Reconstructed Skin Models Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

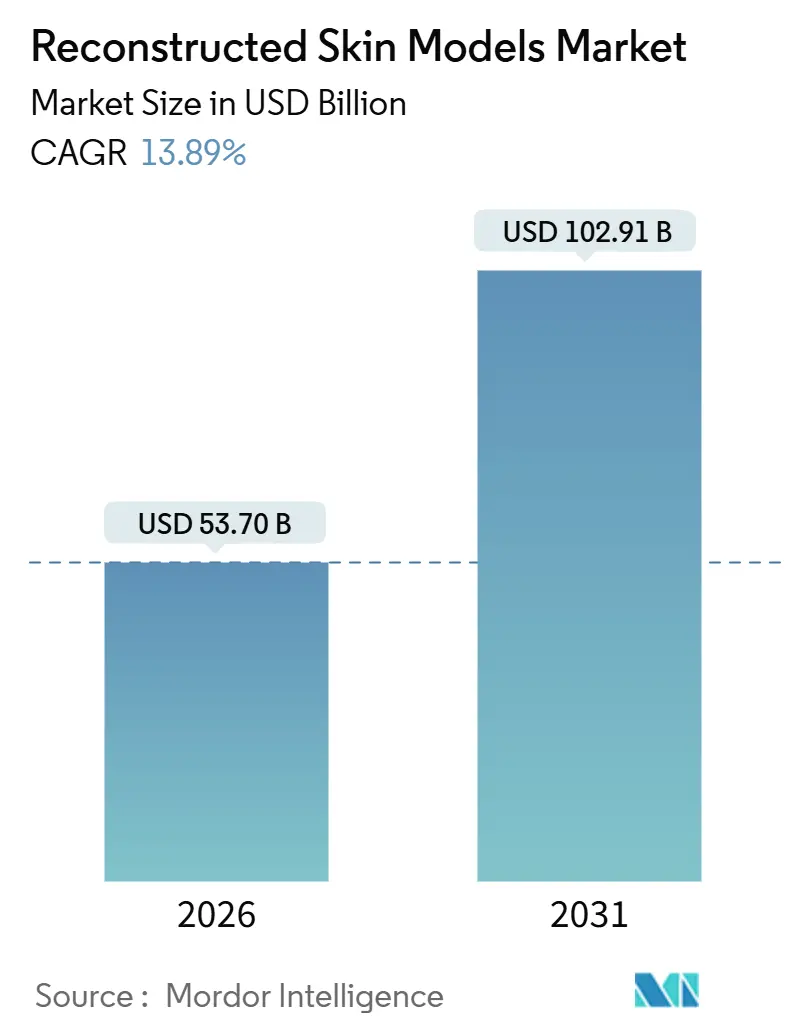

| Market Size (2026) | USD 53.70 Billion |

| Market Size (2031) | USD 102.91 Billion |

| Growth Rate (2026 - 2031) | 13.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reconstructed Skin Models Market Analysis by Mordor Intelligence

The Reconstructed Skin Models Market size is estimated at USD 53.70 billion in 2026, and is expected to reach USD 102.91 billion by 2031, at a CAGR of 13.89% during the forecast period (2026-2031).

Demand is accelerating as pharmaceutical, cosmetic, and chemical companies replace animal studies with human-relevant in vitro platforms that gain swifter regulatory acceptance, lower ethical exposure, and greater clinical predictive power. Europe’s decade-old ban on cosmetic animal testing created the initial pull. At the same time, China’s 2025 repeal of mandatory in-vivo tests removed a final significant trade barrier, intensifying global investment in full-thickness and disease-specific constructs. Continuous R&D in 3D bioprinting, microvascular engineering, and immune-competent tissues is shortening fabrication cycles and expanding use cases from irritation screens to complex melanoma modeling. Competitive focus is shifting toward proprietary, patient-specific models that command premium pricing despite persistent supply-chain constraints in qualified donor tissue. Vendors able to certify ISO 13485 processes and deliver inter-laboratory reproducibility below 15% variation are winning multi-year contracts with contract research organizations and tier-one consumer-health brands.

Key Report Takeaways

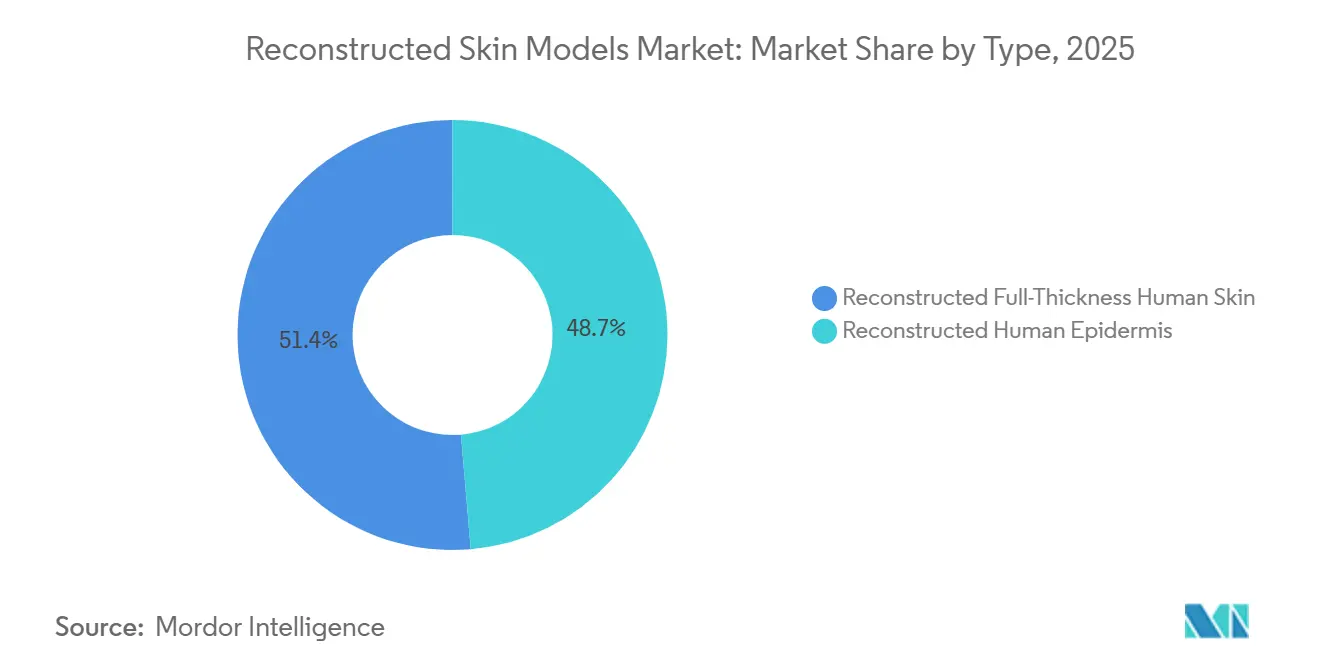

- By type, reconstructed human epidermis led with 48.65% of reconstructed skin models market share in 2025, while reconstructed full-thickness human skin is set to grow at a 15.65% CAGR through 2031.

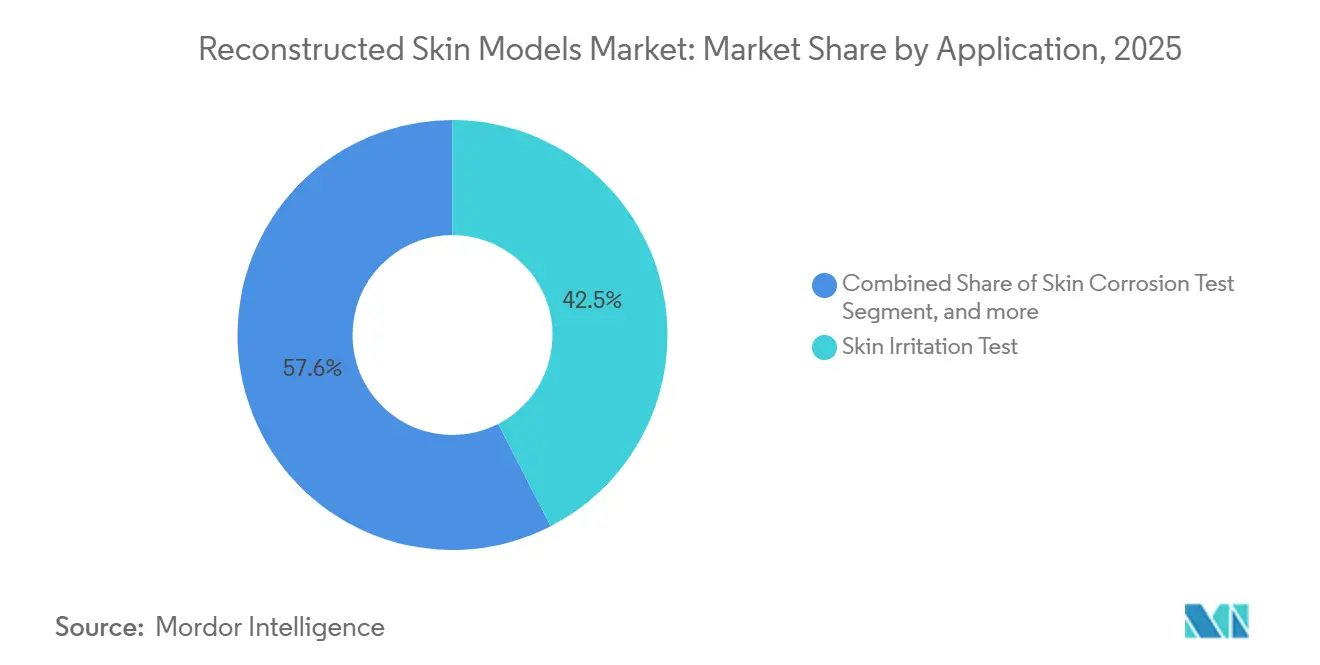

- By application, the skin irritation test accounted for 42.45% of the reconstructed skin models market in 2025; pigmentation & melanoma studies are projected to expand at a 15.87% CAGR through 2031.

- By end-user, cosmetics & cosmeceutical companies captured 64.31% revenue in 2025, whereas pharmaceutical & biotech firms recorded the highest expected CAGR at 16.76% through 2031.

- By geography, North America held 42.54% of the reconstructed skin models market size in 2025; Asia-Pacific is forecast to register a 14.54% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reconstructed Skin Models Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Dermatological Conditions & Cosmetic Procedures | +2.5% | Global, North America & Europe lead | Medium term (2-4 years) |

| Regulatory Shift Toward Animal-Free Safety Assessment | +3.2% | Global, led by EU; China, South Korea rising | Short term (≤ 2 years) |

| Advances in Tissue Engineering & 3D Bioprinting Technologies | +2.8% | North America & Europe core; spill-over to APAC | Medium term (2-4 years) |

| Increasing R&D Spending by Cosmetic & Pharmaceutical Firms | +2.1% | Global, strongest in North America, Western Europe, Japan | Long term (≥ 4 years) |

| Expansion of Microphysiological Systems for Multi-Organ Integration | +1.8% | North America & Europe; early in South Korea | Long term (≥ 4 years) |

| Rising Adoption in Personalized Medicine & Drug Screening | +2.3% | North America & Europe; emerging in China, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Dermatological Conditions & Cosmetic Procedures

Skin disorders such as atopic dermatitis and psoriasis already affect 1.9 billion people worldwide, and melanoma incidence among fair-skinned populations is climbing 3% each year. Pharmaceutical pipelines consequently emphasize immune checkpoint inhibitors and targeted therapies that require disease-specific, immune-competent skin constructs to demonstrate target engagement before human dosing. Simultaneously, cosmetic procedure volumes rose 12% year-over-year in 2025 in North America and Europe, boosting demand for irritation and sensitization assays that reflect post-procedure barrier compromise[1]International Society of Aesthetic Plastic Surgery, “Annual Global Survey 2025,” isaps.org. Regulators now require data on variants of inflamed or aged skin, pushing vendors to diversify beyond standard reconstructed epidermis. As a result, the reconstructed skin models market is embedding chronic-disease pathophysiology into off-the-shelf platforms to attract oncology and aesthetic-dermatology budgets.

Regulatory Shift Toward Animal-Free Safety Assessment

China’s 2025 policy allowing cosmetic registration without animal tests aligns the country with the EU Cosmetics Regulation. It removes a crucial trade barrier, redirecting global validation budgets toward OECD TG 439-compliant reconstructed human epidermis[2]National Medical Products Administration, “Technical Guidelines for Non-Animal Testing 2025,” nmpa.gov.cn. South Korea plans a blanket alternative-methods mandate by 2027, and the U.S. FDA Modernization Act 2.0 now allows IND sponsors to replace animal data with qualified in vitro evidence. These synchronized reforms compress adoption cycles and favor vendors holding OECD and ISO dossiers, driving a near-term spike in demand for reconstructed skin models across the three largest cosmetic-consuming regions.

Advances in Tissue Engineering & 3D Bioprinting Technologies

Sub-100-micron bioprinting resolution, achieved in 2025 on BICO Group’s CELLINK systems, enables precise deposition of keratinocytes, fibroblasts, and melanocytes to replicate papillary and reticular dermis architecture. Organovo’s patent-pending microvascular networks maintain perfusion for 28 days, extending assay windows for systemic-absorption studies. Epithelix demonstrated innervated constructs that allow neuro-dermatitis and chronic-itch assays, opening entirely new revenue streams. These innovations shorten fabrication from 21 to 7 days, reduce labor costs per insert, and broaden the application scope, reinforcing the reconstructed skin models market's trajectory.

Increasing R&D Spending by Cosmetic & Pharmaceutical Firms

L’Oréal invested EUR 1.1 billion (USD 1.2 billion) in 2024 R&D, earmarking 18% for predictive toxicology platforms that rely on its EPISKIN subsidiary. Estée Lauder redirected USD 450 million in 2025 to in-house in-vitro testing infrastructure. Pharmaceutical heavyweights such as Pfizer boosted dermatology-pipeline outlays by 22% in 2025, using reconstructed skin to differentiate biosimilars. Contract research organizations reported a 30% uptick in client demand for integrated reconstructed skin and computational modeling packages, reinforcing long-term funding flows into the reconstructed skin models market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost & Pricing Pressure | −1.5% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Complex, Fragmented Regulatory Pathways | −0.9% | Global, most pronounced in APAC & Latin America | Medium term (2-4 years) |

| Limited Standardization & Inter-Laboratory Variability | −1.2% | Global, critical in North America & Europe | Medium term (2-4 years) |

| Supply Constraints of Qualified Human Donor Tissue | −0.8% | Global, severe in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost & Pricing Pressure

Full-thickness inserts still retail at USD 800-1,200, a 3-5× premium over 2D cell cultures. Fabrication spans 21-28 days and suffers 10-15% batch rejection, inflating the cost of goods. Capital prices for semi-automated bioprinters can reach USD 500,000, discouraging smaller contract labs. Chinese and South Korean vendors are scaling aggressively, threatening price compression that could squeeze thin European margins. These dynamics restrain near-term reconstructed skin models' market penetration among budget-constrained brands.

Complex, Fragmented Regulatory Pathways

Vendors must finance separate ring trials for OECD TG 439, TG 431, and TG 442D, each costing up to USD 1 million and 24 months. China’s 2025 technical standards diverge from OECD barrier-integrity thresholds, requiring tweaks to the formula. FDA's silence on multi-organ chips leaves sponsors unsure of their eligibility for expedited review. Such fragmentation inflates time-to-market and diverts R&D funds away from innovation, damping the growth of reconstructed skin models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Full-Thickness Models Accelerate on Drug-Delivery Needs

In 2025, reconstructed human dermis accounted for 48.65% of the reconstructed skin models market revenue, yet full-thickness constructs are forecast to expand 15.65% annually through 2031. Full-thickness platforms replicate fibroblast-mediated contraction, vascular permeability, and angiogenesis, which are critical for evaluating transdermal monoclonal antibody delivery. The segment commanded 50% of the reconstructed skin models market size for transdermal drug projects in 2025 and is on track to deepen its share as ISO 10993-10 explicitly recognizes full-thickness tissue for device biocompatibility screens.

Epidermal models remain a staple for high-throughput cosmetic testing, where rapid barrier-function readouts suffice. However, their intrinsic limitations—no dermal stroma, immune cells, or perfusable capillaries—curb use in complex pharmacology. Automation advances lowered full-thickness labor costs by 25% between 2024-2025, narrowing the price gap and encouraging pharmaceutical switching. The reconstructed skin models market consequently shows a mix shift favoring multilayered architectures.

By Application: Melanoma Constructs Outpace Routine Irritation Tests

Skin irritation test retained 42.45% market share in 2025 thanks to entrenched OECD TG 439 compliance. Yet Pigmentation & Melanoma Studies are poised to grow 15.87% per year to 2031, the fastest-rising application segment, as oncology divisions insert immune-competent melanoma constructs into lead-selection workflows. These disease-specific platforms captured 25% of the reconstructed skin models market size for oncology-screening services in 2025 and will likely exceed 35% by 2031.

China’s alternative-methods mandate is adding hundreds of irritation-test requests, sustaining volume while moderating prices. Corrosion and sensitization assays benefit similarly, while rare-disease histology and phototoxicity screens expand niche demand. The reconstructed skin models market thus tilts from compliance-driven batch testing toward high-value discovery biology.

By End-User: Pharma & Biotech Lead Future Expansion

Cosmetics & cosmeceutical companies accounted for 64.31% of revenue in 2025, after a decade of regulatory pressure, but their growth is plateauing. Pharmaceutical & Biotech Firms are projected to grow at a 16.76% CAGR, driven by biosimilar differentiation, personalized medicine, and rare-disease pipelines. In 2025, pharma accounted for 30% of the reconstructed skin models market size in immune-oncology screening and is expected to approach 40% by 2031.

Chemical companies and CROs contribute to ancillary demand, leveraging reconstructed tissue to comply with REACH and to offer turnkey predictive toxicology suites. NIH subsidies for academic users will further diversify the client base, embedding reconstructed skin across the discovery-to-preclinical stages.

Geography Analysis

North America held 42.54% of reconstructed skin models market share in 2025 on the back of USD 102 billion pharmaceutical R&D outlays and FDA acceptance of alternative methods[3]Pharmaceutical Research and Manufacturers of America, “Biopharmaceutical R&D Expenditures 2025,” phrma.org. Lead times average 10-14 days due to a tight integration of tissue banks and contract manufacturers. Europe, the regulatory pioneer, still accounts for nearly one-third of global sales, but high labor costs and a saturated cosmetics segment slow expansion to 10-11% CAGR. Germany and France remain R&D hubs, yet post-Brexit UK divergence could fragment standards and impose duplicate validations.

Asia-Pacific is the fastest-growing region at 14.54% CAGR. China’s 2025 reform removed the last mandatory animal-testing hurdle, and South Korea is staging a 2027 ban, pulling demand toward regional production. Japan Tissue Engineering’s GMP facility pivot reinforces local supply. These dynamics should lift Asia-Pacific’s reconstructed skin models market size from 22% of global revenue in 2025 to around 28% by 2031.

South America and the Middle East & Africa combined account for under 10% of revenue, held back by import duties and cold-chain challenges. Brazil’s draft ANVISA guidance and GCC halal requirements are emerging niche drivers. Long-term growth depends on establishing regional fabrication hubs to avoid seven-day product shelf-life constraints.

Competitive Landscape

MatTek, EPISKIN, and Genoskin jointly controlled 45-50% of the reconstructed skin models market revenue in 2025, yet none exceeded a 25% individual share, leading to moderate concentration. Their standardized epidermal constructs face commoditization as OECD validation levels the playing field. Competitive advantage is migrating to full-thickness, vascularized, and patient-specific models sold at double or triple the unit price. BICO’s 2024 acquisition of Sciperio cut print times to seven days, aligning with just-in-time pharmaceutical workflows. Organovo and Epithelix hold patents on microvasculature and innervation, targeting neuro-immune applications poorly served by incumbents.

ISO 13485 certification and <15% inter-lab variability are emerging as procurement thresholds. Only six to eight vendors meet both, creating a barrier for small contract labs. Chinese entrants, aided by lower labor costs and domestic tissue sourcing, are scaling aggressively and could trigger price erosion. Conversely, academic spin-outs leveraging iPSC technology may disrupt supply-chain constraints once regulatory acceptance materializes post-2027.

Strategic collaborations surged: MatTek earned OECD validation for EpiDermFT Plus in 2025; EPISKIN partnered with TissUse on multi-organ chips; Organovo inked a USD 15 million deal with a top-10 pharma for vascularized constructs. Such alliances illustrate a pivot from compliance to high-value disease modeling within the reconstructed skin models market.

Reconstructed Skin Models Industry Leaders

EPISKIN

MatTek Corporation

Genoskin SA

BICO Group AB

Japan Tissue Engineering Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: CUTISS secured EUR 57.9 million in Series C funding to accelerate the development of regenerative skin therapies. The funding aims to enhance their innovative skin reconstruction technologies for medical and cosmetic applications.

- August 2023: EPISKIN launched SkinEthic HBE (Human Bladder Epithelium) model at the 12th World Congress on Alternatives and Animal Use in Life Sciences. This new epithelium model aims to advance in vitro research on bladder tissue.

Global Reconstructed Skin Models Market Report Scope

As per scope of the report, reconstructed skin models are lab-grown, artificial skin tissues that mimic the structure and function of natural human skin. They are used for research, testing cosmetics, and studying skin diseases. These models provide a cruelty-free alternative to animal testing and enable better understanding of skin biology.

The Reconstructed Skin Models Market is Segmented by Type (Reconstructed Human Epidermis and Reconstructed Full-Thickness Human Skin), Application (Skin Irritation Test, Skin Corrosion Test, Skin Sensitisation Test, Skin Biopsy & Histology Support, Radioallergosorbent Test, Pigmentation & Melanoma Studies, and Other Applications), End-User (Cosmetics & Cosmeceutical Companies, Chemical & Agro-Chemical Companies, Pharmaceutical & Biotech Firms, and CROs & Academic Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Reconstructed Human Epidermis |

| Reconstructed Full-Thickness Human Skin |

| Skin Irritation Test |

| Skin Corrosion Test |

| Skin Sensitisation Test |

| Skin Biopsy & Histology Support |

| Radioallergosorbent Test (RAST) |

| Pigmentation & Melanoma Studies |

| Other Applications |

| Cosmetics & Cosmeceutical Companies |

| Chemical & Agro-Chemical Companies |

| Pharmaceutical & Biotech Firms |

| CROs & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Type | Reconstructed Human Epidermis | |

| Reconstructed Full-Thickness Human Skin | ||

| By Application | Skin Irritation Test | |

| Skin Corrosion Test | ||

| Skin Sensitisation Test | ||

| Skin Biopsy & Histology Support | ||

| Radioallergosorbent Test (RAST) | ||

| Pigmentation & Melanoma Studies | ||

| Other Applications | ||

| By End-User | Cosmetics & Cosmeceutical Companies | |

| Chemical & Agro-Chemical Companies | ||

| Pharmaceutical & Biotech Firms | ||

| CROs & Academic Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the reconstructed skin models market?

The reconstructed skin models market size is USD 53.70 billion in 2026 and is projected to reach USD 102.91 billion by 2031.

Which segment is growing fastest within reconstructed skin models?

Full-thickness human skin models are expanding at a 15.65% CAGR, driven by transdermal-drug and wound-healing research needs.

How are recent regulations affecting adoption?

EU, U.S., and China now allow or encourage human-relevant in-vitro safety data, removing animal-testing barriers and accelerating uptake.

Why are pharmaceutical companies increasing their use of reconstructed skin?

Patient-specific constructs improve target validation and reduce Phase I trial failures, leading pharma to invest heavily in these models.

What technological advance is most disruptive?

3D bioprinting that creates vascularized and innervated full-thickness tissues in 7 days is cutting costs and unlocking new applications.

Which region will drive the next wave of growth?

Asia-Pacific, led by China and South Korea, is forecast to post a 14.54% CAGR as regional regulations shift to alternative methods.

Page last updated on: