Retinal Vein Occlusion Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 3.79 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

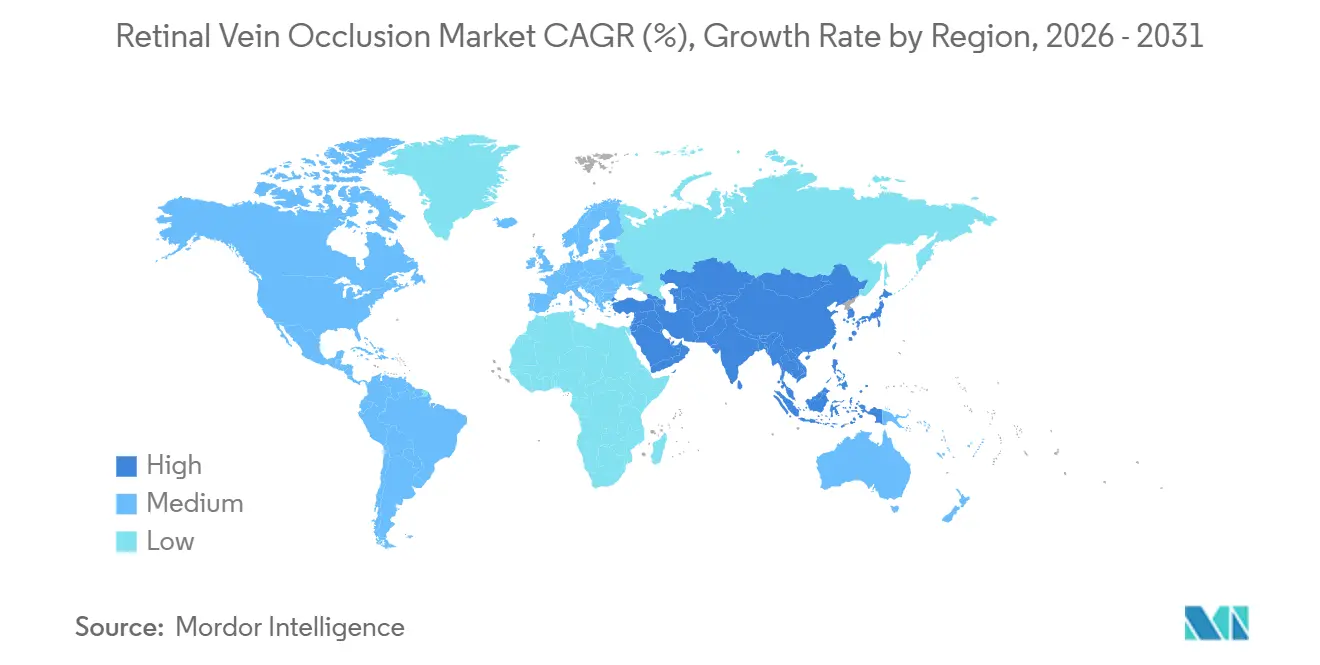

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

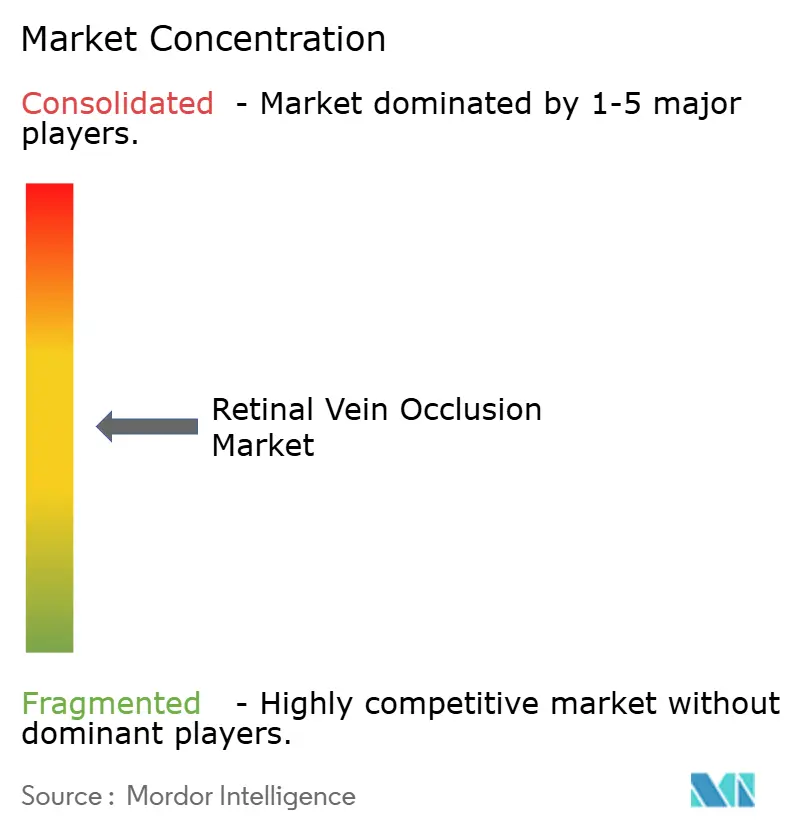

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retinal Vein Occlusion Market Analysis by Mordor Intelligence

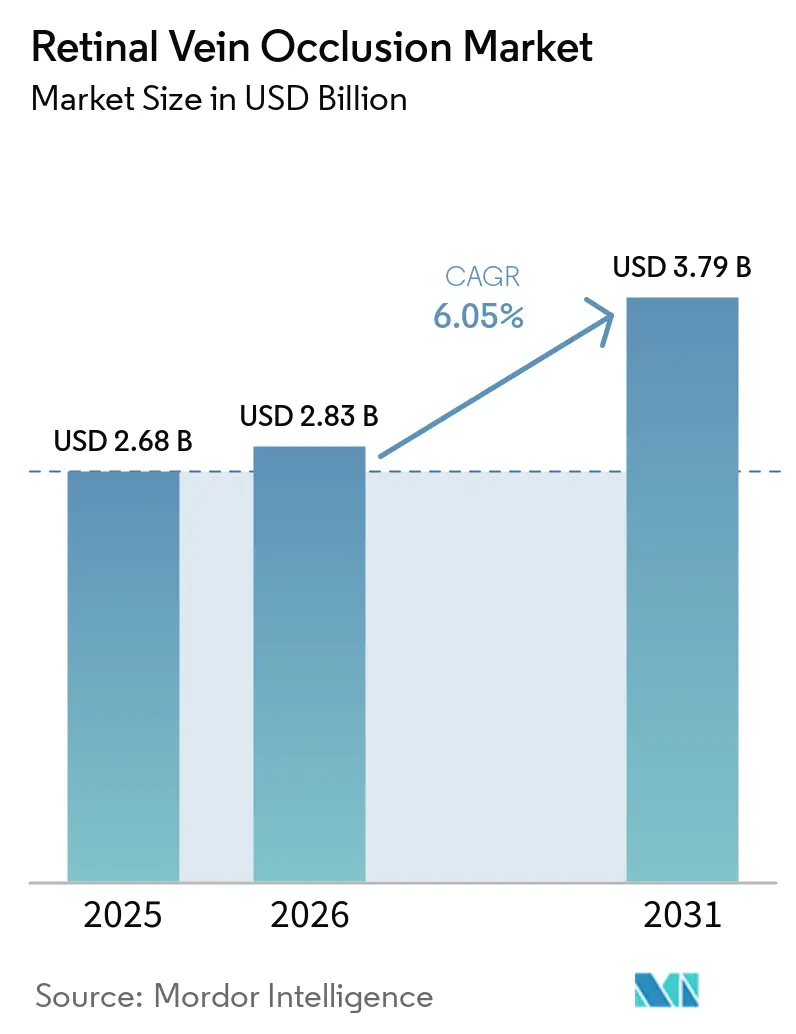

The Retinal Vein Occlusion Market size is projected to expand from USD 2.68 billion in 2025 and USD 2.83 billion in 2026 to USD 3.79 billion by 2031, registering a CAGR of 6.05% between 2026 to 2031.

The retinal vein occlusion market is being shaped by wider use of extended-interval biologics, the persistence of anti-VEGF as first-line care, and earlier detection that brings more patients into treatment. The retinal vein occlusion market is also being supported by a broader clinical view of RVO as a marker of systemic vascular risk rather than an isolated eye event. A 2025 longitudinal study showed materially higher mortality risk in both branch and central RVO after adjustment for major cardiovascular factors, which is widening referrals from cardiology, nephrology, and endocrinology. Imaging advances in OCT and OCTA are helping clinicians identify ischemic change earlier and monitor capillary nonperfusion with greater precision, which supports faster treatment decisions. At the same time, longer dosing intervals and lower procedure intensity in selected regimens are creating room for outpatient retina centers to handle more follow-up care while hospitals continue to manage complex cases.

Key Report Takeaways

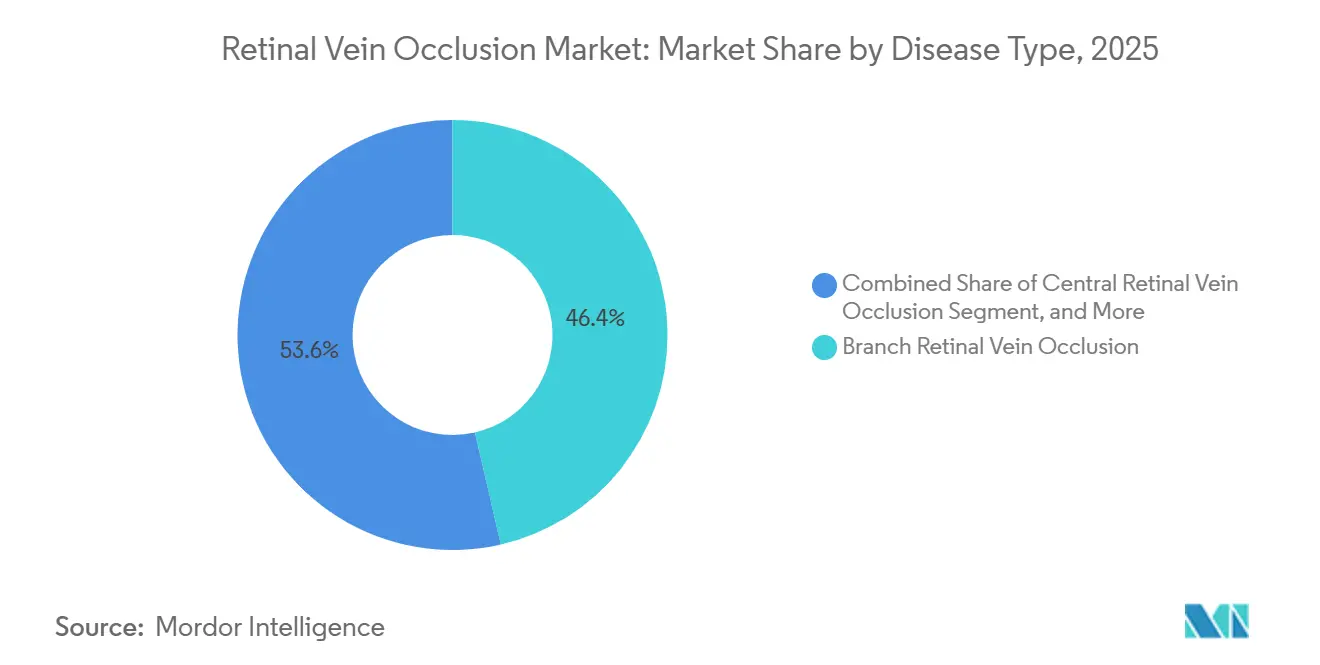

- By disease type, branch retinal vein occlusion held 46.37% of the retinal vein occlusion market share in 2025, while central retinal vein occlusion is projected to expand at an 8.23% CAGR through 2031.

- By condition, ischemic RVO accounted for 37.51% of the retinal vein occlusion market size in 2025, while non-ischemic RVO is forecast to grow at a 7.93% CAGR through 2031.

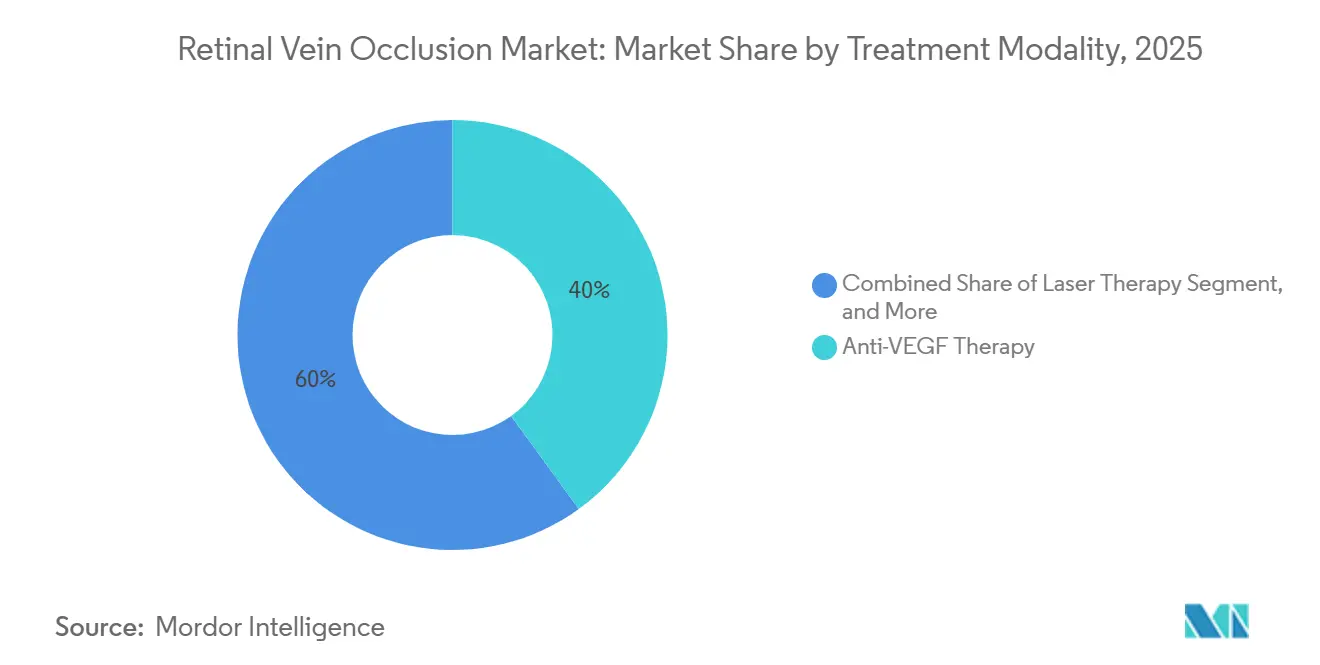

- By treatment modality, anti-VEGF therapy held 39.98% of retinal vein occlusion market share in 2025, while laser therapy is expected to advance at an 8.85% CAGR through 2031.

- By end user, hospitals captured 41.99% of the retinal vein occlusion market size in 2025, while ophthalmology clinics and retina centers are projected to record the fastest growth at a 10.02% CAGR through 2031.

- By geography, North America led with 36.43% of the retinal vein occlusion market in 2025, while Asia-Pacific is forecast to expand at a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retinal Vein Occlusion Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-Related and Cardio-Metabolic Risk Expansion | +1.2% | Global, with intensity in APAC including Japan, China, and South Korea and in Western Europe | Long term (≥ 4 years) |

| Anti-VEGF Standard-of-Care Persistence | +1.0% | Global, with highest value contribution in North America and Europe | Medium term (2-4 years) |

| New Approvals and Durability-Led Regimen Expansion | +0.8% | North America primarily, with spillover to Europe and APAC as registrations cascade | Short term (≤ 2 years) |

| OCT and OCTA-Led Earlier Detection and Monitoring | +0.6% | North America and Europe core, with early gains in China, Japan, and South Korea | Medium term (2-4 years) |

| Retina-Clinic Throughput Gains From Extended-Interval Therapy | +0.5% | North America and Europe, with emerging gains in Australia and GCC | Short term (≤ 2 years) to Medium term (2-4 years) |

| Teleophthalmology and Community OCT Triage Adoption | +0.4% | APAC and South America primarily, with supplementary gains in rural North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging-Related and Cardio-Metabolic Risk Expansion

Population aging and the rise of cardiometabolic disease are creating a structural increase in the at-risk pool for the retinal vein occlusion market. RVO incidence doubled after age 50 and reached 4.6 per 1,000 in people older than 80 years, which was a 20-fold increase over the 40 to 49 cohort. In East Asian populations, hypertension carried an odds ratio of 4.11 and chronic kidney disease carried an odds ratio of 4.14 for RVO. The 2025 Gutenberg Health Study also showed that CRVO patients faced a 3.83-fold elevated mortality risk independent of traditional cardiovascular factors. This is widening screening and referral activity beyond ophthalmology and bringing more patients into earlier retinal evaluation.[1]Anna Maria Voigt, Hisham Elbaz, Elsa Wilma Böhm, et al., “Incidence of Retinal Vein Occlusion and Its Association with Mortality, Results from the Gutenberg Health Study,” Ophthalmology, aaojournal.org

Anti-VEGF Standard-Of-Care Persistence

Anti-VEGF therapy kept its central role in the retinal vein occlusion market because the 2024 American Academy of Ophthalmology Preferred Practice Pattern continued to place intravitreal anti-VEGF agents at the front of care for macular edema secondary to RVO. The clinical need behind this position is durable, since up to 70% of eyes in the LEAVO trial showed persistent or recurrent macular fluid over 100 weeks. That pattern means repeat dosing remains necessary for a large share of patients even after the initial response phase.[2]Christiana Dinah et al., “What Is Occluding Our Understanding of Retinal Vein Occlusion,” Ophthalmology and Therapy, link.springer.com Price competition can change product mix, but it does not remove the underlying need for ongoing injections when fluid persists. This gives the segment a durable demand floor even as therapy choice becomes more varied.

New Approvals and Durability-Led Regimen Expansion

The retinal vein occlusion market is being reshaped by durability-led regimen expansion rather than by a simple rise in treatment starts. In the BALATON extension phase, 32% of faricimab patients completed 2 consecutive q16w cycles, which showed that a meaningful subset could move to a lighter treatment schedule.[3]Hoffmann-La Roche Limited, “VABYSMO Is Now Reimbursed in Ontario for the Treatment of Macular Edema Secondary to Retinal Vein Occlusion,” Roche Canada, rochecanada.com Kodiak Sciences reported that half of patients in the Phase 3 BEACON study remained injection-free through the second 6 months of treatment with tarcocimab. These durability profiles matter because they reduce clinic congestion and make follow-up care easier for smaller retina centers to absorb. The commercial and clinical value of longer intervals is therefore becoming a major point of differentiation across the treatment field.

OCT and OCTA-Led Earlier Detection and Monitoring

OCT and OCTA are moving from supportive imaging tools to decision-critical inputs across the retinal vein occlusion market. A 2025 meta-analysis that covered 2,119 RVO eyes across 53 studies confirmed that OCTA can quantify capillary nonperfusion, foveal avascular zone enlargement, and vessel density loss in a reliable manner. In CRVO, OCTA captured deeper ischemic asymmetry in 91.7% of cases, which reduced dependence on fluorescein angiography in moderate-complexity settings. This is making earlier referral easier from general ophthalmology and community optometry settings. Real-world monitoring is also improving, with one Swiss center validating AI-assisted macular fluid tracking across a 2-year follow-up period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Branded Biologic Cost and Repeat Injection Burden | -1.0% | Global, with strongest pressure in middle-income APAC markets including China and India and in Latin America | Long term (≥ 4 years) |

| Steroid-Related Cataract and Intraocular Pressure Risks | -0.4% | Global, particularly limiting second-line steroid uptake in phakic patients | Medium term (2-4 years) |

| Retina-Clinic Capacity Constraints and Poor Persistence | -0.6% | North America, Europe, and APAC urban centers, with acute pressure in markets with low specialist-to-patient ratios | Short term (≤ 2 years) to Medium term (2-4 years) |

| AI and OCT Workflow Interoperability Bottlenecks | -0.4% | High-volume centers in North America and Europe and early-stage markets with mismatched systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Branded Biologic Cost and Repeat Injection Burden

High biologic cost and repeat intravitreal dosing still limit full treatment conversion in the retinal vein occlusion market. The chronic-care profile of anti-VEGF means many eyes need ongoing retreatment rather than a short fixed course, and persistent or recurrent macular fluid remained present in up to 70% of eyes over 100 weeks in LEAVO. By contrast, the Phase IV YANGTZE study reported a mean of 2.3 dexamethasone implant injections over 12 months in Chinese RVO patients, which helps explain why lower-procedure options remain relevant when visit burden is high. The gap between frequent retreatment need and patient capacity creates discontinuation risk in both self-pay and reimbursed settings. For that reason, pricing pressure and dosing burden remain linked restraints even when treatment efficacy is well established.

Retina-Clinic Capacity Constraints and Poor Persistence

Retina specialist capacity places a practical ceiling on how much of the retinal vein occlusion market can move from diagnosis to active treatment. A University of Tokyo study showed that starting anti-VEGF therapy more than 28 days after the first CRVO presentation was associated with statistically significant long-term vision loss, while avoiding that delay required monitoring every 1 to 2 weeks. A Swiss real-world cohort then showed that a mean 10-week interruption during COVID lockdowns caused fluid recurrence and short-term vision loss, even though 2-year outcomes were comparable. That same cohort also suggested that some eyes may not need continuous high-intensity retreatment, since 17% required no further injections after the disruption. Extended-interval regimens help relieve this bottleneck, but they do not fully solve the scheduling burden for patients who remain in monthly loading or close monitoring cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: BRVO Dominates, CRVO Grows With Diagnostic Precision

Branch retinal vein occlusion retained 46.37% of the retinal vein occlusion market share in 2025. BRVO leads because it is 4 times more prevalent than CRVO globally, with risk clustering at the superotemporal crossing, where arterial compression is common in hypertensive patients. A pooled BRVO prevalence of 4.42 per 1,000 translates into a large clinical pool across treated and untreated patients. That structural case volume gives the retinal vein occlusion market a durable base in diagnosis, monitoring, and repeat therapy.

Central retinal vein occlusion is the fastest-growing disease subtype in the retinal vein occlusion market, with an 8.23% CAGR from 2026 to 2031. Growth is being supported by OCTA-based ischemia markers such as foveal avascular zone perimeter, which identified ischemic conversion with 88.9% sensitivity. This matters because previously missed or undertreated CRVO cases are now more likely to be escalated before neovascular complications appear. Hemiretinal vein occlusion remains the smallest segment, but its clearer recognition in clinical protocols is gradually improving diagnostic coding and treatment uptake.

By Condition: Ischemic RVO Commands Value, Non-Ischemic Builds Volume

Ischemic RVO accounted for 37.51% of the retinal vein occlusion market size in 2025. Its higher value weight reflects the greater treatment intensity that often comes with neovascular complications, where anti-VEGF, pan-retinal photocoagulation, and corticosteroids can be used together. Non-ischemic retinal vein occlusion is the fastest-growing condition subtype at a 7.93% CAGR through 2031. The larger non-ischemic patient pool is supported by the approximate 3:7 ischemic-to-non-ischemic presentation split and by the steady rise in older at-risk populations.

The retinal vein occlusion market is also changing because imaging can now separate ischemic and non-ischemic presentations earlier in the care pathway. DRIL and the prominent middle-limiting membrane sign differentiated ischemic from non-ischemic RVO in 57% and 58% of cases, respectively. These markers are useful in settings where fluorescein angiography is not always practical. Better triage can move higher-risk patients toward faster escalation when ischemic features are present.

By Treatment Modality: Anti-VEGF Leads, Laser Grows on Combination Protocols

Anti-VEGF therapy accounted for 39.98% of the retinal vein occlusion market size in 2025. Its lead position reflects AAO guidance that places intravitreal anti-VEGF agents at the center of treatment for macular edema secondary to RVO. Demand remains strong because many eyes show persistent or recurrent fluid over long follow-up, which keeps repeat dosing clinically necessary. This leaves anti-VEGF as the anchor of the retinal vein occlusion industry even as other modalities expand around it.

Laser therapy is projected to grow at an 8.85% CAGR through 2031 in the retinal vein occlusion market. The rise is tied to its role in combination use for peripheral ischemia management and for prevention of neovascular glaucoma, not to a return to routine standalone photocoagulation. A 2026 Tokyo study found that OCT and OCTA-guided focal photocoagulation achieved macular edema remission in 48.9% of BRVO-associated microaneurysm cases without anti-VEGF escalation. Corticosteroids remain the main second-line option, and the Phase IV YANGTZE study reported a mean of 2.3 dexamethasone implant injections over 12 months in Chinese patients.

By End User: Hospitals Anchor Revenue While Clinics Capture New Growth

Hospitals held 41.99% of the retinal vein occlusion market in 2025. They remain the main site for first diagnosis, initial loading therapy, and complex presentations that involve vitreous hemorrhage or neovascular glaucoma. This keeps hospitals central to revenue generation even as more routine follow-up is redistributed. The retinal vein occlusion industry still depends on hospital systems for advanced imaging access, emergency assessment, and surgical backup.

Ophthalmology clinics and retina centers are projected to expand at a 10.02% CAGR through 2031. Their gain is tied to longer interval regimens that lower scheduling pressure for repeat visits. Roche Canada reported that 32% of faricimab patients completed 2 consecutive q16w cycles in the BALATON extension phase, which shows how selected patients can be managed within lighter outpatient workflows. Ambulatory surgical centers continue to support laser and combination procedures when compliance and billing rules allow those services to be delivered outside hospitals.

Geography Analysis

North America accounted for 36.43% of the retinal vein occlusion market share in 2025. The region benefits from established retina specialist networks, strong adoption of AAO-guided anti-VEGF care, and broad access to advanced imaging. Canada widened public access in 2025 when faricimab reimbursement expanded in Ontario and Quebec. That expansion extends access beyond private insurance and supports treatment continuity for RVO-related macular edema. North America therefore remains the reference market for high-value biologic use and structured follow-up care.

Europe held the second-largest share of the retinal vein occlusion market in 2025. Access is being shaped by national reimbursement pathways rather than a single regional decision, which creates uneven but expanding uptake. France issued a positive faricimab reimbursement decision, and Spain published a therapeutic positioning report that recognized faricimab as an equivalent first-line alternative to ranibizumab and aflibercept. This mix of national assessments is likely to sustain differences in treatment access and pricing across the region.

Asia-Pacific is projected to record the fastest growth in the retinal vein occlusion market, with a 9.18% CAGR through 2031. Growth is supported by a large future patient base in Asia, by China’s expanding retinal care pathway, and by Japan’s evidence that delayed anti-VEGF initiation beyond 28 days can worsen long-term vision outcomes. The Phase IV YANGTZE study also showed strong 12-month follow-up completion in Chinese patients on dexamethasone implant therapy, which points to strengthening treatment infrastructure in hospital-based ophthalmology. Middle East, Africa, and South America remain smaller contributors, but government-led retinal screening in GCC systems and Mexico’s public assessment of aflibercept point to a gradual build-out of access models outside the largest regions.

Competitive Landscape

The retinal vein occlusion market showed a moderately concentrated structure in 2025, with Roche and Genentech on one side and Regeneron and Bayer on the other holding the strongest branded positions. Competition is centered on durability, treatment interval, and the ability to protect formulary access as follow-up care moves toward longer dosing cycles. Roche strengthened its position through wider public reimbursement for faricimab in Canada during 2025, which improved access in 2 major provinces. Regeneron and Bayer still retain strong reach through the established Eylea franchise in major ophthalmology markets. This keeps leadership concentrated among a small group of global ophthalmology players even as price competition widens around them.

The retinal vein occlusion market is also being shaped by pipeline programs that focus on durability and non-VEGF biology. Kodiak Sciences reported that tarcocimab allowed half of Phase 3 BEACON patients to remain injection-free through the second 6 months of the study, and the company later confirmed plans for a single BLA submission spanning wet AMD, RVO, and diabetic retinopathy in 2026. That profile makes tarcocimab the closest late-stage challenge to current branded leaders on treatment interval. AbbVie’s Ozurdex remains relevant in second-line care because lower procedure frequency can matter when repeat anti-VEGF visits are hard to sustain.

Competitive white space is still most visible in patients who do not fit neatly into pure VEGF-driven disease patterns. Current care still separates anti-VEGF, laser, and corticosteroid use by clinical need rather than through an approved combined mechanism that addresses vascular leakage and inflammatory signaling in one product. Imaging-led precision is reinforcing this split because ischemic conversion, DRIL, and other OCT or OCTA markers are guiding escalation choices with greater confidence. As a result, commercial success in the retinal vein occlusion market increasingly depends on pairing durable efficacy with operational simplicity rather than relying on vision gains alone.

Retinal Vein Occlusion Industry Leaders

Amgen Inc.

Bayer AG

Novartis AG

Regeneron Pharmaceuticals, Inc.

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Kodiak Sciences confirmed plans for a single BLA submission covering wet AMD, RVO, and diabetic retinopathy for tarcocimab (Zenkuda), supported by data from 5 Phase 3 studies including the BEACON trial in RVO; this positions Zenkuda as the most advanced new molecular entity seeking FDA approval for RVO within the current forecast window.

- August 2025: Roche Canada announced that faricimab (Vabysmo) is now publicly reimbursed in Ontario under the Ontario Drug Benefit Program for RVO-related macular edema, following Health Canada’s July 2024 authorization. Faricimab is now reimbursed across both Ontario and Quebec for its 3 approved indications, completing its Canadian public access rollout.

- June 2025: Phase IV YANGTZE trial results published in the Open Ophthalmology Journal confirmed that the dexamethasone intravitreal implant (Ozurdex, AbbVie) required a mean of 2.3 injections over 12 months in Chinese RVO patients while achieving significant improvements in BCVA and central retinal thickness, data positioned to support formulary expansion in China’s hospital-based ophthalmic care system.

Global Retinal Vein Occlusion Market Report Scope

Retinal Vein Occlusion (RVO) is a blockage of the veins that drain blood from the retina, making it the second most common retinal vascular disease after diabetic retinopathy. The blockage causes fluid and blood to leak into the retina, often leading to macular edema and sudden, painless vision loss.

The Retinal Vein Occlusion (RVO) Market is structured across several key dimensions that reflect the complexity of the condition and its management. By disease type, it is segmented into Branch Retinal Vein Occlusion (BRVO), Central Retinal Vein Occlusion (CRVO), and Hemiretinal Vein Occlusion. In terms of condition, the market distinguishes between ischemic and non-ischemic forms. The treatment modalities include Anti-VEGF therapies, corticosteroids, laser treatments, and combination approaches. By end user, the market is segmented into hospitals, ophthalmology clinics, retina centers, and ambulatory surgical centers (ASCs). Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa (MEA), and South America. Forecasts are provided in terms of market value (USD), highlighting the expected financial trajectory of this therapeutic area.

| Branch Retinal Vein Occlusion |

| Central Retinal Vein Occlusion |

| Hemiretinal Vein Occlusion |

| Ischemic Retinal Vein Occlusion |

| Non-ischemic Retinal Vein Occlusion |

| Anti-VEGF Therapy | Aflibercept |

| Faricimab | |

| Ranibizumab | |

| Bevacizumab | |

| Biosimilar Ranibizumab | |

| Biosimilar Aflibercept | |

| Corticosteroid Therapy | Dexamethasone Intravitreal Implant |

| Intravitreal Triamcinolone | |

| Laser Therapy | Grid Laser Photocoagulation |

| Scatter Panretinal Photocoagulation | |

| Combination Therapy |

| Hospitals |

| Ophthalmology Clinics and Retina Centers |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Branch Retinal Vein Occlusion | |

| Central Retinal Vein Occlusion | ||

| Hemiretinal Vein Occlusion | ||

| By Condition | Ischemic Retinal Vein Occlusion | |

| Non-ischemic Retinal Vein Occlusion | ||

| By Treatment Modality | Anti-VEGF Therapy | Aflibercept |

| Faricimab | ||

| Ranibizumab | ||

| Bevacizumab | ||

| Biosimilar Ranibizumab | ||

| Biosimilar Aflibercept | ||

| Corticosteroid Therapy | Dexamethasone Intravitreal Implant | |

| Intravitreal Triamcinolone | ||

| Laser Therapy | Grid Laser Photocoagulation | |

| Scatter Panretinal Photocoagulation | ||

| Combination Therapy | ||

| By End User | Hospitals | |

| Ophthalmology Clinics and Retina Centers | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value for retinal vein occlusion by 2031?

The retinal vein occlusion market is forecast to reach USD 3.79 billion by 2031, up from USD 2.68 billion in 2025, at a 6.1% CAGR over 2026 to 2031.

Which treatment type leads revenue in retinal vein occlusion care?

Anti-VEGF therapy led treatment revenue with a 39.98% share in 2025 because it remains the first-line approach for macular edema secondary to RVO.

Why is central retinal vein occlusion growing faster than branch retinal vein occlusion?

CRVO is projected to grow at an 8.23% CAGR through 2031 because OCTA-based biomarkers are improving detection of ischemic conversion and helping clinicians escalate treatment earlier.

Which care setting is growing fastest for RVO treatment?

Ophthalmology clinics and retina centers are the fastest-growing end-user group, with a 10.02% CAGR through 2031, supported by longer treatment intervals that reduce visit pressure.

Which region leads current revenue and which region is growing fastest?

North America led with 36.43% share in 2025, while Asia-Pacific is expected to grow fastest at a 9.18% CAGR through 2031.

Page last updated on: