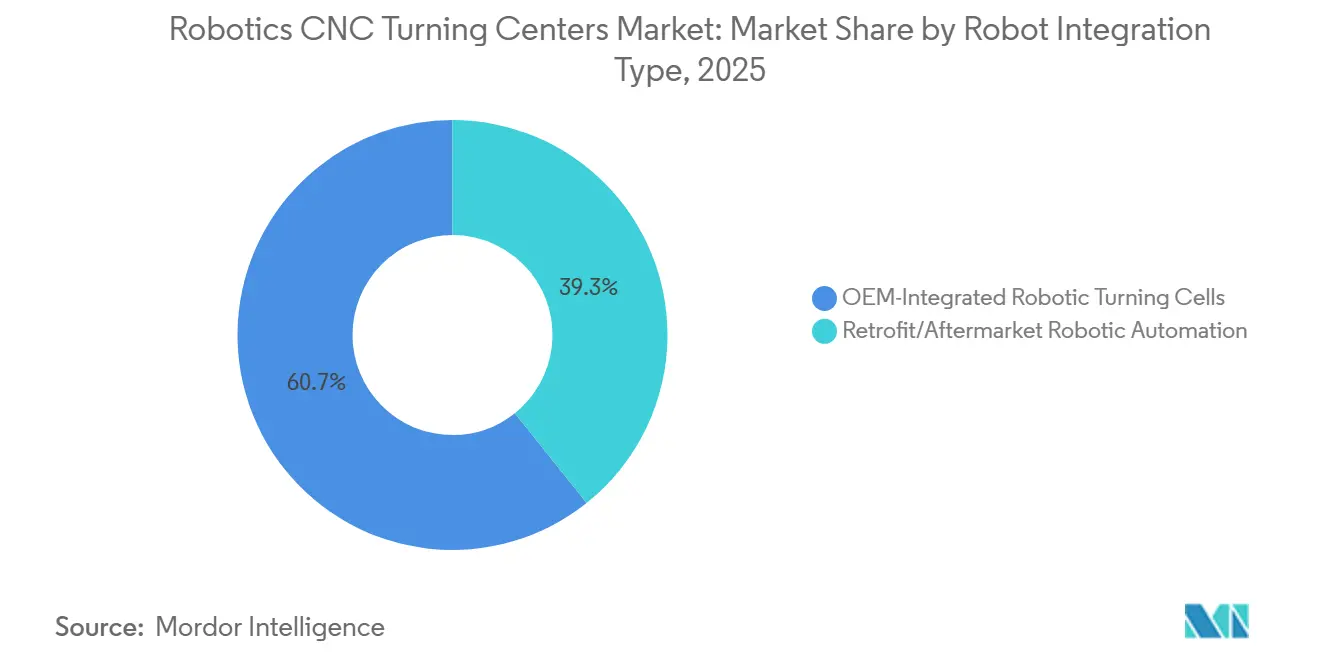

- By robot integration type, OEM-integrated robotic turning cells led with 60.72% share in 2025, while retrofit/aftermarket robotic automation is expected to advance at a 14.9% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles captured 34.26% of the robotics CNC turning centers market share in 2025, while medical devices and surgical instruments are projected to grow at a 17.6% CAGR through 2031.

- By geography, Asia Pacific held 45.21% of the robotics CNC turning centers market share in 2025 and is projected to expand at a 14.9% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robotics CNC Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Costs and Skilled-Operator Shortage Accelerating Robotic Tending Adoption | +2.8% | Global, most acute in North America, Europe, Japan, and South Korea | Short term (≤ 2 years) |

| Growth of Lights-Out and Unmanned Shift Manufacturing | +2.1% | Global, most advanced in Japan, Germany, and the United States | Medium term (2-4 years) |

| Growing Complexity of Precision Components Driving Adoption of Robotic CNC Turning Cells | +1.8% | Global, concentrated in Germany, Japan, the United States, and core Asia-Pacific markets | Medium term (2-4 years) |

| Ramp-up of Next-Generation Aerospace Production Programs | +1.4% | North America and Europe primarily, with Asia-Pacific growing | Short term (≤ 2 years) |

| Declining Cost and Improved Accessibility of Collaborative Robots | +1.2% | Global, with high impact in SME-dense economies, including Germany, Japan, the United States, and China | Short term (≤ 2 years) |

| Government-backed Reshoring and Industrial Modernization Incentives | +0.9% | North America, Europe, Japan, India, and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Costs and Skilled-Operator Shortage Accelerating Robotic Tending Adoption

Manufacturing labor cost pressure has become one of the clearest supports for the robotics CNC turning centers market. United States Bureau of Labor Statistics data showed that manufacturing unit labor costs rose across all 20 covered three-digit NAICS manufacturing industries in 2025, with an average increase of 4.5%.[1]U.S. Bureau of Labor Statistics, “Productivity and Costs by Industry: Manufacturing and Mining Industries – 2025,” BLS News Release, bls.gov In CNC turning environments, that cost trend matters because skilled setup, loading, and tending work remains hard to scale when output schedules tighten. The robotics CNC turning centers market also gains momentum as automation shifts labor toward supervision, programming, and process control, making the remaining manual roles more specialized and harder to fill. The International Federation of Robotics identified labor shortage mitigation as one of the top global robotics trends for 2025, which supports the view that robotic tending is becoming a standard capacity response rather than a discretionary upgrade.[2]International Federation of Robotics, “World Robotics 2025 – Industrial Robots: Global Robot Demand in Factories Doubles Over 10 Years,” IFR Press Release, ifr.org

Growth of Lights-Out and Unmanned Shift Manufacturing

The robotics CNC turning centers market is also being driven by the wider use of lights-out production in turning cells. Automation, once limited to large aerospace and automotive plants, is now expanding into mid-sized job shops that aim to keep machines running through second shifts, weekends, and holiday periods. NIST published work in 2025 on an improved robotic workcell for operational technology research, demonstrating that unmanned discrete manufacturing has moved into active research and standards work rather than remaining a narrow plant-level experiment.[3]National Institute of Standards and Technology, “An Improved Robotic Workcell for Operational Technology (OT) Research,” NIST, nist.gov The practical issue is no longer whether unattended turning is possible, but whether fixturing, grippers, and repeatable workholding can support stable batch changes without manual resets. In the robotics CNC turning centers market, plants that solve that problem can spread capital over more machine hours, while those that do not still bear the cost of automation without capturing full utilization gains.

Growing Complexity of Precision Components Driving Adoption of Robotic CNC Turning Cells

The robotics CNC turning centers market is benefiting from higher demand for parts with tighter tolerances and more complex geometries. In aerospace and medical production, quality systems such as AS9100D and ISO 13485 require documented process control, while many critical features operate within very tight dimensional ranges. Robotic loading helps because part placement, handling force, and cycle consistency are easier to repeat than in a manual tending setup, especially for thin shafts and other parts that are sensitive to distortion or unstable clamping. That is why the robotics CNC turning centers market is seeing stronger demand for multitasking cells that can perform turning, milling, and indexed operations within a single controlled setup.

Ramp-up of Next-Generation Aerospace Production Programs

Aerospace output is creating a direct volume tailwind for the robotics CNC turning centers market. Lockheed Martin reported record F-35 deliveries of 191 aircraft in 2025, following the September 2025 finalization of Lots 18 and 19 contracts covering up to 296 aircraft valued at USD 24 billion. Airbus stated that it is progressing toward a rate of 70 to 75 A320-family aircraft per month by the end of 2027, indicating sustained demand for precision-machined components throughout the supply chain. Boeing also communicated its long-term 737 MAX target of 63 aircraft per month, with current production stabilizing at 47 per month as supplier and sequencing constraints are worked through. In the robotics CNC turning centers market, this matters because more aerospace suppliers now treat robotic cell capability as a baseline requirement when they evaluate production readiness for growth programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Investment for Integrated Robotic Cells | -1.9% | Global, most constraining in SME-heavy markets, including South America, Middle East and Africa, and Southeast Asia | Short term (≤ 2 years) |

| Lack of Standardized Robot-CNC Controller Interfaces | -1.5% | Global | Medium term (2-4 years) |

| Cybersecurity Exposure of Networked Robotic-CNC Systems | -1.1% | Global, most acute in interconnected facilities and defense-adjacent manufacturing | Medium term (2-4 years) |

| Safety Certification and Regulatory Compliance Complexity | -0.8% | Global, intensified in the EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Investment for Integrated Robotic Cells

High initial spending remains the clearest limit on wider adoption in the robotics CNC turning centers market. A full robotic cell includes the turning center, the robot, end-of-arm tooling, safety systems, software, and installation work, so the investment case depends on high machine utilization and stable order flow. Smaller contract manufacturers often hesitate because the payback can stretch when commissioning takes longer than expected or when part families shift faster than expected. This becomes even harder in mixed-production environments, where dedicated automation has to justify itself across batches with uneven volumes. New financing models such as leasing and service-based automation may help over time, but they still have limited reach among the smaller firms that make up much of the global turning base.

Lack of Standardized Robot-CNC Controller Interfaces

The robotics CNC turning centers market also faces a structural drag from interface fragmentation between robots and CNC platforms. ISO 21919 was created to support automated machine tending, and the umati (universal machine technology interface) initiative has advanced OPC UA for Machine Tools as a common path for semantic data exchange. Even with that progress, system integrators still work across OPC UA, MTConnect, and proprietary controller environments, so each new robot-machine pairing often requires custom engineering. This constraint is particularly significant in retrofit applications, where the required engineering effort can reduce the economic viability of automating older yet still serviceable turning centers. Until broader standardization is achieved, the robotics CNC turning centers market is expected to record slower retrofit conversion than the installed base may otherwise indicate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Multi-Tasking Configurations Redefine Turning Cell Economics

Horizontal robotic turning centers held 52.41% of the global market in 2025, making them the largest machine format in the robotics CNC turning centers market. Their lead stems from a practical advantage: horizontal layouts work well with bar feeders, robot loaders, automatic tool changes, and modular storage systems that support steady, unattended cycles. Vertical turning centers continue to serve large-diameter and heavy-part work where gravity helps with seating, chucking consistency, and fixture stability during robotic loading. Multi-tasking robotic turning centers are projected to grow at a 17.1% CAGR from 2026 to 2031, making them the fastest-growing machine type in the robotics CNC turning centers market.

That growth reflects a broader change in how plants measure value from automation. Buyers are now comparing a multi-tasking robotic cell to the combined costs of several machines, more operators, extra floor space, and the work-in-progress inventory created by moving parts between steps. In aerospace and medical production, that comparison often favors single-setup machining because feature relationships are easier to protect when the part remains in a single controlled cell. DMG MORI’s NTX 3rd Generation launch in September 2025 demonstrated how machine builders are designing mill-turn platforms with built-in automation compatibility from the start. That product direction supports the robotics CNC turning centers market by lowering commissioning effort and reducing the penalty that used to come with complex multi-function cells.

By Robot Type: Cobots Unlock Automation for High-Mix Job Shops

Articulated robots accounted for 54.62% of the robotics CNC turning centers market in 2025, which kept them in the lead among robot formats. Their position reflects clear operational strengths in reach, payload, cycle speed, and the ability to serve multiple spindles or process points from a single cell. They also fit high-volume environments where deburring, marking, or gauging can be added inside the same work envelope. Gantry and Cartesian robots still hold value in large-part turning because they offer structural stiffness and straightforward motion for heavy payload work.

Collaborative robots are forecast to grow at a 18% CAGR from 2026 to 2031, making them the fastest-growing segment of the robotics CNC turning centers market. IFR reported that cobot installations rose 12% in 2024 to 64,500 units, while their share of global industrial robot installations reached 12% and more than doubled from 2020. That increase matters most in high-mix job shops, where shorter runs and more frequent changeovers make simple programming and compact deployment more valuable than peak speed. ISO 10218-2:2025 also supports the wider use of collaborative setups under properly risk-assessed configurations, helping first-time automation buyers approach the robotics CNC turning centers market with a lower integration barrier.

By Robot Integration Type: Retrofit Market Accelerates as Installed Base Grows

OEM-integrated robotic turning cells held 60.72% of the market in 2025, which made them the largest integration route in the robotics CNC turning centers market. Buyers favor these packages because the machine builder owns the integration logic, assumes system-level responsibility, and usually provides a single warranty path for the entire cell. That reduces project risk for plants that want quick deployment and limited internal engineering involvement. DMG MORI’s Robo2Go 3rd Generation, introduced in January 2026, aligns with this direction with a plug-and-work design and a 50% increase in workpiece storage capacity.

Retrofit/aftermarket robotic automation is forecast to grow at a 14.9% CAGR through 2031, indicating that the installed base remains a major opportunity in the robotics CNC turning centers market. Many turning machines bought during the 2015 to 2022 investment cycle still have useful mechanical life, but they need automated loading if operators want higher output per shift. That creates a strong business case when the machine platform is sound, and demand is steady. The challenge is that interface customization still increases retrofit costs, which is why the robotics CNC turning centers market depends heavily on broader controller standardization before retrofit volumes can scale more quickly. As more OEMs align with common communication frameworks, retrofit economics should improve, and the reachable base should expand.

By End-User Industry: Medical Devices Outpacing Automotive on Growth Rate

Automotive and commercial vehicles accounted for 34.26% of the robotics CNC turning centers market in 2025, maintaining the segment's lead among end users. That lead reflects years of investment in automated production for shafts, housings, suspension parts, and other repeatable turned components. The move toward electric vehicles has not weakened this demand base, because EV programs still require precision-turned housings, fittings, and rotating parts with consistent quality. IFR noted that 63% of industrial robot installations in Mexico in 2024 went to the automotive sector, underscoring the continued deepening of automation's role in regional vehicle manufacturing.

Medical devices and surgical instruments are projected to grow at a 17.6% CAGR from 2026 to 2031, making them the fastest-growing end-user segment in the robotics CNC turning centers market. This segment depends on very tight tolerances, full traceability, and stable process capability under ISO 13485 and FDA-style quality systems, so robotic consistency carries clear value. The shift of some medical manufacturing toward North America and Europe also supports the development of new automated facilities designed from the beginning for cell-based production. Aerospace and defense remain important because long production contracts and qualification requirements favor controlled, repeatable machining environments. Oil and gas, energy, electronics, semiconductor equipment, and general industrial demand also add volume to the robotics CNC turning centers market, especially where part-damage risk and handling repeatability affect yield.

Geography Analysis

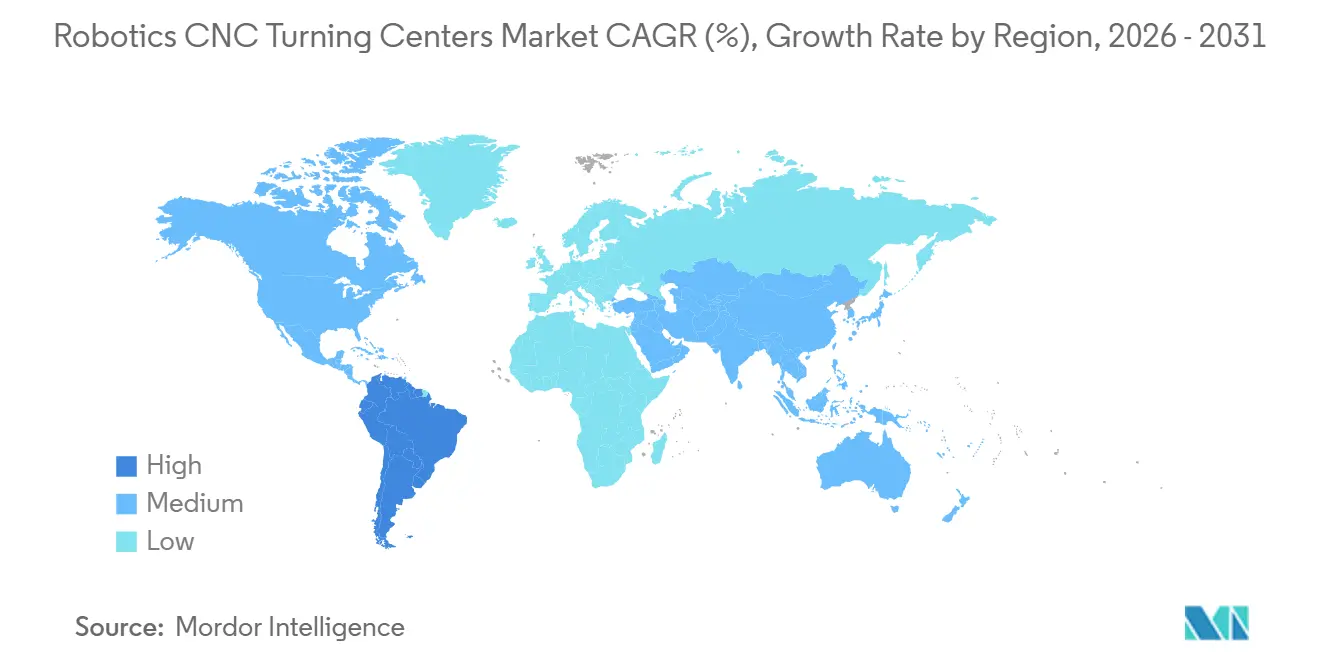

Asia Pacific held 45.21% of the robotics CNC turning centers market share in 2025 and is expected to remain the fastest-growing regional segment with a CAGR 14.9% through 2031. The region benefits from dense automotive, electronics, and precision engineering manufacturing clusters across China, Japan, South Korea, and India. China led global industrial robot installations in 2024 with 295,000 units, the highest annual total ever recorded for a single country. Japan recorded 44,500 industrial robot installations in 2024 and continued to lead in robot density, which supports wider use of robotic turning cells in lights-out production. India reached a record 9,100 robot installations in 2024, while South Korea and Southeast Asian markets such as Indonesia, Vietnam, Thailand, and Malaysia continue to see strong demand in electronics and automotive sub-assembly manufacturing.

Europe and North America remain technology-intensive regions in the robotics CNC turning centers market, with demand centered on software-rich, flexible, and safety-certified turning cells. Germany was the largest European market for industrial robots in 2024, with 26,982 installations, supporting robotic CNC turning adoption across toolmaking, automotive Tier 1 suppliers, and precision engineering applications. German machine tool order intake showed its first quarterly recovery signal in Q4 2025, rising 4% year over year after a prolonged period of weak domestic demand. North America continues to benefit from the CHIPS for America program, advanced manufacturing incentives, and defense industrial expansion policies that require greater domestic precision machining capacity. The Reshoring Initiative documented 244,000 United States manufacturing job announcements through reshoring and foreign direct investment in 2024, reinforcing the case for new turning capacity and higher automation intensity.

South America remains an emerging opportunity in the robotics CNC turning centers market, supported by automotive nearshoring, commodity-linked precision machining demand, and industrial modernization efforts. Brazil anchors regional demand as the largest manufacturing base, with automotive assembly driving much of the immediate need for robotic turning cells. The Middle East and Africa market remains smaller, but industrial strategies in Saudi Arabia and the United Arab Emirates are widening interest in domestic precision manufacturing capacity. South Africa adds support through its automotive assembly and mining equipment base, and planned investments in defense, and energy are expected to lift regional adoption through the forecast period.

Competitive Landscape

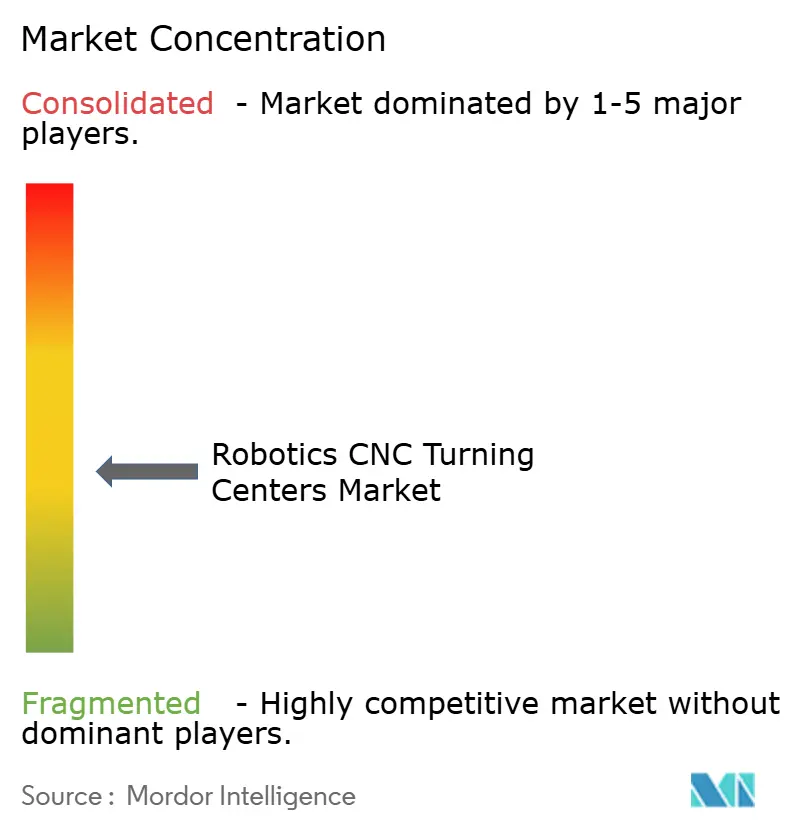

The robotics CNC turning centers market remains moderately fragmented, with competition led by major machine tool manufacturers that combine turning center design, automation readiness, controls integration, and service support. The leading participants in this market are Yamazaki Mazak Corporation, DMG MORI Co., Ltd., Okuma Corporation, DN Solutions Co., Ltd., and JTEKT Corporation. These companies hold strong positions because they offer broad portfolios of turning centers, established global distribution networks, and growing support for robot-ready production cells. Hyundai WIA Corporation, INDEX-Werke GmbH & Co. KG, EMAG GmbH & Co. KG, and Hwacheon Machinery Co., Ltd. also remain visible competitors across precision turning, multi-axis machining, and application-specific production systems. The robotics CNC turning centers market is shaped by suppliers that can reduce integration time, improve reliability of unattended machining, and support high-mix manufacturing with flexible automation packages.

Competition also extends across companies with strong positions in general CNC equipment, precision machining systems, and robotic automation support. Haas Automation, Inc., Hardinge Inc., Nakamura-Tome, etc., contribute to the competitive structure through machine tools, robotic platforms, motion systems, and factory automation capabilities that support robotic turning cells. In practice, buyers in the robotics CNC turning centers market often compare not only spindle performance and turning accuracy, but also software usability, robot interface readiness, cell footprint, and after-sales responsiveness. This keeps the market open to both large global brands and specialized regional suppliers that can address precise production needs.

Recent company actions continue to show how suppliers are trying to strengthen their positions through automation-oriented product development. DMG MORI introduced the Robo2Go 3rd Generation in January 2026 with up to 50% more workpiece storage capacity, reflecting a clear push toward faster deployment and longer autonomous operating windows. The company also launched the CTX 450 4A in January 2026 as a compact turning platform designed for 6-sided complete machining with compatibility for autonomous 3-shift robotic operation. DMG MORI further expanded its automation-ready offering with the NTX 3rd Generation mill-turn series in September 2025, aimed at aerospace, medical device, EV, and semiconductor production environments. Across the robotics CNC turning centers market, this pattern suggests that suppliers are competing less on standalone machines and more on complete cell readiness, integration simplicity, and reliable unattended production capability.

Robotics CNC Turning Centers Industry Leaders

Yamazaki Mazak Corporation

DMG MORI Co., Ltd.

Okuma Corporation

DN Solutions Co., Ltd.

JTEKT Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: KUKA Robotics announced that it would showcase robotic machine tending, material handling, and robotic milling solutions at IMTS 2026 alongside OEM and integration partners, demonstrating scalable automation packages for CNC machine tools.

- January 2026: DMG MORI unveiled the CTX 450 4A universal turning center at its Pfronten Open House as a world premiere, featuring dual spindles, up to 36 tool positions, 6 µm positioning accuracy, a 10.8 m² footprint, and automation readiness, including compatibility with Robo2Go Turning.

- January 2026: DMG MORI introduced the 3rd Generation of its Robo2Go system, expanding workpiece storage capacity by up to 50% relative to the previous generation, with redesigned installation layouts that reduce commissioning time for robot-tended turning and milling cells.

Global Robotics CNC Turning Centers Market Report Scope

The Robotics CNC Turning Centers Market is Segmented by Machine Type (Horizontal Robotic Turning Centers, and More), by Robot Type (Articulated Robots, and More), by Robot Integration Type (OEM-Integrated Robotic Turning Cells, and More), by End-User Industry (Oil, Gas, and Energy, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers |

| Multi-Tasking Robotic Turning Centers |

| Others |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Gantry/Cartesian Robots |

| OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Oil, Gas, and Energy |

| Electrical, Electronics and Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Machine Type | Horizontal Robotic Turning Centers | |

| Vertical Robotic Turning Centers | ||

| Multi-Tasking Robotic Turning Centers | ||

| Others | ||

| By Robot Type | Articulated Robots | |

| Collaborative Robots (Cobots) | ||

| Gantry/Cartesian Robots | ||

| By Robot Integration Type | OEM-Integrated Robotic Turning Cells | |

| Retrofit/Aftermarket Robotic Automation | ||

| By End-User Industry | Automotive and Commercial Vehicles | |

| Aerospace & Defense | ||

| Medical Devices and Surgical Instruments | ||

| Oil, Gas, and Energy | ||

| Electrical, Electronics and Semiconductor Equipment | ||

| General Industrial Machinery | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the expected value of robotics CNC turning centers by 2031?

The robotics CNC turning centers market is forecast to reach USD 4.3 billion by 2031, up from USD 2.5 billion in 2026, with a 11.4% CAGR from 2026 to 2031.

Which region leads global demand for robotic CNC turning centers?

Asia-Pacific led in 2025 with a 45.21% share, and recording a fastest growth rate of 14.9% CAGR, supported by high robot installations in China, Japan, and South Korea, as well as rising adoption in India.

Which machine type is growing the fastest in robotic turning cells?

Multi-tasking robotic turning centers are the fastest-growing machine type, with a projected CAGR of 17.1% through 2031.

Why are manufacturers adopting robotic turning cells faster now?

Rising labor costs, difficulty finding skilled operators, demand for lights-out production, and stricter precision requirements are pushing more factories toward robotic tending.

Which end-user segment is expanding the quickest?

Medical devices and surgical instruments are expected to record the fastest growth, with a 17.6% CAGR from 2026 to 2031.

What is the main barrier to broader adoption in small and mid-sized plants?

The largest barrier remains the high upfront cost of a full robotic cell, especially when utilization levels or product volumes are not stable enough to shorten the payback period.

Page last updated on: