RF-Microwave For 5G Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

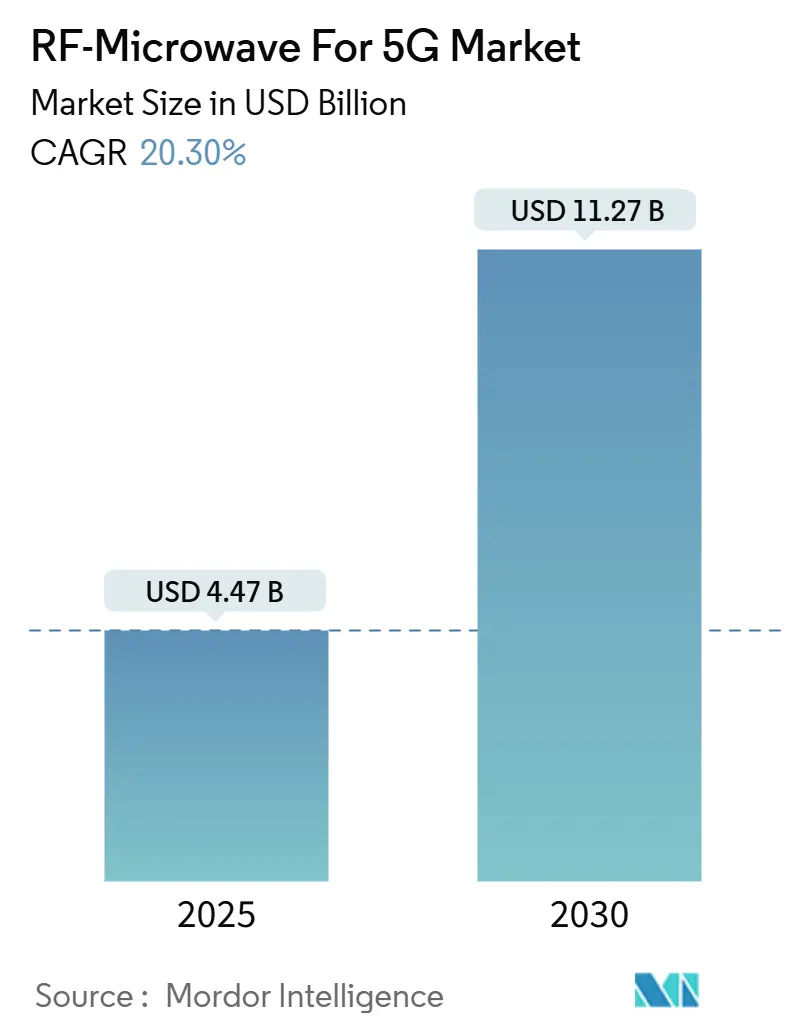

| Market Size (2025) | USD 4.47 Billion |

| Market Size (2030) | USD 11.27 Billion |

| Growth Rate (2025 - 2030) | 20.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RF-Microwave For 5G Market Analysis by Mordor Intelligence

The RF-Microwave for 5G market size stands at USD 4.47 billion in 2025 and is forecast to reach USD 11.27 billion by 2030, advancing at a 20.3% CAGR. This strong momentum reflects the accelerating shift from 4G to 5G infrastructure, where higher-frequency operation and stringent power-efficiency targets amplify demand for sophisticated RF front-ends. Operators installed 4.2 million 5G base stations worldwide by end-2024, up from 1.8 million in 2023, creating a steep, multiplicative uptick in RF component volumes.[1]Ericsson Mobility Report, “Global 5G Infrastructure Deployment Trends,” Ericsson.com, ericsson.com Component innovation is paced by gallium-nitride (GaN) power amplifiers that deliver 30–40% efficiency gains over legacy gallium-arsenide devices, easing thermal constraints in massive-MIMO radios. Smartphone OEMs are simultaneously integrating mmWave antenna modules, broadening RF-front-end requirements beyond traditional infrastructure.[2]Apple Inc., “Annual Report for Fiscal Year 2024,” Apple.com, investor.apple.com In parallel, private-5G adoption across manufacturing hubs is opening fresh revenue streams that diversify the RF-Microwave for 5G market beyond carrier deployments

Key Report Takeaways

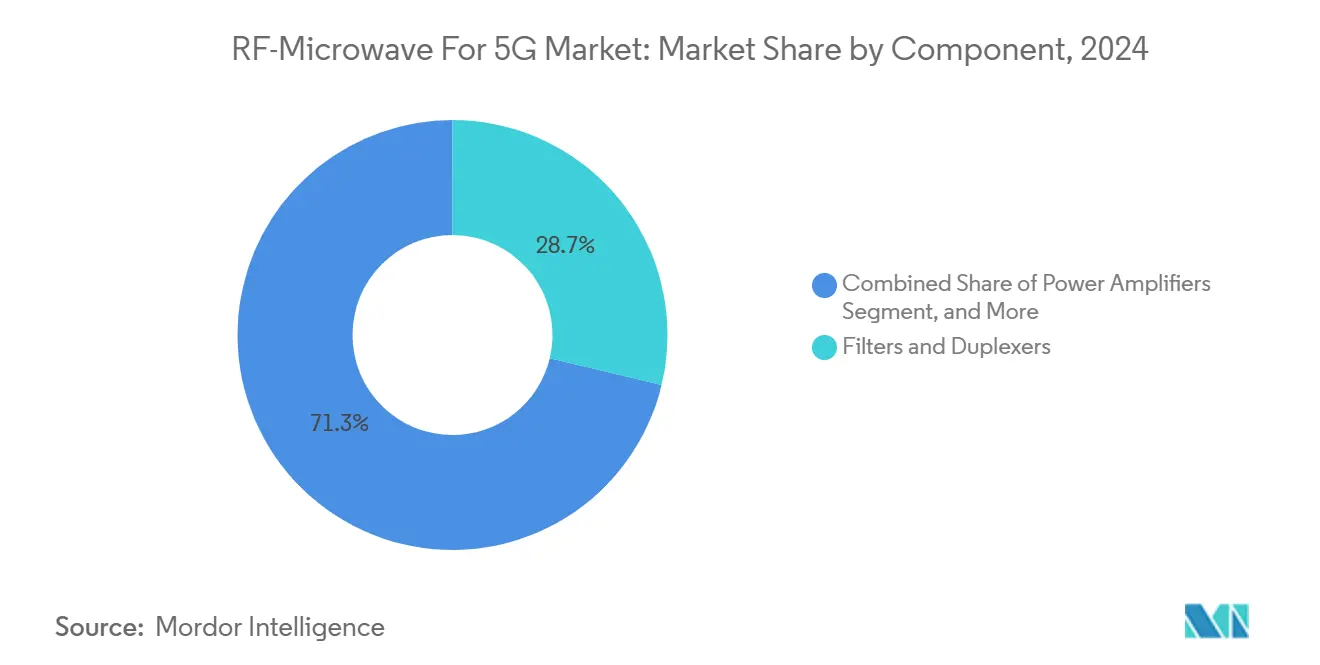

- By component, filters and duplexers led with 28.73% of the RF-Microwave for 5G market share in 2024, while power amplifiers are projected to grow at a 20.77% CAGR to 2030.

- By frequency band, sub-6 GHz captured 61.73% of the RF-Microwave for 5G market size in 2024; the 40-52 GHz band is tracking a 21.44% CAGR through 2030.

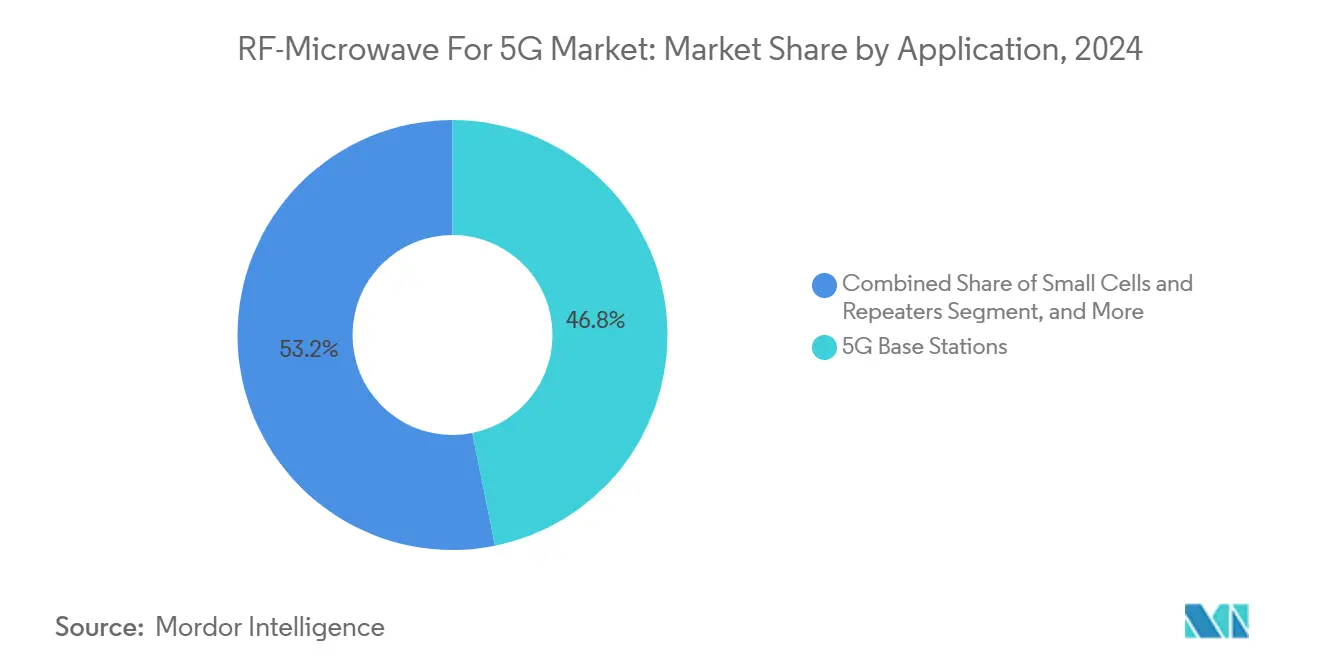

- By application, base stations held 46.83% revenue share of the RF-Microwave for 5G market size in 2024, whereas automotive V2X communications is set to expand at 21.19% CAGR to 2030.

- By material technology, Gallium Arsenide (GaAs) led with 34.82% of the RF-Microwave for 5G market share in 2024, while GaN is projected to grow at a 20.89% CAGR to 2030.

- By geography, North America accounted for 39.84% of the RF-Microwave for 5G market size in 2024; Asia-Pacific is advancing at a 21.22% CAGR during the same period.

- Broadcom, Qualcomm and Skyworks together controlled about 45% of 2024 revenue, with GaN-focused entrants such as Wolfspeed gaining share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global RF-Microwave For 5G Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential surge in 5G base-station roll-outs | +4.2% | Global, with APAC leading deployment volumes | Medium term (2-4 years) |

| Proliferation of mmWave-enabled smartphones | +3.8% | North America and EU early adoption, APAC mass market | Short term (≤ 2 years) |

| Rising demand for RF front-end modules in small cells | +3.1% | Global urban deployments, concentrated in dense metros | Medium term (2-4 years) |

| Shift toward open RAN requiring modular RF units | +2.9% | North America and EU regulatory push, selective APAC adoption | Long term (≥ 4 years) |

| Commercialization of GaN-on-Si power amplifiers | +3.5% | Global technology transition, led by advanced fabs | Medium term (2-4 years) |

| Private-5G roll-outs for industrial IoT and backhaul | +2.8% | Industrial regions globally, concentrated in manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exponential Surge in 5G Base-Station Roll-Outs

Base-station density is the single biggest multiplier of RF-component demand. Operators deployed 4.2 million 5G radio sites by end-2024, versus 1.8 million in 2023, primarily in China’s state-backed build program. Each massive-MIMO site now integrates 64–256 antenna elements, compared with eight or fewer in 4G, lifting per-site RF channels more than tenfold. Higher element counts compound with sheer site volume, yielding a step-function increase in filter, switch and power-amplifier shipments. Operators in North America and Europe are mirroring this template, although spectrum and zoning rules make their roll-outs more phased.

Proliferation of mmWave-Enabled Smartphones

Premium handsets such as Apple’s iPhone 15 employ Qualcomm’s X70 modem with dedicated mmWave arrays, validating consumer demand for multi-gigabit speeds. Samsung’s Galaxy S24 integrates Murata modules to house filters, duplexers and power amplifiers in sub-3 mm stack heights, shrinking board area while lowering insertion loss.[3]Samsung Electronics, “Technology Innovation and Market Strategy,” Samsung.com, samsung.com Thermal design margins remain tight, so handset OEMs are shifting toward GaN-on-Si power amplifiers that maintain linearity at higher efficiencies. Volume smartphone adoption accelerates learning curves and economies of scale for advanced PA technologies, indirectly fueling infrastructure designs that share wafer flows.

Rising Demand for RF Front-End Modules in Small Cells

Small-cell shipments increased to 2.1 million units in 2024 as urban operators chase indoor coverage and street-level capacity. Space and thermal limits in compact housings require single-package front-ends combining filters, switches and amplifier chains. Neutral-host deployments add the requirement to re-tune remotely across multiple carrier bands, spurring programmable RF architectures. The RF-Microwave for 5G market therefore leans on module vendors capable of multi-band design, software calibration and co-existence testing.

Shift Toward Open RAN Requiring Modular RF Units

O-RAN Alliance specifications break traditional base-station silos, mandating open interfaces across remote radio heads, distribution units and centralized controllers. Hardware suppliers must now certify radio units that interoperate with diverse baseband vendors, pushing RF designs toward standardized connectorized modules. European operators have committed up to 30% of new macro sites to open RAN beginning 2025, a trend expected to spread once performance parity with integrated solutions is proven.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compound-semiconductor wafer shortages | -2.8% | Global supply chain, concentrated in Asian fabs | Short term (≤ 2 years) |

| High cost and complexity of mmWave RF design/testing | -2.1% | Global technology adoption, higher impact in cost-sensitive markets | Medium term (2-4 years) |

| Thermal limits in dense radio units | -1.6% | Global deployment challenge, acute in hot climates | Medium term (2-4 years) |

| Export-control barriers on advanced RF components | -1.9% | US-China trade restrictions, spillover to allied nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compound-Semiconductor Wafer Shortages

Lead times for GaAs and GaN wafers have extended to 30 weeks, double pre-2024 norms, because China controls roughly 80% of refined gallium, and rival sectors like EV power devices compete for the same substrates. Foundries are adding 150 mm GaN lines, yet greenfield plants need 18 months, causing near-term mismatches between demand surges and wafer availability.

High Cost and Complexity of mmWave RF Design/Testing

Full-band mmWave vector-network analyzers and anechoic chambers push capex above USD 2 million per lab; this locks out smaller entrants and lengthens design cycles. Specialized electromagnetic talent is scarce, raising labor costs and limiting the diversity of commercial offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Power Amplifiers Lead Innovation Drive

Power amplifiers contributed USD 732 million to the RF-Microwave for 5G market size in 2024, and are projected to expand at a 20.77% CAGR to 2030. Efficiency gains from GaN-on-Si reduce energy operating expenses in dense antenna arrays, sharpening operator focus on premium PA designs. Filters and duplexers remained the largest component class, supporting 28.73% of revenue by handling multi-band spectrum coexistence across sub-6 GHz and mmWave carriers.

The segment’s future hinges on integrating multiple PA stages with digital predistortion into single packages, a trend already evident in Skyworks’ system-in-package roadmap. Rising data-throughput targets accelerate demand for low-noise amplifiers and high-isolation switches, yet PA technology remains the critical differentiator for thermal and linearity budgets that define macro-cell reliability in the RF-Microwave for 5G market.

By Frequency Band: mmWave Segments Accelerate Despite Sub-6 Dominance

Sub-6 GHz bands delivered 61.73% of 2024 revenue, anchoring nationwide 5G coverage where propagation losses remain manageable. Nonetheless, the 40–52 GHz tier, though a smaller base, is forecast to grow 21.44% annually as fixed wireless access and enhanced-mobile-broadband services seek fiber-class throughput.

RF-front-end complexity rises non-linearly with frequency, pushing suppliers to use advanced laminate PCBs, flip-chip packaging and GaN e-mode devices to offset path losses. Upper mmWave adoption remains skewed to North America, but EU digital-decade targets and APAC trials will widen global applicability, reinforcing the RF-Microwave for 5G market’s shift toward ultra-high-frequency componentry.

By Application: Base Stations Drive Volume While Automotive Shows Promise

Macro and small-cell base stations absorbed 46.83% of RF-Microwave for 5G market share in 2024, underlining carrier capex orientation. Each site requires dozens of PAs, filters and transceivers, making infrastructure the volume anchor for most suppliers.

Automotive V2X communications posted the fastest trajectory at a 21.19% CAGR, propelled by regulatory mandates and OEM safety agendas. Vehicle platforms demand ruggedized RF modules qualified to AEC-Q104 standards, prompting semiconductor firms to spin automotive-grade variants of infrastructure parts. Smartphones and tablets remain critical for peak-volume years, yet emerging industrial and vehicular use cases diversify long-term demand, broadening the RF-Microwave for 5G market revenue mix.

By Material Technology: GaN Disrupts Traditional GaAs Dominance

GaAs preserved 34.82% revenue share in 2024, owing to mature processes and cost-effective mid-band performance. GaN, however, is growing at 20.89% CAGR as its superior breakdown and electron-mobility parameters fit mmWave PAs and high-power radio heads. Silicon germanium thrives in cost-sensitive, moderate-frequency applications, while CMOS consolidation benefits low-gain front-end switches, demonstrating an application-optimized material mix rather than a zero-sum contest.

Manufacturing capacity is the gating metric: Wolfspeed’s Durham expansion and European fabs backed by the CHIPS Act aim to localize compound-semiconductor supply chains, mitigating geopolitical risk and stabilizing the RF-Microwave for 5G market’s long-term cost curve

Geography Analysis

North America led with 39.84% revenue in 2024, as CHIPS-driven incentives pulled RF-component manufacturing onshore and carriers like Verizon commercialized mmWave in metro clusters. Infrastructure roll-outs emphasize 28 GHz and 39 GHz backhaul links, elevating demand for GaN PAs and ceramic-based filters that meet harsh thermal cycling in rooftop enclosures. Mid-band 3.45–3.98 GHz coverage layers added in 2025 expand shipments of sub-6 GHz modules, sustaining balanced demand across the RF-Microwave for 5G market.

Asia-Pacific is projected to clock a 21.22% CAGR to 2030. China alone operates over 3.2 million 5G macro sites, creating scale economies unmatched elsewhere. Smartphone OEM clustering across China, South Korea and Vietnam further cements regional pull for RF-front-end components. Export-control frictions around advanced EDA tools and wafer tools push local firms toward indigenous GaN capacity, reshaping global supplier share.

Europe trails in deployment pace but gains momentum as Digital Decade targets mandate ubiquitous 5G by 2030. Spectrum harmonization in the 26 GHz band supports consistent RF design across member states, easing design-win scaling for component vendors. Open RAN trials in Germany, the U.K. and the Nordics are testing multi-vendor radio stacks, broadening supplier pools in the RF-Microwave for 5G market.

Competitive Landscape

The RF-Microwave for 5G market is moderately concentrated; the top five vendors hold roughly 45% combined share, giving it a concentration score of 6. Broadcom leverages FBAR filter leadership and tight carrier relationships, while Qualcomm capitalizes on modem-to-antenna integration for smartphones and emerging small-cell platforms. Skyworks’ 2024 purchase of Silicon Labs’ infrastructure unit broadens its footprint beyond handsets.

GaN capacity is a key battleground. Wolfspeed scales vertically from substrate to packaged devices, supplying both infrastructure and automotive PAs. Qorvo’s GaN foundry services underpin collaborations with Samsung for front-end modules that shrink handset RF boards by 40%. Such moves reposition traditional GaAs stalwarts into wide-bandgap powerhouses, redrawing the competitive map of the RF-Microwave for 5G market.

Strategic alliances are rising as barriers to entry increase. Broadcom’s 2024 FBAR portfolio integrates temperature-compensated resonators for mid-band massive-MIMO radios, while start-ups focus on AI-assisted RF design automation. Export-control risk drives U.S. and EU operators to favor domestic or allied suppliers, creating regionalized sourcing and localized production incentives.

RF-Microwave For 5G Industry Leaders

Broadcom Inc.

Qualcomm Incorporated

Skyworks Solutions, Inc.

Qorvo, Inc.

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Industry-wide component movements indicate numerous RF and mixed-signal releases and demonstrations throughout mid-2025, highlighting rapid innovation in RF/microwave components (power amplifiers, LNAs, switches, etc.) aligned with 5G and related wireless tech growth.

- March 2025: At MWC 2025, major connectivity announcements highlighted ongoing 5G Advanced and 5G-AI integration trends, with Qualcomm introducing the X85 5G modem and high-performance fixed wireless access products.

- January 2025: OpenPR reports the global RF-Microwave for 5G market is projected to reach ~USD 3.5 billion by 2031, growing at a ~16.3% CAGR from 2025–2031 as 5G deployments expand and demand for high-frequency signal amplification and filtering rises.

Global RF-Microwave For 5G Market Report Scope

| RF Front-End Modules |

| Power Amplifiers |

| Low-Noise Amplifiers |

| Filters and Duplexers |

| Antenna and Antenna Modules |

| Switches |

| Circulators and Isolators |

| Sub-6 GHz (FR1) |

| 24–30 GHz (Lower mmWave) |

| 30–40 GHz (Mid mmWave) |

| 40–52 GHz (Upper mmWave) |

| 5G Base Stations |

| Small Cells and Repeaters |

| Customer-Premises Equipment (CPE) |

| 5G Smartphones and Tablets |

| Automotive and V2X Communications |

| Industrial IoT Devices |

| Gallium Arsenide (GaAs) |

| Gallium Nitride (GaN) |

| Silicon Germanium (SiGe) |

| Silicon CMOS |

| Indium Phosphide (InP) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | RF Front-End Modules | ||

| Power Amplifiers | |||

| Low-Noise Amplifiers | |||

| Filters and Duplexers | |||

| Antenna and Antenna Modules | |||

| Switches | |||

| Circulators and Isolators | |||

| By Frequency Band | Sub-6 GHz (FR1) | ||

| 24–30 GHz (Lower mmWave) | |||

| 30–40 GHz (Mid mmWave) | |||

| 40–52 GHz (Upper mmWave) | |||

| By Application | 5G Base Stations | ||

| Small Cells and Repeaters | |||

| Customer-Premises Equipment (CPE) | |||

| 5G Smartphones and Tablets | |||

| Automotive and V2X Communications | |||

| Industrial IoT Devices | |||

| By Material Technology | Gallium Arsenide (GaAs) | ||

| Gallium Nitride (GaN) | |||

| Silicon Germanium (SiGe) | |||

| Silicon CMOS | |||

| Indium Phosphide (InP) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 revenue forecast for RF-microwave components used in 5G?

The market stands at USD 4.47 billion in 2025 and is projected to reach USD 11.27 billion by 2030, reflecting a 20.3% CAGR.

Which component category shows the fastest growth?

Power amplifiers are expanding at a 20.77% CAGR due to the shift toward GaN-on-Si technology and higher efficiency demands.

Which frequency band will grow the quickest through 2030?

The 40–52 GHz upper mmWave tier is forecast to rise at 21.44% CAGR as operators pursue fixed-wireless access and ultra-high-speed links.

Why is GaN important for 5G RF designs?

GaN offers superior power density and thermal performance, enabling 30–40% efficiency gains in mmWave power amplifiers over GaAs alternatives.

Which region currently leads in RF-microwave demand for 5G?

North America held 39.84% of 2024 revenue, driven by aggressive mmWave deployments and domestic manufacturing incentives.

Page last updated on: