Residential Built-in Kitchen Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

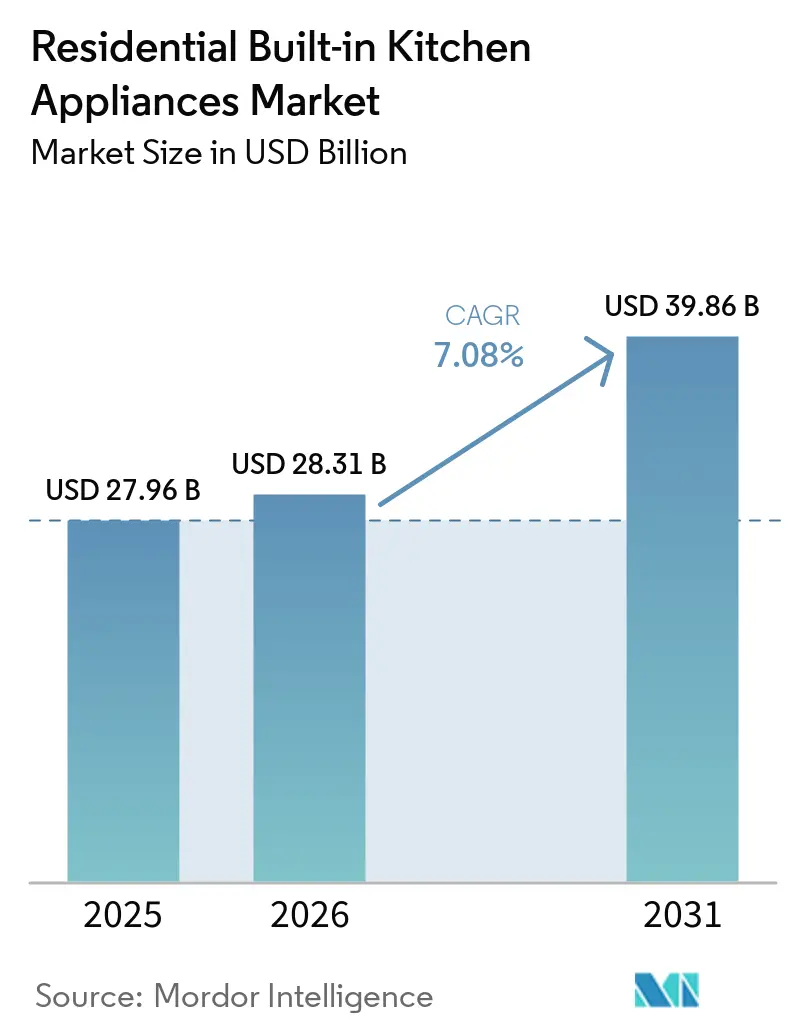

| Market Size (2026) | USD 28.31 Billion |

| Market Size (2031) | USD 39.86 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Built-in Kitchen Appliances Market Analysis by Mordor Intelligence

The residential built-in kitchen appliances market size is projected to expand from USD 27.96 billion in 2025 and USD 28.31 billion in 2026 to USD 39.86 billion by 2031, registering a CAGR of 7.08% between 2026 and 2031. This acceleration reflects a structural shift toward seamless integration into cabinetry, driven by premium kitchens that prioritize aesthetics alongside performance. LG Electronics unveiled its complete built-in suite at EuroCucina 2026, addressing Europe's rising energy costs and space constraints through AI-driven efficiency and 189-millimeter ultra-slim cooktop designs that maximize under-counter storage[1]LG Electronics PR Team, “LG Electronics Unveils New Full Built-in Kitchen Suite at EuroCucina 2026,” LG Electronics Newsroom, en.prnasia.com. Samsung's extractor induction hob, launched in April 2026, eliminates the need for separate range hoods. Its Boost mode delivers 720 m³/h suction while achieving A+ energy efficiency, a response to open-plan layouts where visible ventilation disrupts design continuity[2]Samsung Communications, “Samsung Expands Kitchen Portfolio With Intelligent Performance and Refined Design,” Samsung Global Newsroom, news.samsung.com. Regulation acts as a filter, accelerating premium efficiency and electrification, especially in the European Union and select United States states, thereby influencing product roadmaps and the retirement of legacy models. Digital channels and direct-to-consumer strategies increase reach for configurable built-ins, while builder and kitchen studio partnerships remain critical for high-value projects. Competitive intensity is high as global conglomerates anchor supply and premium specialists expand design-led portfolios, creating more choice for buyers who prioritize integration, energy savings, and smart orchestration.

Key Report Takeaways

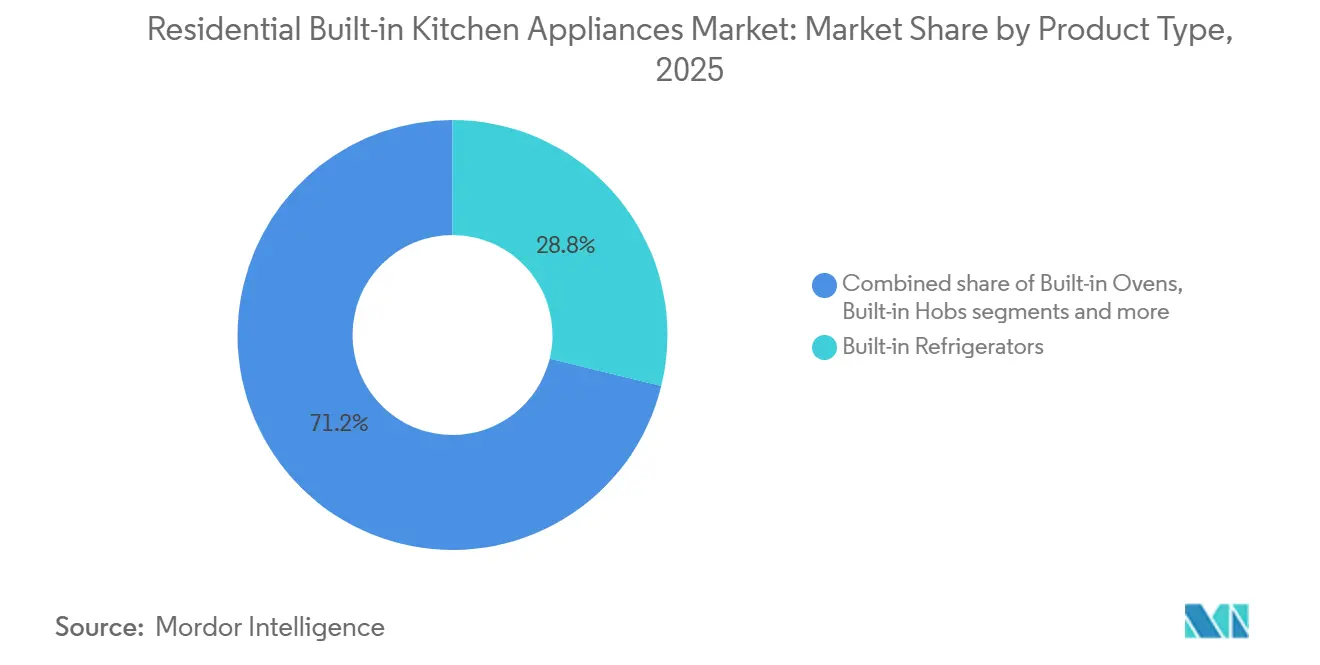

- By product type, built-in refrigerators led with 28.82% of the residential built-in kitchen appliances market share in 2025, while built-in hobs/cooktops are projected to expand at a 7.33% CAGR through 2031.

- By installation/integration, standard built-in (visible fronts) held 45.92% of the residential built-in kitchen appliances market share in 2025, whereas fully integrated/panel-ready is forecast to grow at a 7.25% CAGR through 2031.

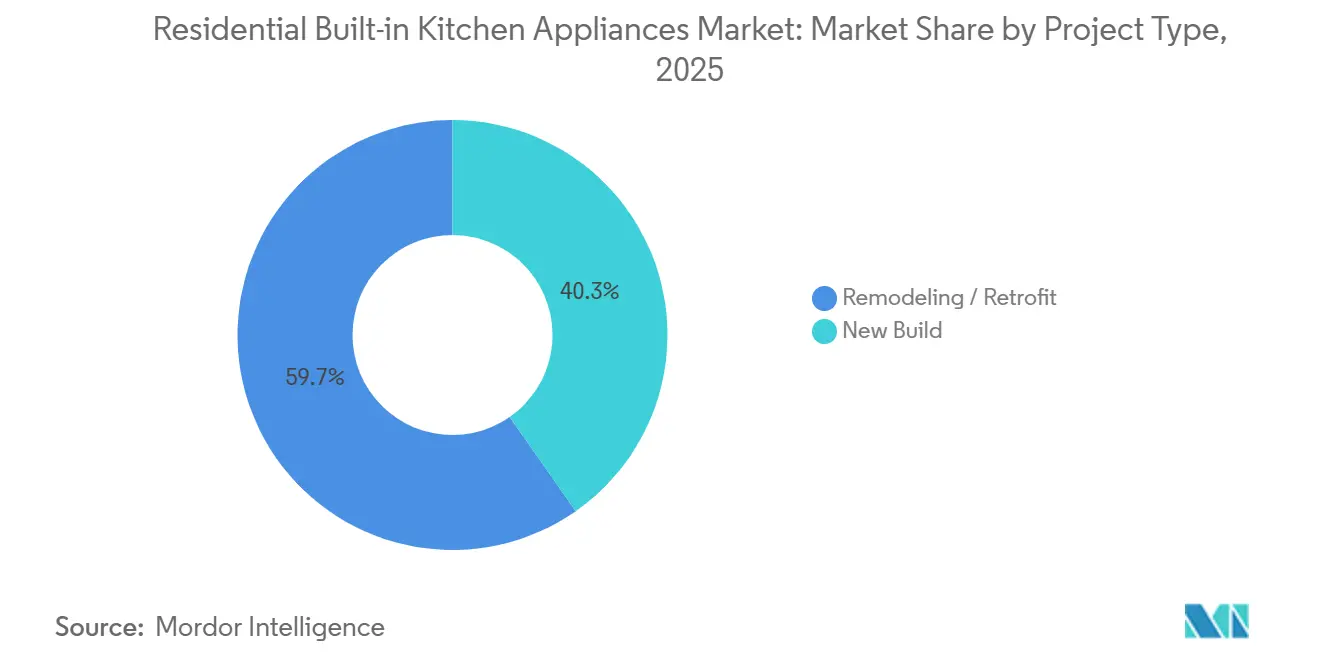

- By project type, remodeling/retrofit accounted for 59.71% of the residential built-in kitchen appliances market share in 2025, while new-build installations are set to grow at a 7.10% CAGR through 2031.

- By distribution channel, exclusive brand stores held 40.12% of the residential built-in kitchen appliances market share in 2025, while online channels are expected to grow at a 7.58% CAGR through 2031.

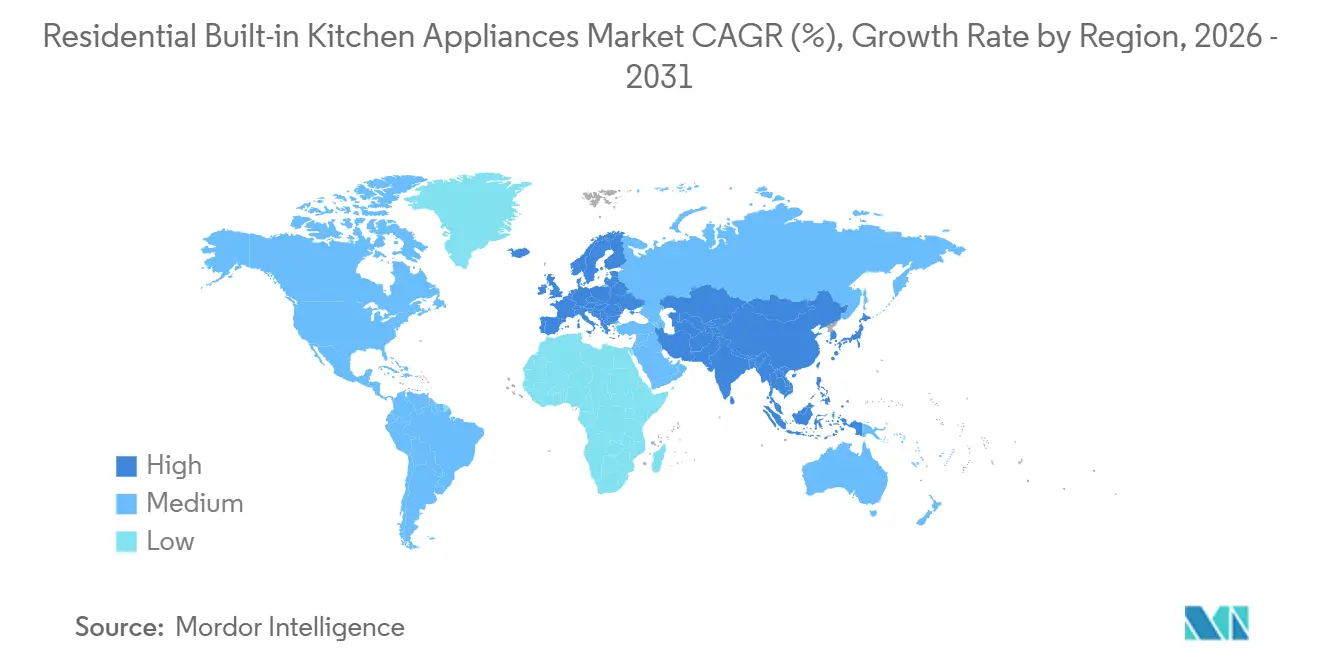

- By geography, Europe captured 44.64% of the residential built-in kitchen appliances market share in 2025, while Asia-Pacific is projected to grow at an 8.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Residential Built-in Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and modular kitchens are raising integrated adoption | + 1.8% | Global, particularly Europe, North America, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Smart/connected built-ins are gaining traction | + 1.5% | North America, Western Europe, China, South Korea | Medium term (2-4 years) |

| Energy-efficiency regulations and labeling steer purchase | + 1.3% | EU (A–G rescaling), California (Title 24), United Kingdom, Australia | Short term (≤ 2 years) |

| Omnichannel and online acceleration for built-in categories | + 1.0% | Global, with early gains in North America, China, and urban India | Short term (≤ 2 years) |

| Building electrification is accelerating induction and electric built-ins | + 1.2% | California, EU member states, Canada (select provinces), Australia | Long term (≥ 4 years) |

| Beverage centers and built-in coffee/wine surge with at-home entertaining | + 0.3% | North America, Western Europe, Middle East (UAE, Saudi Arabia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization and Modular Kitchens Raising Integrated Adoption

Buyers now prize flush-mounted, panel-ready formats that unify appliances with cabinetry, maintaining clean sightlines in premium kitchens. This design-led preference aligns with expanded luxury lineups, such as SKS integrated columns with bead-blasted all-metal interiors that maintain tight temperature tolerances favored by culinary enthusiasts. SKS, early selection during renovation cycles is essential because cabinet dimensions, ventilation routes, and electrical provisions must be planned months in advance to achieve a seamless outcome. Performance and aesthetics are converging, which insulates premium built-ins from broader slowdowns, as shown by a 4% lift in BSH’s built-in segment in Europe in 2025 amid a challenging demand backdrop[3]BSH Corporate Communications, “BSH Showcases Personalized AI for the Kitchen at CES 2026,” BSH Pressroom, press.bsh-group.com. At EuroCucina 2026, brands emphasized integrated designs that address energy costs and limited space, reinforcing the momentum behind panel-ready systems that disappear into millwork.

Smart/Connected Built-ins Gaining Traction

Connectivity is shifting from novelty to expectation as Wi-Fi, Matter protocol, and AI assistants enable remote support, OTA updates, and multi-appliance orchestration. BSH presented the first Matter-enabled refrigerator, then committed to shipping all new United States. BSH refrigerators with Matter in 2025, lowering ecosystem barriers for mixed-brand homes. The European Commission's Joint Research Centre expanded its Code of Conduct for energy-smart appliances in March 2026 to cover energy management systems, photovoltaic inverters, batteries, and EV chargers alongside white goods, promoting semantic interoperability so products from different brands can coordinate demand response—nearly 130 compliant models were in production or imported into the EU by March 2026, with a searchable filter added to the EPREL database[4]Joint Research Center Team, “Energy Smart Appliances Code of Conduct Expands Coverage,” European Commission JRC, joint-research-center.ec.europa.eu. GE Profile introduced a Kitchen Assistant with a Scan-to-List barcode scanner and in-fridge camera integration that ties directly into digital grocery workflows, signaling how appliances will manage more of the planning and replenishment process. Bosch’s Cook AI blends agentic AI with sensors and the Home Connect App to coordinate cooking tasks across appliances in real time.

Energy-Efficiency Regulations and Labeling Steering Purchase

Tighter rules are pushing lower-performing appliances out of the channel and raising the floor on new model launches. The United States Department of Energy standards and ENERGY STAR specifications for electric cooking products establish clear IAEC thresholds that guide brand portfolios for the next product cycles. In Europe, the A–G label rescale and updated EEI values for the cold and dishwashing categories are already in effect, with new tumble dryer rules taking effect in July 2025. APPLiA has advised the Commission to adopt digital labels alongside printed ones and allow 24–36 months for implementation to reduce scrap risk and improve investment planning for manufacturers. Premium products are now beating baseline A-grade thresholds, with Samsung’s AI dishwasher reaching A-20% performance on the Eco cycle, and LG pushing A-grade efficiency through AI control systems. California’s Title 24 raises the bar further by requiring 240-volt kitchen circuits in new homes and setting higher ventilation requirements for gas, nudging builders toward electric built-ins.

Building Electrification Accelerating Induction and Electric Built-ins

Decarbonization goals across regions are speeding the shift from gas to induction and other electric formats that deliver higher efficiency and improved indoor air quality. CalMTA’s Induction Cooking Market Transformation Initiative targets significant system benefits and aims to have induction reach 50% of cooktop and range sales in California by 2035. Field studies on 120-volt battery-equipped induction ranges show that integrated energy storage can support daily cooking loads on standard circuits, which helps multifamily properties avoid costly panel upgrades. Premium induction platforms continue to add flexible power zones for oversized cookware, as shown by SKS’s 36-inch Full-Flex Induction Cooktop with Power Shift Plus and AI Water Boiling Alert. LG’s hood-integrated induction design, with a 189-millimeter ultra-slim body, addresses both space constraints and open-plan ventilation, which supports adoption in compact European kitchens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership and complex installation | - 1.5% | Global, magnified in price-sensitive markets (Latin America, Southeast Asia, Eastern Europe) | Medium term (2-4 years) |

| Skilled labor shortages and extended lead times | - 0.8% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Smart home interoperability is still maturing across ecosystems | - 0.5% | Global, with early friction in North America, Western Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Cabinet dimension standards limit universal fitment across regions | - 0.4% | Global, particularly Europe (60cm) vs. North America (30/36-inch) divergence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Complex Installation

Built-ins typically command price premiums over freestanding models, while installation adds costs for cabinetry, electrical work, and professional labor, which can strain budgets in retrofit projects. CalMTA found that 27–41% of California homes would need panel upgrades for 240-volt ranges, with single-family upgrades commonly ranging from USD 2,500 to USD 5,000 and multifamily conversions reaching much higher levels depending on building infrastructure. Battery-integrated induction ranges that operate on standard 120-volt circuits show promise for sidestepping panel constraints, though current retail pricing positions them for early adopters. Operating cost dynamics can also deter switching from gas when electricity rates are unfavorable. However, California’s planned fixed-charge reform, scheduled for late 2025 or early 2026, is expected to improve per-kWh economics. Service and repair costs add to total cost concerns for induction cooktops, while the vulnerability of glass tops to impact damage remains a risk factor cited by consumers. To ease retrofit friction, Whirlpool’s Fit System Limited Guarantee offers up to USD 300 toward cabinet modifications if wall ovens do not fit existing cutouts, addressing a common barrier to replacements.

Skilled Labor Shortages and Extended Lead Times

Electrification policies are boosting demand for licensed electricians who perform panel upgrades and new circuit runs, and CalMTA has cautioned that workforce capacity could become a bottleneck during adoption surges. Manufacturers are also addressing skilled trade gaps by redesigning work patterns and investing in plant automation, as seen at GE Appliances’ cooking plant in Georgia, with flexible staffing and new roles aligned with robotics. The residential built-in kitchen appliances market faces schedule risk from localized production and parallel SKUs that respond to regional standards, and regional slowdowns have already highlighted supply fragility. Lead times for panel-ready dishwashers and column refrigeration stretched in 2024–2025 due to slower real estate turnover, prompting some distributors to adopt stock-and-hold strategies. These pressures reinforce the importance of early specification and capacity planning across projects that rely on integrated formats with narrow installation tolerances.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hobs Drive Electrification, Refrigeration Anchors Share

Built-in refrigerators held 28.82% of the residential built-in kitchen appliances market share in 2025, maintaining leadership due to category necessity, broad format choice, and stronger premium attachment to panel-ready columns and smart inventory features. Built-in hobs and cooktops are projected to grow fastest at a 7.33% CAGR to 2031 as induction adoption accelerates with electrification policies, integrated downdraft designs, and performance advances that remove fixed-zone constraints. Venting induction platforms are eliminating separate hoods in many layouts, with Samsung’s extractor induction hob achieving A+ energy efficiency and 720 m³/h Boost suction, suited to islands and open-plan spaces. LG’s flexible induction surfaces and boil alerts further improve usability, bringing responsive control and chatty alerts into daily workflows. SKS has also elevated sustainability signaling by introducing ENERGY STAR-certified induction platforms at luxury price points, supporting high-end buyers who want both design and efficiency.

Dishwashers and ovens are regaining momentum as upgrades pair premium finishes with energy gains and lower noise. BSH reported that its 60-centimeter dishwashers in Europe reached an A energy class across all models, and global dishwasher sales rose in 2025, reinforcing confidence in this core built-in. GE Appliances’ Monogram panel-ready 24-inch dishwasher launched with a 37 dBA quiet cycle, widening appeal among noise-sensitive buyers and open-plan layouts. Combination wall oven designs also converge ovens and microwaves to compress footprints while adding air fry and smart control features that meet modern cooking preferences. Ovens are improving with in-oven cameras and AI-assisted cooking that handle recognition and temperature control, reducing guesswork and supporting consistent results across varied cuisines.

By Installation/Integration: Panel-Ready Gains Momentum, Standard Formats Hold Majority

Standard built-ins accounted for 45.92% in 2025, keeping the largest share with visible fronts that fit most remodel budgets, while fully integrated or panel-ready formats are forecast to grow at 7.25% CAGR as buyers lean into invisible appliances and architectural continuity. The residential built-in kitchen appliances market size for fully integrated or panel-ready formats is poised to expand faster as premium kitchens prize uniform cabinet faces and minimal visual noise. Panel-ready columns are central to this shift, with SKS offering integrated columns that accept custom or branded panels and provide professional or transitional handle options for a flush aesthetic. Samsung’s handle-less flat-front refrigeration and Auto Open Door design fit side-by-side configurations and support pairable installations. Low-noise panel-ready dishwashers reinforce the silent, seamless kitchen trend by disappearing behind cabinet facades while improving the sound profile during operation.

Standard formats continue to thrive because they deliver recognizable finishes, a more straightforward fit, and lower installation complexity. Bosch’s carbon black glass fronts and digital control ring meet contemporary tastes without the added cost of custom panels. Siemens’ matte finishes and improved scratch resistance aim to preserve clean lines for longer in heavy-use kitchens. Whirlpool’s flush-install over-the-range oven with hidden venting reduces visual clutter for customers who want a built-in look around standard cabinet depths, and ADA-compliant wall ovens broaden the addressable base in standard openings. These options sustain balance in the residential built-in kitchen appliances market by giving mid-market remodels a clear path while panel-ready formats scale in premium tiers.

By Project Type: Remodels Dominate, New Construction Electrifies Faster

Remodeling or retrofit projects accounted for 59.71% of demand in 2025, reflecting replacement cycles and layout upgrades, while new builds are projected to grow at a 7.10% CAGR on the back of electrification-ready codes and builder differentiation strategies. The residential built-in kitchen appliances market benefits from Title 24 standards in California, which set 240-volt kitchen circuits as a baseline in new homes, lowering the future conversion cost for electric cooking. Retrofit complexity can be a constraint when panel upgrades are required for new ranges and wall ovens, raising overall project costs and extending timelines. Battery-integrated induction products that run on standard circuits offer a path for constrained buildings, although current pricing skews toward early adopters.

New-build projects have an advantage in early specification, with developers locking in SKUs months before occupancy and coordinating electrical, ventilation, and cabinetry with appliance dimensions. Brands invest in North American manufacturing capacity to capitalize on this opportunity and reduce supply volatility risks in high-demand categories. Premium brands are refining integrated lines that suit modular layouts, with hinges and door profiles that enable flush fits even in tight spaces. These factors combine to support a healthy pipeline for the residential built-in kitchen appliances market across both renovation and construction channels.

By Distribution Channel: Online Surges, Exclusive Brand Stores Anchor Premium

Exclusive brand stores captured 40.12% of demand in 2025 by enabling hands-on trials, cabinet integration planning, and high-touch consultations for panel-ready suites, while online channels are forecast to grow at 7.58% CAGR as e-commerce reduces friction with configurators and bundled services. The residential built-in kitchen appliances market size for online channels is supported by direct-to-consumer launches, delivery offers, and transparent inventory signals that fit premium buyer expectations. Samsung’s 2026 rollout paired website availability with retail partners and added delivery incentives, which align with the rising role of digital-first research paths. KitchenAid highlighted how online-exclusive promotions and service details can speed purchase decisions for higher-spec dishwashers. B2B and contract portals are also integrating with developer workflows to ensure a reliable supply of builder-focused SKUs at scale.

Experience centers are expanding across North America and Asia to complement digital journeys with tactile evaluations that often decide panel-ready investments. Online category growth is also reinforced by brand apps that simplify setup and usage, from scan-to-connect to guided cooking and OTA updates. As e-commerce and retail showrooms work in tandem, the residential built-in kitchen appliances market extends reach to both premium and mid-market buyers with distinct service expectations.

Geography Analysis

Europe accounted for 44.64% of the residential built-in kitchen appliances market share in 2025, while Asia-Pacific is projected to record the highest growth at an 8.26% CAGR through 2031, driven by urbanization and the adoption of modular kitchens. EU energy labels, rescaled to A–G, and updated ecodesign limits are driving rapid product refreshes in core categories, while new tumble dryer rules take effect in July 2025. APPLiA’s 2026 recommendations call for digital labels and longer lead times for regulatory changes to stabilize investments and avoid unnecessary component scrap. EuroCucina 2026 showcased continued focus on slim, efficient, and panel-ready solutions, with LG and Samsung highlighting AI features that address energy costs and compact footprints. Miele’s MasterCool III launch, with FoodView cameras and master-fresh systems, illustrates the region’s premium preservation trend.

Asia-Pacific expands faster as incomes rise and urban living prioritizes modular spaces that fit 60-centimeter formats, compact columns, and panel-ready machines. BSH strengthened its R&D presence in China to support regional specificity even as competitive intensity weighed on Greater China in 2025. Haier and GE Appliances brands focus on city living and small-space solutions, which align with high-density housing in leading Asian metros. Australia’s premium segment illustrates how online bundles can simplify decision-making for built-in packages, supporting e-commerce growth in the region. India’s designation as an independent BSH region from 2026 highlights the potential for future expansion of modular kitchens and integrated lines tailored to local tastes.

North America benefits from sustained remodeling activity, electrification codes, and resurgent premium brands. GE Appliances has expanded its United States manufacturing footprint and supplier network to reduce risk and bring production closer to buyers, which supports availability for high-volume SKUs and emerging induction demand. California’s Title 24 and the Induction Cooking MTI point to steady electrification of cooking, with long-term targets that will influence kitchen specifications. Premium players continue to expand their presence through design centers and new launches that emphasize AI, cameras, and quiet performance, reinforcing the value of integrated suites. South America’s demand is tied to economic recovery and urban infill, with brands emphasizing localized production and pricing strategy to manage currency volatility, and Middle East & Africa growth often follows premium residential development and expatriate demand.

Competitive Landscape

The residential built-in kitchen appliances market is anchored by multi-brand conglomerates that span mass to ultra-luxury tiers, with BSH Home Appliances Group, Electrolux Group, Whirlpool Corporation, and Haier Smart Home shaping global supply. Premium specialists such as Sub-Zero Group, Miele, V-ZUG, SMEG, and Bertazzoni lead design-forward adoption, particularly for panel-ready suites and specialized preservation technologies that reward long-term performance. Strategy execution shows portfolio management to avoid cannibalization, localization to reduce supply risk, and technology differentiation through AI-assisted experiences. BSH remains the largest non-Chinese home appliance manufacturer in China and has defended its position through regional growth. At the same time, its North American business also gained share through portfolio expansion and local market tailoring. Sub-Zero’s premium positioning is reinforced by its built-in refrigeration focus and long-life quality promise, which aligns with design-led kitchen demand.

Recent launches illustrate how AI, camera integration, and app coordination are now central to differentiation across refrigerators, dishwashers, and ovens. GE Profile’s Kitchen Assistant and FridgeFocus camera reframe the refrigerator as a planning tool, while Bosch’s Cook AI and Miele’s CulinaryCoach aim to simplify precision cooking with guided steps and personalized recommendations. Samsung’s Auto Connectivity highlights the appeal of single-brand orchestration that automates ventilation and lighting based on range usage, increasing utility without user input. As these features become standard, buyers expect consistent support, transparent update cycles, and interoperability beyond single-brand suites, a direction also emphasized in the EU’s interoperability work.

Investment in regional production and supply resilience continues alongside premiumization. GE Appliances’ sustained United States investments support speed-to-market and builder availability, while European brands emphasize design centers and showpieces at flagship events to reinforce leadership. Emerging innovators such as Copper’s battery-equipped induction range demonstrate alternative paths to electrification through 120-volt operation that reduce installation friction in multifamily housing, though current price points still limit scale. Collectively, these moves reinforce a market where design, connectivity, and efficiency gains drive purchasing decisions as much as traditional performance metrics.

Residential Built-in Kitchen Appliances Industry Leaders

BSH Home Appliances Group

Electrolux Group (incl. AEG)

Whirlpool Corporation

Haier Smart Home

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: LG Electronics unveiled its complete LG Built-in kitchen suite at EuroCucina 2026 in Milan, expanding beyond cooking appliances to include refrigeration and dishwashing. The suite features a Wide Combi Refrigerator with AI Inverter Compressor for A-grade energy efficiency, a Camera Oven with AI Gourmet food identification, a Hood Integrated Induction Cooktop (189mm ultra-slim body, iF Design Award 2026), and a dishwasher completing wash/dry in one hour via QuadWash Pro and Dynamic Heat Dry+. The launch addresses Europe's rising energy costs and space constraints through AI-driven efficiency.

- April 2026: Samsung expanded its kitchen portfolio with new Bespoke AI built-in appliances unveiled on April 21, 2026, including a Bespoke AI Single 1Door Fridge & Freezer with handle-less flat-front and Auto Open Door, a Bespoke AI Dishwasher achieving A-20% energy efficiency (20% better than minimum A-grade) via Active Fan Dry, and an Extractor Induction Hob combining cooking and ventilation in one appliance with A+ energy efficiency (EU Regulation No. 65/1024) and Boost mode suction up to 720 m³/h. The line emphasizes seamless integration and intelligent performance for modern kitchens.

- April 2026: Samsung's 2026 Bespoke AI Kitchen Appliances became available in the United States, featuring Bespoke AI 3-Door French Door Refrigerators (counter-depth 24 cu. ft. and full-depth 29 cu. ft. models starting at USD 2,799) with Zero Clearance Fit for flush installation, AutoView Glass Door (launching later in 2026) that illuminates upon approach to reduce cold-air loss, and Bespoke Smart Slide-in Ranges (starting at USD 1,349) with No Preheat Air Fry Max, True Convection, and Air Sous Vide. Products are available on Samsung.com and select retailers.

- April 2026: BSH Home Appliances Group showcased its multi-brand portfolio at EuroCucina 2026 in Milan (April 21–26), with Bosch presenting a built-in vacuum/mop robot and high-capacity cooling appliances with doors supporting up to 70 kg, Siemens highlighting a matt black product range and an intelligent oven with AI camera celebrating 100 years of Siemens ovens. Neff is showcasing Slide & Hide ovens and venting cooktops. Gaggenau exhibited off-site at Villa Necchi during FuoriSalone. BSH generated EUR 15 billion turnover in 2025 with over 56,000 employees.

Global Residential Built-in Kitchen Appliances Market Report Scope

Residential built-in kitchen appliances are designed to seamlessly integrate into kitchen cabinetry, offering a combination of functionality, space efficiency, and modern aesthetics for household use. The residential built-in kitchen appliances market is segmented by product type, installation/integration, project type, distribution channel, and geography. By product type, the market is segmented into built-in ovens, built-in hobs/cooktops, cooker hoods/chimneys, built-in dishwashers, built-in microwaves, built-in refrigerators, built-in coffee machines, wine coolers/beverage centers, and others (warming drawers, etc.). By installation/integration, the market is segmented into fully integrated/panel-ready, semi-integrated, and standard built-in (visible fronts). By project type, the market is segmented into new build and remodeling/retrofit. By distribution channel, the market is segmented into B2C/retail channels (multi-brand stores, exclusive brand stores, online, and other distribution channels) and B2B/contract sales (kitchen studios, developers, and architects). By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The report provides the market size in USD for all the above-mentioned segments.

| Built-in Ovens |

| Built-in Hobs /Cooktops |

| Cooker Hoods /Chimneys |

| Built-in Dishwashers |

| Built-in Microwaves |

| Built-in Refrigerators |

| Built-in Coffee machines |

| Wine Coolers / Beverage centers |

| Others (Warming drawers etc) |

| Fully Integrated / Panel-ready |

| Semi-integrated |

| Standard Built-in (Visible Fronts) |

| New Build |

| Remodeling / Retrofit |

| B2C/Retail Channels | Multi-Brand Stores |

| Exclusive Brand Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contract Sales (Kitchen Studios, Developers, Architects) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Built-in Ovens | |

| Built-in Hobs /Cooktops | ||

| Cooker Hoods /Chimneys | ||

| Built-in Dishwashers | ||

| Built-in Microwaves | ||

| Built-in Refrigerators | ||

| Built-in Coffee machines | ||

| Wine Coolers / Beverage centers | ||

| Others (Warming drawers etc) | ||

| By Installation / Integration | Fully Integrated / Panel-ready | |

| Semi-integrated | ||

| Standard Built-in (Visible Fronts) | ||

| By Project Type | New Build | |

| Remodeling / Retrofit | ||

| By Distribution Channel | B2C/Retail Channels | Multi-Brand Stores |

| Exclusive Brand Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contract Sales (Kitchen Studios, Developers, Architects) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected CAGR for the Residential built-in kitchen appliances market through 2031?

The residential built-in kitchen appliances market is projected to grow at a 7.08% CAGR from 2026 to 2031.

How large will the Residential built-in kitchen appliances market be by 2031?

It is forecast to reach USD 39.86 billion by 2031, up from USD 28.31 billion in 2026.

Which regions lead and grow fastest in Residential built-in kitchen appliances?

Europe led with a 44.64% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 8.26% CAGR to 2031.

Which product categories are most important in Residential built-in kitchen appliances?

Built-in refrigerators held the largest share in 2025 of 28.82%, and built-in hobs or cooktops are projected to grow fastest as induction adoption rises at 7.33%.

What channels are gaining momentum for Residential built-in kitchen appliances?

Exclusive brand stores remain crucial for high-touch sales, while online channels are projected to grow at the fastest 7.58% CAGR through 2031.

Which regulations most influence Residential built-in kitchen appliances?

EU A–G label rescaling and the United States. Title 24 provisions for electric-ready kitchens are shaping product designs and installation planning.

Page last updated on: