Responsible AI and Sustainability Governance Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 5.32 Billion |

| Growth Rate (2026 - 2031) | 24.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Responsible AI and Sustainability Governance Platform Market Analysis by Mordor Intelligence

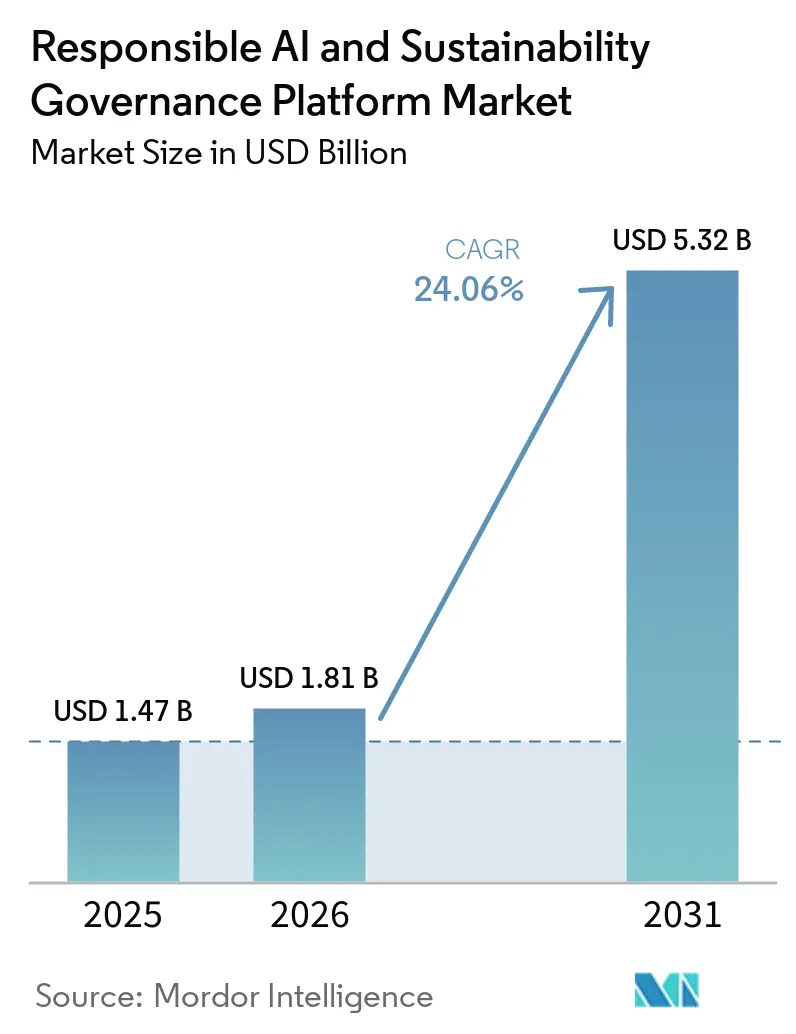

The responsible AI and sustainability governance platform market size is projected to expand from USD 1.47 billion in 2025 and USD 1.81 billion in 2026 to USD 5.32 billion by 2031, registering a CAGR of 24.06% between 2026 and 2031. These platforms bring AI model risk management, bias and fairness controls, ESG data governance, and regulatory disclosure management into a single operating layer, making them more central to enterprise control systems. Demand is rising because boards, audit teams, and regulators now expect companies to show how AI decisions and sustainability disclosures are managed with the same level of discipline. The August 2, 2026, activation of key EU AI Act obligations and the March 18, 2026, entry into force of the EU Omnibus I Directive are pushing multinational companies to move faster on shared governance architecture. Vendor competition is also shifting as buyers favor platforms that integrate policy controls, evidence trails, monitoring, and reporting in a single environment. Growth remains strong, though adoption speed still depends on how companies handle cross-border rule differences and the limited availability of talent that understands both AI governance and sustainability compliance.

Key Report Takeaways

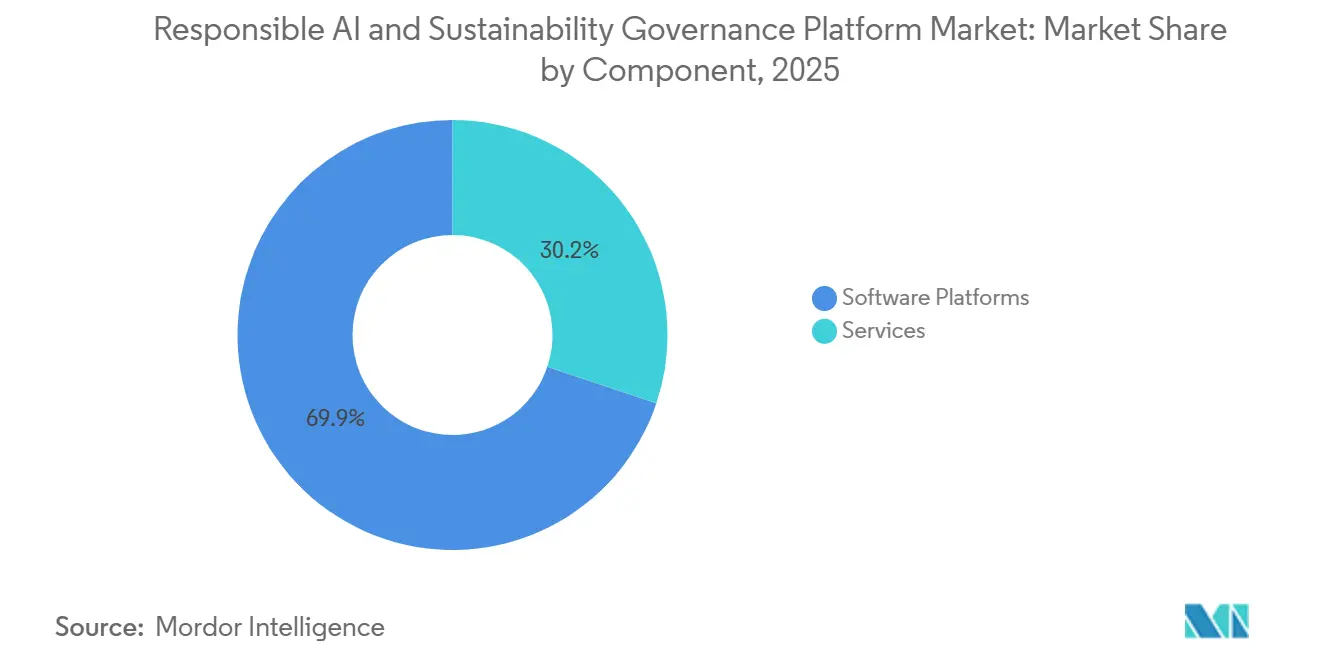

- By component, software platforms held 69.85% of revenue of the responsible AI and sustainability governance platform market in 2025, while services are projected to expand at a 24.78% CAGR through 2031.

- By deployment mode, cloud-based held 66.41% of the responsible AI and sustainability governance platform market share in 2025, while hybrid deployment is expected to record the highest CAGR at 25.12% through 2031.

- By enterprise size, large enterprises accounted for 65.23% of the market share in 2025, while SMEs are projected to grow at a 24.95% CAGR through 2031.

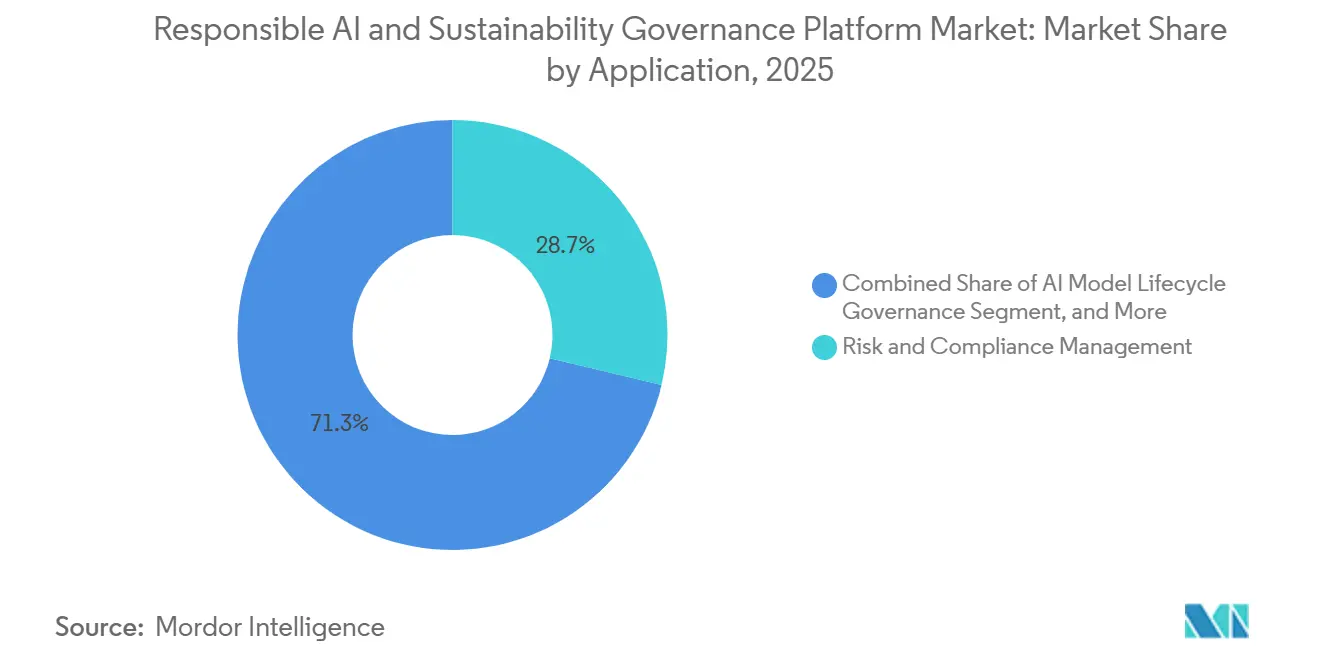

- By application, risk and compliance management represented 28.74% share in 2025, while bias, fairness, and explainability management are expected to expand at a 25.34% CAGR through

- By end-use industry, IT and telecom captured 26.41% share of the responsible AI and sustainability governance platform market in 2025, while retail and e-commerce are projected to advance at a 24.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Responsible AI and Sustainability Governance Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global AI and Sustainability Disclosure Mandates | +5.2% | Global, with highest intensity in Europe and North America | Short term (≤ 2 years) |

| Rising Demand for Audit-Ready AI and ESG Evidence Trails | +4.8% | Global, with adoption concentration in North America and Europe | Short term (≤ 2 years) |

| Expansion of Generative AI and Agentic AI Requiring Continuous Governance | +4.3% | Global, led by North America with rapid acceleration in Asia-Pacific | Medium term (2-4 years) |

| Shift Toward Cloud-Native Governance Architecture and Centralized Control | +3.1% | North America and Europe core, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Convergence of AI Risk, Data Governance, And Sustainability Compliance Workflows | +2.5% | Global, with early mover advantage in BFSI and IT and telecom | Medium term (2-4 years) |

| Board-Level Demand for Quantifiable Trust, Transparency, and Responsible Innovation | +2.0% | Global, especially large enterprises in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global AI and Sustainability Disclosure Mandates

The responsible AI and sustainability governance platform market is moving faster as regulatory obligations for AI and sustainability reporting are converging across major economies. The EU Omnibus I Directive entered into force on March 18, 2026, and confirmed that large companies with material European exposure remain within a stricter disclosure perimeter, which keeps governance spending focused on enterprise-scale buyers.[1]European Council, “Council Signs Off Simplification of Sustainability Reporting and Due Diligence Requirements to Boost EU Competitiveness,” Consilium, consilium.europa.eu The SEC proposed rescinding its 2024 climate disclosure rules on May 29, 2026, and that widened the policy gap between Europe and the United States rather than reducing governance needs for global companies. This has made the responsible AI and sustainability governance platform market more dependent on multinational firms that need a single control framework across multiple jurisdictions. It also shortens buying cycles for companies that cannot delay compliance decisions while separate AI and disclosure rules continue to move forward on different timelines.

Rising Demand for Audit-Ready AI and ESG Evidence Trails

The responsible AI and sustainability governance platform market is also benefiting from the need to keep complete records of how AI systems and sustainability disclosures are produced and reviewed. OneTrust reported that governance teams spent 37% more time managing AI risk in 2025, underscoring why manual evidence gathering is becoming harder to sustain. Companies now need proof that model decisions, policy approvals, source data, and reporting changes can be traced from start to finish. NIST guidance also reinforces the need to document governance, measurement, and risk treatment in a structured manner, thereby supporting platform demand beyond highly regulated sectors.[2]National Institute of Standards and Technology, “Artificial Intelligence Risk Management Framework: Generative Artificial Intelligence Profile,” NIST, nist.gov In the responsible AI and sustainability governance platform market, vendors with strong audit logs, approval histories, and evidence retention are gaining attention because they reduce the risk of failures in separate AI oversight and ESG disclosure review processes.

Expansion Of Generative AI and Agentic AI Requiring Continuous Governance

The responsible AI and sustainability governance platform market is expanding as generative and agentic AI spread, because these systems create a much larger monitoring burden than earlier predictive models. IBM reported in 2026 that enterprises expect to deploy an average of 1,661 AI agents by 2027, and organizations that build governance into design-time processes deploy 16 times more agents than peers using manual oversight.[3]IBM Institute for Business Value, “2026 Tech Leader Study: Building the IT Foundation for Agentic AI at Scale,” IBM, ibm.com The same IBM research found that these organizations also deliver 18% higher operating margins, shifting governance from a pure control function to a scale enabler. This matters for the responsible AI and sustainability governance platform market because autonomous systems need ongoing controls, not one-time reviews, when they act across business processes and external data sources. As enterprises add more agents to customer support, reporting, internal operations, and decision support, they create recurring demand for monitoring, policy enforcement, and documentation tools.

Shift Toward Cloud-Native Governance Architecture and Centralized Control

The responsible AI and sustainability governance platform market is being shaped by a move toward cloud-native control models that can supervise AI systems across multiple environments. Buyers want a single governance layer that can observe models, agents, and data, whether workloads run in the cloud, in a hybrid environment, or on-premises. ServiceNow expanded its AI Control Tower in May 2026 to enable enterprises to discover, observe, govern, secure, and measure AI deployed across any system, reflecting this broader move toward centralized oversight. This trend is driving the responsible AI and sustainability governance platform market, as companies no longer want separate governance tools for each technical estate or reporting workflow. It also supports vendors that can offer remote policy enforcement, consistent evidence capture, and a single operating view across cloud-native and sovereign data environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory Interpretations Across Jurisdictions | -2.8% | Global, most acute in cross-border operations spanning Europe, the United States, and Asia-Pacific | Short term (≤ 2 years) |

| High Integration Complexity Across AI, ESG, and Enterprise Data Stacks | -2.1% | Global, with heightened impact in large enterprises with legacy infrastructure | Medium term (2-4 years) |

| Shortage Of Specialized AI Governance and Sustainability Compliance Talent | -1.6% | Global, particularly acute in emerging markets and mid-market enterprise segments | Medium term (2-4 years) |

| Budget Deferral Among Mid-Market Buyers Facing Multi-System Implementation Costs | -1.2% | North America and Europe, where mid-market adoption is most active | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Interpretations Across Jurisdictions

The responsible AI and sustainability governance platform market still faces friction because companies are trying to align governance programs across rules that differ in scope, legal force, and reporting logic. Europe is moving forward with binding AI and sustainability requirements, while the U.S. federal position on climate disclosure has become less direct following the SEC's rescission proposal in May 2026.[4]U.S. Securities and Exchange Commission, “Rescission of Climate-Related Disclosure Rules,” SEC, sec.gov NIST continues to provide a widely used AI risk management framework, but its role is different from that of a binding rulebook, leaving multinational companies to balance formal compliance in one region with risk-based practices in another. This slows the responsible AI and sustainability governance platform market because buyers want localized policy templates, flexible documentation standards, and reporting logic that can change without a full system rebuild. It also favors larger vendors that can absorb the recurring cost of updating rule libraries and workflow settings across several legal regimes.

High Integration Complexity Across AI, ESG, and Enterprise Data Stacks

The responsible AI and sustainability governance platform market is also constrained by the difficulty of linking AI oversight systems with sustainability reporting, enterprise data platforms, and legacy control tools. NIST guidance makes clear that trustworthy AI governance requires structured measurement, documentation, and continuous management, but those requirements do not automatically map to ESG reporting workflows or materiality frameworks. In practice, companies often need custom data bridges, new taxonomies, and revised approval flows before they can connect model governance with disclosure management. Novisto’s 2026 acquisition of Minimum reflects how vendors are seeking to reduce this burden by integrating carbon accounting and reporting into a more unified system. Even so, implementation can still take longer than buyers expect, delaying revenue recognition for suppliers and pushing some customers to phase adoption over several budget cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Anchor Spending While Services Deepen Adoption

Software platforms captured 69.85% of the responsible AI and sustainability governance platform market in 2025, showing that buyers are prioritizing persistent control systems over project-led support. This segment benefits from subscription revenue, embedded workflows, and long replacement cycles once governance rules are integrated into daily operations. Enterprises typically begin by setting up policy libraries, approval paths, model inventories, and evidence stores within software, rather than relying solely on short-term support. That approach makes software harder to displace after deployment, since governance logic often spans legal, risk, sustainability, data, and technology teams simultaneously. The largest contracts also tend to favor platforms that can support ongoing monitoring, audit preparation, and cross-functional reporting from one interface.

Services are the fastest-growing component, with a 24.78% CAGR through 2031, underscoring that implementation work remains critical even as software dominates the revenue mix. The industry is moving toward a model where advisory, integration, and workflow design accelerate software usability. Credo AI launched advisory services in August 2025, reflecting growing customer demand for hands-on help in translating governance principles into measurable operating controls. Services growth also stems from the fact that many buyers still need support aligning internal ownership across legal, compliance, sustainability, and data teams before software can deliver full value. Over time, service demand is likely to remain strongest in policy customization, evidence readiness, control testing, and change management rather than only in first-time deployment work.

By Deployment Mode: Cloud Leads Today While Hybrid Gains Ground Fast

Cloud-based deployment accounted for 66.41% of the responsible AI and sustainability governance platform market in 2025, supported by easier provisioning, faster updates, and continuous monitoring across large AI estates. Cloud delivery fits this market because enterprises want policy changes, approvals, and alerts to move across many models without long release cycles. It also supports shared governance teams that need one view across business units, geographies, and reporting functions. Buyers often prefer cloud-based tools when governance programs are expanding quickly, and internal teams want less infrastructure overhead. This keeps cloud as the default path for organizations that need speed, scale, and centralized administration.

Hybrid deployment is projected to grow at a 25.12% CAGR through 2031, making it the most important structural shift inside the responsible AI and sustainability governance platform market. Growth is coming from organizations that want cloud-based policy orchestration while keeping sensitive data, audit logs, or core models in on-premises environments. That mix is especially relevant in banking, healthcare, government, and critical infrastructure, where sovereignty and residency requirements remain practical limits to full cloud migration. ServiceNow’s 2026 expansion of AI Control Tower shows how vendors are building governance functions that can operate across deployment settings, rather than requiring a single hosting model. On-premises deployment will remain part of the market for highly restricted workloads, but its growth is likely to remain slower as buyers increasingly seek portability across cloud and on-premises environments.

By Enterprise Size: Large Enterprises Lead While SMEs Enter Through Value-Chain Pressure

Large enterprises held 65.23% share in 2025, reflecting the scale of their AI estates, regulatory exposure, and ability to fund multi-team governance programs. In the responsible AI and sustainability governance platform market, these buyers often manage many models, several reporting standards, and multiple internal review functions simultaneously. The EU Council confirmed in 2026 that the revised sustainability reporting perimeter remains centered on larger companies, which keeps enterprise-scale demand strong. Large firms were also early adopters because they already had model risk, compliance, or disclosure teams that could anchor platform rollouts. Databricks’ 2026 position in unified AI governance platform recognition signals how enterprise data and platform providers are targeting this higher-complexity buyer group.

SMEs are projected to grow at a 24.95% CAGR through 2031, reflecting a different entry path into the responsible AI and sustainability governance platform market. Many smaller firms are not direct targets of every major rule, but they are being asked by larger customers already inside formal reporting frameworks for supplier data, documentation, and evidence. This extends governance requirements through commercial relationships, especially in supply chains where disclosure requests and model accountability records move downstream. OneTrust said in 2025 that it served more than 14,000 global customers, showing that governance platforms are already broadening beyond the largest enterprises. The challenge for vendors is that SME growth depends on simpler onboarding, clearer pricing, and lower implementation effort than large-enterprise products usually require.

By Application: Risk And Compliance Remains The Core While Fairness and Explainability Advance

Risk and compliance management accounted for 28.74% of the responsible AI and sustainability governance platform market size in 2025, making it the main starting point for platform adoption. Most companies begin with risk registers, policy mapping, control ownership, and gap assessment before expanding into more advanced governance modules. This gives the market a strong compliance-first structure, especially in sectors that already operate under formal review and validation routines. Once those controls are established, companies typically add lifecycle tracking, evidence retention, and audit response functions around the same governance core. That is why risk and compliance remain the application areas that tie together legal obligations, board reporting, and operational control.

Bias, fairness, and explainability management is projected to grow at a 25.34% CAGR through 2031, showing that buyers are moving from basic control coverage toward deeper model oversight. NIST guidance emphasizes the need to measure, document, and manage trustworthy AI characteristics in a disciplined way, supporting stronger demand for fairness testing and explanation tools. This part of the market is also expanding because enterprises need to demonstrate not only that reviews occurred, but that uneven outcomes were identified, assessed, and addressed. Explainability is becoming more important as generative and agentic systems enter workflows where outputs affect reporting, recommendations, approvals, and customer treatment. Continued investment is likely here because buyers want governance systems that make model behavior easier to trace and defend under both internal review and external challenge.

By End-Use Industry: IT And Telecom Sets The Pace While Retail And E-Commerce Accelerates

IT and telecom commanded 26.41% share in 2025, placing it at the center of current demand in the responsible AI and sustainability governance platform market. Firms in this sector often build, sell, deploy, and monitor AI systems simultaneously, which places a greater governance burden on them than in many other industries. Their larger scale also makes centralized policy enforcement and evidence capture more valuable. OneTrust’s reach across more than 14,000 organizations, including over half of the Fortune 500, reflects the strong pull from enterprise technology-heavy buyers. BFSI remains another important contributor, since existing model risk expectations make it easier for governance spending to expand from traditional analytics into broader AI and disclosure oversight.

Retail and e-commerce are forecast to expand at a 24.87% CAGR through 2031, giving this segment one of the strongest upside positions in the market. Growth is being driven by supplier data needs, emissions disclosure demands, and rising pressure to explain automated pricing, recommendations, and personalization systems. Governance is becoming more important in a sector that historically emphasized commercial speed over formal oversight. Retail buyers also face a practical need to manage numerous external data relationships, which makes integrated evidence trails and workflow controls more useful. As a result, the responsible AI and sustainability governance platform market is expanding beyond heavily regulated verticals into sectors where AI scale and supply-chain complexity are now creating their own control demands.

Geography Analysis

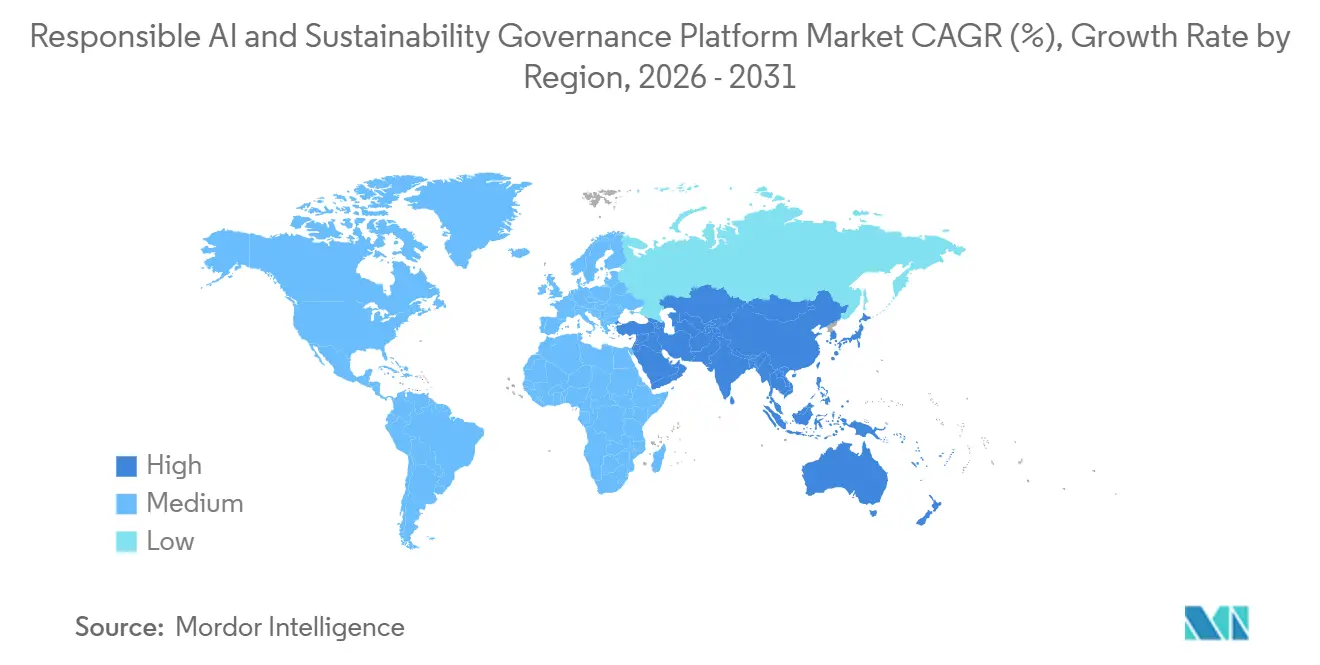

Europe held 34.56% of the responsible AI and sustainability governance platform market share in 2025, making it the largest regional contributor. The region leads because it combines binding sustainability reporting obligations with a clear AI governance direction, giving buyers fewer reasons to delay platform decisions. The EU Council’s 2026 action on sustainability reporting kept large companies with material European operations within a meaningful compliance perimeter, and that continues to support enterprise demand. Germany, France, and the United Kingdom remain central to regional adoption because they combine large corporate bases, stronger disclosure discipline, and greater readiness to fund cross-functional governance programs.

North America held the second-largest share of the market, with adoption led by large enterprises in BFSI and technology. The SEC’s May 2026 proposal to rescind climate-related disclosure rules reduced one near-term federal reporting driver, but it did not remove governance needs for multinational firms with European exposure. This created a split market where large cross-border companies still need unified governance infrastructure, while some domestic mid-market buyers can move more slowly. The region remains important because many early adopters already had mature data, privacy, and model governance capabilities that can be extended into combined AI and sustainability oversight.

Asia-Pacific is projected to register the fastest growth at 25.45% CAGR through 2031, making it the key expansion region for the responsible AI and sustainability governance platform market. Much of that demand is tied to export manufacturing and supply-chain transparency, since firms in the region are often pulled into Western disclosure expectations through customer relationships. The region is also seeing stronger board-level attention to AI oversight as companies deploy more enterprise AI across operations, customer engagement, and reporting workflows. South America remains an emerging market, with demand supported by privacy regulation, multinational subsidiaries, and increasing sustainability reporting discipline among larger corporates. The Middle East and Africa is still the smallest regional segment, but government-led digital programs in the Gulf are creating early demand in public services, finance, and large-scale infrastructure projects.

Competitive Landscape

The responsible AI and sustainability governance platform market remains fragmented, with no single vendor controlling both AI governance and ESG management. Competition is divided between responsible AI specialists such as Credo AI, ArthurAI, and Monitaur, and sustainability-focused platforms such as Novisto, Watershed Technology, and Greenly SAS. The main shift in 2026 is that both groups are broadening their product coverage, as buyers increasingly want a single platform that can handle controls, evidence, and reporting. This keeps the market active for specialists while also giving larger platform companies room to extend into adjacent governance functions.

Another clear pattern is the push to deepen integrations with major enterprise ecosystems, so governance tools become easier to buy and deploy. ArthurAI launched its Agent Discovery and Governance platform on Google Cloud Marketplace in January 2026, after making it available on AWS in 2025, demonstrating how distribution strategy is becoming a competitive lever. OneTrust expanded its AI governance offering in March 2026 to add real-time monitoring and enforcement across agents, models, and data, moving its product closer to a continuous control plane. These moves matter because buyers are favoring platforms that integrate with existing cloud, data, and governance stacks rather than standalone ones.

A third pattern is the use of product expansion and acquisition to close gaps faster than internal development alone would allow. Novisto acquired Minimum in March 2026 to strengthen carbon accounting and audit-trail capabilities, supporting the broader move toward a single system of record for sustainability data. DataRobot acquired Agnostiq in February 2025 to strengthen agentic AI application development and orchestration, underscoring how platform vendors are preparing for governance needs that will rise as more autonomous systems emerge. Credo AI’s May 2025 integration with Microsoft Azure AI Foundry also demonstrated how governance vendors are moving closer to the developer workflow instead of staying only in downstream compliance review. Even with these moves, the market still has room for mid-market unified offerings, multilingual compliance support, and managed governance services for companies that lack internal specialists.

Responsible AI and Sustainability Governance Platform Industry Leaders

Credo AI, Inc.

ArthurAI, Inc.

Fiddler Labs, Inc.

Holistic AI Limited

Monitaur, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Persefoni AI unveiled the Persefoni Analytics Agent on May 5, 2026, an agentic AI tool that enables natural language emissions queries, on-demand data visualizations, and tailored data cuts within the platform. The launch also brought the company’s total raised capital to USD 179 million.

- May 2026: Sweep SAS announced a global partnership with Arcadis on May 6, 2026, combining Sweep’s enterprise sustainability intelligence platform with Arcadis’s engineering and advisory capabilities. The partnership targets organizations that want to turn sustainability data into capital investment decisions and also extends Sweep’s presence in the U.S. market.

- April 2026: Watershed Technology launched a suite of AI agents and a Sustainability AI Fellowship program at San Francisco Climate Week on April 21, 2026. Early customers reported an 80% reduction in time to actionable sustainability data and a 93% reduction in data cleaning time, with one user completing a task in 20 minutes that had previously taken 5 hours.

- April 2026: Sweep SAS and CFGI announced a strategic partnership on April 14, 2026, to help enterprises build audit-ready sustainability data and processes. The arrangement combines Sweep’s platform with CFGI’s accounting and ESG program management capabilities.

Global Responsible AI and Sustainability Governance Platform Market Report Scope

The Responsible AI and Sustainability Governance Platform market refers to platforms and services that integrate ethical AI practices with sustainability governance frameworks to ensure transparency, accountability, and compliance in AI-driven operations. These solutions provide functionalities such as AI model lifecycle governance, risk and compliance management, bias and fairness monitoring, explainability tools, auditability, and evidence management. By embedding governance and sustainability intelligence into AI workflows, these platforms help organizations mitigate risks, ensure ethical AI deployment, and align operations with ESG and regulatory requirements.

The Responsible AI and Sustainability Governance Platform market report is segmented by Component (Software Platforms and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (AI Model Lifecycle Governance, Risk and Compliance Management, Bias, Fairness, and Explainability Management, Auditability and Evidence Management), End-Use Industry (IT and Telecom, BFSI, Industrial Manufacturing, Energy and Utilities, Oil and Gas, Retail and E-Commerce, Construction and Infrastructure, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Platforms |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| AI Model Lifecycle Governance |

| Risk and Compliance Management |

| Bias, Fairness, and Explainability Management |

| Auditability and Evidence Management |

| IT and Telecom |

| BFSI |

| Industrial Manufacturing |

| Energy and Utilities |

| Oil and Gas |

| Retail and E-Commerce |

| Construction and Infrastructure |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Software Platforms | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By Application | AI Model Lifecycle Governance | ||

| Risk and Compliance Management | |||

| Bias, Fairness, and Explainability Management | |||

| Auditability and Evidence Management | |||

| By End-Use Industry | IT and Telecom | ||

| BFSI | |||

| Industrial Manufacturing | |||

| Energy and Utilities | |||

| Oil and Gas | |||

| Retail and E-Commerce | |||

| Construction and Infrastructure | |||

| Government and Public Sector | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the responsible AI and sustainability governance platform market?

The responsible AI and sustainability governance platform market is valued at USD 1.81 billion in 2026 and is forecast to reach USD 5.32 billion by 2031 at a 24.06% CAGR.

Which region currently leads demand for responsible AI and sustainability governance platforms?

Europe leads with 34.56% share in 2025, supported by stricter sustainability reporting and AI governance requirements.

Which deployment model is growing fastest in responsible AI and sustainability governance platforms?

Hybrid deployment is growing the fastest at a 25.12% CAGR through 2031 because many buyers want centralized governance with local data control.

Why are large enterprises the biggest buyers of these governance platforms?

Large enterprises held 65.23% share in 2025 because they manage larger AI estates, face wider disclosure obligations, and have more complex internal control needs.

Which application area is expanding the fastest?

Bias, fairness, and explainability management is projected to grow at a 25.34% CAGR through 2031 as enterprises need stronger documentation and oversight of model outcomes.

Which end-use sector shows the strongest growth outlook?

Retail and e-commerce is expected to grow at a 24.87% CAGR through 2031 as supply-chain disclosure needs and AI transparency requirements become more important.

Page last updated on: