Pulsed Field Ablation Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 6.44 Billion |

| Growth Rate (2026 - 2031) | 26.12% CAGR |

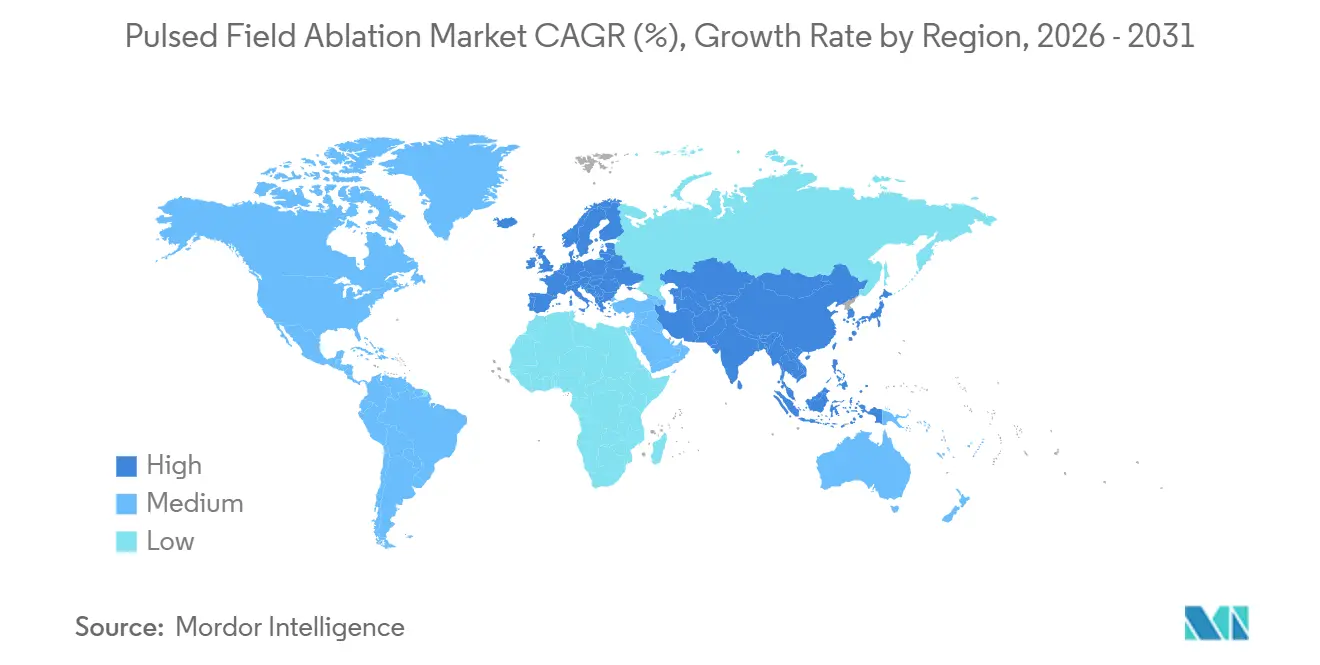

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pulsed Field Ablation Market Analysis by Mordor Intelligence

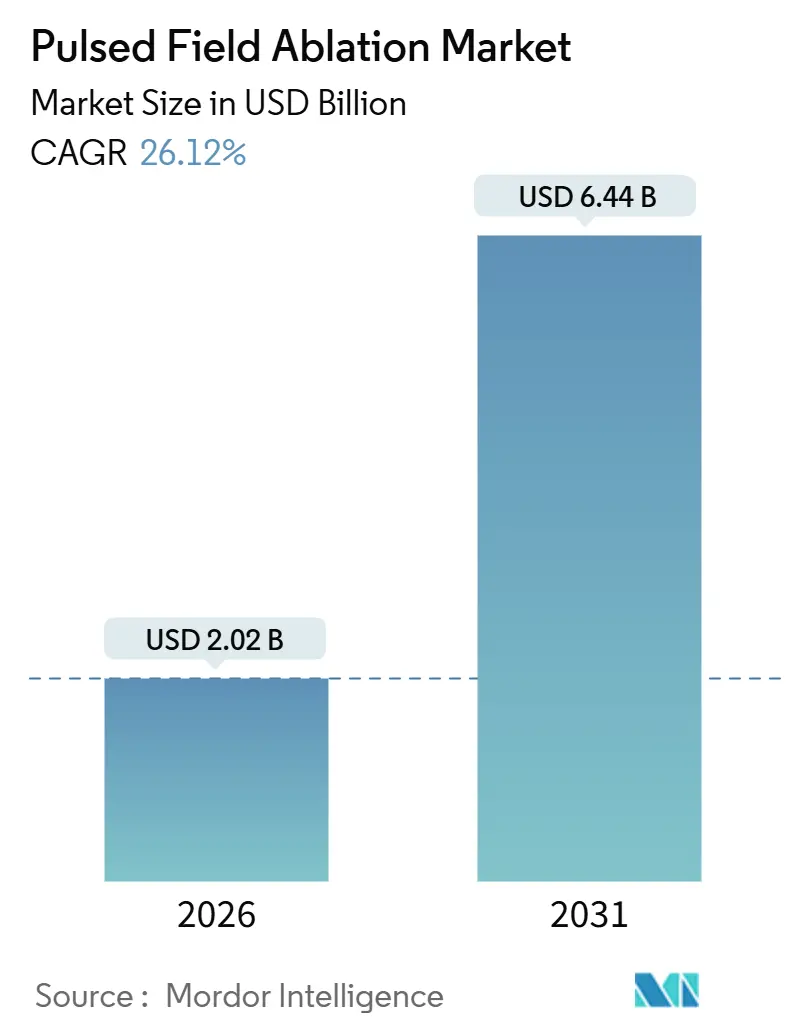

The Pulsed Field Ablation Market size is estimated at USD 2.02 billion in 2026, and is expected to reach USD 6.44 billion by 2031, at a CAGR of 26.12% during the forecast period (2026-2031).

The growth trajectory reflects a wholesale shift in electrophysiology lab economics: tissue-selective electroporation removes the esophageal-injury risk that limits radiofrequency (RF) and cryoablation, while trimming procedure times by 30–40 minutes and cutting readmission costs. Rapid regulatory clearances across the United States, Europe, and Japan during 2024–2025 unlocked an installed-base expansion worth USD 890 million, allowing more than 1,200 electrophysiology labs to replace aging RF systems with pulsed field generators. Hospitals welcome the model because fewer complications translate into shorter observation periods, same-day discharges, and materially lower per-case costs. Vendors, in turn, are leaning into a razor-and-blade strategy: every generator placement secures 80–120 catheter procedures a year, guaranteeing five to seven years of high-margin consumable revenue.

Key Report Takeaways

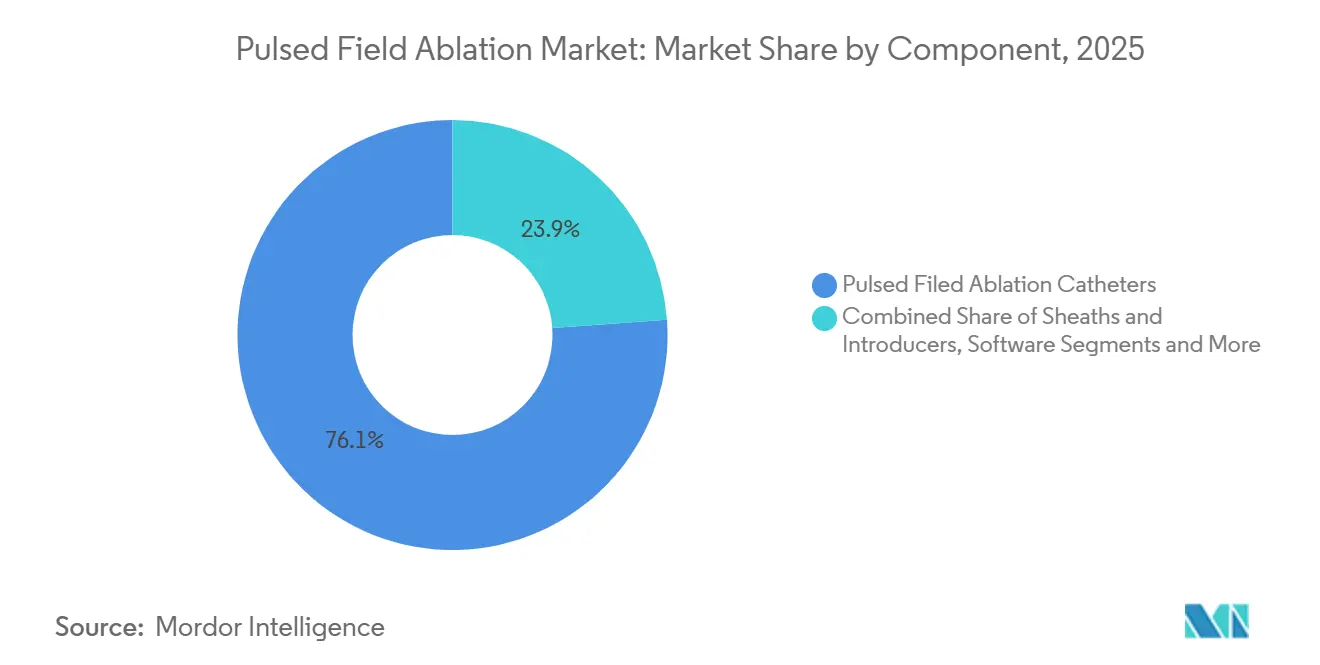

- By component, catheters commanded 76.13% of 2025 revenue, whereas generators and consoles will expand the fastest at a 29.73% CAGR through 2031.

- By delivery form factor, balloon and single-shot circular systems led with 58.21% share in 2025, while lattice and hybrid designs are projected to rise at a 28.56% CAGR.

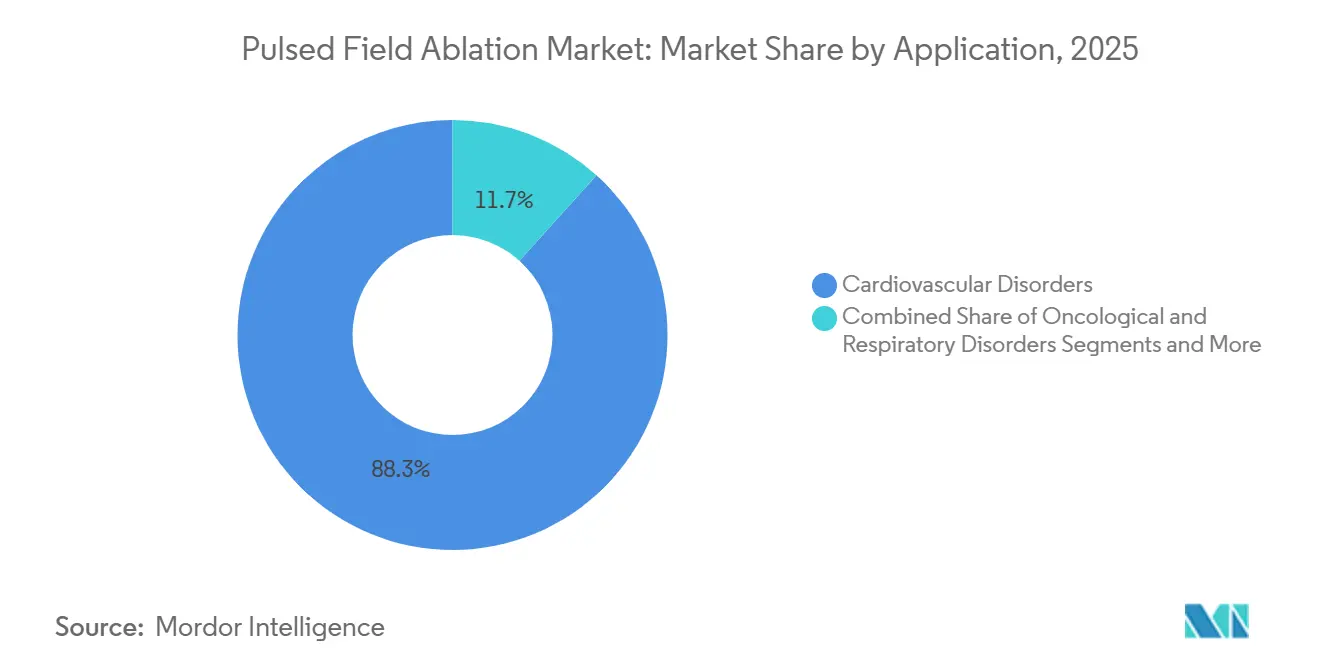

- By application, cardiovascular procedures accounted for 88.32% of 2025 revenue; oncological uses are poised to surge at a 29.43% CAGR.

- By end user, hospitals captured 78.17% of 2025 procedures, yet ambulatory surgery centers (ASCs) show the quickest climb at a 28.74% CAGR.

- By geography, North America held 44.11% market share in 2025; Asia-Pacific is forecast to accelerate at a 29.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pulsed Field Ablation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-FDA/CE commercialization expands eligible population and installed base | +5.2% | Global, early focus on North America and Western Europe | Short term (≤ 2 years) |

| Clinically favorable safety profile versus thermal ablation | +4.8% | Global | Medium term (2–4 years) |

| Procedural efficiency shortens lab time and boosts throughput | +3.9% | Global, especially high-volume centers in North America and Asia-Pacific | Short term (≤ 2 years) |

| Integration with leading mapping ecosystems and dual-energy platforms | +3.6% | North America and Europe, spillover to Asia-Pacific | Medium term (2–4 years) |

| Coronary-spasm mitigation protocols enable safer linear and non-PV ablation | +2.7% | Global, early adoption in academic centers | Long term (≥ 4 years) |

| Expansion into ventricular tachycardia (VT) and surgical-hybrid workflows | +3.1% | North America and Europe first, Asia-Pacific next | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-FDA/CE Commercialization Expands Installed Base

Clearances issued between January 2024 and December 2025 transformed pulsed field ablation from an investigational option to a reimbursed standard-of-care in more than 1,800 labs worldwide. Hospitals invested USD 1.1 billion in capital equipment during that window, exchanging aging RF generators for pulsed-field consoles and broadening treatment eligibility beyond paroxysmal atrial fibrillation to persistent atrial flutter. Medicare’s Q2 2024 decision to pay roughly USD 28,000 per case wiped out the last reimbursement hurdle, while Germany, France, and Japan followed with positive coverage at lower, but still attractive, price points.[1]Centers for Medicare & Medicaid Services, “Centers for Medicare & Medicaid Physician Fee Schedule 2024,” Centers for Medicare & Medicaid Services, cms.gov The installed-base dynamic is powerful: every generator drives consumable pull-through that compounds revenue for five to seven years.

Clinically Favorable Safety Profile Versus Thermal Ablation

Electric fields selectively permeabilize cardiomyocytes yet spare adjacent vasculature, nerves, and the esophagus. Zero esophageal fistulas and zero phrenic nerve palsies were reported across 614 Farapulse patients in the pivotal ADVENT trial, contrasting sharply with historical thermal-ablation complication rates.[2]Vivek Reddy, “Safety and Efficacy Results from the ADVENT Trial,” Journal of the American College of Cardiology, jacc.org Abbott’s VOLT-AF study echoed these outcomes, logging a 1.2% major-adverse-event rate against 2.8% in RF controls.[3]Abbott Laboratories, “VOLT-AF Study Demonstrates Superior Safety Profile for Pulsed Field Ablation,” Abbott Laboratories, abbott.com This margin of safety enables operators to forgo temperature probes, saving 12–15 minutes and reducing procedure anxiety. PFA is also safe in patients with pacemakers or implantable cardioverter-defibrillators, a cohort often excluded from MRI-guided thermal ablations.

Procedural Efficiency Shortens Lab Time and Boosts Throughput

Single-shot balloon PFA cuts pulmonary-vein-isolation times from 90–120 minutes to 45–60 minutes. Medtronic’s PulseSelect system achieves complete isolation with six two-second applications, while Boston Scientific’s Farapulse posted median procedure times of 52 minutes in ADVENT. A 600-bed academic center can therefore grow annual ablation volume by 130–150 cases without extending lab hours, translating into USD 3.6–4.2 million in incremental revenue. The productivity boost is greatest in regions that face electrophysiologist shortages, such as Japan and the U.S. Midwest.

Integration with Mapping Ecosystems and Dual-Energy Platforms

Abbott designed Volt to work natively with EnSite X and EnSite Omnipolar, while Medtronic’s PulseSelect is locked to CARTO 3 Version 7—a tie-in that imposes USD 400,000–500,000 in switching costs on any facility that hopes to change vendors. Boston Scientific chose an open approach, enabling Farapulse to connect with both CARTO and EnSite, which proved attractive in mixed-vendor labs. Johnson & Johnson raised the bar in November 2025 by launching Varipulse-RF, a hybrid catheter that provides PFA and RF in a single pass, eliminating the need to swap tools during persistent-AF cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Durability evidence gaps for persistent AF and complex lesions | -2.4% | Global | Medium term (2–4 years) |

| Capital intensity and ecosystem lock-in slow purchasing cycles | -1.8% | Global, pronounced in cost-sensitive markets | Short term (≤ 2 years) |

| Coronary spasm and hemolysis risks require training and protocols | -1.5% | Global, high impact in community hospitals | Short term (≤ 2 years) |

| Price pressure compresses average selling prices (ASPs) and margins | -1.2% | Europe, Asia-Pacific, value-based U.S. systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Durability Evidence Gaps

Twelve-month reconnection rates in ADVENT and PULSED-AF trials reached 14.2% and 11.8%, exceeding the 5–7% benchmark for point-by-point RF. Histology indicates that electroporation may fail to create deep, transmural lesions in atrial walls thicker than 3.5 mm, a limitation that matters most in persistent AF. Until 24-month data from the MANIFEST-17K study arrive in 2026, guideline committees keep PFA as a Class IIa recommendation for complex cases, tempering widespread adoption.

Capital Intensity and Ecosystem Lock-In

A full PFA suite costs USD 320,000–420,000 versus USD 180,000–240,000 for RF. More than 60% of U.S. labs record fewer than 75 ablations a year, making a positive return on investment difficult. Proprietary integration compounds the burden: a CARTO-based lab that adds Farapulse faces an extra USD 150,000 in interface fees and 40–60 hours of retraining. Leasing and pay-per-procedure models are emerging but shave vendor gross margins by up to 600 basis points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Generators Prime Long-Term Revenue Despite Catheter Dominance

Catheters generated 76.13% of 2025 revenue, confirming the consumable-driven nature of electrophysiology. Yet the pulsed field ablation market size tied to generators is slated to rise at a 29.73% CAGR, reflecting an arms-race to lock hospitals into proprietary ecosystems through 2031. Generators carry lower gross margins—about 45%—but every placement anchors recurring catheter demand, producing the lion’s share of profit over a seven-year cycle. Catheter revenue remains the cash engine, with single-use ASPs of USD 3,200–4,800 and gross margins above 70%. Sheaths, introducers, accessories, and fledgling software subscriptions round out the component mix, offering cross-sell opportunities and incremental annuity streams.

Generous trade-in programs—Abbott’s USD 40,000–50,000 credit for legacy RF consoles, for example—are front-loading generator adoption and temporarily dampening profit. Vendors plan to recoup the margin through software analytics and outcome-based service contracts. If 30% of installed generators adopt subscription lesion-analytics packages by 2029, software could contribute USD 150 million in high-margin revenue to the pulsed field ablation industry.

By Delivery Form Factor: Balloon Systems Maintain Lead While Lattice Designs Gain Ground

Balloon and single-shot circular devices held 58.21% share in 2025. Their procedural simplicity shortens learning curves and allows community labs to complete pulmonary-vein isolation in under an hour. Lattice and hybrid catheters are the fastest-growing group, climbing at a 28.56% CAGR as operators tackle thicker ventricular and atrial substrate in persistent AF and VT. Johnson & Johnson’s Varipulse-RF hybrid, cleared in late 2025, merges the speed of PFA for pulmonary vein isolation with the durability of RF for substrate modification, eliminating catheter exchanges and shaving 20 minutes off persistent-AF procedure time.

Focal and multielectrode catheters, currently at about 30% share, serve redo and anatomically complex cases. Should durability concerns prompt guideline downgrades, hybrid systems may cannibalize balloon share by 2028. Vendors therefore hedge by keeping broad portfolios that span balloon, lattice, and dual-energy solutions.

By Application: Cardiovascular Dominates but Oncology Offers Highest Growth

Cardiovascular applications represented 88.32% of 2025 revenue, making them the cornerstone of the pulsed field ablation market. Pulmonary-vein isolation for atrial fibrillation claims more than 90% of cardiac procedures, owing to an aging population and rising AF prevalence. Ventricular tachycardia, though lower in volume, drives higher per-case revenue, bolstering average selling prices. Oncological applications logged sub-3% share in 2025 yet will advance at a 29.43% CAGR, propelled by Pulse Biosciences and Field Medical trials in pancreatic and hepatic tumors.

Dermatological and respiratory uses remain niche because existing low-cost options—cryotherapy and RF trans-septal incision—are entrenched. If Pulse Biosciences proves survival benefits in pancreatic cancer, oncology could claim 6–7% of pulsed field ablation market share by 2031. That upside is attractive but requires distinct regulatory and reimbursement playbooks, fragmenting the competitive landscape.

By End User: Hospitals Anchor Volume as ASCs Cement Growth

Hospitals performed 78.17% of pulsed-field procedures in 2025 owing to capital-equipment requirements and payer mandates for overnight observation. Academic medical centers execute two-thirds of those cases, leveraging fellowship programs and surgical backup. The pulsed field ablation market size attributable to ASCs will expand rapidly, however, thanks to Medicare’s decision to reimburse outpatient ablations at 95% of hospital rates. Facility fees in ASCs are USD 10,000 lower per case, a boon for value-based payer models.

ASC migration accelerates in states such as Florida and Texas, where wait lists are long and EP capacity is constrained. Vendors now offer ASC-specific training, conscious-sedation protocols, and compact generator footprints. The end-user split is expected to level at roughly 60% hospital and 40% ASC by 2031, mirroring outpatient trends in orthopedic and ophthalmic surgery.

Geography Analysis

North America owned 44.11% of 2025 revenue, driven by Medicare’s USD 28,000 reimbursement per procedure, more than 340 cleared labs, and catheter ASPs that sit 25–40% above European and Asian price points. Penetration in major metropolitan areas now exceeds one-quarter of eligible AF patients, so vendors pivot to tier-2 cities and ASCs for growth. The installed-base effect is potent: each of the 1,200-plus generators placed across the region during 2024–2025 will create USD 320,000–480,000 in annual catheter pull-through through 2030.

Asia-Pacific will post the fastest expansion at 29.01% CAGR through 2031. Japan’s May 2024 approval of PulseSelect and China’s CNY 420 million tender awards to Boston Scientific and Hangzhou Deno EP opened high-volume channels, though ASPs remain 35–40% below U.S. levels. Domestic Chinese vendors, such as APT Medical and MicroPort EP, offer catheters at a 40% discount, enabling penetration into tier-2 and tier-3 hospitals. India, South Korea, and Australia contribute about one-fifth of APAC volume, but India’s out-of-pocket payment model tempers adoption.

In Europe, Germany’s positive reimbursement decision landed in September 2024, but hospital-level negotiations shaved 15–20% off list prices. France limited reimbursement to high-volume labs, while the United Kingdom capped catheter prices at GBP 2,800 under a framework agreement that exchanged discounts for guaranteed volumes. Volume growth in Southern and Eastern Europe lags because of lower EP-lab density and tighter capital budgets. Elsewhere, the Middle East, Africa, and South America each account for less sahre of global revenue, limited by physician shortages and import tariffs.

Competitive Landscape

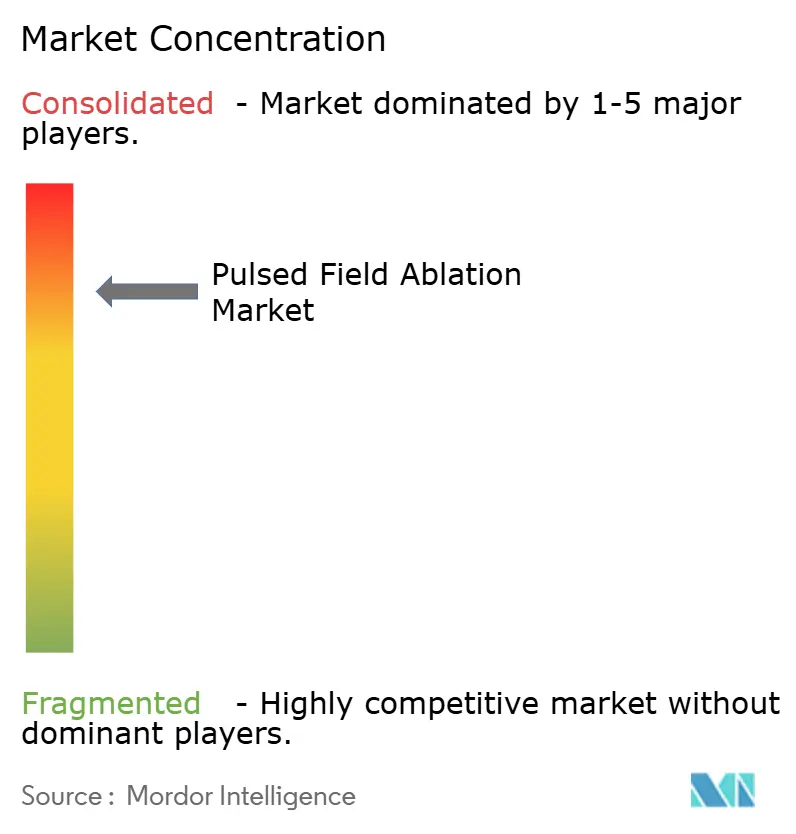

The top four companies include Boston Scientific, Medtronic, Johnson & Johnson, and Abbott, giving the pulsed field ablation market a moderately concentrated structure. Boston Scientific capitalized on its open-platform strategy, while Medtronic and Abbott doubled down on proprietary tie-ins to CARTO and EnSite. Johnson & Johnson entered late but differentiated with a dual-energy hybrid catheter. Regulatory filings reveal heavy investment: Boston Scientific submitted 14 patents in 2024–2025 around pulse-wave optimization, while Medtronic focused on AI-assisted lesion tagging.

Challengers pursue white-space niches. Galvanize Therapeutics aims at VT ablation with a lattice-tip catheter, and AtriCure targets redo procedures through its surgical hybrid system. Chinese firms APT Medical and Hangzhou Deno EP play the price card in domestic tenders, securing hospital share in cost-sensitive segments. The next inflection point hinges on durability data: if 24-month reconnection rates remain below 15%, current leaders will consolidate; if they exceed 20%, payers may curtail indications, opening the door for lower-priced entrants.

Pulsed Field Ablation Industry Leaders

Abbott Laboratories

Johnson & Johnson

Medtronic plc

MicroPort Scientific Corporation

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Abbott received FDA clearance for Volt and bundled EnSite X upgrades with USD 40,000–50,000 trade-in credits for legacy RF generators.

- November 2025: MicroPort EP won Chinese NMPA approval for PulseMagic TrueForce, a pressure-sensing PFA catheter that rounds out its multimodality platform.

- July 2025: Boston Scientific gained expanded U.S. labeling for Farapulse to include drug-refractory persistent atrial fibrillation.

Global Pulsed Field Ablation Market Report Scope

Pulsed Field Ablation (PFA) is a non-thermal, tissue-selective ablation technology that treats cardiac arrhythmias, such as atrial fibrillation, by using high-voltage electrical pulses to target cardiac cells while sparing surrounding tissues.

The Pulsed Field Ablation Market Report is segmented by Component, Delivery Form Factor, Application, End User, and Geography. By Component, the market is segmented into Generators & Consoles, Catheters, Sheaths & Introducers, Accessories, Software, and Services. By Delivery Form Factor, the market is segmented into Balloon/Single-shot, Focal/Multielectrode, and Lattice/Hybrid. By Application, the market is segmented into Cardiovascular, Oncological, Respiratory, and Dermatological. By End User, the market is segmented into Academic Hospitals, Community Hospitals, and ASCs. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Generators & Consoles |

| Pulsed Field Ablation Catheters |

| Sheaths & Introducers |

| Accessories & Disposables |

| Software |

| Services |

| Balloon / Single‑shot Circular Systems |

| Focal / Multielectrode Catheters |

| Lattice / Hybrid & Other Designs |

| Cardiovascular Disorders |

| Oncological Disorders |

| Respiratory Disorders |

| Dermatological Disorders |

| Academic/Teaching Hospitals (EP Labs) |

| Community Hospitals |

| Ambulatory Surgery Centers (ASCs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Generators & Consoles | |

| Pulsed Field Ablation Catheters | ||

| Sheaths & Introducers | ||

| Accessories & Disposables | ||

| Software | ||

| Services | ||

| By Delivery Form Factor | Balloon / Single‑shot Circular Systems | |

| Focal / Multielectrode Catheters | ||

| Lattice / Hybrid & Other Designs | ||

| By Application | Cardiovascular Disorders | |

| Oncological Disorders | ||

| Respiratory Disorders | ||

| Dermatological Disorders | ||

| By End User | Academic/Teaching Hospitals (EP Labs) | |

| Community Hospitals | ||

| Ambulatory Surgery Centers (ASCs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the pulsed field ablation market in 2026 and how fast is it growing?

The market stands at USD 2.02 billion in 2026 and is expanding at a 26.12% CAGR toward USD 6.44 billion by 2031.

Which delivery form factor currently dominates sales?

Balloon and single-shot circular catheters lead with 58.21% of 2025 revenue, thanks to their procedural speed and ease of use.

What is the biggest restraint on long-term adoption?

Unresolved durability data in persistent AF keeps PFA at a Class IIa guideline rating, limiting uptake in risk-averse centers.

Why are ambulatory surgery centers gaining share?

Medicare now reimburses ASC ablations at 95% of hospital rates, and facility fees are USD 10,000 lower, making outpatient settings cost-attractive.

Which region is forecast to grow the fastest?

Asia-Pacific, propelled by China’s bulk-purchase tenders and Japan’s universal coverage, is projected to rise at a 29.01% CAGR through 2031.

Page last updated on: