ReRAM Crossbar In-Memory Computing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

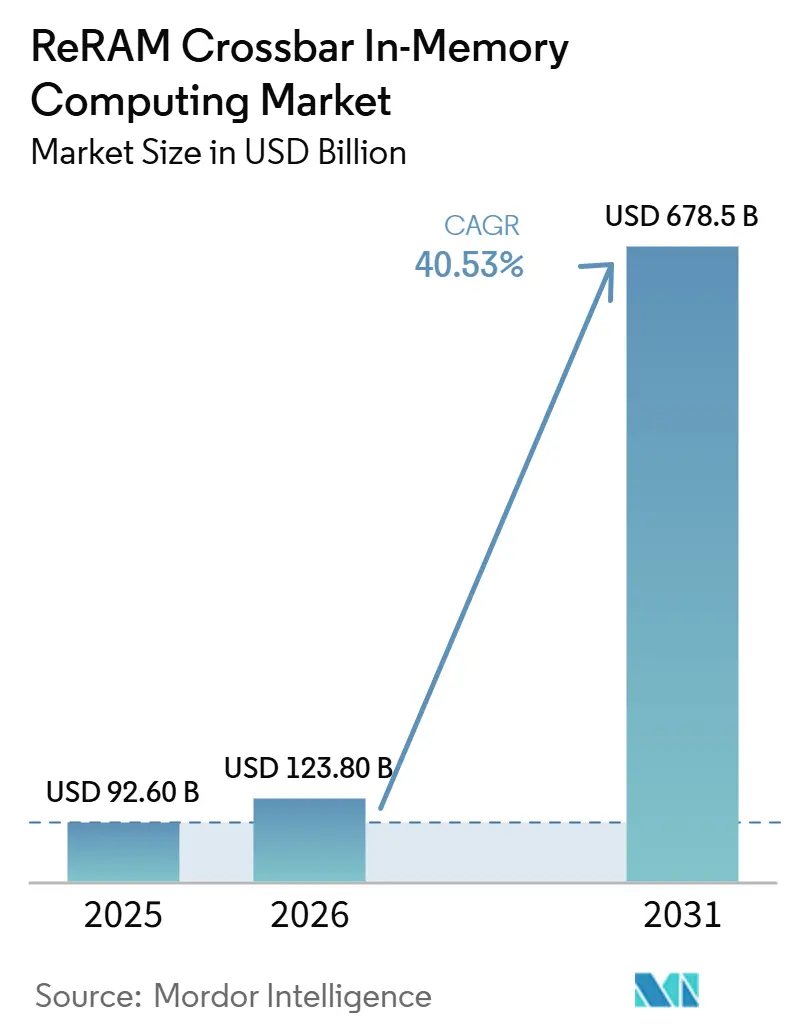

| Market Size (2026) | USD 123.80 Billion |

| Market Size (2031) | USD 678.5 Billion |

| Growth Rate (2026 - 2031) | 40.53% CAGR |

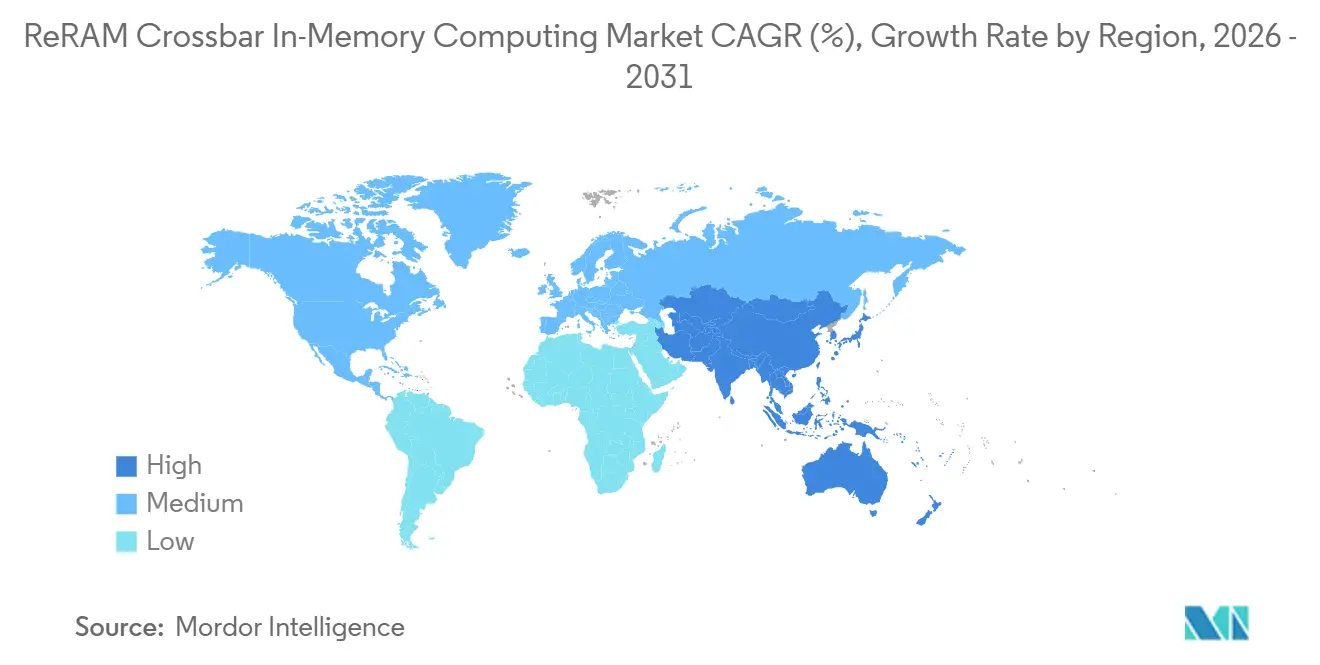

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

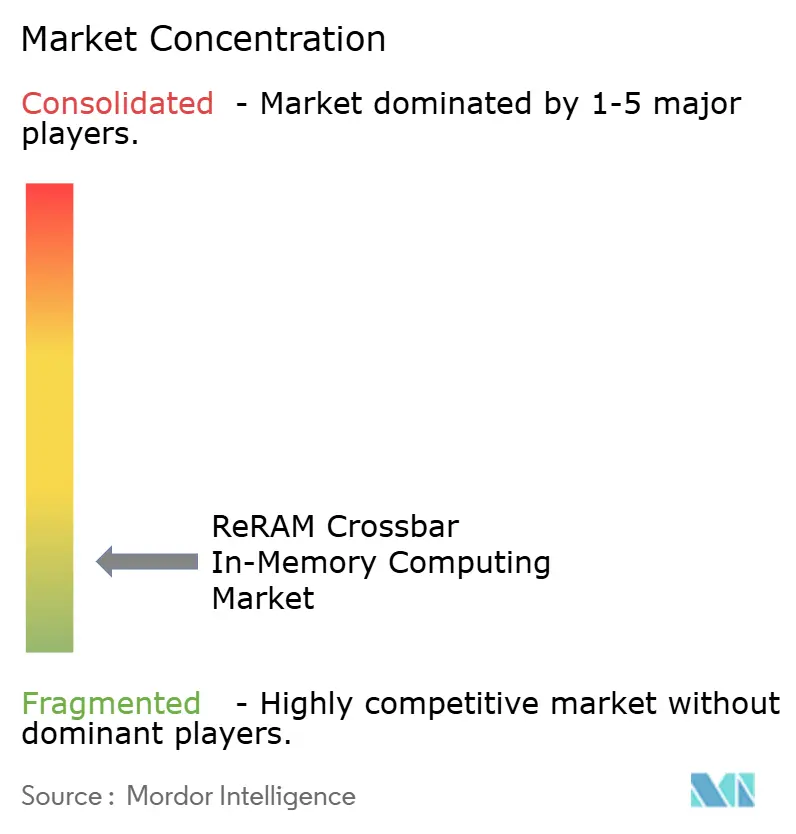

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ReRAM Crossbar In-Memory Computing Market Analysis by Mordor Intelligence

The ReRAM crossbar in-memory computing market size is projected to expand from USD 92.60 million in 2025 and USD 123.80 million in 2026 to USD 678.50 million by 2031, registering a CAGR of 40.70% between 2026 to 2031. The rise in data center electricity use during 2025, along with the expectation of much higher power demand by 2030, has made lower-energy memory architectures a more urgent priority for hyperscalers and edge device makers. The ReRAM crossbar in-memory computing market is benefiting from its ability to execute vector-matrix operations inside memory, which reduces data movement and directly addresses the long-standing processor-to-memory bottleneck. Demand is also strengthening as edge AI spreads across phones, cameras, industrial sensors, and autonomous systems, where power limits, latency, and always-on operation matter as much as raw throughput. Competitive activity remains split between large manufacturers that control process qualification and specialist licensors that monetize device and array expertise through licensing and milestone payments. Commercialization still faces limits from manufacturing maturity at advanced nodes, while device drift, variability, and endurance qualification continue to slow adoption in high-reliability deployments.

Key Report Takeaways

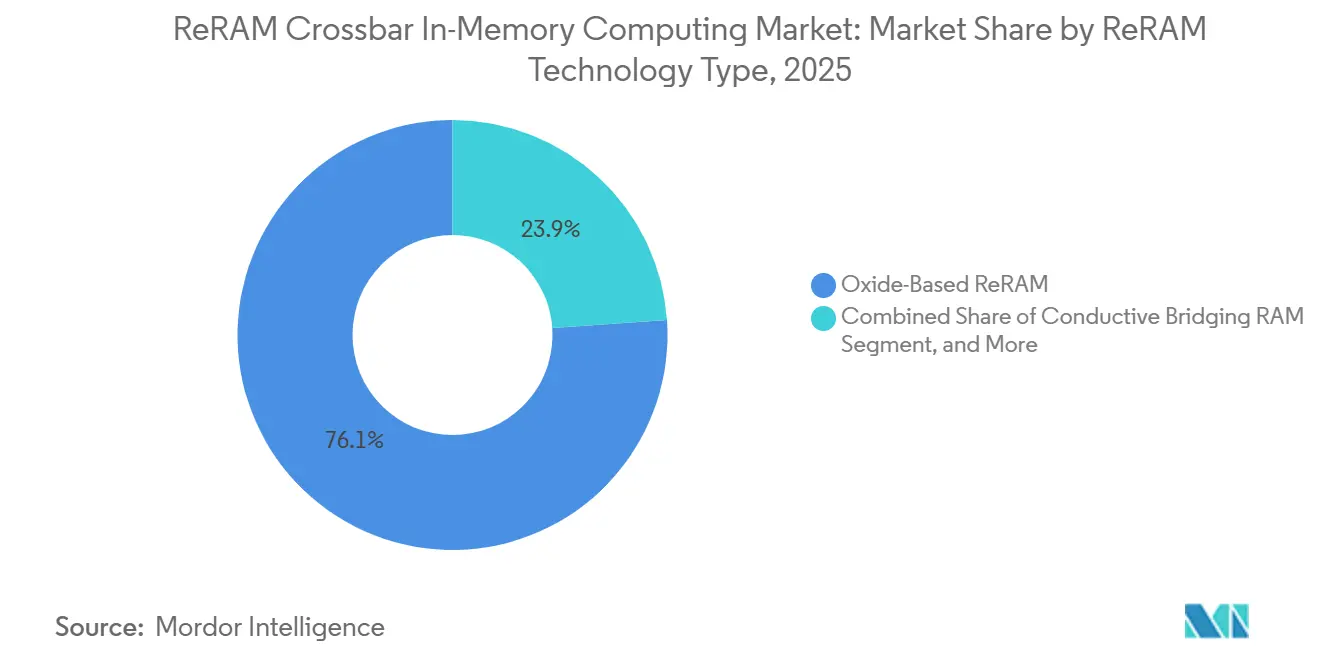

- By ReRAM technology type, oxide-based ReRAM led with 84.12% revenue share of the ReRAM crossbar in-memory computing market in 2025, while conductive bridging RAM is projected to expand at a 41.29% CAGR through 2031.

- By integration, embedded held 66.83% share of the ReRAM crossbar in-memory computing market in 2025 and is projected to expand at a 41.08% CAGR through 2031.

- By computing architecture, analog in-memory computing accounted for 64.31% share in 2025, while hybrid computing is projected to expand at a 41.26% CAGR through 2031.

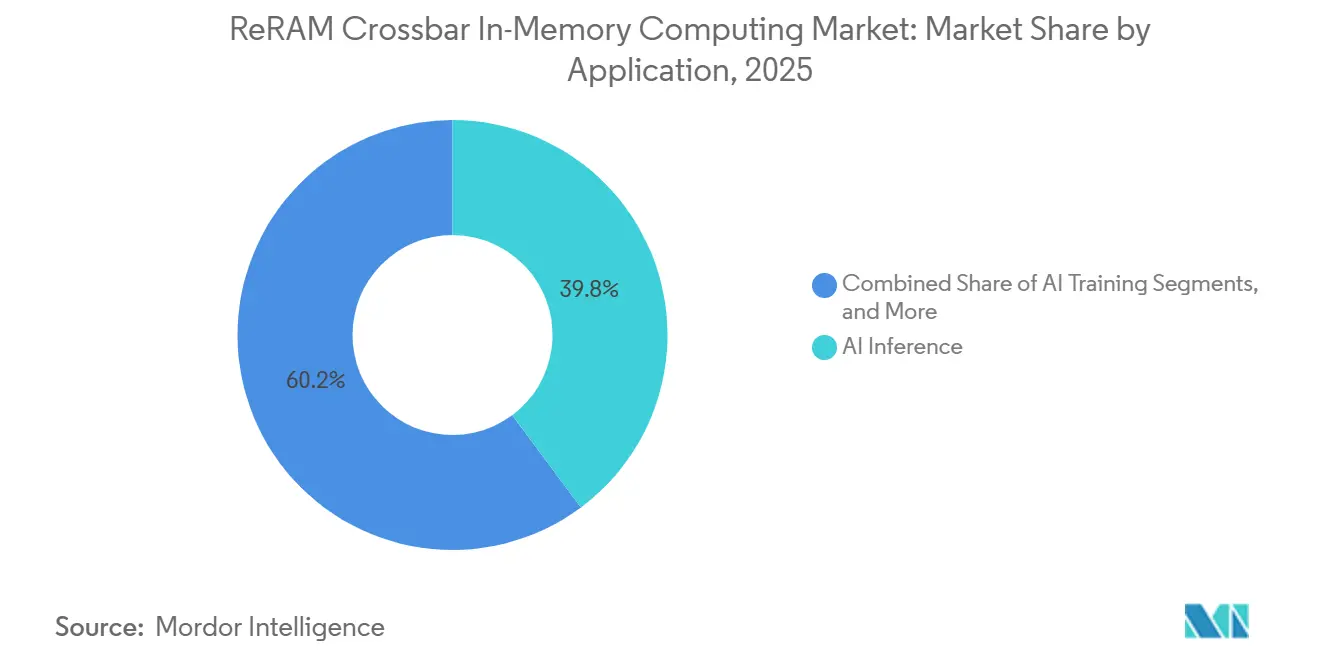

- By application, AI inference held 52.96% share in 2025, while AI training is projected to expand at a 41.66% CAGR through 2031.

- By end user, data centers and HPC accounted for 57.77% share in 2025, while automotive is projected to expand at a 42.24% CAGR through 2031.

- By geography, North America held 49.07% of the ReRAM crossbar in-memory computing market share in 2025, while Asia-Pacific is projected to expand at a 41.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ReRAM Crossbar In-Memory Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Edge AI and On-Device Inference Workloads | +8.5% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Growing Need to Reduce Data-Movement Energy in Compute Systems | +7.2% | Global | Short term (≤ 2 years) |

| Expansion of Neuromorphic and In-Memory Computing Prototypes | +6.8% | Asia-Pacific and North America, spillover to Europe | Medium term (2-4 years) |

| Scaling Pressure From Advanced Driver Assistance and Industrial Embedded Compute | +5.5% | Europe, Japan, North America | Medium term (2-4 years) |

| ReRAM Crossbar Adoption in Analog Matrix Multiplication for AI Accelerators | +5.1% | North America, Taiwan, China | Medium term (2-4 years) |

| Qualification Momentum in High-Reliability Embedded Memory Platforms | +4.3% | Global, early gains in Japan, South Korea, Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Edge AI And On-Device Inference Workloads

The spread of AI inference across smartphones, cameras, industrial sensors, and autonomous systems is pushing conventional memory hierarchies closer to their power and latency limits at the device edge. The ReRAM crossbar in-memory computing market is responding to that pressure because the architecture performs multiply-accumulate work inside the array and reduces repeated movement of data between memory and logic. Weebit Nano’s licensing agreement with Texas Instruments, confirmed in 2026 with working silicon across multiple foundry nodes, showed that a major embedded processing supplier now sees ReRAM as a practical embedded non-volatile memory option below 28nm.[1]Weebit Nano Ltd., “Weebit Nano's ReRAM Selected for Korean National Compute-in-Memory Program,” Weebit Nano, weebit-nano.com That step matters beyond one customer because early foundry and device qualification tends to build process knowledge that later entrants struggle to match. It also shortens the path from prototype to embedded product design, which supports faster commercial uptake in the ReRAM crossbar in-memory computing market. Power-sensitive edge devices are therefore becoming one of the clearest early demand pools for this technology.

Growing Need To Reduce Data-Movement Energy In Compute Systems

The cost of moving data through the compute stack has become a central design issue as large technology companies continue to increase spending on AI infrastructure and data centers. The International Energy Agency stated that data center electricity consumption rose 17% in 2025 and remains on a path toward much higher demand by 2030, further strengthening the case for architectures that reduce memory traffic.[2]International Energy Agency, “Data Centre Electricity Use Surged in 2025, Even With Tightening Bottlenecks Driving a Scramble for Solutions,” International Energy Agency, iea.org The ReRAM crossbar in-memory computing market benefits directly because crossbar arrays place computation where data resides instead of moving weights back and forth between memory and processors. Scientific work on memristive compute-in-memory engines has also shown that near-threshold in-memory designs can deliver strong energy efficiency while sustaining useful throughput for edge intelligence tasks. As models grow in parameter count, the penalty from memory movement increases faster, making the value of in-memory architectures stronger rather than flatter over time. That pattern supports continued interest in the ReRAM crossbar in-memory computing market from both cloud and edge system designers.

Expansion Of Neuromorphic And In-Memory Computing Prototypes

Institutional support for neuromorphic and in-memory computing has moved beyond theory and small simulation efforts into broader silicon validation work. IBM Research demonstrated a hardware implementation of an oscillatory neural network that used ReRAM crossbar arrays as coupling elements in back-end-of-line CMOS integration, exhibiting a class of behavior that standard SRAM-centered digital designs do not readily reproduce. In March 2026, Weebit Nano’s ReRAM was selected for a Republic of Korea government-funded analog compute-in-memory program targeting 200 TOPS/W and bringing together ETRI, universities, AnalogAI, and DB HiTek. That matters for the ReRAM crossbar in-memory computing market because national programs create durable demand, funding continuity, and local validation pathways that extend beyond one product cycle. It also broadens the technology base beyond a single geography, reducing dependence on a narrow set of fabs or IP owners. The result is a more credible route from prototype arrays to commercial compute products across several national ecosystems.

Scaling Pressure From Advanced Driver Assistance And Industrial Embedded Compute

Advanced driver assistance systems and industrial controllers place unusual demands on embedded memory, requiring fast response, stable retention, high endurance, and reliable operation under harsh conditions. Work presented at IEEE VLSI Technology in 2025 described a 16Mbit RRAM macro on 55nm BCD for 150°C automotive operation, with a cell density of 2.56Mbit/mm² and stable AEC-Q100 performance under high temperature conditions. Weebit Nano’s 2025 presentation also framed AEC-Q100 operation at 150°C, 10-year retention, and 100,000 endurance cycles as meaningful qualification criteria for embedded ReRAM programs intended for automotive use. Those requirements matter for the ReRAM crossbar in-memory computing market because automotive and industrial buyers do not adopt device-level novelty without long qualification evidence. Once those benchmarks are met, the same device characteristics also fit industrial automation, where deterministic operation and high-temperature tolerance are equally important. That makes automotive qualification a wider gateway for commercial expansion rather than a narrow niche event.[3]IEEE, “A Prototype 16Mbit RRAM on 55nm BCD With 56% Compact-Area Wordline Driver and Constant Write-Current Scheme for Automotive 150°C Operation,” IEEE VLSI Technology, doi.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Manufacturing Maturity at Volume Production Nodes | -3.2% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Reliability Drift, Variability, and Endurance Qualification Complexity | -2.8% | Global | Medium term (2-4 years) |

| Fragmented IP Landscape and Licensing Friction | -1.5% | North America, Europe | Medium term (2-4 years) |

| Weak Standardization Across Interfaces, Test Methods, and Qualification Criteria | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Manufacturing Maturity At Volume Production Nodes

The ReRAM crossbar in-memory computing market still faces a supply-side constraint because working silicon across several nodes does not automatically translate into stable, high-volume manufacturing. Product programs can reach tape-out and functional prototypes before the full qualification process is complete, leaving a gap between technical proof and reliable shipment scale. Weebit Nano stated in May 2026 that mass-production qualification for taped-out customer products is expected to take 12 to 18 months from tape-out, indicating how long commercialization can remain in transition even after silicon is available. That lag matters because fabless AI and embedded chip designers must secure foundry capacity that is not only available, but also fully validated for yield, retention, and endurance. When qualification remains concentrated in a small number of manufacturing paths, demand can rise faster than reliable supply. The result is a near-term bottleneck that can slow program timing in the ReRAM crossbar in-memory computing market even when buyer interest remains strong.

Reliability Drift, Variability, And Endurance Qualification Complexity

Analog ReRAM crossbar arrays face a physical challenge: stored conductance states drift over time, potentially weakening inference accuracy if compensation is not built into the design. Researchers from the University of Tokyo and Nuvoton Technology Japan showed in 2025 that multi-level cell ReRAM compute-in-memory can reach 10-year retention by combining a hybrid 1-bit and multi-level cell structure with drift-compensation circuits. That result improved the technical outlook, but it also showed that stronger retention often comes with increased circuit overhead, greater area usage, and greater design complexity. At the device level, the IEEE Transactions on Electron Devices reported in 2025 that access-transistor degradation under overdrive stress in 28nm 1T1R RRAM arrays requires careful gate-oxide engineering and voltage optimization. Those processes and circuit burdens lengthen qualification cycles for the ReRAM crossbar in-memory computing market, especially in safety-critical applications where endurance and retention need multi-lot validation. They also keep deployment slower in automotive, industrial, and other high-reliability settings than in less demanding edge use cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By ReRAM Technology Type: Oxide-Based Chemistry Anchors Revenue As Bridging RAM Scales

Oxide-based ReRAM accounted for 84.12% of revenue in 2025, making this material family the largest contributor to the ReRAM crossbar in-memory computing market at the start of the forecast period. Its lead comes from the commercial maturity of HfO₂ and TaOₓ stacks, which fit back-end-of-line CMOS integration without requiring front-end transistor changes. IBM Research’s conductive-metal-oxide and HfOₓ platform demonstrated all-in-one analog AI hardware with both on-chip training and inference, which supports the view that oxide-based devices remain the near-term commercial anchor. That demonstration achieved 96.9% analog training accuracy against a 98.3% floating-point baseline, underscoring why oxide systems still dominate practical product roadmaps. In the ReRAM crossbar in-memory computing market, that combination of process compatibility and system-level validation makes oxide-based chemistry the most dependable current path for broader rollout.

Conductive bridging RAM is projected to grow at a 41.29% CAGR through 2031, making it the fastest-expanding type despite its smaller base. Research presented at IEEE IEDM 2025 described a 3D-stackable FTJ and CBRAM hybrid memory device with more than 10⁹ endurance cycles, 3-bit storage per cell, and 10-year retention at room temperature. Those results matter because endurance and retention have been the two most persistent objections to CBRAM in crossbar compute uses. Other variants still serve narrower niches, including interface-switching approaches pursued by 4DS Memory with partners such as Infineon and imec for advanced test chips. 4DS also reported a 4.7ns write speed milestone in 2025, which shows that newer device approaches continue to push performance even if their commercial footprint is still smaller than oxide-based lines.

By Integration: Embedded Dominance Holds As Standalone Momentum Builds

Embedded integration held 66.83% share in 2025 and, based on the provided input, also carries the strongest near-term growth profile at a 41.08% CAGR through 2031. The embedded route remains central because placing ReRAM close to logic on the same die reduces off-chip traffic and supports a low-power architecture for edge inference and control tasks. Weebit Nano’s licensing and technology transfer program with Texas Instruments confirmed that major embedded processing suppliers are putting ReRAM into practical qualification and product planning flows rather than treating it as a lab feature. The same company stated in May 2026 that 2 product customers had already taped out chip designs using its module, and 1 of them had functional prototype silicon in hand. In the ReRAM crossbar in-memory computing market, those developments show that embedded deployment is no longer limited to early feasibility work.

Standalone integration is still gaining attention because model sizes and memory footprints can exceed what a single embedded die can efficiently store. Work on memory-centric and large-model acceleration architectures has pointed toward a broader role for near-memory and multi-die compute layouts that reduce bandwidth pressure. That shift creates a practical niche for standalone ReRAM tiles placed close to processor chiplets, even if embedded products remain the main commercial route today. The ReRAM crossbar in-memory computing industry therefore has 2 parallel integration paths, one serving near-term embedded control and edge inference, and another supporting larger memory-centric compute systems. As qualification broadens, the balance between these paths may depend less on raw device novelty and more on package-level economics, memory scale, and system architecture choices. Those conditions explain why embedded still leads while standalone keeps building momentum from a smaller base.

By Computing Architecture: Analog Arrays Lead As Hybrid Configurations Gain Traction

Analog in-memory computing held 64.31% share in 2025, which kept it at the center of the ReRAM crossbar in-memory computing market because crossbar vector-matrix multiplication is already the most mature commercial use case. Silicon-verified work published in Nature Communications in 2025 showed a near-threshold memristive compute-in-memory engine with peak throughput of 10.49 TOPS and energy efficiency of 55.21 to 88.51 TOPS/W. That performance explains why analog arrays still lead near-term deployment discussions despite the calibration and drift challenges that remain. Analog designs fit the strengths of crossbar hardware because they handle dense multiply operations with very low data-movement overhead. In the ReRAM crossbar in-memory computing market, which gives analog architectures the clearest installed base and the strongest immediate commercial familiarity.

Hybrid computing is projected to expand at a 41.26% CAGR through 2031, which reflects a practical move toward balancing accuracy, efficiency, and controllability. A mixed-precision memristor and SRAM compute-in-memory AI processor published in Nature during 2025 showed that combining ReRAM and SRAM blocks can deliver a more deployable compromise than either pure analog or pure digital designs alone. That approach matters because it keeps the efficiency benefit of analog ReRAM while using digital structures where precision or buffering needs are higher. A fully digital RRAM compute-in-memory chip reported in 2026 also showed zero bit-error rate, 72.30% silicon area reduction, and 57.26% energy savings versus analog RRAM compute-in-memory, which supports the case for reliability-oriented digital use cases. The ReRAM crossbar in-memory computing market is therefore moving from single-paradigm design toward architecture mixing, where system goals decide the balance between analog speed, digital accuracy, and hybrid flexibility.

By Application: AI Inference Commands Share, Training Workloads Accelerate

AI inference held 52.96% share in 2025, which made it the largest application in the ReRAM crossbar in-memory computing market size because edge devices are already demanding faster and lower-power neural processing. A 2025 analog compute-in-memory core validated for embedded applications reached 107 TOPS/W and showed how instruction-controlled inference hardware is moving closer to practical deployment. Inference leads because it tolerates present-day analog limits more easily than training, while still benefiting strongly from lower memory traffic and always-on non-volatile operation. It also maps well to hardware in IoT sensors, automotive controllers, cameras, and low-power voice or vision systems. The ReRAM crossbar in-memory computing market continues to see inference as the first volume destination because it combines visible system value with a lower qualification threshold than full training workloads.

AI training is projected to expand at a 41.66% CAGR through 2031, which shows that the application mix is no longer limited to inference-only assumptions. IBM Research presented transfer learning on a 14nm CMOS-compatible ReRAM array at IEEE IEDM 2025, using an analog in-memory training algorithm with performance that stayed close to floating-point baselines on edge-scale tasks. That result matters because it shifts ReRAM from a read-mostly inference story toward a broader training-and-inference platform. Neuromorphic computing also benefits from IBM’s hardware work on oscillatory neural networks that use ReRAM crossbar coupling elements. Logic computing and edge intelligence remain smaller today, but both benefit when non-volatile compute can remove repeated conversions or support continuous local processing under tight power budgets. In the ReRAM crossbar in-memory computing industry, training progress is important because it opens a second layer of demand that could deepen the technology’s role in future AI hardware stacks.

By End User: Data Centers Lead On Volume, Automotive Fastest To Scale

Data centers and HPC held 57.77% share in 2025, which gave them the largest demand position in the ReRAM crossbar in-memory computing market as AI workloads kept raising memory bandwidth and energy costs. The International Energy Agency reported a 17% increase in data center electricity use during 2025, which explains why architectures that reduce memory movement are drawing stronger operator attention. Hyperscaler spending trends reinforce that pressure because energy per operation and memory efficiency now influence both cost and scaling decisions for training and inference infrastructure. Consumer electronics and telecommunications add breadth to the user base, but data center demand remains the clearest volume anchor because the compute stack there pays a direct penalty for every unnecessary memory transfer. That is why the ReRAM crossbar in-memory computing market keeps strong alignment with HPC and cloud AI use cases even as edge demand grows.

Automotive is projected to expand at a 42.24% CAGR through 2031, making it the fastest-growing end-user segment in the provided input. The segment is advancing because automotive memory needs combine high-temperature tolerance, long retention, strong endurance, and deterministic behavior in a way that conventional embedded flash struggles to sustain as nodes shrink. Weebit Nano’s 2025 presentation highlighted AEC-Q100 operation at 150°C, 10-year retention, and 100,000 endurance cycles, which gives a practical benchmark for automotive qualification expectations. Industrial automation follows a closely related path because controllers in that setting face similar durability and latency demands. Aerospace and defense remain smaller, but IEEE MECON 2025 work on radiation-hardened conductive-bridge RAM shows why specialized high-reliability variants could still matter in selected programs.

Geography Analysis

North America held 49.07% share in 2025, which gave it the largest regional position in the ReRAM crossbar in-memory computing market. The region benefits from a dense mix of AI chip design activity, licensing relationships, and hyperscaler infrastructure spending that keeps energy-efficient memory architectures in active evaluation. IBM Research’s continued work on analog ReRAM hardware, including 14nm transfer learning on CMOS-compatible arrays, supports North America’s role as a major source of advanced system-level validation. Weebit Nano’s licensing progress with Texas Instruments also reinforces the region’s position in embedded processing and commercialization pathways. Together, those factors keep North America at the center of current demand formation and product planning.

Asia-Pacific is projected to expand at a 41.61% CAGR through 2031, which makes it the fastest-growing regional block in the provided input and a major driver of the ReRAM crossbar in-memory computing market size over the forecast period. South Korea’s national analog compute-in-memory program is a key regional signal because it links government funding, universities, public research institutes, and manufacturing partners around a 200 TOPS/W target. Japan is also contributing important device-level progress through the University of Tokyo and Nuvoton Technology Japan work on multi-level cell ReRAM compute-in-memory with 10-year retention. These advances matter because they address both performance ambition and reliability barriers within the same region. They also strengthen Asia-Pacific’s position as a place where public support, manufacturing capability, and practical device research can reinforce one another.

Europe remains a meaningful third regional position because the region combines automotive electronics demand with a public research base that continues to fund low-power compute hardware. A 2025 embedded analog compute-in-memory core supported under a European ECSEL-JU framework shows that Europe is still building practical silicon demonstrations rather than limiting activity to academic modeling. The region’s automotive and industrial profile also aligns well with the high-reliability strengths that support future ReRAM adoption. South America and the Middle East and Africa remain earlier-stage areas, where adoption is more likely to come through industrial automation and communications equipment than through local manufacturing leadership.

Competitive Landscape

The ReRAM crossbar in-memory computing market remains moderately fragmented, with one group focused on manufacturing qualification and another focused on licensing and specialized device development. The manufacturing side matters because advanced memory adoption depends on stable process integration, validated retention, and repeatable yield rather than on device novelty alone. The licensing side matters because many companies do not own major fabs, but they do control process modules, array know-how, or specific circuit architectures that are needed for product qualification. This split gives the ReRAM crossbar in-memory computing market a layered structure where manufacturing scale and IP control do not always sit inside the same company.

One important strategic move came from Weebit Nano’s agreement with Texas Instruments, which included embedded ReRAM IP licensing, technology transfer, tape-out support, and qualification work for selected embedded processing products. A second move came when Weebit Nano’s ReRAM was selected for the Republic of Korea’s government-funded analog compute-in-memory program, which gave the company a role in a nationally backed development path rather than only a private commercial program. A third example came from 4DS Memory, which reported a 4.7ns write speed milestone in 2025 and a design agreement with Infineon, imec, and a major Taiwanese foundry for a custom memory test chip at 20nm. These moves show that companies are competing through qualification partnerships, national programs, and device-level performance proof rather than through broad volume shipments alone. They also show why a strategic position in this market depends on being useful to foundries and system designers at the same time.

Commercial barriers remain high because retention, endurance, drift management, and safety validation all need evidence that goes beyond one successful demonstration chip. The University of Tokyo and Nuvoton's work on 10-year retention and drift compensation shows how much circuit and device engineering is still required to make multi-level operation reliable enough for deployment. IBM’s training and inference demonstrations, along with Nature and Nature Communications publications on mixed-precision and memristive compute-in-memory, also show that system-level success depends on architecture choices as much as on raw device physics. In practical terms, the winners in the ReRAM crossbar in-memory computing market are likely to be companies that can tie qualification, architecture, and customer integration into one dependable commercial package. That is why the field still looks fragmented today, even though barriers to entry remain difficult.

ReRAM Crossbar In-Memory Computing Industry Leaders

Samsung Electronics Co., Ltd.

Taiwan Semiconductor Manufacturing Company Limited

Micron Technology, Inc.

SK Hynix Inc.

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Weebit Nano confirmed that two product customers had taped-out chip designs integrating its ReRAM module, one, Overlord Labs' next-generation smart battery management system, fabricated at DB HiTek, already received functional prototype silicon. Weebit cited growing demand for faster, lower-power embedded non-volatile memory as the driver, and anticipated additional tape-outs before year-end. Mass production qualification is expected to take 12 to 18 months from tape-out.

- April 2026: Weebit Nano upgraded FY26 revenue guidance to at least AUD12 million (USD 8.38 million), confirmed that the Texas Instruments ReRAM program was initiated and progressing on schedule, and stated that the onsemi project advanced in parallel, highlighting how Tier-1 IDM licensing is translating into commercially validated production capacity.

- March 2026: Weebit Nano's ReRAM was selected for a Republic of Korea government-funded program advancing ultra-low-power analog compute-in-memory technology for AI applications, targeting 200 TOPS/W. The consortium includes Seoul National University, Daegu Gyeongbuk Institute of Science and Technology, Chungbuk National University, ETRI, and AnalogAI, with DB HiTek manufacturing devices. The program targets scalable, device-array-based silicon verification of ACiM for inference and longer-term training workloads.

- December 2025: IBM Research presented a demonstration of transfer learning on a 14nm CMOS-compatible ReRAM array using an analog in-memory training algorithm at IEEE IEDM 2025, showing competitive performance with floating-point baselines on edge-scale tasks. This established 14nm as the commercial frontier for IBM's analog AI hardware roadmap and directly challenged the prevailing assumption that ReRAM-based training is confined to research settings.

Global ReRAM Crossbar In-Memory Computing Market Report Scope

ReRAM Crossbar In-Memory Computing Market refers to systems and components that use resistive RAM crossbar arrays to perform computation directly inside memory. This architecture reduces data movement, lowers latency, and improves energy efficiency compared with conventional von Neumann computing.

The ReRAM Crossbar In-Memory Computing Market Report is Segmented by ReRAM Technology Type (Conductive Bridging RAM, and Oxide-Based ReRAM), Integration (Embedded, and Standalone), Computing Architecture (Analog In-Memory Computing, Digital In-Memory Computing, and Hybrid Computing), Application (AI Inference, AI Training, Neuromorphic Computing, Logic Computing, and Edge Intelligence), End User (Data Centers and HPC, Consumer Electronics, Automotive, Industrial Automation, Telecommunications, Healthcare, and Aerospace and Defense), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Conductive Bridging RAM |

| Oxide-Based ReRAM |

| Other ReRAM Technology Type |

| Embedded |

| Standalone |

| Analog In-Memory Computing |

| Digital In-Memory Computing |

| Hybrid Computing |

| AI Inference |

| AI Training |

| Neuromorphic Computing |

| Logic Computing |

| Edge Intelligence |

| Data Centers and HPC |

| Consumer Electronics |

| Automotive |

| Industrial Automation |

| Telecommunications |

| Healthcare |

| Aerospace and Defense |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By ReRAM Technology Type | Conductive Bridging RAM | |

| Oxide-Based ReRAM | ||

| Other ReRAM Technology Type | ||

| By Integration | Embedded | |

| Standalone | ||

| By Computing Architecture | Analog In-Memory Computing | |

| Digital In-Memory Computing | ||

| Hybrid Computing | ||

| By Application | AI Inference | |

| AI Training | ||

| Neuromorphic Computing | ||

| Logic Computing | ||

| Edge Intelligence | ||

| By End User | Data Centers and HPC | |

| Consumer Electronics | ||

| Automotive | ||

| Industrial Automation | ||

| Telecommunications | ||

| Healthcare | ||

| Aerospace and Defense | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the ReRAM crossbar in-memory computing space?

The ReRAM crossbar in-memory computing market was valued at USD 92.60 million in 2025, stands at USD 123.80 million in 2026, and is forecast to reach USD 678.50 million by 2031 at a 40.70% CAGR.

Why is this technology gaining attention in AI hardware?

It reduces data movement by performing vector-matrix operations inside memory, which helps lower power use and latency in both edge and data center AI systems.

Which application leads demand today?

AI inference led with 52.96% share in 2025 because it aligns well with current edge hardware needs and benefits quickly from lower memory traffic.

Which end-user group is growing the fastest?

Automotive is the fastest-growing end-user segment, with a projected 42.24% CAGR through 2031, because qualification progress is improving for high-temperature and high-endurance embedded use cases.

Which region is strongest right now?

North America led with 49.07% share in 2025, supported by AI chip design activity, licensing pipelines, and hyperscaler demand for more efficient memory architectures.

What is the main commercialization challenge through 2031?

Manufacturing maturity and reliability qualification remain the key obstacles, especially at advanced nodes and in safety-critical applications that need long retention, endurance, and drift control.

Page last updated on: