Radiopharmaceutical CDMO/CMO Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.75 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 9.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Radiopharmaceutical CDMO/CMO Services Market Analysis by Mordor Intelligence

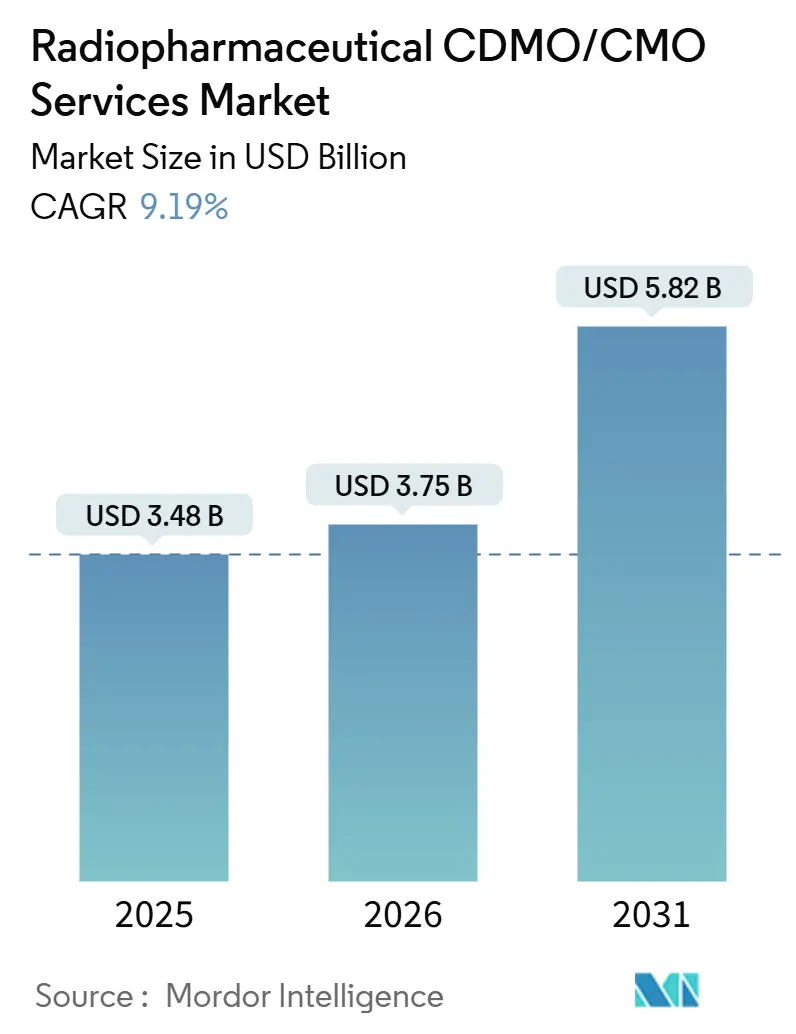

The Radiopharmaceutical CDMO/CMO Services Market size is expected to grow from USD 3.48 billion in 2025 to USD 3.75 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 9.19% CAGR over 2026-2031.

A surge of lutetium-177 radioligand approvals, regional manufacturing hubs that solve half-life logistics, and early investments in actinium-225 supply form the backbone of this advance. Sponsors are outsourcing complex radiochemistry earlier, both to avoid capital outlays on hot cells and to accelerate IND filings. Long-term isotope contracts are now table stakes, while CDMOs that integrate process development with GMP output enjoy higher margins. Capacity expansions in North America and Europe still dominate, yet Asia-Pacific’s cyclotron build-out is shifting volumes closer to patients, mitigating decay-related losses during transport.

Key Report Takeaways

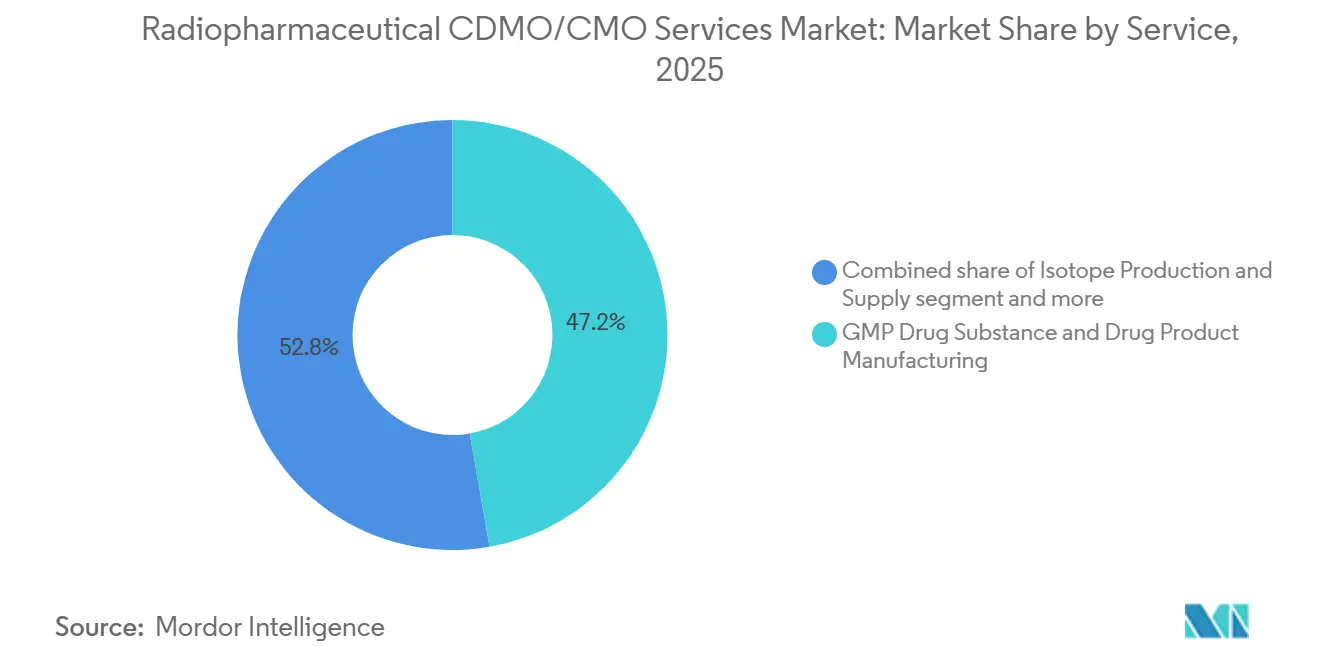

- By service, GMP Drug Substance & Drug Product Manufacturing held 47.24% of the Radiopharmaceutical CDMO/CMO Services Market share in 2025; Process Development & Radiolabeling/Conjugation is growing at a 10.40% CAGR through 2031.

- By modality, diagnostic radiopharmaceuticals led with 58.36% revenue share in 2025, while therapeutic products are projected to expand at a 9.76% CAGR through 2031.

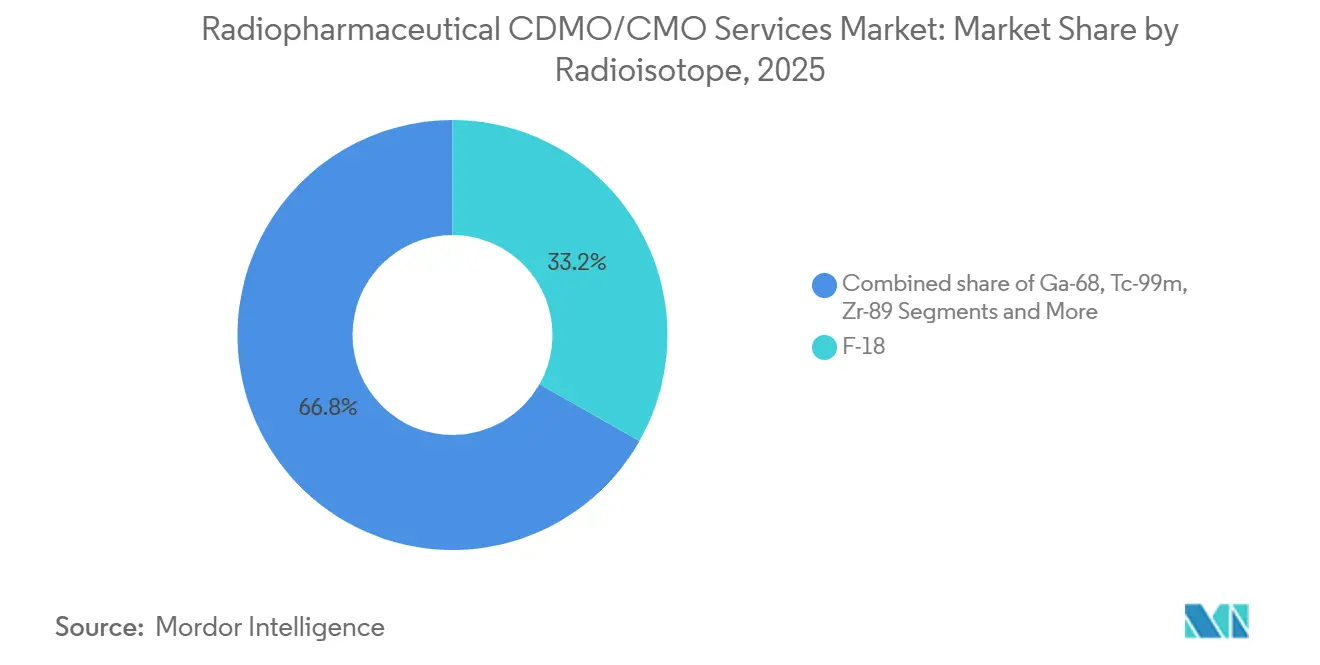

- By radioisotope, F-18 accounted for 33.27% of the Radiopharmaceutical CDMO/CMO Services Market size in 2025, and lutetium-177 is advancing at a 9.95% CAGR to 2031.

- By scale of operation, clinical-stage services made up 38.87% of 2025 revenue; preclinical outsourcing posts the highest forecast CAGR at 9.58% to 2031.

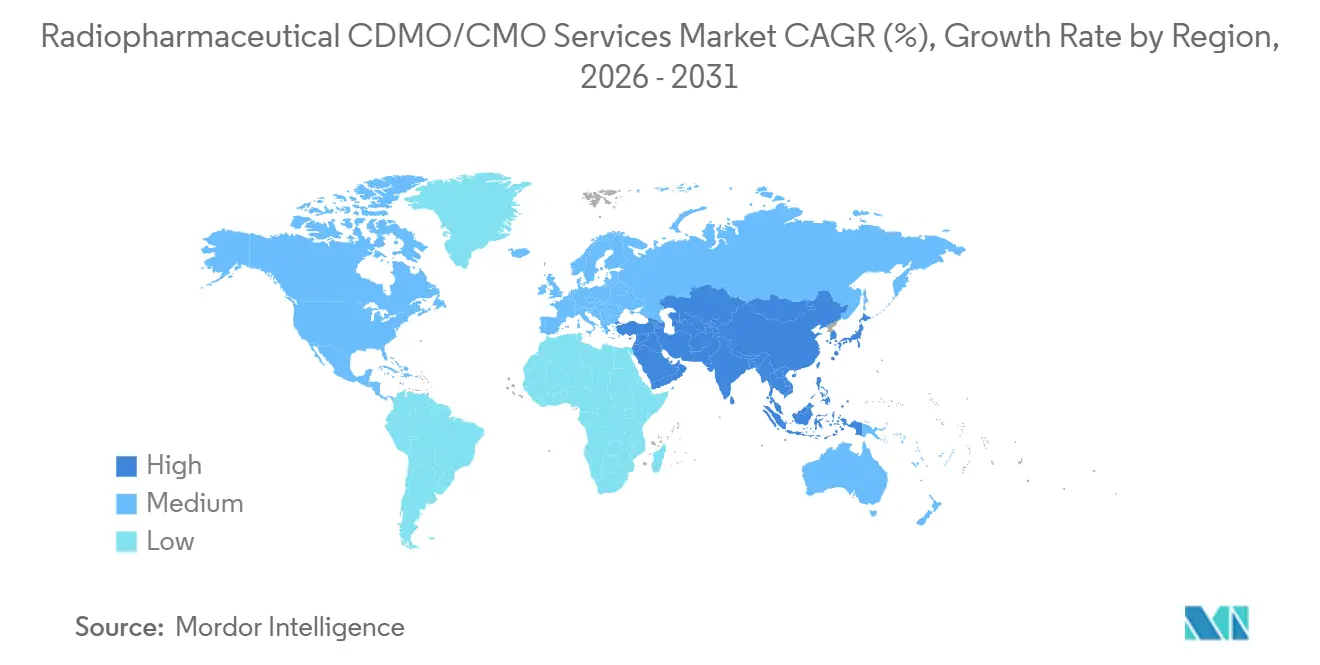

- By geography, North America held 47.35% share in 2025; Asia-Pacific is registering the fastest regional CAGR at 9.60% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Radiopharmaceutical CDMO/CMO Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| RLT approvals elevate outsourced GMP demand | +2.1% | Global, with North America and Europe leading regulatory pathways | Medium term (2-4 years) |

| Regionalization boosts APAC outsourcing | +1.8% | North America, Asia-Pacific (China, Japan, India, Australia) | Long term (≥ 4 years) |

| Lu-177 and Ac-225 investment catalyzes new programs | +2.3% | Global, with supply hubs in North America, Europe, and emerging APAC nodes | Medium term (2-4 years) |

| Specialist CDMOs add capacity and sites | +1.5% | Global, concentrated in North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Decentralized networks beat half-life losses | +1.2% | Global, with regional hubs in North America, Europe, APAC | Medium term (2-4 years) |

| Alpha-emitter containment expertise emerges | +0.9% | North America and Europe, with selective APAC sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

RLT Approvals and Scaling Raise Outsourced GMP Demand

Commercial-stage lutetium-177 therapies have moved batch volumes from grams to kilograms, tightening GMP slots at dual-licensed plants. Sponsors now reserve capacity two years ahead, as shown by Eckert & Ziegler’s March 2025 deal with Actinium Pharmaceuticals for actinium-225 supply [1]Eckert & Ziegler SE and Actinium Pharmaceuticals Inc., “Eckert & Ziegler to Supply Actinium Pharmaceuticals with Ac-225,” HealthCapital, healthcapital.de. Alpha-emitter containment adds extra hot-cell construction and radioprotection layers, driving earlier outsourcing of process development. The shift from PET imaging tracers to therapeutic payloads means CDMOs must re-validate purification, stability, and QC methods under cGMP before scale-up. Limited radiochemistry talent compounds the squeeze, reinforcing premium pricing for integrated offerings.

Regionalization (NA Leadership, APAC Build-Out) Increases Outsourcing

North America commands mature regulatory pathways and proximate isotope suppliers, yet the Asia-Pacific is building cyclotrons that lower delivered isotope cost. GE HealthCare’s 100% acquisition of Nihon Medi-Physics in April 2025 turns Japan into a theranostics hub that can serve the wider region from 13 plants. China’s domestic F-18 and Ga-68 output trims import reliance and attracts cost-sensitive clinical trials. India and Australia stand out as secondary nodes, leveraging pharmaceutical scale-up know-how and access to ANSTO’s reactor-based lutetium-177. Local plants cut transport time for short-lived isotopes and reduce decay-driven yield losses.

Lu-177 and Emerging Ac-225 Supply Investments Unlock New Programs

Isotope security now dictates project timelines. NorthStar and BWXT’s July 2024 pact to process radium-226 underpins future actinium-225 demand for late-stage trials. ITM’s Actineer joint venture with Canadian Nuclear Laboratories will feed Cellectar Biosciences’ CLR 121225 study under a September 2025 supply contract. Cardinal Health says it is first to distribute cGMP-grade actinium-225 at commercial scale, backed by TerraPower reactor output. These multi-year deals allow CDMOs to lock production calendars without fear of isotope shortages that can derail pivotal studies.

Specialist CDMOs Expand Capacity and Sites

SpectronRx opened a 170,000-sq-ft actinium-225 labeling plant in Belgium in Q1 2025 after securing EMA GMP certification. PharmaLogic’s network exceeds 45 sites across four countries, giving it unique reach to supply a commercial therapeutic to over 30 nations. ABX operates six dedicated development hot cells and the largest array of synthesizers for parallel optimization across F-18, Ga-68, Lu-177, and I-123. Charles River couples an in-house cyclotron with small-animal imaging to streamline IND-enabling work. Investments span automated modules, QC suites, and waste treatment, raising entry barriers for newcomers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity and price volatility of key isotopes (Lu-177, Ac-225, Ga-68) | -1.4% | Global, with acute constraints in APAC and emerging markets | Short term (≤ 2 years) |

| Dual GMP and nuclear transport/licensing burden slows tech transfer | -1.1% | Global, with regulatory complexity highest in North America and Europe | Medium term (2-4 years) |

| Talent gaps in radiochemistry, health physics, QA/QP | -0.9% | Global, most acute in North America and Europe, where therapeutic programs concentrate | Long term (≥ 4 years) |

| Radioactive waste handling and site licensing bottlenecks | -0.8% | Global, with infrastructure constraints most severe in APAC and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity and Price Volatility of Key Isotopes (Lu-177, Ac-225, Ga-68)

Clinical-grade actinium-225 still depends on limited thorium-229 generators. Actinium Pharmaceuticals claims its cyclotron method will deliver 10-20 times cheaper isotope at 99.8% purity, yet commercial scale is pending. Reactor outages spike lutetium-177 prices, while Ga-68 generator bottlenecks restrict PSMA PET imaging. APAC shortages are sharper because cyclotron density trails Western levels. CDMOs respond with multi-year offtake contracts that secure volumes but hamper flexibility for ad-hoc studies.

Dual GMP and Nuclear Transport/Licensing Burden Slows Tech Transfer

CDMOs must satisfy FDA or EMA GMP audits and separate nuclear rules from NRC or IAEA affiliates, often adding 12-18 months to facility build-out. SpectronRx’s Belgium site required iterative licensing rounds before actinium-225 production began. Cross-border shipments need IAEA-compliant packaging, carrier certification, and customs clearances. Delays can consume half-life windows, rendering shipments unusable and forcing repeat production. Smaller sponsors lacking regulatory staff struggle, pushing them toward turnkey CDMOs that can navigate dual compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Early Chemistry Outsourcing Drives Premium Margins

Process Development & Radiolabeling/Conjugation services are rising at a 10.40% CAGR to 2031 as sponsors front-load chemistry risk mitigation. ABX’s six development hot cells highlight the depth of capability needed to perfect labeling and purification across isotopes [2]ABX, “Development of radiochemical labelling process,” abx.de. Meanwhile, GMP Drug Substance & Drug Product Manufacturing still captured 47.24% of 2025 revenue, reflecting mature diagnostic output and commercial lutetium-177 runs. The Radiopharmaceutical CDMO/CMO Services Market size for isotope production continues to expand as companies like Cardinal Health shift from commodity sales to long-term actinium-225 partnerships. Other bundled services, such as regulatory CMC and cold-chain logistics, remain niche but gain value as developers seek one-stop solutions.

Sponsors gravitate to CDMOs that can bridge preclinical and GMP chemistry without re-validation. Perceptive has supported more than 80 IND packages by integrating precursor synthesis, analytical methods, and documentation. High-volume F-18 FDG batches carry lower margins, so CDMOs use these runs to feed cash flow while investing profits in therapeutic infrastructure. Those without development expertise risk relegation to price-driven commodity roles within the Radiopharmaceutical CDMO/CMO Services Market.

By Modality: Therapeutics Outpace Diagnostics in Value Capture

Diagnostic agents retained 58.36% of 2025 revenue, yet therapeutic pipelines are advancing at a 9.76% CAGR to 2031. Therapeutic batches command premium pricing due to isotope scarcity and stringent containment. Eckert & Ziegler’s deal with Actinium Pharmaceuticals underpins pivotal alpha-emitter trials, exemplifying how CDMOs leverage isotope access for differentiation. Diagnostic F-18 FDG margins compress as cyclotron capacity spreads across APAC, eroding Western suppliers’ pricing power.

Therapeutics carry longer timelines but promise blockbuster revenue on approval, attracting big-ticket mergers like GE HealthCare’s full purchase of Nihon Medi-Physics. Modality divergence is driving geographic specialization: North America and Europe focus on alpha- and beta-therapeutic expertise, while APAC scales high-volume diagnostic plants to serve burgeoning PET demand.

By Radioisotope: Lutetium-177 Leads Growth Curve

Lutetium-177 is expanding at 9.95% CAGR, riding the wave of approved radioligand therapies, whereas F-18 still holds the largest slice at 33.27% in 2025. Ga-68’s growth is capped by generator shortages, and technetium-99m faces reactor aging risks. Zirconium-89 and iodine-131 gain traction in immuno-oncology and radioimmunotherapy, though from smaller bases. The Radiopharmaceutical CDMO/CMO Services Market size tied to actinium-225 remains small today but could scale rapidly once commercial alpha-emitters win approvals.

Fragmentation of isotope demand forces CDMOs to maintain multi-isotope hot cells with strict segregation to avoid cross-contamination. Large providers like ABX and Charles River can switch isotopes fast, giving them an edge when sponsors adjust dosimetry strategies mid-program.

By Scale of Operation: Preclinical Outsourcing Climbs Fastest

Preclinical work is growing at a 9.58% CAGR, fueled by PDX models and scarce-isotope labeling that inform candidate selection. Champions Oncology provides radiopharmaceutical screening on 1000-plus PDX models, shortening translation time. Clinical-stage services still hold 38.87% of revenue, yet tighter reimbursement on mature diagnostics squeezes margins. Sponsors aim to iron out chemistry issues early to avoid costly GMP failures, hence demand for preclinical CDMOs with integrated imaging, toxicology, and radiochemistry. The radiopharmaceutical CDMO industry thus sees a two-tier structure: high-throughput diagnostic screening and bespoke alpha-emitter programs.

Geography Analysis

North America commanded 47.35% of 2025 revenue due to FDA clarity and proximity to isotope suppliers such as NorthStar and Cardinal Health. The Radiopharmaceutical CDMO/CMO Services Market size in Asia-Pacific is catching up, expanding at a 9.60% CAGR through 2031 on the back of China’s cyclotron rollout and Japan’s theranostics pivot after GE HealthCare’s buyout of Nihon Medi-Physics. India leverages low-cost manufacturing and English-language filings, though isotope access remains a hurdle. Australia benefits from ANSTO’s reactor-based lutetium-177 supply, drawing South-East Asian clinical trials that need predictable isotope deliveries.

Europe’s strong nuclear research base, exemplified by SCK CEN in Belgium, supports capacity ramps such as SpectronRx’s actinium-225 plant operationalized in Q1 2025 [3]SCK CEN, “Opening of SpectronRx's European facility draws closer,” sckcen.be Competitive Landscape. EMA harmonization eases pan-EU distribution, yet transport logistics remain complex for high-specific-activity isotopes. Middle East & Africa and South America are small today but may grow as GCC healthcare investments and Brazil’s pharma sector push for local PET and therapy supply to cut import costs.

The Radiopharmaceutical CDMO/CMO Services Market therefore operates on a hub-and-spoke model: process development concentrates in North America and Europe, while GMP manufacturing spreads to regional nodes that minimize decay loss during transport.

Competitive Landscape

The market is moderately fragmented. Cardinal Health, Curium, ITM, and Jubilant Radiopharma leverage isotope ownership and multi-site reach to secure large contracts. Cardinal Health markets the first cGMP actinium-225 supply chain, backed by TerraPower, cementing its leadership. ITM’s partnerships via Actineer give it long-term actinium-225 flow, illustrated by supply to Alpha-9 Oncology in April 2025. SpectronRx and Evergreen Theragnostics use tie-ups with government labs to sidestep cap-ex on reactors or cyclotrons.

Technology investments dictate competitive edges. PharmaLogic distributes a commercial therapeutic to more than 30 nations, using automated modules and a broad geography to outpace rivals. Champions Oncology pairs PDX models with radiolabeling, winning early-stage work that feeds downstream GMP campaigns. CDMOs are lacking in isotope integration or alpha-emitter containment risk margin erosion as prices for routine diagnostic batches fall.

Radiopharmaceutical CDMO/CMO Services Industry Leaders

Cardinal Health

Curium

ITM

Jubilant Radiopharma

SpectronRx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SpectronRx, a global radiopharmaceutical contract development and manufacturing organization (CDMO), contract manufacturing organization (CMO), and isotope producer, secured USD 85 million in financing from OrbiMed. This investment aims to enhance SpectronRx's production and manufacturing capabilities for medical isotopes.

- September 2025: BWXT’s Kinectrics unit expanded isotope output to provide North American Yb-176 supply.

- April 2025: Medi-Radiopharma opened a new FDA- and EMA-approved plant with a capacity of 3.5 million vials per year, emphasizing sustainable design and operational efficiency.

Global Radiopharmaceutical CDMO/CMO Services Market Report Scope

As per the scope of the report, Radiopharmaceutical CDMO services provide specialized end-to-end outsourcing solutions for the development, production, and distribution of radioactive drugs used in nuclear medicine. These organizations manage the entire lifecycle of a drug, from initial process optimization and analytical development to large-scale commercial manufacturing and rigorous regulatory compliance.

The Radiopharmaceutical CDMO/CMO Services Market is segmented by service, modality, scale of operation, radioisotopes, and geography. By service, the market is categorized into isotope production & supply, process development & radiolabeling/conjugation, GMP drug substance & drug product manufacturing, and others (Cold-chain Logistics, Regulatory & CMC Support, etc.). By modality, the market is divided into diagnostic and therapeutic. By scale of operation, it is segmented into preclinical, clinical, and commercial. By radioisotopes, the segmentation includes F-18, Ga-68, Tc-99m, Zr-89, I-131, Lu-177, and Others (Y-90, Cu-64/67, etc.). Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Isotope Production & Supply |

| Process Development & Radiolabeling/Conjugation |

| GMP Drug Substance & Drug Product Manufacturing |

| Others |

| Diagnostic |

| Therapeutic |

| F-18 |

| Ga-68 |

| Tc-99m |

| Zr-89 |

| I-131 |

| Lu-177 |

| Others |

| Preclinical |

| Clinica |

| Commercial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Isotope Production & Supply | |

| Process Development & Radiolabeling/Conjugation | ||

| GMP Drug Substance & Drug Product Manufacturing | ||

| Others | ||

| By Modality | Diagnostic | |

| Therapeutic | ||

| By Radioisotope | F-18 | |

| Ga-68 | ||

| Tc-99m | ||

| Zr-89 | ||

| I-131 | ||

| Lu-177 | ||

| Others | ||

| By Scale of Operation | Preclinical | |

| Clinica | ||

| Commercial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Radiopharmaceutical CDMO/CMO Services Market in 2026?

The Radiopharmaceutical CDMO/CMO Services Market is expected to reach USD 3.75 billion in 2026

What CAGR is forecast for radiopharmaceutical CDMO services to 2031?

The radiopharmaceutical CDMO market is expected to grow at 9.19% CAGR.

Which service segment is growing fastest?

Process Development & Radiolabeling/Conjugation is expected to grow at 10.40% CAGR.

Which region is expected to post the highest growth?

Asia-Pacific is expected to grow with a 9.60% CAGR

Why are actinium-225 supply contracts critical?

They secure scarce isotope volumes needed for pivotal alpha-emitter trials.

Page last updated on: