Refurbished Dental Equipment And Maintenance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

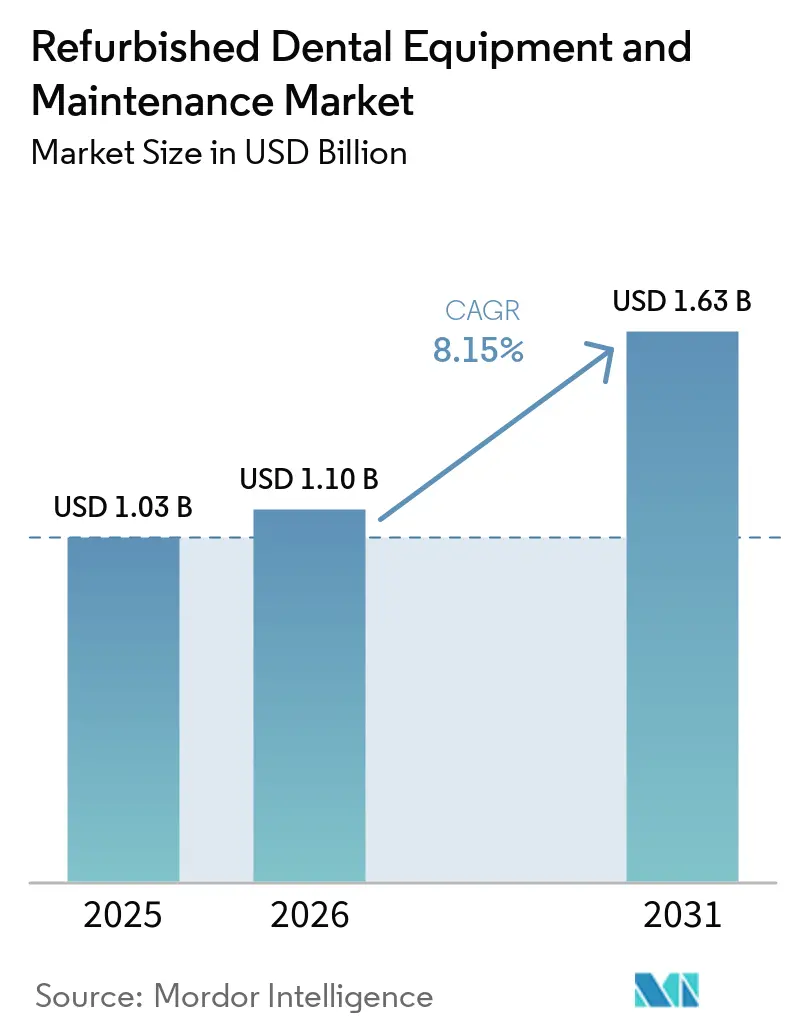

| Market Size (2026) | USD 1.10 Billion |

| Market Size (2031) | USD 1.63 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refurbished Dental Equipment And Maintenance Market Analysis by Mordor Intelligence

The Refurbished Dental Equipment & Maintenance Market size is projected to be USD 1.03 billion in 2025, USD 1.10 billion in 2026, and reach USD 1.63 billion by 2031, growing at a CAGR of 8.15% from 2026 to 2031.

Practices worldwide continue to chase lower up-front costs, greener supply chains, and predictable service outlays, pushing bulk purchases of recertified imaging systems, chairs, and handpieces into mainstream procurement cycles. Corporate dental service organizations (DSOs) are aggregating demand, often writing multi-year contracts that bundle replacement parts, remote diagnostics, and software upgrades, while independent clinics negotiate group-buying rates to preserve cash flow. EU and U.S. circular-economy mandates now require Digital Product Passports that track component provenance, turning high-quality refurbishment into a compliance shortcut rather than a compromise. Simultaneously, AI-driven predictive maintenance is shrinking unplanned downtime by two-thirds, extending device life spans well beyond manufacturers’ 8-10-year assumptions, and smoothing monthly cash-flow planning. Together, these forces reinforce steady, double-digit unit growth even as only 24% of U.S. dentists expect to commit to new-equipment capex in 2026.

Key Report Takeaways

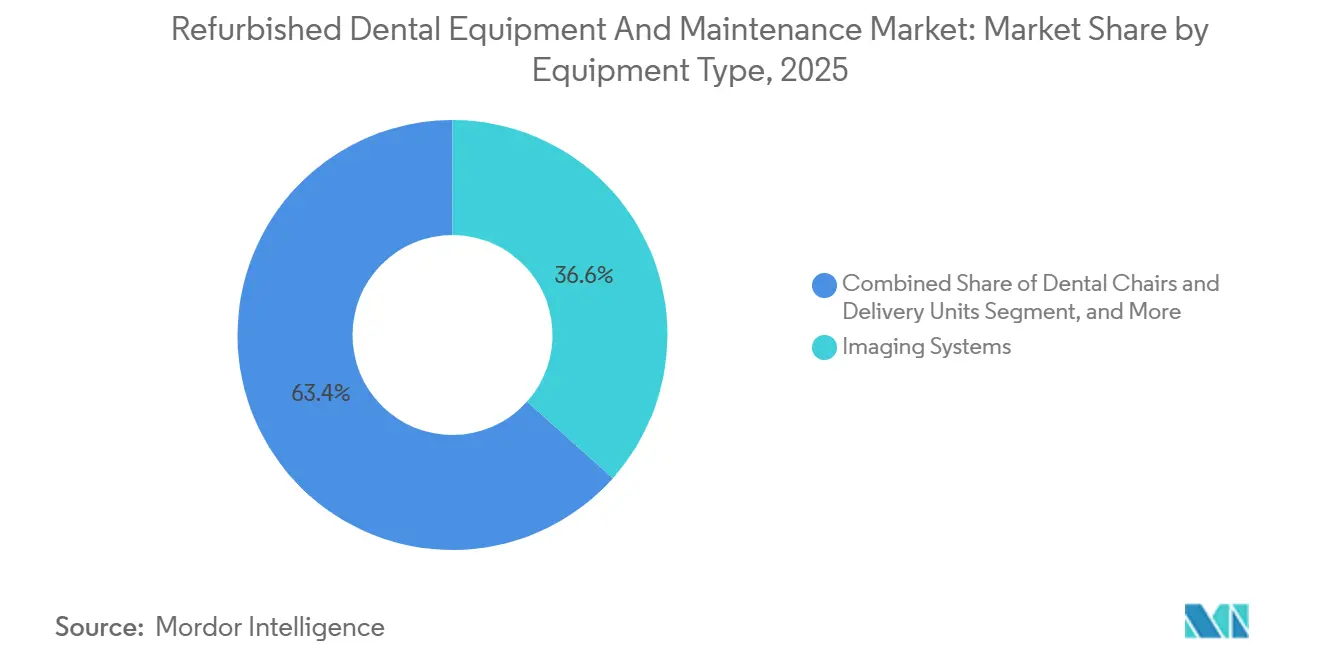

- By equipment type, imaging systems led with 36.62% of the refurbished dental equipment & maintenance market share in 2025. CAD/CAM & 3-D Printing Systems are forecast to advance at an 8.98% CAGR through 2031, the fastest among equipment segments.

- By service type, preventive maintenance accounted for 44.38% of the refurbished dental equipment & maintenance market size in 2025. Full-service contracts are projected to grow at 9.35% CAGR over 2026-2031, outpacing all other service models.

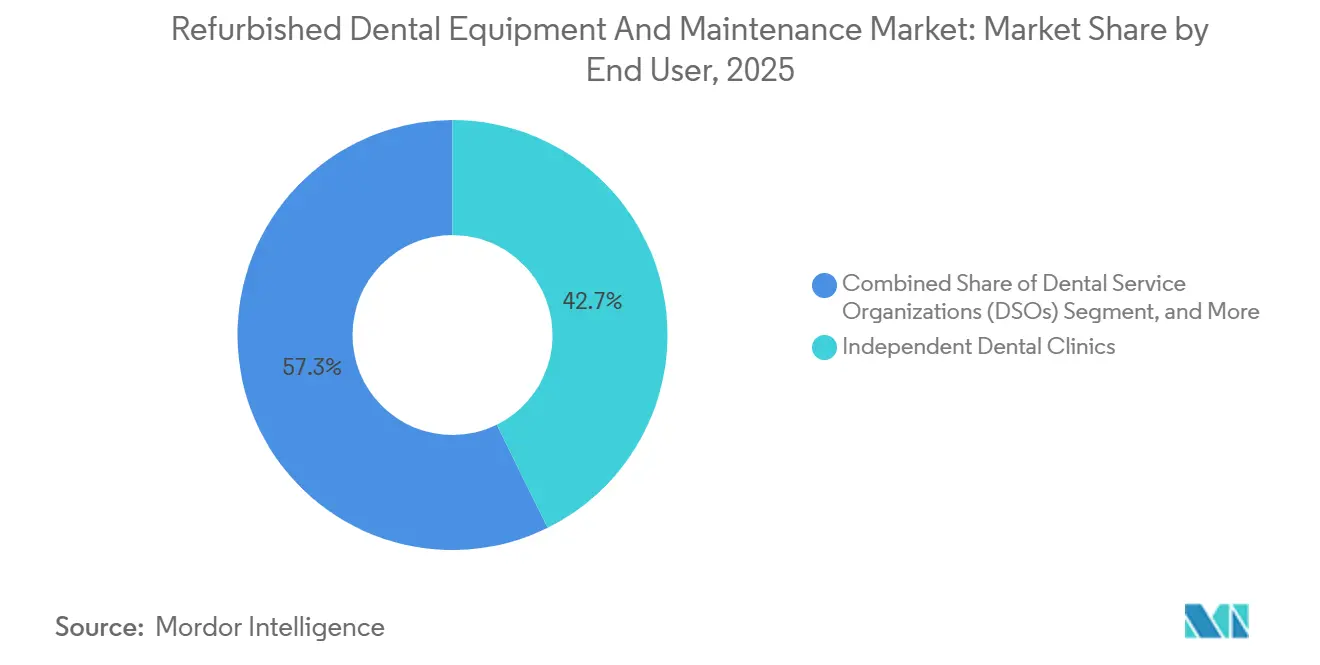

- By end user, independent dental clinics held 42.71% revenue share in 2025, whereas DSOs are poised to grow at an 8.92% CAGR through 2031.

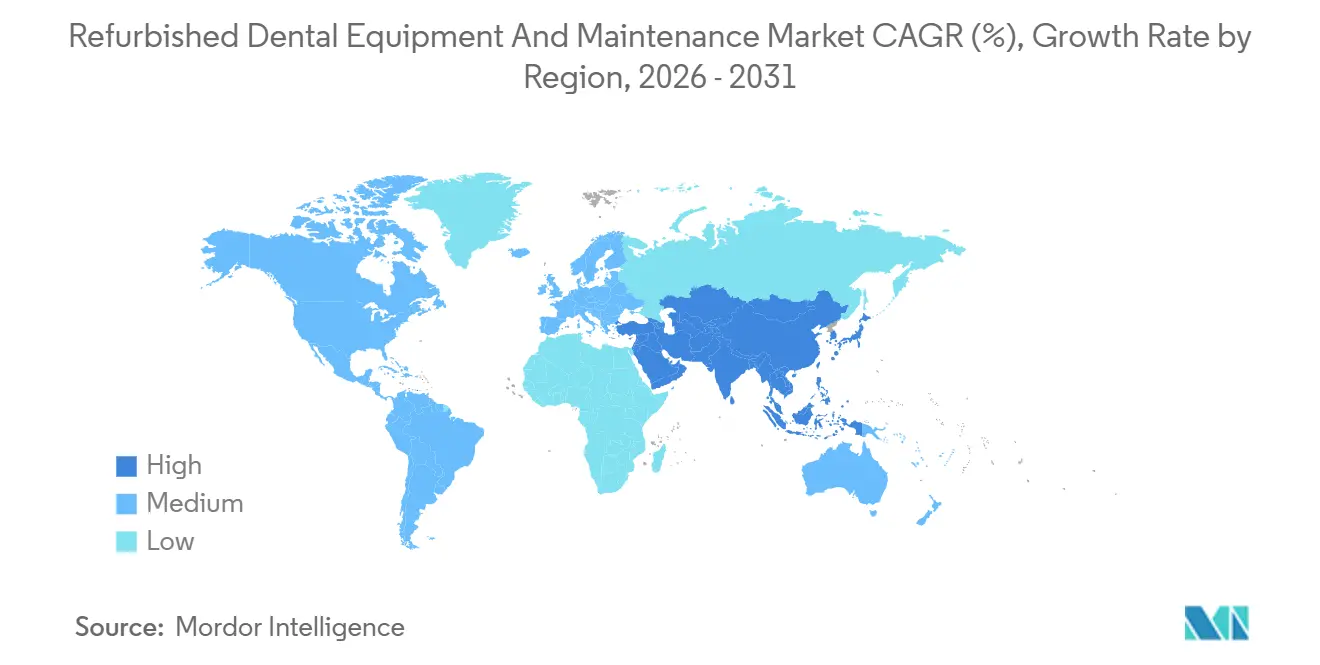

- Geographically, North America captured 39.38% of the value in 2025; Asia-Pacific is projected to expand at a 9.03% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Refurbished Dental Equipment And Maintenance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Cost-Containment Pressure on Small Dental Practices | +2.1% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Growing Circular-Economy Legislation in Europe and United States | +1.8% | Europe core, spillover to North America | Medium term (2-4 years) |

| Rising Adoption of Intra-Oral 3D Scanners in Emerging Markets | +1.3% | Asia Pacific, Latin America | Medium term (2-4 years) |

| Rapid Expansion of Corporate DSOs in Southeast Asia | +1.5% | APAC core, spillover to Middle East & Africa | Short term (≤ 2 years) |

| Surge in Carbon-Neutral Pledges by Dental Manufacturers | +0.9% | Global, led by Europe & North America | Long term (≥ 4 years) |

| AI-Enabled Predictive Maintenance Contracts | +1.2% | North America early adopters, expanding to Europe & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cost-Containment Pressure on Small Dental Practices

Costs for equipment and consumables climbed 5-6% year-on-year in 2025, outstripping general inflation and flattening margins even before wage pressure enters the equation.[1]American Dental Association, “HPI Q4 2025 Survey,” ada.org With reimbursement schedules covering less than half of billed fees in many U.S. states, 55% of dentists named low payer rates as their top threat, and only one in four planned any large capital purchase for 2026. Clinics facing EBITDA compression of USD 150,000-170,000 annually now swap USD 100,000 new scanners for USD 40,000 recertified analogs, freeing cash for hygiene staff and marketing. Similar arithmetic echoes in Canada, where public-plan fees trail provincial schedules by double digits, nudging practices toward group-buying cooperatives. These realities embed the Refurbished Dental Equipment & Maintenance market firmly into standard procurement playbooks, not just recession stopgaps.

Growing Circular-Economy Legislation in Europe and United States

The EU’s Ecodesign for Sustainable Products Regulation mandates Digital Product Passports for all medical devices by July 2026, meaning every chair, sensor, and motor must carry traceable refurbishment data.[2]European Commission, “Ecodesign for Sustainable Products Regulation,” europa.eu Separately, Regulation 2024/1849 already bans mercury amalgam fillings, accelerating intraoral-scanner demand that dovetails with refurbishment economics. France’s AGEC law layers an 85% reused-component threshold onto “Reconditioned Origin France” labels, favoring certified refurbishers over gray-market resellers. U.S. agencies mirror the trend: federal purchasing guidelines now score bids on life-cycle carbon, making refurbished inventory a competitive lever. Combined, these measures lift compliant refurbishers from optional suppliers to mandated partners inside public tender documents.

Rising Adoption of Intra-Oral 3D Scanners in Emerging Markets

A 2026 survey in Vietnam revealed 85-95% intraoral-scanner penetration at top-tier clinics yet only 30-35% nationally, exposing a wide adoption gap.[3]Picasso Dental, “Vietnam Dental Technology Survey 2026,” picassodental.vn Refurbished scanners priced at USD 8,000-12,000 slash entry barriers versus USD 25,000 new units, opening mid-tier practices to same-day crown workflows that erase external lab fees. Clinics in India, Indonesia, and the Philippines report similar math, spurred by rising dental-tourism flow from budget-conscious outbound patients. As digital workflows remove gypsum impressions, practices also chip away at landfill waste, aligning with national sustainability pledges and reinforcing the equipment’s value proposition.

Rapid Expansion of Corporate DSOs in Southeast Asia

Q&M Dental Group raised USD 130 million in August 2025 to fund regional roll-ups, aiming for 300 Singapore clinics within five years. Oracare Group doubled its Thai footprint to 30 sites and lifted group profit margins to 22% by pooling procurement across 62 clinics. DSOs capitalize on uniform layouts, ordering refurbished chairs and CBCT units in bulk at 30-60% discounts and locking in five-year full-service contracts that guarantee uptime. Beyond procurement leverage, multi-site chains can share surplus equipment between locations, maximizing utilization and shrinking payback periods for refurbished assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived Infection-Control Risks Post-COVID-19 | -0.8% | Global, heightened in Asia Pacific | Short term (≤ 2 years) |

| Limited OEM Warranty and Certification Frameworks | -1.1% | Global, acute in APAC & Latin America | Medium term (2-4 years) |

| Fragmented Regulatory Definitions Across APAC | -0.9% | Asia Pacific | Long term (≥ 4 years) |

| Shortage of Specialized Biomedical Technicians | -0.7% | Global, severe in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Perceived Infection-Control Risks Post-COVID-19

Systematic reviews remain inconclusive on whether reprocessed single-use devices elevate risk, but perception, not evidence, often drives buyer hesitation. Infection-control committees worry that microcracks in refurbished upholstery trap biofilms that survive autoclave cycles. Refurbishers now counter with third-party sterilization-validation certificates, video walkthroughs of teardown steps, and surface-integrity guarantees. Despite these assurances, heightened vigilance in Asia keeps some practices on the fence, slightly tempering otherwise robust uptake.

Limited OEM Warranty and Certification Frameworks

A-dec’s three-year parts warranty on certified chairs contrasts sharply with the six-month parts-only coverage many third-party refurbishers offer, breeding uncertainty among risk-averse clinics. Regulatory bodies in China and Japan require refurbishers to carry near-OEM documentation, raising entry barriers and handling-time costs. Where certification is ambiguous, buyers often negotiate extended service contracts or demand escrow holdbacks until performance milestones are met, nudging refurbishers toward stricter quality-management systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Imaging Systems Remain the Anchor, Digital Workflows Propel CAD/CAM

Imaging Systems held 36.62% Refurbished Dental Equipment & Maintenance market share in 2025, underscoring persistent demand for CBCT and panoramic devices that cost well over USD 100,000 new, versus roughly 40% of that sticker price when recertified. Recertified imaging proves attractive even for academic centers that need multiple training units but lack capital allocations for new hardware.

The CAD/CAM & 3-D Printing category is pacing at an 8.98% CAGR, propelled by clinics racing to offer same-day crowns and eliminate outsourcing fees. Vietnam’s top-tier facilities already log 85-95% usage, a bellwether for adoption curves across Indonesia, Thailand, and the Philippines where only about one-third of practices have converted. Digital workflows also dovetail with green-procurement narratives, as scanners replace gypsum models and single-use trays.

Dental Chairs & Delivery Units see steady demand from DSOs standardizing operatory layouts. Bulk refurbished chairs sell at 30-50% below new, allowing chains to open de-novo sites on thinner capital budgets. Handpieces & Accessories exhibit shorter three-to-five-year cycles; however, limited warranty parity slows refurbishment uptake, particularly for high-speed turbines that face FDA scrutiny over retipping alterations.

Sterilization & Infection Control units gained heightened attention post-pandemic. Although autoclaves are complex electro-mechanical devices, refurbishers that document full pressure-cycle recalibrations and gasket replacement win contracts in cost-sensitive community clinics. Lighting & Monitor Arms remain small, yet integrators often throw them into refurb bundles to increase deal value with minimal added overhead.

By Service Type: Preventive Maintenance Dominates but Full-Service Contracts Gain Speed

Preventive protocols captured 44.38% refurbished dental equipment & maintenance market size in 2025, reflecting clinics’ push to milk every extra year from chairs and sensors. Standard kits include annual IEC 62353 electrical checks, lubrication, and software patches.

Corrective or break-fix visits still account for emergency calls averaging USD 6,000, though AI predictive platforms are poised to shrink that pie. Calibration & Validation work, mandatory for X-ray generators under FDA 21 CFR 820, delivers recurring margin to service firms that bundle annual image-quality testing.

Full-Service Contracts, while starting from a smaller base, should climb 9.35% CAGR through 2031. Darby’s TotalOp and similar bundles roll equipment sensors, remote monitoring, parts, and labor into fixed monthly fees, improving cost certainty for DSOs juggling dozens—or hundreds—of sites. Some programs layer cybersecurity patches for networked devices, satisfying GDPR and HIPAA audit trails in one swing.

By End User: Fragmented Independents Lead Today, DSOs Reshape Tomorrow

Independent Dental Clinics retained 42.71% share in 2025, but many now join buying cooperatives or informal alliances to secure DSO-like pricing. With solo practitioners still representing the majority of owners in North America and Europe, refurbishment remains an attractive hedge against flat reimbursement.

DSOs, forecast to post an 8.92% CAGR, lean on scale to squeeze suppliers and standardize operatories. Q&M Dental Group’s SGD 34 million profit-guarantee acquisition in March 2026 exemplifies confidence in margin lift through centralized refurbishment procurement. Dental Hospitals lag due to tighter accreditation hurdles, yet satellite clinics inside teaching networks increasingly fit recertified CBCT units where case volumes do not justify new devices. Academic & Research Institutes selectively buy refurbished benches and phantom heads for simulation labs, reserving new gear for flagship clinics where manufacturer partnerships fund the latest technology.

Geography Analysis

North America generated 39.38% of global revenue in 2025 as inflation-adjusted reimbursement stagnated, prompting clinics to stretch budgets with refurbished chairs and imaging units. Canada’s public dental-care rollout added patients but shaved fee schedules by up to 15%, a margin hit offset by DSOs sourcing recertified equipment at half the new price.

Europe progresses steadily on the back of Circular Economy Action Plan milestones. From July 2026, Digital Product Passports will become mandatory, effectively turning compliant refurbishers into preferred vendors for public tenders. France’s AGEC rules amplify this demand with strict reused-component ratios, nudging gray-market traders out of contention.

Asia-Pacific is the fastest mover, set for a 9.03% CAGR through 2031. DSOs mushroom across Singapore, Malaysia, Indonesia, and China, pooling orders for 40-60% discounts on refurbished CBCTs and CAD/CAM blocks. Regulatory fragmentation raises transaction friction, but large refurbishers absorb extra compliance costs and still undercut new-equipment sticker prices.

South America and the Middle East & Africa trail in absolute dollars yet register double-digit unit gains off a small base. Henry Schein’s stake acquisitions in Brazil signal distributor appetite to build early dominance before OEM recertification programs proliferate. Technician shortages and customs hurdles remain real, yet the allure of 50% capex savings is hard to ignore in price-sensitive, cash-based markets.

Competitive Landscape

Competition is moderately fragmented. OEM-certified programs from A-dec, Henry Schein, and Dentsply Sirona coexist with specialist refurbishers like Atlas Resell Management and Dental Planet. A-dec’s three-year parts warranty differentiates it from independents that normally extend six-to-twelve-month coverage, easing buyer risk when infection-control committees demand OEM signatures.

Henry Schein Outlet recertifies units through manufacturer-trained technicians, leaning on a 5.3-million-square-foot logistics network to ship same-day replacements and parts. Dentsply Sirona, after USD 650 million in 2025 goodwill write-offs, tightened distribution deals with Patterson, Benco, and Burkhart to protect its installed base.

Envista Holdings, parent to Nobel Biocare and DEXIS, posted double-digit revenue gains in late 2025, lifted by refurbished sensor packages that bundle AI-driven monitoring analytics. Technology leadership matters: Planmeca and Carestream Dental launched predictive maintenance in 2024, while Henry Schein embedded TechCentral network diagnostics in 2025 units. Disruptors like Viva AI integrate scheduling, patient communication, and equipment health in unified dashboards, selling data-rich service plans rather than hardware alone.

OEM programs hold an advantage in tightly regulated markets that require ISO 13485 and MDR certificates; independents thrive where oversight gaps allow faster turnarounds. Overall, the five largest suppliers control roughly 40-45% of global refurbished revenue, indicating moderate concentration with room for regional specialists to carve profitable niches.

Refurbished Dental Equipment And Maintenance Industry Leaders

Envista Holdings

Carestream Dental

Dentsply Sirona

Planmeca Oy

Henry Schein Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Darby Dental Supply, DentalEZ, and UptimeHealth launched the TotalOp subscription service, embedding Aeras predictive technology that monitors equipment sensors in real time, issues failure alerts 7-14 days in advance, and bundles parts, labor, and software updates into a single monthly payment, targeting practices seeking to reduce unplanned downtime by 67%.

- February 2026: Dentsply Sirona expanded its distribution partnership with Burkhart Dental Supply to include dental technology equipment, complementing existing agreements with Patterson Dental, Benco Dental, and A-dec, as the company navigates USD 650 million in goodwill impairments and restructuring targeting USD 120 million in annualized cost savings.

- June 2025: AAMI and UptimeHealth partnered to host a Dental Fix pavilion at the 2026 eXchange conference, spotlighting solutions to the U.S. biomedical technician shortage, which constrains refurbished-equipment adoption by lengthening repair lead times and raising service-contract premiums

- April 2025: Ormco and DentalMonitoring announced a partnership to deliver AI-powered remote monitoring and Smart STL integration for orthodontic workflows, demonstrating cross-specialty adoption of predictive-maintenance technologies that extend equipment lifespans and improve patient outcomes.

Global Refurbished Dental Equipment And Maintenance Market Report Scope

The refurbished dental equipment and maintenance market comprises the sale, repair, and servicing of pre-owned dental devices (e.g., chairs, X-rays, scanners) that are restored to full functionality, safety, and performance standards, often at lower cost than new items. This market helps clinics improve affordability and access high-quality equipment.

The refurbished dental equipment & maintenance market report is segmented by equipment type, service type, end user, and geography. By equipment type, the market is segmented into imaging systems, dental chairs & delivery units, handpieces & accessories, CAD/CAM & 3D printing systems, sterilization & infection control, and lighting & monitor arms. By service type, the market is segmented into preventive maintenance, corrective/repair service, calibration & validation, and full-service contracts. By end user, the market is segmented into dental hospitals, independent dental clinics, dental service organizations (DSOs), and academic & research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Imaging Systems |

| Dental Chairs & Delivery Units |

| Handpieces & Accessories |

| CAD/CAM & 3-D Printing Systems |

| Sterilization & Infection Control |

| Lighting & Monitor Arms |

| Preventive Maintenance |

| Corrective / Repair Service |

| Calibration & Validation |

| Full-Service Contracts |

| Dental Hospitals |

| Independent Dental Clinics |

| Dental Service Organizations (DSOs) |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Equipment Type | Imaging Systems | |

| Dental Chairs & Delivery Units | ||

| Handpieces & Accessories | ||

| CAD/CAM & 3-D Printing Systems | ||

| Sterilization & Infection Control | ||

| Lighting & Monitor Arms | ||

| By Service Type | Preventive Maintenance | |

| Corrective / Repair Service | ||

| Calibration & Validation | ||

| Full-Service Contracts | ||

| By End User | Dental Hospitals | |

| Independent Dental Clinics | ||

| Dental Service Organizations (DSOs) | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the refurbished dental equipment & maintenance market be by 2031?

The refurbished dental equipment & maintenance market size is forecast to reach USD 1.63 billion by 2031, growing at an 8.15% CAGR.

Which equipment category contributes the most revenue?

Imaging systems led with 36.62% refurbished dental equipment & maintenance market share in 2025, largely because CBCT and panoramic units carry high new-purchase prices.

What segment is growing the fastest?

CAD/CAM & 3-D printing systems are projected to expand at an 8.98% CAGR through 2031 as clinics adopt same-day crown workflows.

Which service model is gaining traction?

Full-service contracts should post a 9.35% CAGR between 2026 and 2031 thanks to AI-driven predictive maintenance that bundles parts, labor, and software.

Why is Asia-Pacific considered the most promising region?

Asia-Pacific is set for a 9.03% CAGR because DSOs are consolidating practices, raising capital, and ordering refurbished equipment in bulk, especially in Singapore, Malaysia, and China.

Page last updated on: