Reference Thermometer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.7 Billion |

| Market Size (2030) | USD 2.51 Billion |

| Growth Rate (2025 - 2030) | 8.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

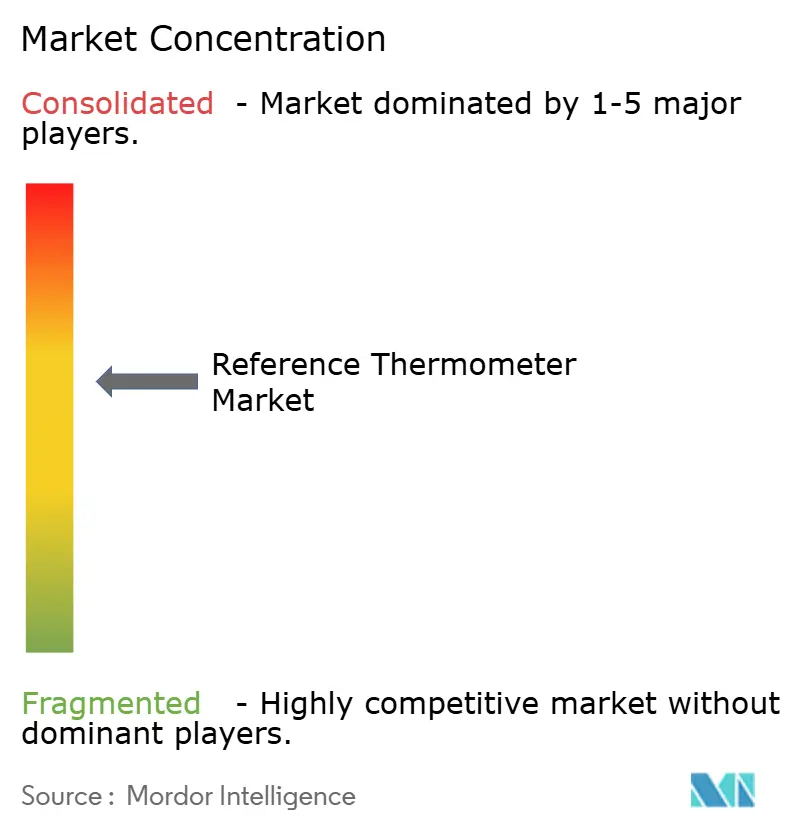

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reference Thermometer Market Analysis by Mordor Intelligence

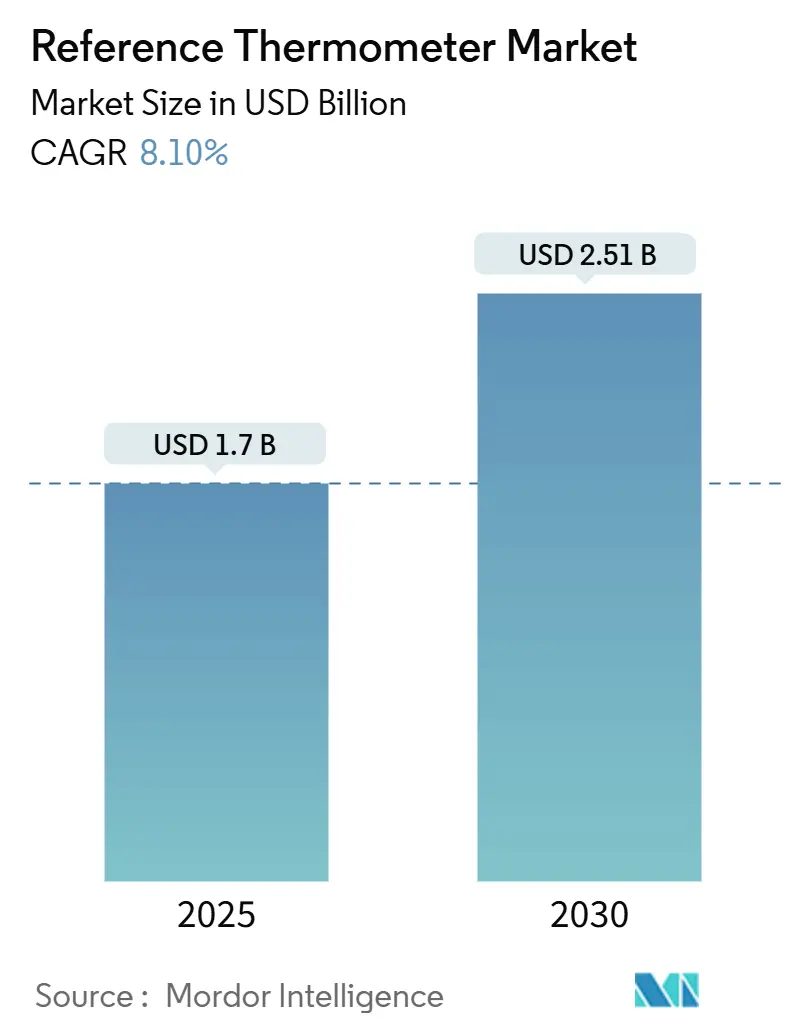

The reference thermometer market size currently stands at USD 1.70 billion and is forecast to reach USD 2.51 billion by 2030, growing at an 8.1% CAGR from 2025 to 2030. This healthy trajectory is underpinned by rising precision demands across biopharma cold-chain validation, quantum-computing cryogenics, and geothermal resource monitoring, all of which require lower measurement uncertainties and traceable calibration equipment. Laboratories are accelerating the transition to digital workflows, investing in connected instruments that generate tamper-proof electronic calibration certificates while integrating seamlessly with ISO/IEC 17025 quality systems. Industrial IoT adoption further lifts demand by enabling real-time drift detection and predictive maintenance, reducing unplanned process downtime. In parallel, regulatory tightening, especially around FDA-mandated temperature validation, sustains replacement cycles for outdated instruments. Competitive intensity remains moderate as global players bundle hardware, software, and service contracts to defend share, while smaller specialists target niche applications with cost-effective or ultra-high-accuracy offerings.

Key Report Takeaways

- By product type, SPRTs led with a 31.6% share of the reference thermometer market in 2024, whereas infrared reference thermometers are projected to expand at a 10.2% CAGR through 2030.

- By calibration type, primary fixed-point systems accounted for 44.1% of the reference thermometer market size in 2024, while on-site/in-process calibration is forecasted to grow at a 9.8% CAGR through 2030.

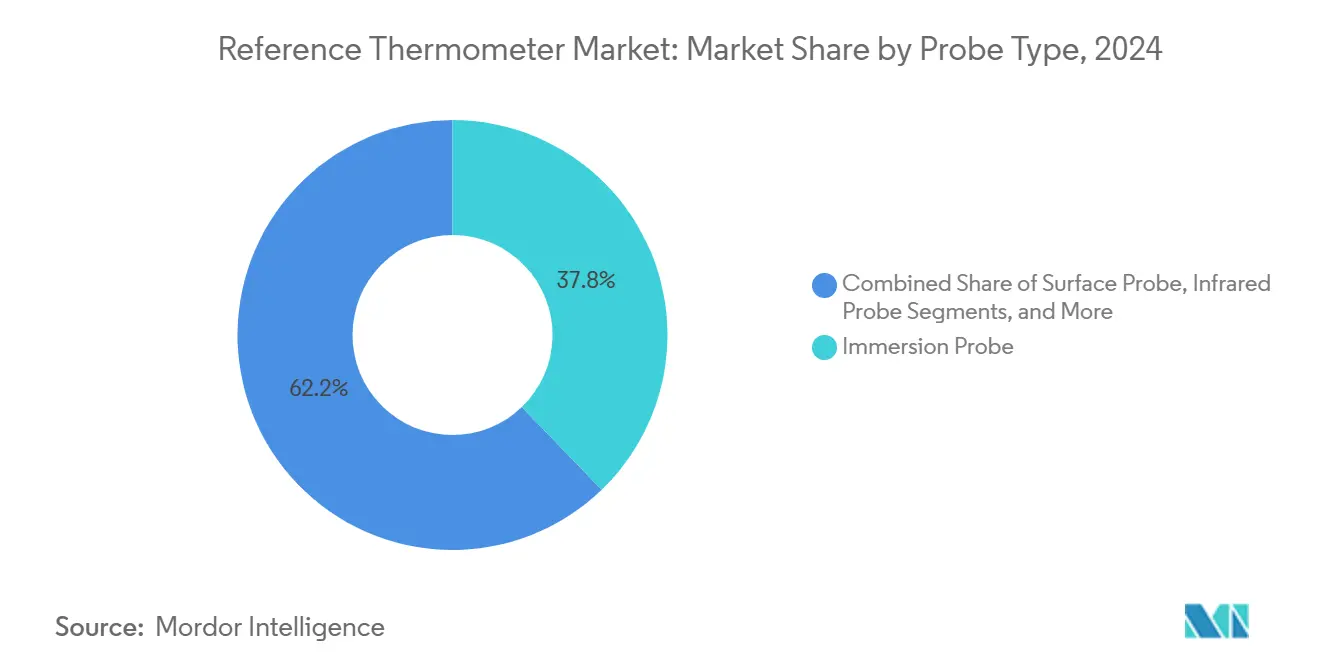

- By probe type, immersion probes captured 37.8% of the reference thermometer market size in 2024; infrared probes show the strongest momentum with a 9.9% CAGR through 2030.

- By end-user industry, the healthcare and life sciences sector accounted for 26.9% of the reference thermometer market size in 2024, whereas the energy and utilities sector is advancing at a 9.1% CAGR between 2025 and 2030.

- By geography, North America held 26.2% of the reference thermometer market share in 2024; Asia-Pacific is poised for the fastest expansion at an 8.8% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reference Thermometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift to digital calibration labs | +1.8% | Global; early uptake in North America and EU | Medium term (2-4 years) |

| Tighter ISO/IEC 17025 accreditation cycles | +1.5% | EU and North America | Short term (≤ 2 years) |

| Expansion of biopharma cold-chain auditing | +1.2% | North America, EU, APAC pharma hubs | Medium term (2-4 years) |

| Industrial IoT integration in temperature metrology | +1.4% | Global; faster in developed markets | Long term (≥ 4 years) |

| Emergence of cryogenic quantum-computing labs | +0.9% | North America, EU, select APAC | Long term (≥ 4 years) |

| Growing demand for high-precision geothermal monitoring | +1.1% | Geothermal-rich regions worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Digital Calibration Labs

Digital laboratories now generate more than 60% of new calibration certificates, a leap that minimizes transcription errors and expedites audit readiness.[1]ISO, “ISO/IEC 17025:2017 General requirements for the competence of testing and calibration laboratories,” iso.org Reference thermometers equipped with Ethernet, USB, or wireless modules are preferred because they can be directly integrated into laboratory information management systems. Self-diagnostic firmware flags sensor drift early, shortening recalibration intervals and lowering lifetime ownership costs. Vendors also embed blockchain-enabled certificate repositories that allow clients to verify authenticity without manual paperwork. Heightened demand is evident in North American pharmaceutical laboratories, where remote regulatory inspections are increasingly relying on digital documentation. This irreversible shift underpins the growing global demand for smart reference thermometers, specifically those tailored for automated comparison baths.

Tighter ISO/IEC 17025 Accreditation Cycles

The revision of ISO/IEC 17025 shortened the renewal intervals from five to three years and tightened the permissible uncertainty budgets. Laboratories unable to document compliance have faced a 40% rise in non-conformance citations since 2024, prompting accelerated upgrades to high-stability reference thermometers that minimize drift. Secondary standard instruments must now demonstrate repeatability over extended soak periods, incentivizing the purchase of low-self-heat SPRTs with proven long-term stability. Accreditation bodies in Germany, Canada, and Japan have increased surveillance visits, ensuring sustained baseline demand despite macroeconomic volatility. As a result, suppliers offering bundled calibration plus uncertainty calculation software enjoy a competitive edge.

Expansion of Biopharma Cold-Chain Auditing

Revised FDA guidance mandates multi-point temperature mapping during storage and transit of cell and gene therapies.[2]FDA, “Guidance for Industry: Quality Considerations for Continuous Manufacturing,” fda.gov Biopharma firms, therefore, deploy redundant reference-grade probes inside qualification chambers to validate uniformity. Budget allocations for temperature validation hardware rose by double digits in 2025 among U.S. vaccine producers. Similar rules from the European Medicines Agency are forcing contract manufacturing organizations to modernize calibration assets. Demand extends to blood banks and clinical-trial logistics, where data-logged reference thermometers confirm traceability across entire distribution networks. Suppliers with sterile, low-mass probes designed for −70 °C dry-ice boxes see particularly strong order books.

Industrial IoT Integration in Temperature Metrology

Smart-factory programs connect reference thermometers to plant-wide networks that feed drift data into predictive algorithms.[3]NIST, “Smart Manufacturing Program,” nist.gov Facilities report 25% reductions in calibration-related downtime after deploying wireless standards in heat-treating furnaces and clean-room HVAC systems. Cloud dashboards visualize uncertainty trends and trigger alerts before instruments exceed tolerance, converting calibration from a calendar-based to a condition-based activity. Early adopters in South Korea's semiconductor fabs now issue electronic certificates directly into their enterprise resource planning suites, eliminating the need for manual reconciliation. As manufacturers scale the concept, incremental unit sales of reference thermometers with embedded MQTT or OPC-UA protocols are expected to climb.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial cost of fixed-point cells | -1.20% | Global; strongest in emerging markets | Short term (≤ 2 years) |

| Shortage of skilled metrologists | -0.80% | APAC, Latin America, Africa | Medium term (2-4 years) |

| Drift issues in secondary SPRTs under extreme cycling | -0.60% | Global; pronounced in industrial sectors | Medium term (2-4 years) |

| Lack of harmonised standards for wireless probes | -1.00% | Global; strongest in regulated industries | Long term (>4 years) |

| Source: Mordor Intelligence | |||

High Initial Cost of Fixed-Point Cells

A complete fixed-point furnace, controller, and triple-point cell can exceed USD 100,000 and requires specialized ambient-condition control, which strains budgets for mid-tier laboratories.[4]BIPM, “Consultative Committee for Thermometry,” bipm.org Capital constraints are pronounced in Southeast Asia and Sub-Saharan Africa, where facilities rely instead on third-party calibration services. Even in developed markets, CFOs often postpone upgrades during economic uncertainty, slowing penetration of advanced primary standards. Suppliers attempt to mitigate sticker shock with leasing models and modular designs; yet, affordability remains a near-term brake on the widespread adoption of ITS-90 realization equipment.

Shortage of Skilled Metrologists in Emerging Markets

Many universities in emerging economies do not offer comprehensive thermometry programs, resulting in a limited pool of qualified personnel able to evaluate uncertainty budgets or service SPRTs.[5]OIML, “Technical Committee 12,” oiml.org Laboratories consequently face extended turnaround times or must import expertise from Europe, inflating operational costs. The scarcity also affects maintenance; mishandling delicate SPRTs during transport or immersion can lead to resistance drift, thereby shortening instrument life. While remote training modules are helpful, language barriers and limited lab infrastructure hinder progress, making talent development a crucial prerequisite for deeper penetration of the reference thermometer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Precision Demands Anchor SPRT Dominance

Standard platinum resistance thermometers (SPRTs) anchored 31.6% of the reference thermometer market share in 2024, underscoring their status as the cornerstone of ITS-90 traceability. The reference thermometer market size generated by SPRT shipments is expected to grow steadily as labs cycle older sensors out of service to meet tighter accreditation criteria. Their ±0.001 °C long-term stability aligns with demands from high-stakes pharmaceutical validation and cryogenic physics research. Infrared reference thermometers, although representing a smaller market, are projected to grow at a 10.2% CAGR through 2030 as contactless measurement gains traction in semiconductor wafer processing lines operating above 300 °C. Industrial PRTs remain relevant for on-site verification, offering rugged sheaths and moderate uncertainties that meet the requirements of chemical plants.

Competitive product strategies are increasingly focusing on specialty coatings and low-self-heating designs that extend drift intervals. Thermistor reference thermometers are used in biomedical freezers, which can reach temperatures as low as −90 °C, where higher sensitivity compensates for the limited temperature range. Thermocouple reference thermometers are used in ultra-high-temperature metallurgy applications above 1,200 °C, although their typical ±0.5 °C uncertainty restricts their usage to secondary calibration roles. Product diversification into digital-output SPRTs with integrated ADCs simplifies uncertainty budgets by removing lead-wire effect corrections, a feature gaining popularity among newly accredited labs in Mexico and Thailand.

By Calibration Type: Mobility Reshapes Service Models

Primary fixed-point calibration systems accounted for 44.1% of the reference thermometer market size in 2024, reflecting their indispensable role in establishing national traceability chains. Yet on-site/in-process calibration exhibits the highest 9.8% CAGR as manufacturing clients prioritize uptime and deploy mobile baths or dry-blocks that bring the lab to the process line. Portable reference standards, housed in vibration-isolated cases, now achieve a stability of ±0.003 °C across a 0-260 °C span, which is adequate for many secondary verification tasks.

Service providers bundle subscription-based programs that involve technicians calibrating instruments in situ while synchronizing results with cloud databases, thereby satisfying auditors and minimizing shipping risks. Secondary comparison calibration maintains significance, especially among contract labs serving regional industrial clusters with moderate accuracy needs. The calibration type mix highlights a shift from centralized, equipment-heavy facilities toward agile, digital workflows, a transition that boosts recurring revenues for vendors offering cloud software licenses.

By Probe Type: Immersion Sensors Retain Versatility

Immersion probes held a 37.8% revenue share in 2024 due to their superior heat transfer and suitability for liquid-in-glass bath calibrations. Their glass-encased SPRT variants remain indispensable for fixed-point cells, while stainless-steel-sheathed industrial PRTs dominate process validation. The reference thermometer market continues to demand low-stem-conductance designs that mitigate gradient errors, especially in deep freezers used for biologics storage. Infrared probes, projected to grow at a 9.9% CAGR, benefit from furnace and glass-melt monitoring, where contact sensors tend to degrade quickly.

Surface probes with flat-tip construction find niche roles in electronics thermal profiling, while air/gas probes validate HVAC environmental chambers to ±0.1 °C. Penetration probes, featuring reduced-diameter tips, satisfy food-safety audits that require minimal sample disturbance. Suppliers now offer interchangeable probe assemblies calibrated as a system with the readout, simplifying uncertainty statements and supporting tighter alignment with ISO/IEC 17025 clauses.

By End-User Industry: Healthcare Commands Budget Priority

The healthcare and life sciences sector captured 26.9% of the reference thermometer market share in 2024, driven by FDA and EMA protocols that require validated temperature mapping for every GMP suite. Vaccine manufacturers in the United States upgraded walk-in freezer arrays with redundant SPRTs to safeguard mRNA formulations. Hospital blood banks likewise deploy reference-grade thermistors for platelet incubators where ±0.5 °C excursions risk product wastage. The energy and utilities sector, forecasted to grow at a 9.1% CAGR, adopts high-temperature thermocouple standards to calibrate super-critical steam sensors in power plants and to monitor geothermal boreholes, where flux data underpin reservoir models.

Food and beverage processors utilize penetration PRTs to meet HACCP plans, maintaining a solid baseline demand, whereas aerospace and defense clients specify radiation-hard reference thermometers for re-entry vehicle testing. Research institutions are pioneering ultra-low-uncertainty cryogenic probes that will eventually transition into commercial quantum-computing supply chains, illustrating how academic advances can seed future industrial revenue streams.

Geography Analysis

North America generated 26.2% of global revenue in 2024, reflecting entrenched FDA oversight, a dense network of ISO/IEC 17025-accredited laboratories, and sizable defense and space research funding that demands extreme-temperature calibration. U.S. metrology firms actively cross-sell cloud software and service contracts alongside hardware, reinforcing customer lock-in. Canadian mining operations add incremental volume through ruggedized PRT purchases for arctic exploration rigs where ambient shocks challenge sensor integrity.

The Asia-Pacific is the fastest-growing cluster, projected to grow at an 8.8% CAGR, driven by China’s investment in biologics plants and Japan’s increasing semiconductor temperature control requirements. South Korea’s electronics giants now mandate electronic calibration certificates, pushing suppliers to integrate secure digital signatures. India’s government incentives for pharmaceutical exports spur domestic calibration labs to procure SPRTs that are traceable to national standards, thereby broadening the reference thermometer market base.

Europe maintains stable growth, anchored by Germany’s automotive and chemical sectors and bolstered by EU climate policy that directs funding to geothermal heat-recovery monitoring. Manufacturers in Austria and Switzerland specialize in fixed-point cells, exporting high-purity metal capsules across the continent. The United Kingdom’s life-sciences corridor around Cambridge accelerates demand for cryogenic reference sensors used in cell-therapy logistics, underscoring the region’s premium-priced niche opportunities.

Competitive Landscape

The market is moderately fragmented. Fluke Corporation, AMETEK Inc., and WIKA collectively account for a significant yet non-dominant share, leveraging global service centers and vertically integrated manufacturing to protect margins. Fluke’s 1595A Super-Thermometer, launched in January 2025, incorporates algorithms that automatically calculate the combined standard uncertainty, thereby reducing the analyst's workload during audits. AMETEK’s acquisition of ThermoProbe GmbH adds cryogenic depth, enabling entry into quantum-computing supply chains where sub-Kelvin stability is critical.

Mid-tier players such as Anton Paar and Testo emphasize ergonomic handheld instruments integrated with Bluetooth apps, appealing to field technicians. Meanwhile, niche specialists like Isothermal Technology and Hart Scientific focus on ultra-low-uncertainty SPRTs for national metrology institutes. Price competition intensifies in emerging markets, where local distributors introduce lower-cost probes; however, reliability concerns hinder uptake among high-stakes pharmaceutical clients.

Strategic alliances are trending toward complete ecosystem offerings. Vendors pair hardware with subscription-based calibration management platforms that automate scheduling, certificate archival, and auditor-ready reporting. Manufacturers also court OEM contracts with thermal-equipment builders, embedding calibrated sensors directly into freezers or furnaces to secure recurring consumables revenue. Overall, technology differentiation around connectivity and uncertainty analytics remains the decisive battleground for share gains.

Reference Thermometer Industry Leaders

Fluke Corporation (Fluke Calibration)

AMETEK Inc.

WIKA Alexander Wiegand SE and Co. KG

Spectris plc (OMEGA Engineering)

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Fluke Corporation launched its 1595A Super-Thermometer with enhanced digital connectivity and automated uncertainty calculation capabilities.

- December 2024: AMETEK Inc. acquired ThermoProbe GmbH for USD 45 million, expanding cryogenic measurement offerings.

- November 2024: Thermo Fisher Scientific invested USD 25 million to expand temperature calibration services in Singapore and Brazil.

- October 2024: WIKA introduced a wireless reference thermometer series with cloud connectivity for industrial IoT applications.

Global Reference Thermometer Market Report Scope

| Standard Platinum Resistance Thermometers (SPRT) |

| Industrial Platinum Resistance Thermometers (IPRT) |

| Thermistor Reference Thermometers |

| Thermocouple Reference Thermometers |

| Infrared Reference Thermometers |

| Primary (Fixed-Point) Calibration |

| Secondary / Comparison Calibration |

| On-site / In-process Calibration |

| Immersion Probe |

| Surface Probe |

| Air / Gas Probe |

| Penetration Probe |

| Infrared Probe |

| Healthcare and Life Sciences |

| Food and Beverage |

| Industrial Manufacturing |

| Energy and Utilities |

| Aerospace and Defense |

| Research and Academia |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product Type | Standard Platinum Resistance Thermometers (SPRT) | |

| Industrial Platinum Resistance Thermometers (IPRT) | ||

| Thermistor Reference Thermometers | ||

| Thermocouple Reference Thermometers | ||

| Infrared Reference Thermometers | ||

| By Calibration Type | Primary (Fixed-Point) Calibration | |

| Secondary / Comparison Calibration | ||

| On-site / In-process Calibration | ||

| By Probe Type | Immersion Probe | |

| Surface Probe | ||

| Air / Gas Probe | ||

| Penetration Probe | ||

| Infrared Probe | ||

| By End-User Industry | Healthcare and Life Sciences | |

| Food and Beverage | ||

| Industrial Manufacturing | ||

| Energy and Utilities | ||

| Aerospace and Defense | ||

| Research and Academia | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the reference thermometer market?

The reference thermometer market size stands at USD 1.70 billion in 2025 and is projected to reach USD 2.51 billion by 2030.

Which product category holds the largest share?

Standard platinum resistance thermometers lead with 31.6% reference thermometer market share in 2024.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at an 8.8% CAGR through 2030, outperforming all other regions.

What key factor drives demand in healthcare?

Tight FDA temperature validation rules for biologics and vaccines prompt continual upgrades to high-accuracy reference probes.

How are digital trends affecting calibration?

Industrial IoT connectivity and electronic certificates lower downtime and improve traceability, spurring adoption of smart reference thermometers.

Which calibration type is growing quickest?

On-site/in-process calibration services are expanding at a 9.8% CAGR as manufacturers prioritize equipment uptime.

Page last updated on: