Refrigerated Display Cases Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

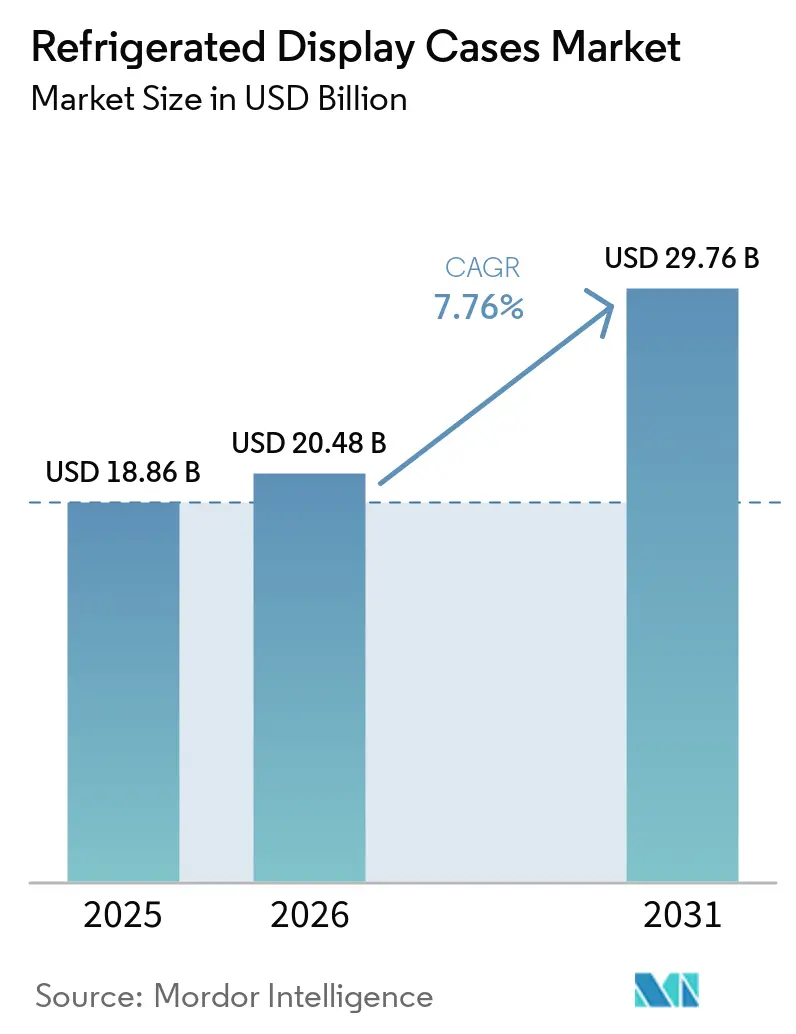

| Market Size (2026) | USD 20.48 Billion |

| Market Size (2031) | USD 29.76 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refrigerated Display Cases Market Analysis by Mordor Intelligence

The refrigerated display cases market size is projected to expand from USD 18.86 billion in 2025 and USD 20.48 billion in 2026 to USD 29.76 billion by 2031, registering a CAGR of 7.76% between 2026 and 2031. Growth in the refrigerated display cases market is being shaped by a replacement cycle that is now tied more closely to compliance deadlines than to optional store upgrades. Regulatory changes in the United States and Europe are pushing operators to replace older equipment more quickly, creating a stronger demand base across food retail, foodservice, and convenience channels. Store modernization is adding to that demand as retailers redesign layouts around fresh food, frozen items, and grab-and-go assortments that need stronger chilled visibility. The refrigerated display cases market is also benefiting from a broader shift in merchandising, as restaurants, cafés, and hotels increasingly use front-of-house chilled displays to support packaged meal sales. Competitive positioning is increasingly centered on natural refrigerants, energy performance, digital monitoring, and service capabilities, leaving room for suppliers that can support both retrofit demand and new-format store builds.

Key Report Takeaways

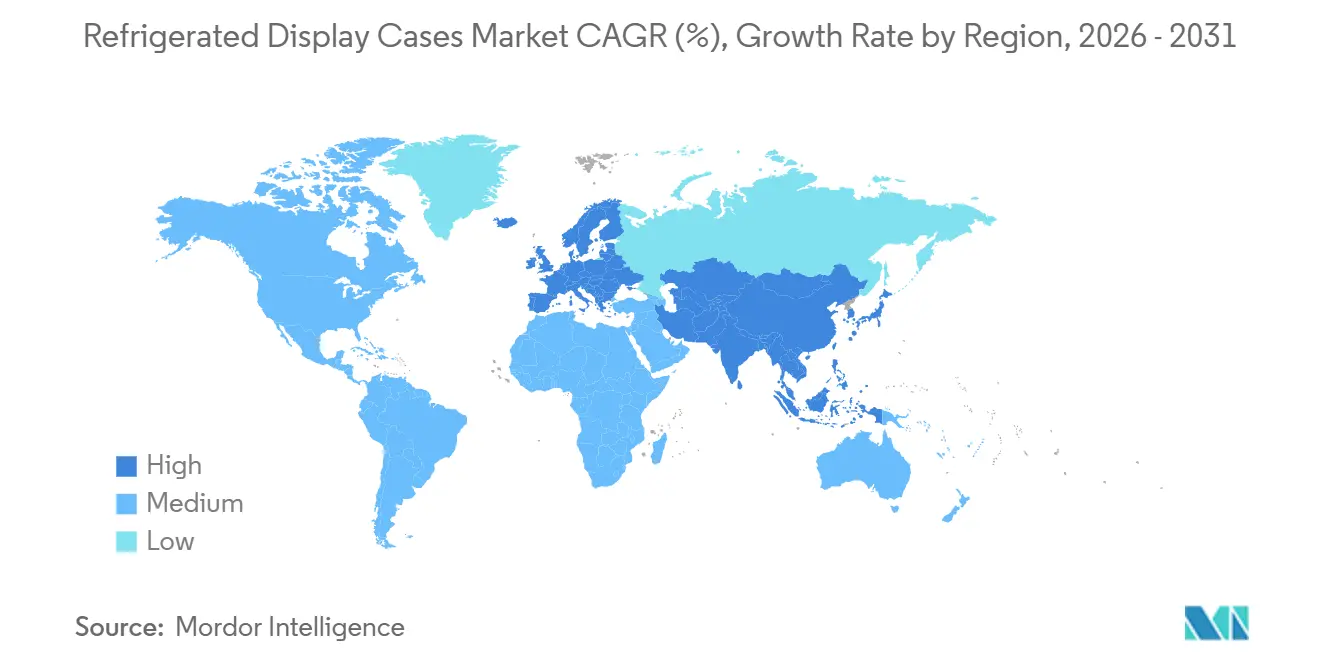

- By geography, Europe led the refrigerated display cases market with 39.41% share in 2025, while Asia-Pacific is projected to expand at 8.73% CAGR through 2031.

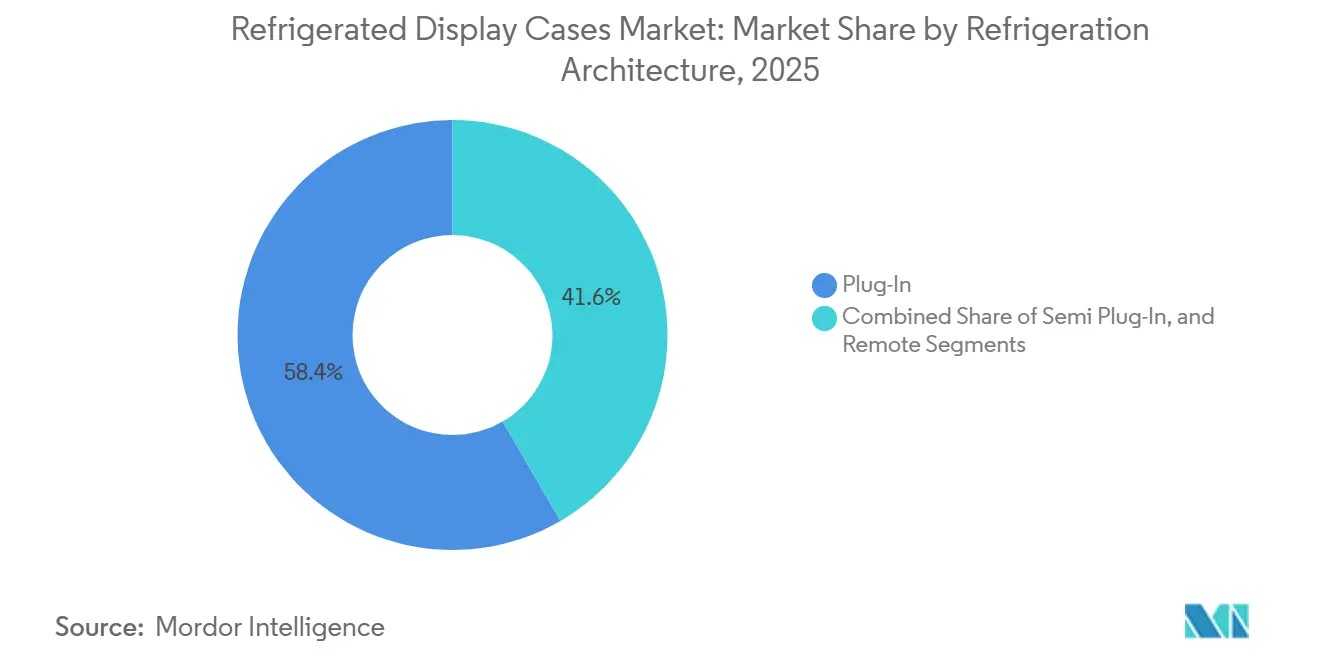

- By refrigeration architecture, plug-in cases held 58.37% of the refrigerated display cases market share in 2025, while remote systems are projected to grow at 8.34% CAGR through 2031.

- By product design, vertical cases accounted for 55.12% of the refrigerated display cases market size in 2025, while hybrid configurations are projected to expand at 8.56% CAGR through 2031.

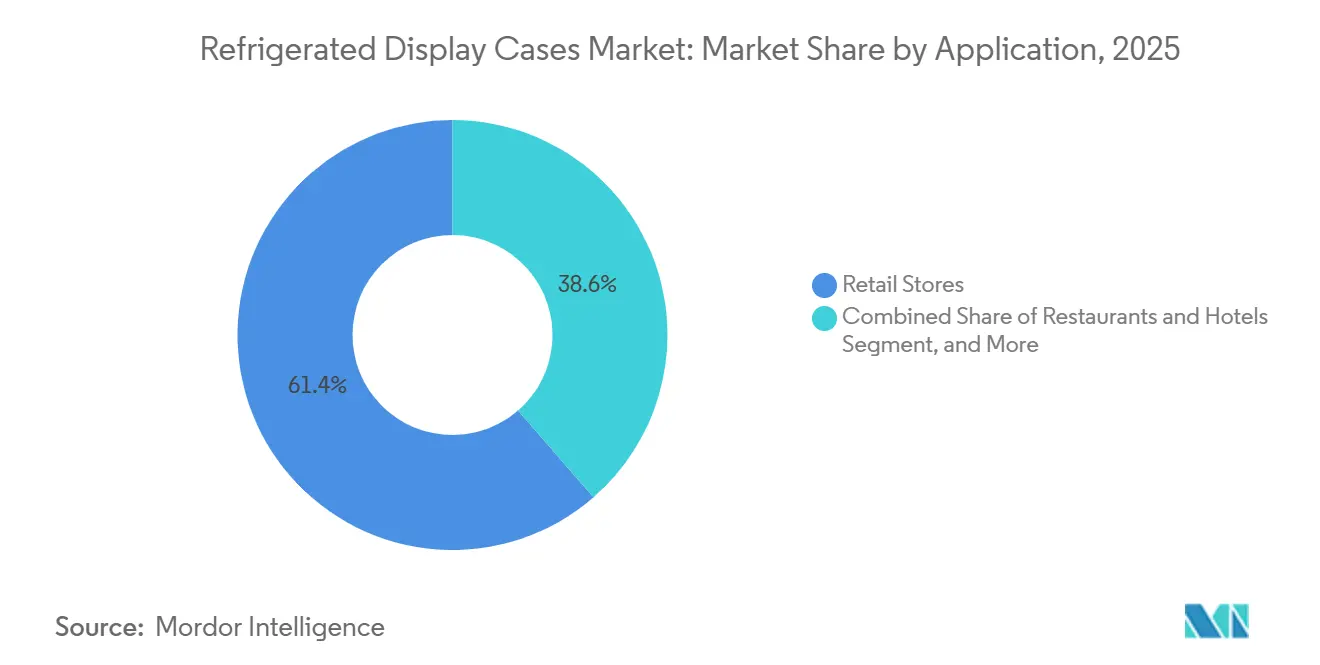

- By application, retail food and beverage outlets captured 61.39% of the market share in 2025, while restaurants and hotels are expected to record the highest CAGR of 8.28% through 2031.

- By end user, supermarkets and hypermarkets held 67.93% share in 2025, while convenience stores are projected to grow at 9.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Refrigerated Display Cases Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail Chain Refurbishment and Convenience Store Expansion | +2.0% | Global, with strongest effect in North America, Asia-Pacific, and Europe | Short term (≤ 2 years) |

| Natural Refrigerant and Energy-Efficiency Retrofit Cycle | +1.7% | North America and Europe, with spillover to core Asia-Pacific markets | Short term (≤ 2 years) to Medium term (2-4 years) |

| Fresh, Frozen, and Grab-and-Go Food Merchandising Growth | +1.4% | Global, led by North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Smart Monitoring and Predictive Maintenance Adoption | +0.8% | Global, with Asia-Pacific leading IoT deployment pace | Medium term (2-4 years) |

| Omnichannel Grocery Pickup and Micro-Fulfillment Chilled Staging | +0.6% | North America and Western Europe, with early adoption in China | Medium term (2-4 years) |

| Premium Fresh Food Perimeter Remodeling | +0.4% | Western Europe, North America, Japan, and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Retail Chain Refurbishment and Convenience Store Expansion

Retail modernization programs are extending demand for refrigerated display cases beyond a typical replacement cycle. Convenience stores are allocating more floor space to prepared meals, packaged beverages, and chilled foodservice, which raises the number of cases needed in each remodeled outlet. C-store foodservice accounted for 28.5% of total in-store sales in 2025, up from 11.9% in 2005, and contributed 38.9% of in-store gross profit, underscoring why operators are redesigning stores around chilled food visibility. Love's Travel Stops committed USD 700 million in 2026 to open 20 locations and remodel 35 existing sites under its Road Ahead Plan, with a stronger food-and-beverage offer at the center of the program. In the refrigerated display cases market, that pattern matters because a food-led convenience format typically needs more linear chilled frontage than a legacy fuel-centered layout. This is keeping demand active in both new openings and store refresh work.

Natural Refrigerant and Energy-Efficiency Retrofit Cycle

The refrigerated display case market is undergoing a replacement wave driven by refrigerant rules rather than discretionary spending. Regulation (EU) 2024/573 took effect in March 2024 and tightened the phasedown path for fluorinated greenhouse gases across the European Union.[1]European Commission, “Regulation (EU) 2024/573 of the European Parliament and of the Council on Fluorinated Greenhouse Gases,” Official Journal of the European Union, climate.ec.europa.eu In the United States, newer federal rules have pushed the sector toward lower-global-warming-potential refrigerants in new commercial refrigeration equipment, thereby shortening the replacement window for older HFC-based systems. The EPA also raised the R290 charge limit for self-contained display cases in 2024, which widened the use case for propane-based plug-in systems in larger footprints than before. Between 2025 and 2029, U.S. food retailers planned to install 1,470 new transcritical CO₂ stores and replace 13,400 existing systems, which shows how large the transition pipeline has become. In the refrigerated display cases market, these compliance deadlines are serving as a floor for demand, as operators cannot indefinitely defer equipment decisions.

Fresh, Frozen, and Grab-and-Go Food Merchandising Growth

Fresh, grab-and-go assortments are changing how space is planned in the refrigerated display cases market. Retailers are giving more room to perimeter departments, ready meals, chilled snacks, and visible beverage lines because these categories support both traffic and basket value. H Mart retrofitted 1,500 linear feet of refrigerated case doors at 5 California locations and projected nearly USD 300,000 in annual electricity savings across those stores, which shows how merchandising and energy savings are now being addressed together. Tops Friendly Markets also used a flagship remodel to expand fresh produce, seafood, and grab-and-go areas, installing high-efficiency, self-contained units selected for upcoming refrigerant compliance. This pattern is important for the refrigerated display cases market because case demand rises when retailers expand chilled assortment depth rather than only replace like-for-like units. It also favors suppliers that can combine visibility, energy performance, and flexible store placement.

Smart Monitoring and Predictive Maintenance Adoption

Digital monitoring is becoming harder to separate from case selection in the refrigerated display cases market. Operators are facing higher service complexity as natural refrigerants spread, while the technician base remains tight in several developed markets. Predictive maintenance platforms have shown reductions of 30-50% in unplanned downtime and 60-75% in emergency repair calls, which is meaningful because emergency service events are far more expensive than scheduled maintenance visits. Fujitsu and Beisia began rolling out IoT temperature monitoring across all 138 Beisia supermarket stores in Japan, replacing manual temperature checks for an average of 150 refrigeration units per store. In the refrigerated display cases market, that shift is steering procurement toward connected units that can feed into broader store operations platforms. It is also helping premium case suppliers protect pricing by tying hardware to service and data tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Retrofit and Installation Costs | -1.4% | Global, most acute in SME-dominated retail markets in South America, Africa, and South Asia | Short term (≤ 2 years) to Medium term (2-4 years) |

| Energy and Lifecycle Service Cost Burden | -0.9% | Global, with compounding effect in high-ambient climates such as the Middle East, South Asia, and West Africa | Medium term (2-4 years) |

| Technician Shortage for CO₂, R290, and A2L Systems | -0.6% | North America and Northern Europe, with spillover to Asia-Pacific as natural refrigerant adoption grows | Short term (≤ 2 years) to Medium term (2-4 years) |

| High-Ambient and Grid-Volatility Performance Risk | -0.3% | Middle East, Sub-Saharan Africa, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Retrofit and Installation Costs

Capital costs remain a direct brake on adoption in the refrigerated display case market, especially for smaller operators. Transcritical CO₂ systems can cost 10-20% more than conventional HFC systems in new builds, and retrofit projects often require additional infrastructure work, widening the gap further.[2]North American Sustainable Refrigeration Council, “Food Retailer Survey Report, Understanding the Food Retail Industry's Current and Future Refrigerant Use,” NASRC, nasrc.org That burden becomes harder to absorb when operators are also funding store remodels, energy upgrades, and refrigerant compliance in the same planning cycle. New York State awarded USD 350,000 to support 2 Bronx Key Food stores in shifting to R290 cases, demonstrating that public support is already helping smaller retailers cover the economic costs. In the refrigerated display cases market, this favors large chains that can spread transition costs across bigger store networks and longer capital programs. It also slows conversion in fragmented retail environments where stores lack scale purchasing power.

Energy and Lifecycle Service Cost Burden

The refrigerated display cases market also faces pressure from service and operating costs that extend well beyond the initial equipment purchase. Commercial refrigeration accounts for more than 60% of energy consumption in a typical grocery or convenience store, so case efficiency has a significant impact on store economics. H Mart's retrofit program at 5 California stores projected nearly USD 300,000 in annual electricity savings, which highlights how costly older case estates can be when left in place. At the same time, newer CO₂ and R290 systems often need specialized parts, longer service calls, and technicians with narrower skill sets. The North American Sustainable Refrigeration Council highlighted the labor gap in the commercial refrigeration workforce, which adds to cost pressures in installation and maintenance planning. In the refrigerated display cases market, those lifecycle burdens make total cost of ownership a more important buying factor than headline equipment price alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Refrigeration Architecture: Plug-In Leadership With Remote CO₂ Expansion

Plug-in refrigerated display cases held 58.37% of the market share in 2025, maintaining their position as the largest architecture segment in the refrigerated display cases market. Their lead reflects the deep installed base of self-contained units across convenience stores, bakeries, specialty retailers, and smaller grocery formats. Plug-in systems remain the default choice in many retrofit projects because they are easier to install and do not require a centralized refrigeration plant. The 2024 increase in EPA charge limits for R290 self-contained cases widened the range of store formats that propane-based plug-in units can serve, which strengthened the case for replacement in smaller and medium-sized outlets.

Remote systems are projected to grow at a 8.34% CAGR from 2026 to 2031, making them the fastest-growing architecture in the refrigerated display cases market. Growth is being driven by new supermarket builds and large remodel programs that favor centralized CO₂ racks for broader temperature control and system integration. Food Lion's late-2025 remodel program in the Charlotte region included CO₂-based cooling systems in select stores, which shows how large chains are pairing store renewal with refrigerant transition. Semi plug-in systems continue to occupy the middle ground, especially in European retail, where heat recovery and waterloop layouts support medium-format stores that need more flexibility than a full remote setup. The refrigerated display cases industry is therefore splitting more clearly between retrofit-friendly plug-in units and chain-led remote builds.

By Product Design: Vertical Formats Hold Scale While Hybrid Models Gain Momentum

Vertical cases accounted for 55.12% share in 2025 and remained the core design format across the refrigerated display cases market. Their position comes from strong use in dairy, fresh food, beverage, and perimeter merchandising, where shelf visibility and broad SKU display are critical. Epta's Zenith line, launched in 2026, delivered up to 36% energy savings compared to prior models while expanding the display area by up to 13%, demonstrating how vertical cabinets improve both efficiency and sales performance. That combination helps vertical formats defend their lead as retailers look for higher productivity from existing floor space.

Hybrid configurations are projected to expand at a 8.56% CAGR through 2031, making them the fastest-growing design segment in the refrigerated display cases market. Retailers are showing more interest in mixed-display formats that can combine open and closed presentation within a single run while improving energy control. Horizontal cases continue to serve freezer chest and ice cream applications, and AHT's KIGALI XL launch in late 2024 demonstrated continued product development focused on visibility and R290-based performance in that market segment. Hybrid growth is important because it reflects retailer demand for fewer separate case lines across the store and better flexibility in category placement. In the refrigerated display case industry, design competitions are now centered less on simple form factors and more on how each cabinet layout supports both energy savings and merchandising quality.

By Application: Retail Volume Base With Faster Foodservice Uptake

Retail stores captured 61.39% of the market share in 2025 and remained the volume anchor of the refrigerated display cases market. Demand in this application remains high, but the mix is shifting away from pure new-store supply toward remodel and retrofit replacements in mature grocery markets. That shift is especially visible in North America and Western Europe, where store counts are more stable, but case estates are aging into replacement cycles. The refrigerated display cases market is therefore drawing steady support from established retail networks that need to upgrade equipment to comply with regulations, reduce energy use, and implement layout changes.

Restaurants and hotels are projected to grow at a 8.28% CAGR through 2031, making them the fastest-growing application in the refrigerated display cases market. This increase reflects the spread of front-of-house chilled displays for grab-and-go meals, packaged desserts, drinks, and pre-prepared food that blur the line between foodservice and retail. The model works because chilled display units allow operators to add impulse sales without expanding full kitchen throughput, thereby improving revenue per square foot. Other applications, such as hospitals, airports, and sports venues, are also widening chilled merchandising footprints, although their procurement cycles are longer and more centralized than in retail. Across the refrigerated display cases market, that means foodservice-led demand is becoming more structurally important rather than remaining a niche add-on.

By End User: Supermarkets Stay Central While Convenience Stores Drive Faster Growth

Supermarkets and hypermarkets accounted for 67.93% of the market in 2025, making them the largest buyer group in the refrigerated display cases market. Their importance comes not only from scale but also from the age of the installed base, as many units placed during the supermarket expansion phase of the 2010s are now approaching replacement. The U.S. Department of Energy noted an average commercial case lifespan of 14 years, which supports a sizable baseline replacement cycle through the forecast period. In the refrigerated display cases market, this gives supermarkets a durable role even when headline store expansion slows.

Convenience stores are projected to grow at a 9.56% CAGR from 2026 to 2031, making them the fastest-growing end-user segment in the refrigerated display cases market. Yesway's five-year expansion plan filed in early 2026 included 130 new stores through 2031 and larger floor plans than its legacy standard, which supports a higher refrigerated case count per location. Large operators are also scaling the opportunity through remodels and acquisitions, with 7-Eleven planning more than 7,000 North American remodels through 2030 and Alimentation Couche-Tard targeting 750-plus additional stores over the following five years from 2026. Specialty stores, discount outlets, fuel stations, and HoReCa buyers remain smaller but stable demand pools for the refrigerated display cases market. The balance of growth is therefore shifting toward convenience-led formats, even though supermarkets still account for the largest share of purchases.

Geography Analysis

Europe held 39.41% of the refrigerated display cases market share in 2025, making it the largest regional contributor. The region's lead reflects a dense supermarket base and an earlier move into CO₂ refrigeration, supported by tighter environmental rules than in most other markets. Regulation (EU) 2024/573 strengthened the phase-out path for fluorinated greenhouse gases and is forcing operators across the European Union to bring forward system replacement plans.[3]European Commission, “Regulation (EU) 2024/573 of the European Parliament and of the Council on Fluorinated Greenhouse Gases,” Official Journal of the European Union, climate.ec.europa.eu That policy backdrop is being reinforced by store refresh activity, including projects such as Waitrose Coulsdon's 2025 refrigeration replacement and store update, which linked system renewal with broader modernization work.

Asia-Pacific is projected to grow at a 8.73% CAGR through 2031, making it the fastest-growing region in the refrigerated display cases market. Urbanization, the expansion of convenience retail, and continued investment in cold chain infrastructure are driving broader demand across China, India, South Korea, and Southeast Asia. South Korea's convenience store base has entered a quality-upgrade phase, with operators replacing older units with inverter-based, high-efficiency display cases at conversion rates above 70%. India is also emerging as a stronger demand center, with domestic commercial refrigeration growth supported by organized retail expansion and supplier investments such as Elanpro's 2025 experience center initiative.

North America remained the second-largest regional market and a key battleground for natural refrigerant adoption in the refrigerated display cases market. The United States entered a more binding compliance phase when new federal restrictions on higher-GWP refrigerants in self-contained installations took effect in January 2025 and were further extended to remote condensing applications in January 2026. Large retailers, including Kroger, ALDI, Whole Foods, and Walmart, have already aligned their new-store refrigeration strategy with CO₂ transcritical adoption, which is tightening the direction of travel for the region. South America is supported more by organized retail expansion and imported plug-in units, while the Middle East remains constrained by high ambient conditions that are less favorable to standard CO₂ transcritical designs. Africa is still at an earlier stage of cold chain development, but Frigoglass's Egypt expansion, with a target of 100,000 units of annual production through its partnership with Fresh S.A.E, points to a longer-term growth position for the refrigerated display cases market in the region

Competitive Landscape

The refrigerated display cases market remains moderately fragmented, with a strong European manufacturer group led by Epta S.p.A., Arneg S.p.A., and AHT Cooling Systems GmbH, while North American suppliers such as Hill PHOENIX, Inc., and True Manufacturing Co., Inc. hold meaningful positions through refrigerant expertise and channel reach. Epta strengthened that position in early 2026 when it completed the acquisition of Hauser GmbH, creating a group with more than EUR 2 billion in revenue (approximately USD 2.26 billion) and a wider footprint across DACH and Central and Eastern Europe. That move reflects how scale is becoming more valuable in the refrigerated display cases market, as large grocery customers increasingly want full project capability rather than a narrow cabinet-supply relationship. It also raises pressure on mid-sized independent players that lack comparable engineering, service, and regional depth.

Consolidation is also accelerating in North America through targeted acquisitions across adjacent refrigeration categories in the refrigerated display cases market. AeriTek Global Holdings added Due North in 2025, Federal Industries in March 2026, and Continental Refrigerator in April 2026, thereby building a broader platform across front-of-house displays, back-of-house reach-ins, and foodservice refrigeration.[4]AeriTek Global Holdings LLC, “AeriTek Acquires Federal Industries, Significantly Bolstering U.S. Presence,” AeriTek, aeritekna.com Hoshizaki also expanded its food display case exposure through the 2025 acquisition of Structural Concepts Corporation, which added U.S. display capabilities to its broader refrigeration portfolio. These deals show that portfolio breadth now matters more in the refrigerated display cases market because customers often procure display, storage, and service support together. They also suggest that there is likely greater overlap between supermarket-focused and foodservice-focused equipment suppliers.

Technology is becoming a stronger point of separation than price alone in the refrigerated display cases market. Hill PHOENIX launched its Next Generation Flex Mini CO₂ transcritical system in 2026, with design changes aimed at reducing service time and improving maintenance, directly addressing technician-cost pressure for operators. Frigoglass moved further into smart retail in late 2025 through its partnership with NU!, combining sensors, cameras, and cloud-based transaction tools with cooler hardware. TEFCOLD continued to broaden its product line in 2026 with new cooler launches for fresh meat, dairy, and beverage applications, underscoring the importance of broader catalog coverage even as digital capabilities rise. Overall, the refrigerated display cases market is moving toward a structure where scale, refrigerant transition readiness, service reach, and connected hardware capabilities matter more than simple cabinet supply.

Refrigerated Display Cases Industry Leaders

Epta S.p.A.

Arneg S.p.A.

Metalfrio Solutions S.A.

AHT Cooling Systems GmbH

ISA S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hillphoenix confirmed plans to launch water-cooled R290 display cases in the second half of 2026 as an extension of its SoloChill micro-distributed line, targeting urban and high-rise retail formats, with next-generation CO₂ condensing units also scheduled for late summer 2026.

- April 2026: AeriTek Global Holdings completed the acquisition of Continental Refrigerator and National Comfort Products from National Refrigeration and Air Conditioning Products, its third North American commercial refrigeration acquisition in under 8 months, thereby establishing a combined platform spanning front-of-house display and back-of-house food-preparation refrigeration.

- April 2026: Epta S.p.A. launched the Zenith line of positive vertical refrigerated cabinets, developed under the Costan and Bonnet Névé brands, at EuroShop 2026, featuring up to 36% energy savings versus prior-generation models, EU Energy Class B certification, 100% natural refrigerants, PFAS-free insulation, and full integration with the SwitchOn remote monitoring platform.

- April 2026: True Manufacturing Co., Inc. entered into a service collaboration with Nationwide Refrigeration, Inc. to strengthen commercial refrigeration and HVAC support for restaurant and grocery operators in the Washington, D.C., Maryland, and Virginia region, focusing on preventive maintenance and diagnostics for walk-in coolers, glass-door merchandisers, and prep tables.

Global Refrigerated Display Cases Market Report Scope

The Refrigerated Display Cases Market refers to the global industry that designs, manufactures, distributes, installs, and commercializes temperature-controlled display equipment used to store, preserve, merchandize, and present perishable food and beverage products in retail and foodservice environments. Refrigerated display cases are specialized refrigeration systems designed to maintain controlled cooling conditions while maximizing product visibility, accessibility, and merchandising effectiveness for fresh, frozen, chilled, and ready-to-consume products.

The Refrigerated Display Cases Market is Segmented by Refrigeration Architecture (Plug-In, Semi Plug-In, and Remote), Product Design (Vertical, Horizontal, Hybrid, and Semi-Vertical), Application (Retail Stores, Restaurants and Hotels, and Other Applications), End User (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Discount Stores, Fuel Station Stores, Restaurants and Cafes, Bakeries, and Other End User Outlets), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Plug-In |

| Semi Plug-In |

| Remote |

| Vertical |

| Horizontal |

| Hybrid |

| Semi-Vertical |

| Retail Stores |

| Restaurants and Hotels |

| Other Applications |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Discount Stores |

| Fuel Station Stores |

| Restaurants and Cafes |

| Bakeries |

| Hotels |

| Other End User Outlets |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Refrigeration Architecture | Plug-In | |

| Semi Plug-In | ||

| Remote | ||

| By Product Design | Vertical | |

| Horizontal | ||

| Hybrid | ||

| Semi-Vertical | ||

| By Application | Retail Stores | |

| Restaurants and Hotels | ||

| Other Applications | ||

| By End User | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Discount Stores | ||

| Fuel Station Stores | ||

| Restaurants and Cafes | ||

| Bakeries | ||

| Hotels | ||

| Other End User Outlets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and future size of refrigerated display cases?

The refrigerated display cases market stood at USD 20.48 billion in 2026 and is forecast to reach USD 29.76 billion by 2031, growing at a CAGR of 7.76% over 2026-2031.

Which region leads sales today and which one is growing the fastest?

Europe held the largest share at 39.41% in 2025, while Asia-Pacific is projected to post the fastest growth at 8.73% CAGR through 2031.

Which refrigeration architecture is most widely used?

Plug-in systems led with 58.37% share in 2025 because they fit retrofit projects, convenience stores, and smaller retail formats more easily than centralized systems.

Why are natural refrigerants becoming more important for buyers?

Regulatory changes in the United States and Europe are pushing operators toward lower-GWP systems, which is accelerating demand for CO2 and R290-based display cases.

Which end-user group is expanding the fastest?

Convenience stores are projected to grow at 9.56% CAGR through 2031 as chains add stores, enlarge foodservice zones, and remodel older outlets with more chilled merchandising space.

What is the main challenge facing suppliers and store operators?

High retrofit costs and a shortage of trained technicians are the main constraints, especially for CO? and R290 systems that need specialized installation and service capability.

Page last updated on: