Rayon Fibers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.65 Billion |

| Market Size (2031) | USD 32.52 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rayon Fibers Market Analysis by Mordor Intelligence

The Rayon Fibers Market size is expected to increase from USD 22.17 billion in 2025 to USD 23.65 billion in 2026 and reach USD 32.52 billion by 2031, and is expected to grow at a CAGR of 6.58% over 2026-2031. The rayon fibers market is growing as apparel manufacturers, home textile producers, and nonwoven converters shift away from petroleum-based fibers toward biodegradable cellulosic materials. This shift is also driven by cost changes, as increased lyocell capacity additions in Asia are narrowing the price gap with polyester in several volume applications. Asia-Pacific remains the primary production and demand base for the rayon fibers market, while North America is growing faster as sourcing standards for certified cellulosics become more stringent. Competition is dividing between high-volume producers with integrated pulp-to-fiber operations and differentiated suppliers competing on traceability, solvent recovery, and brand-backed fiber platforms. The market continues to face cost pressure from tighter effluent and emissions compliance requirements, and the high capital requirements for greenfield lyocell facilities keep entry barriers high for smaller producers.

Key Report Takeaways

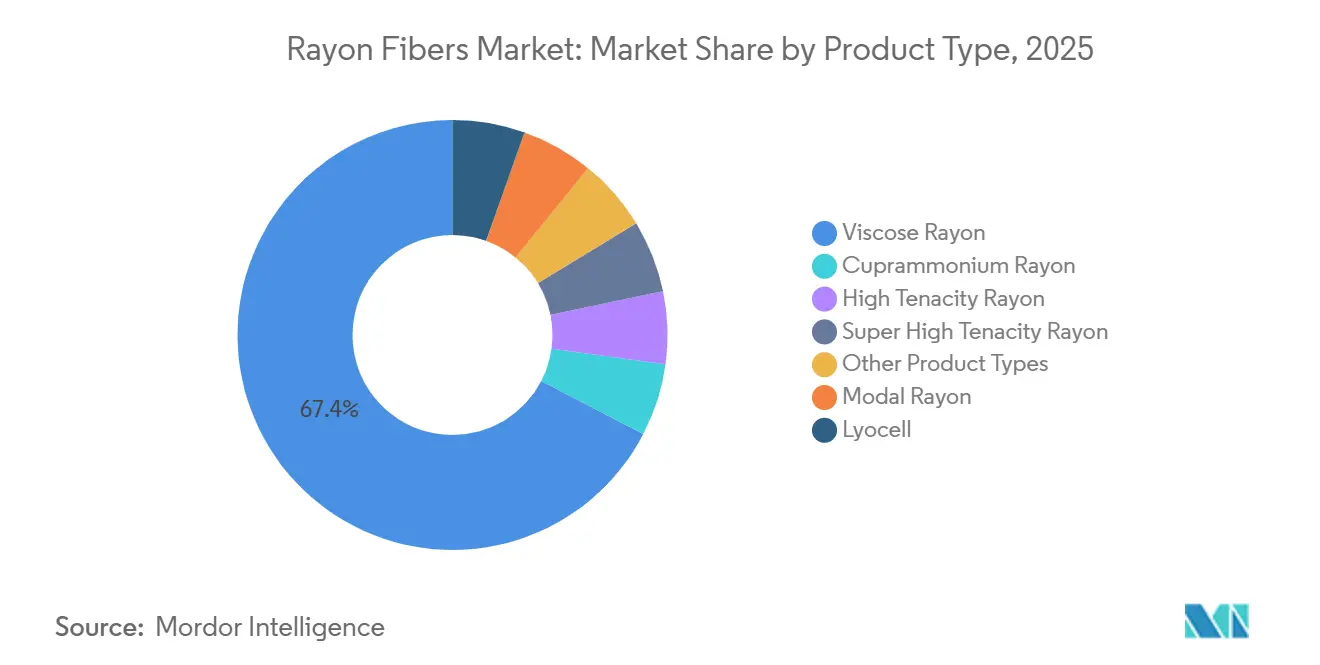

- By product type, viscose rayon led with 67.38% of the Rayon fibers market share in 2025, while lyocell is forecast to expand at an 8.52% CAGR through 2031.

- By fiber form, staple fiber held 73.82% share in 2025, while filament fiber recorded the highest projected CAGR at 7.11% through 2031.

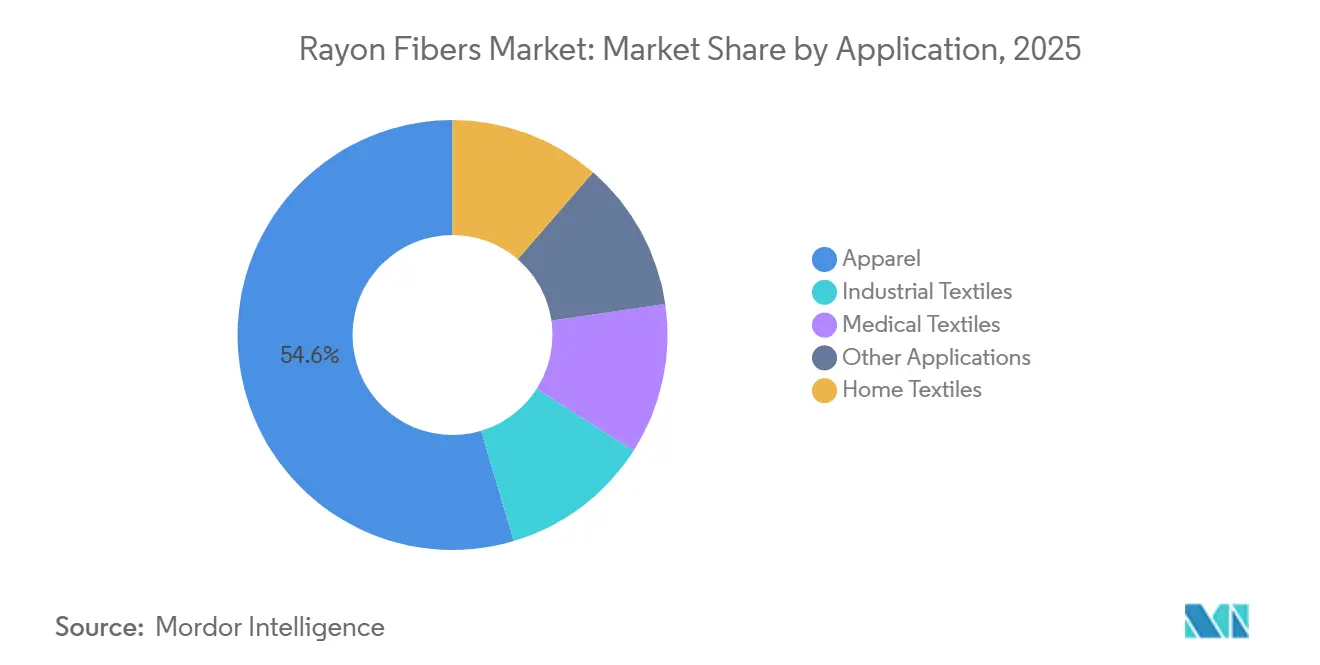

- By application, apparel accounted for 54.61% share of the Rayon fibers market size in 2025, while medical textiles are advancing at a 7.83% CAGR through 2031.

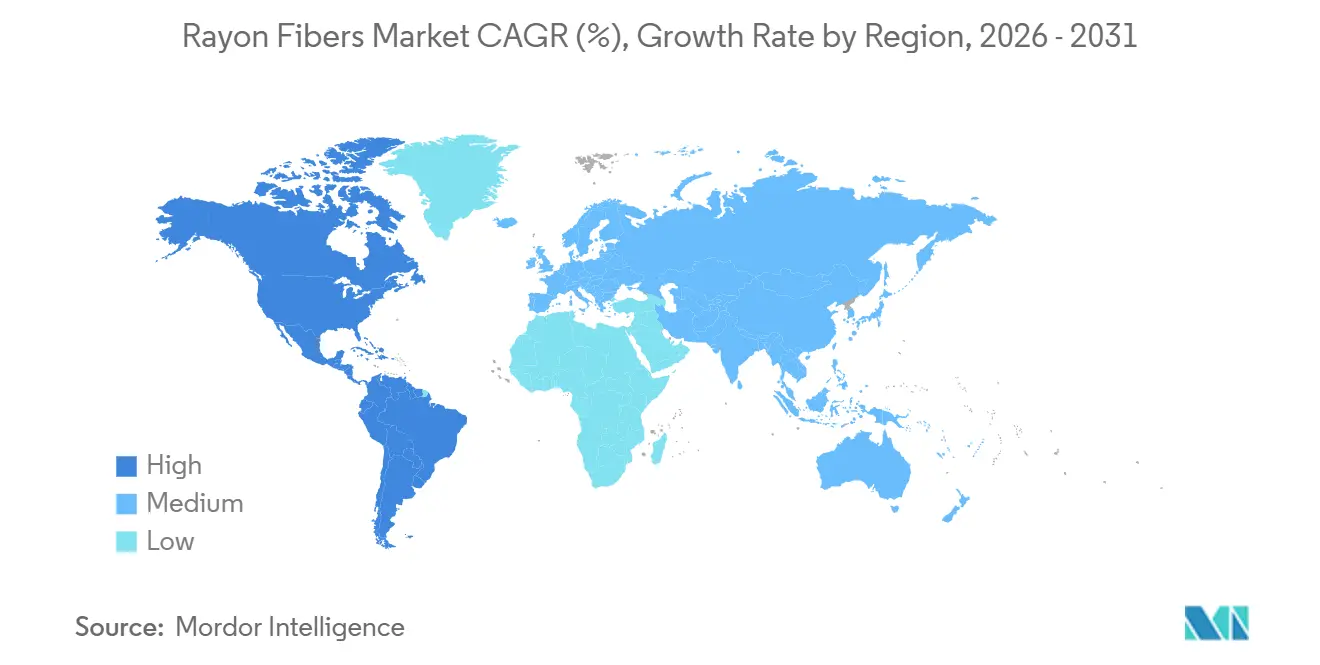

- By geography, Asia-Pacific held 62.44% share in 2025, while North America is projected to grow at a 7.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rayon Fibers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable and Biodegradable Fibers | +2.1% | Global, most acute in North America and the EU | Medium term (2-4 years) |

| Increasing Consumption in Apparel and Home Textiles | +1.8% | Asia-Pacific core, spill-over to South America | Short term (≤ 2 years) |

| Expansion of Lyocell and Modal Fiber Production Capacity | +1.2% | China, India, and the export-linked impact on the EU and North America | Medium term (2-4 years) |

| Growth of Eco-Friendly Fashion Initiatives | +0.9% | EU, North America, Japan | Medium term (2-4 years) |

| Increasing Use of Regenerated Cellulose Fibers Across Sectors | +0.7% | Global, concentrated in Asia-Pacific and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable and Biodegradable Fibers

The rayon fibers market is benefiting from greater buyer focus on fiber biodegradability and reduced dependence on fossil-derived materials. Concerns over synthetic microplastic contamination are prompting sustainability teams to incorporate fiber selection into formal sourcing standards, rather than treating it as a voluntary brand commitment. The market is also seeing a clearer distinction between conventional viscose and closed-loop lyocell, as buyers now evaluate chemical intensity and solvent recovery as separate criteria rather than grouping all regenerated cellulosics together. Birla Cellulose's Livaeco Lyocell, with up to 99.7% solvent recovery and 100% Forest Stewardship Council (FSC)-certified wood pulp, illustrates how closed-loop processing and documented sourcing are becoming purchasing criteria for premium cellulosics[1]Birla Cellulose, “Livaeco Lyocell Fibre – Sustainable Cellulosic Textile Solution,” Liva by Birla Cellulose, livabybirlacellulose.com. As procurement standards tighten, this demand pattern is extending beyond apparel into home textiles and hygiene applications, where traceable raw materials are increasingly important.

Expansion of Lyocell and Modal Fiber Production Capacity

The rayon fibers market is shifting as lyocell production moves from specialty-scale output to larger, more standardized volumes. Global lyocell capacity exceeded 1.3 million tons by 2025, and Sateri's lyocell capacity reached 600,000 metric tons across four sites in 2026 following the start of production at its Yutai facility in Shandong province. Grasim Industries Limited operates 890,000 tons per annum (TPA) of cellulosic staple fiber at 97% utilization in fiscal year 2026 and has approved a Phase II lyocell expansion at Harihar for INR 3,094 crore (USD 324 million), building toward 210,000 TPA of total lyocell capacity upon completion of Phase I and Phase II. This shift is expected to result in lower unit costs and broader adoption in mid-market apparel categories that had previously considered lyocell too expensive. Modal is also expected to benefit, as buyers increasingly apply tiered sourcing policies that place viscose, modal, and lyocell on a defined scale of cost and sustainability performance.

Growth of Eco-Friendly Fashion Initiatives

The rayon fibers market is being shaped by fashion supply chains that now link material selection more directly to traceability and verified sourcing. Producers that can document forest origin, solvent handling, and chain-of-custody are gaining a stronger commercial position with brands that apply closer scrutiny to sustainability claims. Birla Cellulose's Livaeco lyocell reflects this direction by combining certified wood pulp with documented closed-loop recovery, making transparency a product attribute rather than a background claim. The market is therefore moving toward a structure where undifferentiated fiber supply faces greater pressure, while fibers supported by certification and process disclosure gain better access to premium channels. This shift is raising standards across all suppliers, particularly in Europe, North America, and Japan, where brand compliance requirements tend to advance faster than fiber capacity.

Increasing Use of Regenerated Cellulose Fibers Across Sectors

The rayon fibers market is expanding beyond fashion, as regenerated cellulose offers moisture absorption, softness, skin comfort, and biodegradability across multiple end uses. These properties support demand in medical, personal care, wipes, and hygiene products, where petroleum-based substrates face increasing scrutiny. In 2025, Lenzing AG expanded VEOCEL lyocell production at its Prachinburi facility in Thailand, introducing nonwoven-grade lyocell fibers in Asia for the first time and improving regional access for wipes, facial masks, and hygiene products. Also in 2025, Lenzing AG introduced hygiene products featuring VEOCEL lyocell fibers to the North American market in partnership with Edgewell Personal Care, indicating that bio-based nonwovens can compete in premium hygiene categories that had long relied on fossil-derived inputs. As a result, the rayon fibers market is developing a demand base that is less dependent on apparel cycles and more closely aligned with recurring healthcare and personal care consumption.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carbon Disulfide and Effluent Compliance Raising Production Costs | -1.2% | Global, acute in China, India, and the EU | Medium term (2-4 years) |

| Environmental Regulations Governing Viscose Production Methods | -0.8% | EU, with progressive spill-over to APAC export-oriented producers | Long term (≥ 4 years) |

| High Capital Investment for Advanced Lyocell Manufacturing | -0.5% | Global, most limiting in South America and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carbon Disulfide and Effluent Compliance Raising Production Costs

The rayon fibers market faces a cost challenge in conventional viscose production, as CS2 recovery and sulfur-related treatment systems require sustained investment. The U.S. Environmental Protection Agency regulates effluent discharge from viscose rayon plants under the Organic Chemicals, Plastics, and Synthetic Fibers Effluent Guidelines, keeping pollution control closely tied to plant economics[2]United States Environmental Protection Agency, “Organic Chemicals, Plastics and Synthetic Fibers Effluent Guidelines – 40 CFR Part 414,” U.S. EPA, epa.gov. Asia Pacific Rayon's 2025 EU Best Available Techniques (BAT) Assessment Report showed that advanced abatement systems can reduce sulfur-to-air emissions below 20 kg per ton of fiber to meet EU BAT benchmarks, but this level of control requires capital that not every mid-scale producer can sustain. The rayon fibers market also recorded a notable development in Europe when Kelheim Fibres closed operations as of March 31, 2026, after insolvency proceedings failed to secure a viable long-term solution. The Zero Discharge of Hazardous Chemicals (ZDHC) MMCF Guidelines broaden compliance expectations across regenerated cellulose value chains, meaning cost pressure is no longer limited to a narrow group of viscose producers.

Environmental Regulations Governing Viscose Production Methods

The rayon fibers market is also under pressure from broader textile regulation in Europe, where compliance is expanding beyond emissions control into product-level documentation. The EU Ecodesign for Sustainable Products Regulation came into force on July 18, 2024, and the textile delegated act remains under development through 2026, with an impact assessment expected in Q4 2026. The framework does not single out viscose alone, but requirements around recyclability, traceability, substance disclosure, and digital product documentation create a heavier compliance burden for producers of undifferentiated fiber without audited credentials. The European Commission's textile preparatory work is also examining how sustainably sourced renewable cellulosics may be treated within future obligations, which carries commercial importance for suppliers that can demonstrate closed-loop processing and chain-of-custody. As a result, the rayon fibers market is likely to see tighter access conditions in European branded supply chains for conventional viscose producers that cannot provide certified sourcing and verifiable process transparency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Viscose Anchors Volume as Lyocell Narrows the Price Gap

Viscose rayon held 67.38% of the rayon fibers market share in 2025, reflecting its low-cost position, the scale of wet-spinning processes, and wide compatibility with standard spinning and finishing equipment across Asian textile hubs. The rayon fibers market continues to rely on viscose as the volume base because it aligns better with the economics of mass apparel and home textiles than higher-priced regenerated cellulosics. Modal occupied a middle tier between commodity viscose and premium lyocell, with its softer hand-feel and higher moisture absorption supporting use in intimate apparel, sportswear, and premium bedding. Lyocell was the fastest-growing product type, with an 8.52% CAGR through 2031, supported by brand sustainability requirements, the appeal of its closed-loop process, and a narrowing cost gap with viscose as new capacity comes online.

Cuprammonium rayon retained a niche role, mainly in the Japanese luxury apparel segment, where ultra-fine filament characteristics support silk-like drape and surface finish. High tenacity rayon and super high tenacity rayon remained tied to industrial uses such as tire cord reinforcement, industrial belting, and filtration fabrics, where tensile performance and thermal stability matter more than softness. The rayon fibers market is separating more clearly between a large viscose base that supports scale and a smaller lyocell segment that is capturing premium growth. Birla Cellulose's Livaeco Lyocell, made with up to 99.7% solvent recovery and 100% Forest Stewardship Council (FSC)-certified wood pulp, raises the sustainability benchmark that product portfolios in the rayon fibers market increasingly need to meet.

By Fiber Form: Staple Delivers Scale, Filament Commands Premiums

Staple fiber held 73.82% share of global rayon fiber consumption in 2025, reflecting the rayon fibers market's dependence on ring spinning, open-end spinning, and carding systems across Asian manufacturing networks. It remained the default format for viscose use in commodity apparel and home textiles because processing speed, yarn count consistency, and cost efficiency outweigh the visual benefits of filament in large-volume programs. Filament fiber is projected to grow at a 7.11% CAGR through 2031, making it the fastest-growing format within the rayon fibers market. This growth is driven by woven apparel that requires fluid drape, lining fabrics that need smoother surfaces, and hygiene substrates where continuous filament geometry supports more even coverage.

The shift toward filament is tied to premium positioning, as buyers increasingly associate format choice with traceability, product finish, and compliance readiness. Lenzing's Fiber Division generated EUR 1.9 billion (~USD 2.18 billion) in revenue in 2025, of which 36% came from nonwoven fibers, indicating the growing commercial importance of performance-led fiber applications that extend beyond standard staple demand. The rayon fibers market is rewarding suppliers that combine filament performance with documented sourcing rather than competing on format alone. Audited chain-of-custody systems, including Forest Stewardship Council (FSC)-linked documentation, are becoming stronger buying filters in filament programs, particularly where retailers require both visual quality and compliance visibility.

By Application: Apparel Anchors Demand, Medical Textiles Accelerate

Apparel accounted for 54.61% of the rayon fibers market size in 2025, keeping the market aligned with fashion demand, fabric drape, breathability, moisture handling, and dye response. Rayon remains attractive in apparel because it offers a softer, more natural feel than many synthetic alternatives, particularly in categories where touch and appearance influence material choice. Home textiles ranked second and continued to benefit from household formation and rising demand for bedding, curtains, and upholstery across Southeast Asia, South Asia, and Latin America. Industrial textiles formed a separate demand stream through tire cord reinforcement and filtration fabrics, providing the rayon fibers market with demand support outside of apparel cycles.

Medical textiles are growing at a 7.83% CAGR through 2031, making them the fastest-growing application in the rayon fibers market. Growth is tied to rayon-based nonwovens used in wound dressings, surgical drapes, hygiene wipes, and personal care substrates where skin contact and absorbency are important. The rayon fibers market is finding support in this segment, as hypoallergenic performance, moisture absorption, and biodegradability compare favorably with petrochemical nonwovens in several premium-use cases. Other applications, including specialty packaging nonwovens and technical substrates, still represent smaller volumes but are becoming increasingly relevant as producers seek uses beyond traditional textile channels.

Geography Analysis

Asia-Pacific accounted for 62.44% of the global rayon fibers market in 2025, making it the largest region for both production and consumption. China remained the largest single production base, with Tangshan Sanyou, Sateri, and Yibin Grace Group operating at multi-hundred-thousand-ton annual scales. India also played a notable role, as Grasim Industries operated 890,000 tons per annum (TPA) of cellulosic staple fiber at 97% utilization in fiscal year 2026, indicating strong demand and limited spare capacity. Japan remained smaller in volume but relevant in specialty filament and cuprammonium applications tied to luxury apparel and fine drape. South Korea contributed downstream spinning capacity, while Vietnam, Bangladesh, and Indonesia continued to absorb greater volumes of Chinese and Indian fiber through garment assembly networks.

North America is projected to grow at a 7.13% CAGR through 2031, making it the fastest-growing region in the rayon fibers market. Growth is driven less by large domestic fiber output and more by sourcing shifts toward certified sustainable cellulosics. Lenzing's 2025 launch of VEOCEL lyocell-based hygiene products in North America with Edgewell Personal Care demonstrated that premium nonwovens can enter categories long dominated by fossil-derived materials. Mexico is also becoming more relevant, as nearshoring under the United States-Mexico-Canada Agreement (USMCA) framework supports rayon-based garment assembly for U.S. brands seeking shorter supply chains.

Europe represented a meaningful share of global rayon fiber demand in 2025, with the market shaped by fashion, hygiene nonwovens, and sustainability compliance requirements. The EU textiles policy agenda is directing brand procurement toward certified cellulosic fibers with stronger traceability and process documentation. Germany and the United Kingdom remained the largest national markets in Europe, combining strong textile demand with concentrated fashion retail activity. South America, led by Brazil and Argentina, remains a smaller market but is building demand through urbanization and investment in textile manufacturing. The Middle East and Africa also remain early-stage targets for Asian exporters seeking to diversify beyond established intra-Asia trade routes.

Competitive Landscape

The rayon fibers market is moderately fragmented, with a small group of Chinese producers leading in viscose volume and a smaller set of global suppliers competing through traceability and sustainability positioning. Tangshan Sanyou, Sateri, Yibin Grace Group, and Xinxiang Bailu Chemical Fiber form the core of a large-scale viscose supply, while Lenzing AG and Birla Cellulose compete through certified product platforms and premium end-use alignment. The market does not operate as a purely cost-led space, as buyer requirements now distinguish commodity fiber from branded and audited cellulosic offerings. Lenzing's Fiber Division generated EUR 1.9 billion in revenue in 2025 from 904,000 tons of fiber; 61% of group revenue came from Asia and 29% from Europe, including Turkey. This geographic mix indicates that even European-headquartered suppliers depend heavily on Asian demand and that competition in the rayon fibers market is increasingly shaped by the ability to supply Asia at scale while meeting European and North American compliance requirements.

Strategic developments in 2026 have reinforced this pattern. Grasim Industries approved a Phase II lyocell expansion at Harihar for INR 3,094 crore (USD 324 million), adding 110,000 Tons Per Annum (TPA) across 2 production lines and bringing the planned total lyocell capacity to 210,000 TPA upon full completion. Lenzing had already expanded VEOCEL lyocell production in Thailand in 2025, strengthening its position in biodegradable nonwovens for Asian customers. These developments indicate that the rayon fibers market is moving toward larger capacity clusters supported by stronger application specialization.

The closure of Kelheim Fibres in March 2026 altered the competitive landscape by removing Europe's only specialty viscose producer for hygiene nonwovens. This gap creates an opportunity for suppliers with nonwoven-grade lyocell and stronger compliance credentials to capture displaced demand, particularly in hygiene applications. Asia Pacific Rayon and other mid-tier producers are working to improve access to global brand supply chains by aligning operations with EU Best Available Techniques (BAT) expectations and Zero Discharge of Hazardous Chemicals (ZDHC) Man-Made Cellulosic Fibers (MMCF) Guidelines. The rayon fibers market is becoming more polarized between producers that can demonstrate process quality and sourcing discipline and those that rely primarily on volume scale and cost position. This dynamic should sustain active competition, but it also raises the entry threshold for smaller producers that lack both capital depth and audited supply chains.

Rayon Fibers Industry Leaders

Lenzing AG

Sateri

Grasim Industries Limited

Xinxiang Bailu Chemical Fibre Group Co., Ltd.

Tangshan Sanyou Group Xingda Chemical Fibre Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Grasim Industries approved INR 3,094 crore (USD 324 million) for a Phase II lyocell expansion at Harihar, Karnataka, adding 110,000 TPA across 2 production lines targeted for commissioning in 2028 and 2030. Combined with the Phase I plant under construction, Grasim's total lyocell capacity will reach approximately 210,000 TPA upon completion.

- January 2026: Sateri signed the Phase III lyocell project agreement in Changzhou, planning to add 360,000 TPA using fifth-generation lyocell line technology, which is characterized by large single-line capacity and advanced process automation. The project targets Liyang as the world's largest lyocell production base upon full completion.

Global Rayon Fibers Market Report Scope

Rayon is a semi-synthetic fiber made from reconstituted cellulose, typically derived from wood pulp or plant materials. Although made from natural polymers, it requires extensive chemical processing to convert the cellulose into soft, versatile filaments that mimic the feel of silk, cotton, or linen.

The rayon fibers market is segmented by product type, fiber form, application, and geography. By product type, the market is segmented into viscose rayon, modal rayon, lyocell, cuprammonium rayon, high tenacity rayon, super high tenacity rayon, and other product types. By fiber form, the market is segmented into staple fiber and filament fiber. By application, the market is segmented into apparel, home textiles, industrial textiles, medical textiles, and other applications. The report also covers market size and forecasts for rayon fibers across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Viscose Rayon |

| Modal Rayon |

| Lyocell |

| Cuprammonium Rayon |

| High Tenacity Rayon |

| Super High Tenacity Rayon |

| Other Product Types |

| Staple Fiber |

| Filament Fiber |

| Apparel |

| Home Textiles |

| Industrial Textiles |

| Medical Textiles |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Viscose Rayon | |

| Modal Rayon | ||

| Lyocell | ||

| Cuprammonium Rayon | ||

| High Tenacity Rayon | ||

| Super High Tenacity Rayon | ||

| Other Product Types | ||

| By Fiber Form | Staple Fiber | |

| Filament Fiber | ||

| By Application | Apparel | |

| Home Textiles | ||

| Industrial Textiles | ||

| Medical Textiles | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Rayon Fibers Market?

The Rayon Fibers Market size is expected to increase from USD 22.17 billion in 2025 to USD 23.65 billion in 2026 and reach USD 32.52 billion by 2031, and is expected to grow at a CAGR of 6.58% over 2026-2031.

Which product type leads in rayon fibers today?

Viscose rayon led demand with a 67.38% share in 2025 because it remains the lowest-cost regenerated cellulosic option for large-scale textile production.

Which product segment is growing the fastest in rayon fibers?

Lyocell is the fastest-growing product type with an 8.52% CAGR through 2031, helped by stronger sustainability requirements and expanding production capacity.

Why is Asia-Pacific so important in rayon fibers?

Asia-Pacific held a 62.44% share in 2025 because it combines the largest pulp-to-fiber production base with the world’s biggest apparel and home textile manufacturing ecosystem.

Page last updated on: