QPCR Instruments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

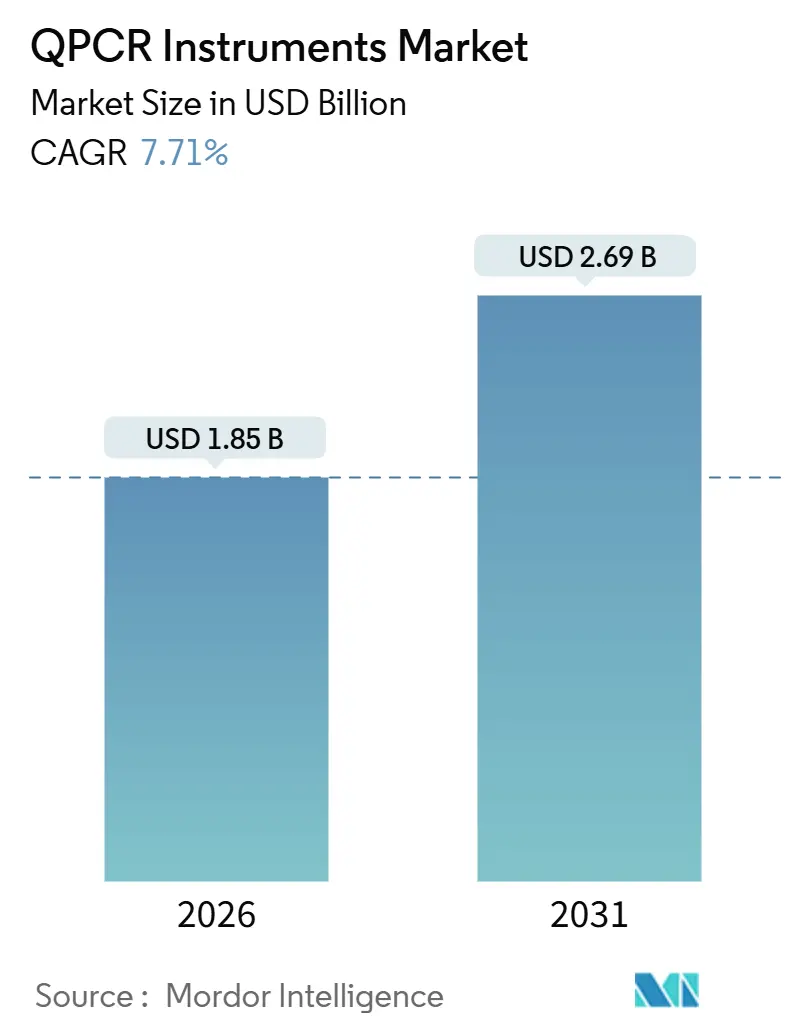

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

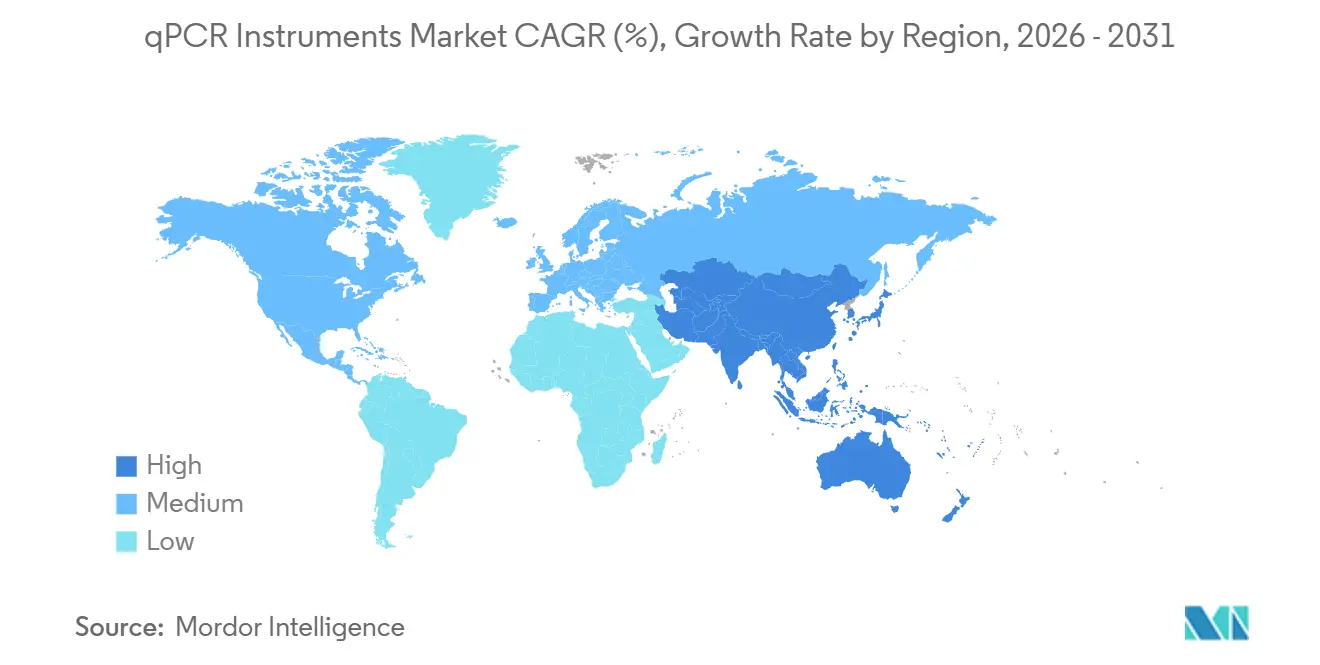

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

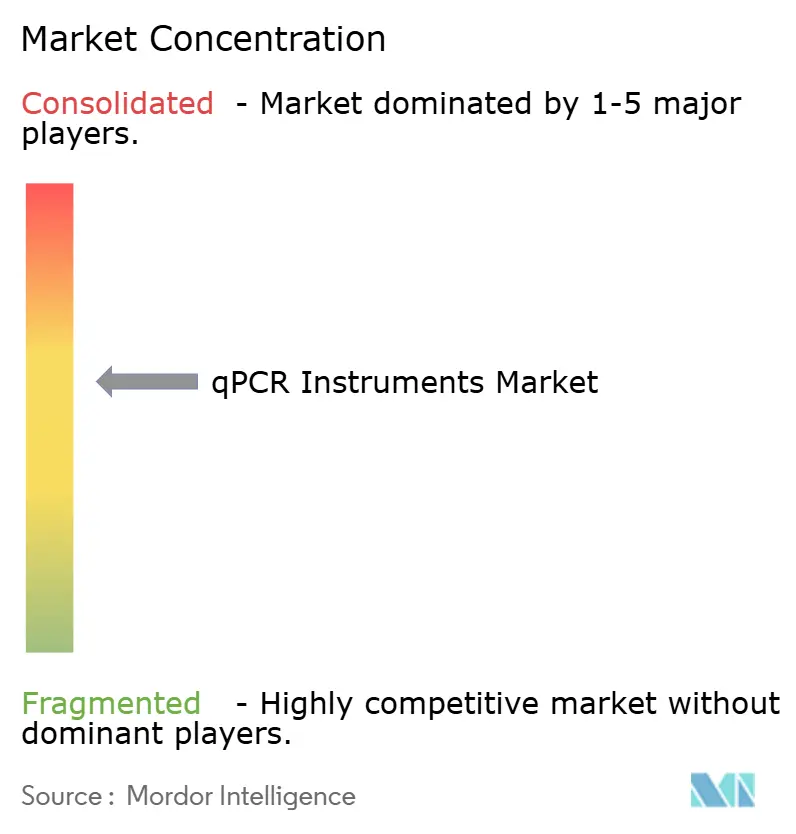

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

QPCR Instruments Market Analysis by Mordor Intelligence

The qPCR instruments market size is estimated at USD 1.85 billion in 2026 and is projected to reach USD 2.69 billion by 2031, advancing at a 7.71% CAGR over the forecast period. Rapid enforcement of the United States FDA Laboratory Developed Test (LDT) Final Rule, the growing need for real-time quality control in cell and gene therapy manufacturing, and the broader push toward decentralized molecular diagnostics are accelerating capital-equipment refresh cycles, thereby underpinning demand growth. Laboratories replacing legacy thermal cyclers now prioritize audit-trail functionality, laser-based multiplex optics, and 21 CFR Part 11-ready software that streamline regulatory submissions. Payers tightening reimbursement for multi-gene sequencing panels are directing clinicians toward targeted qPCR assays when a rapid, single-biomarker answer is clinically sufficient, preserving instrument utilization even in highly sequencer-equipped hospitals. Meanwhile, vector-copy-number testing, residual DNA quantification, and in-process contaminant detection have become mandatory release assays for commercially approved gene therapies, embedding the qPCR instruments market deeper into biopharmaceutical production workflows.

Key Report Takeaways

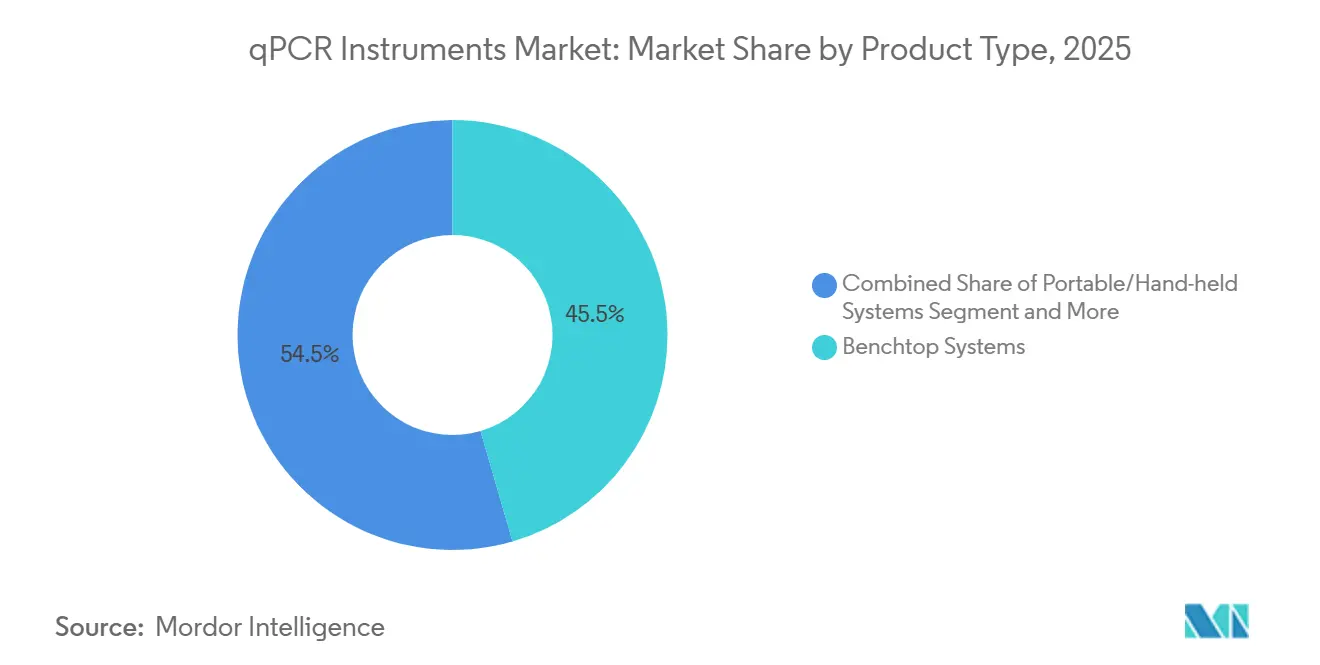

- By Product Type, Benchtop systems led with a 45.55% qPCR instruments market share in 2025, while portable and handheld systems are forecast to post an 11.25% CAGR through 2031, the fastest among product types.

- By Throughput Capacity, Medium-throughput instruments (48–384 wells) accounted for 50.53% of 2025 revenue, yet low-throughput platforms are advancing at a 12.85% CAGR on the back of point-of-care roll-outs.

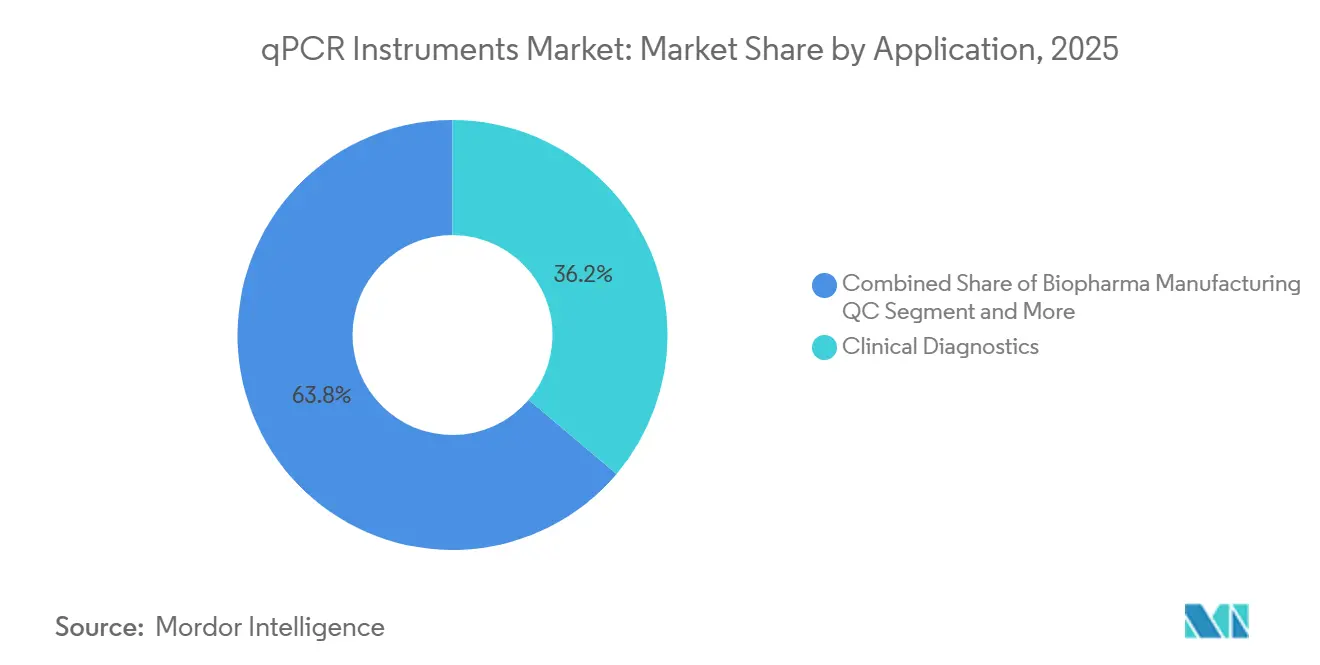

- By Application, Clinical diagnostics represented 36.23% of applications in 2025, whereas biopharma manufacturing quality control is expanding most rapidly at an 11.15% CAGR.

- By End User, Hospitals and reference laboratories held a 40.25% revenue share in 2025, but CROs and CDMOs are projected to grow at a 12.21% CAGR as outsourcing of biomarker testing intensifies.

- By Geography, North America contributed 38.15% to 2025 sales, while Asia-Pacific is expected to clock the highest regional growth at a 10.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global QPCR Instruments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in precision & companion-diagnostic testing | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Surging infectious-disease screening post-COVID-19 | +1.5% | Global, with emphasis on APAC & MEA | Short term (≤ 2 years) |

| Rising NGS-workflow bottlenecks shifting demand back to qPCR | +1.2% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Expanding decentralized/POC molecular-testing roll-outs | +1.4% | APAC core, expanding to MEA & South America | Long term (≥ 4 years) |

| AI-driven assay-design platforms shortening time-to-result | +0.9% | North America & EU, early adoption in China | Medium term (2-4 years) |

| Government bio-surveillance programs | +0.9% | Global, led by North America & EU public-health agencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Precision & Companion-Diagnostic Testing

Drug developers filed 14 new FDA-cleared companion diagnostics relying on qPCR in 2024, a 56% jump from 2023, signaling the platform’s growing indispensability for single-gene oncology markers and cell-therapy release assays. CAR-T sponsors Kite Pharma and Novartis both integrate high-sensitivity qPCR or droplet-digital PCR in manufacturing protocols, elevating baseline demand. Payers reinforce this trajectory by linking oncology drug reimbursement to companion-diagnostic evidence, prompting hospitals to maintain compliant instruments even when NGS systems are on-site. Europe’s In Vitro Diagnostic Regulation (IVDR) phases in stringent traceability requirements through 2027, further favoring qPCR platforms with validated optical calibration and data-integrity logs. Collectively, these forces cement the qPCR instruments market as a regulatory mainstay across precision-medicine pathways.

Surging Infectious-Disease Screening Post-COVID-19

National pandemic investments have been repurposed toward routine pathogen monitoring, preserving elevated instrument utilization. The CDC’s Pathogen Genomics Centers of Excellence now screen outbreaks with rapid qPCR triage before sequencing confirmation, trimming investigation turnaround from 10 days to 48 hours. WHO guidance published in September 2024 recommends member states maintain qPCR capacity equivalent to 1 test per 1,000 population per week for respiratory pathogens. India’s Integrated Disease Surveillance Programme earmarked USD 120 million for portable units in district labs, a procurement that alone boosts the regional installed base by thousands of instruments. Sustained government funding insulates the qPCR instruments market from cyclical private-sector spending.

Rising NGS-Workflow Bottlenecks Shifting Demand Back to qPCR

Median turnaround for hospital-run targeted NGS panels remains 9–10 days, compared with next-day qPCR results, prompting oncologists to order PCR-based EGFR and KRAS tests whenever treatment decisions are time sensitive. Illumina acknowledged in its 2024 10-K that clinical customers use qPCR triage assays to select samples for sequencing, a trend that sustains dual-modality labs. In bioprocessing, qPCR offers same-day viral-vector quantification, whereas sequencing-based QC adds several days of batch hold, reinforcing real-time PCR’s operational value.

Expanding Decentralized/POC Molecular-Testing Roll-Outs

Cepheid’s GeneXpert network surpassed 35,000 placements by end-2024, 40% of which reside in non-hospital sites such as retail pharmacies and work-site clinics. The U.S. Department of Defense deployed ruggedized battery-powered qPCR units at forward operating bases under a USD 25 million award in June 2024, underscoring battlefield demand for rapid pathogen detection. Draft FDA guidance published August 2024 paves the path for CLIA-waived molecular tests, letting non-laboratory personnel run assays and expanding the addressable footprint. These developments funnel incremental revenue into the qPCR instruments market long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex vs. isothermal & CRISPR diagnostics | -0.8% | Global, most acute in price-sensitive APAC & MEA markets | Medium term (2-4 years) |

| Reagent-supply chain volatility & cold-chain cost | -0.6% | Global, with elevated impact in MEA & South America | Short term (≤ 2 years) |

| Skilled-labor shortage for protocol optimisation | -0.5% | North America & EU, emerging in urban APAC | Long term (≥ 4 years) |

| Instrument obsolescence due to rapid optical-module upgrades | -0.4% | North America & EU, limited impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex vs. Isothermal & CRISPR Diagnostics

CRISPR-Cas detection platforms like Sherlock Biosciences’ INSPECTR use readers priced near USD 5,000, far below the USD 30,000–50,000 entry point for basic qPCR units. Mammoth Biosciences’ 2024 pact with GSK to develop CRISPR companion diagnostics signals drug-maker openness to cheaper alternatives. Loop-mediated isothermal amplification (LAMP) assays, operating on simple heat blocks, are winning veterinary and agricultural accounts. While qPCR maintains superior quantitation accuracy, capital-cost gaps could redirect budgets in price-sensitive regions, trimming qPCR instruments market expansion.

Reagent-Supply Chain Volatility & Cold-Chain Cost

Thermo Fisher’s 2024 10-K revealed an 18% jump in enzyme raw-material costs amid fermentation bottlenecks. Separately, IATA logged a 22% rise in cold-chain freight rates in 2024, pressuring labs in sub-Saharan Africa and rural South America that already struggle with unreliable electricity[1]International Air Transport Association, “Cold Chain Logistics Report 2024,” IATA.ORG. Lyophilized master mixes mitigate cold-storage exposure yet sometimes sacrifice sensitivity or require reconstitution, complicating standardization. Supply shocks remain a near-term drag on the qPCR instruments market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Benchtop Versatility Anchors Market, Portables Surge

Benchtop platforms contributed 45.55% to 2025 revenue, a dominant foothold that equates to roughly USD 0.85 billion of the qPCR instruments market size at current exchange rates. Hospitals, contract testing organizations, and academic cores favor these units for interchangeable blocks supporting 96-well and 384-well plates. Portable and handheld systems, while smaller in absolute terms, are posting an 11.25% CAGR that could lift their slice of the qPCR instruments market to nearly one-quarter by 2031. Battery operation, cellular data upload, and ruggedized housings make devices like Cepheid’s GeneXpert Edge viable in clinics lacking stable power, propelling geographic reach beyond traditional labs[2]Cepheid, “GeneXpert Systems Global Deployment,” CEPHEID.COM.

Competitive positioning diverges sharply. Benchtops win on optical precision, service support, and assay breadth, aided by regulatory-cleared reagent menus that simplify validation. Portables compete on ease of use and minimal infrastructure needs, an increasingly important differentiator as pharmacies, disaster-relief teams, and wildlife health programs adopt molecular testing. Vendors mitigate reagent-storage limitations by shipping lyophilized mixes stable at ambient temperature, a step forward that extends usable life in tropical deployments. Ultimately, both formats complement rather than cannibalize each other, expanding the overall qPCR instruments market footprint.

By Throughput Capacity: Mid-Range Dominates, Low-Throughput Gains in POC

Medium-throughput platforms (48–384 wells) secured 50.53% of 2025 sales, translating to roughly USD 0.94 billion of the qPCR instruments market size and reflecting balanced economics for labs running 50–200 specimens daily. Low-throughput devices under 48 wells trail in revenue but outpace growth at a 12.85% CAGR, buoyed by pharmacy-based flu testing, district-level tuberculosis screening, and forward-deployed military biosurveillance. U.S. Department of Defense contracts awarded in 2024, for instance, centered on 16-well rugged units promising 45-minute run times.

High-throughput automation remains niche due to USD 150,000–300,000 capital outlays, yet biobanks and large CROs justify spend by processing thousands of specimens nightly. Bio-Rad’s CFX Opus 384 integrates barcode tracking to trim manual touches 60%. Medium-throughput platforms will likely maintain the largest qPCR instruments market share through 2031, reinforced by 6-color multiplex optics that cut reagent expense per sample.

By Application: Biopharma QC Outpaces Clinical Diagnostics Growth

Clinical diagnostics held 36.23% of demand in 2025, equating to roughly USD 0.67 billion of the qPCR instruments market size. Infectious-disease panels and oncology biomarkers underpin routine utilization, yet reimbursement shifts toward bundled payments temper incremental volume. Biopharma manufacturing quality control, by contrast, is rising at an 11.15% CAGR and could surpass USD 0.45 billion by 2031. FDA gene-therapy CMC guidance compels lot-release qPCR assays for vector titer and residual DNA, turning instruments into non-negotiable production assets.

Academic research and environmental testing deliver steady, if slower, growth. USDA rules introduced in 2024 require qPCR confirmation of Salmonella and E. coli in ground meat, nudging food-safety labs to upgrade to multiplex-capable systems. Overall, differential growth rates across applications diversify the revenue mix and cushion the qPCR instruments market against single-segment shocks.

By End User: CROs & CDMOs Accelerate, Hospitals Hold Steady

Hospitals and reference labs generated 40.25% of 2025 purchases, roughly USD 0.75 billion of qPCR instruments market size. Device-registration rules push smaller hospital labs to outsource LDTs, consolidating testing in high-complexity centers. CROs and CDMOs, meanwhile, are growing 12.21% annually. IQVIA reported 28% molecular-diagnostics service growth in 2024, reflecting oncology-trial demand for rapid biomarker screening. CDMOs producing AAV and lentiviral vectors invest heavily in automated qPCR lines to meet batch-release timelines and regulatory scrutiny.

Government public-health labs, expanded during COVID-19, now repurpose capacity for early-warning surveillance of influenza and antimicrobial resistance. Academic institutes replace instruments on grant-funding cycles rather than on throughput constraints, leading to predictable yet slower refresh rates. The varied end-user mix distributes revenue streams, supporting resilience in the qPCR instruments market.

Geography Analysis

North America, commanding 38.15% of 2025 revenue, benefits from roughly 12,000 high-complexity CLIA labs running molecular assays. FDA enforcement of the LDT Final Rule triggers accelerated retirements of thermal cyclers lacking compliance features, pushing the qPCR instruments market toward audit-capable models. Canada funnels CAD 45 million (USD 33 million) into portable qPCR units for remote northern communities, shortening infectious-disease turnaround in previously underserved areas. Mexico’s epidemiological institute expanded qPCR capacity 40% in 2024 to combat dengue and tuberculosis, yet market penetration remains concentrated in private labs.

Asia-Pacific is poised for a 10.51% CAGR, propelled by China’s fast-track IVD registration pathway that halves approval timelines to nine months[3]China National Medical Products Administration, “Fast-Track IVD Registration Pathway,” NMPA.GOV.CN. India’s USD 120 million portable-system procurement fuels district-level deployments, while Japan lifts cancer-screening budgets 22%, encouraging liquid-biopsy qPCR adoption. Australia and South Korea focus on biosurveillance, with Australia allocating AUD 30 million (USD 20 million) to zoonotic-pathogen sentinel sites. Together, these programs enlarge the regional qPCR instruments market footprint beyond tertiary centers.

Europe holds a mature but compliance-driven landscape, shaped by IVDR enforcement that rewards suppliers offering traceable reagent lots and secure data capture. Germany and the U.K. lead per-capita instrument density, while southern Europe upgrades to harmonize cross-border outbreak detection. Middle East & Africa present fast-growth pockets: Saudi Arabia invested SAR 800 million (USD 213 million) for regional reference labs, and South Africa broadens qPCR for HIV viral-load and TB resistance monitoring. South America’s momentum concentrates in Brazil, which ordered 2,500 portable units for Amazonian states to tackle arboviral outbreaks. Cold-chain logistics and reagent import tariffs constrain further acceleration but are partially alleviated by lyophilized reagents.

Competitive Landscape

The top five suppliers—Thermo Fisher Scientific, Roche Diagnostics, Bio-Rad Laboratories, QIAGEN, and Agilent Technologies—collectively controlled significant percentage of global shipments in 2025, positioning the qPCR instruments market as moderately concentrated. Each leverages proprietary chemistries and closed software to lock in consumables revenue. Thermo Fisher’s TaqMan assays and Roche’s LightCycler probes generate recurring reagent margins that eclipse hardware sales. Bio-Rad’s laser-based multiplexing upgrade path incentivizes trade-ins, while Agilent’s 2024 acquisition of Biovectra shored up enzymatic supplies, mitigating upstream risk.

Smaller competitors exploit white-space niches. Analytik Jena earned ISO 13485 for its open-architecture qTOWER³ G, appealing to biobanks that demand interoperability with third-party LIMS. Standard BioTools (Fluidigm) launched Biomark HD Flex targeting high-multiplex gene-expression screens, differentiating via microfluidic nanoplates that lower reagent use. AI-infused design platforms serve as intangible moats; QIAGEN’s machine-learning toolkit compresses assay-development timelines, strengthening its offering beyond hardware.

Patent activity remains brisk, with 47 U.S. grants in 2024 covering optical detectors, lyophilized mixes, and multiplex algorithms. ISO 13485 quality management certification is now table stakes for entry into Europe and North America, raising compliance costs for emerging manufacturers. Service contracts, cloud-based data analytics, and predictive-maintenance subscriptions are emerging as decisive battlegrounds shaping revenue longevity in the qPCR instruments market.

QPCR Instruments Industry Leaders

Agilent Technologies

Bio-Rad Laboratories

Roche Diagnostics

Qiagen

Thermo Fisher Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Alamar Biosciences launched the RUO NULISAqpcr AD 5-plex assay enabling simultaneous quantitation of five Alzheimer’s-related blood biomarkers from a single sample.

- April 2025: Biocartis introduced a real-time qPCR assay detecting POLE and POLD1 mutations in endometrial cancer.

Global QPCR Instruments Market Report Scope

As per the scope of the report, qPCR instruments are specialized laboratory devices used to perform quantitative polymerase chain reaction (qPCR), a technique that amplifies and simultaneously quantifies targeted DNA molecules.

The qPCR instruments market is segmented by product type into benchtop systems, portable/hand-held systems, and high-throughput automated platforms. By throughput capacity, the market is categorized into low-throughput (<48 wells), medium-throughput (48–384 wells), and high-throughput (>384 wells). By application, the market is divided into clinical diagnostics, research and academic, biopharma manufacturing QC, and other applications. By end user, the market includes hospitals and reference labs, academic and research institutes, pharma and biotech companies, CROs and CDMOs, and government and public health labs. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Benchtop Systems |

| Portable/Hand-held Systems |

| High-Throughput Automated Platforms |

| Low-Throughput (<48 wells) |

| Medium-Throughput (48-384 wells) |

| High-Throughput (>384 wells) |

| Clinical Diagnostics |

| Research & Academic |

| Biopharma Manufacturing QC |

| Other Applications |

| Hospitals & Reference Labs |

| Academic & Research Institutes |

| Pharma & Biotech Companies |

| CROs & CDMOs |

| Government & Public Health Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Benchtop Systems | |

| Portable/Hand-held Systems | ||

| High-Throughput Automated Platforms | ||

| By Throughput Capacity | Low-Throughput (<48 wells) | |

| Medium-Throughput (48-384 wells) | ||

| High-Throughput (>384 wells) | ||

| By Application | Clinical Diagnostics | |

| Research & Academic | ||

| Biopharma Manufacturing QC | ||

| Other Applications | ||

| By End User | Hospitals & Reference Labs | |

| Academic & Research Institutes | ||

| Pharma & Biotech Companies | ||

| CROs & CDMOs | ||

| Government & Public Health Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the qPCR instruments market?

The qPCR instruments market size stands at USD 1.85 billion in 2026 and is forecast to reach USD 2.69 billion by 2031.

Which product type leads global revenues?

Benchtop systems held a 45.55% share of 2025 revenue, maintaining leadership due to versatility across clinical, research, and biopharma settings.

Which application segment is growing fastest?

Biopharma manufacturing quality control is projected to grow at an 11.15% CAGR through 2031, driven by stringent release testing for cell and gene therapies.

How will Asia-Pacific contribute to future demand?

Asia-Pacific is expected to post a 10.51% CAGR, supported by China's streamlined IVD approvals and Indias investment in district-level portable units.

What competitive strategies sustain vendor margins?

Leading companies bundle proprietary reagents, 21 CFR Part 11-ready software, and predictive-maintenance contracts to lock in recurring revenue even as hardware prices face pressure.

How does CRISPR technology affect qPCR adoption?

CRISPR-based diagnostics offer lower instrument costs, posing a medium-term capex threat, but qPCR retains superior quantitation accuracy and regulatory acceptance in high-stakes testing.

Page last updated on: