Rigid-Flex PCB Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

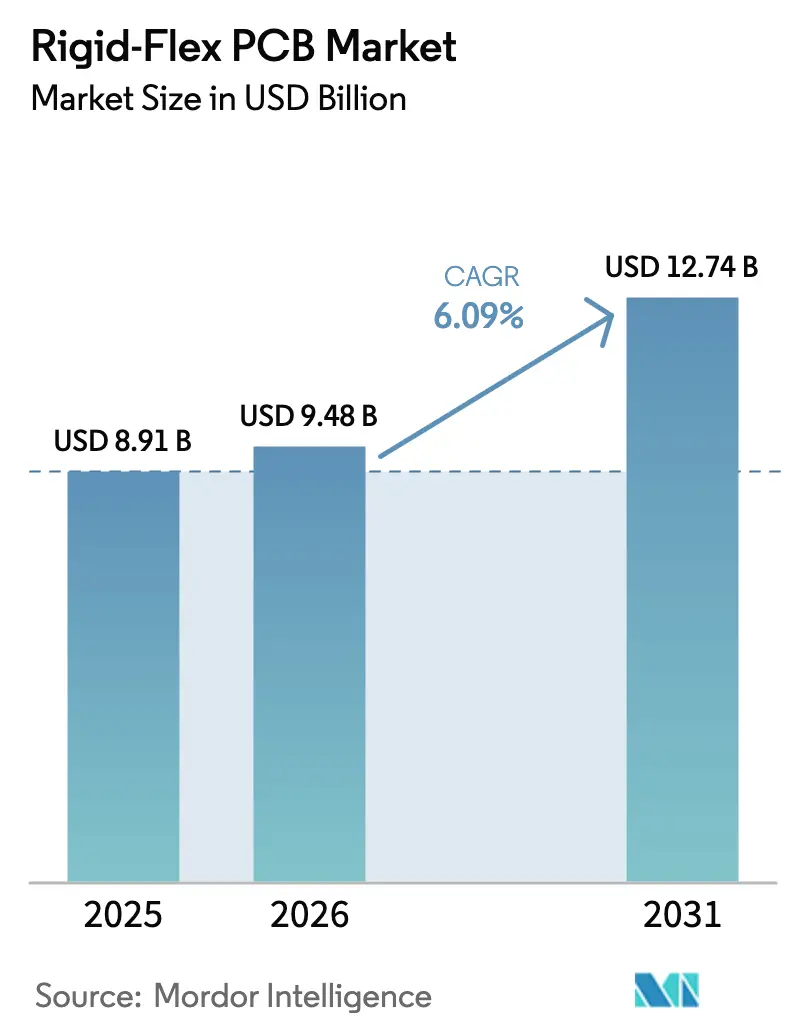

| Market Size (2026) | USD 9.48 Billion |

| Market Size (2031) | USD 12.74 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

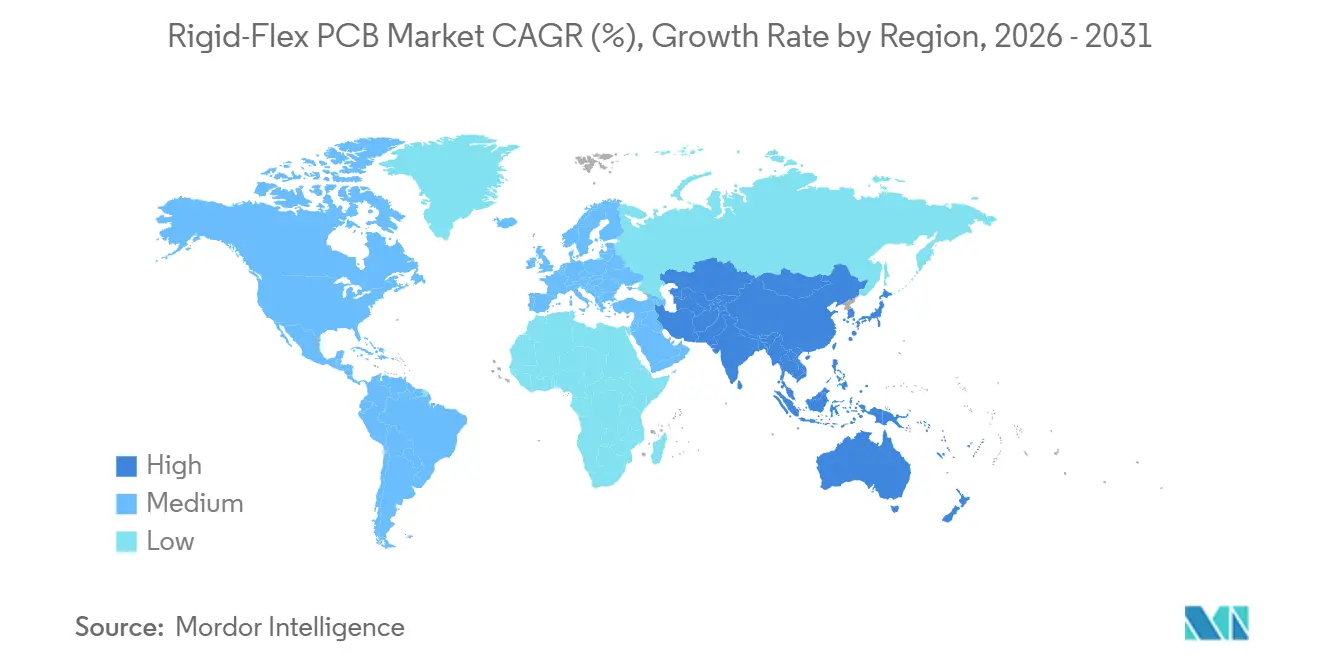

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rigid-Flex PCB Market Analysis by Mordor Intelligence

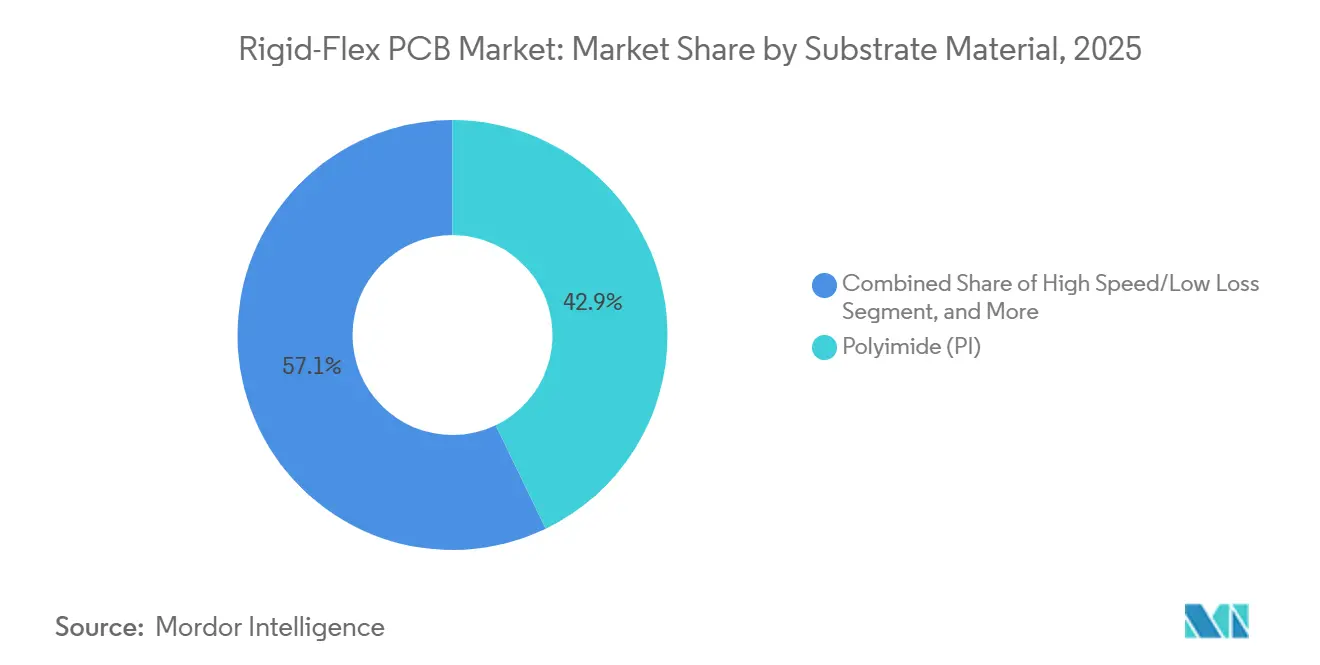

The Rigid-Flex Printed Circuit Board Market was valued at USD 8.91 billion in 2025 and expected to grow from USD 9.48 billion in 2026 to reach USD 12.74 billion by 2031, at a CAGR of 6.09% during the forecast period (2026-2031). Demand is accelerating as smartphone and tablet brands chase ultra-thin foldable designs, automakers move battery-management circuitry onto integrated boards, and 5G infrastructure designers specify low-loss signal paths above 28 GHz. Polyimide substrates captured 42.87% revenue in 2025 because they combine thermal stability with extreme bendability. Telecommunications and 5G applications are set to grow the fastest at 7.12% through 2031 due to densification of small-cell networks. Competitive pressure is intensifying as fabricators automate inspection and form joint ventures with film suppliers to secure constrained polyimide capacity.

Key Report Takeaways

- By substrate material, polyimide led with 42.87% of Rigid-Flex Printed Circuit Board market share in 2025 and is forecast to expand at a 6.53% CAGR to 2031.

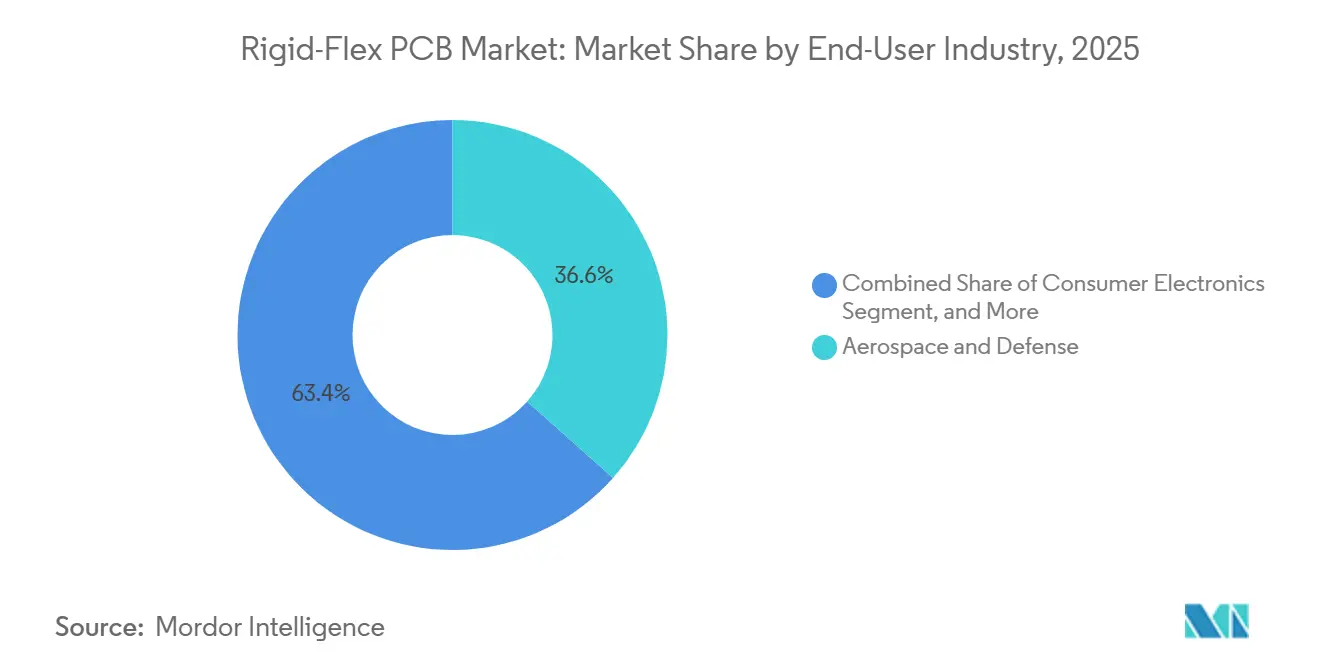

- By end-user industry, aerospace and defense held 36.58% revenue in 2025, while telecommunications and 5G is advancing at the highest 7.12% CAGR through 2031.

- By geography, Asia-Pacific accounted for 83.73% of global revenue in 2025 and is projected to accelerate at a 7.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rigid-Flex PCB Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for ultra-thin foldable consumer devices | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Rapid electrification of automobiles and EV battery management systems | +1.5% | Global, strongest in China, Europe, North America | Long term (≥ 4 years) |

| Migration to 5G and high-speed data centers requiring low-loss interconnects | +1.8% | Global, led by Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Regionalization of PCB supply chains in U.S. and EU to improve resilience | +0.7% | North America and Europe, spillover to Mexico and Eastern Europe | Long term (≥ 4 years) |

| Integration with advanced chiplet/Si-interposer packaging architectures | +0.9% | Asia-Pacific core, expanding to North America | Medium term (2-4 years) |

| Adoption of AI-driven EDA tools that shorten rigid-flex design cycles | +0.5% | Global, early adoption in North America, Europe, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Ultra-Thin Foldable Consumer Devices

Samsung shipped 12 million foldables in 2025, and Chinese brands added another 8 million, pushing the global installed base above 35 million units. Designs require bend radii of 1.5 mm and boards that endure more than 200,000 fold cycles, forcing a shift to polyimide films with elongation-at-break above 40%. The 2025 launches of the Google Pixel Fold and Motorola Razr validated the format, prompting collaborative PCB-display layouts that route high-speed differential pairs through flex zones without impedance jumps. Laser-drilled microvias and rolled-annealed copper foils that hold ductility under strain command a 20-30% premium, yet device makers accept the cost to keep products slim. Momentum around augmented-reality functions is likely to add even more flex regions inside future handsets, underpinning robust unit growth for the Rigid-Flex Printed Circuit Board market.

Rapid Electrification of Automobiles and EV Battery Management Systems

Tesla integrated rigid-flex boards into its 4680 packs, trimming interconnect length by 35% and improving thermal paths.[1]Wall Street Journal, “Tesla 4680 Battery Integration,” wsj.com General Motors is committed to implementing rigid-flex monitoring for all Ultium batteries by 2027 to reduce assembly steps and connector failures. BYD’s Blade Battery achieved a 15% weight reduction after adopting rigid-flex layouts. Over-the-air updates for battery firmware now travel through CAN-FD or Ethernet lines embedded in the flex stack. With global EV output targeting 20 million vehicles by 2028, the automotive industry is poised to become the second-largest segment of the Rigid-Flex Printed Circuit Board market, after the aerospace industry.

Migration to 5 G and High-Speed Data Centers

Massive-MIMO radios route RF traces from baseband to antenna arrays on rigid-flex substrates, improving link budgets by 0.3 dB compared with cable harnesses.[2]IEEE, “Massive MIMO Base Station PCB Requirements,” ieee.org Ericsson and Nokia both standardized the design for mid-band units launched in 2025. Hyperscale clouds are adopting liquid-crystal-polymer layers with dielectric constants below 3.0 to support 800-gigabit Ethernet channels. Although LCP costs roughly twice as much as polyimide, premium switches justify the outlay. Edge-computing nodes and small-cell radios extend demand to millions of additional boards, representing a USD 1.2 billion opportunity by 2030.

Regionalization of PCB Supply Chains in the U.S. and EU

The U.S. CHIPS and Science Act steered USD 3 billion toward advanced substrates, spurring TTM to allocate USD 150 million for a North Carolina rigid-flex line opening in 2027. Europe’s EUR 43 billion Chips Act enabled ATandS to break ground on a EUR 300 million (USD 330 million) plant in Austria for 20-layer automotive boards. While Western capacity remains a fraction of Asia, defense primes and automotive OEMs now prize traceable domestic supply over unit cost. Labor cost headwinds persist, yet incentives and export-control compliance reinforce a gradual move of the Rigid-Flex Printed Circuit Board market production closer to end users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polyimide film and copper foil pricing | -0.8% | Global, most acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Yield challenges in ultra-thin multilayer rigid-flex fabrication | -1.1% | Global, particularly impacting smaller fabricators | Medium term (2-4 years) |

| Signal-integrity losses above 28 GHz without LCP substrates | -0.4% | North America, Europe, advanced segments in Asia-Pacific | Medium term (2-4 years) |

| Stringent end-of-life recycling and RoHS/REACH compliance costs | -0.6% | Europe, North America, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polyimide Film and Copper Foil Pricing

Polyimide film prices climbed 18% between mid-2024 and early 2025 after outages reduced capacity by 15,000 t. Spot copper-foil quotes jumped from USD 12/kg to USD 16/kg as EV battery demand tightened supply. Fabricators operating on 60-day contracts saw margins compress by 200-300 basis points before repricing. Mid-tier Asian suppliers even reported negative earnings in late 2025. Vertical integration surged, with several fabricators buying equity in film producers to lock allocations. Price swings remain a near-term drag on the Rigid-Flex PCB market until new capacity stabilizes raw-material flows.

Yield Challenges in Ultra-Thin Multilayer Fabrication

First-pass yields for boards thinner than 0.3 mm still hover below 70% as delamination, via-barrel cracks, and impedance drift drive scrap. Sequential lamination demands ±25 µm alignment, forcing investment in laser registration and climate-controlled rooms. Each automated-optical-inspection module adds USD 5-8 million to line capital, a hurdle for smaller firms. AI control algorithms now tweak lamination temperature in real time, boosting yields 8-12 percentage points and cutting annual scrap by up to USD 3 million per site.[3]Cadence Design Systems, “AI-Driven Defect Detection,” cadence.com Even so, new entrants need 18-24 months to stabilize their processes, which is muting near-term capacity additions in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: Polyimide Continues to Dominate Performance-Driven Applications

Polyimide accounted for 42.87% of the Rigid-Flex PCB market share in 2025 and is projected to expand at a 6.53% CAGR through 2031, preserving its lead thanks to a glass-transition point above 300 °C and endurance beyond 200,000 flex cycles. High-speed or low-loss resins, such as modified epoxies and liquid-crystal polymers, followed at roughly 22%, fueled by 5G radios and 800-gigabit switches that run above 28 GHz.

Glass epoxy FR-4 retained about 18% of revenue in cost-sensitive industrial controls, while BT or ABF packaging resins accounted for 12% linked to chiplet substrates. Ceramic and metal-core composites filled a 6% niche for radar and LED modules. Device makers that specify total board thickness under 0.2 mm increasingly default to polyimide, lifting absolute Rigid-Flex PCB market volumes. New products such as Panasonic MEGTRON 8 and Rogers RO3000 already offer dielectric constants below 3.2, giving designers more headroom for GHz signals without sacrificing bend radius.

By End-User Industry: Aerospace Still Leads, Telecommunications Surges Ahead

Aerospace and defense accounted for 36.58% of revenue in 2025, reflecting stringent IPC-6013 Class 3 requirements and long platform lifecycles. Telecommunications and 5G remain the fastest risers, with a 7.12% CAGR to 2031, as operators deploy millions of small cells and Open RAN radios.

Consumer electronics delivered roughly 20% of sales tied to foldable phones and wearables, while computing and data centers contributed 15% amid 800-gigabit Ethernet upgrades. Automotive and EV held about 12% and is accelerating on battery boards and advanced driver-assist systems. Healthcare captured 8% but faces protracted regulatory cycles, while the industrial and energy segments closed the gap at 9%. Diversification cushions cyclical swings in any single vertical and keeps the overall Rigid-Flex PCB market on a stable upward path.

Geography Analysis

Asia-Pacific generated 83.73% revenue in 2025 and is projected to grow at a 7.24% CAGR to 2031, anchored by Taiwan, China, and Japan’s deep packaging ecosystems. Taiwanese leaders Unimicron, Zhen Ding Technology, and Flexium shipped more than USD 7 billion in rigid-flex boards, serving smartphones and cloud servers. Chinese firms Shennan Circuits and Dongshan Precision increased capacity by 18% in 2025 to supply domestic EVs and 5G build-outs. Japan’s Nippon Mektron and Ibiden retained preferred-supplier status for aerospace and automotive buyers that demand AS9100 and IATF 16949 traceability.

South Korea’s Samsung Electro-Mechanics earmarked KRW 200 billion (USD 150 million) in 2025 to boost foldable-display boards by 25% by 2027. Vietnam and Thailand emerged as low-cost hubs for mid-complexity boards, drawing Taiwanese investment.

North America accounted for about 10% of revenue, driven by aerospace, defense, and medical programs that require domestic production under the Trusted Foundry framework. TTM Technologies and Molex run ITAR-registered plants, though total regional output remains capacity-constrained. Europe represented roughly 6% revenue. ATandS and Schweizer Electronic benefit from the EU Chips Act yet face high labor and strict environmental rules that price them out of mainstream consumer electronics. Rest of World, mainly Latin America, the Middle East and Africa, captured under 1%, focusing on assembly rather than fabrication.

Competitive Landscape

Global revenue is moderately concentrated, with the top ten players accounting for a considerable revenue share, leaving room for more than 200 niche suppliers that drive persistent price competition in the Rigid-Flex PCB market. Nippon Mektron took a 30% stake in a domestic polyimide producer in 2024 to secure raw material and improve bargaining leverage. Leaders now differentiate on process depth, executing laser microvias below 75 µm, 20-plus-layer sequential lamination, and AI-based defect detection that lifts yields by 8–12 points.

White-space prospects include co-packaged optics for cloud data centers and ultra-thin battery boards for electric scooters, where no incumbent yet dominates. Smaller firms occupy profitable, quick-turn and low-volume niches for medical implants and defense prototypes, trading speed and compliance for premium pricing. Chinese challengers are scaling high-automation lines to erode cost advantages long held by Taiwanese peers. More than 1,200 patents filed in 2025 cover embedded passives and hybrid rigid-flex-rigid stacks, signaling sustained innovation intensity. Compliance with IPC-6013 and ISO 9001 has become table stakes as customers demand full material traceability under REACH and Dodd-Frank rules.

Rigid-Flex PCB Industry Leaders

Nippon Mektron

Unimicron Technology

Young Poong Group

Samsung Electro-Mechanics

TTM Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Unimicron allocated TWD 15 billion (USD 480 million) for a new Taoyuan plant that will add 30% rigid-flex capacity by 2027, targeting foldables and chiplet substrates.

- November 2025: AT&S completed phase one of its EUR 300 million (USD 330 million) Leoben expansion, enabling 20-layer boards for automotive battery management, with full capacity expected mid-2027.

- October 2025: Samsung Electro-Mechanics and LG Innotek formed a KRW 180 billion (USD 135 million) joint venture to develop thinner hinges and 300 000-cycle rigid-flex boards for next-gen foldable displays.

- September 2025: TTM Technologies bought 51% of a Mexican fabricator for USD 85 million, adding 12 000 m² of automotive and industrial capacity, trimming U.S. lead times by 30%.

- August 2025: Shennan Circuits launched an LCP-based product line for 5 G base stations and data-center switches after investing CNY 800 million (USD 110 million) in laser drilling and AOI gear.

Global Rigid-Flex PCB Market Report Scope

The Rigid-Flex Printed Circuit Board Market Report is Segmented by Substrate Material (Glass Epoxy FR-4, High-Speed/Low-Loss, Polyimide PI, Packaging Resins BT/ABF, Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Healthcare/Medical, Aerospace and Defense, Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value USD.

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-User Industries |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Netherlands | |

| Rest of Europe | |

| Asia Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Rest of World |

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Other Substrate Materials | ||

| By End-User Industry | Consumer Electronics | |

| Computing and Data Centers | ||

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Healthcare / Medical | ||

| Aerospace and Defense | ||

| Other End-User Industries | ||

| By Region | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the Rigid-Flex PCB market size in 2026 and its growth outlook to 2031?

The Rigid-Flex PCB market size reached USD 9.48 billion in 2026 and is forecast to hit USD 12.74 billion by 2031, translating into a 6.09% CAGR.

Which substrate material leads recent adoption?

Polyimide dominates with 42.87% revenue in 2025 and is projected to expand at a 6.53% CAGR on the strength of high heat resistance and bend endurance.

Which end-user vertical will grow the fastest through 2031?

Telecommunications and 5G applications lead with a 7.12% CAGR as operators densify small-cell networks and upgrade backhaul links.

Why are automotive OEMs switching to rigid-flex boards?

Battery-management systems that formerly used wire harnesses now benefit from weight reduction, improved thermal paths, and easier over-the-air updates when built on rigid-flex boards.

How will Western industrial policies affect supply chains?

U.S. and EU incentives are funding new capacity that will shorten lead times and boost supply-chain resilience, though Asia-Pacific will still hold the majority of output through 2031.

Page last updated on: