Retail and E-Commerce IT Sustainability Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 7.20 Billion |

| Growth Rate (2026 - 2031) | 16.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retail and E-Commerce IT Sustainability Software Market Analysis by Mordor Intelligence

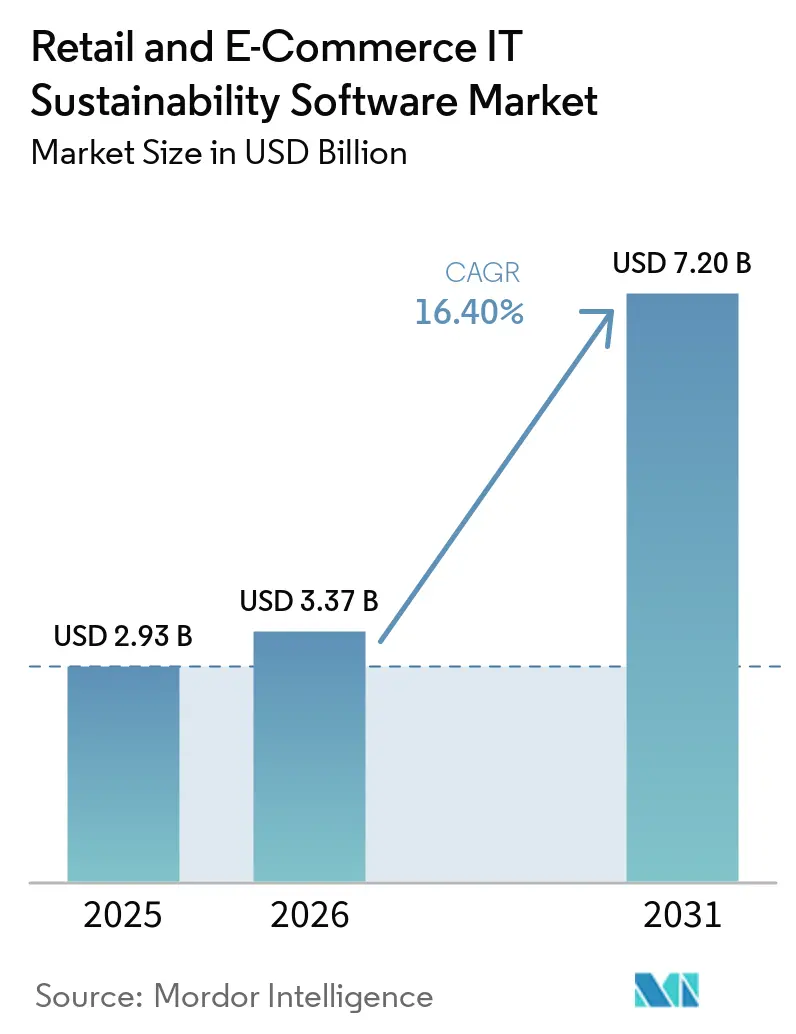

The retail and e-commerce IT sustainability software market size is projected to expand from USD 2.93 billion in 2025 and USD 3.37 billion in 2026 to USD 7.20 billion by 2031, registering a CAGR of 16.40% between 2026 and 2031. The retail and e-commerce IT sustainability software market is moving from a reporting-focused software category into a core operating system for procurement, product claims, supplier engagement, and investor communication. Adoption is rising because disclosure rules, product traceability requirements, and audit expectations are tightening across major retail regions in a short time frame, leaving less room for delayed spending decisions. The retail and e-commerce IT sustainability software market is also benefiting from the growing need to connect carbon data, supplier records, packaging information, and governance workflows within a single, controlled environment. Demand is widening beyond large listed retailers because compliance requirements are now flowing through contracts and supplier scorecards, which brings smaller vendors into the same data architecture. Competitive conditions remain moderate to high, and the strongest opportunities are forming around hybrid deployment, multi-tier supplier data management, and tools that can keep pace with changing reporting frameworks without repeated reconfiguration.

Key Report Takeaways

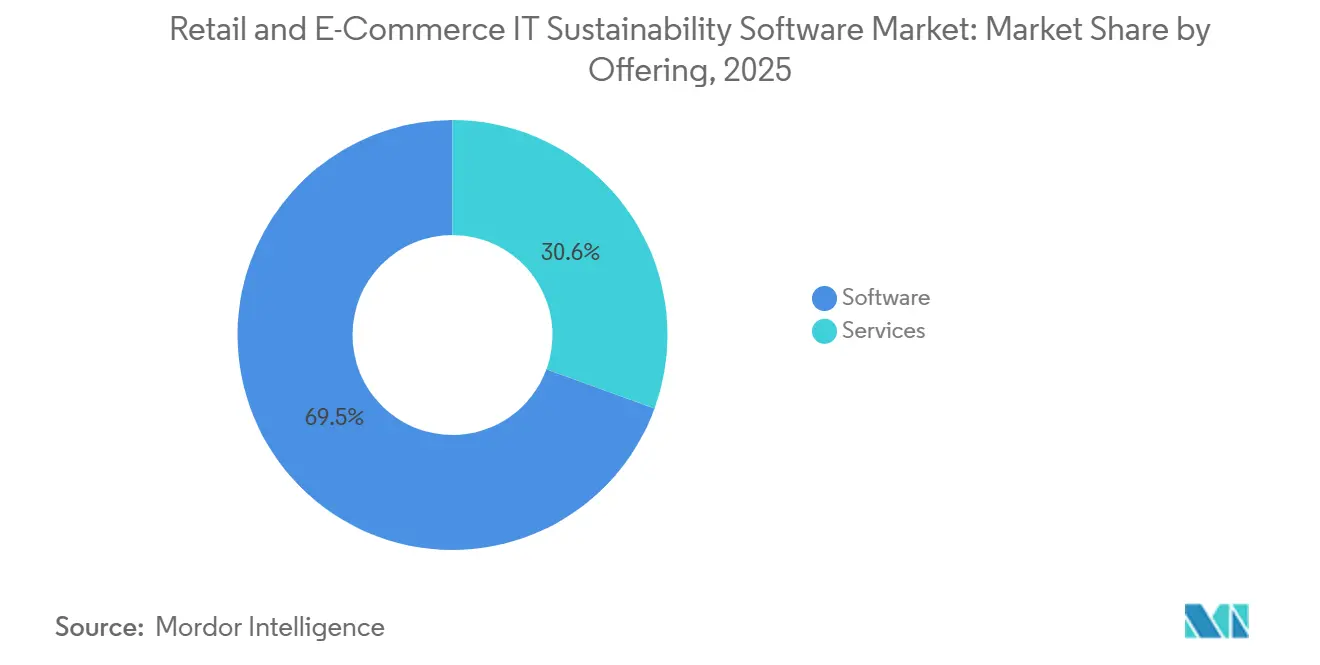

- By offering, software held 69.45% of the retail and e-commerce IT sustainability software market in 2025, while services are projected to expand at a 16.92% CAGR through 2031.

- By deployment, cloud captured 66.12% of the market in 2025, while hybrid is expected to record the fastest growth at a 16.78% CAGR through 2031.

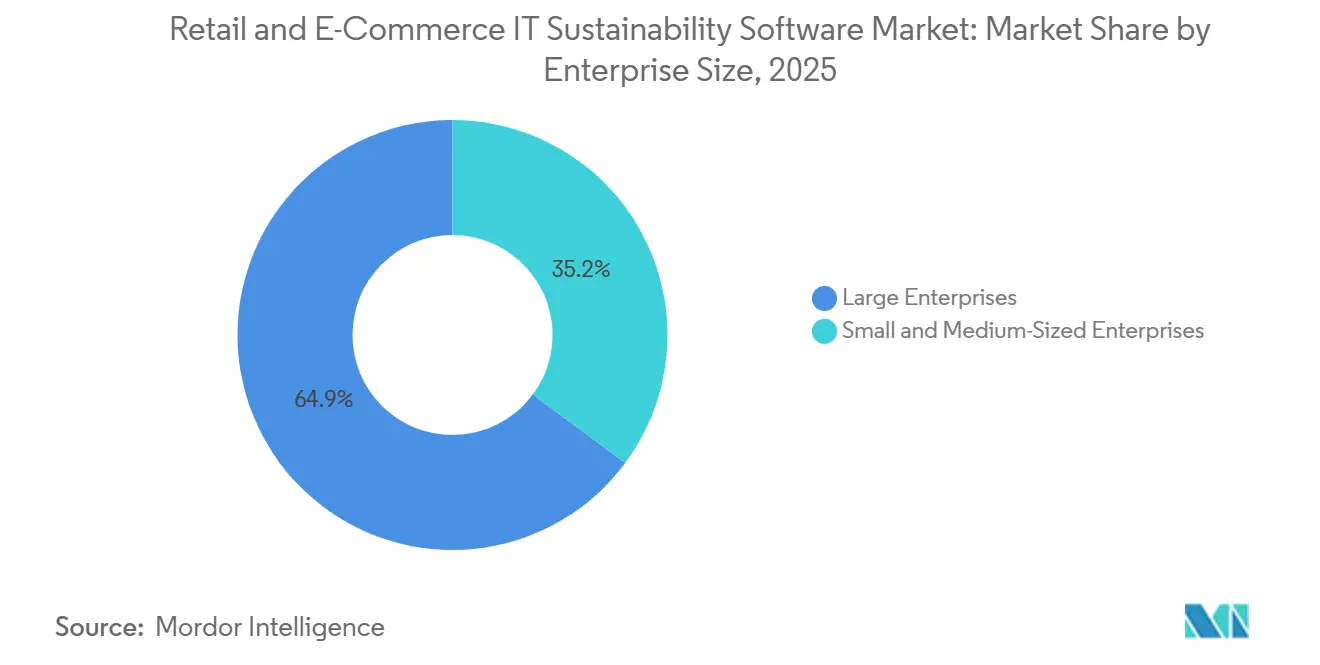

- By enterprise size, large enterprises accounted for 64.85% of the market share in 2025, while SMEs are projected to grow at a 16.55% CAGR through 2031.

- By functionality, carbon accounting and emissions management software accounted for 28.74% of the market in 2025, while supply chain ESG and supplier sustainability management are projected to expand at a 17.05% CAGR through 2031.

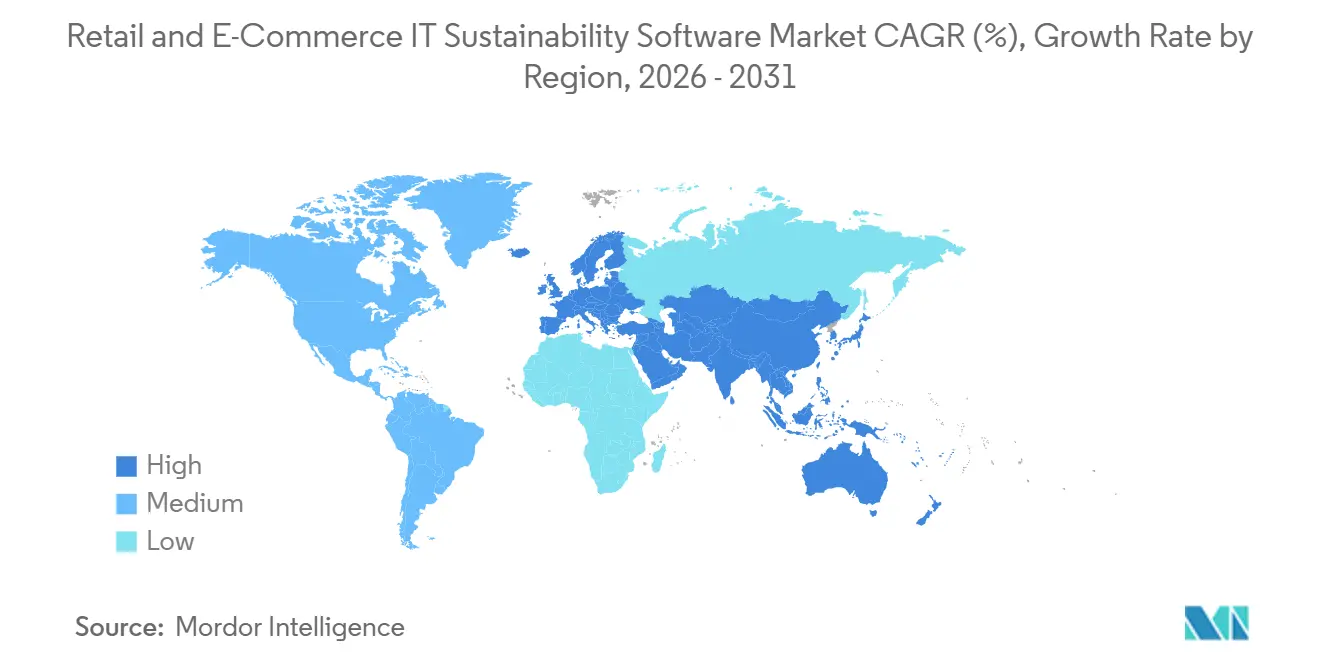

- By geography, Europe held 34.56% share in 2025, while Asia-Pacific is projected to advance at a 17.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Retail and E-Commerce IT Sustainability Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance for ESG Disclosure and Audit Readiness | +5.5% | Global, most acute in Europe and North America, with rising exposure in Asia-Pacific | Short term (≤ 2 years) |

| Retailer Pressure to Prove Scope 3 and Product Footprint Integrity | +3.8% | Global, with early pull from Europe followed by North America | Short term (≤ 2 years) |

| Shift From Spreadsheet Workflows to Enterprise Sustainability Data Platforms | +2.2% | Global, strongest in Europe, North America, and Asia-Pacific enterprise retail | Medium term (2-4 years) |

| AI-Enabled Sustainability Reporting and Exception Detection | +1.7% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Omnichannel Retail Complexity Increasing Traceability Demand | +1.3% | North America, Europe, and Asia-Pacific urban retail corridors | Medium term (2-4 years) |

| Supplier Scorecarding for Sustainable Procurement and Private Label Risk Control | +1.1% | Global, strongest in Europe private label retail and North American direct-to-consumer brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance for ESG Disclosure and Audit Readiness

Regulatory disclosure requirements have moved from voluntary reporting into binding compliance across several retail markets within a short period, and that shift is accelerating platform purchases in the retail and e-commerce IT sustainability software market. In Europe, CSRD-related amendments entered into force in March 2026 and maintained ESRS-aligned reporting obligations for large in-scope companies, thereby preserving demand for disclosure systems built on structured, repeatable reporting workflows.[1]FDM Law, “Omnibus Enters Into Force, Largely Amending CSRD and CS3D,” FDM Law The next layer of pressure comes from consumer-facing environmental claims, as the Empowering Consumers Directive takes effect on September 27, 2026, and extends scrutiny from annual reports to product pages, packaging, and delivery communications used by retailers and e-commerce operators. India also expanded BRSR Core assurance requirements for large listed companies for the fiscal year 2026-27, which adds another audit-driven reporting burden for retail groups and suppliers tied to those issuers. As a result, the retail and e-commerce IT sustainability software market is favoring platforms that can support multiple frameworks, preserve documentation trails, and produce outputs that remain usable when the same retailer must satisfy different reporting regimes simultaneously. Vendors that rely on single-framework configurations face slower adoption, as retailers increasingly need systems that can absorb regulatory changes without restarting implementation work.

Retailer Pressure to Prove Scope 3 and Product Footprint Integrity

The retail and e-commerce IT sustainability software market is benefiting from a direct shift in buyer expectations, as retailers now need product- and supplier-level evidence to support Scope 3 accounting and sustainability claims. Lower-tier supplier visibility remains weak across many retail value chains, so the commercial problem is not only collecting data but also securing reliable data from suppliers that view their upstream relationships as sensitive. Worldly expanded its Product Impact Calculator to 400,000 products across more than 260 consumer goods categories in February 2026, which shows that product-level Scope 3 modeling is moving beyond narrow pilots and into broader operational use. That change matters because retailers need primary supplier data and defensible item-level records well before Digital Product Passport obligations begin affecting selected categories. The retail and e-commerce IT sustainability software market is, therefore, rewarding vendors that can validate, normalize, and link Tier 2 and Tier 3 supplier inputs rather than relying solely on broad spend-based estimates. Premium contract value is shifting toward tools that help retailers defend product claims during audits and customer reviews, not just calculate a high-level carbon footprint.

Shift From Spreadsheet Workflows to Enterprise Sustainability Data Platforms

The retail and e-commerce IT sustainability software market is moving away from spreadsheet-led reporting because sustainability data in retail now spans ERP, procurement, logistics, product, packaging, and commerce systems simultaneously. In omnichannel operations, disclosure-ready reporting typically requires inputs from several enterprise systems, and manual consolidation becomes unstable once assurance requirements tighten and timelines shorten. OECD analysis on retail SME digitalization showed that cloud computing adoption in EU retail rose from 14% in 2014 to 39% in 2023, creating a stronger base for connected software workflows, even though integration complexity remains.[2]Organisation for Economic Co-operation and Development, “The Twin Transition of Retail SMEs, Local Retail, Global Trends,” OECD Workiva’s leadership recognition in ISG’s 2025 sustainability software assessment reflected this broader shift, as buyers are increasingly selecting governed platforms that combine data automation, reporting, and controls rather than maintaining disconnected reporting files. The retail and e-commerce IT sustainability software market is therefore favoring vendors with native connectors and implementation models that reduce the effort required to consolidate retail data into a single reporting structure. Platforms that reduce deployment friction are also improving budget approval rates, because retailers can tie software spending to measurable compliance readiness rather than treating it as an open-ended transformation project.

AI-Enabled Sustainability Reporting and Exception Detection

The retail and e-commerce IT sustainability software market is also being lifted by AI tools that reduce manual review work, speed up scenario analysis, and help teams identify unusual data before it reaches an auditor or regulator. SAP announced in May 2026 that its sustainability AI agents, including tools for footprint optimization, regulatory readiness, and packaging compliance, would become generally available by the end of 2026, with beta programs showing large reductions in review time and compliance errors.[3]EcoVadis, “EcoVadis Continues Expansion of Carbon Data Network With Workiva,” EcoVadis Persefoni launched its Analytics Agent in May 2026 to enable natural language queries against emissions data within the platform, signaling a broader move toward more accessible analysis for finance, procurement, and sustainability teams. In practical terms, AI matters most where retail teams need to detect supplier anomalies, incomplete product records, and reporting inconsistencies that can pass ordinary review but create problems during assurance. The retail and e-commerce IT sustainability software market is therefore placing more value on audit-traceable automation than on generic AI messaging. Vendors that embed AI into core reporting and data-quality workflows are strengthening retention by speeding compliance work without removing the controlled structure that regulated reporting still requires.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Cost Across ERP, PIM, POS, and Supply Chain Systems | -3.5% | Global, most acute in SME-heavy markets in Asia-Pacific and South America, and material in North American mid-market retail | Medium term (2-4 years) |

| Fragmented Supplier Data and Low Traceability in Tier 2 and Tier 3 Networks | -2.7% | Global, structurally most severe in Asia-Pacific and South America manufacturing supply networks | Long term (≥ 4 years) |

| Shortage of Retail Sustainability Analytics Talent and ESG Control Owners | -1.8% | Global, most acute in Asia-Pacific SME retail and South American markets | Medium term (2-4 years) |

| Reporting Standard Volatility Causing Reconfiguration and Compliance Rework | -1.2% | Europe and North America primarily, with secondary exposure in Asia-Pacific jurisdictions adopting ISSB-aligned frameworks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Cost Across ERP, PIM, POS, and Supply Chain Systems

The retail and e-commerce IT sustainability software market still faces a significant barrier: the cost of connecting sustainability platforms to the systems retailers already use for products, transactions, suppliers, inventory, and logistics. Many omnichannel retailers operate across 5 to 7 major enterprise systems, and the cost of linking those environments can approach the value of the software license itself when data models do not align. Stronger cloud adoption has improved baseline infrastructure, but it has not removed the work needed to standardize APIs and reconcile data structures across vendor ecosystems. SAP’s 2026 roadmap updates for Sustainability Control Tower also highlighted the importance of embedded reporting and broad ERP connectivity, which reflects how much buyers still value systems that reduce integration effort at the source. This burden is heaviest in the mid-market, where legacy architecture and smaller implementation teams lengthen deployment cycles and delay compliance gains. The retail and e-commerce IT sustainability software market is likely to see faster adoption as vendors offer certified connectors and prebuilt retail workflows, rather than requiring custom integration at each step.[4]SAP, “SAP Sustainability Control Tower, Q1-Q2 2026 Updates and Roadmap Highlights,” SAP Community

Fragmented Supplier Data and Low Traceability in Tier 2 and Tier 3 Networks

Fragmented supplier data remains a durable constraint on the sustainability software market for retail and e-commerce IT, as lower-tier traceability still falls short of the quality level regulators and enterprise buyers now expect. The core problem is structural: supply chains do not operate as a single, transparent line, and information quality declines as data moves from one supplier tier to the next. EcoVadis reported in 2026 that its Carbon Data Network aggregates sustainability performance data from more than 175,000 organizations across 250 industries and 185 countries, which shows the scale of effort required to improve primary supplier data coverage. Sphera’s 2025 N-Tier launch also reflected the same constraint, since the product was designed to improve visibility into complex supplier structures using a mix of automated detection, human validation, and supplier engagement. Even with stronger software, many retailers will still rely on estimation methods and uncertainty disclosure for part of their supplier footprint throughout the forecast period. The retail and e-commerce IT sustainability software market can reduce this gap, but it cannot fully remove the commercial reluctance that still limits upstream transparency in multi-tier sourcing networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads While Services Expand With Ongoing Compliance Needs

Software accounted for 69.45% of the retail and e-commerce IT sustainability software market in 2025, which confirmed that the platform layer remained the center of spending across carbon accounting, ESG disclosure, supply chain analytics, and scenario modeling. This concentration developed because large retailers first needed a governed system of record before they could scale supplier data requests, disclosure preparation, or sustainability planning across multiple business units. The software layer also aligns with the first phase of enterprise buying, where retailers prioritized platform selection, internal data structure, and reporting controls over longer-term operational services. In that sense, the retail and e-commerce IT sustainability software market followed a pattern seen in earlier enterprise software cycles, where foundational platforms attracted the first wave of budget allocation. Even so, the early software lead does not mean services are secondary, because the next stage of buyer demand is increasingly focused on implementation quality, audit support, and cross-system configuration.

Services are projected to grow at a 16.92% CAGR from 2026 to 2031, indicating that the retail and e-commerce IT sustainability software market is shifting from license acquisition to everyday operational use. Retailers moving away from spreadsheet-led ESG workflows often need support for data migration, connector setup, governance design, and first-cycle reporting before they can rely on the platform with confidence. The need for recurring support is also rising as compliance frameworks continue to evolve, requiring retailers to regularly update workflow logic, controls, and documentation standards. Workiva’s strength in multi-framework reporting and automation illustrates why providers that pair software with service depth are positioned well as customers move from initial deployment into repeat reporting cycles. The retail and e-commerce IT sustainability software industry is therefore becoming more relationship-driven, with managed support and advisory execution playing a larger role in renewal and upsell decisions. Vendors that build scalable services teams alongside the platform are likely to capture a greater share of recurring compliance spending over time.

By Deployment: Cloud Remains the Core Model While Hybrid Gains Ground

Cloud deployment captured a 66.12% share in 2025, reflecting the strong fit between SaaS delivery and the distributed operating model used by modern retailers and e-commerce groups. Cloud systems are easier to scale across countries, business units, and reporting teams, and they support faster updates when disclosure templates, packaging rules, or reporting logic change. That made cloud a practical first choice for retailers looking to set up multi-country reporting without waiting for lengthy local infrastructure projects. The retail and e-commerce IT sustainability software market size for cloud remained ahead because enterprise buyers still value centralized administration, lower maintenance burden, and easier access to new features. At the same time, pure cloud is not always sufficient when supplier records, private-label data, or jurisdiction-specific governance requirements require tighter data control.

Hybrid deployment is projected to expand at a 16.78% CAGR from 2026 to 2031, which signals that enterprise buyers increasingly want flexibility rather than an all-or-nothing architecture. Retailers can use the cloud for reporting scale and collaboration while keeping commercially sensitive records in governed, local, or on-premises environments. SAP’s 2026 Sustainability Control Tower updates showed why this model is gaining traction: the company emphasized audit-ready reporting, AI support, and broader coverage across different ERP environments rather than a narrow, single-stack setup. The retail and e-commerce IT sustainability software market is also seeing adjacent service demand rise as hybrid adoption increases, since retailers need middleware, orchestration, and controlled data lineage across systems. Over time, hybrid will appeal most to large omnichannel operators that need both reporting scale and tighter handling of supplier-sensitive information. Vendors without credible hybrid options may remain relevant in simpler use cases, but they risk losing more complex enterprise programs.

By Enterprise Size: Large Enterprises Dominate While SMEs Enter Through Compliance Cascades

Large enterprises held 64.85% of the retail and e-commerce IT sustainability software market share in 2025, which reflected their earlier exposure to listed-company disclosure obligations and their stronger ability to fund multi-system sustainability deployments. These retailers were usually the first to face board-level pressure, investor scrutiny, and assurance requirements, so they built formal data architectures sooner than smaller peers. Their spending also had a wider scope because large retailers needed to connect sustainability data across stores, digital channels, sourcing offices, and supplier networks in several countries. The retail and e-commerce IT sustainability software market, therefore, developed first around the needs of major enterprise buyers, especially those with public reporting obligations and complex product assortments. That early lead is likely to remain important because large organizations continue to set many of the data standards that suppliers must follow.

SMEs are projected to grow at a 16.55% CAGR from 2026 to 2031, and this pace is being driven more by customer requirements than by direct regulation in most cases. The strongest trigger is the compliance cascade, in which large retailers embed ESG data requests into contracts, scorecards, and renewal terms that smaller suppliers cannot easily ignore. Data on retail digitalization suggests that SMEs now have a stronger infrastructure base for SaaS adoption than in earlier years, reducing one of the practical barriers to entry. TrusTrace’s One Retail Hub launch in February 2026 also demonstrated how shared, lower-cost infrastructure can reduce onboarding time for supplier compliance workflows that would otherwise be too resource-intensive for smaller firms. The retail and e-commerce IT sustainability software industry is likely to see SME adoption accelerate most when large retailer procurement teams begin enforcing common data templates across broader supplier groups. That makes SME growth durable, but it also means adoption timing will differ across retail chains and sourcing model rather than following a single universal schedule.

By Functionality: Carbon Accounting Leads While Supply Chain ESG Advances the Fastest

Carbon accounting and emissions management software accounted for 28.74% of the functionality segment in 2025, making it the largest functional block in the retail and e-commerce IT sustainability software market. This leadership stems from the fact that most retailers still begin with emissions measurement before moving into broader reporting, scenario planning, or supplier engagement. Scope 1 and Scope 2 reporting remains the operational entry point for many organizations, and that keeps carbon accounting relevant for both new adopters and companies already expanding their disclosure maturity. Sustainability reporting and disclosure software remains close behind because raw emissions data becomes useful to regulators and investors only when it is mapped, tagged, reviewed, and documented within a controlled reporting process. Sustainability analytics, forecasting, and scenario modeling add another layer, since boards and operating teams increasingly want to test the financial and sourcing effects of different decarbonization paths.

Supply chain ESG and supplier sustainability management is projected to grow at a 17.05% CAGR through 2031, which makes it the fastest-growing functional area in the retail and e-commerce IT sustainability software market. That pace reflects a clear shift from facility-level and corporate reporting toward deeper supplier evidence, product traceability, and category-level footprint data. EcoVadis and Workiva announced a strategic partnership in May 2026 that linked supplier carbon data from EcoVadis’ Carbon Data Network with Workiva Carbon’s calculation and disclosure workflows, demonstrating how the functional focus is shifting toward primary supplier data rather than broad averages. Worldly’s February 2026 expansion of product-level Scope 3 modeling across 260+ categories points in the same direction, as retailers increasingly need functionality that works at the product and supplier levels rather than only at the total company level. The retail and e-commerce IT sustainability software market share is likely to shift gradually toward vendors that can normalize fragmented supplier data and preserve an audit-ready trail for item-level sustainability claims. In practical terms, the fastest functional growth is coming from the part of the stack that connects retailer promises with supplier evidence.

Geography Analysis

Europe accounted for 34.56% of the retail and e-commerce IT sustainability software market in 2025, making it the leading regional contributor to revenue during the period. The region’s position stems from the density of sustainability rules that affect retail reporting, packaging obligations, and consumer-facing environmental claims simultaneously. CSRD-related changes remained active in 2026, while the Packaging and Packaging Waste Regulation and the Empowering Consumers Directive added operational pressure that extends from annual reporting into product communication and e-commerce presentation. The United Kingdom also continued to shape demand by tightening oversight of misleading environmental claims, which kept governance and documentation requirements high for retailers serving European consumers. Within this setting, the retail and e-commerce IT sustainability software market size remains supported not only by large multinationals but also by mid-market operators that must respond to compliance expectations flowing through their customer and supplier relationships.

Asia-Pacific is projected to grow at a 17.12% CAGR from 2026 to 2031, which makes it the fastest-growing region in the retail and e-commerce IT sustainability software market. Growth is being supported by a near-concurrent rollout of ISSB-aligned or expanded sustainability disclosure requirements across several major economies, including Japan, Australia, South Korea, Singapore, China, and India, during the 2025 to 2027 window. The region’s role as the main production base for many global retail supply chains also means software demand is driven by export exposure and retailer-led supplier requests, not solely by domestic listed company regulation. That dual pressure gives Asia-Pacific a broader adoption base, as manufacturers, sourcing partners, and retail groups are drawn into the same compliance data chain.

North America remains commercially important, even though the retail and e-commerce IT sustainability software market is not the regional leader in either share or growth rate. California’s climate disclosure pathway continued to matter in 2026, even as federal uncertainty increased, helping preserve software demand among large retailers doing business in the state. South America is a smaller but active part of the retail and e-commerce IT sustainability software market, with Brazil standing out as a region where companies align with export-linked sustainability expectations and local reporting practices. SAP’s extension of Sustainability Footprint Management into the Brazil São Paulo AWS region in late 2025 reflected this growing demand for localized carbon accounting infrastructure. The Middle East is seeing rising interest as large retail groups and national sustainability agendas push for better ESG data infrastructure, while Africa remains earlier stage, with adoption centered on export-oriented and listed entities. Across these geographies, the retail and e-commerce IT sustainability software market is expanding in scope, but adoption speed still depends heavily on the strength of regulatory enforcement and on how firmly large retailers embed data requirements in supplier contracts.

Competitive Landscape

The retail and e-commerce IT sustainability software market is moderately fragmented, with broad enterprise software platforms, specialized carbon accounting providers, and supplier-network-focused ESG tools all competing across overlapping use cases. SAP, Salesforce, IBM, Workiva, Persefoni, Sphera, Cority, EcoVadis, and Intelex operate within the same broader field, but they do not compete on the same terms in every deal. Some vendors lead with finance-linked disclosure and control environments, some focus on emissions calculation and scenario analysis, and others compete through supplier data depth and network coverage. That structure means procurement decisions in the retail and e-commerce IT sustainability software market often depend on integration depth, regulatory coverage, and the buyer’s need for supplier-level data rather than on price alone. It also means that no single model has become the default architecture for all retailer use cases, which keeps the competitive field open. Buyers are increasingly choosing between modular partnerships and broader suites rather than assuming a single platform should manage every sustainability workflow.

Strategic moves in 2025 and 2026 indicate that the retail and e-commerce IT sustainability software market is evolving through specialization and partnerships rather than simple category consolidation. EcoVadis and Workiva formed a strategic partnership in May 2026 to connect supplier carbon data with calculation and disclosure workflows, demonstrating a model in which one provider provides primary supplier intelligence and another handles reporting execution. SAP took a different approach when it expanded its sustainability AI agent portfolio in 2026, aiming to deepen automation within an existing enterprise software environment that many retailers already use. Sphera also strengthened its position through the 2025 N-Tier launch, which addressed one of the most persistent pain points in the retail and e-commerce IT sustainability software market, deeper supplier visibility across complex sourcing networks. These moves suggest that competitive advantage is shifting toward vendors that can solve a specific data problem well and then connect that capability into a broader reporting chain. The result is a market where interoperability and workflow fit matter as much as headline functionality lists.

The most contested opening remains the mid-market, where retailers and suppliers want compliance-grade tools but still struggle with cost, integration effort, and internal staffing limits. TrusTrace’s One Retail Hub launch is a good example of how vendors are trying to reduce those barriers by giving suppliers a shared starting point for due diligence and reporting workflows. Cority and Intelex have also continued to push product enhancements in 2026, especially around AI-assisted compliance and emissions workflow management, which shows that adjacent EHS and compliance providers still see room to win share in this space. Even with those moves, the retail and e-commerce IT sustainability software market is unlikely to settle quickly into a winner-takes-most structure, as customer needs vary sharply by region, retailer size, deployment preferences, and supplier model. Providers with strong standards coverage and faster update cycles have an advantage when reporting rules change, but they still need deep integration and credible partner ecosystems to keep that advantage. Over the forecast period, the strongest competitive positions are likely to belong to vendors that combine audit-ready reporting, product and supplier traceability, and workable deployment paths for both large enterprises and smaller supply-chain participants.

Retail and E-Commerce IT Sustainability Software Industry Leaders

SAP SE

Salesforce, Inc.

IBM Corporation

Workiva Inc.

OneTrust, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP announced that its sustainability AI agents, including the Footprint Optimization Agent, Sustainability Regulatory Readiness Agent, and Packaging Compliance Agent, will be generally available by end of 2026. Beta program results demonstrated packaging compliance review hours reduced by over 50%, scenario simulation time cut from 1 day to 20 minutes, and packaging compliance errors reduced by more than 20%. The agents automate multi-step workflows across sustainability reporting preparation, packaging compliance assessment, and carbon footprint simulation within SAP Sustainability Control Tower.

- May 2026: EcoVadis and Workiva announced a strategic partnership expanding EcoVadis' Carbon Data Network, connecting primary supplier carbon emissions data with Workiva Carbon's calculation and disclosure platform. The collaboration enables mutual customers to replace spend-based industry averages with granular, audit-ready Scope 3 supplier data, addressing the primary data gap that has undermined retailer Scope 3 disclosure credibility. EcoVadis serves as the data engine for supplier engagement and upskilling, while Workiva handles calculation and disclosure in a single audit-ready environment.

- April 2026: Cority won two 2026 Environment+Energy Leader Awards for product innovation in its Compliance Permit Analysis Agent and Next-Gen Emissions Calculation Management Toolset, both built under the Cortex AI framework introduced in December 2025 and designed to help organizations manage environmental compliance with greater accuracy across complex operations.

- February 2026: TrusTrace launched One Retail Hub, a free AI-assisted supply chain compliance platform co-developed with 7 fashion retailers to standardize human rights and environmental due diligence reporting. AI-assisted completion reduces self-assessment time from 3-4 weeks per retailer to 4-6 days, with instant multi-retailer data sharing and actionable gap analysis.

Global Retail and E-Commerce IT Sustainability Software Market Report Scope

The Retail and E-Commerce IT Sustainability Software market refers to platforms and services that enable retail and e-commerce enterprises to integrate sustainability intelligence into their IT operations, digital commerce platforms, and supply chain ecosystems. These solutions provide functionalities such as carbon accounting and emissions management, sustainability reporting and disclosure, supplier ESG and sustainability tracking, and advanced analytics for forecasting and scenario modeling. By embedding sustainability into IT and commerce workflows, these platforms help organizations reduce energy consumption, optimize IT asset utilization, ensure compliance with ESG frameworks, and improve transparency across digital supply chains.

The Retail and E-Commerce IT Sustainability Software market report is segmented by Offering (Software, and Services), Deployment (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Functionality (Carbon Accounting and Emissions Management Software, Sustainability Reporting and Disclosure Software, Supply Chain ESG and Supplier Sustainability Management, and Sustainability Analytics, Forecasting and Scenario Modeling), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Carbon Accounting and Emissions Management Software |

| Sustainability Reporting and Disclosure Software |

| Supply Chain ESG and Supplier Sustainability Management |

| Sustainability Analytics, Forecasting and Scenario Modeling |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Software | |

| Services | ||

| By Deployment | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Functionality | Carbon Accounting and Emissions Management Software | |

| Sustainability Reporting and Disclosure Software | ||

| Supply Chain ESG and Supplier Sustainability Management | ||

| Sustainability Analytics, Forecasting and Scenario Modeling | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of retail and e-commerce IT sustainability software?

The retail and e-commerce IT sustainability software market stood at USD 2.93 billion in 2025, reaches USD 3.37 billion in 2026, and is forecast to hit USD 7.20 billion by 2031 at a 16.40% CAGR.

What is driving adoption of sustainability software in retail and e-commerce?

The main drivers are tighter ESG disclosure rules, product-level traceability needs, supplier data requirements, and the shift from spreadsheet reporting to governed enterprise platforms.

Which offering category leads spending?

Software led with 69.45% share in 2025 because retailers first needed a core platform for carbon accounting, disclosure workflows, and supplier data management.

Which deployment model is growing the fastest?

Hybrid deployment is projected to grow the fastest at a 16.78% CAGR through 2031 as retailers balance cloud scale with tighter control over sensitive supplier and governance data.

Which functionality is expanding the quickest?

Supply chain ESG and supplier sustainability management is projected to grow at a 17.05% CAGR as retailers move toward primary supplier data and product-level footprint evidence.

Which region is leading and which region is growing the fastest?

Europe led with 34.56% share in 2025 because of its dense compliance environment, while Asia-Pacific is expected to expand the fastest at a 17.12% CAGR through 2031.

Page last updated on: