Residential Washer-Dryer Combo Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.96 Billion |

| Market Size (2031) | USD 9.64 Billion |

| Growth Rate (2026 - 2031) | 6.73% CAGR |

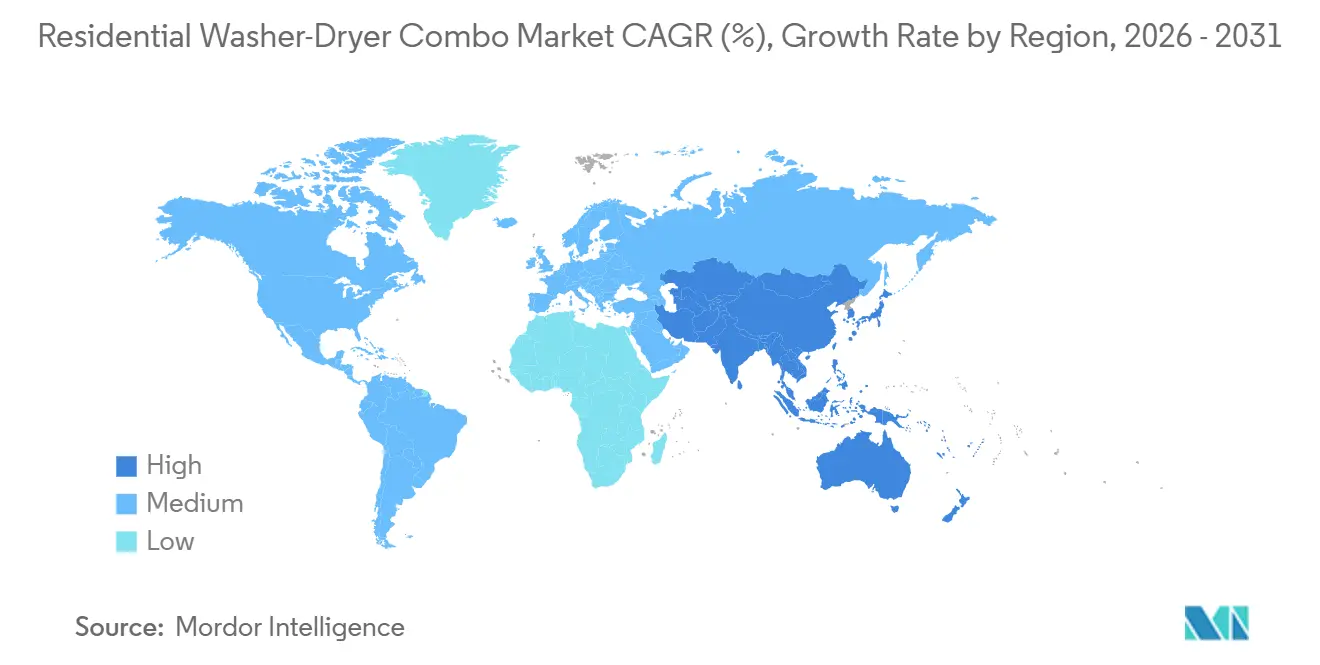

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

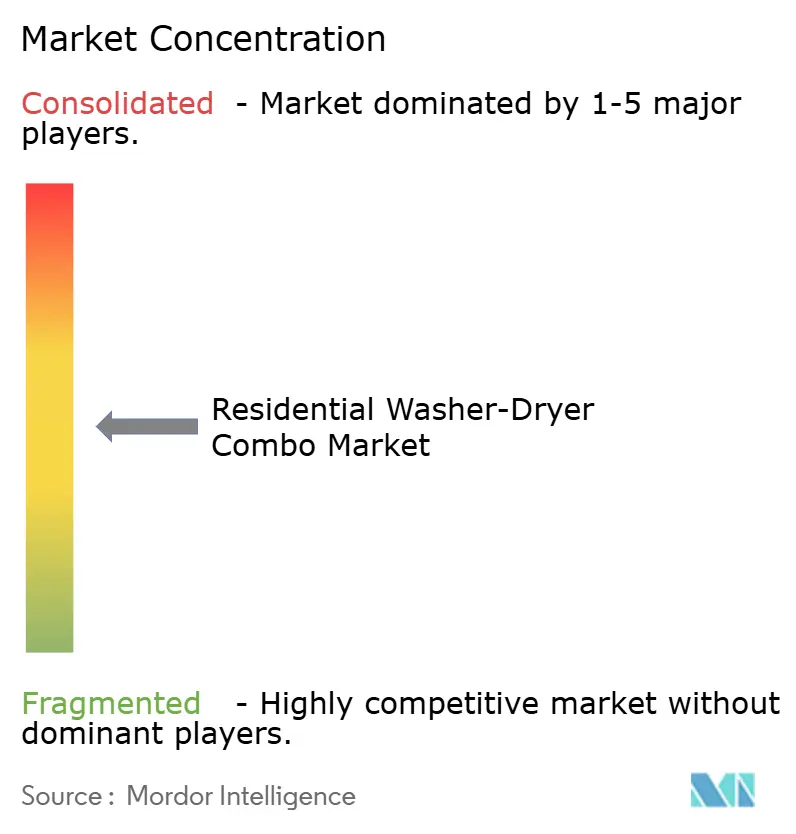

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Washer-Dryer Combo Market Analysis by Mordor Intelligence

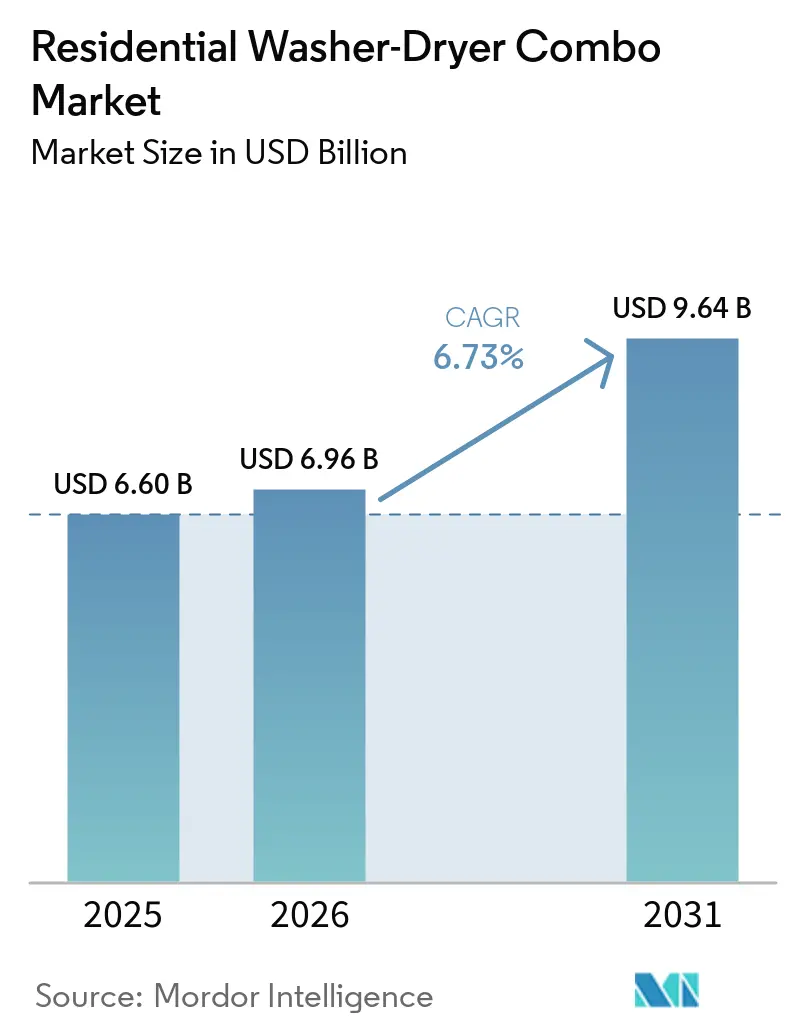

The residential washer-dryer combo market size is projected to expand from USD 6.60 billion in 2025 and USD 6.96 billion in 2026 to USD 9.64 billion by 2031, registering a CAGR of 6.73% between 2026 and 2031. Energy efficiency remains the main competitive advantage because the United States and European rules are pushing manufacturers toward heat pump systems, stronger energy performance, and more rigorous compliance planning. Urban migration and smaller apartments continue to support demand, especially in the Asia-Pacific region, where washing machine ownership is already high, and standalone dryer ownership remains low in key markets such as China. Smart connectivity is also becoming increasingly valuable because utilities can use flexible drying loads, while brands can leverage software updates and app ecosystems to retain premium buyers for longer. In Europe, Regulation (EU) 2019/2023 enforces ecodesign requirements specifically covering washer-dryers since March 2021, locking washers and combo units into an A-to-G energy label that nudges consumers toward higher-performing models, a dynamic confirmed by Germany's Umweltbundesamt, which estimates heat pump drying consumes 73–97 kWh per 100 cycles versus roughly 340 kWh for pre-regulation condenser units[1]Umweltbundesamt, “Wäschetrockner: Bei Kauf Und Nutzung Auf Energieeffizienz Achten,” Umweltbundesamt, umweltbundesamt.de. Freestanding products still anchor demand, but built-in models, online channels, and localized production investment are widening the next phase of opportunity in the residential washer-dryer combo market.

Key Report Takeaways

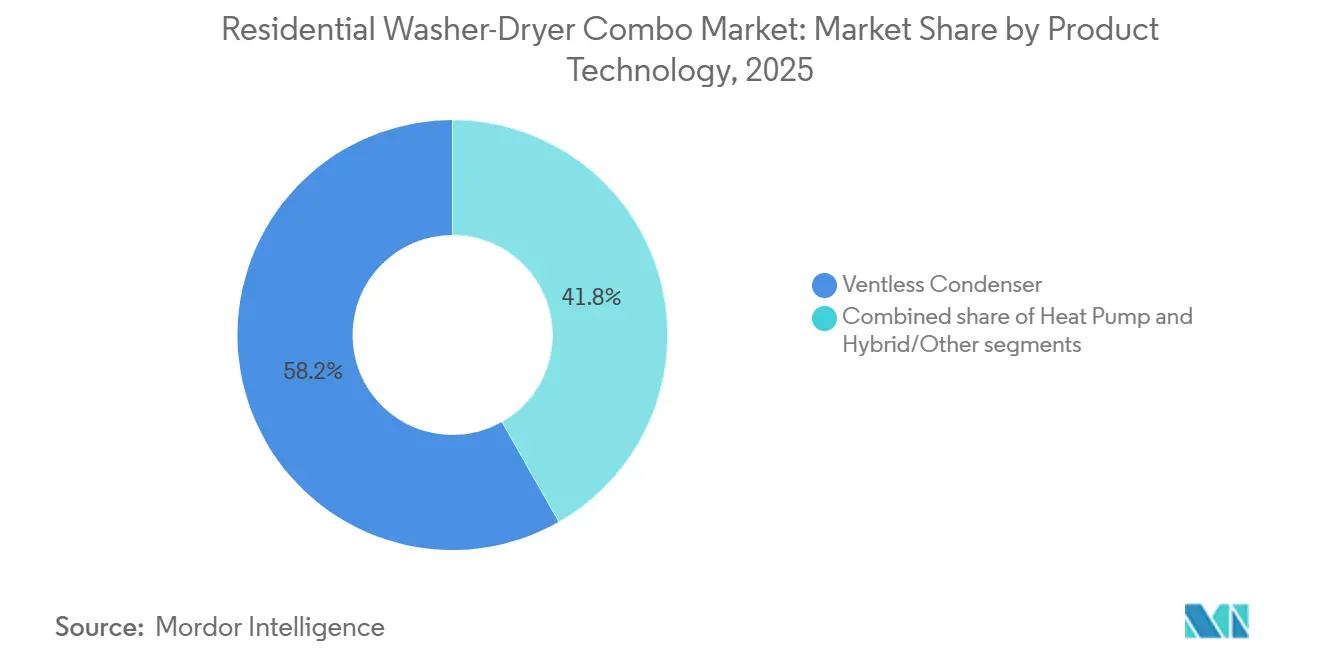

- By product technology, ventless condenser led with 58.24% of the residential washer-dryer combo market share in 2025, while heat pump is projected to expand at a 7.34% CAGR through 2031.

- By loading type, front-load combo washer dryer accounted for 90.00% of the residential washer-dryer combo market share in 2025, while the same segment is forecast to grow at a 7.13% CAGR through 2031.

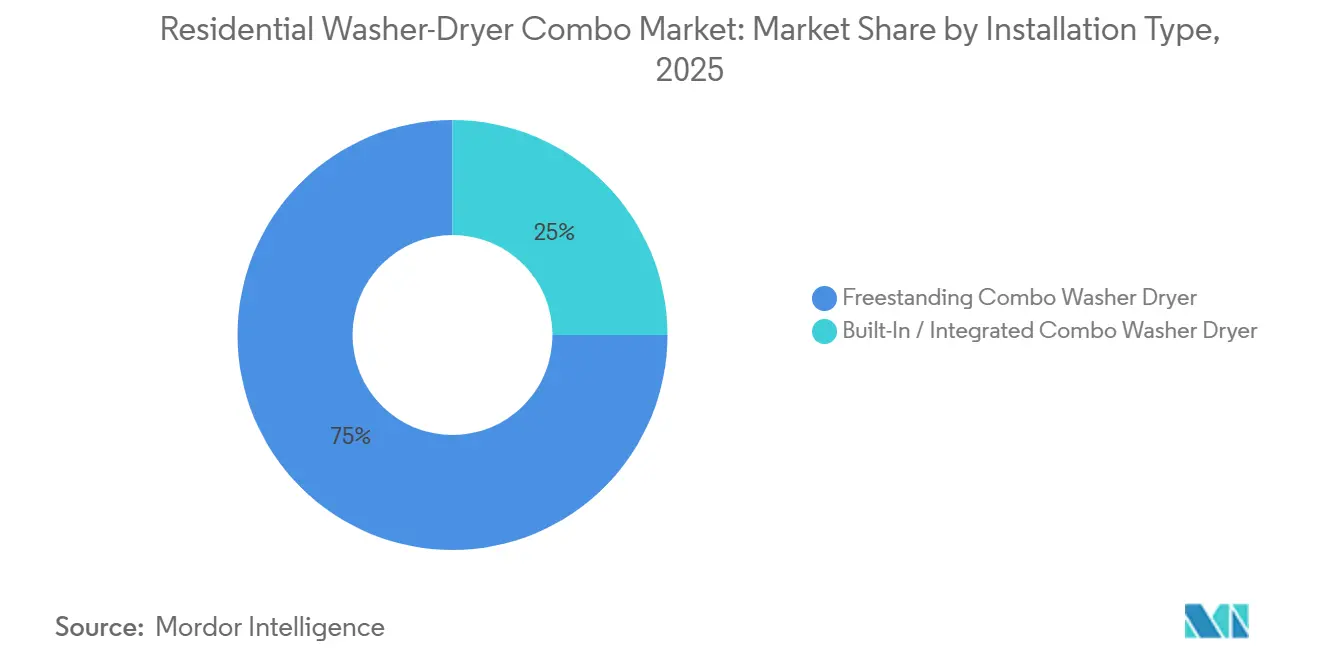

- By installation type, freestanding combo washer dryer captured 75.00% of the residential washer-dryer combo market share in 2025, whereas built-in/integrated combo washer dryer models are projected to advance at a 7.40% CAGR through 2031.

- By capacity, the ≤8 kg segment held 45.21% of the residential washer-dryer combo market share in 2025 and is expected to grow at a 6.94% CAGR through 2031.

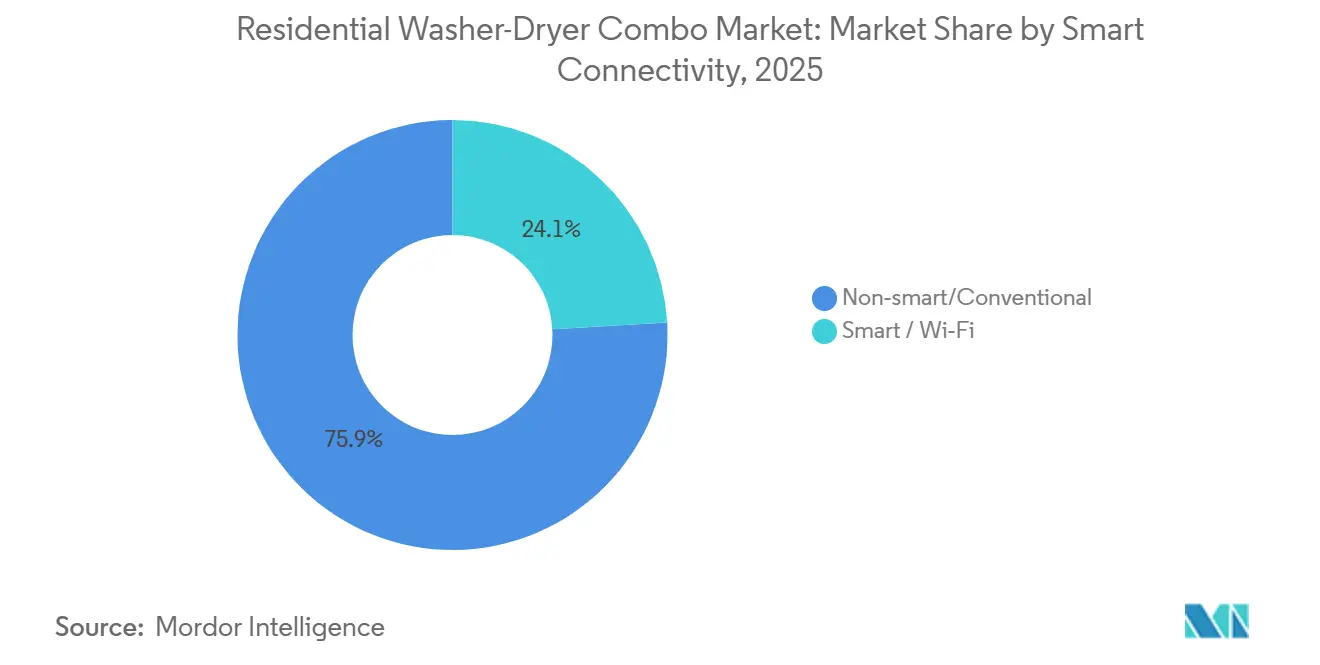

- By smart connectivity, non-smart/conventional models represented 75.92% of the residential washer-dryer combo market share in 2025, while smart/Wi-Fi-enabled models are forecast to expand at a 7.28% CAGR through 2031.

- By distribution channel, multi-brand stores held 42.65% of the residential washer-dryer combo market share in 2025, while online channels are projected to advance at a 7.52% CAGR through 2031.

- By geography, Asia-Pacific accounted for 35.53% of the residential washer-dryer combo market share in 2025 and is projected to grow at a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Residential Washer-Dryer Combo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compact-Urban Households Favor Space-Saving Laundry Appliances | +1.3% | Global, concentrated in East Asia, Western Europe, and North American metro markets | Short term (≤ 2 years) |

| Energy-Efficiency Standards Accelerate Ventless and Heat-Pump Adoption | +1.1% | North America, DOE compliance by 2028, and the EU under Regulation (EU) 2019/2023 | Medium term (2-4 years) |

| Smart-Home Integration Lifts Premium Combo Replacement Demand | +0.9% | North America, South Korea, China, and Western Europe | Medium term (2-4 years) |

| Online Appliance Retail Expands Assortment and Price Transparency | +0.7% | Global, fastest in Asia-Pacific and South America | Short term (≤ 2 years) |

| 120V Ventless Retrofit Fit Unlocks Multifamily Electrification Projects | +0.5% | North America, especially the United States multifamily housing | Medium term (2-4 years) |

| Connected Load-Shifting Creates Utility-Aligned Demand-Response Value | +0.4% | North America and Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compact-Urban Households Favor Space-Saving Laundry Appliances

Urban household formation is reshaping laundry choices, and the residential washer-dryer combo market benefits because one appliance fits homes that cannot easily support separate washer and dryer pairs. A 2024 National Renewable Energy Laboratory review stated that 33% of Americans lived in multifamily buildings, which directly limited floor space, utility capacity, and ducting options for paired units. In China, the China Household Electrical Appliances Research Institute recorded a shift toward drum products with cabinet depths under 600 mm, and retail sales of these slim products rose by 10%, year over year, from January to October 2024[2]China Household Electrical Appliances Research Institute, “2024 China Washing Machine and Dryer Industry Development White Paper,” China Household Electrical Appliances Research Institute, aigc.idigital.com.cn. Buyers in dense cities still expect strong washing performance, gentler drying, and simpler installation even within smaller machine footprints. The practical tradeoff is now more about saving floor area and avoiding an extra vent path than sacrificing everyday laundry quality. This keeps space-saving demand broad in the residential washer-dryer combo market across East Asia, Western Europe, and major North American metro areas. The counter-intuitive implication is that Fabric Care quality has not been sacrificed for compactness: advanced drum agitation patterns, Eco-Hybrid drying approaches, and precision load-sensing now deliver wash ratios above 1.0 in units under 60 cm deep. What buyers are actually trading is floor space for vent ducting, not Fabric Care performance.

Energy-Efficiency Standards Accelerate Ventless and Heat-Pump Adoption

Compliance deadlines are now shaping product road maps across the residential washer-dryer combo market. The United States Department of Energy set a minimum Combined Energy Factor of 2.33 lb/kWh for ventless electric combination washer-dryers, with compliance required by March 1, 2028. The same standards package is projected to deliver USD 21 billion in consumer savings over 30 years, which strengthens the long-term cost case for more efficient combo units. LG stated that its Inverter HeatPump technology uses up to 60% less energy than comparably sized vented dryer models, which shows why established heat pump platforms carry a structural advantage as standards tighten[3]LG Electronics USA, “LG Launches New WashCombo All-In-One Washer/Dryer With Inverter HeatPump Technology and Direct Drive Motor,” LG Electronics USA, lg.com. In Europe, Regulation (EU) 2019/2023 keeps washer-dryers within an A-to-G energy label system, and Germany’s Umweltbundesamt reported that heat pump drying used 73-97 kWh per 100 cycles, compared with around 340 kWh for older condenser units. This means that manufacturers are finding it harder to delay spending on compressors, heat exchangers, and control software. For manufacturers, the strategic implication is that R&D invested in heat pump compressor efficiency and Dual Inverter Heat Pump control algorithms will compound as compliance milestones force competitors into costly retooling.

Smart-Home Integration Lifts Premium Combo Replacement Demand

Connected features are moving from branding tools to practical value layers in the residential washer-dryer combo market. A 2024 California Energy Commission project estimated that default plug-and-play appliance demand flexibility could support 6 GW of flexible grid capacity, and delay-start or load-shifting appliances were identified as major contributors[4]California Energy Commission, “Expanding Flexible Demand Through Public Broadcast of Greenhouse Gas Emissions and Electricity Prices,” California Energy Commission, energy.ca.gov. A 2024 peer-reviewed Journal of Building Engineering study also found that residential dryers had the greatest demand-reduction potential among household appliances, with up to 1,484 MW of curtailable load during weekday peaks across the MISO region. Samsung’s 2026 Bespoke AI Laundry Combo added AI Wash & Dry+, real-time soil sensing, and Bixby control across connected devices, which shows how premium combos are increasingly part of larger device ecosystems. GE Appliances added 5 downloadable Wi-Fi laundry cycles in November 2025, extending product value after purchase without changing the hardware. Software-led upgrades reduce depreciation concerns and support stronger replacement pricing in the residential washer-dryer combo market.

120V Ventless Retrofit Fit Unlocks Multifamily Electrification Projects

The residential washer-dryer combo market is gaining traction in North America because 120V ventless products address two durable retrofit barriers simultaneously. These products reduce the need for a 240V dryer circuit and avoid the need for an exterior exhaust penetration in many multifamily layouts. The Colorado Housing and Finance Authority’s 2026 electrification guidance recommended 120V heat pump combo units as an alternative to costly panel upgrades in retrofit work. California’s ETCC launched a market and technical evaluation of combination washer-dryer units for multifamily buildings, with the work focused on energy and greenhouse gas outcomes in low-income and disadvantaged communities. California also offered an HEEHRA rebate of USD 840 per unit for multifamily heat-pump clothes dryers, which improves the economics of electrification-oriented installations. This combination of standard-circuit fit, policy support, and simpler retrofit execution makes higher-priced combo units easier to justify in existing residential buildings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Upfront Pricing Versus Separate Washer and Dryer Sets | -1.2% | Global, most acute in price-sensitive South America, Southeast Asia, the Middle East, and Africa | Medium term (2-4 years) |

| Longer Drying Cycles Weaken Consumer Performance Perception | -0.7% | Global, particularly constraining in larger-household segments in the Asia-Pacific and Europe | Medium term (2-4 years) |

| Rebate and Code-Treatment Gaps Limit Integrated Combo Payback | -0.5% | North America, where separate-appliance rebate structures dominate utility programs | Medium term (2-4 years) |

| Heat-Pump Combo Service-Network and Parts Depth Remain Limited | -0.4% | Non-metro North America, Rest of Europe, Rest of Asia-Pacific, and the Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Upfront Pricing versus Separate Washer and Dryer Sets

Upfront price remains the clearest barrier to faster mass adoption in the residential washer-dryer combo market. The premium is widest in heat pump models, which is also the part of the category where manufacturers are investing most heavily. GE Appliances priced its expanded UltraFast Combo range from USD 2,599 to USD 2,999 in November 2025, showing how premium positioning still shapes the segment even as the assortment broadens. Samsung and LG have also continued to frame new combo launches around advanced drying, AI sensing, and energy efficiency, which supports margins but keeps entry pricing elevated. In price-sensitive regions, financing availability, replacement timing, and local electricity costs all shape whether that premium looks reasonable. Broader volume adoption in the residential washer-dryer combo market will depend on a smaller price gap, more localized production, and stronger post-sale support.

Longer Drying Cycles Weaken Consumer Performance Perception

Drying time still shapes buyer perception in the residential washer-dryer combo market more than many technical specifications do. Shoppers often compare a combo with a separate dryer, which makes any long drying cycle feel like a direct performance loss. Samsung’s March 2025 Bespoke AI Laundry Vented Combo for the United States market featured a 68-minute full-load Super Speed cycle, underscoring how aggressively brands are addressing speed concerns. Samsung’s May 2026 global Bespoke AI Laundry Combo again emphasized Enhanced Super Speed and a redesigned heat exchanger, underscoring that the same issue remains central to premium product development. The concern becomes stronger in larger households where multiple loads are common, and timing matters more. Until faster-drying performance moves beyond premium models and into broader price bands, recommendation rates will remain less consistent in the residential washer-dryer combo market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Technology: Heat Pump Formats Disrupt Condenser Dominance

Ventless Condenser technology accounted for 58.24% of product-technology revenue in 2025, making it the largest format in the residential washer-dryer combo market. Its position still rests on lower purchase cost, simpler servicing, and long-standing OEM and retail relationships across Europe and Asia. Heat Pump is forecast to expand at 7.34% CAGR through 2031, making it the fastest-growing product-technology segment. The European Commission’s July 2025 tumble dryer ecodesign update showed the policy direction moving clearly toward heat pump systems, even though washer-dryer combo rules follow their own product path. LG and Samsung continue to use inverter heat pump and upgraded heat exchanger systems to widen the performance gap at the premium end of the residential washer-dryer combo market.

Hybrid and other transitional formats still matter to households seeking a middle ground between efficiency and shorter cycle times. These products also give manufacturers a bridge while heat pump sourcing, scale, and cost structures improve. The residential washer-dryer combo industry is therefore shifting in layers rather than through one abrupt format change. United States and European efficiency rules keep reinforcing the value of better drying architectures, which means product development budgets will continue to shift toward heat pump platforms. Brands that narrow the heat pump price premium faster will be in the strongest position to convert the large condenser base after 2027. That conversion path is gradual, but it remains the clearest long-term product shift inside the residential washer-dryer combo market.

By Loading Type: Front-Load Hegemony Reinforced by Efficiency Credentials

Front-Load combos accounted for 90.00% of loading-type revenue in 2025, keeping them firmly in control of the residential washer-dryer combo market. The segment is also forecast to sustain a 7.13% CAGR through 2031, making it both the largest and the fastest-moving core format. Front-loaders maintain this lead because higher spin extraction leaves less moisture for the drying phase, which supports lower downstream energy use. That operating advantage also aligns well with ENERGY STAR Most Efficient recognition and European energy-label priorities. The DOE’s 2024 direct final rule set front-loading standard-size EER minimums at 5.52 lb/kWh/cycle, which reinforced the efficiency case for this format.

Top-Load combos continue to serve a smaller but durable place in the residential washer-dryer combo market. They remain relevant where under-counter installation is not possible, where housing layouts are narrow or unconventional, or where buyers strongly prefer lid-access loading. That means the remaining top-load share is structural rather than a near-term innovation engine. Most premium product launches continue to focus on front-load ventless systems because those platforms better align with heat pump drying and advanced sensing. The result is that most R&D spending continues to flow into front-load improvements such as smarter load detection, better moisture management, and stronger efficiency performance. Top-load portfolios are therefore more likely to remain selective and region-specific than to regain broad-category momentum.

By Installation Type: Built-In, Momentum Challenges, Freestanding, Default

Freestanding units accounted for 75.00% of installation-type revenue in 2025, making them the volume base of the residential washer-dryer combo market. Their scale comes from lower entry pricing, simpler delivery and installation, and wide compatibility with existing laundry spaces. Freestanding products also fit first-time buyers well because they do not require cabinetry planning or custom enclosure work. Built-In or Integrated combos are forecast to grow at 7.40% CAGR through 2031, making them the fastest-growing installation format. Bosch’s 2024 compact laundry launch in the United States reflected the same small-space design direction, with the company directly linking the offer to compact living and space-conscious planning.

Built-in demand rises when developers and designers treat laundry as part of the finished interior instead of a stand-alone appliance decision. This is becoming more visible in open-plan apartments, premium multifamily projects, and fitted kitchen environments. The format rewards low-vibration designs, cleaner cabinet integration, and quieter operation because the appliance sits closer to living spaces. Certification depth also matters more in this part of the residential washer-dryer combo market because enclosed ventless installations must perform well without creating user concerns around heat, moisture, or noise. Freestanding products will remain the dominant base for many years. Even so, built-in specifications are gaining greater strategic value because they tie appliance choice more closely to new housing design and developer planning.

By Capacity: ≤8 kg Compact Units Define the Market's Mass Segment.

The ≤8 kg band accounted for 45.21% of 2025 revenue and is forecast to grow at a 6.94% CAGR through 2031. That makes it the clearest mass segment within the residential washer-dryer combo market. This capacity range fits the smaller households and compact apartments that define much of the category’s demand base in dense cities. The China Household Electrical Appliances Research Institute reported a 10 percentage-point year-over-year gain in retail sales of drum products in the sub-600 mm depth category from January to October 2024, indicating that physical footprint is strongly shaping product choice. In this size band, brands compete more on energy performance, cycle intelligence, and load sensing than on dramatic increases in drum volume. This keeps compact units at the center of the residential washer-dryer combo market in both mature and developing urban housing corridors.

The 8.1 kg to 10 kg band serves family households that need more wash volume for bed linen, mixed weekly loads, and bulkier garments. Even so, many combo products at this size still dry less than they wash, which creates a load-splitting habit that limits convenience. The >10 kg tier remains smaller, and it is mainly aimed at larger households that still want a single-machine laundry solution. In this upper range, the convenience promise improves only when the wash and dry capacities stay closer together. The residential washer-dryer combo industry still has room to improve the wash-to-dry ratio for large-family use cases. Until that gap narrows more consistently, the largest-capacity segment will stay more selective than the compact mass segment of the residential washer-dryer combo market.

By Smart Connectivity: Wi-Fi Combos Gain Ground via Demand-Response Value

Non-smart or Conventional units accounted for 75.92% of connectivity revenue in 2025, while Smart or Wi-Fi products are forecast to grow at a 7.28% CAGR through 2031. This means conventional models still anchor current volume, but connected models hold the stronger strategic position. A 2024 Journal of Building Engineering study found that residential dryers have the highest demand-reduction potential among household appliances, underscoring the value of connected laundry products beyond convenience alone. That evidence matters because it links connectivity to grid flexibility, utility programs, and future rebate design. The residential washer-dryer combo market is therefore starting to treat connectivity as part of energy management, rather than just a premium lifestyle add-on. This broadens the role of software in a category that was once defined almost entirely by mechanical performance.

California’s ETCC is testing smart single-unit combination laundry appliances to measure the impacts on efficiency and load flexibility in disadvantaged community households. Samsung’s SmartThings Energy AI Mode and LG’s ThinQ platform show how connected ecosystems can extend value after installation through updates, alerts, and remote diagnostics. Downloadable cycles also reduce the risk that a product will feel outdated too quickly. This raises the long-term value of app support inside the residential washer-dryer combo market. Brands that build stronger utility ties and smarter service layers should deepen customer retention faster than rivals that compete solely on hardware.

By Distribution Channel: Online Price Transparency Erodes Multi-Brand Loyalty

Multi-brand Stores accounted for 42.65% of distribution revenue in 2025, but Online is projected to grow at a 7.52% CAGR through 2031. Physical retail remains important because buyers still want to compare drum access, cycle claims, and control interfaces in person before making a higher-value purchase. Online channels are gaining share because price transparency is greater, assortment is wider, and model comparison is easier across retailers. Brand-led digital ecosystems from GE Appliances, Samsung, and LG also support online selling, as features can continue to improve after installation through downloadable updates and connected services. This keeps online momentum strong within the residential washer-dryer combo market, even though buyers still rely on stores for final product evaluation.

China’s 2024 trade-in subsidy program lifted September 2024 domestic washing machine sales value by more than 20% year over year. The same program rewarded higher-efficiency products, which helped e-commerce channels participate more actively in the uplift. That showed online channels can absorb policy-led demand spikes quickly and at scale. Exclusive brand outlets still matter for premium explanation, while project supply and hospitality channels are gradually becoming more relevant as built-in specifications rise. As service, diagnostics, and cycle upgrades move deeper into apps, digital channels should continue to take a larger share of the residential washer-dryer combo market. This does not remove the role of stores, but it does weaken the hold of traditional multi-brand comparison shopping over time.

Geography Analysis

Asia-Pacific held 35.53% of the residential washer-dryer combo market share in 2025 and is forecast to grow at a 7.61% CAGR through 2031. China sits at the center of that position because washing machine penetration reached 98.2 units per hundred households by the end of 2023, while standalone dryer penetration remained below 5%. China’s 2024 trade-in subsidy program also pushed domestic washing machine sales value up by more than 20% year over year in September 2024. Japan continues to favor compact, quiet appliances, while South Korea remains an important launch market for larger, higher-specification combos. India and Southeast Asia are expanding from a lower base as urban housing growth and e-commerce are widening first-time demand for residential washer-dryer combos.

Europe remains structurally important to the residential washer-dryer combo market because ecodesign and labeling rules keep energy performance visible at the point of purchase. Regulation (EU) 2019/2023 established a clear performance floor for washer-dryers across the region. Germany’s Umweltbundesamt stated that the country’s 40 million households account for one-third of private electricity use, with major appliances accounting for most of it. That makes the running-cost case for efficient combo units easier to communicate in Germany and nearby markets. The United Kingdom, France, Spain, the BENELUX region, and the Nordics continue to support demand for compact front-load models with better energy performance and stronger fabric care positioning.

North America has a distinct role in the residential washer-dryer combo market because 120V ventless formats better meet multifamily electrification needs than many traditional laundry setups. NREL confirmed in 2024 that standard-circuit combo units can help solve panel-capacity constraints in existing multifamily buildings. South America, the Middle East, and Africa are smaller today, but urbanization and dense residential construction are widening the long-run customer base. Mexico, the UAE, Saudi Arabia, South Africa, and Nigeria each follow different income and infrastructure paths, so that adoption will rise unevenly across those markets.

Competitive Landscape

The residential washer-dryer combo market has a semi-consolidated structure in which a limited group of global manufacturers sets the broad direction for technology, pricing, and supply. LG and Samsung remain central to premium heat pump development and connected laundry positioning. Samsung’s May 2026 Bespoke AI Laundry Combo added AI Wash & Dry+, an upgraded heat exchanger, and wider device integration. LG’s current ventless heat pump combo platform continues to emphasize inverter heat pump architecture and AI fabric sensing. BSH, Electrolux, Haier Smart Home, Midea, Whirlpool, GE Appliances, and Hisense are widening the competition through regional portfolios, distribution reach, and manufacturing depth.

Manufacturing geography is becoming a second competitive lever inside the residential washer-dryer combo market. GE Appliances announced a USD 490 million investment in Louisville in June 2025 to expand laundry production in the United States, including combo-related lines. Electrolux Group and Midea Group closed a 55/45 joint venture for fabric care manufacturing in South Carolina in April 2026, with production scheduled for the first half of 2027. These moves show that local production, tariff exposure, and component sourcing now matter almost as much as appliance specification. They also point to a North American demand profile that can support longer-cycle investment in ventless heat pump platforms.

A clear opening remains for a 120V ventless heat pump combo priced below USD 1,500 for multifamily retrofits. NREL’s building electrification work and DOE compliance deadlines both underscore the opportunity, as efficient standard-circuit platforms address real installation challenges in existing buildings. At the same time, service coverage and parts depth still limit faster adoption outside major metro areas. This leaves the residential washer-dryer combo market open enough to reward innovation, yet not so concentrated as to allow any one brand to dictate the category.

Residential Washer-Dryer Combo Industry Leaders

LG Electronics

Samsung Electronics

Whirlpool Corporation

Haier Smart Home

Bosch Home Appliances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Samsung Electronics announced the 2026 Bespoke AI Laundry Combo for global rollout, featuring a booster heat exchanger, AI Wash & Dry+ for expanded fabric type detection (including denim and outdoor wear), and an Enhanced Super Speed cycle directly addressing consumer concerns about the drying cycle.

- April 2026: Electrolux Group and Midea Group closed a 55/45 Fabric Care manufacturing joint venture in Anderson, South Carolina, with production expected to begin in H1 2027. A 50/50 North American sales JV for both brands is set to commence Q3 2026, representing one of the largest cross-border Fabric Care alliances in recent industry history.

- November 2025: GE Profile expanded the UltraFast Combo lineup with new Sapphire Blue and Jade Green finishes and 5 Wi-Fi-downloadable cycle programs (Kids Wear, Hand Wash, Drain & Spin, Sweat Stains, King-Sized Comforter), priced from USD 2,599 for a simplified white model to USD 2,999 for premium finishes.

- August 2025: Samsung showcased the second-generation Bespoke AI Laundry Combo at IFA 2025 in Berlin, with 3 kg additional drying capacity (15 kg to 18 kg) and a 20-minute reduction in drying time, enabled by an 8.5% larger heat transfer surface area from a denser heat exchanger fin layout.

Global Residential Washer-Dryer Combo Market Report Scope

Residential washer-dryer combo appliances are integrated laundry machines that perform both washing and drying in a single unit for household use. These appliances are increasingly adopted in residential settings due to their space-saving design, convenience, advancements in water and energy efficiency, and suitability for apartments, compact urban homes, and modern smart households. The residential washer-dryer combo market is segmented by product technology, loading type, installation type, capacity, smart connectivity, distribution channel, and geography. By product technology, the market is segmented into ventless condenser, heat pump, and hybrid/other technologies. By loading type, the market is segmented into front-load combo washer-dryers and top-load combo washer-dryers. By installation type, the market is segmented into built-in/integrated combo washer-dryers and freestanding combo washer-dryers. By capacity, the market is segmented into ≤8 kg, 8.1–10 kg, and >10 kg. By smart connectivity, the market is segmented into smart/Wi-Fi and non-smart/conventional appliances. By distribution channel, the market is segmented into multi-brand stores, exclusive brand outlets, online, and other distribution channels. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. The report provides the market size in USD for all the above-mentioned segments.

| Ventless Condenser |

| Heat Pump |

| Hybrid/Other |

| Front-Load Combo Washer Dryer |

| Top-Load Combo Washer Dryer |

| Built-In / Integrated Combo Washer Dryer |

| Freestanding Combo Washer Dryer |

| ≤8 kg |

| 8.1–10 kg |

| >10 kg |

| Smart / Wi‑Fi |

| Non‑smart/Conventional |

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia‑Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia‑Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Technology | Ventless Condenser | |

| Heat Pump | ||

| Hybrid/Other | ||

| By Loading Type | Front-Load Combo Washer Dryer | |

| Top-Load Combo Washer Dryer | ||

| By Installation Type | Built-In / Integrated Combo Washer Dryer | |

| Freestanding Combo Washer Dryer | ||

| By Capacity | ≤8 kg | |

| 8.1–10 kg | ||

| >10 kg | ||

| By Smart Connectivity | Smart / Wi‑Fi | |

| Non‑smart/Conventional | ||

| By Distribution Channel | Multi-brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia‑Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia‑Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the outlook for residential washer-dryer combos in 2031?

The category is projected to reach USD 9.64 billion by 2031, up from USD 6.96 billion in 2026, with a 6.73% CAGR over 2026 to 2031.

Which region leads demand and growth in this category?

Asia-Pacific led with 35.53% share in 2025 and is projected to grow at 7.61% CAGR through 2031, supported by compact housing, urban migration, and low standalone dryer penetration in China.

Why are heat pump formats becoming more important?

Heat Pump is projected to grow at a 7.34% CAGR through 2031, and the shift is supported by tighter energy rules in the United States and Europe, as well as manufacturers' greater focus on efficient ventless drying.

Why do front-load combos dominate product sales?

Front-load models accounted for 90.00% of revenue in 2025 because they remove more moisture before drying, support better energy performance, and align with premium ventless product architectures.

How important is smart connectivity to future demand?

Smart or Wi-Fi models are projected to grow at a 7.28% CAGR through 2031, supported by remote diagnostics, downloadable cycles, and utility-aligned demand-response use cases.

What is the biggest barrier to faster mass adoption?

Upfront pricing remains the main barrier because many advanced combo models still sit in premium price bands, especially in heat pump formats, even though long-term efficiency benefits are improving.

Page last updated on: