Resealable Cans Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 3.31 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

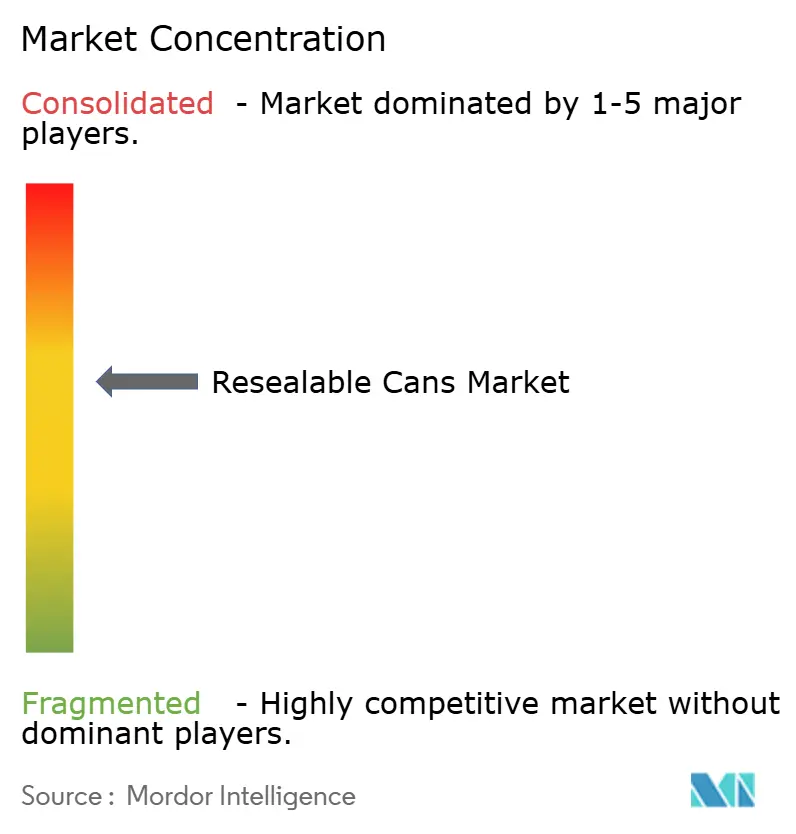

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resealable Cans Market Analysis by Mordor Intelligence

The resealable cans market size is projected to expand from USD 2.32 billion in 2025 and USD 2.57 billion in 2026 to USD 3.31 billion by 2031, registering a CAGR of 5.23% between 2026 and 2031. Growth reflects a lasting shift in food and beverage packaging, as resealability is moving from a premium feature to a more widely expected packaging function across categories where portability and product retention matter. The resealable cans market is also benefiting from stronger on-the-go consumption, wider consumer preference for recyclable metal packaging, and continued improvement in closure systems that are reducing the cost gap with standard easy-open ends. Large can makers are competing through scale, supply agreements, and manufacturing reach, while closure specialists are pushing faster innovation cycles through proprietary mechanism design and licensing. The expansion of deposit return schemes in Europe is improving the economics of can-to-can recycling, which supports the long-term case for premium metal packaging and gives the resealable cans market a stronger sustainability position. At the same time, aluminum cost pressure and stricter packaging compliance rules are still limiting faster adoption in price-sensitive applications.

Key Report Takeaways

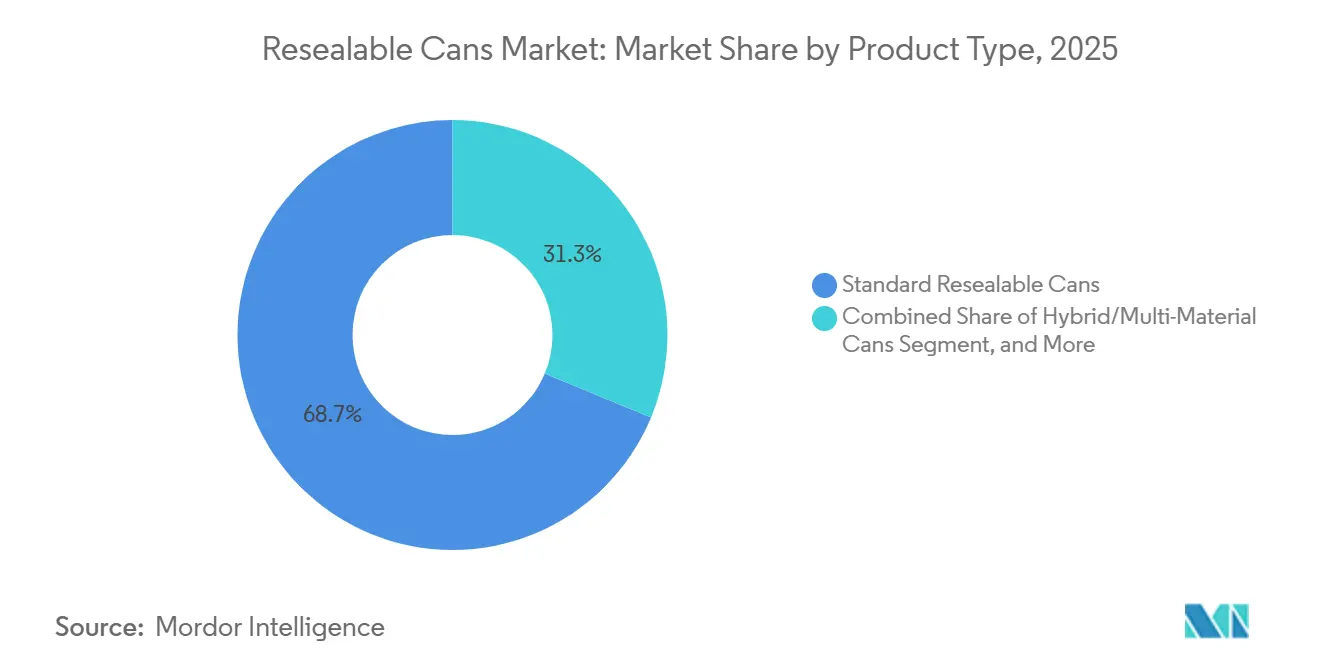

- By product type, standard resealable cans held 68.73% of the resealable cans market share in 2025.

- By material type, the resealable cans market for aluminum is projected to grow at a 6.08% CAGR through 2031.

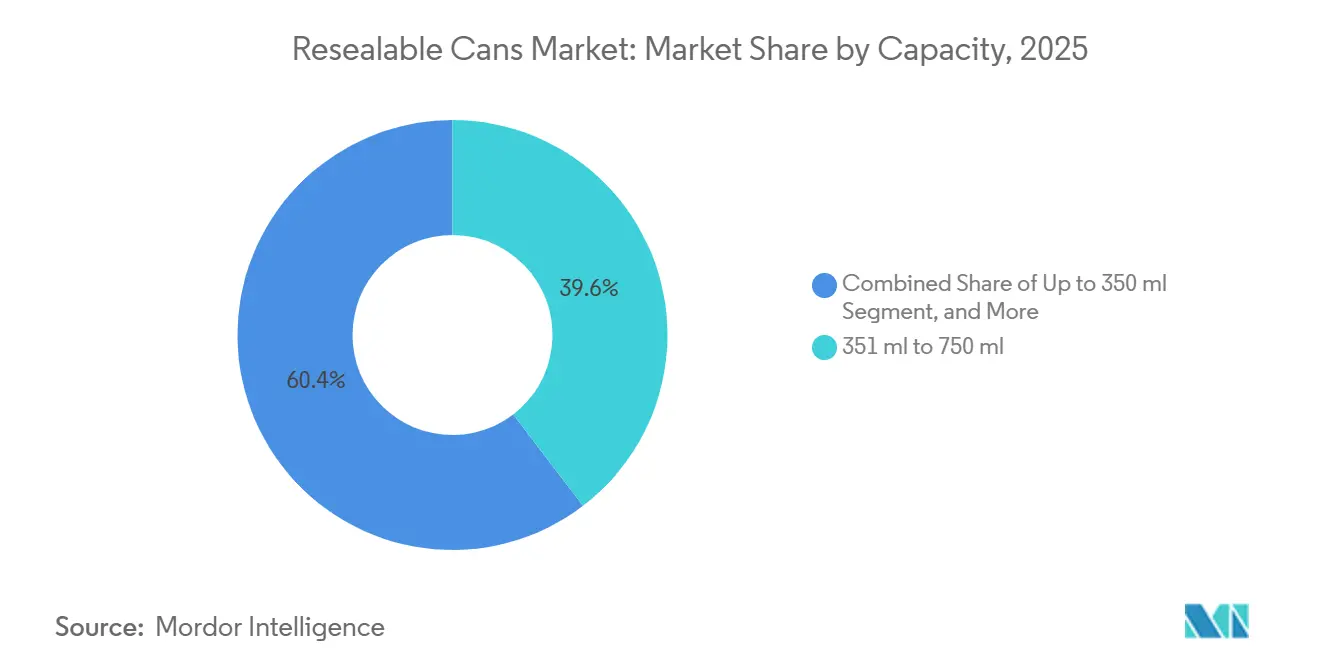

- By capacity, the 351 ml to 750 ml segment captured 39.61% of the resealable cans market share in 2025.

- By end-user industry, the resealable cans market for food and beverage is projected to expand at a 6.34% CAGR through 2031.

- By geography, North America accounted for 38.53% of the resealable cans market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Resealable Cans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for On-the-Go Beverage Packaging | +1.2% | Global, concentrated gains in North America, Asia-Pacific, and Western Europe | Short term (≤ 2 years) |

| Shift Toward Recyclable Metal Packaging | +1.0% | Global, policy-driven acceleration in the EU, the UK, and Asia-Pacific | Medium term (2-4 years) |

| Premiumization of Ready-to-Drink Beverages | +0.9% | North America, Western Europe, Japan, and South Korea | Medium term (2-4 years) |

| Innovation in User-Friendly Closure Systems | +0.7% | Global, early commercial gains in Germany, Austria, and the United States | Medium term (2-4 years) |

| Deposit Return Scheme Expansion Improving Can-to-Can Economics | +0.6% | EU core, the UK, Eastern Europe, and spillover to South America | Medium term (2-4 years) |

| Hygiene and Anti-Spiking Use Cases Favoring Covered Drinking Surfaces | +0.4% | The UK, Western Europe, Australia, and New Zealand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for On-The-Go Beverage Packaging

Portable consumption continues to support the resealable cans market because consumers increasingly use beverage packs outside the home and across multiple occasions. This matters most in 330 ml to 500 ml products, where not every drink is consumed at once, and spill resistance adds direct functional value. Energy drinks, sparkling water, and fitness beverages benefit more from resealability because product loss after opening can change how and where consumers use them. Brands also started using resealable packaging as a visible retail differentiator, as shown by Re: Lid USA's April 2026 launch at Gelson's Markets in Southern California. As this behavior spreads across convenience and immediate-consumption channels, the resealable cans market is likely to secure broader placement in beverage portfolios.

Shift Toward Recyclable Metal Packaging

The resealable cans market is gaining support from aluminum beverage packaging's stronger environmental position. Aluminum beverage cans in the United States had a closed-loop circularity rate of 96.7% and an average recycled content of 71% in 2024, well above comparable levels for glass and PET. In Europe, the aluminum beverage can recycling rate reached 76.3% in 2023, reinforcing the appeal of metal packaging in regulatory environments that are increasingly focused on recovery and recycled content. The resealable cans market benefits even more when closure systems preserve mono-material construction, because that lowers packaging complexity and improves recycling alignment. Sonoco positioned its CapOnCan system in exactly that way at Interpack 2026, highlighting mono-material steel construction and lower EPR fee exposure for food and pet food applications.

Premiumization of Ready-To-Drink Beverages

Premium product positioning is driving the resealable cans market, as higher-value beverage brands are more willing to pay for visible packaging differentiation. This is especially relevant in ready-to-drink categories where convenience, presentation, and repeat use all shape consumer perception. Resealable formats also fit premium retail channels because they offer a cleaner drinking surface and better spill control in travel, event, and convenience-led settings. The Ball, Red Bull, and Rauch partnership on a USD 1.5 billion manufacturing and distribution facility in North Carolina shows how branded beverage players are committing long-term capital to differentiated can supply chains. As premium drink launches continue to favor packaging that stands out on the shelf and performs better after opening, the resealable cans market is likely to attract a larger share of innovation-led volumes.

Innovation In User-Friendly Closure Systems

Closure development accelerated across the resealable cans market in 2025 and 2026, with suppliers advancing sliding tabs, snap closures, rivet-spinner systems, and click-to-seal formats. XOLUTION stated that its XO 2.5 closure reduces plastic content to 2.9 grams per closure and supports fill temperatures up to 85°C with nitrogen, which broadens use across pasteurized beverages. Top Cap Holding also expanded its portfolio through an exclusive September 2025 licensing agreement for SpinClip, adding another mechanism to a field that is increasingly shaped by intellectual property and performance specialization. XOLUTION's new Dachau center, announced in April 2026 with a planned capacity of up to 900 million XO lids per year, shows how the resealable cans market is moving from development-stage closure concepts toward industrial-scale production.[1]XOLUTION Germany GmbH, “Xolution Strengthens Position with New Production Centre,” Packaging Journal, packaging-journal.de As those systems become easier to run at scale, the resealable cans market should see wider use beyond early-adopter beverage programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Closure and Conversion Costs Versus Standard Ends | -1.0% | Global, most acute in Southeast Asia, Africa, and price-sensitive South American markets | Short term (≤ 2 years) |

| Competition From Standard Cans and PET Bottles | -0.8% | Global, most concentrated in North America and Europe | Medium term (2-4 years) |

| Compliance Complexity for PFAS and Bisphenol-Free Food-Contact Systems | -0.5% | EU, United States, India, and emerging Asia-Pacific | Medium term (2-4 years) |

| Aluminum Tariffs and Premium Volatility | -0.4% | North America, with indirect exposure across tariff-linked supply chains globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Closure and Conversion Costs Versus Standard Ends

The largest structural brake on the resealable cans market remains the extra cost of the closure compared with a standard stay-on-tab end. Resealable systems require more parts, tighter manufacturing tolerances, and, in some cases, changes in filling-line handling that many beverage producers have not yet installed. That burden is more difficult for smaller and mid-sized brands because they cannot spread equipment and conversion costs across very high production runs. The market is therefore more accessible to premium beverage programs than to mass-market products, where retailers and brand owners are highly sensitive to packaging cost. XOLUTION's move toward a capacity of up to 900 million lids per year shows why scale is central to cost compression in the resealable cans market.

Competition from Standard Cans and PET Bottles

The resealable cans market still competes with standard cans and PET bottles that benefit from a large installed manufacturing base and long-established buyer familiarity. Standard metal cans remain difficult to displace in mainstream beverage applications because they are efficient, widely available, and fully integrated into high-speed filling networks. PET also offers resealability at a lower absolute package cost, which creates a practical ceiling on adoption for specialty can ends in value-driven categories. At the same time, metal packaging suppliers are trying to displace incumbent glass and multi-part systems where resealability and mono-material construction can create a stronger total proposition. Sonoco's CapOnCan was introduced as a direct alternative to glass-jar-plus-metal-closure combinations in food and pet food, showing that the resealable cans market is advancing, where it can clearly improve convenience and material simplicity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standard Formats Anchor Volume, Threaded Variants Accelerate

Standard resealable cans accounted for 68.73% of the resealable cans market in 2025, leaving them well ahead of other product formats. Their lead stemmed from compatibility with the installed base of high-speed filling and seaming lines, reducing the need for additional capital spending by beverage producers. That infrastructure fit gives standard formats a durable advantage in categories where throughput and operational simplicity still carry more weight than closure sophistication. The resealable cans market, therefore, continues to rely on standard configurations as its main volume base, even while newer designs gain attention in premium niches. This installed-line advantage should keep standard formats relevant through the forecast period.

Threaded and screw-top cans are projected to expand at a 5.86% CAGR through 2031, supported by their ability to retain pressure above 90 psi for longer periods in high-carbonation use cases. That performance makes them attractive for sparkling beverages, craft beer, and selected energy drink applications where carbonation retention after reopening is essential. Slide-tab and snap-fit systems have advanced, but threaded formats still offer a stronger solution in demanding pressure environments. Hybrid/multi-material cans remain a smaller part of the resealable cans industry, with more selective relevance in personal care, pharmaceuticals, and other applications where barrier properties justify added cost. As closure economics improve, the resealable cans market is likely to see threaded variants take a larger share of premium launch activity.

By Material Type: Aluminum's Circular Position Supports Leadership

Aluminum held 41.58% of the resealable cans market share in 2025, and the aluminum resealable cans market is projected to expand at a 6.08% CAGR through 2031. Aluminum leads because it combines low weight, corrosion resistance, and strong barrier performance with an established recycling narrative that brand owners can communicate clearly to retailers and consumers. The resealable cans market is also supported by the material's suitability for carbonated beverage applications, where structural reliability is critical. In the United States, aluminum beverage cans moved from the recycling bin to a newly formed can in less than 60 days on average in 2025, reinforcing the speed and visibility of the closed-loop value proposition. This combination of functionality and circularity keeps aluminum at the center of the resealable cans market.

Closed-loop recycling also improves the material's long-term appeal because can-to-can systems can cut carbon footprint by more than 90% compared with primary aluminum production. The International Aluminum Institute also stated that advanced closed-loop processes can recover up to 18% more metal and lower energy use by 15% compared with mixed-alloy remelting. Steel and tinplate remain important in three-piece can formats for dry goods, confectionery, nutritional powders, and industrial chemicals, where pressure demands are lower and cost competitiveness matters more. Plastic resealable cans keep a role in low-pressure personal care and cosmetic uses, but the resealable cans industry remains more strongly aligned with metal in applications where recycling performance is part of the product story.

By Capacity: Mid-Range Volumes Hold Share, Compact Sizes Gain Momentum

The 351 ml to 750 ml segment accounted for 39.61% of the resealable cans market in 2025, reflecting the concentration of global beverage demand in standard 330 ml, 355 ml, and 500 ml formats. That range benefits from the broadest installed filling infrastructure and the most extensive brand deployment across regions. It also aligns with mainstream ready-to-drink buying habits, where single-serve packs dominate shelf space and drive high repeat turnover. For that reason, the resealable cans market still relies on mid-range capacities as its base volume category. The installed network around these sizes should keep them central to production planning during the forecast period.

The up to 350 ml segment is projected to grow at a 6.17% CAGR from 2026 to 2031, making it the fastest-rising capacity tier in the resealable cans market. Compact formats suit premium single-serve energy drinks, sparkling water, and ready-to-drink cocktails that are sold through convenience and on-premise channels. They also align well with sports, outdoor, and festival consumption occasions, where portability and anti-spillage performance matter more than absolute volume. XOLUTION stated that its closure architecture can support sizes from 150 ml to 750 ml, indicating that suppliers are designing new systems with broad size flexibility rather than a narrow format focus. The above 750 ml segment remains smaller and serves more specialized household and food service use cases where portion control matters more than mobility.

By End-User Industry: Beverages Led Demand, Adjacent Uses Expand the Base

Food and beverage accounted for 36.29% of the resealable cans market share in 2025, and this end-use segment also remains the fastest-growing, with a projected 6.34% CAGR through 2031. The segment leads because resealability directly supports multi-occasion use, reduced spillage, and better product retention after opening. Ready-to-drink beverages, energy drinks, and ready-to-eat liquid foods are the strongest demand drivers within this category. In practical terms, the resealable cans market advances fastest when the package itself improves convenience during consumption rather than only protecting the product in storage. That is why beverage-led applications continue to define the commercial center of the resealable cans market.

Other end uses are broadening the addressable base, even though they are smaller than the food and beverage. Personal care and cosmetics use resealable formats in aerosols and dispensing products where contamination control and repeated application matter. Sonoco's CapOnCan, introduced at Interpack 2026, shows how family-sized food and pet food products are becoming a meaningful adjacent opportunity as resealable metal cans start replacing incumbent multi-material pack formats.[2]Sonoco coverage, “Sonoco Unveils CapOnCan at Interpack 2026,” CanTech International, cantechonline.com Chemicals, paints, and lubricants rely on resealability more for storage integrity and transportation than for consumer convenience. Pharmaceutical applications remain selective and are shaped by strict packaging and hygiene requirements within the resealable cans industry.

Geography Analysis

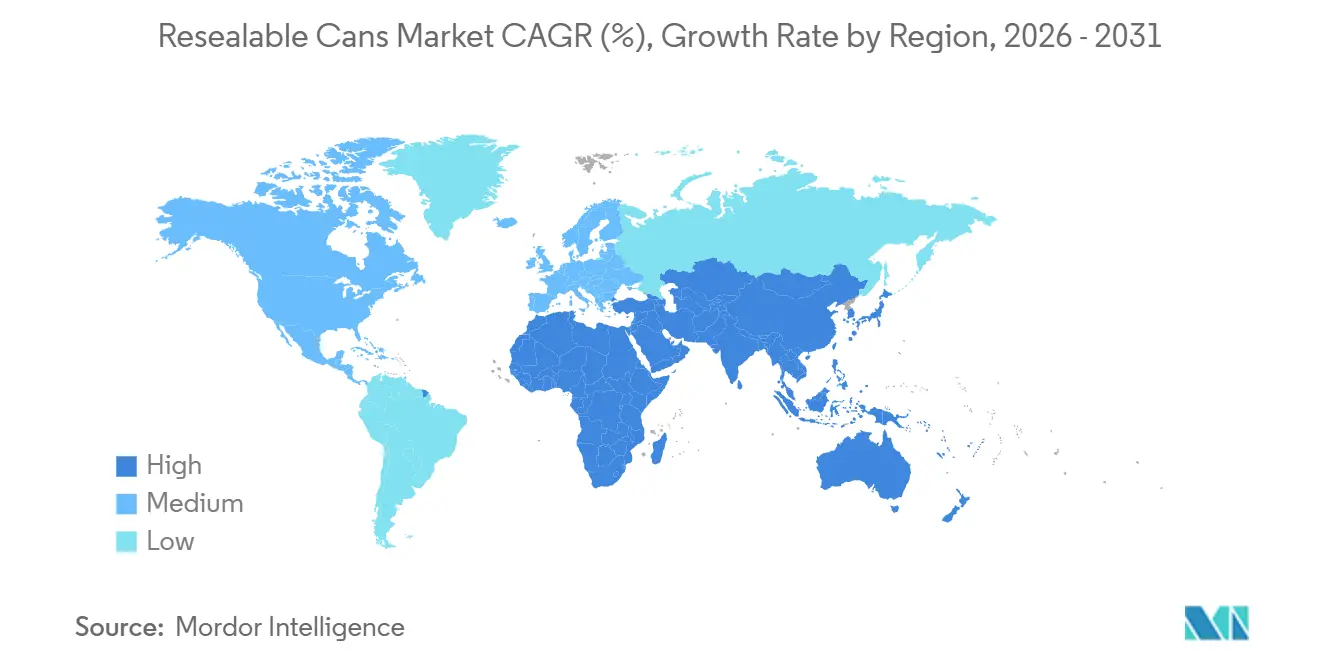

North America accounted for 38.53% of the resealable cans market in 2025, making it the largest regional market. The region benefits from strong penetration of ready-to-drink beverages, a dense distribution infrastructure, and an established aluminum can manufacturing base. The resealable cans market in the United States is also supported by ongoing brand investment in packaging differentiation, especially in beverage categories where shelf visibility and portability matter. Crown Holdings stated that its expanded Ponta Grossa plant in Brazil is expected to begin commercial production in Q3 2026, with an annual capacity of 3.6 billion cans, supporting broader regional supply across the Americas.[3]Crown Holdings, Inc., “Crown Holdings, Inc. to Establish State-of-the-Art Beverage Can Facility in Northern India,” PR Newswire, prnewswire.com North America still faces cost pressure from Section 232 aluminum tariffs, which maintained a 50% rate on aluminum articles through May 2026 and pushed converter uncertainty higher as the Midwest Premium moved above USD 1 per pound in late January 2026.

Asia-Pacific is projected to expand at a 6.12% CAGR through 2031, making it the fastest-growing region in the resealable cans market. Rising disposable income, rapid urbanization, and expanding ready-to-drink categories are driving that pace across major countries. Ball invested USD 60 million in Sri City in 2025, following a USD 55 million investment in Taloja in 2024, citing strong growth in India's beverage can sector and stronger demand for ready-to-drink beverages and dairy products. Crown Holdings also announced a greenfield two-line facility in Northern India in April 2026, with expected output of 2.2 billion cans annually from the second half of 2027. CANPACK reported 2025 results that pointed to India as a meaningful incremental contributor to volume growth, which fits the broader regional outlook for the resealable cans market.

Europe held a significant position in the resealable cans market in 2025, with Germany, the United Kingdom, France, and Italy serving as the main consumption centers. The region is also gaining support from deposit return systems, because those programs strengthen can recovery economics and improve the long-term case for premium metal packaging. Portugal launched the Volta DRS on April 10, 2026, covering aluminum and steel cans below 3 liters with a USD 0.10 deposit per unit. Spain's statutory deadline for a beverage container deposit return system is November 2026, and the UK's confirmed scheme is scheduled for October 2027 with a flat 20 pence deposit.

Competitive Landscape

The resealable cans market is moderately consolidated. Crown Holdings, Ball Corporation, Ardagh Metal Packaging, CANPACK, and Toyo Seikan Group compete through manufacturing scale, regional footprints, and long-term contracts with large beverage customers. This part of the resealable cans market is shaped by cost pass-through ability and operating resilience rather than by closure novelty alone. Ardagh Metal Packaging reported Q1 2026 sales of USD 1.504 billion and adjusted EBITDA growth of 15%, showing how scale and contractual protections can soften raw material volatility in a difficult cost environment.[4]Ardagh Metal Packaging S.A., “Ardagh Metal Packaging S.A. First Quarter 2026 Results,” Ardagh Metal Packaging, ardaghmetalpackaging.com Ball's December 2025 agreement to acquire a majority stake in Benepack's beverage can businesses in Belgium and Hungary further showed how leading players are using acquisitions to lock in regional supply and contracted volume in the resealable cans market.

The specialist tier competes more on mechanism design, licensing, and intellectual property than on global production scale. XOLUTION, Top Cap Holding, can2close, and similar developers are important because they shape the technical performance ceiling of the resealable cans market through differentiated closure systems. XOLUTION's investment in a new Dachau development and manufacturing center, with planned output of up to 900 million XO lids per year, shows how specialist suppliers are moving from selective programs to industrial volume. Top Cap Holding's September 2025 SpinClip licensing deal added to this competitive pattern, because it expanded a portfolio strategy built on multiple closure concepts rather than a single mechanism.

Competition is therefore moving in two directions at the same time in the resealable cans market. Large manufacturers are expanding capacity and geographic reach, while specialists are trying to protect technical niches through patents, licensing, and first-mover positioning. Sonoco's CapOnCan launch at Interpack 2026 showed that mid-sized packaging groups are also entering the field with new hardware aimed at replacing glass-plus-closure systems in food and pet food. White-space opportunities remain in pharmaceutical tamper-evident packs, non-beverage liquid personal care, and mono-material formats designed for markets where deposit systems and packaging compliance rules are becoming more influential.

Resealable Cans Industry Leaders

Crown Holdings, Inc.

Ball Corporation

CANPACK S.A.

Toyo Seikan Group Holdings, Ltd.

Silgan Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Crown Holdings announced plans for a greenfield 2-line beverage can manufacturing facility in Northern India, targeting commercial operations in the second half of 2027 with annual capacity of approximately 2.2 billion cans.

- May 2026: Sonoco unveiled its CapOnCan resealable metal can at Interpack 2026 in Düsseldorf, the first hermetically sealed, airtight resealable food can in mono-material steel construction. The design targets the replacement of glass jars with metal closures in family-sized food and pet food applications, reduces EPR fees in regulated markets, and supports refrigerated post-open storage.

- April 2026: XOLUTION Germany GmbH held the groundbreaking ceremony for its new production and development center in Dachau, consolidating R&D, administration, and manufacturing from Bremen and the Czech Republic. At full capacity, the facility is designed to produce up to 900 million XO lids per year, a production scale that signals the transition of resealable closure supply from prototype to industrial volume.

- April 2026: Ardagh Metal Packaging reported Q1 2026 sales of USD 1.51 billion, adjusted EBITDA growth of 15%, and reaffirmed full-year 2026 guidance of USD 750-775 million in adjusted EBITDA. European volume growth and a favorable currency tailwind drove outperformance against market expectations.

Global Resealable Cans Market Report Scope

The scope of the report covers the analysis of the resealable cans market, including cans equipped with mechanisms that allow resealing after opening. These cans are primarily used in the beverage and food industries to enhance product freshness and convenience. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the current market dynamics and future projections.

The Resealable Cans Market Report is Segmented by Product Type (Standard Resealable Cans, Threaded/Screw-Top Cans, and Hybrid/Multi-Material Cans), Material Type (Aluminum, Steel and Tinplate, and Plastic), Capacity (Up to 350 ml, 351–750 ml, and Above 750 ml), End-User Industry (Food and Beverage, Personal Care and Cosmetics, Chemicals, Pharmaceuticals, Paints and Lubricants, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Resealable Cans |

| Threaded / Screw-Top Cans |

| Hybrid / Multi-Material Cans |

| Aluminum |

| Steel and Tinplate |

| Plastic |

| Up to 350 ml |

| 351 ml to 750 ml |

| Above 750 ml |

| Food and Beverage |

| Personal Care and Cosmetics |

| Chemicals |

| Pharmaceuticals |

| Paints and Lubricants |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Standard Resealable Cans | ||

| Threaded / Screw-Top Cans | |||

| Hybrid / Multi-Material Cans | |||

| By Material Type | Aluminum | ||

| Steel and Tinplate | |||

| Plastic | |||

| By Capacity | Up to 350 ml | ||

| 351 ml to 750 ml | |||

| Above 750 ml | |||

| By End-User Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Chemicals | |||

| Pharmaceuticals | |||

| Paints and Lubricants | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the resealable cans market in 2026 and where is it headed by 2031?

The resealable cans market is valued at USD 2.57 billion in 2026 and is projected to reach USD 3.31 billion by 2031 at a 5.23% CAGR.

Which product format leads demand in this space?

Standard resealable cans lead demand, with 68.73% share in 2025, because they work with existing high-speed filling and seaming infrastructure.

Which material is gaining the most traction?

Aluminum is the leading material, with a 41.58% share in 2025, and is also projected to grow at a 6.08% CAGR through 2031.

Which end-use segment is driving the most adoption?

Food and beverage is the largest end-use segment with 36.29% share in 2025 and the fastest growth at a 6.34% CAGR through 2031.

What is the main barrier to wider adoption of resealable cans?

The biggest constraint is the higher closure and conversion cost versus standard ends, especially for smaller brands and price-sensitive beverage categories.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, with a projected 6.12% CAGR through 2031, supported by rising ready-to-drink demand and new can capacity in India and other regional markets.

Page last updated on: