Prurigo Nodularis Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

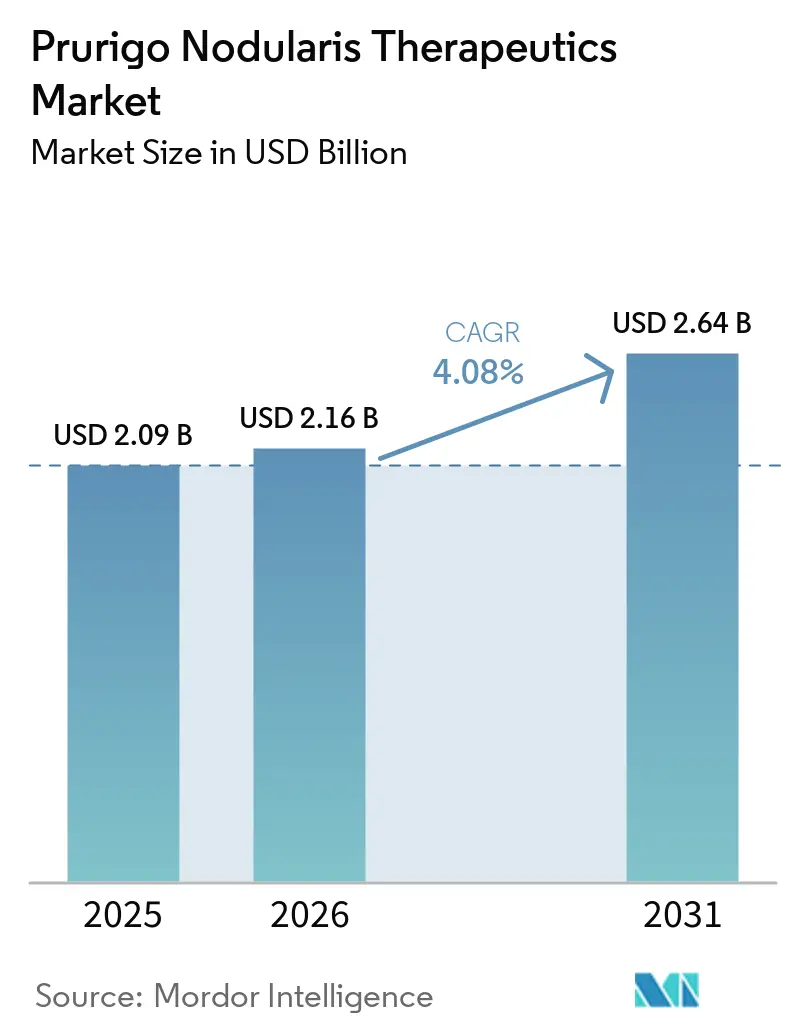

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.64 Billion |

| Growth Rate (2026 - 2031) | 4.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Americas |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prurigo Nodularis Therapeutics Market Analysis by Mordor Intelligence

The Prurigo Nodularis Therapeutics Market size is expected to increase from USD 2.09 billion in 2025 to USD 2.16 billion in 2026 and reach USD 2.64 billion by 2031, growing at a CAGR of 4.08% over 2026-2031.

The prurigo nodularis therapeutics market is shifting from symptomatic care to targeted neuroimmune pathways that address the itch-scratch-fibrosis cycle, which is driving faster adoption of systemic agents across major treatment centers. The U.S. approval of nemolizumab in August 2024 confirmed IL-31 receptor alpha as a validated target and accelerated global clinical interest in adjacent mechanisms. The U.K. authorization in February 2025 signaled alignment among leading regulators and gave prescribers a clear therapeutic framework for moderate-to-severe disease. Teledermatology triage and store-and-forward models are helping clinics preserve in-person slots for patients who require systemic initiation and monitoring, which supports sustained demand in the prurigo nodularis therapeutics market. Patient registries and academic rare-disease consortia are also shortening enrollment cycles for trials that evaluate new mechanisms and combination regimens, which strengthens the long-run launch cadence for late-stage assets in the prurigo nodularis therapeutics market.

Key Report Takeaways

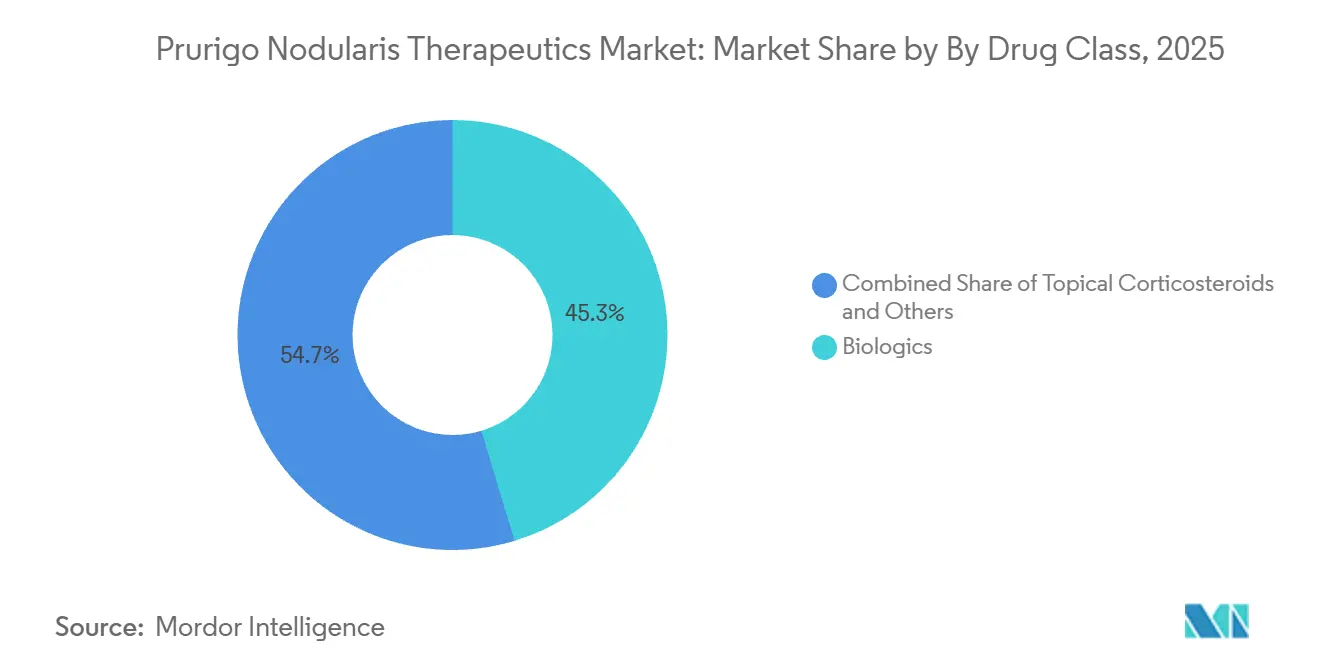

By drug class, biologics led with 45.34% revenue share in 2025, while biologics are projected to expand at a 7.49% CAGR through 2031.

By route of administration, subcutaneous and intramuscular injection captured 45.80% in 2025, and injectables are expected to advance at a 4.77% CAGR to 2031.

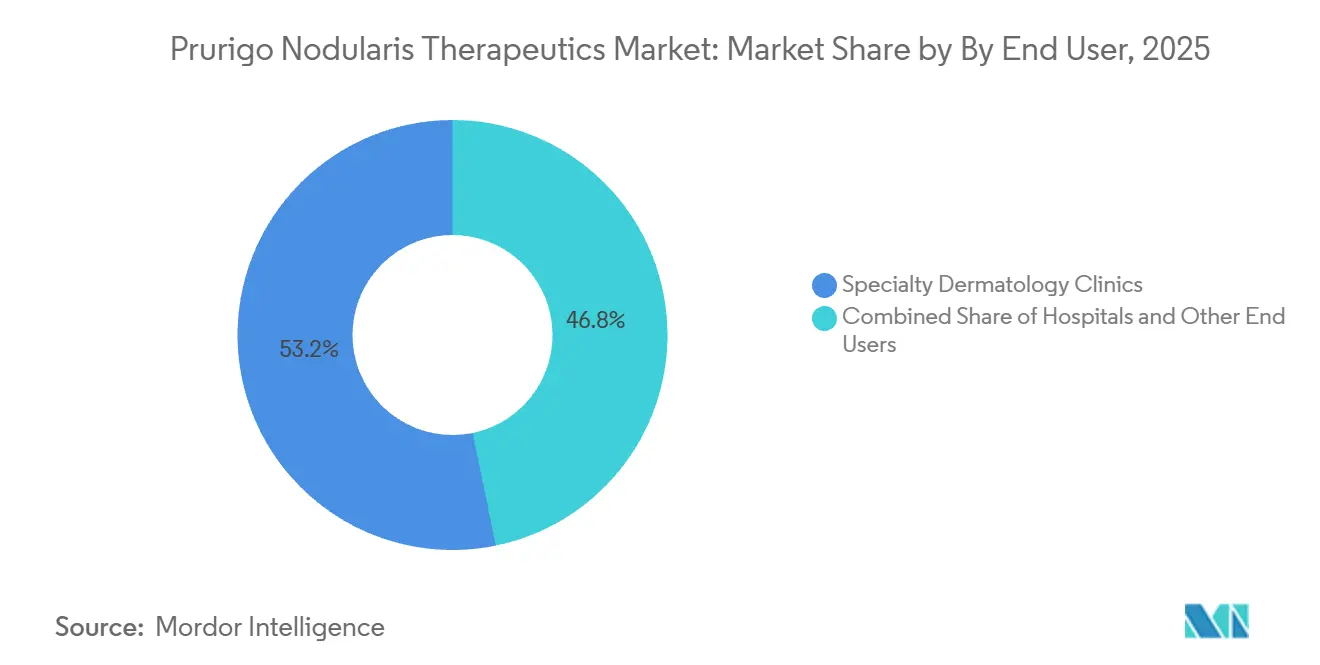

By end-user setting, specialty dermatology clinics held 53.23% in 2025, and home-care and self-administration is the fastest-growing at a 4.90% CAGR.

By geography, North America accounted for 42.11% in 2025, while Asia-Pacific is forecast to grow at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Prurigo Nodularis Therapeutics Market Trends and Insights

Regulatory Tailwinds for Orphan & Rare-Disease Biologics (US & EU)

Accelerated pathways and rare-disease incentives are compressing time from submission to launch for therapies that address severe pruritus and refractory lesions. Nemolizumab’s U.S. priority review approval in February 2024 showcased how priority review can move efficacious biologics to market on faster timelines for adult patients who had limited systemic options[1]U.S. Food and Drug Administration, “FDA Approves First Treatment for Adults with Prurigo Nodularis". U.K. authorization in February 2025 reinforced the trend of cross-border regulatory convergence that now supports earlier clinician familiarity and coordinated payer reviews. These precedents clarify approvability criteria rooted in clinically meaningful itch reduction and physician assessment scales, which benefit agents that target upstream cytokine signaling. Sponsors also gain economic benefits through fee waivers and exclusivity windows, which improve the risk-adjusted return profiles of late-stage assets in the prurigo nodularis therapeutics market. As more dossiers leverage consistent endpoints and robust patient-reported outcomes, submission quality rises, and review cycles become more predictable for follow-on mechanisms.

Rapid Expansion of Tele-Dermatology & E-Pharmacy Fulfillment

Synchronous and asynchronous teledermatology is expanding specialist reach by triaging routine follow-ups and image-based consultations outside crowded clinics. Peer-reviewed work demonstrates that store-and-forward workflows can lower in-person demand and modestly reduce acute care visits in underserved communities, which preserves capacity for systemic initiation and monitoring. Specialty pharmacy networks supply home delivery of prefilled injectors and align with virtual education models, which improve adherence and support stable persistence for injectable biologics. Autoinjector formats also reduce per-dose administration costs compared with clinic-based injections, which aligns payer incentives with home-care use in the prurigo nodularis therapeutics market. As clinics implement tele-triage and remote documentation for adherence, dermatology teams can allocate in-person time to complex flares and comorbidities. This integrated model enables consistent follow-up for patients who live far from specialist centers, which stabilizes chronic-care workflows around targeted biologics and late-stage small molecules.

IL-31 / OSM Pathway Breakthroughs Accelerating Novel MoA Pipeline

Validation of IL-31 receptor alpha has spurred work across adjacent signaling hubs, including OSMRβ and downstream JAK-STAT cascades. A growing body of peer-reviewed literature maps neuroimmune circuits that link pruritus, inflammation, and tissue remodeling, which supports the rationale for agents that interrupt both itch and fibrotic pathways. Clinical programs for oral and injectable candidates are refining dose regimens and endpoint hierarchies around itch scores and investigator assessments, which is improving comparability across readouts. Developers are also designing studies that target defined phenotypes, such as atopic versus non-atopic forms, to improve signal detection within heterogeneous cohorts. As head-to-head and add-on studies emerge against approved biologics, evidence on durability and lesion clearance should become more granular, which informs positioning within the prurigo nodularis therapeutics market.

Rise of Patient-Advocacy Rare-Disease Registries Speeding Clinical Trial Enrollment

Patient registries run by advocacy groups and academic centers are accelerating trial activation and screening by consolidating consented data and biosamples. These infrastructures create virtual channels for outreach and prequalification, which shortens the time to enroll moderate-to-severe patients who meet strict inclusion criteria. Registry-linked sites also improve longitudinal data capture and facilitate transition from trials to post-approval follow-up, which strengthens real-world evidence packages. As investigators coordinate across networks, multi-center studies can scale without duplicating intake processes, which reduces friction that slows rare-disease research. The net effect is faster validation of promising mechanisms and more robust safety datasets, which supports a steadier launch sequence for high-need indications within the prurigo nodularis therapeutics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High biologic therapy cost & payer utilisation controls | -1.3% | Global, most acute in North America | Short term (≤ 2 years) |

| Limited dermatology capacity in public health systems (APAC, Africa) | -0.7% | APAC, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Heterogeneous disease phenotypes complicate endpoint standardisation in trials | -0.4% | Global, regulatory impact in US & EU | Long term (≥ 4 years) |

| Supply-chain fragility for biologic fill-finish capacity | -0.5% | Global, spill-over from North America to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Biologic Therapy Cost & Payer Utilization Controls

Biologic list prices and site-of-care costs continue to draw intense scrutiny, which sustains step-therapy and prior authorization requirements that delay treatment starts. Medicare Part B reimbursement mechanics use average sales price formulas that adjust with a lag, which can pressure provider economics for buy-and-bill launches. Federal analyses and policy discussions on biosimilars aim to reduce spending while maintaining access, which creates uncertainty for innovators that rely on stable margins to fund follow-on research. Payer controls also vary across plan types, which means that the same patient profile can experience different access pathways depending on coverage. These factors can slow uptake novel biologics and shift more care to home-based self-administration, where payers seek lower total costs. The prurigo nodularis therapeutics market continues to navigate these constraints by expanding patient support programs and by aligning delivery models to plan preferences.

Heterogeneous Disease Phenotypes Complicate Endpoint Standardization in Trials

Prurigo nodularis shows wide variation in lesion burden and immune pathway activation, which complicates fixed primary endpoints across global trials. Transcriptomic analyses have documented subgroup differences that shape cytokine profiles and may influence response to targeted mechanisms. These findings reinforce the need to stratify by atopic status and disease chronicity when interpreting itch reduction and lesion clearance. Sponsors must power studies to detect changes across diverse cohorts, which extends recruitment and raises development costs. Aligning patient-reported outcomes with objective clearance metrics also remains a design challenge, since improvements in itch can outpace skin resolution in some regimens. As endpoint conventions mature, developers can refine hierarchy and responder definitions that reflect both symptom relief and visible lesion change within the prurigo nodularis therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Redefine the Care Pathway While Orals Build Optionality

Biologics captured 45.34% of the prurigo nodularis therapeutics market in 2025, and the prurigo nodularis therapeutics market size for biologics is projected to expand at a 7.49% CAGR through 2031. Targeting upstream cytokines has improved itch control and disease management compared with symptomatic regimens, which is why dermatology clinics are transitioning moderate-to-severe patients to IL-31RA and IL-4/IL-13 blockade once initial measures fall short. Nemolizumab’s approval brought a distinct IL-31 mechanism into routine practice and created clear sequencing options alongside an established IL-4/IL-13 biologic. Topical corticosteroids and other local therapies remain a first step in mild presentations, but they function mainly as adjuncts once systemic therapy begins for refractory itch and persistent nodules. Antihistamines have limited utility because non-histaminergic circuits drive itch signaling in this disease, which keeps them peripheral to control strategies for severe cases.

Small-molecule programs are advancing to offer alternatives for patients who prefer oral routes or who face injection barriers. Oral agents that modulate JAK-STAT signaling are designed to intercept downstream pathways activated by multiple cytokines, which could broaden responsiveness across phenotypes. Published reviews highlight that dose optimization and safety monitoring are central to long-term use as these agents mature through late-stage trials[2]Matteo Bianco et al., “New and Emerging Biologics and JAK Inhibitors for the Treatment of Prurigo Nodularis: A Narrative Review". As evidence accumulates, clinicians are considering combination strategies that pair systemic agents with targeted topical care to enhance clearance and lower flare risk. The prurigo nodularis therapeutics market is therefore organizing around a biologics-led core with oral entrants providing greater choice on delivery, which supports adherence patterns that suit patient preferences and payer policies.

By Route of Administration: Subcutaneous Dominance Meets Rising Home-Based Care

Subcutaneous and intramuscular injection accounted for 45.80% of the prurigo nodularis therapeutics market in 2025, and the prurigo nodularis therapeutics market size for injectables is set to grow at a 4.77% CAGR to 2031. Every two to four weeks, dosing fits established specialty workflows and aligns with home-delivery infrastructure that supports disease-modifying biologics. Prefilled autoinjector pens for nemolizumab enable reliable self-administration without routine in-clinic supervision, which lowers per-dose administration costs and reduces travel burdens for patients. This shift toward home settings complements virtual check-ins and remote documentation of adherence, which streamlines payer audits and clinic throughput. Oral routes are also poised to expand as late-stage data clarifies durability and safety in populations that remain injection-averse.

Topicals continue to play a supportive role across disease stages by managing localized inflammation and serving as bridge therapy during access steps for systemic stages. Intravenous infusion remains limited in this indication because current leading agents are formulated for subcutaneous use, which reduces time in infusion suites. As more sites migrate to remote training and support, home-based injection should take a larger share of delivery, provided that usability and persistence remain high for autoinjectors. The prurigo nodularis therapeutics market reflects these delivery shifts by dispersing care across patient homes, specialty pharmacies, and fewer in-person follow-ups for stable regimens, which supports broad access across urban and rural populations.

By End-User Setting: Specialty Clinics Anchor Initiation While Home-Care Scales

Specialty dermatology clinics held 53.23% of the prurigo nodularis therapeutics market in 2025 due to the complexity of systemic initiation, education on injection technique, and safety monitoring protocols. These clinics coordinate baseline labs and ongoing assessments that are essential for safe biologic use, which concentrates new starts and persistence programs within specialist settings. Hospital outpatient departments manage acute flares and complications but face cost barriers for routine visits that are often unnecessary once patients are stable. Home-care and self-administration are the fastest-growing segments at a 4.90% CAGR, and the prurigo nodularis therapeutics market size in home-based care is expected to increase as payers favor lower-cost delivery and patients embrace the convenience of at-home dosing. Press materials show usability data for autoinjectors that support high rates of successful self-injection, which reduces the need for repeated in-clinic instruction.

Connected education by specialty pharmacies, which includes nurse coaching and virtual refreshers, supports adherence and decreases the administrative burden on clinics. Rare adverse events, including eczematous flares in select cases, underscore the importance of structured follow-up and rapid access to specialist advice, which home-based models can accommodate through teleconsults when needed. As remote training and documentation mature, more patients can maintain long-term therapy without frequent in-person visits. The prurigo nodularis therapeutics market, therefore, balances specialist-led starts with decentralized maintenance, which supports steady volume growth while protecting clinic capacity for complex cases.

Geography Analysis

North America accounted for 42.11% of the prurigo nodularis therapeutics market in 2025, reflecting mature specialty pharmacy systems and broad clinician familiarity with targeted immunology agents. U.S. coverage for nemolizumab advanced rapidly, with first-line biologic access extending to a substantial share of commercially insured lives soon after launch, which reinforced early momentum in the prurigo nodularis therapeutics market. Canada contributes a smaller base due to provincial variations in formulary timing, which can space out access milestones after federal authorization.

Across Western Europe, dermatology networks are integrating new biologics as national-level assessments advance, and the U.K. authorization in early 2025 helped catalyze earlier clinician adoption[3]Medicines and Healthcare products Regulatory Agency, “Nemolizumab Approved to Treat Prurigo Nodularis and Atopic Dermatitis (Eczema) for Patients in the UK". Germany and the Nordics have experience scaling targeted biologics across immune-mediated diseases, which can help absorb prurigo nodularis starts once budget processes conclude. Southern European markets proceed more gradually due to regional decision layers and local budget constraints, though specialist centers often become early adopters. As teledermatology programs expand, clinics can reserve in-person capacity for systemic starts and complex comorbidity management, which supports stable use patterns in the prurigo nodularis therapeutics market.

Asia-Pacific is expected to post the fastest growth at a 5.24% CAGR, supported by targeted launches and scaling teledermatology that helps extend specialist reach to underserved areas. Australia’s regulatory clearance in 2025 created a path for commercial rollout that can accelerate once funding decisions align with clinical practice. Japan has deep experience with biologics for inflammatory conditions, and the presence of the original developer in that market supports clinician education and patient onboarding. The Middle East & Africa and South America remain early in adoption due to capacity and reimbursement constraints, though selected private centers are building capability to manage biologic regimens. As supply chains for cold-chain delivery expand and home-based support normalizes, regional gaps in access should narrow within the prurigo nodularis therapeutics market.

Competitive Landscape

Competition in the prurigo nodularis therapeutics market centers on mechanism and durability rather than price, since payers manage all biologics under similar utilization policies. Two approved systemic agents anchor current practice, and late-stage candidates are working to differentiate on lesion clearance, onset, and sustained itch reduction. Field execution has become a lever for speed, with dermatology-focused teams offering streamlined prior-authorization support, benefits verification, and patient onboarding to reduce clinic workload. Company materials show strong early U.S. coverage for nemolizumab, which helped accelerate in-therapy growth within the prurigo nodularis therapeutics market.

Investment in investigator networks and translational research is also shaping share capture. A 2025 funding commitment by a leading biologics partnership to support academic work on type 2 inflammation signals ongoing engagement with dermatology thought leaders, which can yield faster dissemination of best practices across clinics. Manufacturing resiliency has become a strategic priority as demand for subcutaneous biologics scales. One leading dermatology company disclosed plans for expanded U.S. fill-finish and final assembly capacity to reduce supply risk and support sustained launch trajectories, which can protect continuity of care in the prurigo nodularis therapeutics market.

Looking ahead, differentiation will likely come from evidence on deep lesion clearance and stable long-term control rather than nominal changes in dosing intervals. Oral entrants that reach strong itch reduction with acceptable safety could broaden patient preference segments, especially for those who prefer to avoid injections. Partnerships with specialty pharmacies and home-care providers will remain critical to scale adherence support and remote documentation, which together can reduce friction for clinics and payers. As more post-approval evidence accumulates, real-world outcomes on persistence and healthcare utilization should inform clinical positioning and payer contracts across the prurigo nodularis therapeutics market.

Prurigo Nodularis Therapeutics Industry Leaders

Galderma SA

Incyte Corporation

Kiniksa Pharmaceuticals Ltd.

Pfizer Inc.

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: U.S. FDA approved nemolizumab for adults with prurigo nodularis after an expedited review supported by pivotal data on itch reduction and lesion outcomes.

- February 2025: The U.K. MHRA authorized nemolizumab for adult patients with prurigo nodularis, enabling prescriber use following national review.

- May 2025: Australia’s Therapeutic Goods Administration approved nemolizumab in prurigo nodularis, creating a pathway for commercial rollout pending funding alignment.

- April 2025: A leading biologics partnership funded multi-year awards for dermatology investigators focused on type 2 inflammation, including prurigo nodularis, to accelerate translational insights.

Global Prurigo Nodularis Therapeutics Market Report Scope

| Topical Corticosteroids |

| Capsaicin Cream |

| Antihistamines |

| Anticonvulsants |

| Antidepressants |

| NK-1 Receptor Antagonists |

| Biologics |

| Opiate Receptor Modulators |

| Others (Phototherapy, Cryotherapy, etc.) |

| Topical |

| Oral |

| Subcutaneous / Intramuscular Injection |

| Hospitals |

| Specialty Dermatology Clinics |

| Home-care / Self-administration |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Topical Corticosteroids | |

| Capsaicin Cream | ||

| Antihistamines | ||

| Anticonvulsants | ||

| Antidepressants | ||

| NK-1 Receptor Antagonists | ||

| Biologics | ||

| Opiate Receptor Modulators | ||

| Others (Phototherapy, Cryotherapy, etc.) | ||

| By Route of Administration | Topical | |

| Oral | ||

| Subcutaneous / Intramuscular Injection | ||

| By End-User Setting | Hospitals | |

| Specialty Dermatology Clinics | ||

| Home-care / Self-administration | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the prurigo nodularis therapeutics market?

The prurigo nodularis therapeutics market size reached USD 2.16 billion in 2026 and is projected to reach USD 2.64 billion by 2031 at a 4.08% CAGR, supported by targeted biologics and expanding home-based care.

Which treatment class leads usage within prurigo nodularis?

Biologics led with 45.34% share in 2025 and are forecast to grow at 7.49% CAGR, driven by uptake of IL-31RA and IL-4/IL-13 mechanisms and broader access in specialist pathways.

How is care delivery evolving for prurigo nodularis?

Subcutaneous injections remain the core route at 45.80% share in 2025, while home-care and self-administration is the fastest-growing setting at 4.90% CAGR as payers favor lower-cost delivery and patients opt for at-home dosing.

Which regions show the strongest momentum?

North America accounted for 42.11% in 2025 on faster access and specialty infrastructure, while Asia-Pacific is expected to post the highest growth at 5.24% CAGR through 2031 as launches and teledermatology scale.

What are the main constraints to faster adoption?

High biologic costs and payer controls, along with heterogeneous disease phenotypes that complicate end points, continue to shape access and trial design, although regulatory and registry advances are easing some barriers.

Page last updated on: