Rare Disease Contract Research Organization (CRO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

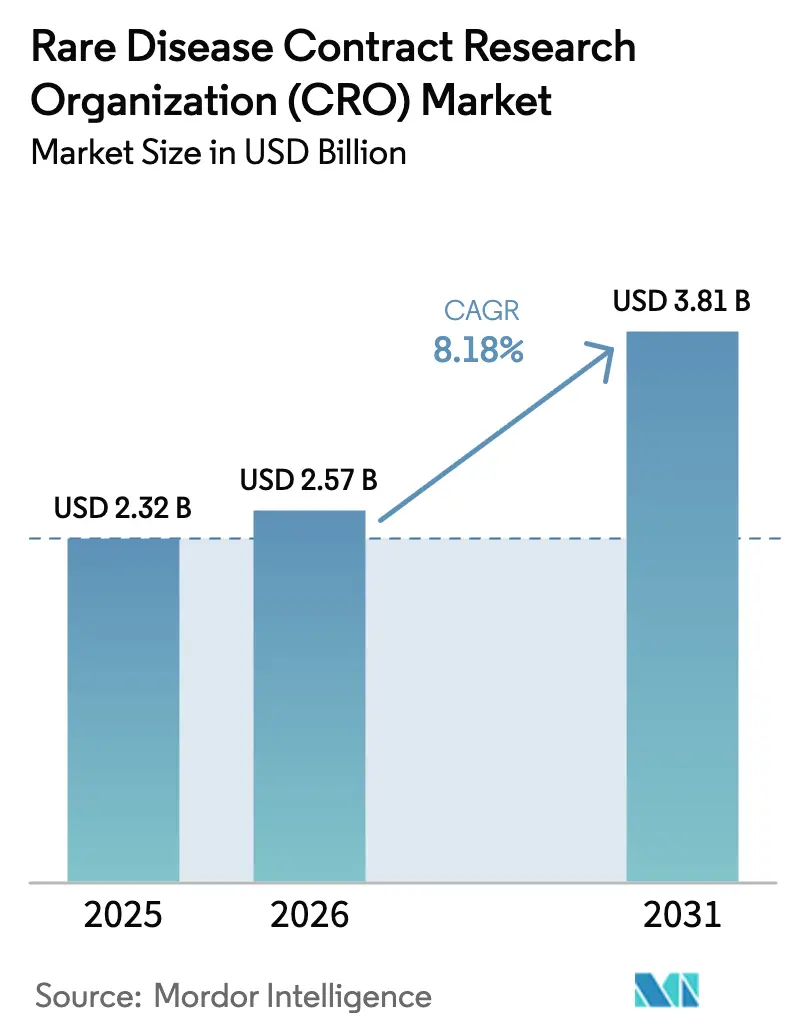

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rare Disease Contract Research Organization (CRO) Market Analysis by Mordor Intelligence

The Rare Disease Contract Research Organization Market size is projected to expand from USD 2.32 billion in 2025 and USD 2.57 billion in 2026 to USD 3.81 billion by 2031, registering a CAGR of 8.18% between 2026 to 2031.

This trajectory reflects a decisive pivot by drug developers toward outsourcing the intricate logistics of ultra-rare disease trials, often involving fewer than 1,000 patients worldwide, to specialist contract research organizations (CROs). Sponsors are prioritizing speed, geographic reach, and regulatory fluency, while regulators are sustaining momentum: the U.S. Food and Drug Administration (FDA) granted 34 orphan drug designations in the first quarter of 2024 alone. Gene and cell therapies now dominate new rare-disease pipelines, as illustrated by the European approval of Lenmeldy for metachromatic leukodystrophy in March 2024 and the U.S. clearance of Casgevy and Lyfgenia for sickle cell disease in December 2023, each requiring multi-site CRO coordination across continents. Economic incentives reinforce demand; the Inflation Reduction Act’s carve-out for orphan biologics exempts qualifying therapies from Medicare negotiation for 13 years post-approval, extending the window for post-marketing registries that CROs manage.

Key Report Takeaways

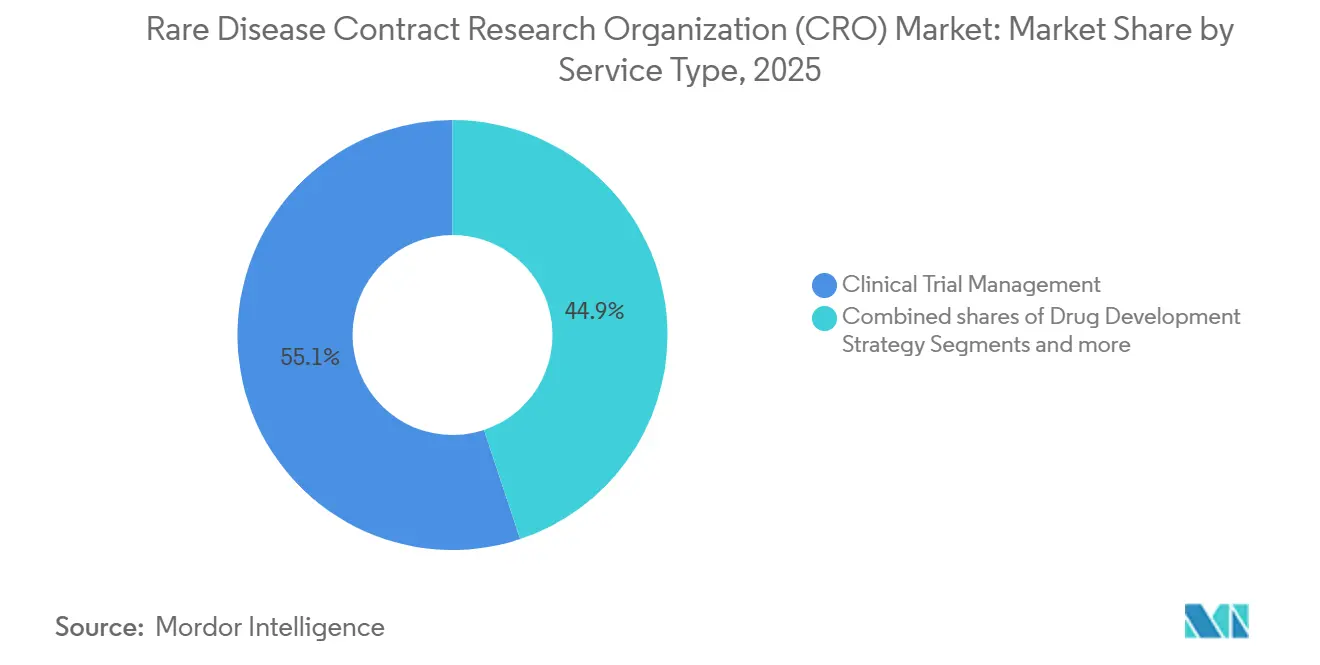

- By service type, Clinical Trial Management led with a 55.10% revenue share in 2025, while Data Management & Biostatistics is advancing at a 9.20% CAGR through 2031.

- By therapeutic area, oncology held 35.1% of the rare disease contract research organization (CRO) market share in 2025; neuroscience is projected to register the fastest 9.15% CAGR to 2031.

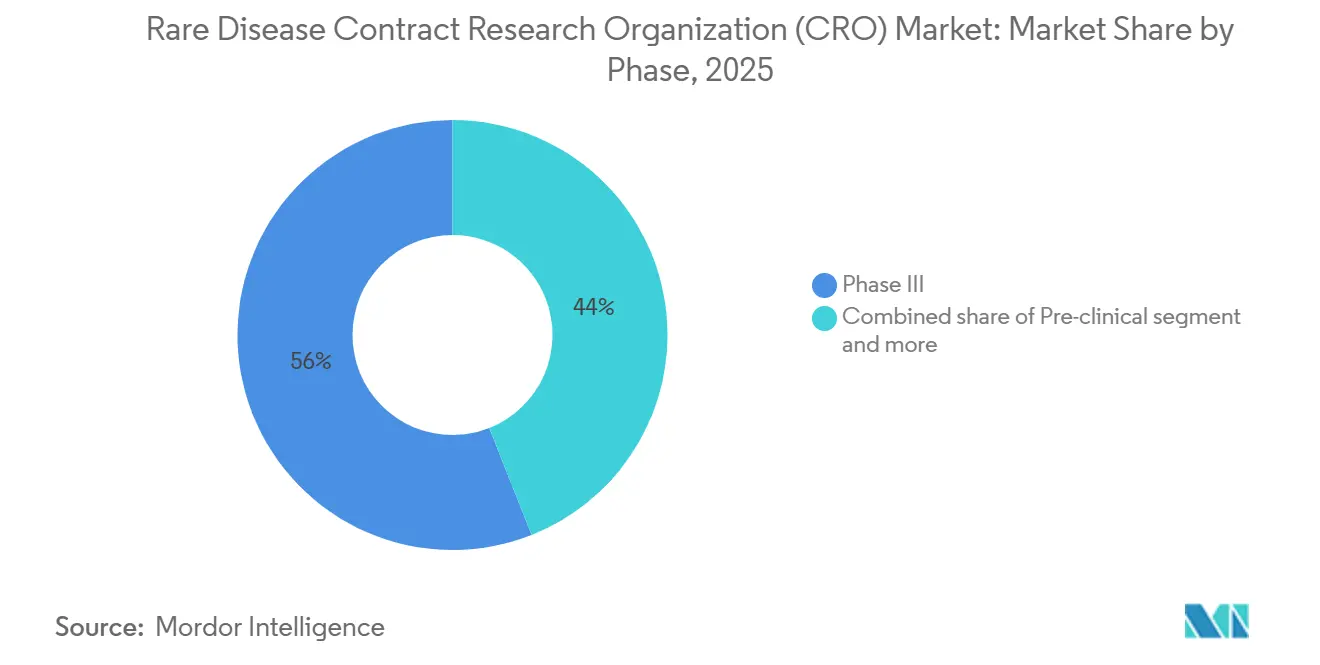

- By phase, Phase III captured 56% of revenue in 2025, yet Phase I is expanding at an 8.90% CAGR as sponsors outsource first-in-human studies earlier in development.

- By end-user, pharma & biotech companies accounted for 72.30% of spending in 2025, whereas non-profit & government sponsors are scaling at an 8.80% CAGR through 2031.

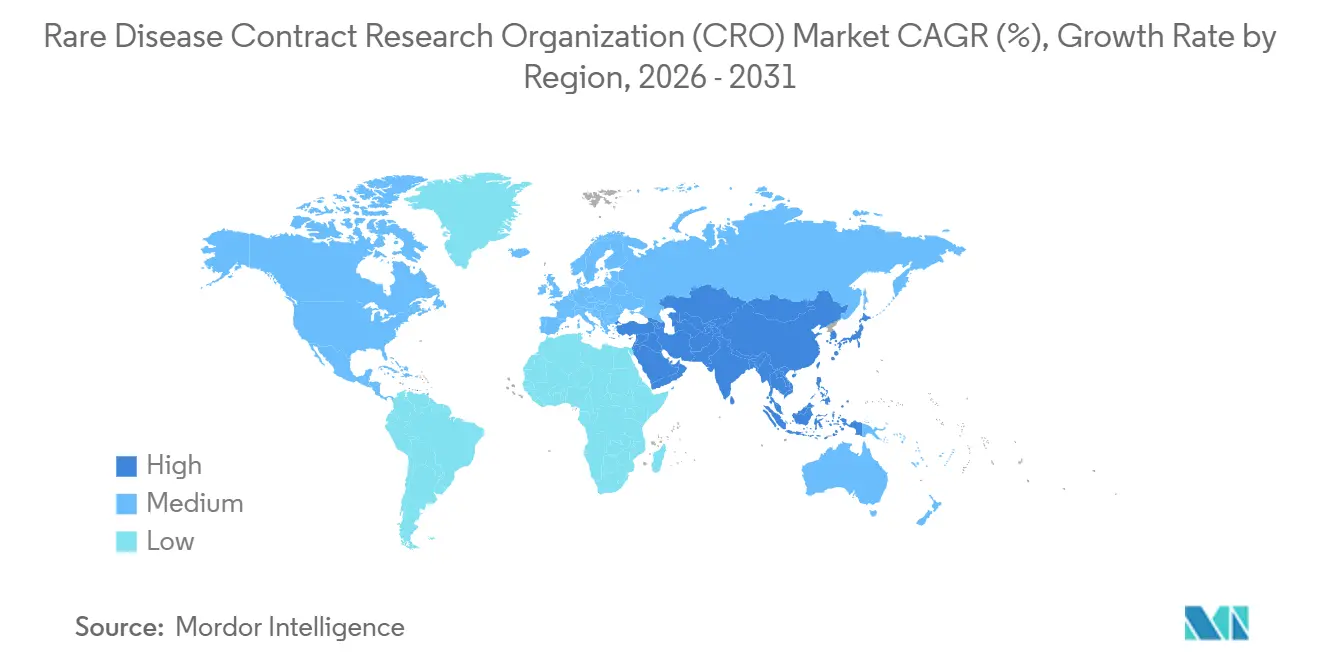

- By geography, North America held 47.5% of the rare disease contract research organization (CRO) market size in 2025, while Asia-Pacific is forecast to be the fastest-growing region at 9.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rare Disease Contract Research Organization (CRO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence & awareness of rare diseases | +1.4% | Global, with accelerated diagnosis in North America & EU | Medium term (2-4 years) |

| Regulatory incentives (Orphan Drug Act, EU frameworks) | +1.8% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Surge in gene & cell therapy pipelines | +2.1% | North America & EU, early adoption in China & Japan | Medium term (2-4 years) |

| Rising outsourcing of complex orphan trials | +1.5% | Global, led by US & EU biotech hubs | Short term (≤ 2 years) |

| AI-driven patient-matching registries | +0.9% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| IRA-exemption expansion via OBBB Act | +0.7% | United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence & Awareness of Rare Diseases

Patient advocacy networks and newborn-screening programs have cut the average diagnostic journey from seven years in 2015 to under three years in 2025, enlarging the trial-eligible population for CROs. The National Organization for Rare Disorders logged a 42% rise in member inquiries between 2023 and 2025, evidencing better disease literacy among caregivers and clinicians [1]National Organization for Rare Disorders, “Rare Disease Patient Engagement Report 2024,” rarediseases.org. EveryLife Foundation reported that 68% of rare-disease patients joined at least one registry in 2024, up from 51% in 2022, giving CROs readily searchable cohorts for feasibility work. Centralized Gaucher disease registries maintained by industry sponsors now aggregate more than 10,000 patients worldwide, enabling Phase III studies to complete enrollment in 18 months rather than the historical 36. Accelerated genetic testing in neonatal intensive-care units is surfacing ultra-rare phenotypes such as aromatic L-amino-acid decarboxylase deficiency, creating fresh pipelines of enzyme-replacement and gene-augmentation studies that CROs coordinate.

Regulatory Incentives for Orphan Therapeutics

The FDA’s Rare Disease Evidence Principles, finalized in June 2024, permit sponsors to replace concurrent control arms with curated natural-history data in trials enrolling fewer than 200 patients, trimming an estimated year from development timelines [2]U.S. Food and Drug Administration, “Biologics License Approvals 2023–2024,” fda.gov. In Europe, orphan designation confers 10 years of exclusivity and free protocol assistance, spurring 312 applications in 2024, up 19% from 2023. Japan widened its SAKIGAKE fast-track program in 2025 to include ultra-rare metabolic and neuromuscular disorders, halving review cycles to six months for qualifying therapies. These frameworks collectively lower regulatory friction, catalyze capital deployment, and expand the serviceable addressable market for CROs.

Surge in Gene & Cell Therapy Pipelines

Gene and cell therapies accounted for 27% of orphan approvals in 2024 versus 18% in 2022, reflecting maturing viral-vector manufacturing and ex vivo engineering that CROs orchestrate. Casgevy and Lyfgenia, cleared in December 2023, each carry 15-year post-marketing surveillance mandates that CROs must deliver. Lenmeldy’s European approval in March 2024 required four years of multi-site coordination to enroll 37 patients, underscoring the operational intensity that drives outsourcing. The NIH-led Bespoke Gene Therapy Consortium launched in 2024 with USD 25 million to develop individualized vectors for conditions affecting fewer than 30 patients worldwide, a model entirely dependent on CRO infrastructure.

Rising Outsourcing of Complex Orphan Trials

Sixty-four percent of Phase I rare-disease studies were CRO-managed in 2025, up from 48% in 2020, as virtual trial models gain regulator acceptance and strain small-company bandwidth. FDA guidance on remote data capture, issued December 2023, legitimized home-based assessments, yet demands validation that many sponsors delegate to CROs. The EU Clinical Trials Regulation, fully in force since January 2023, created a single submission portal but preserved national ethical oversight, driving demand for regulatory-consulting expertise to navigate country-specific amendments. Sponsors cite cost avoidance and speed as primary motives: a 50-patient Phase III study executed across four regions incurs USD 8.2 million in incremental regulatory and site-activation spend compared with a U.S.-only design, a premium that CRO scale mitigates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient-recruitment scarcity & dispersion | -1.2% | Global, acute in ultra-rare conditions (<5,000 cases) | Short term (≤ 2 years) |

| High cost of multi-regional micro-cohort trials | -0.9% | Global, pronounced in emerging markets | Medium term (2-4 years) |

| Stringent ESG compliance for suppliers | -0.4% | EU & North America, expanding to APAC | Long term (≥ 4 years) |

| Cross-border genomic-data privacy barriers | -0.6% | EU & North America, friction in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patient-Recruitment Scarcity & Dispersion

Ultra-rare disorders with worldwide prevalence below 5,000 cases require recruitment timelines exceeding 48 months, delaying submissions and inflating CRO budgets. FDA analysis of orphan approvals in 2024 showed trials for diseases affecting fewer than 1 in 100,000 people took an average of 4.2 years from first-patient-in to database lock, versus 2.8 years for more prevalent rare disorders. Decentralized designs reduce travel but must still pass equivalence testing against in-clinic endpoints, extending protocol build by six to nine months. Advocacy groups mitigate friction 73% of metabolic-disorder participants learned of trials via such channels in 2025, but oncology recruitment lags, as only 41% of rare-cancer patients rely on advocacy referrals [3]Global Genes, “Patient Recruitment and Advocacy Report 2025,” globalgenes.org. Per-patient CRO costs for ultra-rare Phase III programs run 2.5 times higher than standard oncology trials owing to specialized navigators and elongated site-startup cycles.

High Cost of Multi-Regional Micro-Cohort Trials

Executing micro-cohort studies across multiple jurisdictions drives steep overhead. Although the EU’s single-portal regulation simplifies initial filing, country ethics boards can impose divergent consent language, forcing CROs to juggle parallel protocol versions. China’s National Medical Products Administration (NMPA) demands domestic bridging PK studies even when global data exist, adding 12–18 months and USD 3–5 million to CRO invoices. India’s fast-track framework, launched in 2024, improves review speeds but mandates clinical-trial insurance up to USD 250,000 per participant, inflating budget lines. The compounded expense discourages capital-constrained biotechs or drives them toward regional enrollment strategies, limiting sample diversity and statistical power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Trial Management Anchors Revenue, Biostatistics Captures Innovation Premium

Clinical Trial Management contributed 55.10% of 2025 revenue, a reflection of decentralized trial logistics and real-time oversight needs in the rare disease CRO market. The FDA’s remote-data-capture guidance obliges validation of home-based endpoints, adding six to nine months of effort that CROs absorb. Data Management & Biostatistics, while smaller in absolute terms, is the fastest-growing line at 9.20% CAGR, propelled by Bayesian adaptive designs and master protocols evaluating multiple therapies within a single cohort. Regulatory & Consulting services gain relevance under Europe’s single-portal system, which paradoxically elevates complexity as country-specific ethics amendments proliferate. Drug-development strategy work, including pharmacovigilance and patient-registry design, has accelerated under the IRA orphan-biologics exemption that extends commercial life and demands long-term evidence.

Gene and cell therapies account for 27% of orphan drug approvals and require CRO fluency in viral-vector handling, chain-of-identity logistics, and 15-year follow-up. Bluebird Bio’s Lyfgenia illustrates the burden: the FDA-mandated decade-plus surveillance that the sponsor outsourced to a hematology-registry specialist. Small-molecule rare-disease programs rely more on classic monitoring and regulatory consulting. The NIH-funded Bespoke Gene Therapy Consortium bets entirely on CROs for individualized vectors in cohorts as small as 30 patients. Sponsors therefore gravitate toward modality-specific expertise, favoring mid-tier players such as Precision for Medicine and Novotech over generalists.

By Therapeutic Area: Oncology Dominates, Neuroscience Accelerates on Gene-Therapy Momentum

Oncology controlled 35.1% of 2025 revenue in the rare disease CRO market, buoyed by CAR-T and precision programs targeting low-incidence cancers. Bristol Myers Squibb’s Abecma for multiple myeloma and Gilead’s Yescarta for large B-cell lymphoma demand leukapheresis logistics and safety oversight across 20-plus sites, reinforcing CRO reliance. Neuroscience, led by Duchenne muscular dystrophy and spinal muscular atrophy gene therapies, is projected to grow at a 9.15% CAGR through 2031. The FDA’s approval of Elevidys in June 2023 required enrollment across 15 countries, spotlighting the geographic reach CROs supply.

Ophthalmology remains niche yet lucrative; Spark Therapeutics’ Luxturna validated retinal gene therapy and catalyzed follow-on pipelines now in Phase II/III under CRO stewardship. Cardiovascular rare diseases are re-emerging after tafamidis meglumine’s 2024 approval shortened typical timelines from five years to 30 months. Metabolic disorders are transitioning toward gene-augmentation as AAV trials show supraphysiologic enzyme levels, increasing demand for vector-distribution logistics, and 10-year registries that CROs manage. Across categories, biomarker-driven eligibility compresses enrollment but lifts screening costs; whole-exome sequencing adds a 3.2-fold premium relative to phenotype-only trials.

By Phase: Late-Stage Trials Dominate Revenue, Early-Phase Outsourcing Accelerates

Phase III captured 56% of 2025 revenue, consistent with the capital intensity of pivotal rare-disease studies. FDA endorsement of external natural-history comparators reduces sample-size requirements but entrusts CROs with curation and statistical adjustment. Phase I, growing at 8.90% CAGR, signals early outsourcing as sponsors de-risk first-in-human work for gene therapies and antisense oligonucleotides. Phase II occupies a middle ground, with sponsors often retaining strategy oversight but outsourcing site management. Post-marketing commitments are expanding under the IRA exemption; one-time gene therapies priced above USD 2 million require long-term durability evidence, a task CROs fulfill through registries and claims-data linkages.

By End-Users: Pharma & Biotech Anchor Demand, Non-Profit Sponsors Scale Rapidly

Pharma and biotech firms represented 72.30% of spending in 2025, with companies with fewer than 50 employees outsourcing the majority of clinical operations to CROs. Non-profit and government sponsors, paced by NIH and European Commission programs, are growing at 8.80% CAGR by leveraging public grants to underwrite ultra-rare initiatives. The Bespoke Gene Therapy Consortium funnels funding directly into CRO-managed individualized vector programs. Academic investigators remain seedbeds for proof-of-concept data, accounting for 41% of orphan approvals transitioned to industry between 2020 and 2024. Patient-led foundations fund natural-history studies and biomarker work that CROs convert into streamlined development packages.

Geography Analysis

North America held a 47.5% share of the rare disease CRO market in 2025, supported by the U.S. Orphan Drug Act tax credit that offsets 25% of qualified trial spending and by clusters of gene-therapy innovators in Boston, San Francisco, and the Research Triangle. The FDA’s 34 orphan designations in Q1 2024 underscore continuing regulatory priority. The IRA exemption extends commercial life by 13 years for qualifying biologics, encouraging robust Phase IV investment. Canada contributes expedited review through its Orphan Drug Framework, while Mexico offers cost-effective enrollment for Latin American populations.

Asia-Pacific is forecast to achieve the most rapid 9.50% CAGR through 2031, propelled by China’s NMPA fast-track rare-disease pathway and India’s 2024 accelerated-approval framework. China issued 12 orphan designations in H1 2024, up 50% year on year, reinforcing CRO demand. Japan’s SAKIGAKE expansion halves review cycles, prompting CRO site-network investment. Australia and South Korea streamline Phase I/II ethics approvals, attracting Western sponsors. Data-localization under China’s Personal Information Protection Law forces CROs to maintain parallel servers and prolongs database lock by six weeks.

Europe remains steady, with Germany, the United Kingdom, France, Italy, and Spain accounting for the majority of regional spend. EMA orphan designation recorded 312 applications in 2024. The EU Clinical Trials Regulation simplifies submission yet preserves national amendment authority, reinforcing demand for regulatory consulting. Post-Brexit data transfer now requires standard contractual clauses, adding four to six weeks to timelines. The Middle East & Africa and South America act chiefly as supplemental enrollment regions; South Africa introduced an orphan pathway in 2024, while Brazil’s ANVISA shortened rare-disease reviews to 12 months, though currency volatility tempers enthusiasm.

Competitive Landscape

The rare disease CRO market shows moderate fragmentation: the top five players IQVIA, ICON, Parexel, Medpace, and Labcorp Drug Development, hold majority of the share. IQVIA generated USD 14.4 billion in 2024, with rare-disease programs forming 18% of its clinical-solutions revenue. Syneos Health’s 2024 bankruptcy created white-space opportunities for agile entrants specializing in decentralized trials and AI-based registries. CROs with modality-specific expertise lead gene-therapy opportunities; viral-vector logistics and 15-year follow-up commitments differentiate service offerings. Technology adoption is decisive: AI-powered patient-matching platforms such as MPACT cut screening failure to 22%, justifying premium pricing. CROs that validate proprietary digital endpoints six to nine months faster than peers command higher margins. Ancillary-service consolidation continues: a large number of CROs now provide in vivo toxicology, meeting sponsor demand for integrated packages.

Rare Disease Contract Research Organization (CRO) Industry Leaders

-

IQVIA

-

ICON

-

Parexel

-

Medpace

-

Labcorp Drug Development

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mendra launched with USD 82 million to apply AI-driven drug-discovery approaches to ultra-rare conditions.

- January 2026: Thermo Fisher announced plans to acquire Clario Holdings, integrating endpoint-data solutions across every phase of development.

- May 2025: Comac Medical Group bought ILIFE Consulting to build a pan-European full-service CRO focused on rare diseases and early-phase trials.

Global Rare Disease Contract Research Organization (CRO) Market Report Scope

As per the scope of the report, a rare disease CRO is a specialized service provider that manages clinical trials for conditions affecting small patient populations, often referred to as orphan diseases. Unlike traditional CROs that handle large-scale studies, rare disease specialists focus on high-complexity trials where patient recruitment is extremely challenging due to the geographic dispersion of participants. These organizations provide end-to-end support, including protocol design tailored for small sample sizes, regulatory navigation for orphaned drug designations, and patient-centric recruitment strategies that frequently involve direct collaboration with global patient advocacy groups.

The rare disease CRO Market is segmented by service type, therapeutic area, phase, end-users, and geography. By service type, the market is categorized into drug development strategy, clinical trial management, data management & biostatistics, regulatory & consulting, and other specialist services. By therapeutic area, the market is divided into cardiovascular, neuroscience, ophthalmology, oncology, metabolic & other. By phase, it is segmented into Pre-clinical, Phase I, Phase II, Phase III, and Phase IV. By end-users, the segmentation includes pharma & biotech companies, non-profit & government sponsors, academic & research institutes, and others. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Drug Development Strategy |

| Clinical Trial Management |

| Data Managemet & Biostatistics |

| Regulatory & Consulting |

| Other Specialist Services |

| Cardiovascular |

| Neuroscience |

| Ophthalmology |

| Oncology |

| Metabolic & Other |

| Pre-clinical |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Pharma & Biotech Companies |

| Non-profit & Gov’t Sponsors |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Drug Development Strategy | |

| Clinical Trial Management | ||

| Data Managemet & Biostatistics | ||

| Regulatory & Consulting | ||

| Other Specialist Services | ||

| By Therapeutic Area | Cardiovascular | |

| Neuroscience | ||

| Ophthalmology | ||

| Oncology | ||

| Metabolic & Other | ||

| By Phase | Pre-clinical | |

| Phase I | ||

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By End-Users | Pharma & Biotech Companies | |

| Non-profit & Gov’t Sponsors | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the rare disease CRO market?

The rare disease CRO market size was estimated to be USD 2.57 billion in 2026.

How fast is the rare disease CRO market expected to grow?

It is projected to advance at an 8.18% CAGR, reaching USD 3.81 billion by 2031.

Which service segment commands the largest share?

Clinical Trial Management led with a 55.10% revenue share in 2025.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at a 9.50% CAGR through 2031.

Why are gene and cell therapies important for CRO demand?

They require complex logistics, long-term follow-up, and specialized data management that sponsors typically outsource.

Page last updated on: