Publishing and Print Media Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 357.58 Billion |

| Market Size (2031) | USD 398.03 Billion |

| Growth Rate (2026 - 2031) | 2.17% CAGR |

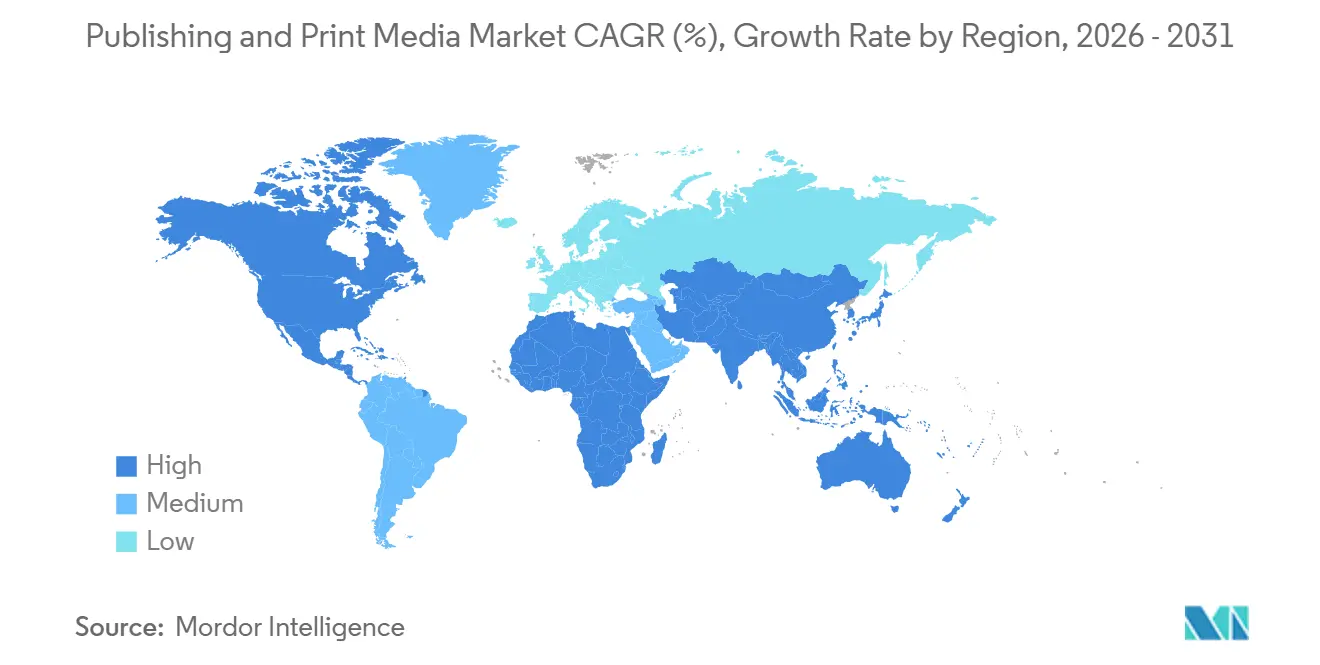

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Publishing and Print Media Market Analysis by Mordor Intelligence

The Publishing and Print Media market size is projected to expand from USD 349.60 billion in 2025 and USD 357.58 billion in 2026 to USD 398.03 billion by 2031, registering a CAGR of 2.17% between 2026 to 2031. The publishing and print media market continues to hold scale because educational demand, professional information services, and recurring subscriptions are offsetting weakness in legacy print advertising and print circulation. The clearest growth path in the publishing and print media market comes from digital subscriptions, direct reader relationships, and content licensing models that convert archives and proprietary content into recurring revenue. The publishing and print media market is also being reshaped by AI, because the same tools that support editorial workflows and new licensing income are also increasing scraping risks and putting pressure on copyright enforcement. Competitive advantage in the publishing and print media market is moving toward companies that combine trusted content, software tools, and distribution control, while businesses that remain tied to print-heavy models face weaker monetization. Regional opportunity in the publishing and print media market remains strongest where educational demand, digital reading adoption, and IP monetization ecosystems are expanding together.

Key Report Takeaways

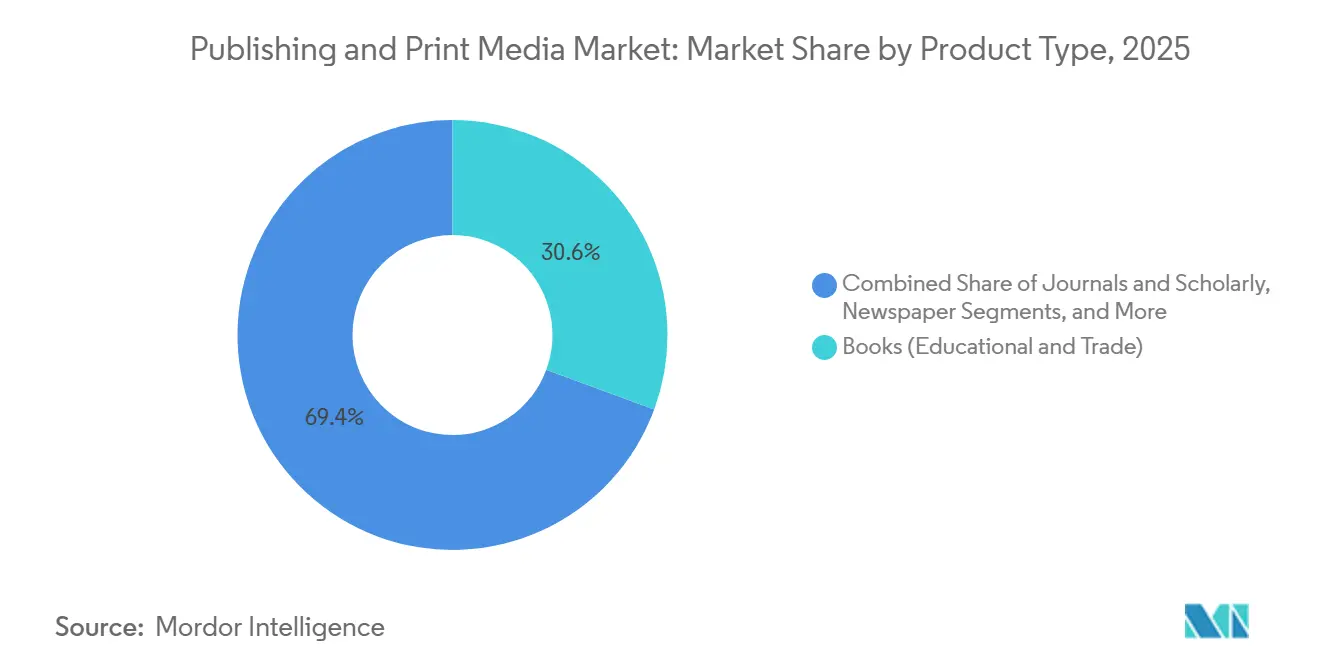

- By Product Type, Books (Educational and Trade) commanded 30.63% of the publishing and print media market share in 2025, while the Others segment, encompassing journals, scholarly, and academic publications, is projected to expand at 3.16% CAGR through 2031.

- By Format, Traditional Formats retained 66.26% of the publishing and print media market share in 2025, while the Digital segment is projected to grow at 5.72% CAGR through 2031.

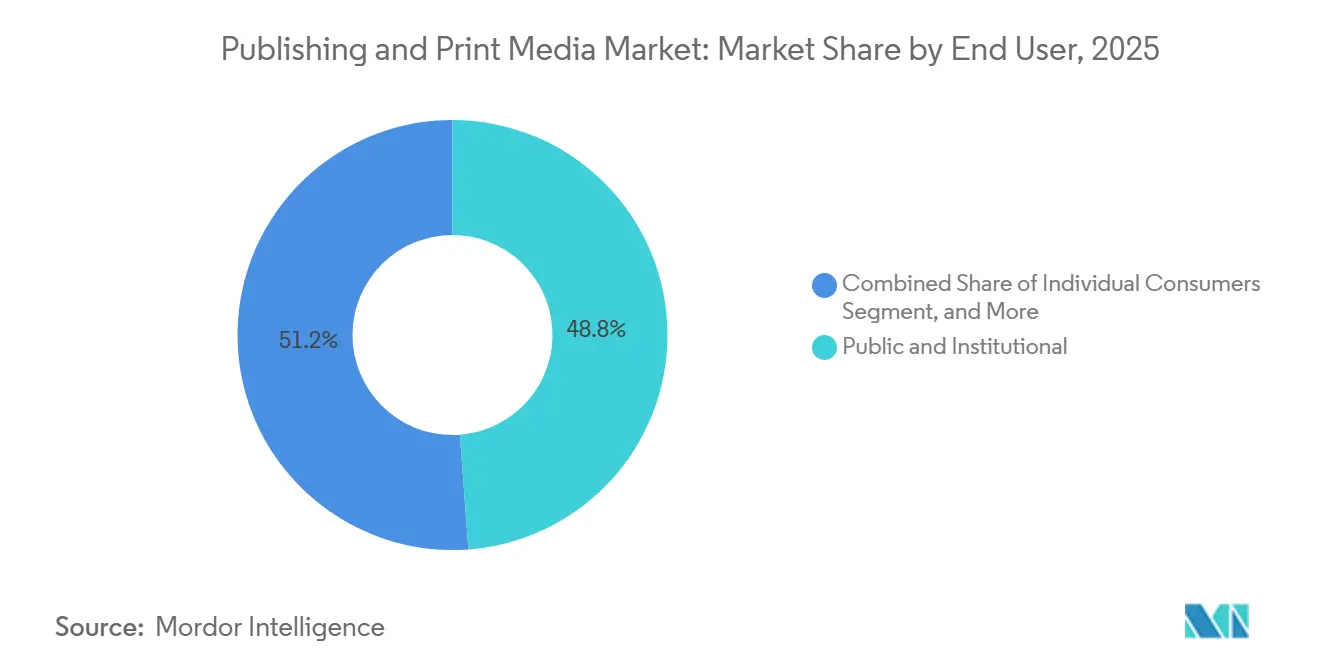

- By End User, the Public and Institutional Sector held 48.82% revenue share in 2025, while Individual Consumers are expected to expand at 4.66% CAGR through 2031.

- By Geography, North America contributed 33.64% of revenue in 2025, while Asia-Pacific is projected to advance at 3.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Publishing and Print Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift to Subscription-Led Digital Revenue Models | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising Demand for Educational and Academic Publishing | +0.5% | Global, especially Asia-Pacific and North America | Long term (≥ 4 years) |

| Growth of Multi-Format Monetization Platforms | +0.4% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expansion of Direct-to-Consumer Reader Engagement | +0.3% | North America, with spillover to Europe | Medium term (2-4 years) |

| Higher Value From Niche, Localized, and Specialized Content | +0.2% | Asia-Pacific core, with spillover to South America and the Middle East | Long term (≥ 4 years) |

| AI-Assisted Editorial and Production Workflows | +0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Subscription-Led Digital Revenue Models

The publishing and print media market is moving further toward subscription-led revenue because recurring digital payments are proving more stable than advertising-led models. FIPP states in 2026 that publishers using bundle strategies and strong direct audience relationships are still recording better retention across regions, even as growth patterns become less uniform.[1]FIPP, “FIPP's Global Digital Subscription Snapshot 2026, Growing Influence of AI Search,” FIPP That matters because the publishing and print media market increasingly rewards operators that can keep readers inside a paid ecosystem across news, books, audio, and specialist content. Subscription businesses also gain better visibility on churn, pricing, and product usage, which helps them plan content investment with more discipline than publishers that depend on volatile traffic and advertising. The result is a publishing and print media market where loyalty, renewal rates, and bundle design are becoming more important than scale in raw audience reach. Companies that establish durable subscription habits now are likely to enter the later years of the forecast period with stronger pricing control and better revenue quality.

Rising Demand for Educational and Academic Publishing

Educational and academic demand remains one of the most stable growth supports in the publishing and print media market. Pearson reports 4% underlying revenue growth for 2025, while its Virtual Learning segment records 8% sales growth on higher enrollments, which shows that institutional learning demand continues to support publisher revenue even in a slower-growth environment.[2]Pearson PLC, “2025 Preliminary Results (Unaudited),” Nasdaq Pearson also signals in 2026 that partnerships with Microsoft, AWS, Google Cloud, and Salesforce.com are supporting the wider shift toward AI-enabled learning content and digital courseware within mainstream procurement. The publishing and print media market benefits from this because academic, professional, and workforce learning content is purchased through multiyear institutional channels that are less exposed to the traffic swings seen in consumer media. Journals and scholarly publishing are also supported by higher research activity and open-access requirements, which widen the submission and usage base for specialized content. This keeps the publishing and print media market anchored by demand that is tied to education, training, and research rather than only consumer discretionary spending.

Growth of Multi-Format Monetization Platforms

The publishing and print media market is gaining from business models that extend a single content asset across print, digital, audio, screen, and merchandise. Hachette Livre and Studiocanal establish the On Screen joint venture in 2026 to develop film and television adaptations from Hachette's catalog, which shows how publishers are turning book rights into a broader content pipeline.[3]Hachette Livre, “Hachette Livre and STUDIOCANAL Announce a Strategic Partnership to Unlock the Full Potential of Book-to-Screen Adaptations,” Hachette Louis Hachette Group also reports that Hachette Livre generated EUR 3.0 billion, USD 3.24 billion, in 2025 revenue, which underlines the scale available to publishers that can monetize IP across more than one format. China Literature reports that its IP merchandise business exceeded CNY 1.1 billion, USD 151.8 million, in gross merchandise value in 2025, more than doubling from the prior year, which shows how digital reading platforms can extend content into consumer products and other formats. This model raises revenue density because one successful title can support multiple monetization paths instead of one sale event. It also gives the publishing and print media market a stronger route to growth in regions where reading platforms, streaming ecosystems, and consumer brands are increasingly linked.

Expansion of Direct-to-Consumer Reader Engagement

Direct reader engagement is becoming more valuable in the publishing and print media market because it reduces dependence on wholesalers and large retail platforms. Publishers that build first-party storefronts and membership channels gain access to reader data that helps with pricing, title positioning, audience retention, and future acquisitions. That matters because the publishing and print media market is no longer competing only on content output, but also on who owns the customer relationship and the usage signals behind it. Direct channels also protect margin by reducing layers between publisher and reader, which is important when print, logistics, and paid acquisition costs remain under pressure. Over time, publishers with direct consumer relationships are likely to operate with better targeting, better upsell potential, and better control over bundle design than publishers that rely mainly on intermediated distribution. This makes reader ownership a practical growth asset in the publishing and print media market rather than a branding exercise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Secular Decline in Print Circulation and Revenue | -0.6% | Global, intensified in North America and Europe | Long term (≥ 4 years) |

| Rising Customer Acquisition Costs for Digital Platforms | -0.3% | North America and Europe | Medium term (2-4 years) |

| Higher Exposure to Content Piracy and Unauthorized Distribution | -0.2% | Asia-Pacific core, with spillover to South America | Long term (≥ 4 years) |

| Margin Pressure From Paper, Logistics, and Supply Chain Costs | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Secular Decline in Print Circulation and Revenue

The publishing and print media market still depends on print revenue in several categories, but the economics of that base continue to weaken. Print remains important in educational books, institutional procurement, and parts of trade publishing, yet it no longer offers the same protection for newspapers and advertising-supported media. The pressure is strongest where younger audiences shift to digital formats faster than legacy revenue can be replaced, which leaves publishers managing a slower decline rather than a stable base. This creates a difficult balance because publishers must keep serving loyal print audiences while also funding digital products that will support future growth. The publishing and print media market therefore carries a structural drag from print-heavy businesses that have not fully diversified toward subscription, licensing, or software-linked services. That drag does not remove demand for print altogether, but it lowers the pace at which total revenue can expand.

Rising Customer Acquisition Costs for Digital Platforms

The publishing and print media market is also facing higher customer acquisition costs as search, discovery, and digital targeting become less efficient. FIPP states that AI search is changing the link between publisher visibility and referral traffic, which pushes more publishers toward direct audience investment and paid acquisition methods. This raises pressure on introductory pricing, bundle discounts, and marketing spend, especially for newer digital products that do not yet have strong organic loyalty. In Europe, privacy rules under the GDPR and evolving consent standards also reduce the precision of behavioral targeting, which weakens conversion efficiency for subscription campaigns.[4]European Union, “Regulation (EU) 2016/679 General Data Protection Regulation,” EUR-Lex Publishers with strong owned brands and established customer databases are better placed to manage this shift than newer entrants that depend on search or platform discovery. As a result, the publishing and print media market is likely to reward early investment in direct traffic, retention systems, and first-party data rather than only spending more on paid growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Books Drive Scale as Others Reshape Academic Revenue

Books (Educational and Trade) held 30.63% of revenue in 2025, making them the largest product category in the publishing and print media market. That scale reflects steady procurement from schools, universities, libraries, and corporate learning buyers, along with persistent consumer demand for trade titles in print and digital forms. The publishing and print media market still depends on books for broad revenue coverage because this category serves both institutional contracts and retail channels. Even where growth is modest, books provide a stable base that many other product lines do not match. Newspapers remain under more pressure because they are more exposed to print circulation weakness and advertising erosion. Magazines and periodicals, along with catalogs, brochures, and flyers, continue to rely on clearer digital monetization paths to defend revenue.

The Others segment is forecast to expand at 3.16% CAGR through 2031, which makes it the fastest-growing product group within the publishing and print media market. John Wiley and Sons acquires Emerald Publishing Limited in June 2026 for GBP 337 million, USD 452 million, adding a business with 92% recurring subscription revenue and more than USD 85 million in projected 2026 revenue. That move shows why journals, scholarly content, academic publishing, audiobooks, podcasts, and born-digital formats are becoming more valuable inside the publishing and print media industry. Open-access mandates and higher research output also support journals and scholarly titles, which strengthens demand for trusted editorial processes and subscription-backed specialist content. Established publishers have an advantage here because they already operate the governance, peer review, and information security systems that institutional buyers expect. This leaves the publishing and print media market with a product mix where books anchor scale, while specialized and recurring content is doing more to improve growth quality.

By Format: Traditional Holds Revenue as Digital Rewrites Margin Economics

Traditional formats accounted for 66.26% of revenue in 2025, which shows that physical books and other legacy formats still carry most of the publishing and print media market size. This large share reflects the staying power of print in education, institutional procurement, and selected consumer categories rather than a return to broad-based growth in traditional media. Many publishers still rely on print because it remains important in classrooms, libraries, and professional reference use cases where format change moves more slowly. The publishing and print media market therefore continues to earn most of its revenue from traditional formats even as growth leadership shifts elsewhere. That split explains why total market expansion remains moderate while format-level economics are changing faster beneath the surface.

Digital is forecast to grow at 5.72% CAGR through 2031, making it the fastest-moving format in the publishing and print media market. McGraw-Hill introduces new AI capabilities in its Connect higher education platform in 2026, adding AI-powered study tools and instructor analytics to a system already used by millions of students worldwide. That type of product improves margin economics because digital content can be updated, distributed, and personalized without the same printing and logistics burden. At the same time, Akamai reports that AI bot activity against publishing sites surged 300% in 2025 and that publishing companies absorbed 40% of such activity, which shows the higher piracy and scraping exposure attached to digital growth. Publishers are therefore pushing digital expansion while also investing more in rights management, access control, and technical protection. This keeps the publishing and print media market in a position where digital improves revenue quality and scalability, but only for companies that can protect content and operate strong workflow systems.

By End User: Institutional Procurement Anchors Scale While Individual Consumers Accelerate

Public and Institutional Sector represented 48.82% of revenue in 2025, which made it the largest end-user group in the publishing and print media market. Universities, libraries, hospitals, law firms, and government agencies support this position because they buy through subscriptions, site licenses, and multiyear agreements that are more predictable than many consumer channels. That stability matters because it gives the publishing and print media market a large demand base that is less tied to short-term audience shifts. Institutional buyers also favor trusted brands, reliable archives, and compliance-ready content, which supports established publishers over smaller entrants. In practical terms, this segment keeps a large part of the market tied to recurring contractual revenue rather than one-time transactions.

Individual Consumers is forecast to expand at 4.66% CAGR through 2031, which makes it the fastest-growing end-user segment in the publishing and print media market. Consumer demand is improving through bundled offers that combine e-books, audiobooks, and social reading features, which makes digital reading more convenient and more frequent. At the same time, the Enterprises and Professional Users segment is changing because buyers increasingly want content embedded in tools that produce answers inside daily work. Thomson Reuters states in 2026 that CoCounsel has reached 1 million professionals across 107 countries, and the company says generative AI-enabled products represent 30% of its total annualized contract value in Q1 2026. This shows that the publishing and print media industry is moving beyond document access toward workflow-linked professional products. It also means the publishing and print media market is seeing consumer growth on one side and software-connected institutional value on the other, which widens the gap between strong and weak business models.

Geography Analysis

North America held 33.64% of revenue in 2025, which gave it the largest regional position in the publishing and print media market size. The region benefits from mature subscription habits, strong educational procurement, and a large base of professional information services revenue. The United States remains the main center of this activity because higher education, legal, tax, healthcare, and business information products generate steady demand across digital and print-linked formats. Canada adds support through educational and professional publishing, while Mexico remains an important Spanish-language consumer market where book revenue grew 7.0% in 2025.

Asia-Pacific is projected to grow at 3.22% CAGR through 2031, making it the fastest-growing region in the publishing and print media market. India stands out because its book market revenue grew 20.7% in 2025, showing strong demand for educational and consumer titles. China is important for a different reason, because digital reading, online fiction, and wider IP monetization are linking publishing to merchandise and screen adaptation. China Literature reports 820,000 original works online and strong growth in merchandise-linked monetization, which points to a broad digital reading infrastructure that extends beyond book sales alone. South Korea adds momentum through digital comics and webtoon ecosystems, while Australia contributes steady institutional and educational demand. Together, these factors make Asia-Pacific the region where the publishing and print media market is changing fastest in format mix, reader behavior, and monetization structure.

Europe presents a mixed picture in the publishing and print media market, with strong export performance in some countries and softer consumer demand in others. The United Kingdom reaches its highest-ever publishing revenue in 2025, with exports rising 4%, which shows the region's continued strength in rights, education, and English-language trade publishing. France declines 1.0% in value to EUR 4.4 billion, USD 4.75 billion, in 2025, while Brazil grows 11.2%, showing that South America is expanding from a lower base through stronger local demand and wider digital access. The Middle East is building publishing infrastructure through literacy programs and digital platform investment, while Africa remains centered on educational and academic demand led by markets such as South Africa, Egypt, and Nigeria. This leaves the publishing and print media market with a regional pattern where North America leads in current revenue, Asia-Pacific leads in growth, and Europe, South America, the Middle East, and Africa each reflect different mixes of institutional demand, consumer recovery, and digital adoption.

Competitive Landscape

The publishing and print media market remains split between a concentrated group of professional information leaders and a broader set of trade, education, and news publishers. RELX PLC, Thomson Reuters Corporation, Wolters Kluwer N.V., and Springer Nature AG and Co. KGaA are the most established names in professional, scientific, legal, tax, and regulatory publishing because they combine proprietary content with workflow software and recurring contracts. RELX strengthened that position in 2025 with 7% underlying revenue growth and a 34.8% adjusted operating margin, supported by large-scale scientific, legal, and risk data assets that are difficult to replicate. Thomson Reuters also widened its lead in AI-enabled professional publishing, with CoCounsel reaching 1 million professionals across 107 countries by February 2026, while generative AI-enabled products represented 30% of its total annualized contract value in Q1 2026. Wolters Kluwer continued to build its compliance and legal technology position through the January 2026 acquisition of StandardFusion and the November 2025 acquisition of Libra Technology GmbH, which strengthened its recurring software and AI-led workflow offering.

In trade and educational publishing, Bertelsmann SE and Co. KGaA, through Penguin Random House, Hachette Livre, Simon and Schuster LLC, Pearson PLC, McGraw Hill, Inc., and Cengage Group remain the major players shaping scale and competitive direction. Bertelsmann reported EUR 5.0 billion, USD 5.40 billion, in 2025 revenue from Penguin Random House and stated in March 2026 that it had a strong pipeline of acquisition targets, which signals continued consolidation in large-format publishing. Hachette Livre expanded on both content and monetization fronts in 2026 by creating the On Screen joint venture with Studiocanal for book-to-screen adaptations and by acquiring Kogan Page in the United Kingdom to deepen its business publishing portfoli. Simon and Schuster also moved to widen distribution and author access through the launch of Simon Global in May 2026 and the July 2026 relaunch of Pocket Books as a platform for self-published authors. Pearson, McGraw Hill, and Cengage are defending their positions through digital courseware, AI-enabled learning tools, and brand integration, which keeps educational publishing tied closely to institutional demand and platform capability.

News and consumer media publishers face a harder operating environment, even though players such as Gannett Co., Inc., Guardian Media Group plc, Daily Mail and General Trust plc, and Postmedia Network Canada Corp. remain important in their respective categories. Gannett responded by signing an AI content licensing agreement with Microsoft in October 2025, showing how news publishers are trying to monetize archives beyond advertising and circulation. Springer Nature also reshaped its portfolio in June 2026 by divesting Scientific American and Spektrum der Wissenschaft, which sharpened its focus on research, health, and education publishing rather than consumer media. Overall competition remains fragmented across product types, but the strongest players are the ones pairing trusted content with subscriptions, AI tools, direct distribution, and rights monetization across multiple formats.

Publishing and Print Media Industry Leaders

RELX PLC

News Corporation

Pearson PLC

Bertelsmann SE & Co. KGaA

Springer Nature AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: John Wiley & Sons, Inc. acquired Emerald Publishing Limited from Cambridge Information Group in an all-cash transaction valued at GBP 337 million (USD 452 million), per Wiley's June 2, 2026 announcement. Emerald projects over USD 85 million in 2026 revenue with 92% recurring subscription revenue, deepening Wiley's research content scale and its proprietary content position for AI data licensing.

- June 2026: Springer Nature AG & Co. KGaA announced the divestiture of Scientific American in the United States to LabX Media Group, completing June 24, 2026, and agreed to sell Spektrum der Wissenschaft in Germany to GeraNova Bruckmann. The two titles contributed approximately EUR 25 million (USD 27.0 million at the 2025 annual average EUR/USD rate of 1.08) to Springer Nature's 2025 revenues, and the transactions refocus the portfolio on research, health, and education publishing.

- May 2026: Hachette Livre and Studiocanal established On Screen, a joint venture dedicated to developing film and television adaptations from Hachette's literary catalogue. Hachette Livre generated EUR 3.0 billion (USD 3.24 billion) in 2025 revenues, per Louis Hachette Group's annual results, and the venture formalizes IP monetization across global screen platforms.

- May 2026: Hachette UK acquired Kogan Page from its previous owners, positioning Hachette as the second-largest publisher of business books in the United Kingdom, per the Lagardère group press release. The acquisition adds award-winning business content across management, leadership, and professional development to Hachette's UK portfolio.

Global Publishing and Print Media Market Report Scope

The Publishing and Print Media Market Report is Segmented by Product Type (Books [Educational and Trade], Newspapers, Magazines and Periodicals, Catalogs, Brochures and Flyers, Journals and Scholarly, and Other Product Types), Format Type (Traditional, and Digital), End User (Individual Consumers, Public and Instituitional Sector, and Enterprises and Professional Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Books (Educational and Trade) |

| Newspapers |

| Magazines and Periodicals |

| Journals and Scholarly |

| Catalogs, Brochures and Flyers |

| Other Product Types |

| Traditional |

| Digital |

| Individual Consumers |

| Public and Instituitional Sector |

| Enterprises and Professional Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Type | Books (Educational and Trade) | |

| Newspapers | ||

| Magazines and Periodicals | ||

| Journals and Scholarly | ||

| Catalogs, Brochures and Flyers | ||

| Other Product Types | ||

| By Format | Traditional | |

| Digital | ||

| By End User | Individual Consumers | |

| Public and Instituitional Sector | ||

| Enterprises and Professional Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the publishing and print media market?

The publishing and print media market stood at USD 349.60 billion in 2025, rises to USD 357.58 billion in 2026, and is forecast to reach USD 398.03 billion by 2031 at a 2.17% CAGR.

Which format is growing the fastest through 2031?

Digital is the fastest-growing format, with a projected 5.72% CAGR through 2031, supported by e-books, digital journals, interactive learning tools, and lower distribution costs.

Which region leads global revenue and which one is growing the fastest?

North America led with 33.64% of revenue in 2025, while Asia-Pacific is projected to grow the fastest at a 3.22% CAGR through 2031.

What is supporting growth in educational and academic publishing?

Institutional demand, workforce reskilling, hybrid learning, research activity, and AI-enabled learning tools are keeping educational and academic publishing more resilient than many other categories.

How is AI changing publisher business models?

AI is creating new revenue options through licensing, analytics, and workflow products, but it is also raising exposure to scraping, piracy, and content protection risks.

Which end-user group matters most today?

Public and Institutional Sector remained the largest end-user group with 48.82% of revenue in 2025, while Individual Consumers is the fastest-growing group at a 4.66% CAGR through 2031.

Page last updated on: