Respiratory Virus Infection Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.80 Billion |

| Market Size (2031) | USD 35.16 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

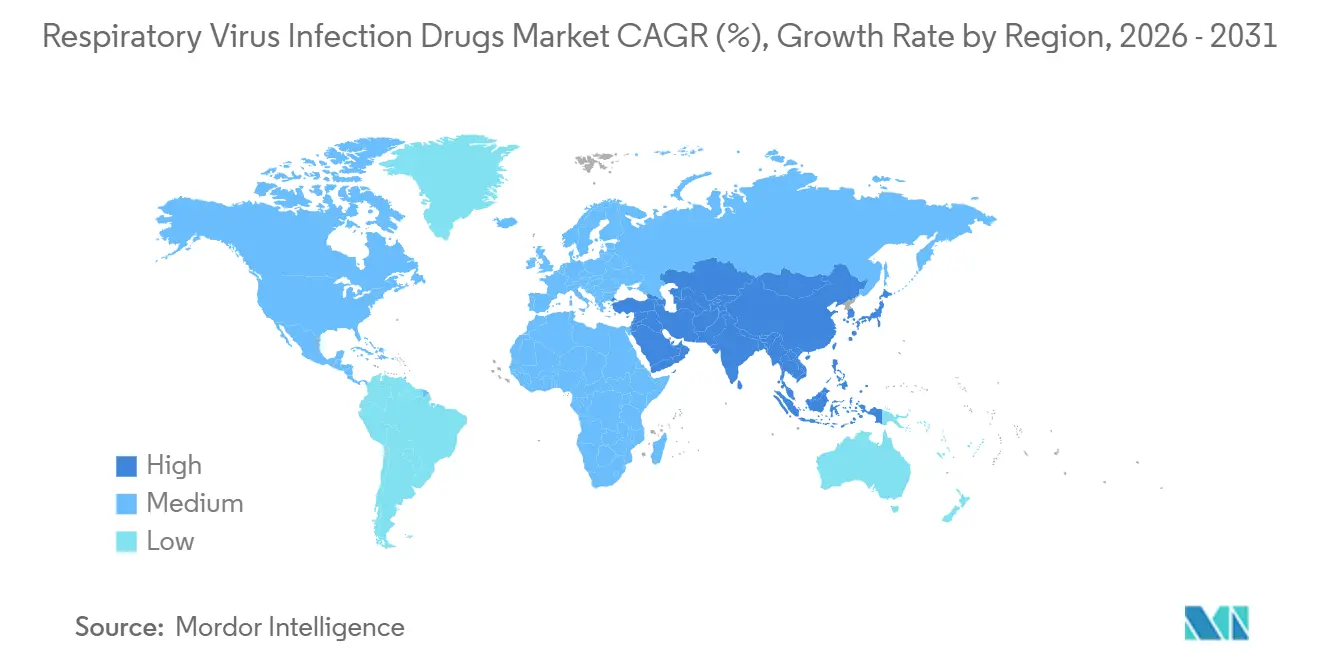

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

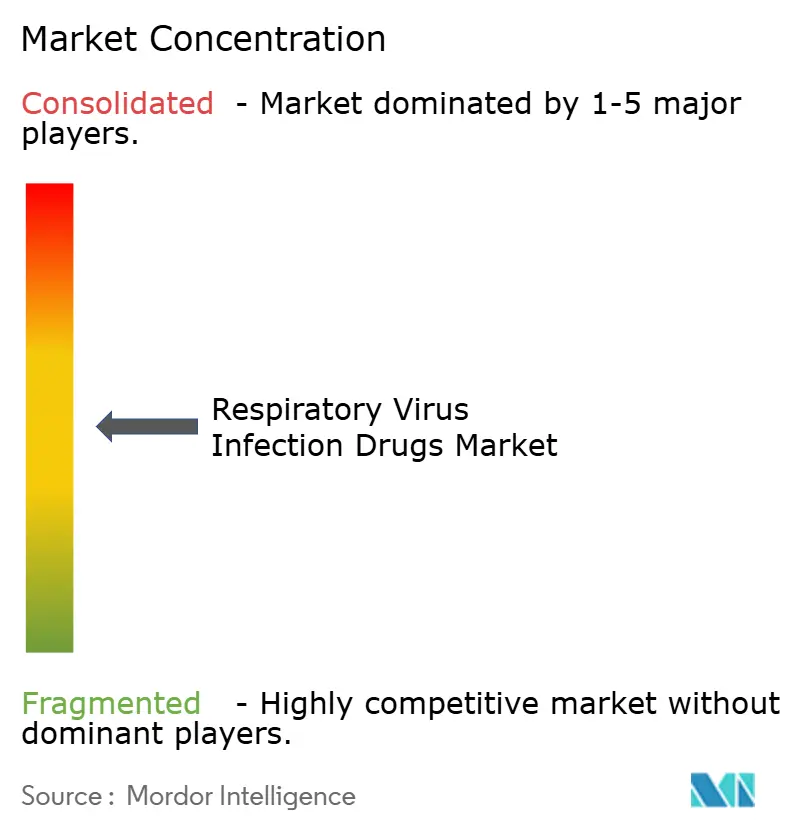

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Virus Infection Drugs Market Analysis by Mordor Intelligence

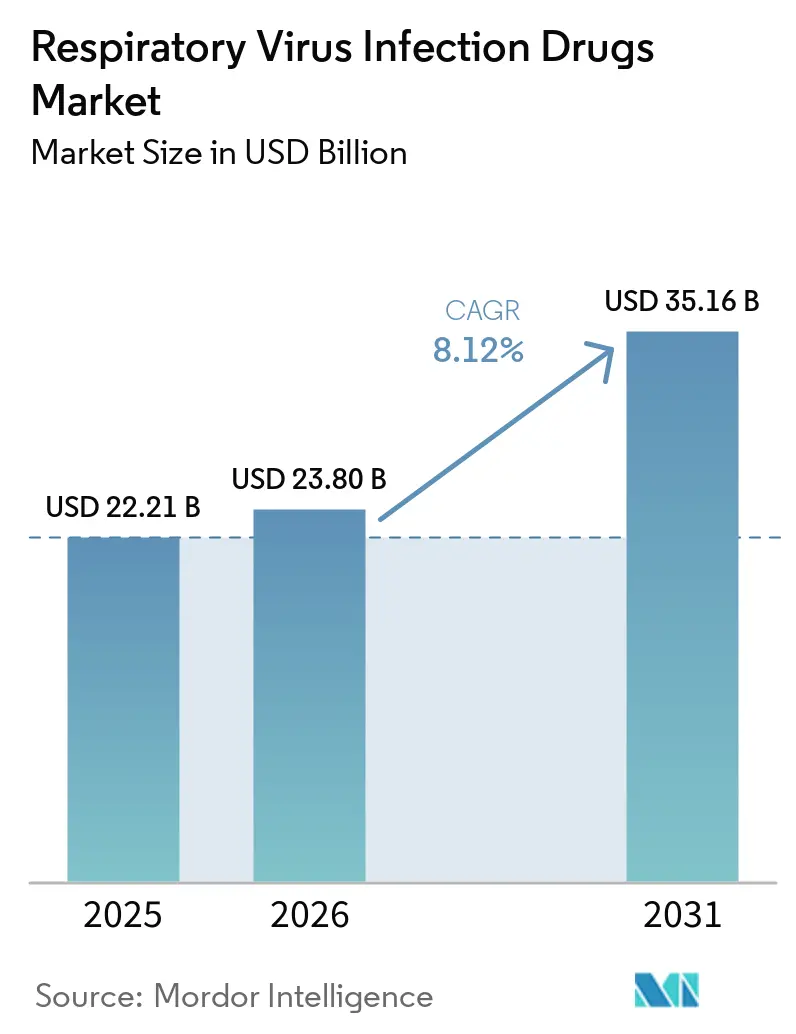

The Respiratory Virus Infection Drugs Market size is projected to be USD 22.21 billion in 2025, USD 23.80 billion in 2026, and reach USD 35.16 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

Demand is shifting from emergency COVID-19 stockpiling toward steady commercial uptake among older adults and infants who remain vulnerable to RSV and influenza. Oral antivirals remain the workhorse for outpatient care, yet single-dose monoclonal antibodies are expanding rapidly as countries fold RSV prevention into routine immunization schedules. Asia-Pacific is emerging as the fastest-growing region on the back of China’s March 2026 conditional approvals for simnotrelvir and VV-116, plus Japan’s November 2025 launch of pediatric baloxavir granules. Competitive intensity is rising as originators defend patents while local manufacturers add lower-cost options, forcing price realignments across middle-income markets.

Key Report Takeaways

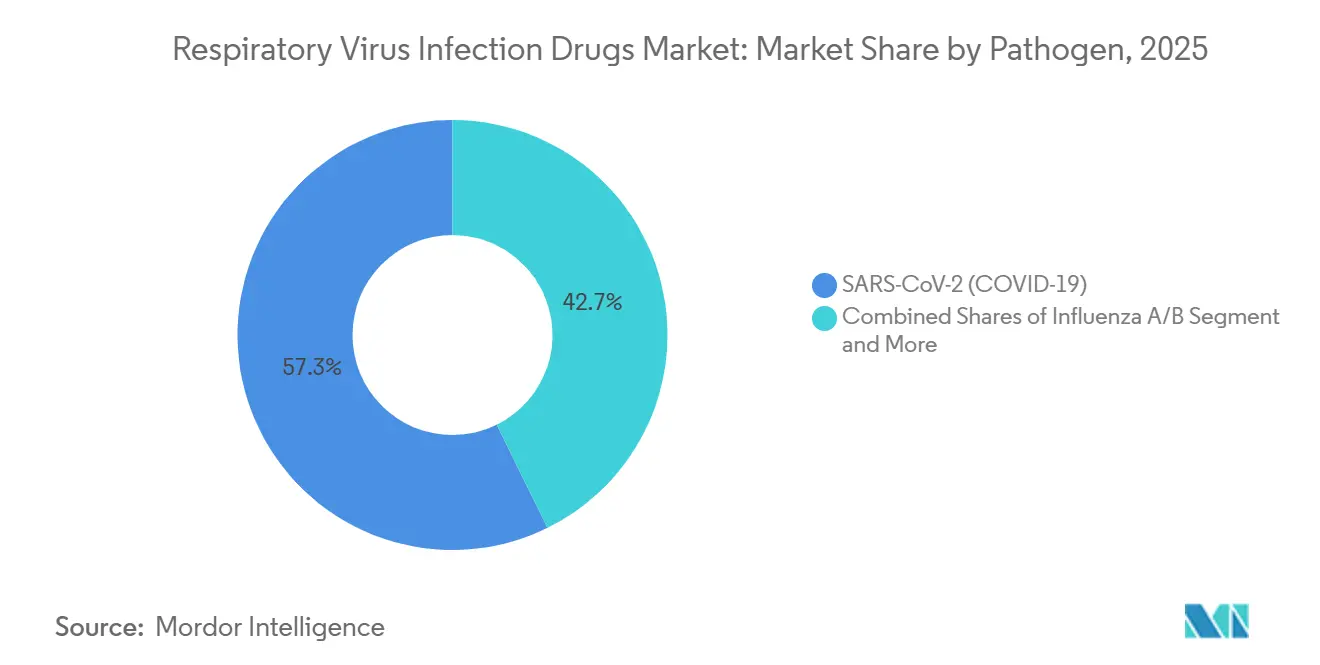

- By pathogen, SARS-CoV-2 therapies led with 57.28% of the respiratory virus infection drugs market share in 2025, while RSV treatments are advancing at an 8.87% CAGR through 2031.

- By modality, small-molecule antivirals accounted for 67.34% of the respiratory virus infection drugs market in 2025, whereas monoclonal antibodies are expanding at a 9.21% CAGR through 2031.

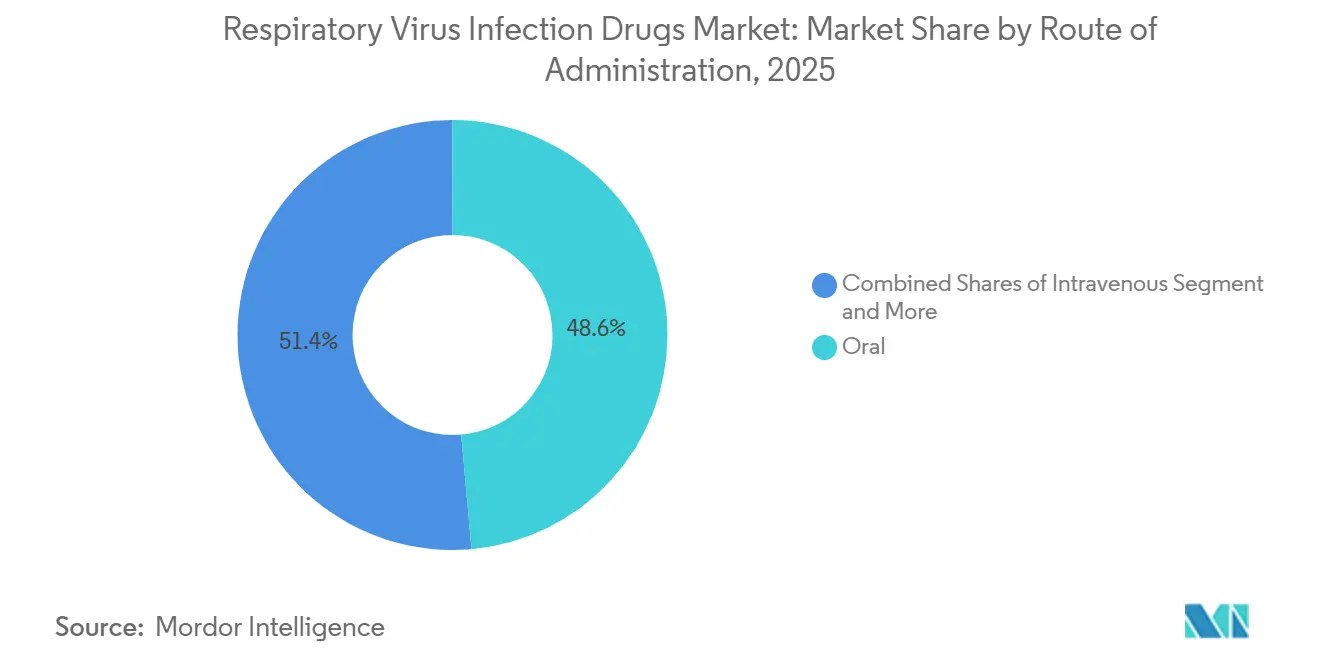

- By route of administration, oral products accounted for 48.59% share of the respiratory virus infection drugs market size in 2025 and are forecast to grow at 8.65% through 2031.

- By setting of care, outpatient and community channels grew at a 9.03% CAGR to 2031, outpacing hospital settings, which accounted for 42.38% of 2025 revenue.

- By geography, North America captured 47.29% of 2025 revenue, yet Asia-Pacific is projected to log an 8.88% CAGR to 2031, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Respiratory Virus Infection Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High elderly and infant RSV/influenza burden sustains antiviral and mAb demand | +1.8% | Global, with peak intensity in North America, Europe, and aging APAC markets (Japan, South Korea) | Long term (≥ 4 years) |

| Oral antivirals enable outpatient treatment and faster access | +1.5% | Global, with early adoption in North America, EU, and urban APAC hubs | Medium term (2-4 years) |

| APAC healthcare expansion and surveillance lift antiviral utilization | +1.3% | APAC core (China, India, Southeast Asia), spill-over to Middle East | Long term (≥ 4 years) |

| Long-acting RSV mAb single-dose immunization scales across countries | +1.2% | North America, EU, with gradual rollout in Latin America and APAC | Medium term (2-4 years) |

| Pharmacist-prescribed test-to-treat broadens same-day antiviral initiation | +0.9% | North America (42 US states, Canadian provinces), pilot programs in EU | Short term (≤ 2 years) |

| China-led uptake of baloxavir and new antivirals accelerates growth | +0.7% | APAC, primarily China, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Elderly and Infant RSV and Influenza Burden Sustains Antiviral Demand

Older adults account for up to 120,000 RSV hospitalizations annually in the United States, while infants under six months face the highest per-capita RSV load [1]Centers for Disease Control and Prevention, “RSV Trends 2025,” cdc.gov. Nirsevimab showed 88.2% effectiveness in Australian infants during the 2024 season and 89.8% in Spain’s 2024–2025 season. Baloxavir resistance stayed low at 1.7% overall but rose to 3.6% in H3N2 cases in Japan through 2025. Growing real-world evidence across geriatric and pediatric cohorts is creating dual pillars of steady demand. GSK and Sanofi together booked USD 1.2 billion in 2024 ex-U.S. nirsevimab sales as European health systems backed preventive biologics.

Oral Antivirals Enable Faster Outpatient Access

Time-critical initiation drives interest in pill-based regimens that bypass infusion suites. Despite eligibility, 69% of U.S. patients missed COVID-19 antivirals in 2024, citing prescriber hesitancy and drug interaction fears with ritonavir-boosted products. Ensitrelvir, under FDA review for June 2026, cleared the virus 82% faster than placebo and avoids ritonavir, improving suitability for polypharmacy patients [2]U.S. Food and Drug Administration, “Ensitrelvir NDA Filing,” fda.gov. Forty-two U.S. states allow pharmacists to test and prescribe antivirals the same day, compressing treatment windows. Japan’s baloxavir granules broke adherence barriers for children unable to swallow tablets, although 138 mutations were observed in 9.7% of treated pediatric cases. China’s March 2026 approvals of oral simnotrelvir-ritonavir and VV-116 added home-use options with higher resistance barriers.

Asia-Pacific Healthcare Expansion Boosts Antiviral Utilization

Infrastructure upgrades are converting latent demand into prescriptions across China, India, and Southeast Asia. China cleared simnotrelvir and VV-116 after trials enrolling 1,800 volunteers, matching global potency thresholds while mandating post-marketing surveillance. India’s 1,400 WHO-GMP facilities underpin generic exports, though CDSCO called for local trials of baloxavir in February 2025 before approval. RSV monoclonal antibodies were introduced into national programs in South Korea and Australia, where nirsevimab demonstrated real-world effectiveness of 88.2%. High telehealth penetration in many Asia-Pacific metros widens access to antivirals without in-person visits.

Long-Acting RSV Monoclonal Antibodies Scale Across Immunization Programs

Single-dose antibodies remove multi-visit hurdles but face seasonal supply peaks. Nirsevimab achieved high effectiveness in U.S. infants, yet France faced shortages from November 2024 to January 2025, triggering prioritization rules. AstraZeneca captured USD 1.03 billion in U.S. Beyfortus revenue in 2024, with 400,000 doses administered. FDA cleared clesrovimab in June 2025, giving payers a second long-acting option and mitigating one-supplier risk. Cold-chain demands of 2 °C to 8 °C persist, stressing rural distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| COVID-19 hospitalization decline and waning public procurement depress volumes | -1.4% | Global, with acute impact in North America and Europe | Short term (≤ 2 years) |

| Antiviral resistance and variant escape (e.g., baloxavir I38, mAb neutralization loss) | -0.8% | Global, with elevated resistance in pediatric and immunocompromised cohorts | Medium term (2-4 years) |

| Seasonal supply and cold-chain limits for RSV mAbs constrain coverage | -0.6% | Europe, North America, with emerging constraints in APAC and Latin America | Short term (≤ 2 years) |

| Underuse of antivirals among high-risk outpatients reduces penetration | -0.7% | Global, with highest underutilization in North America, Southern Europe, and emerging APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

COVID-19 Hospitalization Decline and Lower Public Procurement Depress Volumes

U.S. hospitalizations fell 18% in 2024 versus 2023 and 92% from the January 2022 peak, slashing inpatient demand for remdesivir. Pfizer’s Paxlovid sales shrank to USD 1.5 billion in 2024 from USD 12.5 billion in 2022 as public stockpiles depleted and retail pricing rose to USD 1,390 per course. The United Kingdom wrote off GBP 1.7 billion (USD 2.1 billion) in expired Paxlovid during May 2025 [3]Financial Times, “UK Disposes of Expired Paxlovid,” ft.com. Governments are shifting funds toward RSV and influenza preparedness, leading to a temporary lull in COVID-19 antiviral purchases.

Antiviral Resistance and Variant Escape Events

Baloxavir I38 substitutions reduced susceptibility by up to 50-fold and were detected in 9.7% of treated children and 2.2% of adults, prolonging viral clearance by up to 3 days. SARS-CoV-2 variants evaded multiple monoclonal antibodies, prompting market exits for bebtelovimab and sotrovimab in 2024. Although nirmatrelvir resistance stayed below 0.1%, E166V substitutions in chronically infected patients expose a latent threat. Second-generation inhibitors such as simnotrelvir exhibit stronger activity against these mutants, but real-world surveillance is only beginning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pathogen: RSV Gains as COVID-19 Volumes Normalize

SARS-CoV-2 products delivered 57.28% of 2025 revenue, but RSV therapies are expanding at 8.87% annually through 2031 as monoclonal antibodies enter pediatric schedules. RSV advances underpin the outlook for the respiratory virus infection drugs market, offering insulation from pandemic volatility. Influenza antivirals remain seasonally stable, with Japan’s baloxavir granules widening pediatric reach amid careful resistance monitoring. Combined, non-COVID pathogens contribute over significant share of the current value, and their share is rising steadily.

Real-world data show nirsevimab reaching 88%–90% effectiveness and clesrovimab adding supply depth, reinforcing the respiratory virus infection drugs market share momentum for RSV prophylaxis. COVID-19 demand is flattening at endemic levels, yet ensitrelvir’s potential post-exposure label could expand household use cases, diversifying the portfolio and extending lifecycle revenues for protease inhibitors.

By Modality: Monoclonal Antibodies Outpace Small Molecules

Small molecules retained 67.34% revenue dominance in 2025, but the 9.21% CAGR for antibodies signals a shift toward passive prophylaxis solutions. The respiratory virus infection drugs market for monoclonal antibodies is projected to expand fastest in high-risk infant and elderly segments, driven by single-dose convenience and reduced cold-chain waste.

Ritonavir interactions limit nirmatrelvir use in polypharmacy groups, nudging prescribers toward ritonavir-free or biologic options. AstraZeneca and GSK logged combined revenue of USD 2.2 billion from nirsevimab in 2024, demonstrating commercial viability. Combination therapy remains marginal but attracts R&D investment aimed at raising resistance thresholds.

By Route of Administration: Oral Dominance Amid Intravenous Decline

Oral regimens, already at 48.59% in 2025, are forecast to grow by 8.65% due to preferences for community access and pharmacist-led dispensing. Declining hospital admissions reduced the market share of respiratory virus infection drugs, historically led by intravenous remdesivir, which fell below USD 1 billion in 2024.

Injectable monoclonal antibodies via intramuscular or subcutaneous routes are the fastest-growing niche, aided by prefilled syringes that simplify clinic workflows. Inhaled formulations, such as zanamivir, stay niche but offer alternatives for select patient groups with gastrointestinal intolerance.

By Setting of Care: Outpatient Surge Reshapes Delivery

Hospital settings accounted for 42.38% of 2025 revenue, down from 2024, while outpatient and community channels grew 9.03% annually. Test-to-treat programs and telehealth logistics underpin this pivot, enabling same-day antiviral treatment. The respiratory virus infection drugs market benefits from reduced hospital bottlenecks, leading to higher adherence and earlier disease management.

Long-term care centers remain under-penetrated, with only 31% of eligible residents receiving antivirals in 2024. Targeted education and streamlined reimbursement could unlock incremental volumes across this vulnerable population.

Geography Analysis

North America maintained a 47.29% revenue share in 2025, but growth is plateauing as COVID-19 stockpile use wanes and reimbursement shifts to retail channels. U.S. pharmacist test-to-treat frameworks supply speed advantages, while Canada eyes nationwide expansion after successful provincial pilots. Mexico’s adoption is hampered by uneven insurance coverage, although public clinics are adding generic oseltamivir and molnupiravir to formularies.

Europe demonstrates mixed momentum. Germany and the United Kingdom accelerate pharmacist prescribing, yet supply hiccups in France exposed cold-chain weaknesses for RSV biologics. Southern Europe faces slower reimbursement cycles, delaying the introduction of new antivirals. Eastern European markets remain price-sensitive, favoring generics over premium monoclonals.

Asia-Pacific tops the growth chart at an 8.88% CAGR. China’s approvals of simnotrelvir and VV-116, plus telemedicine penetration, expand reach into lower-tier cities. Japan’s pediatric baloxavir and South Korea’s RSV immunization roll-outs support double-digit gains. India’s vast manufacturing base gives the region a cost edge, though additional local trials for novel agents prolong time-to-market. Australia’s 88.2% nirsevimab effectiveness is catalyzing take-up across Oceania.

Competitive Landscape

Market concentration is moderate. Pfizer, Gilead, AstraZeneca, and the GSK-Sanofi partnership accounted for the majority of 2025 revenue, but share is eroding as Chinese and Japanese innovators advance. Resistance profile, cold-chain handling, and time-to-approval are the new battlegrounds. Simnotrelvir’s potency against E166V mutants, nirsevimab’s one-shot convenience, and China’s swift conditional approvals illustrate differentiated strategies.

Patent activity shows process chemistry toggles by generic firms aiming to bypass protection, while originators pursue formulation tweaks such as baloxavir granules to retain exclusivity. Pfizer's telemedicine distribution in the United States and Ping An's in China illustrate channel diversification that sidesteps traditional prescribers. White-space pathogens like human metapneumovirus, parainfluenza, and adenovirus await the first approved drugs, representing upside for pipeline assets.

Respiratory Virus Infection Drugs Industry Leaders

Gilead Sciences, Inc

Pfizer Inc

AstraZeneca PLC

GSK plc

Lupin Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: China’s NMPA granted conditional approval to simnotrelvir-ritonavir and VV-116 after trials with 1,800 participants.

- November 2025: Shionogi introduced baloxavir granules for pediatric influenza in Japan; surveillance logged 9.7% I38 mutations in treated children.

- June 2025: FDA approved clesrovimab, a long-acting RSV antibody, diversifying supply ahead of the 2025–2026 season.

Global Respiratory Virus Infection Drugs Market Report Scope

As per the scope of the report, Respiratory virus infection drugs primarily target common pathogens such as influenza, COVID-19, and Respiratory Syncytial Virus (RSV), often working best when administered within the first 48 hours of symptom onset. For influenza, common prescription antivirals include neuraminidase inhibitors like oseltamivir (Tamiflu), zanamivir (Relenza), and peramivir (Rapivab), as well as the polymerase acidic endonuclease inhibitor baloxavir marboxil (Xofluza).

The CHO-based biosimilars market is segmented by pathogen, modality, route of administration, settings of care, and geography. Based on pathogen, the market is segmented into SARS-CoV-2 (COVID-19), influenza A/B, respiratory syncytial virus (RSV), human metapneumovirus (hMPV), parainfluenza viruses (PIV 1–4), and adenovirus. By modality, small-molecule antivirals, monoclonal antibodies (treatment and passive prophylaxis), and combination/adjunctive regimens. Based on route of administration, the market is segmented into oral, intravenous, intramuscular/subcutaneous, and inhaled/intranasal. By setting of care, the market is segmented into outpatient/community, hospital/acute care, and long-term care/skilled nursing.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| SARS-CoV-2 (COVID-19) |

| Influenza A/B |

| Respiratory Syncytial Virus (RSV) |

| Human Metapneumovirus (hMPV) |

| Parainfluenza Viruses (PIV 1–4) |

| Adenovirus (respiratory types) |

| Small-Molecule Antivirals |

| Monoclonal Antibodies |

| Combination/Adjunctive Regimens |

| Oral |

| Intravenous |

| Intramuscular/Subcutaneous |

| Inhaled/Intranasal |

| Outpatient/Community |

| Hospital/Acute care |

| Long-term care/Skilled nursing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pathogen | SARS-CoV-2 (COVID-19) | |

| Influenza A/B | ||

| Respiratory Syncytial Virus (RSV) | ||

| Human Metapneumovirus (hMPV) | ||

| Parainfluenza Viruses (PIV 1–4) | ||

| Adenovirus (respiratory types) | ||

| By Modality | Small-Molecule Antivirals | |

| Monoclonal Antibodies | ||

| Combination/Adjunctive Regimens | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Intramuscular/Subcutaneous | ||

| Inhaled/Intranasal | ||

| By Setting of Care | Outpatient/Community | |

| Hospital/Acute care | ||

| Long-term care/Skilled nursing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the respiratory virus infection drugs market by 2031?

The market is set to reach USD 35.16 billion by 2031, growing at an 8.1% CAGR from 2026.

Which pathogen segment is expanding fastest through 2031?

RSV treatments, led by single-dose monoclonal antibodies, are advancing at an 8.87% CAGR through 2031.

Why are monoclonal antibodies gaining share over small-molecule antivirals?

One-shot preventive dosing, strong real-world effectiveness, and fewer drug-drug interactions are propelling antibody uptake, especially among infants and older adults.

Which region will post the highest growth rate?

Asia-Pacific is projected to record the fastest gain at an 8.88% CAGR, buoyed by China’s and Japan’s recent approvals and telehealth expansion .

Page last updated on: