Rhinoplasty Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.21 Billion |

| Market Size (2031) | USD 8.86 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rhinoplasty Devices Market Analysis by Mordor Intelligence

The Rhinoplasty Devices Market size is estimated at USD 6.21 billion in 2026, and is expected to reach USD 8.86 billion by 2031, at a CAGR of 7.39% during the forecast period (2026-2031).

Demand is underpinned by aging populations seeking functional corrections, a younger demographic embracing elective cosmetic enhancements, and device innovations such as piezoelectric bone-cutting and patient-specific 3D-printed implants. Hospitals continue to dominate procedure volumes, yet ambulatory surgical centers are expanding rapidly as payers reimburse same-day discharge models. North America leads adoption of power-assisted systems, while Asia-Pacific benefits from medical tourism and social-media-driven aesthetic aspirations. Heightened regulatory scrutiny in the United States and European Union is reshaping competitive strategy by rewarding firms able to meet stringent quality, cybersecurity, and clinical-evidence mandates.

Key Report Takeaways

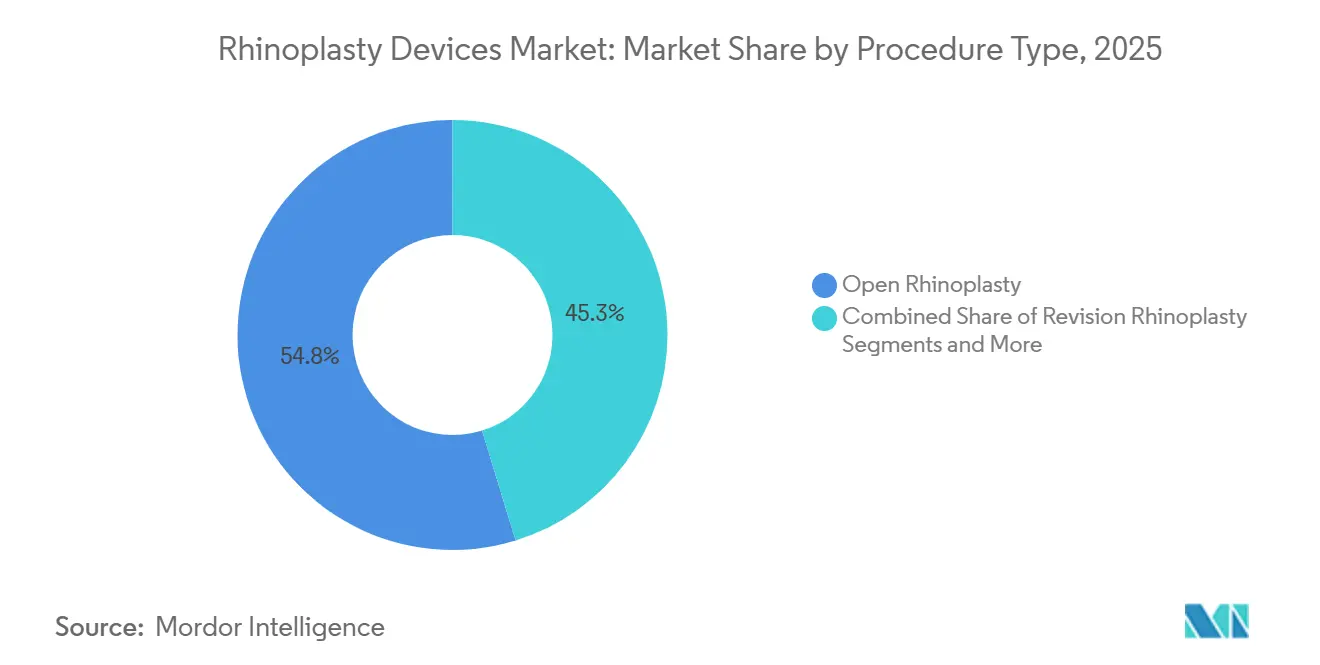

- By procedure type, open rhinoplasty led with 54.75% revenue share in 2025; revision cases are forecast to expand at a 10.46% CAGR through 2031, the fastest among all procedures.

- By indication, cosmetic rhinoplasty accounted for 64.68% of the rhinoplasty devices market share in 2025, while reconstructive and post-trauma applications are projected to grow at 10.67% CAGR to 2031.

- By product type, manual surgical instruments commanded 36.25% share of the rhinoplasty devices market size in 2025 and piezoelectric systems are advancing at an 11.67% CAGR through 2031.

- By end user, hospitals captured 52.63% of the rhinoplasty devices market in 2025, whereas ambulatory surgical centers posted the highest projected CAGR at 9.25% through 2031.

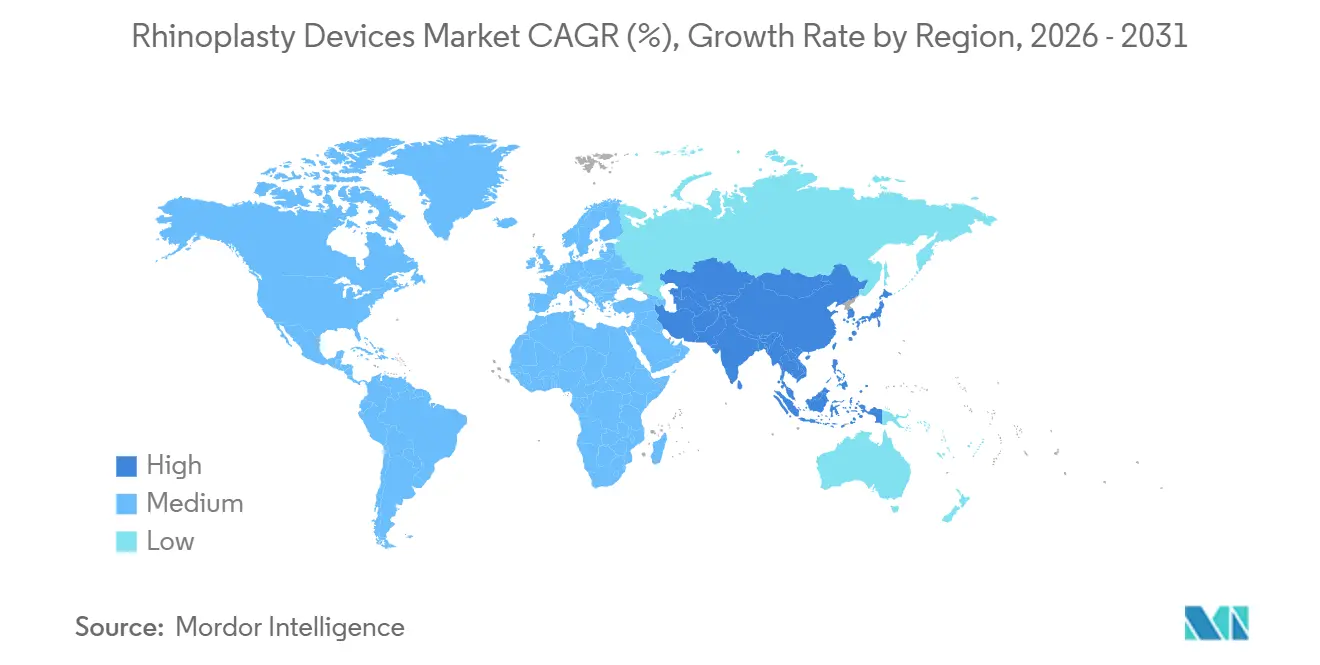

- North America held 39.36% of global revenue in 2025; Asia-Pacific is the fastest-growing geography at a 9.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rhinoplasty Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Elevating Functional Rhinoplasty Demand | +1.2% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rising Popularity of Minimally-Invasive Cosmetic Procedures | +1.5% | Urban North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Rapid Uptake of Piezoelectric Bone-Cutting Systems | +1.8% | North America, Western Europe, South Korea, Japan | Medium term (2–4 years) |

| Medical Tourism Concentrating Aesthetic Volumes | +1.1% | South Korea, Thailand, India, Turkey, Brazil | Short term (≤ 2 years) |

| 3D Printing of Patient-Specific Implants | +0.9% | United States, Europe, Australia | Long term (≥ 4 years) |

| Metaverse-Based Pre-Surgical Visualization | +0.6% | United States, Western Europe, Urban Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Aging Population Elevating Functional Rhinoplasty Demand

Global citizens aged ≥65 will jump from 761 million in 2021 to 1.6 billion by 2050, magnifying septorhinoplasty volumes that correct obstruction linked to septal deviation, turbinate hypertrophy, and nasal valve collapse. A 2024 JAMA study recorded a 32% quality-of-life improvement in patients over 60 following functional rhinoplasty, prompting broader third-party coverage.[1]Lidia E. Ishii et al., “Quality of Life After Functional Rhinoplasty in Older Adults,” JAMA Otolaryngology–Head & Neck Surgery, jamanetwork.com Japanese and German hospitals are procuring power systems to meet surging caseloads without extending operating-room time.

Rising Popularity of Minimally-Invasive Cosmetic Procedures

The American Society of Plastic Surgeons logged 352,555 rhinoplasty procedures in 2023, with non-surgical nose reshaping up 18% year-over-year.[2]American Society of Plastic Surgeons, “2023 Plastic Surgery Statistics Report,” American Society of Plastic Surgeons, plasticsurgery.org Younger consumers favor rapid-recovery options, spurring demand for closed techniques, injectable fillers, and slim piezoelectric handpieces. Surgeons note a lowering average age of first-time candidates, broadening the rhinoplasty devices market base.

Rapid Uptake of Piezoelectric Bone-Cutting Systems

Piezoelectric osteotomy reduces edema by 41% and ecchymosis by 53% versus conventional tools according to a 2022 meta-analysis covering 1,847 patients.[3]Nuno Pereira et al., “Piezoelectric Osteotomy in Rhinoplasty: A Systematic Review and Meta-Analysis,” Aesthetic Surgery Journal, academic.oup.com Stryker and Karl Storz now bundle haptic feedback and irrigation to alleviate thermal risk, yet Asia-Pacific penetration languishes below 20% due to >USD 50,000 unit prices

Medical Tourism Concentrating Aesthetic Volumes

Turkey and South Korea offer rhinoplasty packages priced 40–70% below U.S. facilities, generating international traffic; South Korea performs 19.8 rhinoplasties per 1,000 residents, 35% from foreign patients. Destination nations are tightening ISO 13485 accreditation after U.S. centers reported 22% of revision cases related to procedures performed abroad.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Average Selling Price of Power-Assisted Systems | −0.8% | Emerging Asia-Pacific, Middle East & Africa, South America | Medium term (2–4 years) |

| Stringent FDA & EU MDR Re-classification of Nasal Implants | −1.1% | North America, Europe | Long term (≥ 4 years) |

| Shortage of Rhinoplasty-Skilled ENT Surgeons | −0.7% | Emerging Asia-Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| Cyber-Security Risks in Connected Instruments | −0.5% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Average Selling Price of Power-Assisted Systems

Capital outlays of USD 40,000–80,000 deter many ambulatory centers; 68% of ENT surgeons in India, Brazil, and South Africa cite cost as the prime barrier despite clinical advantages.

Stringent FDA & EU MDR Re-classification of Nasal Implants

FDA upgraded many silicone implants to Class III in 2024, extending approval cycles 18–24 months and adding USD 3–5 million clinical-trial costs. EU MDR clinical-evaluation rules are prompting small vendors to exit Europe, consolidating share among capital-rich incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Piezoelectric Systems Drive Premium Tier

Manual instruments maintained the largest 36.25% share of the rhinoplasty devices market in 2025 thanks to reliability and affordability in resource-constrained settings. Piezoelectric units are growing fastest at an 11.67% CAGR, underpinned by 34% lower intraoperative bleeding and shorter OR times. North American and European reimbursement schemes that reward complication reduction make capital investment attractive. Modular handpieces priced near USD 25,000 are catalyzing uptake in mid-tier Asian hospitals.

Accessories and consumables constitute consistent revenue due to every-procedure usage, while implants supply a growth vector linked to rising revision and trauma volumes. Power-assisted saws occupy a mid-tier niche, valued for speed but lacking ultrasonic finesse.

By Material: Polymers Challenge Silicone Dominance

Silicone retained 44.14% share in 2025 for its carve-ability and long clinical track record, especially in Asian augmentation cases. High-performance polymers—chiefly PEEK—are progressing at a 10.54% CAGR; five-year data showed 19% lower extrusion than silicone owing to superior osseointegration. Titanium remains the reconstructive choice where load bearing is essential. Autologous grafts uphold gold-standard status yet are limited by donor-site morbidity. The rhinoplasty devices market size for polymer implants is poised to expand as additive manufacturing enables bespoke geometries and regulators accept legacy PEEK biocompatibility files.

By Procedure Type: Revision Cases Surge Amid Rising Expectations

Open rhinoplasty held 54.75% share in 2025, favored for visibility during complex corrections. Revision rhinoplasty is the growth standout at a 10.46% CAGR, reflecting social-media-driven aesthetic dissatisfaction and functional complications post primary surgery. Preservation techniques are gaining European traction following 2024 EAFPS endorsement, while non-surgical filler procedures broaden entry-level appeal. Instrument makers respond with versatile sets compatible with hybrid open-preservation approaches.

By Indication: Reconstructive Gains as Trauma Volumes Rise

Cosmetic indications dominated at 64.68% in 2025, but reconstructive and post-trauma procedures are expanding at 10.67% CAGR amid higher road-traffic injuries and oncologic recon protocols. The rhinoplasty devices market share for reconstructive kits is, therefore, set to increase, benefiting suppliers of implants, grafts, and imaging aids. Functional rhinoplasty blends medical necessity with aesthetic refinement, complicating insurance coding yet boosting per-case device use.

By End User: ASCs Capture Outpatient Shift

Hospitals commanded 52.63% of revenue in 2025; however, ASCs are climbing at 9.25% CAGR, offering 38% lower average procedure costs with comparable safety for low-risk patients. Specialty clinics leverage VR consultations and bundled pricing, capitalizing on lifestyle-oriented branding. Device firms tailor ASC-friendly sterile sets to accommodate smaller autoclaves and faster turnover.

Geography Analysis

North America recorded 39.36% of global revenue in 2025, anchored by high disposable income, insurance coverage for functional cases, and early adoption of piezoelectric, 3D-printed, and VR technologies. Mexico’s value proposition for U.S. medical tourists is widening regional demand despite FDA cybersecurity and implant reclassification hurdles that lengthen domestic product launches.

Asia-Pacific is the fastest-growing region at 9.42% CAGR, driven by South Korea’s 19.8 procedures per 1,000 people and expanding middle-class demand in China and India. Manual tools still predominate outside top-tier cities because of cost constraints, yet regulatory harmonization is cutting average approval windows to 16 months. Tele-training programs and government incentives aim to alleviate surgeon shortages.

Europe’s growth is tempered by EU MDR costs that favor well-capitalized suppliers, while preservation rhinoplasty reduces per-case instrument count. Turkey and the UAE draw European, Asian, and African patients via aggressive medical-tourism campaigns. Brazil and Colombia anchor South American growth, stressing portable power systems with serviceability in resource-variable settings. South Africa leads Sub-Saharan uptake though affordability remains a brake.

Competitive Landscape

The rhinoplasty devices market is moderately fragmented. Stryker, Medtronic, and Karl Storz dominate power-assisted niches, cross-leveraging broader ENT portfolios. Integra LifeSciences and Implantech lead implants through surgeon-education programs. Ecosystem strategies emerge as firms bundle devices with VR simulators, planning software, and post-market analytics to lock-in customers under value-based care contracts.

Start-ups such as Xilloc and Surgiform attack white spaces—bioresorbable implants, preservation-specific tools, and cyber-secure connected devices. Consolidation accelerates as MDR compliance costs push smaller European vendors toward acquisition. Technology differentiation is pivotal: Stryker’s 2024 OCT-enabled piezoelectric handpiece promises real-time tissue differentiation, while Medtronic’s Medicrea buyout injects AI planning into its ENT suite. Overall, suppliers race to prove clinical outcome gains and total-cost reductions that justify premium pricing.

Rhinoplasty Devices Industry Leaders

Stryker Corporation

Johnson & Johnson (Ethicon)

Medtronic plc

Karl Storz SE & Co. KG

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Lyra Therapeutics outlined Phase 3 ENLIGHTEN-2 results for LYR-210 targeting chronic rhinosinusitis

- July 2025: Spirair gained FDA 510(k) clearance for its bioabsorbable TurbAlign implant that maintains middle turbinate position after sinus surgery.

- June 2025: Marina Medical and W&H launched the Piezo & Drill Combination Console, the only FDA-cleared piezo/drill system for facial plastics and ENT applications.

Global Rhinoplasty Devices Market Report Scope

Rhinoplasty devices are defined as specialized surgical instruments and advanced technology systems used to reshape and contour the bone and cartilage structure of the nose. These devices are employed during functional or aesthetic nasal reconstruction, commonly referred to as a "nose job," to enhance facial harmony, improve breathing by addressing structural issues like a deviated septum, or repair damage caused by injury.

The Rhinoplasty Devices Market Report is segmented by Product Type, Material, Procedure Type, Indication, End User, and Geography.By Product Type, the market is segmented into Surgical Instruments, Power-Assisted Systems, Piezoelectric Devices, Implants, and Accessories & Consumables. By Material, the market is segmented into Silicone, Titanium, High-performance Polymers, and Autologous Tissue-based Grafts. By Procedure Type, the market is segmented into Open, Closed, Revision, Preservation, and Non-surgical. By Indication, the market is segmented into Cosmetic, Functional, Reconstructive, and Others. By End User, the market is segmented into Hospitals, ASCs, and Specialty Clinics. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Surgical Instruments |

| Power-Assisted Systems |

| Piezoelectric Devices |

| Implants |

| Accessories & Consumables |

| Silicone |

| Titanium |

| High-performance Polymers |

| Autologous Tissue-based Grafts |

| Open Rhinoplasty |

| Closed (Endonasal) Rhinoplasty |

| Revision Rhinoplasty |

| Preservation Rhinoplasty |

| Non-surgical (Liquid) Rhinoplasty |

| Cosmetic / Aesthetic |

| Functional (Airway Obstruction) |

| Reconstructive / Post-Trauma |

| Others (Congenital Deformity Correction, Oncologic Defect Reconstruction etc) |

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty & Cosmetic Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Surgical Instruments | |

| Power-Assisted Systems | ||

| Piezoelectric Devices | ||

| Implants | ||

| Accessories & Consumables | ||

| By Material | Silicone | |

| Titanium | ||

| High-performance Polymers | ||

| Autologous Tissue-based Grafts | ||

| By Procedure Type | Open Rhinoplasty | |

| Closed (Endonasal) Rhinoplasty | ||

| Revision Rhinoplasty | ||

| Preservation Rhinoplasty | ||

| Non-surgical (Liquid) Rhinoplasty | ||

| By Indication | Cosmetic / Aesthetic | |

| Functional (Airway Obstruction) | ||

| Reconstructive / Post-Trauma | ||

| Others (Congenital Deformity Correction, Oncologic Defect Reconstruction etc) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Specialty & Cosmetic Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the rhinoplasty devices market?

The rhinoplasty devices market size is USD 6.21 billion in 2026.

How fast is demand for piezoelectric systems growing?

Piezoelectric devices are advancing at an 11.67% CAGR through 2031 thanks to precision cutting and reduced soft-tissue trauma.

Which region shows the highest growth potential?

Asia-Pacific leads with a 9.42% CAGR, fueled by medical tourism and rising disposable incomes.

Why are ambulatory surgical centers important for suppliers?

ASCs perform cost-effective outpatient procedures, expanding at 9.25% CAGR and spurring demand for compact, easy-to-sterilize instrument sets.

What material is challenging silicone in implants?

High-performance polymers, particularly PEEK, are gaining share due to better osseointegration and lower extrusion risk.

How will stricter FDA and EU regulations influence new product launches?

Longer approval cycles and higher clinical-evidence costs will favor capital-rich incumbents and drive consolidation among smaller vendors.

Page last updated on: