Pulmonary Function Testing Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

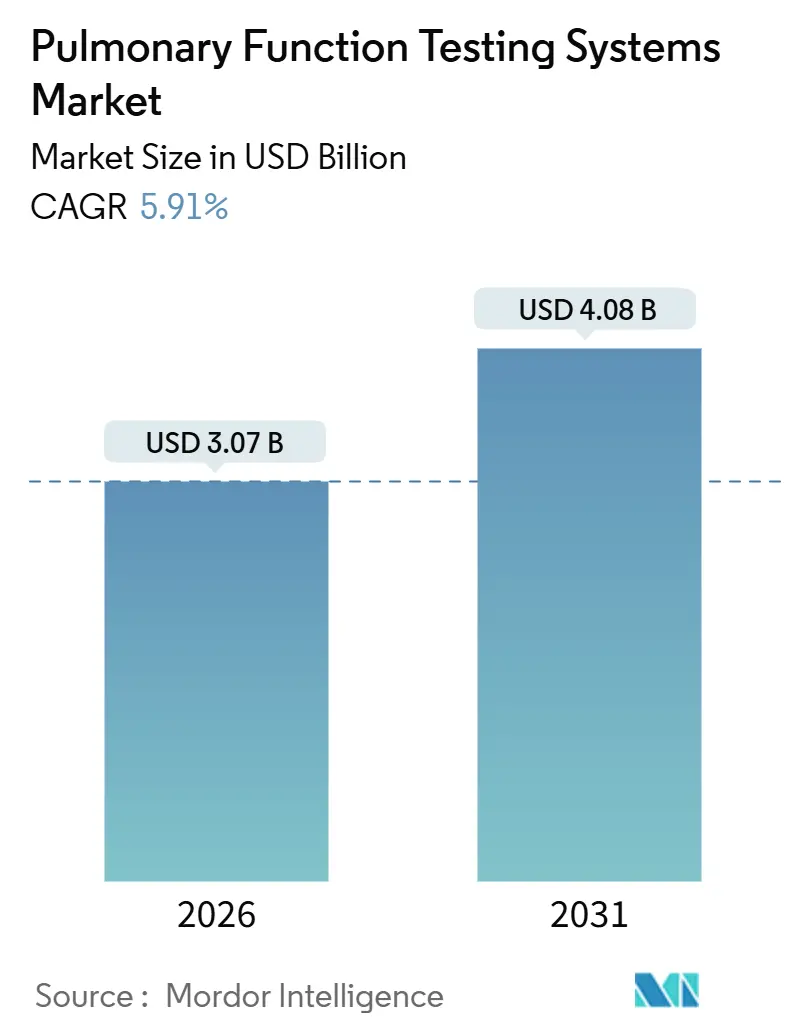

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 4.08 Billion |

| Growth Rate (2026 - 2031) | 5.91% CAGR |

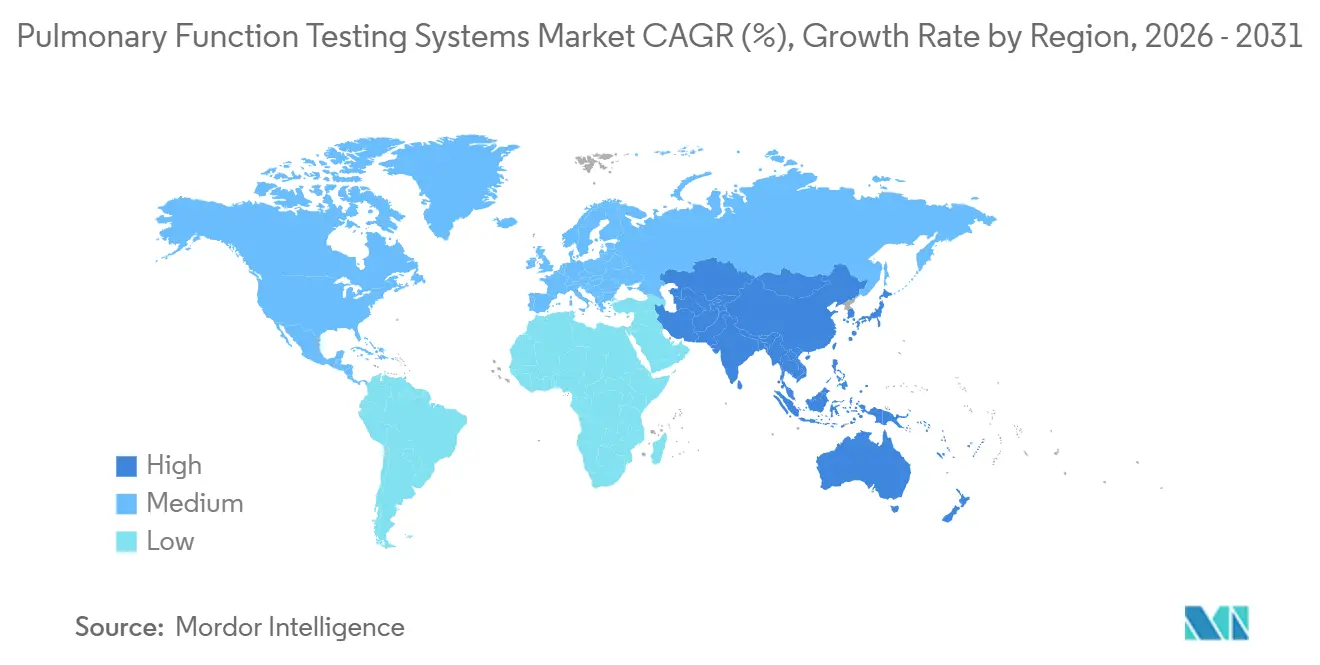

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pulmonary Function Testing Systems Market Analysis by Mordor Intelligence

The Pulmonary Function Testing Systems Market size is estimated at USD 3.07 billion in 2026, and is expected to reach USD 4.08 billion by 2031, at a CAGR of 5.91% during the forecast period (2026-2031).

Uptake is anchored in the rising global burden of chronic respiratory diseases, regulatory pressure for objective lung-function monitoring, and the rapid shift toward home-based diagnostics enabled by portable spirometers. Hospitals remain the primary testing hubs, yet payer reimbursement for remote patient monitoring is redistributing volumes to residences and community clinics. Incumbent manufacturers defend their market share through multi-parameter laboratory systems, while digital health entrants focus on lightweight devices and cloud analytics. Workforce shortages among respiratory therapists create a critical adoption bottleneck that has begun to shape procurement decisions.

Key Report Takeaways

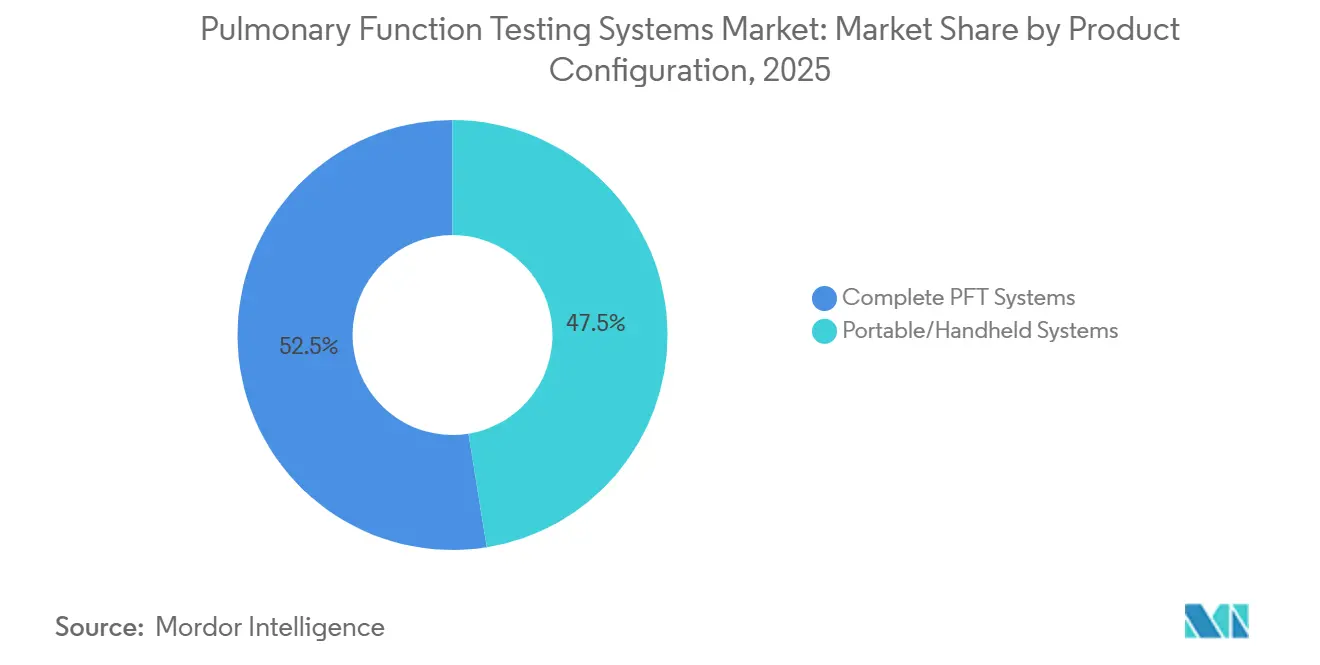

- By product configuration, complete PFT systems held 52.54% of the pulmonary function testing systems market share in 2025, whereas portable and handheld systems are forecast to expand at a 7.54% CAGR through 2031.

- By test type, spirometry accounted for 45.43% of the pulmonary function testing systems market in 2025, while impulse oscillometry is poised for a 7.66% CAGR through 2031.

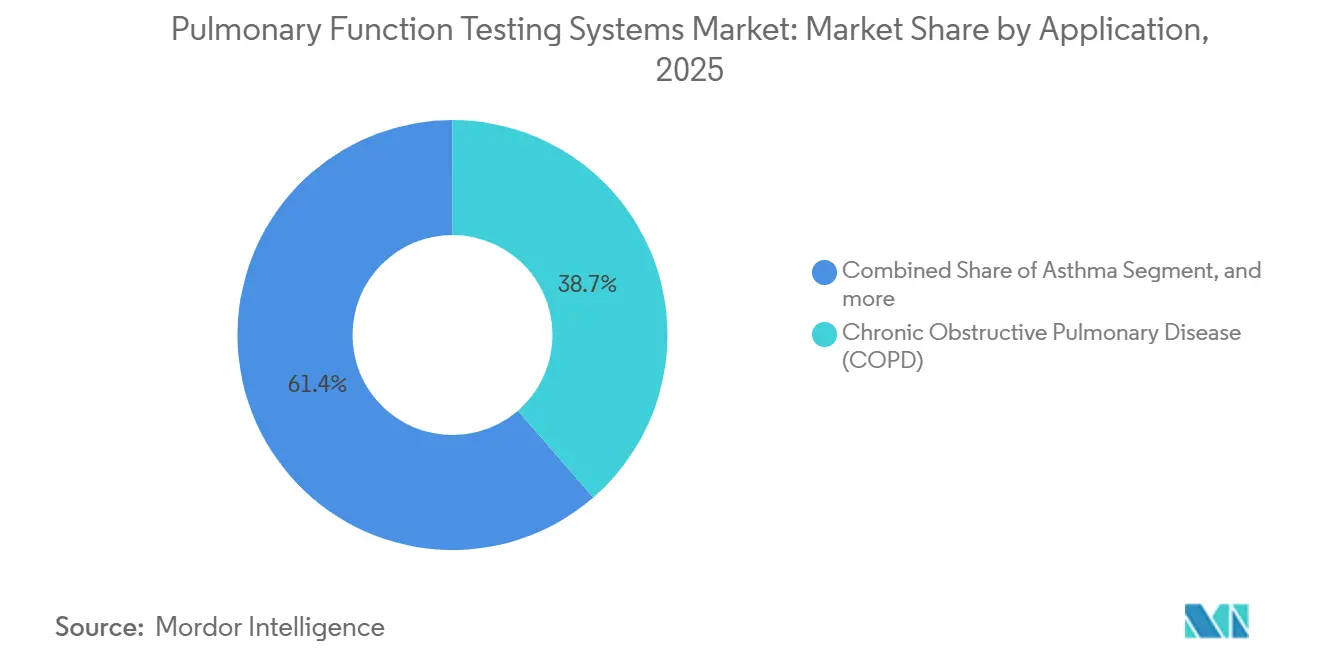

- By application, COPD accounted for 38.65% revenue share in 2025; asthma management is projected to grow at an 8.21% CAGR over the same horizon.

- By end user, hospitals and clinics led with 47.87% of 2025 revenue, but home care settings are projected to climb at an 8.54% CAGR to 2031.

- By geography, North America dominated with a 42.56% share in 2025; Asia-Pacific is the fastest-growing region with a 6.54% CAGR forecast through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pulmonary Function Testing Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Respiratory Disease Burden | +1.2% | Global with APAC and South Asia hot spots | Medium term (2–4 years) |

| Technological Advancements In Pulmonary Function Devices | +0.9% | North America and EU lead, APAC adoption quickening | Short term (≤ 2 years) |

| Growth Of Home Healthcare And Telehealth Adoption | +1.4% | North America and EU core, urban APAC spill-over | Short term (≤ 2 years) |

| Increasing Healthcare Expenditure And Infrastructure Development | +0.7% | China, India, GCC, Latin America | Medium term (2–4 years) |

| Favorable Government Initiatives And Screening Programs | +0.6% | Europe, North America, APAC public-health drives | Short term (≤ 2 years) |

| Expanding Geriatric Population Susceptible To Lung Disorders | +0.8% | Japan, Germany, Italy, United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Respiratory Disease Burden

COPD and asthma case counts continue to climb, making them the third-leading cause of death worldwide. The Institute for Health Metrics and Evaluation reported 392 million COPD cases and 262 million asthma cases in 2021, yet fewer than 30% of symptomatic adults in low- and middle-income nations receive spirometry-confirmed diagnoses. Air pollution levels that exceed World Health Organization PM2.5 limits by five to ten times are accelerating disease onset in South Asia and sub-Saharan Africa, pushing demand for portable testing that can reach community clinics. India’s 2024 National Health Survey showed a 22% rise in breathlessness among adults aged 40–60 compared with 2019, while spirometry use in primary care stays below 5%[1]Ministry of Health and Family Welfare India, “National Health Survey 2024,” mohfw.gov.in. European guidelines issued in 2025 now recommend spirometry for all smokers aged 40 or older, a policy that could double annual testing volumes across the region.

Technological Advancements in Pulmonary Function Devices

Artificial-intelligence coaching has begun to automate quality assurance, trimming technician time per test. NuvoAir’s Air Next, cleared by the FDA in January 2024, flags sub-optimal effort and cuts failed spirometry sessions from 15% to 5%. Thorasys launched a portable impulse oscillometry device in 2025 that measures respiratory impedance across 5–37 Hz and detects small-airway obstruction earlier than spirometry[2]Thorasys Thoracic Medical Systems Inc., “Portable IOS Device Technical Sheet,” thorasys.com. Micro-electromechanical flow sensors now achieve ±2% accuracy in devices under 200 g, fostering field screening and home monitoring. These innovations shorten test workflows, improve data reliability, and broaden adoption outside hospital laboratories.

Growth of Home Healthcare and Telehealth Adoption

Medicare began reimbursing home spirometry under CPT 99457 and 99458 in June 2024, paying USD 64 for setup and USD 52 per month for monitoring. Clinics that distribute devices recover costs within a year while reducing COPD hospitalizations by up to 25% among enrolled patients. Anthem piloted similar coverage in 2025 for high-risk asthma patients and documented a 31% drop in oral steroid courses. China’s reimbursement catalog added home spirometry in March 2025, opening a potential market of 100 million users. FHIR-based data interfaces, now mandatory for new FDA filings, will resolve interoperability gaps by 2027 and streamline telehealth workflows.

Expanding Geriatric Population Susceptible to Lung Disorders

Adults aged 65 and older have COPD prevalence 4.2 times higher than those aged 40–64 and experience faster lung-function decline. Japan expects its 75+ cohort to reach 20.1 million in 2030, with one-third needing chronic respiratory care. Germany and Italy face similar demographic pressures, driving hospital admissions for geriatric respiratory conditions up by 9% per year. Portable testing mitigates travel burdens for mobility-impaired elders and enables more frequent monitoring between clinic visits. The European Union earmarked EUR 120 million in 2025 for digital programs, including home spirometry for age-related disease management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Maintenance Costs | -0.7% | Global, acute in resource-constrained systems | Medium term (2–4 years) |

| Limited Reimbursement And Budget Constraints | -0.9% | Europe, Latin America, emerging-market public payers | Short term (≤ 2 years) |

| Shortage Of Skilled Respiratory Technologists | -0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Stringent Regulatory Approvals And Compliance Requirements | -0.5% | Global, most stringent in U.S. and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs

Complete multifunction systems cost USD 40,000–120,000, while annual service contracts add another 8–12% of the purchase price, stretching payback periods beyond five years for low-volume hospitals. Body-plethysmography chambers require quarterly leak tests costing USD 2,500–4,000 and often require factory visits that sideline equipment for weeks. Many district hospitals in India lack calibration tools and must rely on third-party service providers with 30-day wait times. Portable spirometers priced under USD 5,000 ease entry but cannot perform diffusion capacity or body-volume tests, limiting their use in tertiary diagnostics. Pay-per-test leasing models emerged in 2025 but remain uncommon and have yet to scale globally.

Limited Reimbursement and Budget Constraints

Medicare reimbursement for in-office spirometry ranges from USD 38 to 52 and has stayed flat since 2018, squeezing margins at diagnostic centers. The United Kingdom cut PFT tariffs 6% in 2024, forcing some trusts to limit testing to symptomatic patients. Brazil covers spirometry only for COPD diagnosis, leaving routine monitoring as an out-of-pocket cost of BRL 150–300 (USD 30–60) that many cannot afford. South Africa budgeted ZAR 85 million (USD 4.5 million) for respiratory diagnostics in 2025, equipping just 12% of district hospitals with basic devices. Such funding gaps delay equipment purchases, limit test volumes, and slow market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Configuration: Portability Reshapes Deployment

Portable devices are eroding the entrenched position of laboratory platforms. Complete systems accounted for 52.54% of the pulmonary function testing market share in 2025 and still dominate tertiary centers, while portable and handheld devices are forecast to grow at a 7.54% CAGR through 2031. Leasing schemes and pay-per-test subscriptions convert high capital expenditure into operating costs, broadening access in rural and resource-limited settings. NuvoAir’s 180-g Air Next, cleared by the FDA in 2024, underscores the engineering shift toward lightweight MEMS flow sensors and embedded AI coaching that lowers technician requirements. The pulmonary function testing systems market size for portable models is projected to expand fastest as occupational medicine, home health agencies, and primary-care offices embed field testing into routine workflows.

Tabletop spirometers and modular add-ons remain relevant in specialty practices. Allergists use tabletop units for bronchodilator reversibility testing, while modular configurations allow phased upgrades as test volumes increase. ISO 26782-compliant self-calibration routines embedded in modern devices have eased maintenance, yet multicomponent quality control remains a challenge for smaller institutions with limited biomedical staff. As payers continue shifting costs downstream, stakeholders expect portable units to claim a substantial slice of new installations, especially in Asia-Pacific markets where government programs subsidize home-based chronic-care management.

By Test Type: Spirometry Dominance Faces Oscillometry Challenge

Spirometry accounted for 45.43% of the pulmonary function testing market share in 2025, as guidelines mandate its use for COPD and asthma diagnosis across more than 120 countries. Testing costs average USD 30–60, enabling broad access despite budget constraints. Body plethysmography and diffusion capacity testing support assessments of restrictive and interstitial lung disease, but higher per-test costs limit their expansion. Impulse oscillometry, however, is forecast to advance at 7.66% CAGR through 2031 as evidence mounts that it detects small-airway dysfunction in patients whose spirometry appears normal. Thorasys’ USD 18,000 portable IOS unit, launched in 2025, delivers laboratory-grade impedance metrics without a sealed chamber, lowering adoption thresholds.

Regulatory momentum supports oscillometry’s rise; in 2024, the FDA issued draft guidance endorsing IOS as an asthma-trial endpoint, improving payer receptivity. The pulmonary function testing systems market size tied to IOS remains relatively small but could accelerate as clinicians integrate the test into remote monitoring pipelines. Exercise stress and high-altitude simulation remain niche, driven by sports medicine and aviation. As AI interpretation algorithms mature, the cost of advanced modalities may fall, broadening deployment beyond academic centers.

By Application: Asthma Management Gains Momentum

Although COPD accounted for 38.65% of 2025 revenue, asthma is expected to grow at 8.21% CAGR through 2031, outpacing the total pulmonary function testing systems market. Biologic agents priced at USD 30,000–50,000 annually require objective lung-function documentation for payer approval, doubling spirometry frequency to every three to six months for treated patients. The pulmonary function testing systems market size associated with asthma may therefore capture incremental device placements as allergists and pulmonologists seek to optimize therapy.

Interstitial lung diseases rely heavily on DLCO measurement for staging and treatment response, generating stable demand inside academic centers despite smaller patient numbers. Preoperative assessment, occupational surveillance, and disability evaluations round out steady-state usage. As technology and reimbursement converge to support at-home testing, clinical protocols are already adapting, with home spirometry data being accepted for therapy escalation decisions under certain payer policies.

By End User: Homecare Settings Accelerate

Hospitals and clinics contributed 47.87% of 2025 revenue, reflecting installed laboratory systems and technician capacity. Yet their share is eroding as home care settings are projected to record an 8.54% CAGR to 2031. Medicare remote-monitoring payments cover consumables and professional oversight, enabling pulmonology practices to extend care without expanding brick-and-mortar labs. Published managed-care data show 23% fewer COPD hospitalizations among telemonitored patients, driving net savings of USD 3,200 per capita annually.

Diagnostic centers face tighter margins as reimbursement declines, while occupational health and military medical facilities procure portable devices to comply with exposure-surveillance mandates. The pulmonary function testing systems market size allocated to these niche settings grows modestly, steadying overall demand and ensuring unit shipments remain diversified across care sites.

Geography Analysis

North America accounted for 42.56% of global revenue in 2025, buoyed by Medicare and commercial coverage that reimburse spirometry for a wide range of indications. The United States performs nearly 28 million spirometry tests annually, aided by an Occupational Safety and Health Administration requirement for workers exposed to respirable hazards[3]Occupational Safety and Health Administration, “Respirable Dust Standard,” osha.gov. Canada’s 2024 COPD framework now recommends screening smokers aged 40 and older, potentially boosting national test volumes by 20%. Mexico’s private hospitals in urban zones run full PFT suites, yet public-sector access remains restricted by out-of-pocket fees of MXN 800–1,500. Workforce shortages, with 30% more respiratory therapists needed by 2032, present the region’s chief structural constraint.

Asia-Pacific is projected to advance at a 6.54% CAGR through 2031. China’s healthcare spending reached 7.1% of GDP in 2024, and in 2025, reimbursement for home spirometry opened a market of 100 million candidates. India’s spirometry penetration remains below 5% despite 55 million cases of COPD, highlighting significant untapped demand. Japan’s aging population and mobility challenges fuel portable-device sales, while Australia leveraged its Pharmaceutical Benefits Scheme to extend remote monitoring to rural COPD patients in 2024. South Korea’s 2025 COPD screening program targets 2 million annual tests for high-risk smokers.

Europe faces budgetary headwinds but maintains mature infrastructure. Germany, the United Kingdom, France, Italy, and Spain account for 65% of regional PFT revenue. Horizon Europe’s EUR 120 million allocation in 2025 supports remote pulmonary monitoring pilots across member states. The Middle East and Africa region is nascent but accelerating; the United Arab Emirates mandated national COPD spirometry in 2024, adding 50 000 tests yearly. Latin America exhibits patchwork growth: Brazil reimburses diagnostic spirometry but not monitoring, while Argentina rolled out primary-care screening in 2025 for urban high-risk populations.

Competitive Landscape

The pulmonary function testing systems market demonstrates moderate concentration: the top five vendors collectively hold about 55–60% share in complete systems. BD (CareFusion), Vyaire Medical, MGC Diagnostics, ndd Medical Technologies, and Philips Healthcare rely on installed bases, multi-year service agreements, and regulatory know-how. Vyaire’s 2024 sale to Trudell Medical International highlighted private-equity interest in the predictable cash flows of respiratory diagnostics. Incumbents now bundle software, analytics, and cloud storage to guard margins against hardware commoditization.

New entrants focus on portable devices with embedded AI. NuvoAir’s cellular-enabled Air Next secured a 15,000-patient remote-monitoring deal with a U.S. health system after FDA clearance. Patent filings between 2024 and 2026 reveal 37 MEMS-sensor innovations and 22 machine-learning interpretation models, signaling a shift toward software-driven competitive advantage. Regulatory compliance under ISO 26782 acts as a moat, elongating development cycles by 12–18 months and deterring low-cost imitators that lack quality-management infrastructure.

Growth white space lies in occupational health, where only 40% of workers exposed to hazardous dust receive annual spirometry testing. Portable devices with cellular transmission can close that gap by delivering on-site testing without specialist staff. Manufacturers are exploring subscription models that charge per completed test, aligning revenue with customers’ occupational-screening calendars.

Pulmonary Function Testing Systems Industry Leaders

Becton, Dickinson and Company

KoKo PFT

Schiller AG

COSMED

Vyaire Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Weeks Medical Center (WMC), a proud affiliate of North Country Healthcare (NCH) installed a new Pulmonary Function Test (PFT) unit from MGC Diagnostics.

- November 2024: Vyaire Medical finalized its sale to Trudell Medical International, combining hospital PFT systems with aerosol-therapy portfolios

- January 2024: NuvoAir obtained FDA 510(k) clearance for Air Next, a cellular-enabled home spirometer with AI quality assurance that lowers failed tests from 15% to 5%

Global Pulmonary Function Testing Systems Market Report Scope

As per the scope of the report, pulmonary function testing (PFT) systems are diagnostic tools used to evaluate lung function by measuring airflow, lung volumes, and gas exchange. They help diagnose respiratory conditions such as asthma, COPD, and restrictive lung diseases. These systems provide vital data to assess respiratory health and guide treatment plans.

The Pulmonary Function Testing Systems Market is Segmented by Product Configuration (Complete PFT Systems and Portable/Handheld Systems), Test Type (Spirometry, Body Plethysmography, Gas Diffusion, Impulse Oscillometry, and Exercise Stress & High-Altitude Simulation), Application (COPD, Asthma, Pulmonary Fibrosis & ILD, Chronic Shortness of Breath, and Other Applications), End User (Hospitals & Clinics, Diagnostic Centers, Homecare Settings, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Complete PFT Systems |

| Portable/Handheld Systems |

| Spirometry |

| Body Plethysmography (Lung Volume) |

| Gas Diffusion (DLCO) |

| Impulse Oscillometry |

| Exercise Stress & High-Altitude Simulation |

| Chronic Obstructive Pulmonary Disease (COPD) |

| Asthma |

| Pulmonary Fibrosis & ILD |

| Chronic Shortness Of Breath |

| Other Applications |

| Hospitals & Clinics |

| Diagnostic Centers |

| Homecare Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Configuration | Complete PFT Systems | |

| Portable/Handheld Systems | ||

| By Test Type | Spirometry | |

| Body Plethysmography (Lung Volume) | ||

| Gas Diffusion (DLCO) | ||

| Impulse Oscillometry | ||

| Exercise Stress & High-Altitude Simulation | ||

| By Application | Chronic Obstructive Pulmonary Disease (COPD) | |

| Asthma | ||

| Pulmonary Fibrosis & ILD | ||

| Chronic Shortness Of Breath | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Centers | ||

| Homecare Settings | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current global value of the pulmonary function testing systems market?

The market is valued at USD 3.07 billion in 2026 and is forecast to reach USD 4.08 billion by 2031.

Which product category is expanding fastest within pulmonary function testing?

Portable and handheld devices are expected to grow at a 7.54% CAGR through 2031 as home monitoring gains reimbursement support.

Why is impulse oscillometry attracting attention?

IOS can detect small-airway dysfunction in patients who have normal spirometry, and regulatory draft guidance now recognizes it as a valid asthma-trial endpoint.

How are reimbursement policies influencing adoption?

Medicare and several private and international payers now reimburse remote spirometry, shifting testing from hospital labs to patients homes.

Which region offers the highest growth potential?

Asia-Pacific is projected to expand at a 6.54% CAGR, propelled by China's and India's large patient pools and emerging reimbursement frameworks.

What chief barrier could slow the market's growth trajectory?

Shortages of trained respiratory therapists could limit the speed at which providers integrate advanced testing modalities into routine care.

Page last updated on: