Rigid Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.29 Billion |

| Market Size (2031) | USD 13.09 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

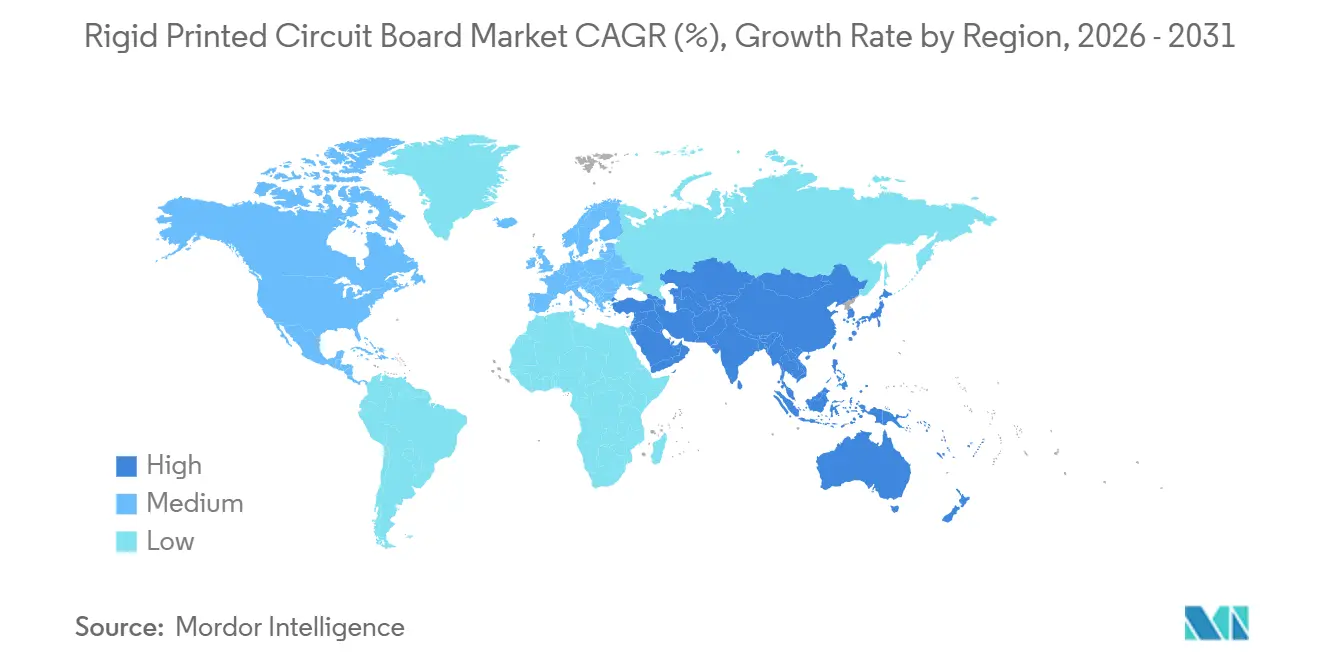

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

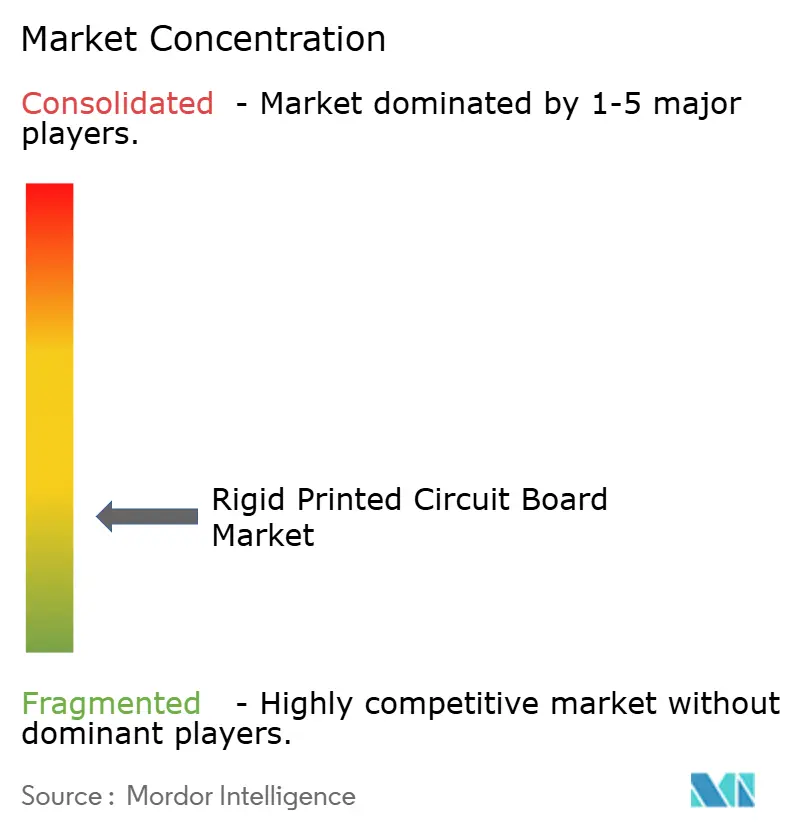

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rigid Printed Circuit Board Market Analysis by Mordor Intelligence

The rigid printed circuit board market size was valued at USD 9.78 billion in 2025 and expected to grow from USD 10.29 billion in 2026 to reach USD 13.09 billion by 2031, at a CAGR of 4.93% during the forecast period (2026-2031). This measured trajectory conceals a pivot toward high-frequency designs and sustainability mandates that shift material demand, alter regional cost structures, and raise competitive barriers. Telecommunications infrastructure is moving from sub-6 gigahertz to millimeter-wave frequencies, boosting the content value of each board and enabling the rigid PCB market to capture incremental pricing even as consumer-electronics volumes fluctuate. Automotive and EV programs are scaling multilayer boards that consolidate distributed control units, while industrial IoT nodes compress sensors and logic onto postage-stamp footprints that require fine-line high-density interconnect. Vertical integration, semi-additive process adoption, and halogen-free laminate requirements now differentiate fabricators more sharply than capacity scale, creating a strategic opportunity for suppliers that co-develop materials and processes with equipment makers.

Key Report Takeaways

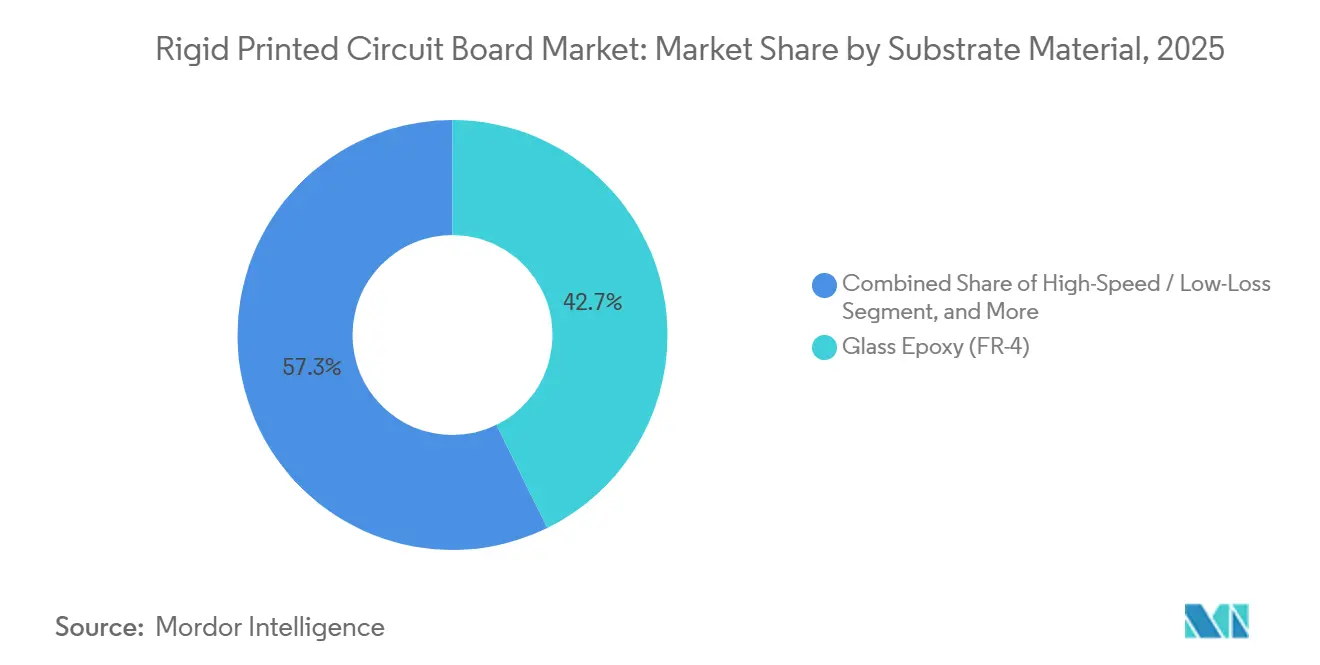

- By substrate material, glass-epoxy FR-4 led with 42.74% of the rigid PCB market share in 2025, while high-speed laminates are growing at a 5.71% CAGR through 2031.

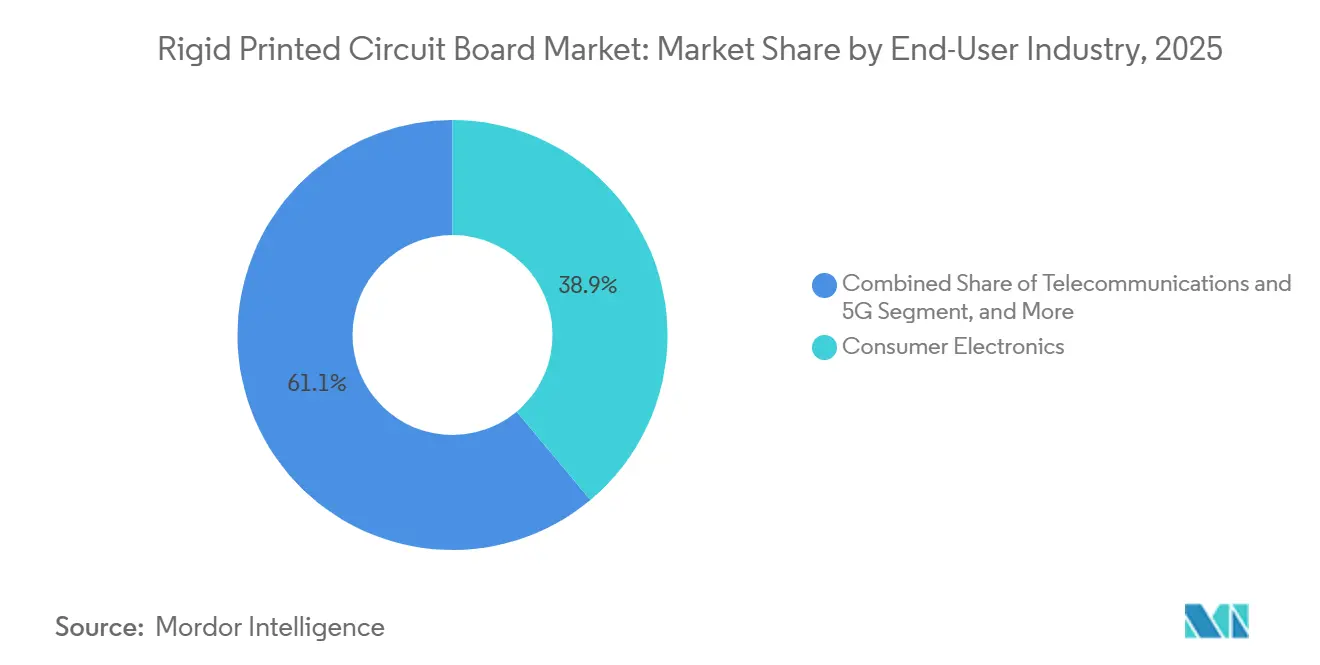

- By end-user industry, consumer electronics accounted for 38.92% of the rigid PCB market share in 2025, whereas telecommunications and 5G infrastructure are the fastest-growing segments at 6.33% CAGR.

- By geography, Asia Pacific accounted for 83.47% of the rigid PCB market share in 2025 and is expanding at a 5.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rigid Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in consumer electronics demand leading to high PCB volumes | +0.8% | Global, with concentration in Asia Pacific manufacturing hubs (China, Vietnam, India) | Short term (≤ 2 years) |

| Rapid expansion of 5G infrastructure requiring high-frequency rigid PCBs | +1.2% | Global, led by China, India, North America, and Europe | Medium term (2-4 years) |

| Rising adoption of ADAS and EV power electronics in automotive | +1.1% | Global, with early gains in Europe, North America, and China | Medium term (2-4 years) |

| Growing use of glass-glass rigid PCBs in solar PV inverter boards | +0.6% | Global, strongest in China, India, and Middle East solar installations | Long term (≥ 4 years) |

| Miniaturized industrial IoT sensors driving demand for fine-line HDI rigid boards | +0.7% | Global, with industrial automation focus in Germany, Japan, and United States | Medium term (2-4 years) |

| OEM push for halogen-free laminates amid Scope 3 emission reporting | +0.5% | North America and Europe, with spillover to Asia Pacific supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of 5G Infrastructure Requiring High-Frequency Rigid PCBs

Global operators installed more than 3.7 million 5G base stations by the end of 2025, with China accounting for the majority and India adding 200,000 sites in the same year. Each radio unit integrates four to six rigid boards that require dielectric constants below 3.5 and dissipation factors below 0.005 to maintain an insertion loss of 1 decibel per meter at millimeter-wave bands.[1]Rogers Corporation, “RO4000 Series High Frequency Circuit Materials,” Rogerscorp.com Low-loss laminates such as RO4000 command a 15-20% premium over FR-4, yet adoption is mandatory for phased-array antennas that electronically steer beams. Equipment makers are also specifying 2-3 ounce copper for power-amplifier stages, extending cycle time by as much as 18 hours and tightening impedance control to ±5%. These requirements help the rigid printed circuit board (PCB) market capture higher average selling prices, enabling 6.33% CAGR for the telecommunications vertical, 140 basis points above total market growth.

Rising Adoption of ADAS and EV Power Electronics in Automotive

Automotive board shipments climbed 6.2% year-on-year in Q3 2025 as zone controllers replaced distributed ECUs, consolidating multiple functions onto 12- to 16-layer boards measuring 300 × 400 millimeters. Radar modules operating at 77 gigahertz use substrates such as RO3003 that maintain dielectric properties from –40 to 125 degrees Celsius, while lidar processors require microvias below 100 micrometers.[2]Texas Instruments, “Automotive Radar Reference Design,” Ti.com Silicon-carbide inverters in EVs push junction temperatures above 175 degrees Celsius, driving demand for polyimide or ceramic-filled FR-4 with glass transition temperatures above 180 degrees Celsius. Meiko Electronics reported automotive PCB revenue up 14.2% in fiscal 2023, illustrating the resilience of this end market.

OEM Push for Halogen-Free Laminates Amid Scope 3 Emission Reporting

More than 4,000 firms must disclose Scope 3 emissions from fiscal 2026 under the Science Based Targets initiative, prompting a shift to halogen-free boards that cut end-of-life emissions by roughly 30%.[3]Environmental Protection Agency, “Scope 3 Emission Reporting Guidelines,” Epa.gov Phosphorus-based flame retardants absorb more moisture, so fabricators extend bake-out protocols by up to six hours to avoid delamination. Intel mandated halogen-free materials for new server platforms in 2024, cascading specifications to tier-two suppliers within 18 months. IPC-4101 now includes phosphorus content and moisture absorption tests, standardizing qualification and favoring vertically integrated shops. The rigid printed circuit board (PCB) market, therefore, rewards suppliers that co-engineer laminate chemistries with OEMs.

Miniaturized Industrial IoT Sensors Driving Demand for Fine-Line HDI Rigid Boards

Industrial IoT nodes shrink to fit inside motor housings, valves, and conveyor bearings, squeezing complete systems onto boards as small as 20 × 30 millimeters. Achieving densities below 75 micrometer line-and-space and stacked microvias with 0.8:1 aspect ratios forces the shift from subtractive etch to semi-additive processes. Semi-additive plating reduces copper waste by 40% and enables trace widths down to 25 micrometers, a capability held by fewer than 30% of global fabricators. Germany’s automation sector drove 9-11% growth in this niche, with Siemens and ABB leading adoption. Similar momentum is evident in Japan and North America, sustaining incremental demand for advanced HDI capabilities and reinforcing pricing power for specialists.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical slowdown in smartphone and PC shipments | -0.9% | Global, most pronounced in China and North America consumer markets | Short term (≤ 2 years) |

| Supply chain volatility for copper foil and epoxy resins | -0.7% | Global, with acute pressure in Europe and North America due to tariffs and logistics | Short term (≤ 2 years) |

| Board warpage failures in advanced packaging limiting yield | -0.4% | Asia Pacific semiconductor hubs (Taiwan, South Korea, Japan, China) | Medium term (2-4 years) |

| Escalating energy tariffs for PCB fabrication facilities in Europe | -0.3% | Europe, particularly Germany, Netherlands, and Central European manufacturing corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyclical Slowdown in Smartphone and PC Shipments

IPC reported North American PCB shipments down 3.1% year-on-year in March 2025 as handset and PC volumes slid, with smartphone units off 6.8% in May 2024 and PCs down 24.1% in September 2024 before stabilizing. Inventories peaked at 14 weeks in mid-2024, well above the 8- to 10-week norm, triggering a destocking cycle that suppressed orders. The book-to-bill ratio rebounded to 1.24 by June 2025, but replacement demand remains constrained by longer smartphone refresh cycles, now 3.2 years in mature markets, and a one-time enterprise PC upgrade ahead of Windows 10 end-of-support in October 2025. Short-term revenue pressure, therefore, tempers the otherwise positive outlook for the rigid printed circuit board (PCB) market.

Supply Chain Volatility for Copper Foil and Epoxy Resins

Copper prices rose from USD 9,173 per metric ton in Q4 2024 to USD 11,114 in Q4 2025 and are projected to hit USD 12,500 in Q2 2026 as a 330-kiloton deficit emerges. Epoxy resin supply also tightened after European Union anti-dumping probes against Asian imports lifted prices 1.8% month-on-month in May 2024. Fabricators pass through raw-material hikes with a 60-90-day lag, compressing margins and discouraging long-term fixed-price contracts. Mid-tier shops with limited working capital bear the brunt, potentially delaying investments in semi-additive lines that the rigid printed circuit board (PCB) market increasingly requires.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: High-Speed Laminates Gain Share as Frequency Demands Rise

High-speed and low-loss materials grew 5.71% annually through 2025, narrowing the gap with FR-4, which still accounted for 42.74% of revenue. The rigid printed circuit board market for high-speed laminates is expanding because 5G antennas and automotive radar cannot meet insertion-loss budgets on standard epoxy-glass laminates. RO4000 laminates, with a dielectric constant of 3.38 and dissipation factor of 0.0027 at 10 gigahertz, cost 15-20% more yet remain non-negotiable for millimeter-wave boards. Polyimide substrates address thermal excursions above 200 degrees Celsius in aerospace avionics and down-hole sensors, while metal-core and ceramic-filled composites manage heat in LED lighting and power modules.

Fabrication complexity steers volume toward advanced specialists. Semi-additive plating and laser-drilled microvias raise capex, but they also consolidate rigid printed circuit board market share among shops that can control copper-seed uniformity within ±5%. IPC-4101 revisions now cover high-frequency tests, easing qualification for new chemistries and accelerating the shift in material mix. As telecommunications and automotive applications expand faster than consumer electronics, the high-speed segment’s share of the rigid printed circuit board market will widen.

By End-User Industry: Telecommunications and Automotive Outpace Legacy Electronics

Telecommunications posted the fastest growth at a 6.33% CAGR, leveraging 4-6 boards per radio unit and premium, low-loss materials that raise average selling prices by up to 30%. Automotive and EV programs delivered 6.2% year-on-year volume growth in Q3 2025, driven by zone controllers and 77-gigahertz radar. Consumer electronics still accounted for 38.92% of 2025 sales but faced unit volatility. Computing and data centers grew 8.1% in the same period, powered by AI accelerator cards that stack ASICs on rigid interposers with microvias under 100 micrometers, a configuration commanding a larger share of the rigid printed circuit board market.

Industrial drives, PLCs, and solar inverters bolster demand for thick-copper boards that dissipate heat from high-current traces, as global solar additions exceeded 500 gigawatts in 2024, and each megawatt requires 0.8 square meters of inverter boards. Healthcare, aerospace, and defense contribute smaller volumes but steady profitability because of stringent reliability demands. These shifts collectively diversify the rigid printed circuit board market and reduce reliance on handset cycles.

Geography Analysis

Asia Pacific delivered 83.47% of 2025 revenue and is forecast to advance at 5.79% CAGR to 2031, anchored by China’s 54% production share and Taiwan’s dominance in ABF substrates. Shennan Circuits posted CNY 15.2 billion (USD 2.1 billion) in 2023 revenue, while Kinwong generated CNY 8.7 billion (USD 1.2 billion), both citing automotive and industrial gains. Japan’s Meiko focuses on automotive quality niches, reporting a 14.2% increase in automotive revenue in fiscal 2023. Samsung Electro-Mechanics and LG Innotek leverage captive demand and plan KRW 500 billion (USD 375 million) FC-BGA expansions by 2026.

Amidst the China-plus-one strategies, India and Southeast Asia are reaping the rewards. Under the Production-Linked Incentive program, Foxconn, Dixon, and Amber ramped up their capacities in India. Meanwhile, Zhen Ding made a significant move, pouring TWD 15 billion (USD 465 million) into Vietnam, targeting telecommunication and automotive boards. Opting for Malaysia over Europe, AT&S channeled a hefty EUR 2 billion (USD 2.2 billion) into new IC-substrate capacity, a decision swayed by energy-price differentials.

North America captured a mid-single-digit share, buoyed by aerospace and defense builds. TTM saw its aerospace revenue rise 7.5% year-on-year in Q3 2025, and the IPC book-to-bill ratio of 1.24 indicates recovery. Europe suffers from industrial electricity prices of EUR 197 per megawatt-hour in H1 2024 (USD 220), eroding competitiveness and prompting some plants to relocate capacity. Unless policy reforms ease tariffs, the European share in the rigid PCB market could slip further despite strong automotive demand.

Competitive Landscape

The rigid PCB market remains moderately concentrated, with the top 20 fabricators accounting for about 60% of 2025 revenue, while hundreds of regional shops compete on speed and engineering support. Scale alone is no longer decisive, because vertical integration and process know-how now separate leaders from fast followers. AT and S illustrate this shift: its new Kulim 2 plant pairs captive laminate production with sub-30-micrometer semi-additive lines, letting the company co-develop materials with data-center customers and capture higher packaging margins. Samsung Electro-Mechanics and LG Innotek apply a different model, using in-house smartphone and automotive demand to stabilize factory loads and justify large investments such as the KRW 500 billion FC-BGA expansion scheduled for completion in 2026.

Technology adoption is the second key divider. Patent filings for semi-additive processes rose 18% in 2024, signaling a race to hit sub-25-micrometer line-and-space rules without yield loss. Early movers report yields above 95% on fine-line HDI boards, whereas shops that still etch copper from foil face chronic undercut and lower throughput. TTM Technologies leverages AS9100 and ITAR credentials to serve aerospace and defense programs that demand this advanced capability, helping the company lift aerospace revenue 7.5% year-on-year in the third quarter of 2025. Meiko Electronics targets automotive zone-controller volumes, pushing microvia reliability while retaining cost discipline, and grew automotive PCB revenue 14.2% in fiscal 2023.

Strategic reshoring and diversification add a third layer of competition. Jabil and Sanmina are backward-integrating into fabrication to secure supply for healthcare and industrial customers, with Jabil redeploying USD 200 million in annual savings from plant closures toward new HDI lines. Zhen Ding and Unimicron spread risk through Southeast Asian capacity, responding to customer requests for China-plus-one sourcing and easing tariff exposure. European players such as AT and S, and Schweizer Electronic mitigate energy-price volatility by placing incremental investment in Malaysia and Thailand rather than adding European square footage, a choice that could erode local share unless policy reforms narrow the cost gap. The resulting landscape rewards firms that combine geographic flexibility, materials science partnerships, and process leadership, while mid-tier vendors without these levers increasingly specialize in short-run consumer electronics or exit the market entirely.

Rigid Printed Circuit Board Industry Leaders

Nippon Mektron Ltd.

Zhen Ding Technology Holding Limited

TTM Technologies Inc.

Unimicron Technology Corp.

HannStar Board Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Electro-Mechanics confirmed that its Busan FC-BGA expansion remains on schedule for Q2 2026 completion.

- October 2025: AT&S commenced production at the Kulim 2 plant in Malaysia, a EUR 2 billion (USD 2.2 billion) advanced IC-substrate facility.

- September 2025: Zhen Ding Technology completed phase one of its TWD 15 billion (USD 465 million) Vietnam campus for 16-layer rigid boards.

- June 2025: TTM Technologies reported USD 599 million Q3 2025 sales, with aerospace and defense up 7.5% and data-center boards up 8.1%.

Global Rigid Printed Circuit Board Market Report Scope

The Rigid Printed Circuit Board Market Report is Segmented by Substrate Material (Glass Epoxy (FR-4), High-Speed and Low-Loss, Polyimide (PI), Other Substrate Materials), End-User Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-User Industries), and Geography (North America, Europe, Asia Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Other Substrate Materials | ||

| By End-user Industry | Consumer Electronics | |

| Computing and Data Centers | ||

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Industrial and Power | ||

| Healthcare / Medical | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the current value of the rigid PCB market?

The rigid PCB market size reached USD 10.29 billion in 2026 and is forecast to grow to USD 13.09 billion by 2031.

Which end-user vertical is expanding the fastest?

Telecommunications and 5G infrastructure leads growth at a 6.33% CAGR through 2031, outpacing all other segments.

Why are high-speed laminates gaining share?

Millimeter-wave 5G radios and 77-gigahertz automotive radar need dielectric constants below 3.5 and dissipation factors under 0.005, performance not achievable with FR-4.

How are Scope 3 emission rules affecting board materials?

OEMs are mandating halogen-free laminates to reduce embodied emissions, favoring suppliers that can co-develop phosphorus-based flame-retardant systems.

Which region dominates production capacity?

Asia Pacific accounts for more than 80% of rigid PCB output, with China alone producing 54% of global volume and Taiwan leading in ABF substrates.

What process technology is critical for fine-line HDI boards?

Semi-additive plating, combined with laser-drilled microvias, enables trace widths down to 25 micrometers, supporting miniaturized industrial IoT sensors.

Page last updated on: