Reclaimed Butyl Rubber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

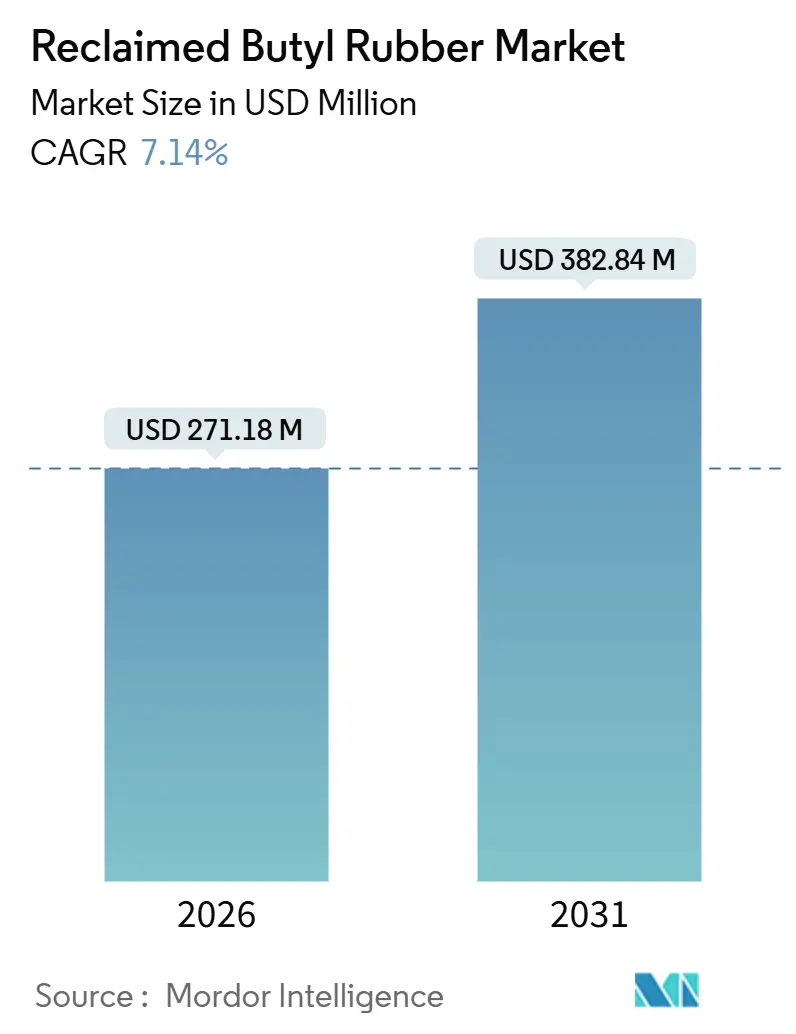

| Market Size (2026) | USD 271.18 Million |

| Market Size (2031) | USD 382.84 Million |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Reclaimed Butyl Rubber Market Analysis by Mordor Intelligence

The Reclaimed Butyl Rubber Market size is estimated at USD 271.18 million in 2026, and is expected to reach USD 382.84 million by 2031, at a CAGR of 7.14% during the forecast period (2026-2031). Tire makers are increasingly turning to recycled grades instead of virgin elastomers. This shift aims to reduce Scope-3 emissions, mitigate the impact of isobutylene price fluctuations, and adhere to circular-economy mandates. Michelin has committed to a reduction in raw-material carbon intensity by 2030[1]French, Florent, “Sustainable Development Report 2024,” Michelin, michelin.com. Similarly, Goodyear is on track to hit a recycled-input target in 2024. These moves underscore a broader trend: procurement strategies are now deeply intertwined with reclaimed feedstocks. Innovations like low-temperature devulcanization and blockchain traceability, coupled with capacity expansions in Asia, are driving down processing costs, enhancing quality control, and reducing lead times for scrap. While feedstock availability is influenced by varying end-of-life tire regulations, increasing extended-producer-responsibility (EPR) targets in regions like China, India, and California are providing a safety net against potential risks. Although concerns over extractables have made OEMs hesitant about pharmaceutical closures, the reclaimed butyl rubber market is flourishing. It's finding new applications in inner liners, sealants, and waterproofing sheets, all of which can incorporate recycled content without any drop in performance.

Key Report Takeaways

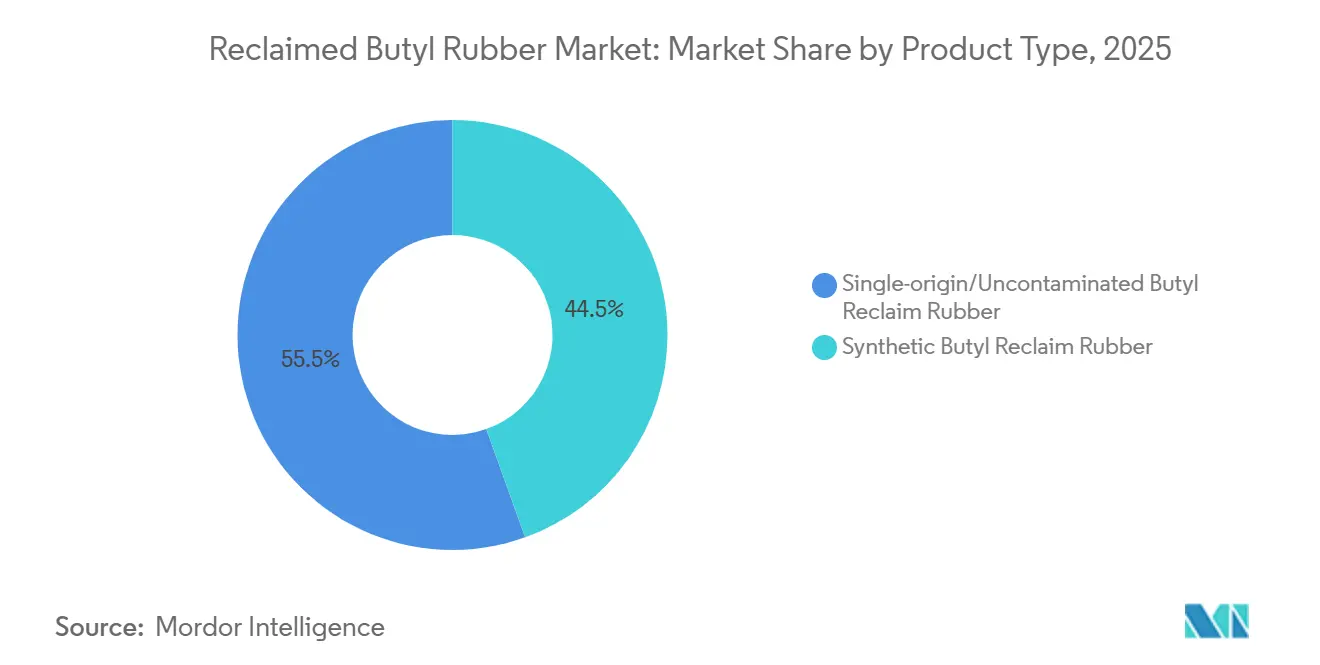

- By product type, single-origin or uncontaminated reclaim captured 55.50% of the reclaimed butyl rubber market share in 2025 and is projected to expand at a 7.59% CAGR to 2031.

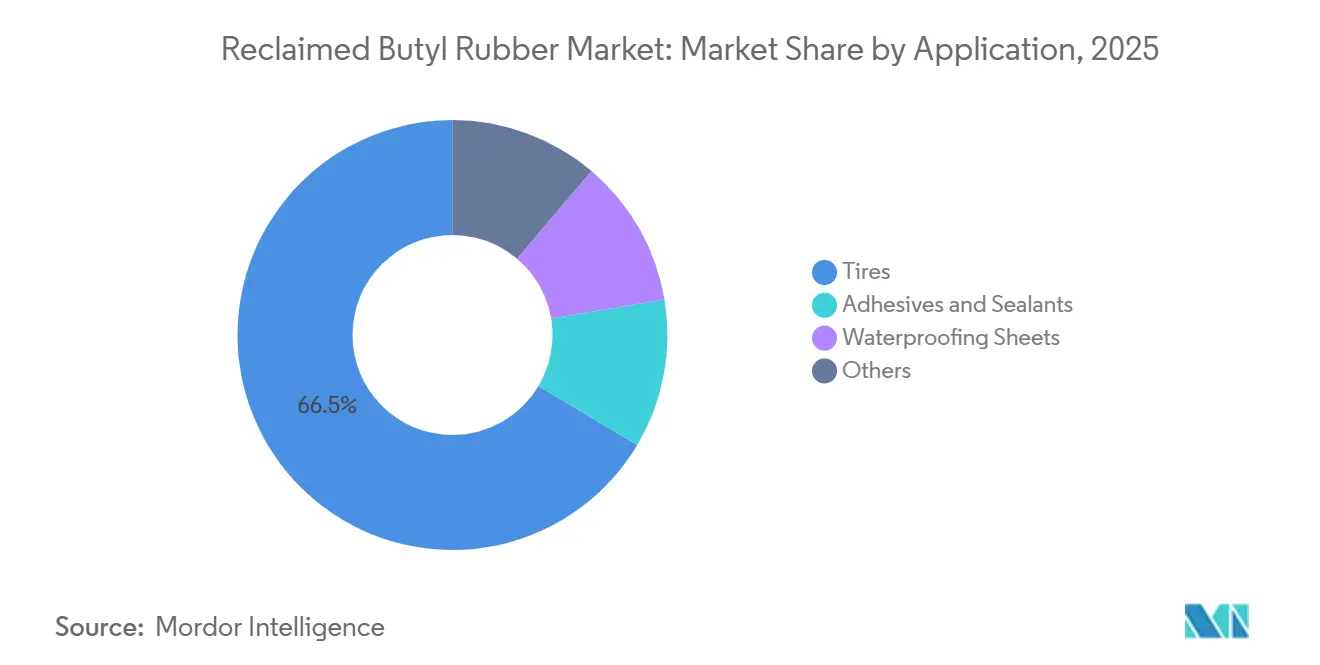

- By application, tires accounted for a 66.46% share of the reclaimed butyl rubber market size in 2025 and are forecast to grow at a 7.72% CAGR through 2031.

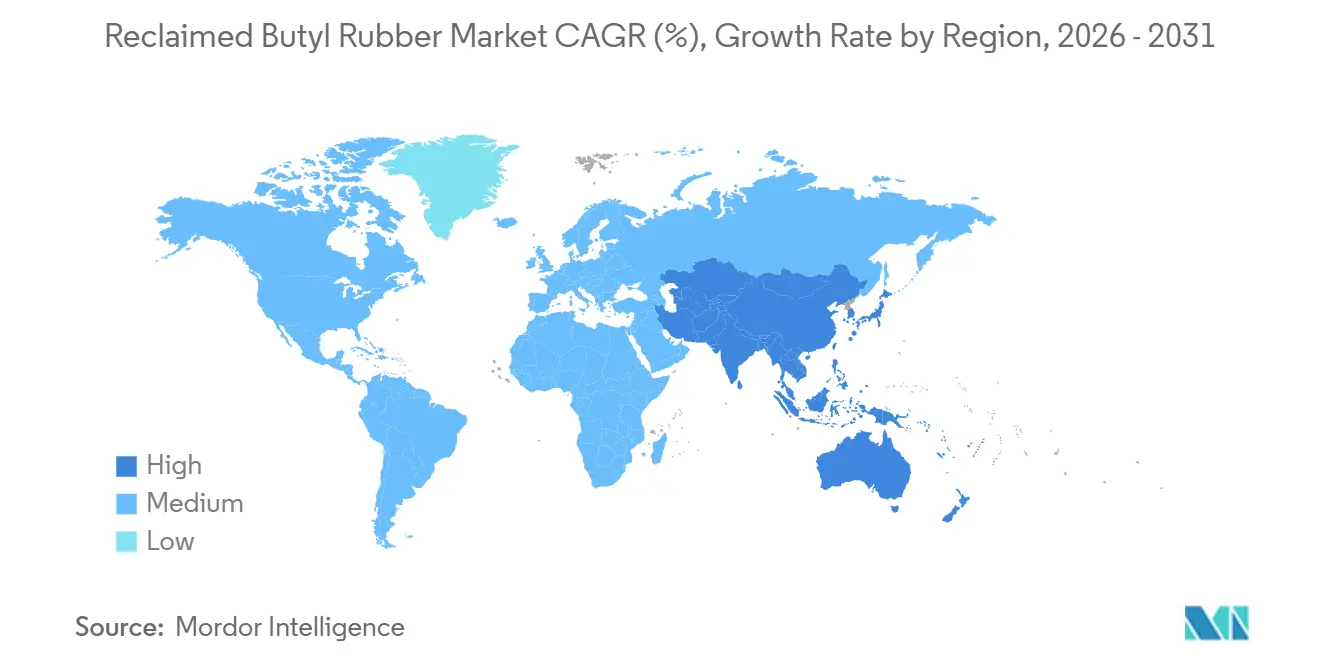

- By geography, Asia-Pacific dominated the reclaimed butyl rubber market with 59.98% revenue share in 2025; the region is anticipated to register the fastest 7.82% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Reclaimed Butyl Rubber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for cost-effective, circular elastomers | +2.1% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Surge in low-temperature devulcanization patents | +1.5% | Global, led by China, EU, and North America | Long term (≥ 4 years) |

| OEM pressure to cut Scope-3 emissions | +1.8% | Europe and North America, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Emergence of blockchain-enabled scrap tracking | +0.9% | Europe and North America, pilot deployments in Asia | Medium term (2-4 years) |

| Asia-centric capacity additions | +1.6% | Asia-Pacific core, particularly China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Cost-Effective, Circular Elastomers

Reclaimed butyl offers a significant cost advantage over virgin butyl, signaling a notable shift in both tire manufacturing and industrial rubber compounding. The persistent discount on reclaimed butyl is primarily influenced by scrap collection and energy costs, diverging from the traditional crude-linked isobutylene pricing. Pirelli has achieved a milestone, integrating recycled and bio feedstock in select product lines for 2025[2]“Sustainability Report 2025,” Pirelli & C. SpA, pirelli.com . This achievement was made possible through the use of reclaimed inner-liner and sidewall compounds. Additionally, a reduction in Mooney viscosity has led to a decrease in mixing cycles, subsequently lowering power consumption in Banbury mixers and enhancing overall cost efficiency. In the pharmaceutical sector, stopper scrap is fetching a premium, attributed to its halogen tolerances. However, even with this premium, demand continues to surpass supply. As more OEMs establish definitive Scope-3 targets, the intersection of cost savings and regulatory compliance is becoming evident, paving the way for the reclaimed butyl rubber market to diversify into new SKUs.

Surge in Low-Temperature Devulcanization Patents

Between 2023 and 2025, global filings for sub-200 °C devulcanization surged. The surge was spearheaded by methods like twin-screw extrusion and microwave surface treatment. These techniques safeguard polymer backbones and align with ASTM D5603 standards for tire compounds. Notably, Chinese inventors dominate the landscape, securing a significant share of the recent grants. Their activities are concentrated around the Shandong tire hubs, where pilot lines are scaling up swiftly. The microwave selectivity method adeptly reduces gel content, effectively halving the amount of scrap that would have otherwise been diverted to low-grade products. With licensees now establishing similar lines in India and Europe, there's a marked reduction in energy intensity. This amplifies profit margins and invigorates the reclaimed butyl rubber market.

OEM Pressure to Cut Scope-3 Emissions

Michelin's Scope-3 emissions overshadow its in-plant emissions, prompting a swift shift towards recycled content. Goodyear aims for a fully sustainable tire by 2030, Continental targets circular content, and Bridgestone sets a goal. Together, these commitments create an annual demand surge for reclaimed elastomers. Mechanical devulcanization produces significantly less CO₂ for every kilogram of output compared to virgin production. This difference gains significance with Europe's Corporate Sustainability Reporting Directive coming into effect in 2026. Such commitments are now pivotal in procurement evaluations, positioning suppliers outside the reclaimed butyl rubber market at a disadvantage in the sustainability arena.

Emergence of Blockchain-Enabled Scrap Tracking

Circularise polymer passports, Hankook’s PROJECT TREE, and BanQu ledgers yield immutable batch histories that track feedstock origin, devulcanization parameters, and quality metrics. Tire makers gain audit-ready proof of recycled content, while processors secure premium pricing for verified lots. Smaller reclaimers lacking digitized workflows struggle with compliance costs, accelerating consolidation. Early pilots show higher yield predictability and double-digit reduction in scrap adulteration, pushing brand owners to mandate traceability across the reclaimed butyl rubber market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent halogen content affecting cure rates | -1.2% | Global, acute in mixed-feedstock markets | Short term (≤ 2 years) |

| Absence of global end-of-life tire mandates | -0.9% | North America, Middle East, parts of Asia-Pacific | Medium term (2-4 years) |

| OEM warranty hesitancy in medical closures | -0.6% | Global, concentrated in pharmaceutical hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Halogen Content Affecting Cure Rates

Regular and halogenated scrap combinations swing halogen levels, shifting scorch time and compelling compounders to elevate accelerator levels. While X-ray fluorescence sorting can maintain a tolerance, its price tag and requirement for skilled labor make it inaccessible for small processors. Until real-time process controls are universally adopted, variability will hinder rapid growth in segments with stringent cure window demands, particularly in inner-liner blends within the reclaimed butyl rubber market.

Absence of Global End-of-Life Tire Mandates

While the EU and Japan successfully recover most scrap tires, the U.S. lags behind, capturing significantly fewer. In India, enforcement of Extended Producer Responsibility (EPR) remains inconsistent. This disparity results in many tires in the U.S. slipping outside formal recovery channels annually. Meanwhile, in India, scrap tires are increasingly directed towards producing pyrolysis oil rather than being mechanically reclaimed. Such a trend intensifies feedstock scarcity, especially when crude prices dip and pyrolysis margins expand, leading to cost volatility that intermittently pressures the reclaimed butyl rubber market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-Origin Feedstock Secures Quality Leadership

Single-origin reclaim accounted for 55.50% of the reclaimed butyl rubber market share in 2025 and is forecast to grow at a 7.59% CAGR to 2031. Reclaimed butyl rubber, known for its superior tensile strength and elongation, meets the ASTM D5603 standards, making it ideal for inner liners and pressure-sensitive adhesives. Pharmaceutical stoppers and curing bladders, when recycled, maintain consistent halogen levels. This consistency not only reduces batch rejections but also allows these materials to command a price premium. In a significant advancement, larger plants in China are now utilizing twin-screw extrusion technology, operating at 0.1-0.4 kW/kg. This process transforms segregated scrap into a high-spec feedstock, aligning with Michelin's ambitious targets.

Synthetic reclaim, derived from a blend of commingled streams, remains relevant in applications like waterproofing membranes and low-grade hoses. However, variability in halogen levels presents challenges. On the technological front, microwave devulcanization emerges as a potential solution for stabilizing viscosity. Yet, the steep million-dollar line costs have limited its adoption to pilot projects in Europe and North America. Despite these challenges, the reclaimed butyl rubber market remains heavily reliant on synthetic grades for volume, awaiting enhancements in global scrap-sorting capacities.

By Application: Tire Inner Liners Set the Growth Pace

Tires absorbed 66.46% of demand in 2025 and are projected to climb at a 7.72% CAGR through 2031, the fastest rate among end uses. Thanks to tighter process control and advances in low-temperature devulcanization, inner liners now incorporate reclaimed content without compromising air permeability. Michelin has surpassed its circular-content goal, achieving this milestone ahead of schedule. Meanwhile, Goodyear is charting a course towards a fully sustainable tire by 2030, banking on a consistent increase in reclaim in its inner-liner compounds. This trend is now the backbone of the reclaimed butyl rubber market.

Adhesives and sealants, prized for their tack and flexibility, are predominantly used in automotive glazing and construction joints. Waterproofing sheets utilize reclaimed feedstock in atactic-polypropylene and styrene-butadiene-styrene modified bitumen, ensuring compliance with ASTM D6162. Industrial hoses and curing bladders also use reclaimed content. While tighter mechanical requirements restrict reclaimed loading to single-digit percentages, closed-loop bladder initiatives in Japan and South Korea hint at significant potential, especially as collection systems evolve in the broader reclaimed butyl rubber landscape.

Geography Analysis

Asia-Pacific generated 59.98% of revenue in 2025 and is tracking a 7.82% CAGR through 2031. Chinese producers dominate the global reclaim capacity. In China, clusters in Shandong and Hebei capitalize on dense flows of tire-plant scrap, significantly cutting logistics costs. Highlighting a shift towards premium materials, Cenway launched its halogenated-butyl line in December 2024. Meanwhile, in India, EPR regulations are prompting tire manufacturers to back-integrate. GRP Limited is upgrading its devulcanization and solvent-recovery systems, aiming to elevate quality standards. Blockchain initiatives, like Hankook’s PROJECT TREE, are enhancing traceability, pushing the regional supply of reclaimed butyl rubber further up the value chain.

In North America, growth is somewhat stifled due to the lack of a federal EPR framework. While California’s SB 876 sets collection fees and targets, the remaining states depend on voluntary programs. This reliance often results in millions of tires being diverted to landfills or exported. Notable milestones, such as Goodyear achieving a recycled-input benchmark and Bolder Industries securing a grant for pyrolysis, underscore the divergent pathways in waste-rubber processing. Mexico's burgeoning tire production is generating more scrap, but its underdeveloped collection infrastructure leads to feedstock shortages in the reclaimed butyl rubber market.

Europe is set to expand, largely driven by mandates like the Waste Framework Directive's collection target and upcoming CSRD audits. Pirelli's achievement of a recycled-input benchmark and Continental's sustainable-content objective underscore the region's commitment to verified reclaim. Initiatives like Circularise's polymer passports are standardizing batch documentation. However, smaller reclaimers, unable to invest in such ledger solutions, face the risk of exiting the market. Major players like Germany, the UK, France, and Italy consistently channel orders into the reclaimed butyl rubber market. Meanwhile, the combined regions of the Middle East, Africa, and Latin America, though currently holding a modest share, are witnessing positive shifts. South Africa's 2024 tire-levy law and Brazil's robust solid-waste policy are steering scrap flows towards more valuable processes.

Competitive Landscape

The reclaimed butyl rubber market is moderately consolidated. Blockchain and X-ray fluorescence deployment are becoming table stakes, raising capex barriers that encourage mergers or closures among smaller Asian processors. Feedstock security remains the arena’s hottest issue. Hankook’s IoT-enabled bale tagging under PROJECT TREE offers a template for backward integration, while tire makers in India consider joint ventures to lock in supply before pyrolysis operators siphon scrap. Technology bifurcation deepens: microwave lines and advanced spectroscopy populate the top tier, whereas oil-bath devulcanization lingers among small workshops, reinforcing a two-speed reclaimed butyl rubber market that favors capital-rich players.

Reclaimed Butyl Rubber Industry Leaders

GRP LTD.

Balaji Rubber Industries Private Limited

NanHui Rubber Co., Ltd.

SINO RUBBER

Tianyu (Shandong) Rubber & Plastic Products Co., Ltd.,

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Elgi Rubber expanded its distributor network across Southeast Asia following TyreXpo Asia 2025 to amplify regional sales of reclaim and retreading solutions.

- February 2025: GRP Ltd. increased reclaim capacity by 3,600 metric tons and started a continuous pyrolysis unit that could lift tire-recycling throughput by 1.5-1.8 times.

Global Reclaimed Butyl Rubber Market Report Scope

Reclaimed Butyl Rubber is a sustainable and eco-friendly material obtained by processing waste butyl rubber products, such as inner tubes and curing bladders, through grinding, devulcanizing, and refining to restore its elastomeric properties. It is known for its high gas impermeability, chemical resistance, and ability to enhance flexibility in rubber compounding.

The reclaimed butyl rubber market is segmented by product type and application. By product type, the market is segmented into single-origin/uncontaminated butyl reclaim rubber and synthetic butyl reclaim rubber. By application, the market is segmented into tires, adhesives and sealants, waterproofing sheets, and others (including hoses, industrial components, etc.). The report also covers the market size and forecasts in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Single-origin/Uncontaminated Butyl Reclaim Rubber |

| Synthetic Butyl Reclaim Rubber |

| Tires |

| Adhesives and Sealants |

| Waterproofing Sheets |

| Others (Hoses, Industrial Components, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Rest of the World |

| By Product Type | Single-origin/Uncontaminated Butyl Reclaim Rubber | |

| Synthetic Butyl Reclaim Rubber | ||

| By Application | Tires | |

| Adhesives and Sealants | ||

| Waterproofing Sheets | ||

| Others (Hoses, Industrial Components, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Rest of the World | ||

Key Questions Answered in the Report

How big is the reclaimed butyl rubber market in 2026?

It stands at USD 271.18 million and is on track to reach USD 382.84 million by 2031, reflecting a 7.14% CAGR.

Which segment grows fastest in reclaimed butyl rubber demand?

Tire inner liners lead with a projected 7.72% CAGR between 2026 and 2031, driven by OEM circular-content targets.

Why is single-origin reclaim priced above mixed-source material?

Pharmaceutical-stopper and curing-bladder scrap deliver tighter halogen tolerances, cutting batch rejections and justifying a price premium.

What regions dominate the reclaimed butyl rubber supply?

Asia-Pacific commands nearly 59.98% of global revenue, with China contributing the majority of capacity.

What restraints could slow market growth?

Halogen variability in mixed feedstocks and patchy global end-of-life tire mandates can disrupt supply chains and inflate processing costs.

Page last updated on: