Refurbished Laboratory Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

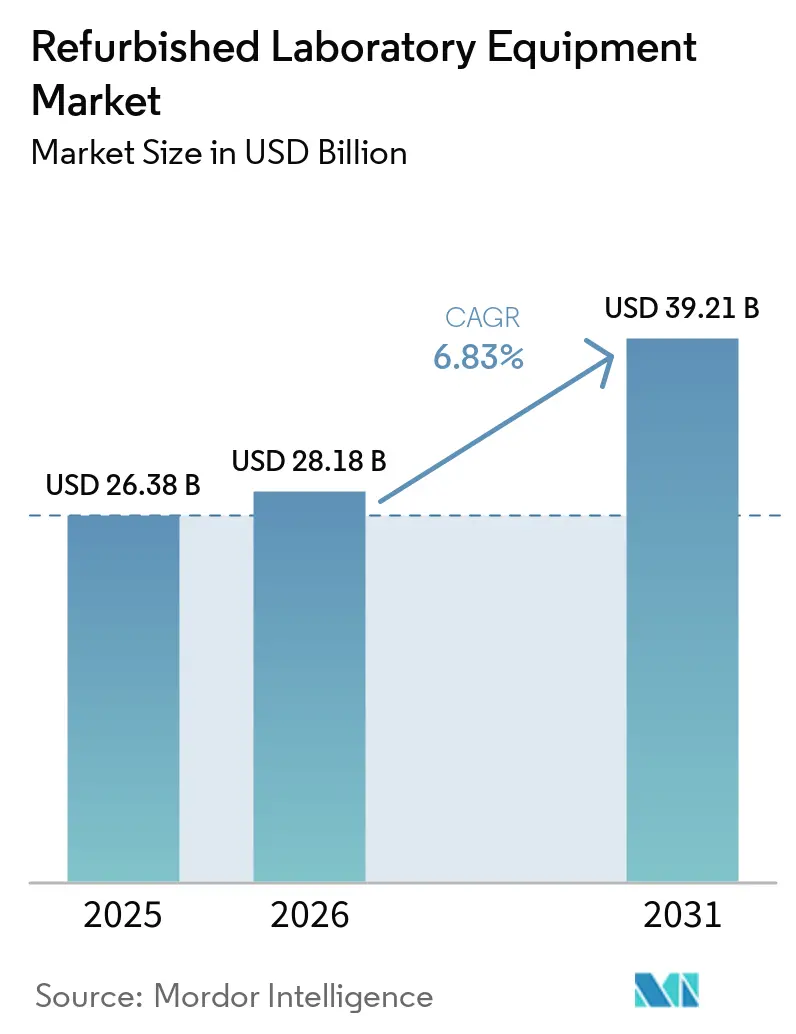

| Market Size (2026) | USD 28.18 Billion |

| Market Size (2031) | USD 39.21 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

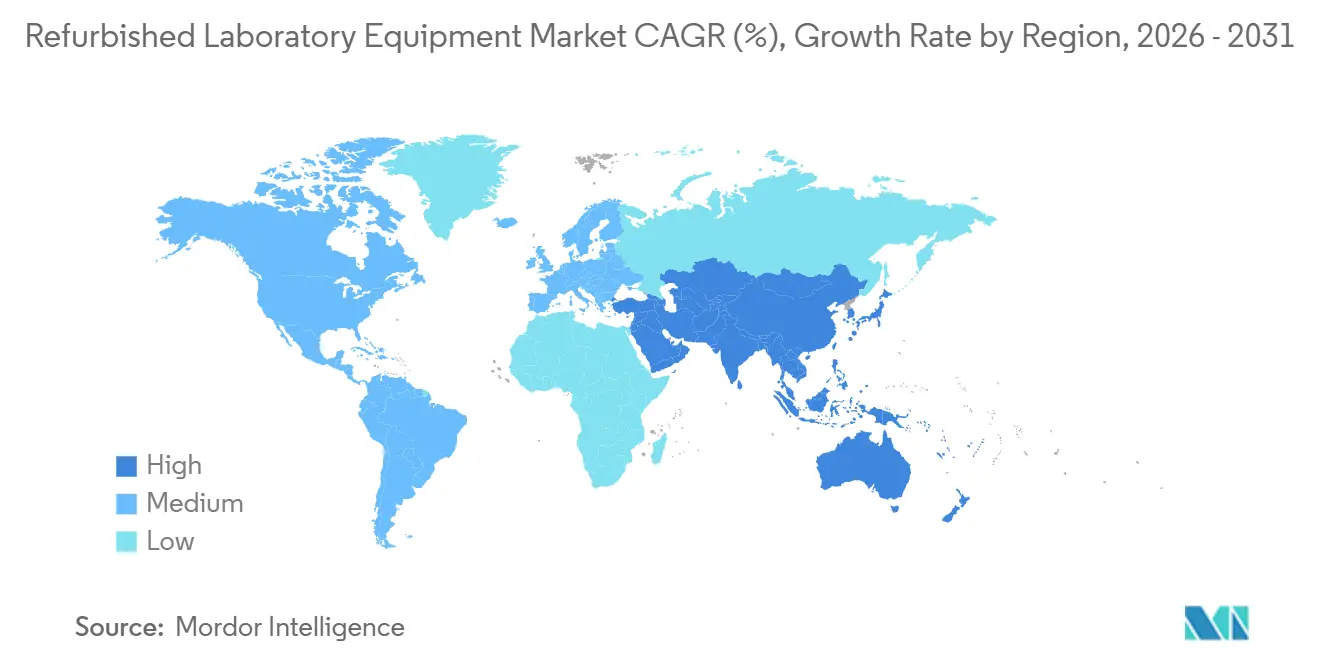

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refurbished Laboratory Equipment Market Analysis by Mordor Intelligence

The Refurbished Laboratory Equipment Market size is expected to grow from USD 26.38 billion in 2025 to USD 28.18 billion in 2026 and is forecast to reach USD 39.21 billion by 2031 at 6.83% CAGR over 2026-2031.

Momentum is building as circular procurement policies and OEM‑certified programs reduce perceived risk and support compliance in regulated environments. Rising R&D intensity among pharmaceutical and biotechnology players expands the installed base that later enters secondary channels during trade‑in cycles or post‑M&A fleet refresh. Academic and research institutions in emerging regions are enlarging laboratory footprints, which increases demand for certified refurbished systems that deliver performance with lower upfront cost. Regional growth is led by Asia‑Pacific with laboratory expansions supported by government programs, while North America maintains leadership through deep secondary‑equipment networks and accreditation‑aligned service ecosystems. Buyers continue to evaluate the total cost of ownership, calibration traceability, and software support to align refurbished acquisitions with quality and uptime requirements.

Key Report Takeaways

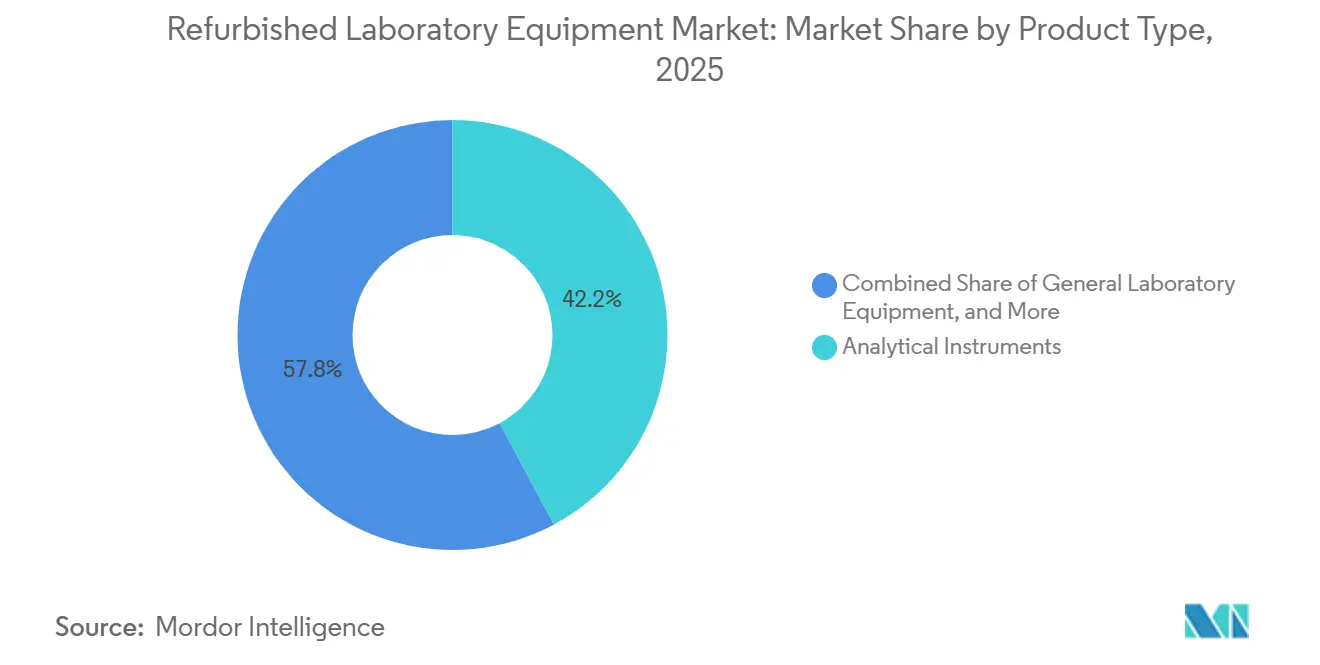

- By product type, Analytical Instruments led with 42.17% revenue share in 2025; General Laboratory Equipment is forecast to expand at a 7.43% CAGR through 2031.

- By end user, Pharmaceutical & Biotechnology Companies represented 32.28% of 2025 revenue; Academic & Research Institutes are expected to record the fastest growth at 8.56% CAGR through 2031.

- By sales channel, OEM Certified Pre-Owned Programs accounted for 48.13% of the revenue by sales channel. Meanwhile, Independent Refurbishers and Dealers are expected to experience the quickest growth at a 7.12% CAGR through 2031.

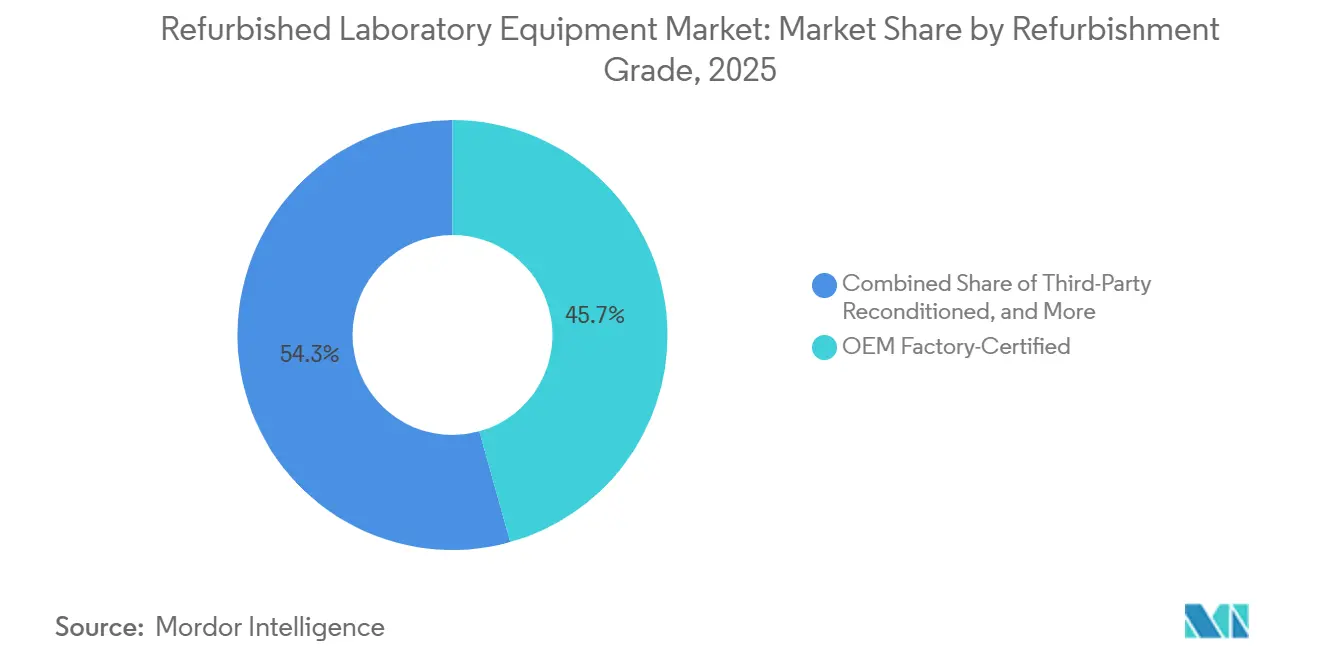

- By refurbishment grade, OEM Factory-Certified dominated with a 45.67% revenue share in 2025, while Third-Party Reconditioned is expected to grow at an impressive 8.09% CAGR through 2031.

- By geography, North America held 36.74% share in 2025; Asia‑Pacific is projected to advance at an 8.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Refurbished Laboratory Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Effective Procurement for Budget-Constrained Labs and Startups | +1.8% | Global, with early gains in Asia-Pacific (India, Southeast Asia) and Latin America | Short term (≤ 2 years) |

| Expansion of Pharma and Biotech R&D Increasing Instrument Demand | +1.5% | North America & EU core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Sustainability and Circular Economy Policies Accelerating Reuse | +1.3% | EU and North America (PFSCM/My Green Lab Act compliance), expanding to China | Medium term (2-4 years) |

| Growth of Academic and Research Capacity in Emerging Economies | +1.4% | Asia-Pacific (China, India, Indonesia), Sub-Saharan Africa (Kenya, Nigeria), Latin America | Long term (≥ 4 years) |

| OEM Certified Pre-Owned and Trade-In Programs De-Risk Purchases | +0.9% | North America & EU (Thermo Fisher, Agilent footprint), scaling to Asia-Pacific | Short term (≤ 2 years) |

| Lab Closures, M&A, and Decommissioning Fueling High-Quality Secondary Supply | +0.6% | North America core (biotech consolidation), EU pharmaceutical restructuring | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost-Effective Procurement for Budget-Constrained Labs and Startups

Budget‑sensitive buyers spanning academia, diagnostics, and contract research redirect capital from new purchases to certified refurbished instruments that meet throughput needs at lower acquisition cost, which allows funds to be reallocated to consumables, personnel, and validation. Public buyers and NGOs frame decisions through total cost of ownership lenses that weigh calibration, parts availability, reagent logistics, and service access over multi‑year horizons to avoid idle assets and procurement lock‑ins. Vendors that publish calibration traceability and pre‑shipment validation gain preference as buyers seek predictable uptime and auditable records. On the supply side, certified refurbishment programs with factory inspection and warranty parity narrow the perceived performance gap compared with new systems. Marketplace specialists that provide documented environmental savings and configured startup bundles strengthen appeal to incubators and early‑stage labs seeking rapid commissioning. Case‑in‑point examples include vendor programs that disclose multi‑point inspections with genuine parts, full warranty, and on‑site installation to support compliant go‑live in regulated workflows[1]PFSCM, “Implementing circular economy practices in lab procurement for a greener supply chain,” . Budget‑conscious labs also validate supplier claims against calibration certificates traceable to national metrology bodies to maintain audit‑ready records.

Expansion of Pharma and Biotech R&D Increasing Instrument Demand

Rising biopharma R&D intensity increases deployments of LC‑MS, chromatography systems, and high‑content imaging platforms, which later become candidates for trade‑in or certified resale during portfolio upgrades. M&A and portfolio shifts add to decommissioning cycles that release high‑value instruments into refurbishment pipelines, often bundled with removal and logistics services to reduce buyer friction. Large OEMs continue to invest in end‑to‑end capabilities and partnerships that reinforce customer relationships and expand access to installed equipment fleets over the asset lifecycle. India’s Vigyan Dhara expanded R&D allocations in 2025–26, supporting equipment grants that add to regional installed bases and set up refresh cycles over subsequent funding windows. OEM acquisitions and capacity expansions that align with biopharma demands signal sustained instrument utilization and repower secondary channels as customers modernize fleets[2]Ema Ruzic, “Unlock High‑Performance LC‑MS with Factory‑Certified Systems from Thermo Fisher Scientific,” . Regulatory convergence around ISO 13485 and FDA QMSR expectations further codifies calibration and documentation, which raises the bar for refurbishers and increases buyer trust in well‑documented offerings.

Sustainability and Circular Economy Policies Accelerating Reuse

ESG objectives and circular procurement mandates prompt laboratories to extend the life of instruments through validated refurbishment, planned trade‑ins, and take‑back programs that quantify carbon and waste reductions. Healthcare supply chains account for most sector emissions, which places pressure on procurement teams to capture environmental savings while maintaining compliance and performance targets. OEM sustainability disclosures reinforce product stewardship around resource efficiency and lifecycle management, and factory‑certified refurbished programs formalize those commitments into procurement‑ready[3]Agilent Technologies, “Certified Pre‑Owned LC/MS Instruments,” . In the EU, substantial refurbishment of regulated devices is treated as manufacturing, which requires CE marking and post‑market controls that standardize quality and reduce buyer uncertainty. Calibration and validation frameworks under ISO/IEC 17025, ISO 13485, and FDA quality regulations push vendors to document traceability, uncertainty, and corrective actions to keep refurbished units audit‑ready for clinical or QC environments[4]Joe DiMarino, “The Role of Calibration in Regulatory Compliance: FDA, ISO 9001, and AS9100,” . These compliance structures support the shift from opportunistic bargains to planned fleet management within the refurbished laboratory equipment market.

Growth of Academic and Research Capacity in Emerging Economies

Government‑backed programs in Asia‑Pacific and Sub‑Saharan Africa are expanding labs across universities and research institutes, which increases near‑term demand for cost‑effective refurbished systems and sets in motion multi‑year upgrade cycles. New centers that serve national research agendas add metabolomics, molecular, imaging, and characterization capabilities, creating installed bases that later channel into certified refurbishment as cohorts refresh equipment. University‑industry and public‑funded initiatives improve equipment utilization and promote resource sharing, which supports the circulation of fit‑for‑purpose instruments across institutions at lower unit cost. Pan‑regional digital infrastructure programs expand connectivity for research and education networks, which in turn requires analytical instrumentation for environmental, clinical, and data‑intensive applications as labs come online. These trajectories support steady growth in certified refurbished adoption, where grants and budget ceilings reward validated performance at reduced capex. Concrete examples include large‑scale university instrumentation centers and cross‑border research connectivity initiatives that directly expand installed bases aligned to future secondary supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy, Reliability, and Calibration Concerns from Non-Uniform Refurb Standards | -0.9% | Global, with heightened impact in FDA-regulated markets (North America, EU) | Short term (≤ 2 years) |

| Limited Warranty/After-Sales Support and Lack of Process Standardization | -0.7% | Emerging markets (Asia-Pacific, Latin America, Africa) with fragmented dealer networks | Medium term (2-4 years) |

| OEM Software Licensing/EoL Support Restrictions Limiting Redeployment | -0.75% | Strong impact in North America and Europe due to strict IP enforcement and regulated lab environments | Long term (≥ 4 years) |

| Parts Obsolescence and Validation Costs for Regulated Workflows | -0.8% | Global, with highest impact in pharmaceutical hubs (North America and Europe) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Accuracy, Reliability, and Calibration Concerns from Non-Uniform Refurb Standards

Calibration quality remains a top concern when refurbishment standards vary, especially where labs must meet FDA, ISO, and CLIA requirements that depend on tight measurement control. Federal letters of nonconformance in recent years have frequently referenced calibration gaps, which elevates buyer scrutiny of traceability, uncertainty budgets, and environmental controls embedded in vendor processes. ISO 13485 and ISO/IEC 17025 frameworks expect documented calibration chains to national metrology bodies, defined tolerances, and investigation of out‑of‑tolerance events to maintain product quality across the lifecycle. FDA quality system requirements also emphasize defined calibration intervals and records that link instrument status to batches or samples tested, which pushes refurbishers to provide auditable documentation from day one. CLIA and related guidance reinforce periodic verification triggers such as reagent‑lot changes and maintenance events, which increase the importance of reliable service access for refurbished units placed in clinical workflows. Labs mitigate this restraint by standardizing on vendors that provide calibration certificates traceable to NIST or BIPM, validated software versions, and environmental conditions documented at the time of calibration.

Limited Warranty/After-Sales Support and Lack of Process Standardization

Warranty variability creates uncertainty around downtime risk and repair costs, which can slow decisions among smaller labs that cannot absorb extended outages. OEM‑certified refurbished units often include 12‑month warranties, on‑site installation, and optional service tiers, while mid‑tier brokers may provide 90‑ to 180‑day coverage with extensions for selected instrument types. Software validation adds another layer, since even off‑the‑shelf tools used in quality environments require defined verification or validation depending on the change scope, which increases documentation and testing obligations during upgrades. FDA Part 11 expectations for electronic records and signatures also apply, which requires labs to align instrument software and LIMS configurations to maintain data integrity. Buyers respond by prioritizing sellers that offer installation, operator training, and documented software states, all supported by access to spare parts and responsive field service. This approach reduces commissioning time and lowers the risk of unplanned downtime in regulated workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Analytical Instruments to Lead Market Share, with General Laboratory Equipment Driven by Packaging Innovations

Analytical Instruments captured 42.17% of revenue in 2025 within the refurbished laboratory equipment market, reflecting sustained demand for LC‑MS, GC, and spectroscopy systems used across discovery and QC workflows. Procurement teams increasingly channel late‑generation instruments into trade‑in programs that return certified LC‑MS platforms with documented factory inspection, firmware updates, and parity warranties, which strengthens trust in this category for regulated uses. Residual value is reinforced by sellers that provide multi‑month warranties, traceable calibration, and installation services, while buyers formalize uptime expectations through service tiers and preventive maintenance plans. Calibration documentation aligned to ISO 13485 and ISO/IEC 17025 remains central to placing refurbished analytical systems in pharma QC and CLIA environments, which influences price premiums for OEM‑certified units over non‑certified alternatives. Where labs retire legacy operating systems or software versions, sellers that provide validated software states at shipment reduce commissioning friction and speed compliance sign‑offs. These factors collectively reinforce category leadership for analytical instruments in the refurbished laboratory equipment market.

General Laboratory Equipment is forecast to be the fastest‑growing product category at a 7.43% CAGR through 2031, supported by broad applicability across academic, hospital, and industrial labs. The refurbished laboratory equipment market size tied to this segment benefits from quick‑turn availability of centrifuges, incubators, biosafety cabinets, balances, and liquid handling systems that can be certified to lab accreditation requirements. Demand is reinforced by modular automation and sustainability‑aligned equipment that reduces energy or consumables usage, which aligns with circular procurement objectives. Sellers differentiate through warranty breadth and ability to ship with documented IQ/OQ/PQ test records for rapid go‑live in audited environments. Buyers increasingly bundle refurbished general equipment with startup kits and training to stand up new labs or expand existing facilities on constrained budgets. Documentation quality and consistency remain the primary selection criteria, with calibration traceability and defined service routes improving decision speed and confidence. These dynamics support sustained expansion for general equipment in the refurbished laboratory equipment market.

By End User: Pharmaceutical and biotechnology companies dominate the market, while academic and research institutes exhibit rapid growth driven by increased government grants.

Pharmaceutical & Biotechnology Companies represented 32.28% of 2025 revenue as R&D investment supported high utilization of LC‑MS, chromatography, and high‑content imaging platforms across development and QC. Active trade‑in and upgrade cycles supply secondary channels with well‑maintained assets as new modalities expand instrumentation needs in discovery and analytics. OEM partnerships and capacity additions that align to drug‑product manufacturing and services strengthen the equipment lifecycle, from primary sale through eventual certified resale. Bioprocess and analytical workflow investments continue to shape installed bases, which later feed the refurbished laboratory equipment market with quality‑documented units. The refurbished laboratory equipment market share tied to pharma buyers remains supported by warranty parity and factory validation that satisfy audit and accreditation requirements. These elements keep refurbished placements viable for non‑GxP and selected GxP contexts where documentation, calibration traceability, and service response times are proven.

Academic & Research Institutes are projected to grow the fastest at an 8.56% CAGR through 2031 as public programs expand laboratory capacity and prioritize hands‑on infrastructure. India’s Vigyan Dhara funding supports instrumentation grants across institutions, which increases near‑term demand for certified refurbished systems and sets multi‑year refresh cycles for future secondary supply. New national instrumentation centers and university‑industry hubs bring metabolomics, molecular, and characterization capabilities online, often with refurbished kits that speed commissioning and training. Procurement teams in academia weigh calibration documentation, installation, and training services to comply with accreditation and grant reporting while maximizing instrument uptime. Suppliers that combine warranty coverage, startup bundles, and service agreements support rapid adoption and long‑term utilization in teaching and research labs. These drivers sustain the fast‑growing academic cohort in the refurbished laboratory equipment market.

By Sales Channel: OEM certified pre-owned programs are expected to lead, while independent refurbishers are projected to grow significantly, driven by flexible warranty innovations.

OEM Certified Pre-Owned Programs captured 48.13% of 2025 revenue in the refurbished laboratory equipment market, reflecting buyer preference for factory validation, genuine-part replacement, and warranty parity that support CLIA and FDA-regulated workflows. Thermo Fisher Scientific’s factory-certified LC-MS program includes a 29-point inspection, reconditioning with only genuine Thermo Scientific parts, firmware and software updates, professional installation by Unity Lab Services, and a full one-year warranty equivalent to new instruments. Agilent’s Certified Pre‑Owned LC/MS portfolio guarantees performance to new-instrument standards, is backed by a 12‑month warranty and operational validation, and offers financing options such as leases, rentals, trade‑ins, and buybacks to ease capital planning. Trade-in workflows further formalize secondary participation by evaluating multi-brand systems, crediting residual value toward upgrades, and bundling free removal to simplify changeovers. Regulatory convergence reinforces this model as the FDA’s Quality Management System Regulation aligns with ISO 13485 expectations for calibration traceability and documentation that refurbishers must evidence for audit readiness. Labs managing clinical or QC workflows prioritize certificates that trace to national metrology bodies and follow calibration verification practices consistent with CLIA guidance to reduce compliance risk during commissioning and routine use.

Independent Refurbishers are projected to expand at a 7.12% CAGR through 2031, benefitting from broader multi-brand inventory, faster turnaround that can be within 30–60 days, and flexible warranties that capture buyers seeking value with essential coverage. American Laboratory Trading lists thousands of instruments from leading OEMs and offers bundled service agreements that help organizations stretch budgets while maintaining uptime and performance. International Equipment Trading highlights savings up to 70% versus new list prices on HPLC, mass spectrometers, and electron microscopes, with warranties ranging from ninety days to two years and service through independent or OEM channels in the U.S. and overseas. Copia Scientific provides factory-tested instruments with a standard 180‑day parts-and-labor warranty, extended to one year for liquid handlers, plus on‑site installation, training, and integration that appeal to startups and academic labs. Digital marketplaces add reach by aggregating listings and qualified buyers, with LabX reporting large volumes of product listings, lead flow, and budget-ready users that streamline discovery and purchase cycles for secondary equipment. Channel choice is influenced by documentation and calibration assurances, since CLIA verification expectations and ISO/IEC 17025 traceability drive many labs to favor sellers that provide NIST‑traceable certificates and validated software states at shipment.

By Refurbishment Grade: OEM certified pre-owned programs are expected to lead, while independent refurbishers are projected to grow significantly, driven by flexible warranty innovations.

OEM Factory‑Certified units accounted for 45.67% of 2025 revenue in the refurbished laboratory equipment market, reflecting demand for standardized reconditioning protocols, documented IQ/OQ/PQ, and calibration traceability that align with FDA QMSR and ISO 13485 requirements. Thermo Fisher details factory-certified LC‑MS refurbishment steps, including multi-point inspection, genuine-part replacement across critical subsystems, firmware and software updates, and on‑site installation under a full one‑year warranty that mirrors new instruments. Agilent’s Certified Pre‑Owned LC/MS instruments undergo factory refurbishment with electromechanical and operational validation, cosmetic restoration, and current firmware and software, and can be paired with CrossLab service plans for ongoing support. Calibration practices that trace to NIST or BIPM with documented uncertainty budgets remain central to audit-readiness in clinical and pharma QC contexts, which sustains buyer preference for OEM-certified offerings in regulated workflows. Labs that operate under Part 11 and CLIA requirements often choose factory‑certified units to minimize validation burden and penalty risk, with industry guidance emphasizing the costs of noncompliance and the need for verifiable electronic records and calibration logs. As circular procurement expands and documentation standards tighten, factory‑certified units are positioned as lower‑risk placements with higher assurance of uptime in regulated environments.

Third‑Party Reconditioned instruments are projected to grow at an 8.09% CAGR through 2031, driven by cost‑performance advantages that satisfy non‑regulated academic research and many industrial QC applications. American Laboratory Trading and International Equipment Trading offer multi‑brand inventories, 30–60 day refurbishment cycles, and warranty options from 180 days to one year and up to two years, which align with budget constraints while meeting core performance needs. Copia Scientific supplements reconditioned instruments with installation, operator training, and integration services, coupled with a standard 180‑day warranty and longer terms for selected categories. Buyers and auditors continue to scrutinize calibration integrity, which pushes reputable third‑party refurbishers to partner with ISO/IEC 17025‑accredited labs and to supply certificates that are traceable to national standards. As‑is or lightly used options also maintain a role among budget‑constrained institutions in emerging regions where service coverage is limited, provided sellers can document instrument status, software versions, and calibration at the time of sale to support reliable start‑up and basic QA practices.

Geography Analysis

North America held 36.74% of 2025 revenue for the refurbished laboratory equipment market, supported by dense pharma and biotech clusters and mature secondary‑equipment channels. Federal and accreditation frameworks favor ISO/IEC 17025‑aligned calibration providers, which reinforces demand for documented refurbishment and traceability standards. OEMs continue to deepen U.S. manufacturing and services partnerships that strengthen lifecycle support and provide clear pathways to certified resale when fleets refresh. Trade‑in programs and factory‑certified refurbished offerings remain prominent in this region due to regulatory rigor and buyer preferences for warranty parity. Brokers and dealers complement OEM channels through inventory breadth and flexible warranties, while academic consortia source configured kits for rapid lab setups. These elements underpin regional leadership and steady adoption in the refurbished laboratory equipment market.

Asia‑Pacific is projected to grow at an 8.90% CAGR through 2031, the fastest among regions in the refurbished laboratory equipment market. University and national lab expansions are adding capacity in priority fields, and public programs in major countries are directing funds toward research infrastructure and training. India’s Vigyan Dhara allocation exemplifies this trend, creating a pipeline for both new and refurbished instruments across universities and institutes. Regional hubs are also building advanced instrumentation centers that will generate installed bases aligned to future secondary supply channels. As cohorts mature and upgrade cycles begin, OEM trade‑in and certified refurbished programs are expected to scale further into Asia‑Pacific. Buyers in the region focus on documentation readiness, service access, and software validation support to align with accreditation and data‑integrity requirements. These developments support sustained regional outperformance in the refurbished laboratory equipment market.

Europe maintains a significant share in the refurbished laboratory equipment market as stringent quality and safety regulations normalize documentation expectations for refurbished units. CE marking requirements for substantial refurbishment of regulated devices raise compliance thresholds but also reduce uncertainty for buyers by standardizing quality across member states. Leading OEMs continue to invest in European manufacturing and service footprints, which supports lifecycle management and certified resale pathways for instruments that exit primary service. Broader sustainability initiatives motivate institutions to extend asset life and adopt circular procurement rules that value refurbishment and take‑back options with provable environmental benefits. Collectively, these dynamics support durable demand for documented refurbished systems that fit regulated workflows and ESG policies in Europe.

In the Middle East and Africa and in South America, the refurbished laboratory equipment market advances as governments and universities build out research and testing capacity. Cross‑border digital infrastructure that connects thousands of institutions is catalyzing equipment demand for scientific programs, which expands installed bases that later recycle into secondary channels. Public‑private programs that strengthen research‑granting capacity and promote equipment utilization are improving access to instruments and supporting shared resource models. Buyers in these regions prioritize reliability, calibration traceability, and access to replacement parts to sustain uptime with limited local service options. Brokers and OEMs that provide remote support, documented installation, and clear warranty terms are positioned to accelerate adoption.

Competitive Landscape

The refurbished laboratory equipment market remains moderately fragmented, with two distinct competitive models. OEM refurbishers leverage factory processes to deliver certified pre‑owned instruments with multi‑point inspections, genuine parts, firmware updates, and 12‑month warranties, all paired with professional installation and service tiers. Specialist brokers aggregate multi‑owner assets from decommissions and trade‑ins, then refurbish and configure to buyer requirements with variable warranty terms that range from 90 to 365 days and options to extend coverage. The first model anchors trust through documented compliance and warranty parity, while the second competes on inventory breadth, price, and speed of turnaround. These models increasingly coexist as OEM trade‑ins capture late‑generation assets and brokers fill category and price gaps across geographies in the refurbished laboratory equipment market.

Strategic moves continue to shape participation and scale. OEMs launched certified LC‑MS programs with 29‑point inspections and full‑year warranties to mirror new‑system guarantees, including on‑site installation and performance verification, which lowers adoption friction and audit risk. Agilent’s certified pre‑owned LC/MS portfolio formalizes performance standards equivalent to new units and includes 12‑month warranty and validation support, which expands access for regulated workflows. Trade‑up and take‑back campaigns, including barcode reader programs and equipment trade‑in arrangements, streamline fleet modernization while capturing residual value and enabling circular participation at scale. These initiatives integrate refurbishment into planned lifecycle management in the refurbished laboratory equipment market.

Technology partnerships signal a next phase where AI and orchestration platforms elevate uptime and validation readiness for both new and refurbished assets. Collaborative work on agent‑to‑agent workflows and natural‑language experiment design indicates a shift toward autonomous orchestration that can standardize method transfer and reduce human error in commissioning or re‑commissioning equipment. AI‑enabled configuration, remote diagnostics, and predictive maintenance help shrink outages and support compliance with lab software validation practices. This digital layer benefits refurbished deployments that must achieve quick go‑lives with limited in‑house resources. Representative collaborations and product launches from lab automation and informatics vendors point to broader adoption of AI support tools across laboratories by 2026. This evolution strengthens the refurbished laboratory equipment market by improving commissioning, documentation, and uptime outcomes.

Refurbished Laboratory Equipment Industry Leaders

Agilent Technologies, Inc.

Becton, Dickinson and Company

Bruker Corporation

Revvity, Inc.

Thermo Fisher Scientific, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GenTech Scientific published technical updates related to mass spectrometry applications, highlighting advancements in analytical performance understanding for laboratory users. The company emphasized improved interpretation and optimization of mass spectrometry resolution in laboratory workflows. This content supported better utilization of analytical instruments commonly used in refurbished laboratory environments. It reflected ongoing engagement in supporting refurbished analytical equipment users.

- April 2025: Surplus Solutions LLC partnered with Certified Genetool to expand its laboratory equipment lifecycle management capabilities. The collaboration focused on refurbishment, maintenance, and redistribution of used laboratory instruments across pharmaceutical and biotechnology sectors. The partnership strengthened the availability of certified refurbished analytical and general laboratory equipment. It supported increasing demand for cost-effective laboratory solutions in research and production environments.

Global Refurbished Laboratory Equipment Market Report Scope

As per the scope of the report, refurbished laboratory equipment refers to previously used laboratory instruments that have been professionally inspected, repaired, recalibrated, and tested to restore them to functional and operational standards. These instruments are restored either by OEMs or certified third-party refurbishers to ensure reliable performance. They are often resold at a lower cost than new equipment while maintaining acceptable quality and accuracy for research, diagnostic, and analytical applications.

The refurbished laboratory equipment market is segmented by product type, end user, sales channel, refurbishment grade, and geography. By product type, the market is segmented into analytical instruments, general laboratory equipment, life science equipment, and clinical diagnostic equipment. By end user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, clinical & diagnostic laboratories, contract research organizations (CROs), and hospitals & healthcare facilities. By sales channel, the market is segmented into OEM certified pre-owned programs, independent refurbishers/dealers, and online marketplaces & auctions. By refurbishment grade, the market is segmented into OEM factory-certified, third-party reconditioned, and as-Is/lightly used with warranty. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Analytical Instruments |

| General Laboratory Equipment |

| Life Science Equipment |

| Clinical Diagnostic Equipment |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Clinical & Diagnostic Laboratories |

| Contract Research Organizations (CROs) |

| Hospitals & Healthcare Facilities |

| OEM Certified Pre-Owned Programs |

| Independent Refurbishers/Dealers |

| Online Marketplaces & Auctions |

| OEM Factory-Certified |

| Third-Party Reconditioned |

| As-Is/Lightly Used with Warranty |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Product Type | Analytical Instruments | |

| General Laboratory Equipment | ||

| Life Science Equipment | ||

| Clinical Diagnostic Equipment | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Academic & Research Institutes | ||

| Clinical & Diagnostic Laboratories | ||

| Contract Research Organizations (CROs) | ||

| Hospitals & Healthcare Facilities | ||

| By Sales Channel | OEM Certified Pre-Owned Programs | |

| Independent Refurbishers/Dealers | ||

| Online Marketplaces & Auctions | ||

| By Refurbishment Grade | OEM Factory-Certified | |

| Third-Party Reconditioned | ||

| As-Is/Lightly Used with Warranty | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026–2031 CAGR for the refurbished laboratory equipment market and where will the market land by 2031?

The refurbished laboratory equipment market is projected to grow at a 6.83% CAGR from 2026 to 2031, reaching USD 39.21 billion by 2031.

Which product category leads and which is growing fastest within the refurbished laboratory equipment market?

Analytical instruments led with 42.17% revenue share in 2025, while general laboratory equipment is the fastest growing category at a 7.43% CAGR through 2031.

Which end user segment is largest in the refurbished laboratory equipment market, and which is the growth leader?

Pharmaceutical and biotechnology companies held 32.28% of 2025 revenue, while academic and research institutes are growing the fastest at an 8.56% CAGR through 2031.

Which region holds the largest share and which is expanding fastest in the refurbished laboratory equipment market?

North America held 36.74% of revenue in 2025, while Asia Pacific is projected to grow the fastest at an 8.90% CAGR over 2026–2031.

What factors most reduce risk for buyers in the refurbished laboratory equipment market?

Factory certified pre owned programs, ISO aligned calibration traceability, one year warranties, and professional installation reduce risk and speed commissioning in regulated environments.

How do circular economy policies influence procurement decisions in this space?

Sustainability mandates and documented take back or trade in programs encourage validated refurbishment, which supports ESG goals and shifts procurement toward planned lifecycle management.

Page last updated on: