Reflux Testing Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.39 Billion |

| Market Size (2031) | USD 5.40 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reflux Testing Devices Market Analysis by Mordor Intelligence

The Reflux Testing Devices Market size is projected to expand from USD 4.22 billion in 2025 and USD 4.39 billion in 2026 to USD 5.40 billion by 2031, registering a CAGR of 4.23% between 2026 to 2031.

Accelerated adoption of Lyon Consensus 2.0 software metrics, hospital replacement cycles, and the pivot toward wireless capsule monitoring are shaping topline growth. Hospitals are refreshing legacy catheter-based fleets with multi-modal pH-impedance platforms that automate scoring and compress review time, while wireless systems continue to win share because 96-hour monitoring windows capture symptom–reflux correlations that 24-hour studies miss. The June 2025 Class I FDA recall affecting Medtronic’s Bravo CF capsule opened competitive space for Diversatek Healthcare and Jinshan Science & Technology, both of which now bundle Lyon-ready analytics and cloud updates that sidestep on-site firmware visits. Simultaneously, guideline harmonization by the American College of Gastroenterology and the European Society of Gastrointestinal Endoscopy is pushing physicians to document objective reflux evidence before escalating proton-pump inhibitor therapy, broadening procedural demand across gastroenterology, otolaryngology, and pulmonology practices.

Key Report Takeaways

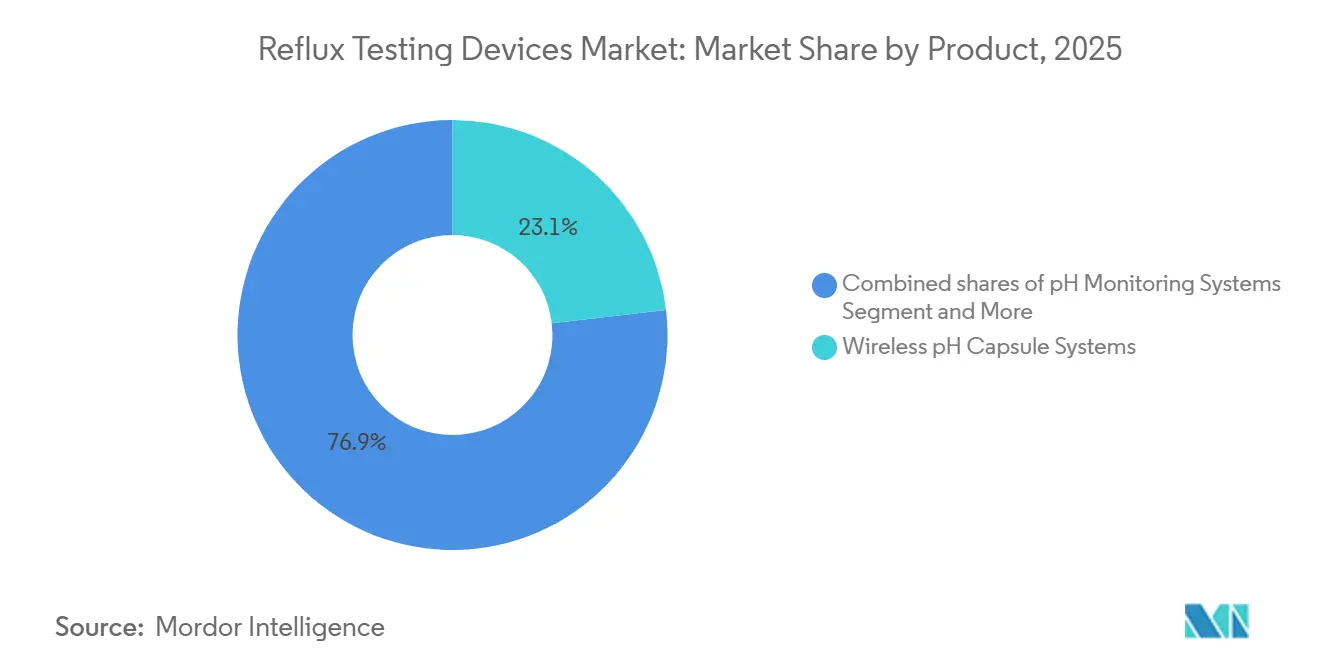

- By product type, wireless pH capsule systems led with 23.14% of the reflux testing devices market share in 2025 and are forecast to expand at a 5.23% CAGR through 2031.

- By end user, hospitals accounted for 52.34% of 2025 revenue, while ambulatory surgical centers are the fastest-growing channel, with a 6.12% CAGR to 2031.

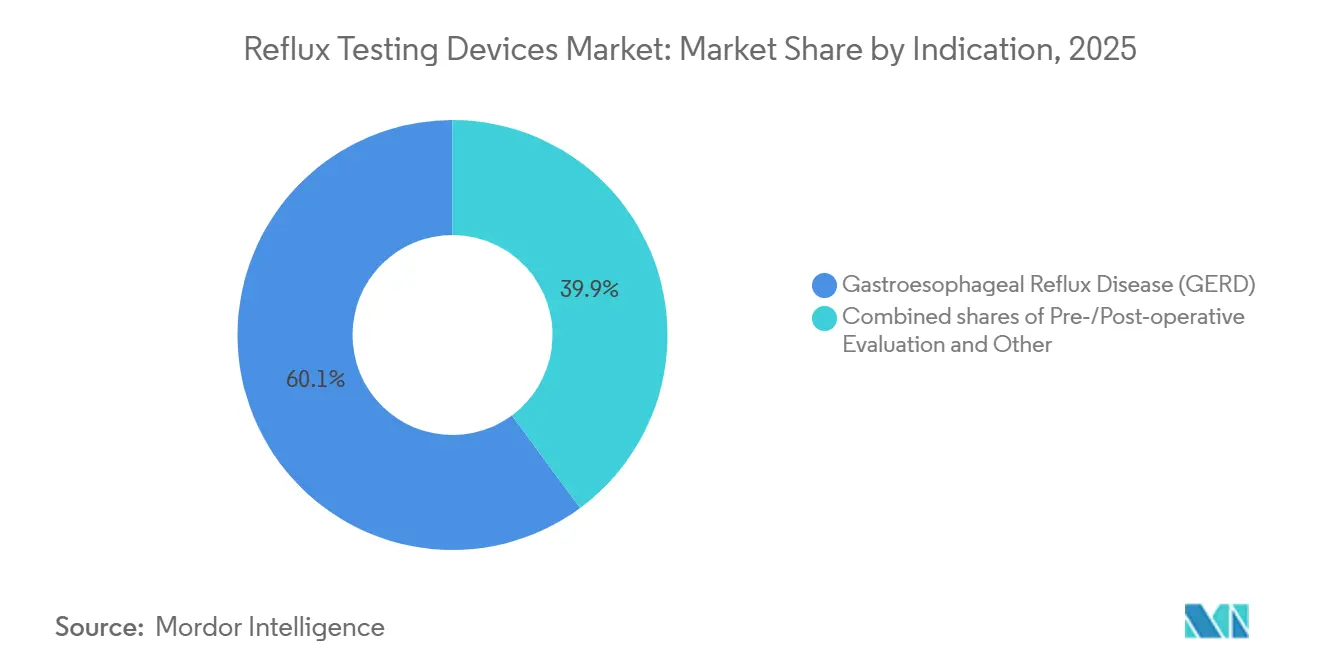

- By indication, gastroesophageal reflux disease accounted for 60.15% of demand in 2025, and gastroesophageal reflux disease (GERD) is the fastest-growing cohort, with a 5.30% CAGR through 2031.

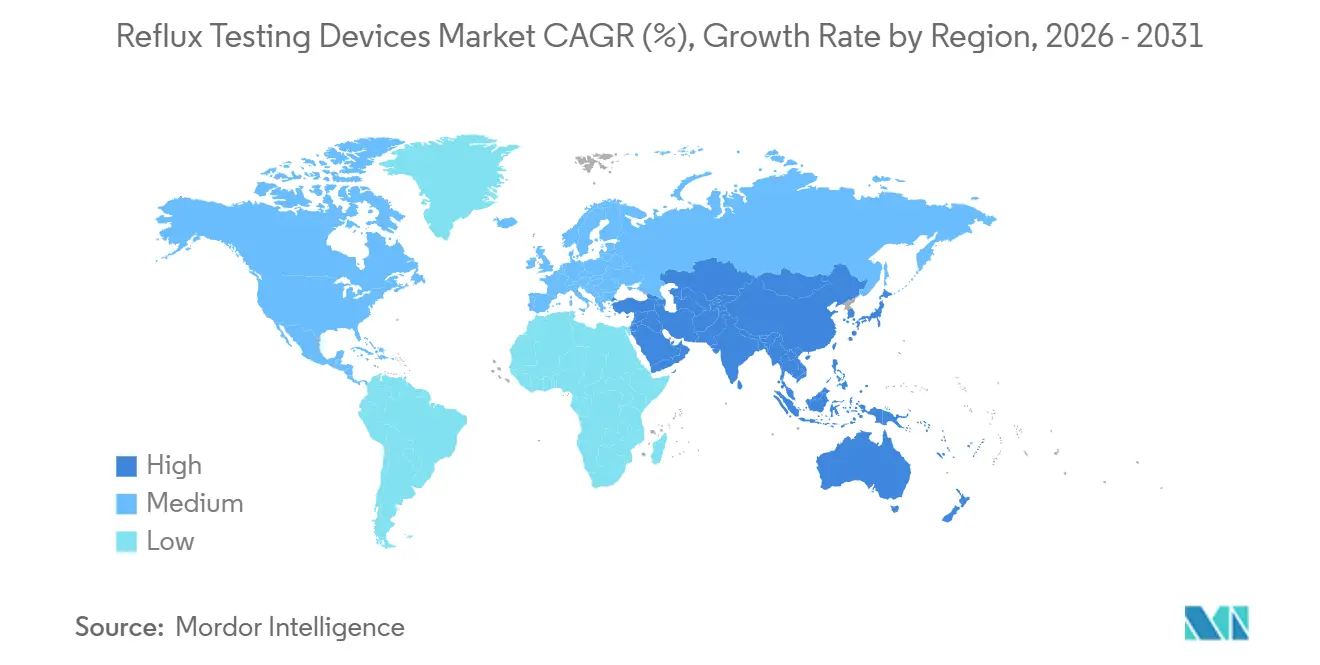

- By geography, North America accounted for 46.54% of global revenue in 2025, yet Asia-Pacific is projected to post the highest regional CAGR of 6.34% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reflux Testing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Updated reflux testing guidelines standardize ambulatory monitoring decisions | +0.8% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Wireless capsule-based monitoring enables longer studies and better tolerance | +1.1% | North America, Europe, and urban Asia-Pacific markets | Short term (≤ 2 years) |

| Rising GERD and extraesophageal symptom burden expands testing referrals | +0.9% | Global, particularly Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Hospital dominance and installed-base upgrades sustain replacement demand | +0.7% | North America and Europe | Medium term (2-4 years) |

| Lyon Consensus 2.0 metrics embedded in software drive objective adoption | +0.6% | North America, Europe, and select Asia-Pacific tertiary centers | Short term (≤ 2 years) |

| IDN and VA procurement standardization consolidates device choices | +0.5% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Updated Reflux Testing Guidelines Standardize Ambulatory Monitoring Decisions

The Lyon Consensus 2.0 framework defines acid exposure time above 6% as conclusive for GERD and below 4% as exclusionary, eliminating subjective gray zones and prompting hospitals to replace recorders that lack automated calculations of mean nocturnal baseline impedance and post-reflux swallow-induced peristaltic wave. Diversatek integrated these metrics into its Zvu 3.4.0 release in June 2025, enabling simultaneous manometry and pH analysis within a single interface [1]Diversatek Healthcare, “AutoSCAN Analytics Overview,” diversatekhealthcare.com. FDA 510(k) clearances now require proof of Lyon metric accuracy, encouraging vendors to embed objective scoring engines and accelerating software-driven refresh cycles. Longer wireless protocols are also mandated for patients with negative 24-hour catheter results, uncovering additional positives and expanding procedural volumes.

Wireless Capsule-Based Monitoring Enables Longer Studies and Better Tolerance

Wireless systems extend observation to 96 hours, reveal circadian acid patterns, and record symptom events during real-world activities that nasal probes disrupt. Patient willingness to repeat wireless testing reaches 90% versus 50% for catheters, a compliance edge that boosts longitudinal monitoring of refractory cases. Medtronic’s 2025 recall briefly constrained supply, but it also triggered hospital evaluations of Jinshan’s alpHaFLEX device, which offers 50 Hz sampling and native Lyon metrics, and of Diversatek’s ZepHr capsule, both of which secured new multiyear contracts during the recall gap [2]Jinshan Science & Technology, “alpHaFLEX Wireless pH-Impedance System,” jinshangroup.net.

Rising GERD and Extraesophageal Symptom Burden Expands Testing Referrals

Global GERD prevalence continues to climb, and referrals now include chronic cough and laryngopharyngeal reflux patients whose pathology involves pepsin rather than acid. Salivary pepsin screening through RD Biomed’s PepsinCheck is gaining traction, showing pooled sensitivity of 73% and specificity of 72% in a 2025 meta-analysis, and funneling suitable candidates into impedance-pH confirmation studies. Direct-to-consumer distribution bypasses hospital capital budgets and accelerates adoption among symptomatic consumers.

Hospital Dominance and Installed-Base Upgrades Sustain Replacement Demand

Integrated delivery networks and the U.S. Veterans Affairs system standardize reflux monitoring protocols and refresh equipment every five to seven years, primarily because software upgrades lag on older hardware. February 2026 VA contracts for Bravo systems illustrate incumbent stickiness, yet Lyon-driven metric requirements still push hospitals toward platforms that support remote cloud updates and electronic health record interoperability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient aversion to nasal catheters dampens test uptake | -0.6% | Global, particularly in markets with low GI specialist density | Short term (≤ 2 years) |

| Coverage variability and prior authorization hurdles for LPR/prolonged tests | -0.5% | United States, with spillover to private-payer markets in Latin America | Medium term (2-4 years) |

| Specialist capacity and training gaps slow throughput | -0.4% | Asia-Pacific, Middle East & Africa, and rural North America | Long term (≥ 4 years) |

| Limited US clearance for some non-US systems constrains competition | -0.3% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patient Aversion to Nasal Catheters Dampens Test Uptake

Despite the advantages of real-time impedance data, nasal probes deter repeat testing. Research shows that only half of subjects would repeat a catheter study, versus 90% for wireless capsules. Manufacturers have introduced softer polyurethane probes, but tolerance gaps persist, especially in the Asia-Pacific region, where cultural expectations favor non-invasive approaches. Reduced uptake delays diagnosis in atypical reflux cases, perpetuating empirical PPI therapy without objective evidence.

Coverage Variability and Prior Authorization Hurdles for Prolonged Tests

U.S. insurers inconsistently reimburse CPT 91037 and 91038 codes for 96-hour wireless studies, with denial rates up to 40%. Practices therefore hold minimal capsule inventory, wary of uncompensated device costs. Extraesophageal reflux claims face even steeper hurdles, driving some patients to self-pay or abandon testing. Direct-to-consumer salivary pepsin kits partially fill this diagnostic void.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wireless Systems Outpace Catheters Despite Recall Setback

Wireless pH Capsule Systems held 23.14% market share in 2025 and will expand at a 5.23% CAGR through 2031, the fastest growth among product segments, driven by 96-hour monitoring windows that capture symptom-reflux correlations missed by 24-hour catheter studies and patient-tolerance advantages that reduce study abandonment. Medtronic's June 2025 Class I recall of Bravo CF capsule delivery devices—linked to 33 serious injuries from adhesive manufacturing defects—temporarily disrupted supply but accelerated evaluations of Jinshan's alpHaFLEX wireless system, which samples at 50 Hz and integrates Lyon Consensus metrics, including post-reflux swallow-induced peristaltic wave detection, offering hospitals a differentiated alternative during the recall period.

pH-Impedance Monitoring Systems, the second-largest segment, benefit from Lyon Consensus 2.0's emphasis on mean nocturnal baseline impedance and bolus clearance metrics, which require impedance channels that catheter-based pH-only systems lack, compelling hospitals to upgrade legacy recorders to multi-modal platforms. Catheter-based pH Monitoring Systems face structural headwinds from patient aversion—only 50% of subjects are willing to repeat, versus 90% for wireless—but retain niche utility for pre-operative assessments, where real-time impedance waveforms guide surgical planning.

By End-User: ASCs Capture Share as Value-Based Care Reshapes Referral Patterns

Hospitals contributed 52.34% of 2025 revenue thanks to centralized procurement and electronic health record integration requirements that favor enterprise-scale vendors. The reflux testing devices market size for Ambulatory Surgical Centers (ASCs) is projected to rise at a 6.12% CAGR, the fastest growth among end-user segments, as value-based care contracts incentivize pre-operative reflux testing for bariatric and anti-reflux surgery candidates to reduce 90-day readmissions, while Medicare's outpatient payment reforms shift reimbursement toward lower-cost ASC settings and away from hospital-based procedures.

Physician-owned ASCs exhibit procurement agility that integrated delivery networks lack: they adopt portable pH recorders such as Diversatek's ZepHr system and Jinshan's alpHaFLEX platform within 60 to 90 days of evaluation, bypassing the 6 to 12-month capital committee cycles that delay hospital purchases, and they negotiate direct vendor contracts that secure 20% to 30% discounts versus hospital group purchasing organization pricing.

By Indication: Gastroesophageal Reflux Disease (GERD) Dominates and is Expected to Grow Fastest Through 2031

Gastroesophageal reflux disease accounted for 60.15% of the 2025 demand, anchoring the reflux testing devices market. The category will expand at a 5.30% CAGR through 2031, driven by guideline-mandated objective testing before long-term PPI therapy or anti-reflux surgery.

Pre- and post-operative evaluation remains high acuity, with surgeons requiring acid exposure documentation to plan and audit fundoplication outcomes. Reimbursement, however, often covers pre-surgical but not post-surgical testing, depressing follow-up volumes. Emerging therapeutics targeting pepsin could further increase diagnostic frequency as drug developers seek companion biomarkers to stratify responders.

Geography Analysis

North America held 46.54% of global revenue in 2025. Growth will moderate as the mature installed base meets reimbursement friction for prolonged wireless studies, yet hospital GI suite modernization projects keep modest capital flowing. Ambulatory surgical centers are expanding reflux testing volumes due to risk-sharing payment models. Canada and Mexico remain underpenetrated because specialist density is lower and provincial formularies emphasize endoscopy.

Asia-Pacific is projected to log a 6.34% CAGR, the fastest worldwide. China’s 43.3 million annual endoscopies create a large procedural funnel, but ambulatory pH monitoring remains concentrated in tier-1 hospitals until regional facilities add trained staff. Domestic vendors like Jinshan leverage lower price points and local service to penetrate rapidly. India’s private hospital chains are early adopters of wireless capsules, although out-of-pocket payment norms temper growth outside metro areas. Developed markets such as Japan, South Korea, and Australia mirror North American replacement patterns but favor non-invasive tools due to cultural preferences.

Europe presents a fragmented payer environment. CE-marked devices face varying remuneration, as illustrated by RefluxStop implant prices ranging from EUR 15,100 to 48,000. Public systems stress the need for cost-effectiveness evidence, pushing manufacturers to supply robust health economic data. Germany and the United Kingdom lead adoption, while Southern European markets progress more slowly due to budget constraints.

Competitive Landscape

The market remains moderately concentrated. Medtronic and Diversatek together control the majority of North American and European installations, yet Medtronic’s 2025 recall weakened incumbent dominance and enabled Jinshan to secure evaluation slots in both Western and Chinese tertiary centers. Competitive advantage is shifting from hardware to analytics. Diversatek’s Zvu 3.4.0 fuses manometry and reflux data, reducing room turnover times, while Jinshan’s cloud suite exports HL7 FHIR messages without middleware, a feature prized by IDNs.

Start-ups pursue niche strategies. RD Biomed’s PepsinCheck addresses the direct-to-consumer segment, selling saliva kits that bypass payer hurdles and create an upstream diagnostic funnel [3]RD Biomed, “PepsinCheck U.S. Launch Announcement,” rdbiomed.com. The Reflux Company plans a vertically integrated model combining diagnosis and therapy after acquiring Restech’s reflux assets. Artificial intelligence accuracy improvements near 90%, shrinking nurse review duties, and forming a new axis of competition. ISO 13485 certification now figures prominently in tender evaluations, limiting small entrants that lack mature quality systems.

Reflux Testing Devices Industry Leaders

Medtronic Plc

Diversatek Healthcare

RD Biomed

Shenzhen Jinshan Science & Technology Co., Ltd.

The Reflux Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The FDA elevated Medtronic’s Bravo CF capsule recall to Class I after 33 serious injuries linked to adhesive defects were confirmed.

- May 2025: RD Biomed signed a five-year exclusive U.S. distribution agreement with The Reflux Company to market PepsinCheck direct to consumers at GBP 79.95 per kit.

- May 2025: Diversatek released Zvu 3.4.0, embedding Lyon-ready metrics and AutoSCAN analytics that cut review time below 10 minutes

Global Reflux Testing Devices Market Report Scope

As per the scope of the report, reflux testing devices are specialized medical tools used to objectively diagnose gastroesophageal reflux disease (GERD) by monitoring the frequency and duration of acid or non-acid exposure in the esophagus. These devices are essential for patients whose symptoms, such as heartburn, regurgitation, or chronic cough, do not respond to standard medications, such as proton pump inhibitors (PPIs).

The reflux testing devices market is segmented by product, end users, indication, and geography. Based on product, the market is segmented into pH monitoring systems (Catheter‑based), pH‑impedance monitoring systems (MII‑pH), wireless pH capsule systems, oropharyngeal pH monitoring systems, and accessories & consumables. By end users, the market is segmented into hospitals, ambulatory surgical centers (ASCs), specialty GI clinics, and diagnostic centers & labs. By indication, the market is segmented into gastroesophageal reflux disease (GERD), pre‑/post‑operative evaluation (anti‑reflux, bariatric), and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| pH Monitoring Systems (Catheter‑based) |

| pH‑Impedance Monitoring Systems (MII‑pH) |

| Wireless pH Capsule Systems |

| Oropharyngeal pH Monitoring Systems |

| Accessories & Consumables |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty GI Clinics |

| Diagnostic Centers & Labs |

| Gastroesophageal Reflux Disease (GERD) |

| Pre‑/Post‑operative Evaluation (Anti‑reflux, Bariatric) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | pH Monitoring Systems (Catheter‑based) | |

| pH‑Impedance Monitoring Systems (MII‑pH) | ||

| Wireless pH Capsule Systems | ||

| Oropharyngeal pH Monitoring Systems | ||

| Accessories & Consumables | ||

| By End‑User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty GI Clinics | ||

| Diagnostic Centers & Labs | ||

| By Indication | Gastroesophageal Reflux Disease (GERD) | |

| Pre‑/Post‑operative Evaluation (Anti‑reflux, Bariatric) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the reflux testing devices market?

The reflux testing devices market size reached USD 4.39 billion in 2026.

How fast will the market grow over the next five years?

It is forecast to expand at a 4.23% CAGR over 2026-2031.

Which product category is growing the quickest?

Wireless pH capsule systems are advancing at a 5.23% CAGR driven by 96-hour monitoring capability and greater patient tolerance.

Why are hospitals replacing legacy catheter systems?

Lyon Consensus 2.0 guidelines require automated scoring metrics that many older recorders lack, prompting hospitals to upgrade to software-enabled platforms.

Page last updated on: