Proliferative Vitreoretinopathy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

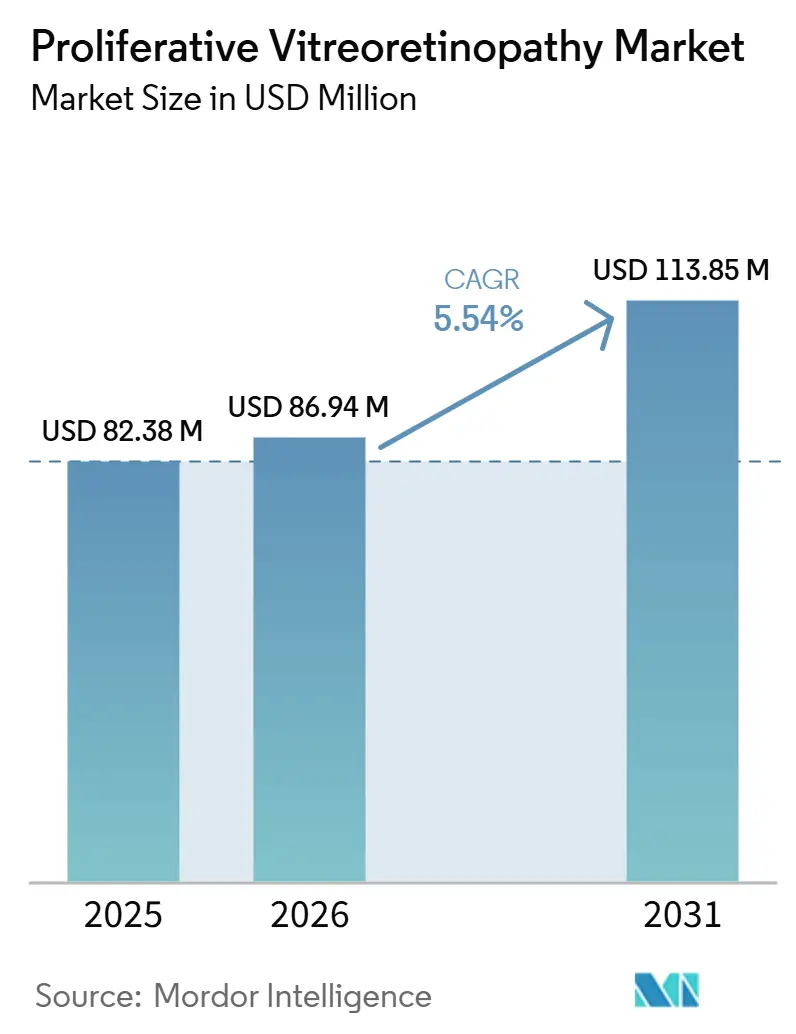

| Market Size (2026) | USD 86.94 Million |

| Market Size (2031) | USD 113.85 Million |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Proliferative Vitreoretinopathy Market Analysis by Mordor Intelligence

The Proliferative Vitreoretinopathy Market size is projected to expand from USD 82.38 million in 2025 and USD 86.94 million in 2026 to USD 113.85 million by 2031, registering a CAGR of 5.54% between 2026 to 2031.

The market remains supported by the persistent clinical burden of PVR, which affects 5% to 10% of primary rhegmatogenous retinal detachment cases and 25% to 50% of recurrent re-detachment surgeries, even though first-surgery anatomic success still sits near 75%. Each recurrent detachment creates additional demand for membrane peeling, tamponade agents, vitrectomy time, and post-operative follow-up, which keeps the proliferative vitreoretinopathy market active beyond the initial repair. The 2025 and 2026 launch cycle for faster cutters, improved fluidics, and better surgical visualization is also lifting revenue per case because hospitals continue to upgrade premium retinal systems. Aging populations and age-linked retinal pathology are widening the pool of patients who are most likely to progress to complex retinal surgery, which supports continued case volumes in both mature and expanding care systems. At the same time, the absence of an approved drug keeps surgery at the center of care, while a more active adjunct pipeline preserves medium-term commercial opportunity in the proliferative vitreoretinopathy market.

Key Report Takeaways

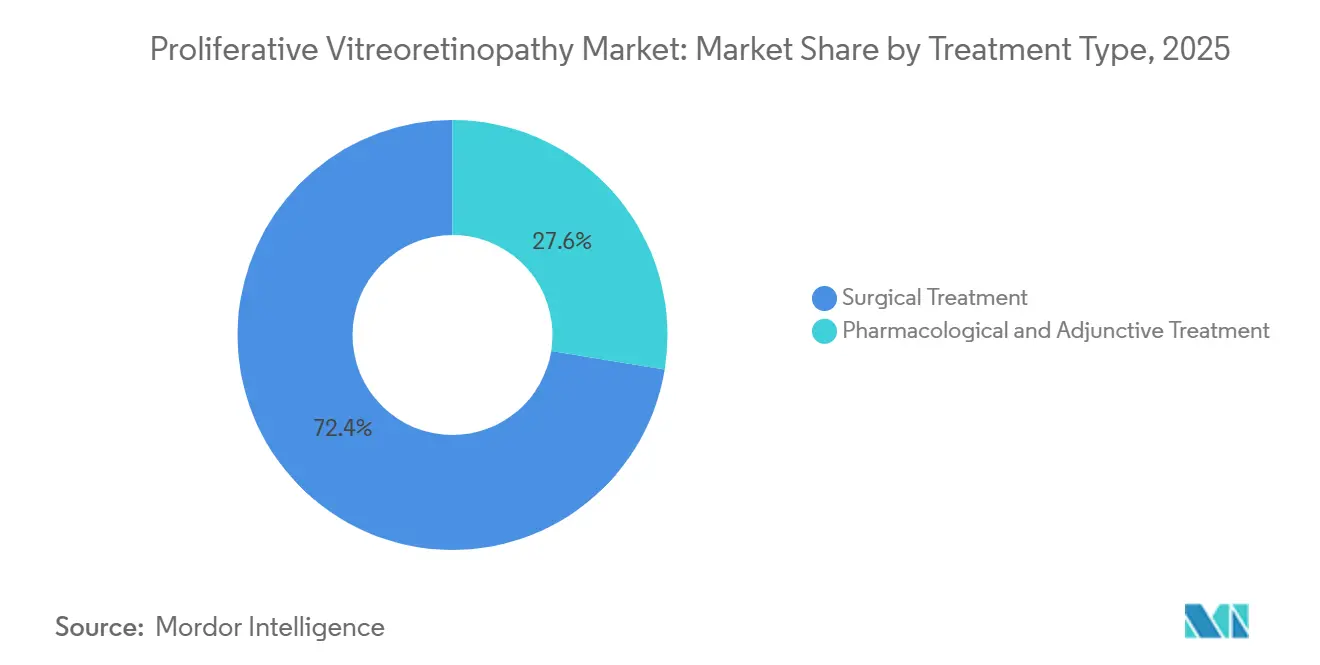

- By treatment type, surgical treatment held 72.43% of revenue in 2025, while pharmacological and adjunctive treatment are projected to expand at 9.23% CAGR through 2031 in the proliferative vitreoretinopathy market.

- By disease stage, grade C held 53.28% of revenue in 2025, while Grade A is projected to grow at 9.79% CAGR through 2031.

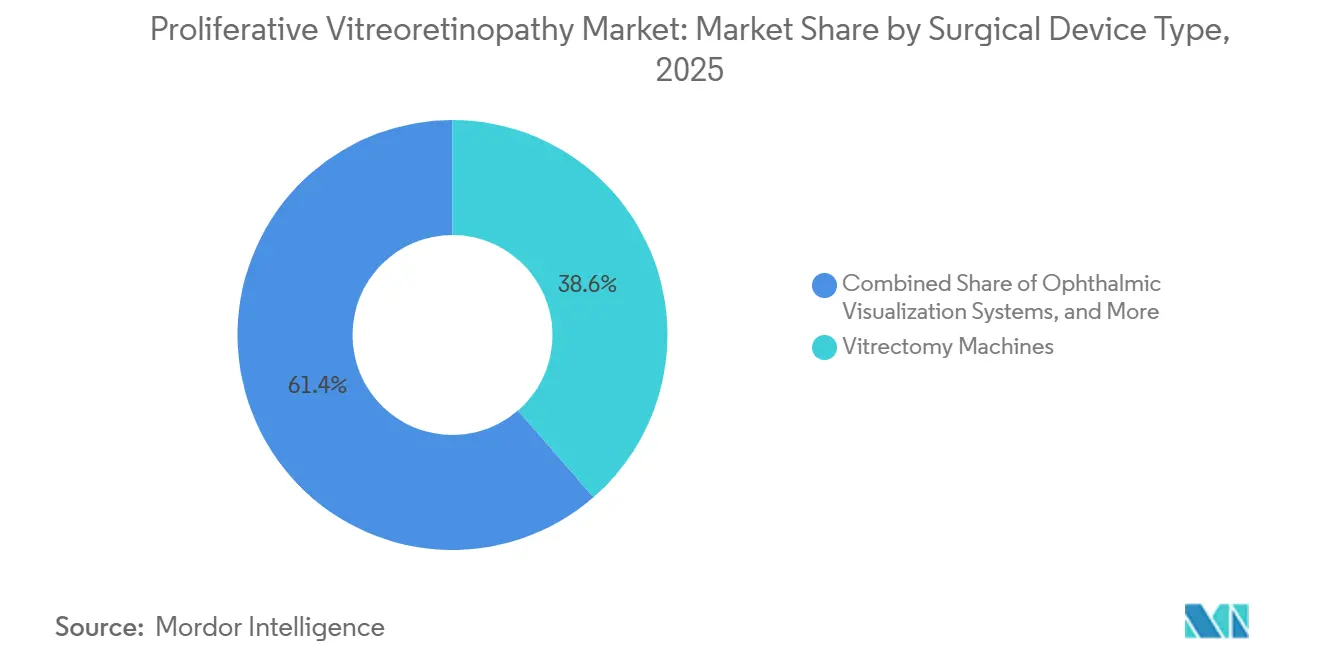

- By surgical device type, vitrectomy machines held 38.62% of revenue in 2025, while ophthalmic visualization systems are projected to expand at 10.43% CAGR through 2031 in the proliferative vitreoretinopathy market.

- By end user, hospitals held 47.38% of revenue in 2025, while specialty eye hospitals are projected to expand at 11.57% CAGR through 2031.

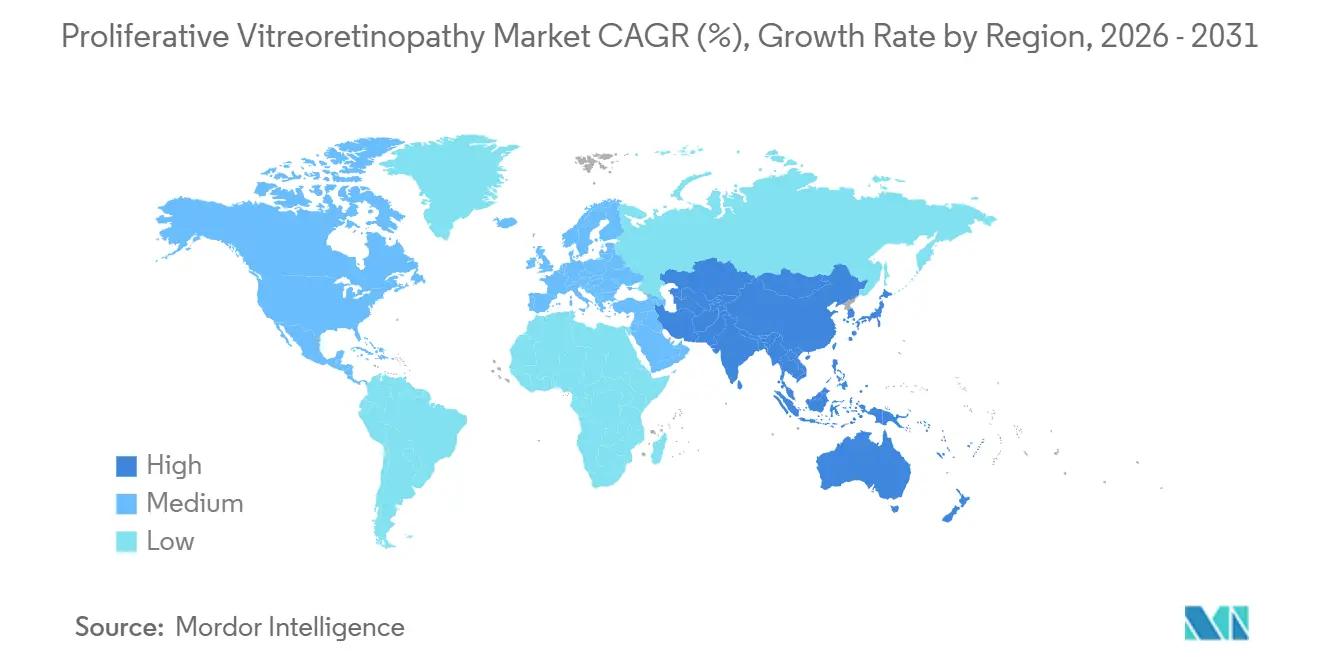

- By geography, North America commanded 38.64% of the proliferative vitreoretinopathy market share in 2025, whereas Asia-Pacific is projected to expand at a 12.38% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Proliferative Vitreoretinopathy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Rhegmatogenous Retinal Detachment Burden | +1.8% | Global, especially Europe and Asia-Pacific core | Short term (≤ 2 years) |

| Advanced Vitreoretinal Surgical Techniques | +1.6% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Aging Population and Retinal Pathology | +1.5% | Global, strongest in Japan, Germany, and Italy | Long term (≥ 4 years) |

| Anti-Fibrotic Adjunct and Combination Therapy Focus | +1.2% | North America and Europe | Medium term (2-4 years) |

| Retina Specialist Access and Referral Network Expansion | +0.8% | Asia-Pacific, Middle East and Africa, and South America | Long term (≥ 4 years) |

| Smaller-Gauge Vitrectomy and Visualization Uptake | +0.9% | North America, Europe, and early-adopter Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Rhegmatogenous Incidence Anchors PVR Procedural Pipeline

Germany’s nationwide data showed rhegmatogenous retinal detachment incidence rising to 24.8 per 100,000 by 2021 from 15.6 per 100,000 in 2005, which confirms that the upstream case pool for complex retinal repair is still growing.[1]“The Rising Tide of Rhegmatogenous Retinal Detachment in Germany, a Nationwide Analysis of the Incidence, From 2005 to 2021,” Graefe’s Archive for Clinical and Experimental Ophthalmology, The share of detachment cases that progress to PVR has remained near 5% to 10%, so absolute PVR volumes increase as detachment volumes increase, even when surgical methods improve.[2]“Atualizações na Prevenção e Tratamento da Vitreorretinopatia Proliferativa,” This matters for the proliferative vitreoretinopathy market because demand is tied to a failure pattern that has not been eliminated by surgical refinement. Myopia continues to sit upstream of this burden, which keeps future case expansion linked to long-duration refractive disease trends rather than only to acute surgical capacity. The result is a durable procedural base for the proliferative vitreoretinopathy market, especially in regions where aging and myopia are moving in the same direction. Hospitals and tertiary retina centers, therefore, continue to treat PVR as a recurring service line rather than as a shrinking surgical complication.

Advanced Vitreoretinal Platforms Reshaping Surgical Standard of Care

The current product cycle remains unusually active, with Alcon’s UNITY VCS moving through commercial rollout with the HYPERVIT 30K probe and upgraded fluidics architecture.[3]“Alcon Elevates Vitreoretinal and Cataract Surgery with UNITY VCS and UNITY CS,” Bausch + Lomb’s Bi-Blade+ dual-port vitrectomy cutter adds another high-specification option with 25,000 cuts per minute and a reported 62% reduction in cutter vibration, which is directly relevant in delicate membrane work. These upgrades improve control, visibility, and workflow efficiency in the operating room, but they do not remove the clinical judgment required in severe PVR surgery. That dynamic supports the proliferative vitreoretinopathy market by raising the revenue value of each procedure without removing the need for repeat intervention in difficult cases. It also sustains a device replacement cycle that benefits premium platform vendors across installed base accounts. As more facilities invest in integrated systems, the proliferative vitreoretinopathy market keeps shifting toward bundled purchases rather than stand-alone instrument decisions.

Aging Population Expands PVR-Eligible Surgical Pool

The global number of vision-impaired people aged 70 and older reached 242 million in 2021, up 156% from 1990, which shows how strongly ophthalmic demand is being shaped by older age groups. Posterior vitreous detachment, which often precedes retinal detachment, peaks in the sixth and seventh decades, so the aging curve feeds directly into a larger surgical candidate pool for the proliferative vitreoretinopathy market. Older patients also present more often with pseudophakic retinal detachment and more advanced disease, which pushes cases toward longer surgery times and higher use of consumables. That pattern improves the revenue mix of the proliferative vitreoretinopathy market, because complex repairs use more specialized tools and support services than routine retinal detachment procedures. The effect is strongest in older societies such as Japan and Germany, where premium microscope and visualization suppliers are already active.[4]“ZEISS Announces NMPA Approval for ZEISS ARTEVO 750 and ZEISS ARTEVO 850,” Facilities are also placing more value on integrated visualization and intraoperative documentation, which fits the needs of older and more complex case profiles.

Anti-Fibrotic Pipeline Redefining Pharmacological Adjunct Strategy

No drug holds regulatory approval for PVR treatment or prevention in 2026, but the clinical pipeline is more active than it was in prior periods. Methotrexate remains the most advanced named mechanism in the current discussion set, and Aldeyra’s ADX-2191 received an FDA Special Protocol Assessment agreement in June 2025 for a pivotal pathway, which keeps investor and clinician attention on adjunct options. Parallel trial activity in prevention settings is also keeping the pharmacological strategy visible within the proliferative vitreoretinopathy market. If even one adjunct reaches approval, it would create a new revenue layer on top of the existing surgical base rather than replacing surgery outright. Until that happens, the proliferative vitreoretinopathy market continues to depend on procedural care while hospitals and sponsors watch the trial pipeline closely. This setup keeps pharmacology strategically important even though it is not yet commercially established.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Approved Pharmacological Treatment | -1.8% | Global | Long term (≥ 4 years) |

| High Recurrence Risk and Uneven Visual Outcomes | -1.5% | Global, stronger in low-resource settings | Medium term (2-4 years) |

| Procedure Complexity and Retina Surgeon Dependence | -1.3% | Middle East and Africa, South America, and peripheral Asia-Pacific | Long term (≥ 4 years) |

| Delayed Diagnosis and Under-Referral in Emerging Markets | -1.0% | Africa, South Asia, rural Asia-Pacific, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Absence of Approved Pharmacological Therapy Narrows Treatment Options

No FDA, EMA, or other major regulatory approval exists for a PVR drug in 2026, which leaves surgery as the only established route of care. A systematic review covering 27 randomized controlled trials and 3,375 patients found that commonly tested pharmacological approaches did not deliver reproducible clinical benefit in large studies. That evidence gap keeps the proliferative vitreoretinopathy market dependent on repeat mechanical intervention, including vitrectomy, silicone oil tamponade, and membrane peeling. Patient heterogeneity also complicates product development, because preoperative PVR grade remains a strong predictor of post-surgical failure and makes clean trial stratification difficult. This slows commercial entry for would-be adjunct therapies even when the unmet need is obvious. As a result, the proliferative vitreoretinopathy market carries high clinical demand but a still-unproven drug pathway.

Recurrence Dynamics Create Clinical and Economic Friction

Established PVR still delivers only around 75% anatomic success after surgery, which means 1 in 4 patients may need further intervention. This recurrence pattern supports procedure volume, but it also makes outcomes less predictable for payers, providers, and patients. Grade C disease is especially difficult because anatomical repair does not always translate into useful visual recovery, which reduces confidence in the overall value of repeated intervention. Procurement teams are therefore likely to judge new equipment more tightly on cost per outcome instead of only on technical specification. That pressure can slow premium purchasing when device upgrades do not clearly change recurrence or recovery. The proliferative vitreoretinopathy market still benefits from unavoidable retreatment demand, but it also faces constant scrutiny over whether added technology changes the real clinical result.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Pharmacological Pipeline Pressures Surgical Dominance

Surgical treatment accounted for 72.43% of revenue in 2025, which made it the largest contributor to the proliferative vitreoretinopathy market size. This dominance reflects the fact that pars plana vitrectomy, membrane peeling, and tamponade remain the only interventions with established efficacy across the disease spectrum. Smaller-gauge surgery and better visualization have improved precision in the operating room, but they have not displaced the core surgical pathway. The revenue base of the proliferative vitreoretinopathy market, therefore, remains centered on procedures, devices, and recurring surgical consumables. Within the proliferative vitreoretinopathy industry, this makes the operating room the primary point of value capture.

Pharmacological and adjunctive treatment is projected to grow at 9.23% CAGR from 2026 to 2031, which makes it the fastest-growing treatment category in the user-supplied structure. That faster pace comes from trial activity and not from present-day commercial scale, which is an important distinction in this segment. Aldeyra’s ADX-2191 remains one of the clearest named assets in this space, with FDA Special Protocol Assessment support already on record for a pivotal pathway. Journal evidence also notes that PVR incidence has not materially declined despite surgical advances, which preserves the case for a pharmacological complement rather than a surgical substitute. That is why the proliferative vitreoretinopathy market can support strong attention to adjunct drugs even while surgery continues to hold the revenue lead.

By Disease Stage: Grade C Dominance Masks Upstream Intervention Opportunity

Grade C captured 53.28% of the proliferative vitreoretinopathy market share in 2025, which shows how heavily real-world treatment still concentrates in advanced disease. This pattern reflects delayed referral, limited specialist access, and the fact that many patients reach tertiary care only after the first retinal repair has already failed. Grade C cases usually require the most resource-intensive mix of membrane peeling, retinotomy, and silicone oil use, which makes them commercially important but clinically difficult. The proliferative vitreoretinopathy market gains revenue from that intensity, but it also inherits weaker efficiency because late-stage care consumes more resources per patient. Within the proliferative vitreoretinopathy industry, Grade C remains the segment where clinical need and economic burden are most concentrated.

Grade A is projected to grow at 9.79% CAGR through 2031, which makes it the fastest-growing disease stage in the segment framework. That change points to a stronger interest in identifying high-risk retinal detachment patients before aggressive scarring becomes established. A 2026 review identified laser flare photometry at a threshold of at least 15 photons/ms as a useful stratification tool for selecting patients at higher risk before clinically significant PVR develops. Grade B is also becoming more important because it sits near the point where academic centers consider adjunctive methotrexate protocols and tighter post-operative monitoring. Over time, the proliferative vitreoretinopathy market is likely to depend more on earlier identification and less on a purely rescue-oriented Grade C treatment model.

By Surgical Device Type: Visualization Systems Redefine Surgical Ergonomics

Vitrectomy machines held 38.62% of the surgical device segment in 2025, which kept them at the center of capital equipment spending for the proliferative vitreoretinopathy market. Their lead position reflects the essential role of fluidics control, cutting speed, and platform reliability in every complex PVR repair. The 2024 to 2026 upgrade cycle has strengthened this segment through launches from Alcon and DORC, with vendors competing on efficiency, stability, and system integration. Probes, tamponades, and other consumables also deepen the value of each installed base machine because they generate recurring revenue long after the initial sale. This keeps the proliferative vitreoretinopathy market tied not only to capital spending, but also to ongoing procedural throughput.

Ophthalmic visualization systems are projected to expand at 10.43% CAGR through 2031, which makes them the fastest-growing device sub-segment. ZEISS ARTEVO 750 and ARTEVO 850 gained NMPA approval in China in 2026, extending access to advanced digital visualization in one of the most important future retinal surgery markets. Heads-up 3D systems and better intraoperative imaging are becoming more valuable in membrane dissection because they can improve depth perception and reduce the risk of iatrogenic trauma in difficult cases. Facilities that commit to a visualization ecosystem often source companion machines and accessories from the same vendor, which expands wallet share across the care setting. In the proliferative vitreoretinopathy industry, that bundling effect strengthens large suppliers that can offer a complete retinal surgery stack rather than a single instrument.

By End User: Specialty Eye Hospitals Consolidate Complex PVR Cases

Hospitals accounted for 47.38% share of the proliferative vitreoretinopathy market size in 2025, which kept them as the largest end-user setting. Their position reflects the need for operating room infrastructure, anesthesia support, imaging, and post-operative care in complex grade C repair. General hospitals also remain the default site in countries where ambulatory retinal surgery capacity is limited or unevenly distributed. That institutional role supports a large share of the proliferative vitreoretinopathy market because difficult cases still need broad surgical backup and referral depth. It also means purchasing decisions often move through formal capital committees rather than individual physician preferences.

Specialty eye hospitals are projected to expand at 11.47% CAGR through 2031, the fastest pace among end-user groups. Their advantage comes from concentrated vitreoretinal expertise and a greater willingness to invest in premium retinal devices. MedPAC reported that ophthalmology held 25.8% of the U.S. ambulatory surgery center market in 2024, and outpatient volume is still rising, but PVR remains less transferable than cataract or routine retinal detachment because of its complexity. Silicone oil use, reoperation risk, and long procedure times all limit large-scale migration of PVR into generic ambulatory settings. This keeps growth in the proliferative vitreoretinopathy market concentrated in specialized centers rather than in broad outpatient expansion alone.

Geography Analysis

North America commanded 38.64% of the proliferative vitreoretinopathy market share in 2025, which made it the largest regional contributor. The United States remains the primary revenue center because it combines a high density of retinal surgeons, established reimbursement pathways, and early adoption of premium vitreoretinal technology. Massachusetts Eye and Ear is running both netarsudil and topotecan prevention studies, which keep the region closely connected to the next wave of adjunct treatment development. Canada received Health Canada approval for Alcon’s UNITY VCS in July 2026, which extends access to current-generation vitreoretinal platform technology across the region. Mexico remains a smaller revenue source, but its contribution improves as tertiary retinal care infrastructure expands in selected hospital systems.

Europe represents the second-largest regional block in the proliferative vitreoretinopathy market, supported by Germany, the UK, France, Italy, and Spain. Germany’s adjusted rhegmatogenous retinal detachment incidence reached 24.8 per 100,000 by 2021, which creates a steady downstream pool for PVR-related surgery. The UK and France remain important through tertiary referral concentration and specialist engagement in trial design, which keeps Europe relevant beyond its installed device base. Suppliers are also benefiting from high surgeon familiarity with premium visualization and vitrectomy systems across academic and large referral centers. EU MDR compliance is raising the barrier for smaller device entrants, which favors suppliers that already have the scale and regulatory capability to stay present in hospital tenders.

Asia-Pacific is forecast to expand at 12.38% CAGR through 2031, making it the fastest-growing region in the proliferative vitreoretinopathy market. China’s 2026 approvals for ZEISS ARTEVO 750 and ARTEVO 850, together with DORC’s 2025 ILM-Blue approval, show that premium retinal technologies are moving deeper into high-volume centers. Japan and South Korea add further demand through older populations and mature retinal surgery capacity, while consensus guidance from APVRS is helping align surgical practice across member markets. Middle East and Africa and South America remain smaller opportunities in the proliferative vitreoretinopathy market, with Brazil and Argentina standing out, but growth still depends on faster referral, earlier diagnosis, and a larger retina specialist base.

Competitive Landscape

The proliferative vitreoretinopathy market shows moderate concentration at the surgical device level, with Alcon, Bausch + Lomb, and Carl Zeiss Meditec, including DORC, holding the strongest technology positions across machines, visualization systems, and key consumables. No company appears to control the full field on its own in the user-supplied material, which keeps competition centered on platform performance, installed base relationships, and surgeon workflow preference. Large suppliers are also benefiting from their ability to serve multiple points in the retinal procedure chain instead of only one product niche. That matters in the proliferative vitreoretinopathy market because hospitals often prefer vendors that can cover machines, cutters, probes, visualization, and service support together. Regulatory complexity is reinforcing that structure, since suppliers with deeper quality systems are better placed to manage FDA, CE, and NMPA pathways than smaller challengers.

A clear strategic pattern in the 2025 and 2026 cycle is the convergence of cataract and vitreoretinal functionality into single platforms. Alcon has pushed UNITY VCS across multiple markets with a focus on speed, fluidics, and operating room efficiency, which strengthens its replacement case in premium accounts. Bausch + Lomb is expanding its retina offer through the Bi-Blade+ dual-port cutter, which gives the Stellaris Elite system a stronger performance story in delicate retinal work. BVI has positioned Virtuoso as a dual-function phaco-vitrectomy platform and backed that move with CE Mark progress and a major capital raise, which shows intent to compete more directly with incumbents. ZEISS is reinforcing its position through Chinese approvals and continued emphasis on digital and AI-supported retina workflows, which broadens its appeal in high-volume centers.

Proliferative Vitreoretinopathy Industry Leaders

AbbVie Inc.

Alcon Inc.

Bausch + Lomb Corporation

Carl Zeiss Meditec AG

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Alcon receives Health Canada approval for UNITY VCS. Health Canada cleared the UNITY Vitreoretinal Cataract System, making Canada the latest market to receive commercial access to the platform's HYPERVIT 30K probe and UNITY Intelligent Fluidics, with a commercial launch expected in early 2026.

- May 2026: Bausch + Lomb launches Bi-Blade+ in Europe. The dual-port vitrectomy cutter with 25,000 cuts per minute and 62% lower vibration than its predecessor was launched on the Stellaris Elite system across European markets following FDA 510(k) clearance in April 2026, strengthening Bausch + Lomb's retina portfolio.

- April 2026: BVI receives CE Mark under EU MDR for Virtuoso surgical platform. The dual-function phaco-vitrectomy platform achieved CE Mark under EU MDR, enabling commercial expansion into CE-accepting markets starting Q3 2026. The Virtuoso integrates IOP control, consistent energy delivery, and advanced vitreous cutting for both cataract and vitreoretinal use.

Global Proliferative Vitreoretinopathy Market Report Scope

As per the scope of the report, proliferative vitreoretinopathy (PVR) is a severe complication of retinal detachment characterized by the formation of fibrotic membranes on and beneath the retina. These membranes contract over time, causing retinal distortion, traction, and recurrent retinal detachment. PVR is primarily managed through vitreoretinal surgery, including vitrectomy, membrane peeling, and intraocular tamponade procedures. It remains one of the leading causes of failure after retinal detachment repair.

The proliferative vitreoretinopathy market is segmented by treatment type, disease stage, surgical device type, end user, and geography. By treatment type, the market is segmented into surgical treatment and pharmacological and adjunctive treatment. By disease stage, the market is segmented into grade A PVR, grade B PVR, and grade C PVR. By surgical device type, the market is segmented into vitrectomy machines, vitrectomy probes, intraocular tamponades, ophthalmic visualization systems, and others. By end user, the market is segmented into hospitals, specialty eye hospitals, ambulatory surgery centers, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Surgical Treatment |

| Pharmacological and Adjunctive Treatment |

| Grade A PVR |

| Grade B PVR |

| Grade C PVR |

| Vitrectomy Machines |

| Vitrectomy Probes |

| Intraocular Tamponades |

| Ophthalmic Visualization Systems |

| Others |

| Hospitals |

| Specialty Eye Hospitals |

| Ambulatory Surgery Center |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Surgical Treatment | |

| Pharmacological and Adjunctive Treatment | ||

| By Disease Stage | Grade A PVR | |

| Grade B PVR | ||

| Grade C PVR | ||

| By Surgical Device Type | Vitrectomy Machines | |

| Vitrectomy Probes | ||

| Intraocular Tamponades | ||

| Ophthalmic Visualization Systems | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Eye Hospitals | ||

| Ambulatory Surgery Center | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of proliferative vitreoretinopathy by 2031?

The proliferative vitreoretinopathy market is forecast to reach USD 113.85 million by 2031 from USD 86.94 million in 2026, growing at 5.54% CAGR.

Why does surgery still account for most revenue in proliferative vitreoretinopathy?

Surgery remains dominant because no approved drug exists for treatment or prevention, and surgical treatment held 72.43% of revenue in 2025.

Which disease stage contributes the most to current demand?

Grade C is the largest disease stage, with 53.28% share in 2025, because many patients still reach tertiary care after disease progression or failed primary repair.

Which device category is growing fastest in retinal PVR procedures?

Ophthalmic visualization systems are the fastest-growing device segment, with a projected 10.43% CAGR through 2031, supported by digital microscope and heads-up surgery adoption.

Which region is growing fastest for proliferative vitreoretinopathy care?

Asia-Pacific is expanding the fastest at 12.38% CAGR through 2031, supported by premium device approvals, growing specialty eye infrastructure, and a larger future case pool.

Page last updated on: