Residential Multi-Functional Kitchen Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.82 Billion |

| Market Size (2031) | USD 22.33 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

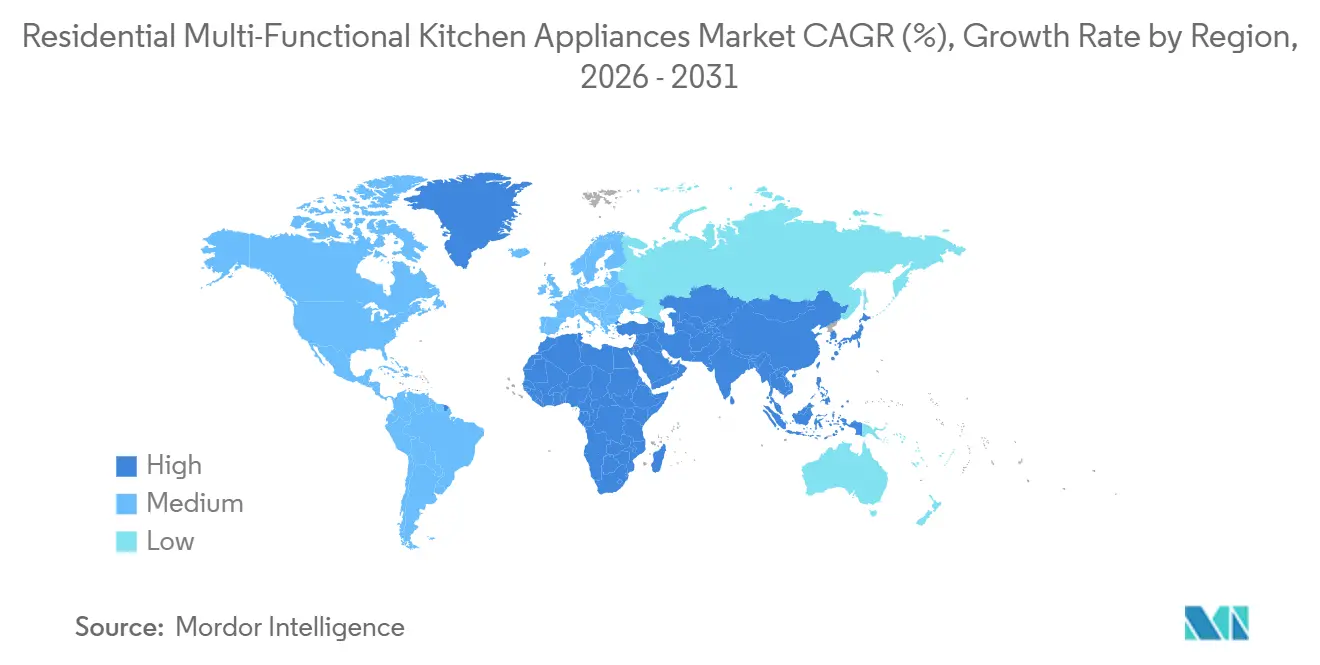

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Multi-Functional Kitchen Appliances Market Analysis by Mordor Intelligence

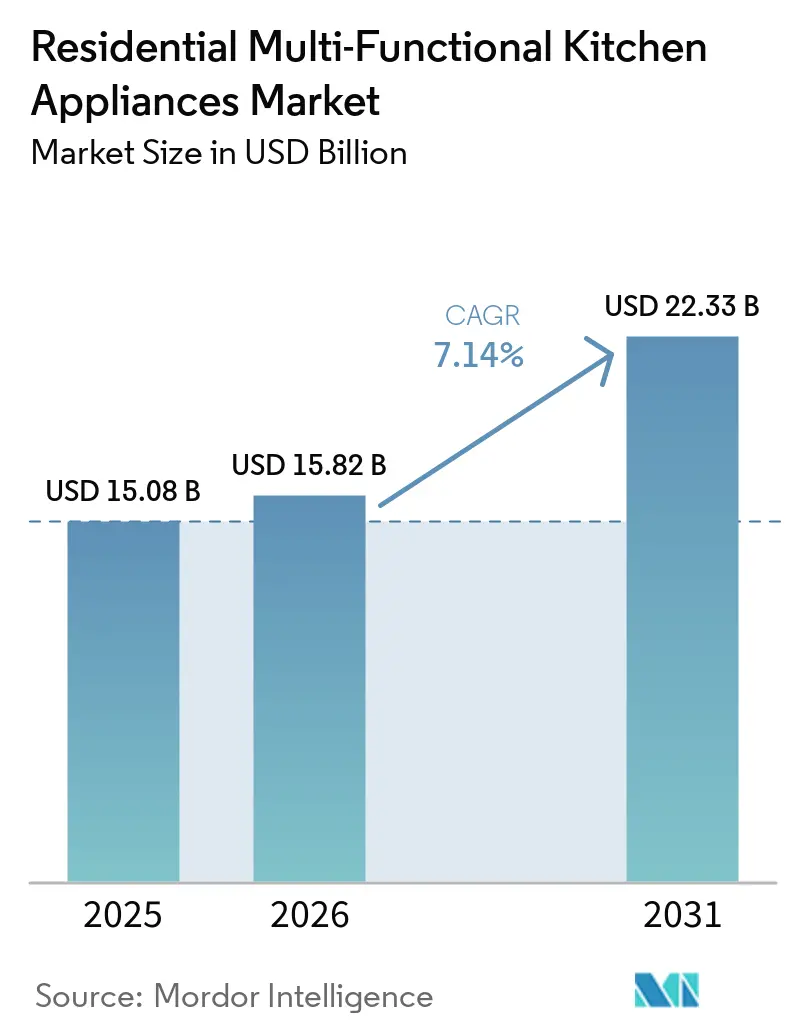

The Residential Multi-Functional Kitchen Appliances Market size is expected to grow from USD 15.08 billion in 2025 to USD 15.82 billion in 2026 and is forecast to reach USD 22.33 billion by 2031 at 7.14% CAGR over 2026-2031. Rising urban density in Asia-Pacific and Europe is reducing kitchen space and increasing the practical value of compact appliances that combine multiple cooking functions in a single unit. PFAS-related regulatory actions across the United States and the EU are also encouraging replacement demand, especially among households that bought PTFE-coated products before 2024 and are now shifting toward certified PFAS-free alternatives. The multi-functional kitchen appliances market is centered in a region where premiumization, urbanization, and policy factors reinforce one another. These conditions are strengthening brands' positions in the multi-functional kitchen appliances market by enabling them to manage digital demand generation, premium product design, and supply chain flexibility while protecting margins from tariff and material cost pressures [1]Breville Group Limited, “H1 FY26 Results for the Half Year Ended December 31, 2025,” Appliance Retailer, applianceretailer.com.au.

Key Report Takeaways

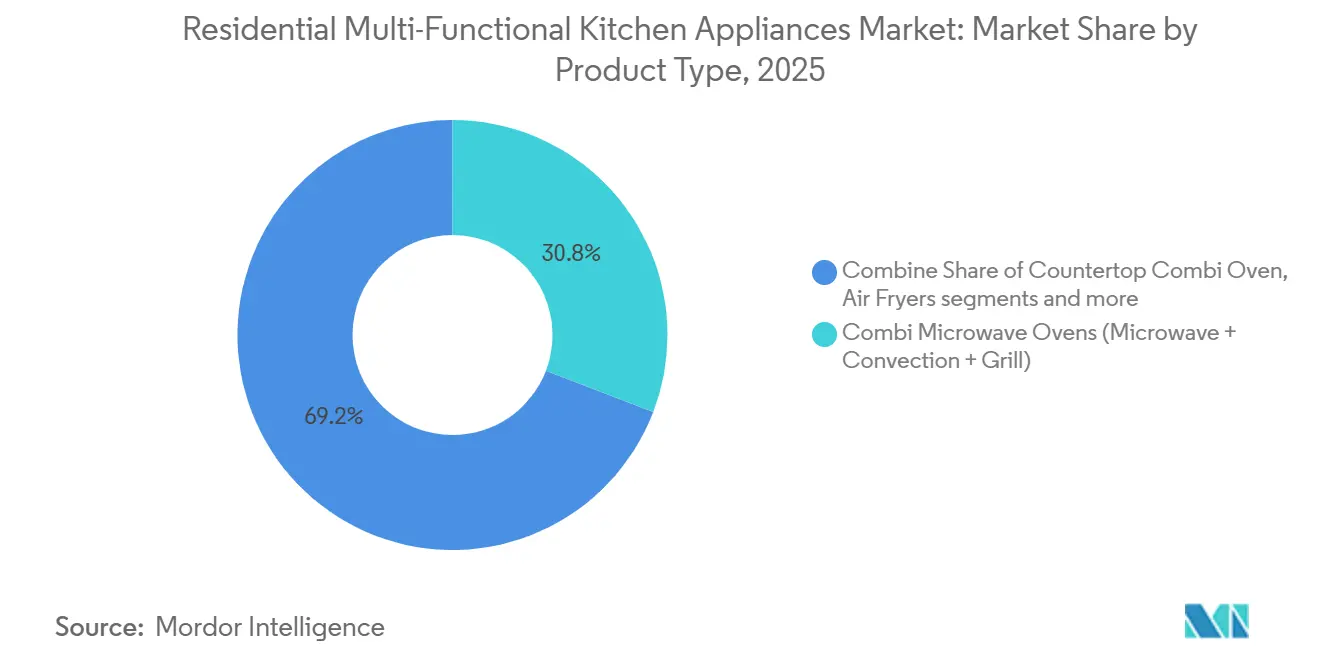

- By product type, combi microwave ovens held 30.82% share of the multi-functional kitchen appliances market size in 2025, while air fryers and air fryer ovens recorded the highest projected CAGR at 7.23% through 2031.

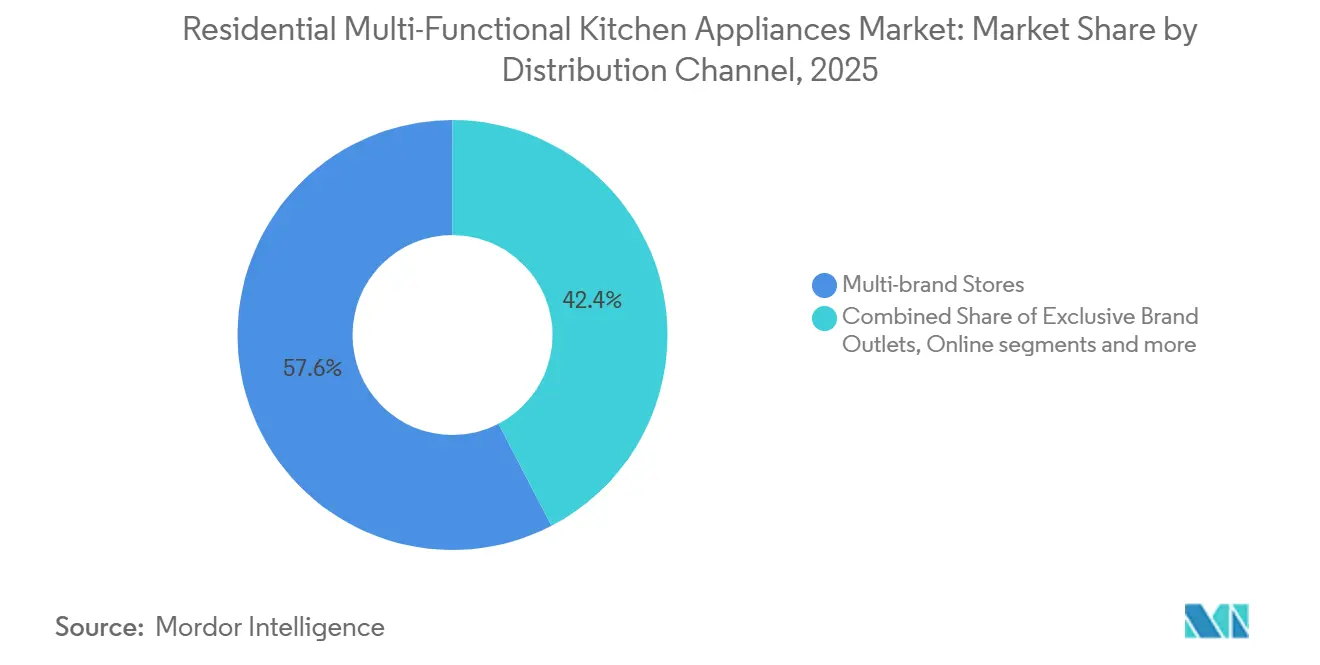

- By distribution channel, multi-brand stores accounted for 57.62% share of the multi-functional kitchen appliances market value in 2025, while online recorded the highest projected CAGR of 7.64% through 2031.

- By geography, Asia-Pacific held 43.82% of the multi-functional kitchen appliances market share in 2025, while the same region recorded the highest projected CAGR at 7.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Residential Multi-Functional Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sleek, space-saving & minimalist multi-functional appliances | +2.0% | Global, concentrated in Asia-Pacific urban centres and Western Europe | Medium term (2–4 years) |

| Health-oriented cooking with less oil boosts demand for air fryers and multi-cookers | +1.8% | Global, with highest intensity in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Energy cost savings per meal versus ovens spur adoption of countertop multi-functional cookers | +1.5% | Europe (energy price volatility), North America, Australia | Medium term (2–4 years) |

| Convenience and time-saving from all-in-one functionality | +1.0% | Global | Long term (≥ 4 years) |

| Algorithmic social virality accelerates category adoption via recipes and challenges | +0.9% | North America, Europe, South-East Asia, South Korea | Short term (≤ 2 years) |

| Regulatory and material shifts (PFAS-free, energy efficiency) catalyze upgrade cycles | +0.5% | North America (state-level bans), EU, Australia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sleek, Space-Saving & Minimalist Multi-Functional Appliances

The multi-functional kitchen appliances market is benefiting from a clear shift in how urban households evaluate kitchen equipment, with compactness now tied directly to practical value. Smaller apartments in Asia-Pacific and Europe are making consumers more selective about what stays on the countertop, favoring products that replace several single-purpose devices. This is changing the category from a discretionary add-on into a more essential kitchen purchase in space-constrained homes. The appeal is not limited to utility, as compact appliances with a clean visual design are also treated as part of the kitchen’s finished look, which supports premiumization across the multi-functional kitchen appliances market. That combination of footprint efficiency and design-led appeal is pushing consumers away from lower-tier products and toward mid-premium formats that cover more functions in a single appliance.

Health-Oriented Cooking With Less Oil Boosts Demand for Air Fryers and Multi-Cookers

The multi-functional kitchen appliance market is also benefiting from a stronger consumer focus on lower-oil cooking and daily use. Xiaomi’s 6.5L air fryer highlighted an 88% fat reduction claim compared with deep frying, a message that aligns well with growing concerns about dietary fat intake in Japan and South Korea. The same health positioning is spreading beyond standalone air fryers into pressure cookers and steam-combi units, broadening the category without losing its core use case. Moulinex launched the Cookeo Infinity in October 2025, combining pressure cooking and air-frying in a single closed system, directly reflecting demand for speed and reduced oil use in a single appliance. In France, household consumption of more than 7 kg of fries per year underscores the enduring relevance of this use case, especially in markets where fried foods already feature in everyday meal habits.

Algorithmic Social Virality Accelerates Category Adoption

The multi-functional kitchen appliance market is being reshaped by digital discovery in ways older appliance cycles did not. SharkNinja spends USD 700 million annually on advertising, with 70% directed to digital channels and 40% of that digital spend allocated to social media platforms. The original Ninja CRISPi glass air fryer has generated more than 715 million social media impressions since its 2024 launch, showing that attention can persist well beyond the initial launch window. Viral content is shortening the path from product release to sell-through because consumers can move from recipe videos or creator endorsements straight into a purchase decision. That favors larger, more integrated brands in the multi-functional kitchen appliances market, since they are better positioned to move quickly on product launches, manufacturing, and replenishment when demand spikes.

Energy Cost Savings Per Meal Versus Ovens Spur Adoption of Countertop Multi-Functional Cookers

The multifunctional kitchen appliance market is also supported by growing consumer focus on per-meal energy costs. In Europe, energy price volatility since 2022 has made the operating costs of full ovens easier for households to notice and compare with countertop alternatives. EU energy labeling was recognized by 93% of consumers in a 2024 Eurobarometer survey, and 75% said it influenced purchase decisions, which shows that efficiency claims are not abstract at the point of sale[2]In Focus, Energy Efficient Appliances,” Directorate-General for Energy, European Commission, energy.ec.europa.eu . Air fryers usually consume 1,200W to 2,000W for a typical cycle, while conventional ovens use 2,000W to 3,500W at full draw, so repeated weekly cooking can create meaningful annual savings for households. The United States Department of Energy’s proposed rescission of microwave oven energy conservation standards in May 2025 may also give brands more room to design next-generation combi microwave products with stronger thermal performance[3]Energy Conservation Program, Energy Conservation Standards for Microwave Ovens,” Federal Register, federalregister.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product safety recalls and overheating risks dampen consumer and retail trust | -0.6% | North America, Europe, Australia | Short to medium term (≤ 3 years) |

| Maturing penetration in developed markets slows incremental growth | -0.5% | North America, Western Europe, Japan, Australia | Long term (≥ 4 years) |

| Capacity and countertop-space limits constrain substitution for full ovens | -0.4% | North America (larger household appliance expectations), Europe | Medium term (2–4 years) |

| PFAS and non-stick scrutiny may raise input costs and restrict available coating materials | -0.4% | EU, North America (Minnesota, Maine, Colorado, Vermont) | Medium to long term (2–5 years) |

| Source: Mordor Intelligence | |||

Product Safety Recalls and Overheating Risks Dampen Trust

The multi-functional kitchen appliances market faces a significant restraint from product recalls, as highly visible safety failures can affect the entire category, not just the affected brand. In March 2024, Best Buy recalled 187,400 Insignia air fryers and air fryer ovens in the United States and 99,900 units in Canada due to overheating that could melt handles or shatter glass doors. USA TODAY’s review of CPSC data found that more than 3 million air fryers from multiple brands had been recalled in recent years for fire or burn hazards, and nearly 20% of the 259 incidents reviewed involved injuries that needed first aid or emergency room treatment. SharkNinja also initiated a voluntary recall of the Ninja Foodi OP300 pressure cooker in May 2025, with accrued recall remedy costs of USD 1.8 million reported as of Q1 2026. These events tend to shift retailers and consumers toward established brands, which can tighten distribution access for private-label and white-label suppliers across the multi-functional kitchen appliances market.

Maturing Penetration in Developed Markets Slows Incremental Growth

The multi-functional kitchen appliances market is also encountering slower incremental demand in developed economies where household penetration is already high. Groupe SEB reported that North America consumer sales declined 8.3% like-for-like in the first nine months of 2025, with Q3 alone down 14.4% like-for-like, reflecting weaker retail conditions after earlier adoption peaks. In these markets, growth depends less on first-time buyers and more on replacement cycles, and countertop appliances often have replacement intervals of 5 to 8 years. That changes the revenue model because brand performance starts to depend more on upgrades, accessories, and software-related attachment rather than fast unit expansion. As this shift becomes more visible, the multi-functional kitchen appliances market is likely to show a wider performance gap between leaders with stronger ecosystems and mid-tier brands that were built around volume-led household penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combi Microwave Ovens Lead While Air Fryers Extend Growth

Combi microwave ovens held 30.82% of the multi-functional kitchen appliances market share in 2025, making them the largest product segment by value. Their lead comes from long-established household use in Asia-Pacific and Europe, where microwave speed, convection baking, and grill functionality can be combined in one appliance without taking the space of 3 separate products. Air fryers and air fryer ovens are projected to grow at a 7.23% CAGR through 2031, which makes them the fastest-growing product type in the multi-functional kitchen appliances industry. That split between current leadership and future growth shows a category where mature formats still anchor revenue while newer formats are expanding household adoption among younger urban consumers.

The multi-functional kitchen appliances market is seeing especially strong product momentum from premium air fryer innovation and broader kitchen substitution use cases. Iris Ohyama launched a superheated-steam air fryer in Japan in December 2025, combining steam injection with hot-air crisping to improve moisture retention and product differentiation. Countertop combi ovens are also building a premium niche because they target renters and smaller households that want oven-like results without installing a full-size appliance. Instant Pot Brands launched the InstantHeat Toaster Oven line in August 2025 with graphene-powered heating, positioning it around the removal of preheat time and cooking that can be up to 60% faster than conventional ovens. Multi-cookers continue to attract demand in markets where electric cooking has added relevance, while food processors, blender-processor combinations, and stand mixers remain viable upgrade paths in the multi-functional kitchen appliances market through premium attachments, local cooking presets, and format consolidation.

By Distribution Channel: Multi-brand Stores Remain the Base While Online Gains Speed

Multi-brand stores commanded 57.62% of value in 2025, so they remain the main route to purchase in the multi-functional kitchen appliances market. Their position is tied to tactile product comparison, live demonstrations, and the trust that large retail banners provide in a category where safety, build quality, and ease of use matter at the point of sale. Online is the fastest-growing channel with a 7.64% CAGR through 2031, reflecting how search algorithms, creator content, and direct-to-consumer selling are changing appliance discovery. This is widening the role of digital content in the multi-functional kitchen appliances industry because many consumers now encounter products through recipes, short videos, and creator-led reviews before they ever visit a store.

At the same time, physical retail still matters because many purchases in the multi-functional kitchen appliances market remain considered decisions rather than impulse buys. Breville added 300 store-in-store locations at Best Buy USA in H1 FY26, showing that premium brands still value controlled physical presentation even while online expands. Other routes, including wholesale clubs, department stores, and quick-commerce platforms, keep a meaningful role in selected geographies, especially in India and North America where delivery speed and bundled pricing can influence channel choice. The likely result is a more showroom-like role for stores by 2031, with more consumers researching online, validating products in person, and then completing the final transaction digitally. Brands that manage consistent pricing, strong product video assets, and clear omnichannel coordination should be better placed to capture share as the multi-functional kitchen appliances market shifts further toward blended buying journeys.

Geography Analysis

Asia-Pacific held 43.82% of the multi-functional kitchen appliances market share in 2025 and is projected to expand at a 7.56% CAGR through 2031, which keeps it both the largest and fastest-growing regional market. China remains central to the region’s value base, and Supor reported 3.4% like-for-like growth in kitchen electric sales during the first nine months of 2025, supported by strength in rice cookers, oil-less fryers, and woks alongside digital channel investment. Japan is showing a clear preference for hybrid formats, with Thanko launching the Fry 2 Buddy in March 2025 as a 2-in-1 air fryer and electric pot, and Xiaomi Japan adding smart air fryer SKUs with app-led positioning through 2025. India is entering a more active premium demand phase, and SharkNinja’s April 2026 entry, with 330+ service centers and multiple e-commerce channels, shows that the multi-functional kitchen appliances market in the country now supports direct investment from global branded players.

North America and Europe remain the main centers of premium demand, but they are also the regions where maturity is becoming more evident in the multi-functional kitchen appliances market. In France, Moulinex held 84% value share in the multi-cooker segment as of August 2025, showing how dominant incumbents can become in established subcategories. Versuni and Unilever Foods announced a multi-year co-marketing partnership in May 2026 that will place Philips Airfryer products alongside Knorr seasoning lines in Tesco United Kingdom from July 2026, signaling a shift toward increasing usage frequency among existing owners rather than focusing solely on new device sales. In the United States, Instant Pot remained the 1 multicooker by sales as of June 2025, showing that brand leadership still matters in replacement-led demand environments. Regulation is also driving change across both regions, with Minnesota’s PFAS ban taking effect in January 2025 and the EU REACH evaluation advancing toward an end-of-2026 opinion, accelerating PFAS-free product pipelines across incumbent and challenger brands.

South America, the Middle East and Africa represent smaller value pools today. Still, they offer a stronger upside in the multi-functional kitchen appliances market as branded penetration expands from a lower base. Groupe SEB reported double-digit growth in electrical cooking and food preparation in Colombia during Q3 2025, while Brazil remained robust in blenders and single-serve coffee, showing that regional demand is broadening across adjacent countertop categories. In the Middle East and Africa, the UAE and Saudi Arabia are the main anchors of premium demand. At the same time, South Africa and Nigeria are still early-stage markets where affordability and power reliability continue to shape adoption. SharkNinja’s FY2026 guidance for 10% to 11% net sales growth and its ongoing expansion into additional retailers and markets indicate that international growth plans increasingly include these emerging geographies within the multi-functional kitchen appliances market.

Competitive Landscape

The multi-functional kitchen appliances market is low concentrated at the top and across a broad mid-tier and regional brand base. One competitive cluster includes Western brand-builders such as SharkNinja, Instant Brands, Breville, and Versuni, which compete on fast product cycles, strong digital selling, and direct-to-consumer execution. SharkNinja reported net sales of Cooking and Beverage Appliances of USD 1.82 billion in FY2025, with international net sales up 20.8%, indicating that global expansion is becoming a major growth lever for the company[4]SharkNinja, Inc., “SharkNinja Reports Fourth Quarter and Full Year 2025 Results,” SharkNinja Newsroom, newsroom.sharkninja.com. A second cluster includes Asian conglomerates such as Midea, Haier, Samsung, LG, and BSH, which tend to compete on manufacturing scale, combi microwave depth, and broad retail reach across Asia-Pacific and EMEA. In contrast, a third cluster includes premium and design-led specialists such as Vorwerk, Breville, and other focused connected-cooking brands.

A major theme in the multi-functional kitchen appliances market is the shift from hardware-only competition toward a closer integration of devices, software, and recurring content. Recipe subscriptions, app-guided cooking, and personalized usage prompts are becoming part of the value proposition because they help brands hold attention after the original appliance sale. Breville expanded the B2B footprint of its Beanz coffee subscription platform to Williams Sonoma, Crate & Barrel, and John Lewis Partners in FY2025, showing how service extensions can deepen ecosystem presence around the appliance relationship. Instant Pot’s app-connected products also point in the same direction, where branded content and digital support sit alongside physical product performance. The white space remains strongest in affordable connected formats, where the multi-functional kitchen appliances market still has room for credible brands that can pair mid-market price points with useful software and service layers.

Cost pressure is making scale and execution even more important in the multi-functional kitchen appliances market. Breville said United States tariffs on China-manufactured goods reduced gross margin by 130 basis points in H1 FY2026, even after 80% of United States gross margin production had been moved outside China by December 2025. PFAS reformulation adds another layer of costs and compliance work, which raises the minimum investment needed to remain credible in premium non-stick categories. As recalls, tariff exposure, and material changes increase operating complexity, the likely outcome is that stronger brands with supply chain flexibility, trusted quality, and better digital demand generation will keep widening the gap with smaller, commodity-volume participants.

Residential Multi-Functional Kitchen Appliances Industry Leaders

SharkNinja (Ninja)

Versuni (Philips Domestic Appliances)

Groupe SEB

Midea Group

Instant Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Versuni (Philips) and Unilever Foods (Knorr) launched a multi-year co-marketing partnership beginning in Tesco United Kingdom in July 2026, combining Philips Airfryer product placement with Knorr seasoning lines.

- April 2026: SharkNinja entered India with five products including the Ninja Combi 14-in-1 multicooker, Ninja DoubleStack and DualZone air fryers, and the Shark FlexBreeze fan, establishing presence across 330+ service centers and multiple e-commerce platforms from day one.

- January 2026: Cosori (VeSync) launched the Iconic smart air fryer, a USD 249 stainless-steel, PFAS-free ceramic-coated 6.5-quart appliance with a 5-year limited warranty, 3 to 5 times the industry norm, and VeSync app integration. The product won the 2025 Red Dot Design Award and is positioned explicitly at the premium health-conscious segment

- October 2025: SharkNinja expanded its glass air frying system with the Ninja CRISPi PRO, a USD 279 6-quart countertop glass air fryer available at Target and SharkNinja.com.

Global Residential Multi-Functional Kitchen Appliances Market Report Scope

| Air Fryers & Air Fryer Ovens |

| Countertop Combi Ovens (Convection/Air Fry/Steam) |

| Combi Microwave Ovens (Microwave + Convection + Grill) |

| All-in-One Cookers or Multi-Cookers |

| Multi-Cookers (Electric pressure/slow/rice) |

| Food Processors & Blender-Processor Combos |

| Stand Mixers with Multi-Functional Attachments |

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Air Fryers & Air Fryer Ovens | |

| Countertop Combi Ovens (Convection/Air Fry/Steam) | ||

| Combi Microwave Ovens (Microwave + Convection + Grill) | ||

| All-in-One Cookers or Multi-Cookers | ||

| Multi-Cookers (Electric pressure/slow/rice) | ||

| Food Processors & Blender-Processor Combos | ||

| Stand Mixers with Multi-Functional Attachments | ||

| By Distribution Channel | Multi-brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for the multi-functional kitchen appliances market?

The Residential Multi-Functional Kitchen Appliances Market size is expected to grow from USD 15.08 billion in 2025 to USD 15.82 billion in 2026 and is forecast to reach USD 22.33 billion by 2031 at 7.14% CAGR over 2026-2031.

Which product category leads revenue today and which one is growing fastest?

Combi microwave ovens led with a 30.82% share in 2025, while air fryers and air fryer ovens are projected to grow fastest at a 7.23% CAGR through 2031.

Why are compact all-in-one appliances gaining traction in urban homes?

Smaller kitchens in Asia-Pacific and Europe are raising the value of every countertop inch, which is making combination appliances more attractive than single-purpose products.

Which region is leading demand globally?

Asia-Pacific held 43.82% of value in 2025 and is also the fastest-growing region with a projected 7.56% CAGR through 2031

How is online shopping changing appliance sales?

Multi-brand stores still led with 57.62% of value in 2025, but online is growing fastest at 7.64% CAGR as social discovery and algorithm-led search shorten the purchase path.

Page last updated on: