Professional Coffee Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

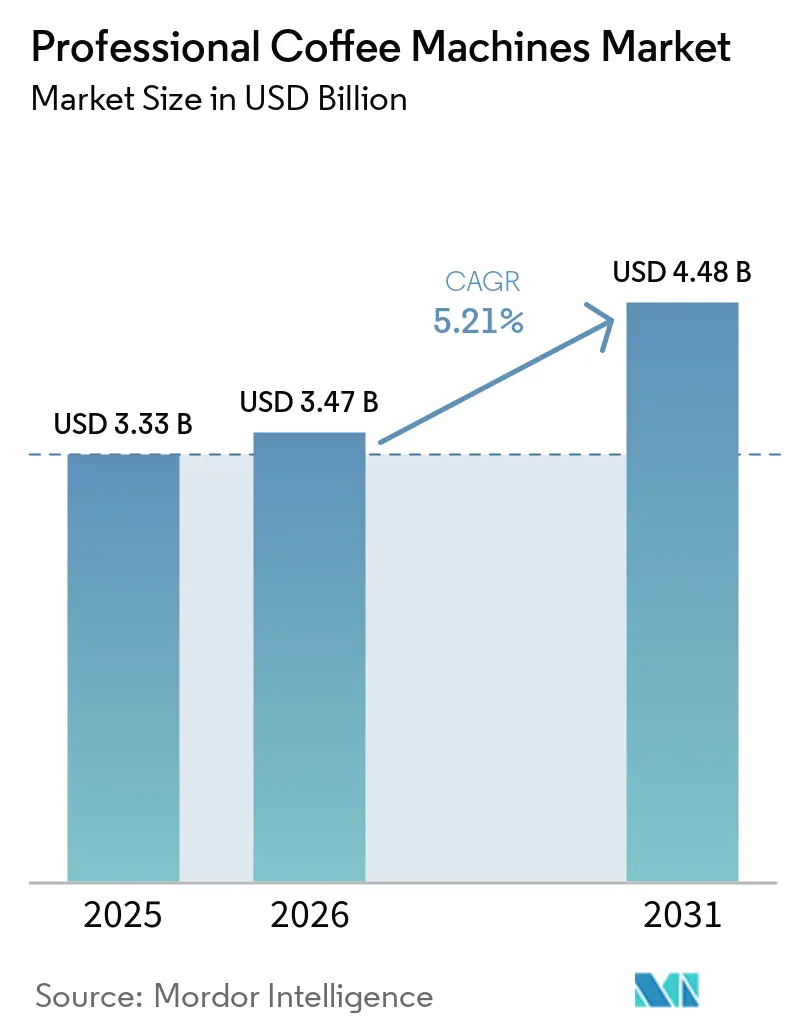

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 4.48 Billion |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

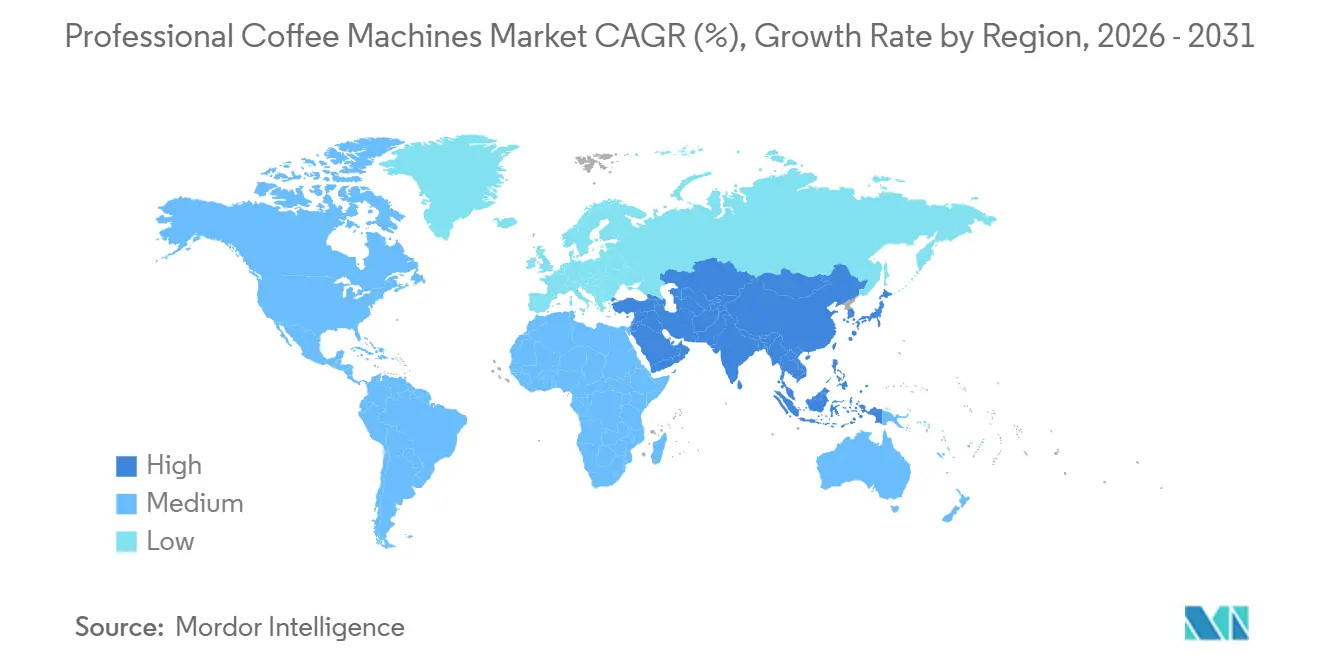

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

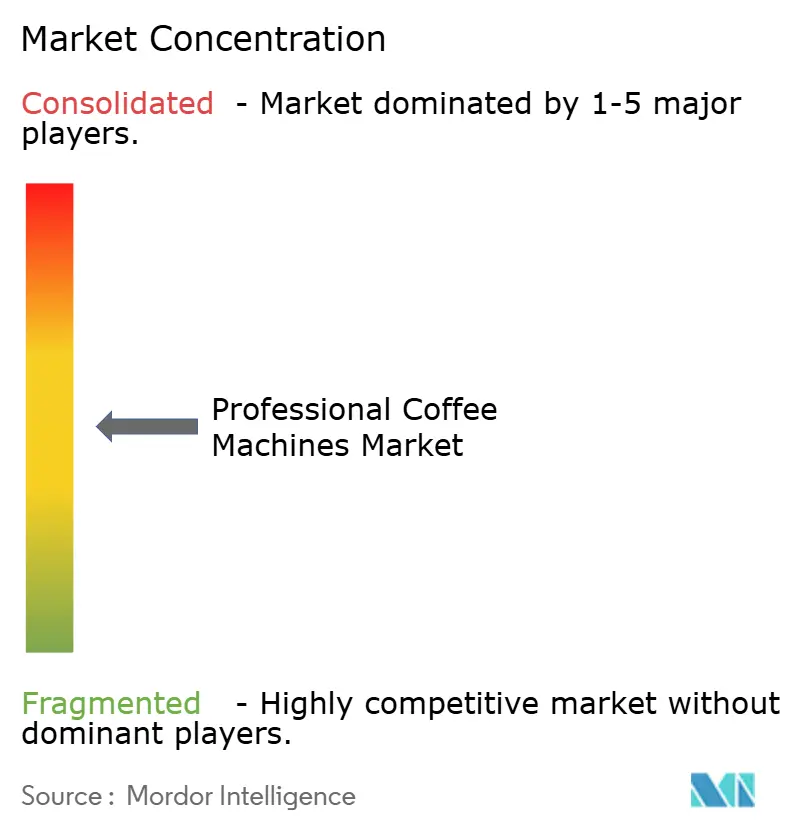

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Professional Coffee Machines Market Analysis by Mordor Intelligence

The global professional coffee machines market size stood at USD 3.47 billion in 2026, up from USD 3.33 billion in 2025, and is projected to reach USD 4.48 billion by 2031 at an 5.21% CAGR. Momentum strengthened from the 2024 to 2025 period as hybrid work patterns stabilized and investment cycles lengthened for premium bean-to-cup installations. Buyers favored modular platforms that integrate telemetry, automated cleaning functions, and milk systems designed for dairy and plant-based options. These capabilities address uptime, consistency, and labor-savings goals that traditional semi-automatic espresso formats struggle to match at scale. Divergence by segment and region remains pronounced, with Europe maintaining a lead in installed base and Asia-Pacific growing faster as QSR formats scale and office environments modernize.

Key Report Takeaways

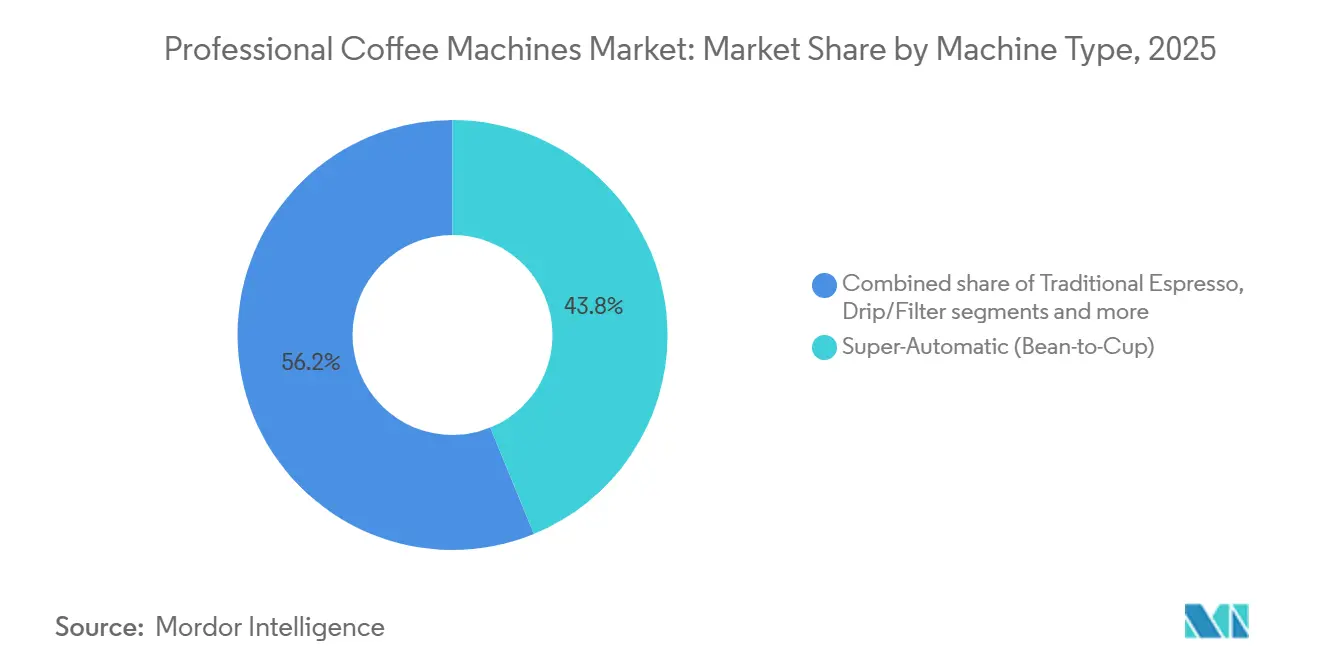

- By machine type, super-automatic bean-to-cup systems led with 43.82% of the global professional coffee machines market share in 2025 and are projected to grow at a 5.92% CAGR to 2031.

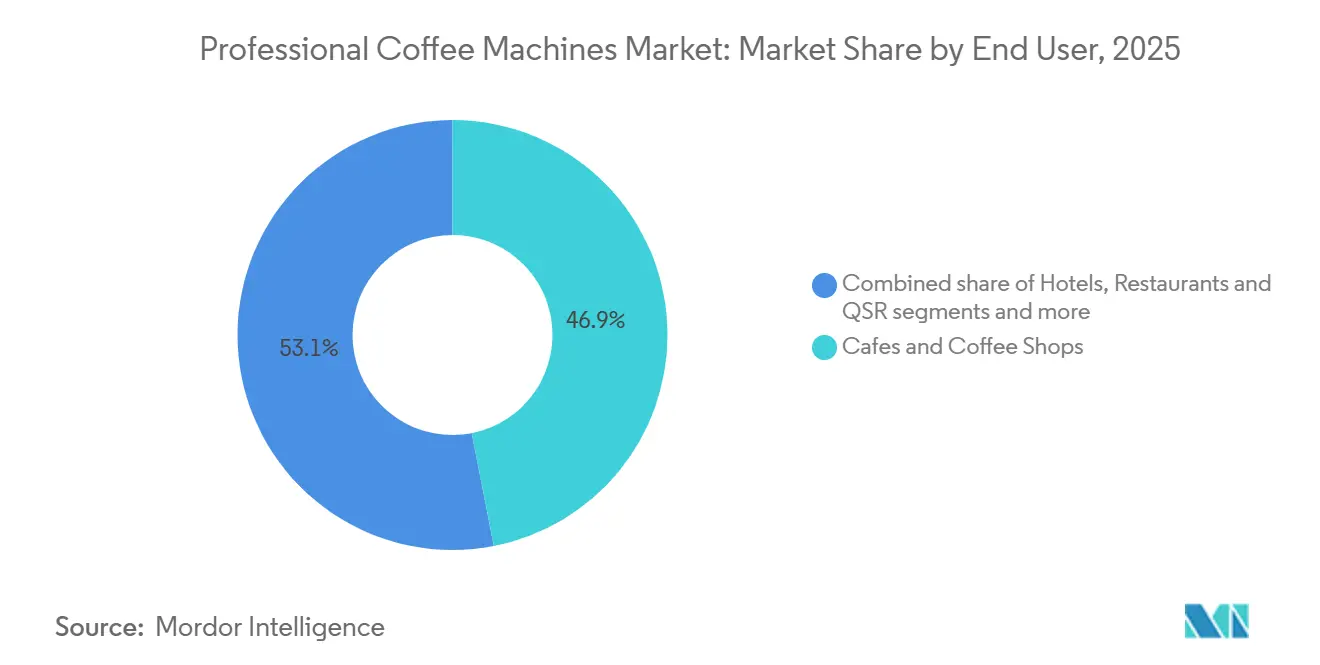

- By end user, cafes and coffee shops held 46.92% of the global professional coffee machines market share in 2025 and are projected to expand at a 5.81% CAGR through 2031.

- By distribution channel, authorized distributors and dealers accounted for 35.62% of the global professional coffee machines market share in 2025, while office coffee service providers recorded the highest projected CAGR at 5.66% through 2031.

- By geography, Europe retained the largest share at 34.24% of the global professional coffee machines market in 2025, and Asia-Pacific recorded the fastest projected CAGR at 6.13% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Professional Coffee Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of specialty cafes and QSR coffee programs | +1.2% | Global, with spill-over gains in North America drive-through formats and Asia-Pacific quick-service chains | Medium term (2-4 years) |

| Shift to super-automatic bean-to-cup to mitigate barista shortages and ensure consistency | +1.8% | North America, Western Europe, and urban Asia-Pacific hubs are facing tight labor markets | Medium term (2-4 years) |

| Premiumization of office coffee service and amenity-driven return-to-office | +0.9% | North America and Europe core, with early signals in Asia-Pacific tier-one cities | Short term (≤ 2 years) |

| Telemetry/IoT connectivity enabling fleet uptime, recipe control, and predictive maintenance | +0.7% | Global, led by multi-location operators in North America and Europe, has a slower uptake in fragmented Asia-Pacific markets | Long term (≥ 4 years) |

| Self-serve premium coffee rollouts in convenience retail and micro-markets | +0.5% | North America's convenience networks and urban Europe travel hubs | Medium term (2-4 years) |

| ESG- and hygiene-driven replacement, including low-standby energy and automated cleaning | +0.4% | Western Europe leading on EU PPWR compliance, North America lagging but accelerating post-2026 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Specialty Cafes and QSR Coffee Programs Fuels Equipment Demand

Drive-thru concepts in the United States have added scale and shifted equipment preferences toward high-throughput automated systems that maintain beverage quality under heavy morning peaks. 7 Brew, for example, expanded to more than 500 locations by October 2025 and increased its visit share to 3.8% in the U.S. coffee category by the third quarter of 2025, up from 0.1% in the first quarter of 2020[1]NACS https://www.convenience.org/Media/Daily/2026/January/5/4-Drive-Thru-Coffee-Chains-Expand_Research. Dutch Bros increased its visit share from 4.1% to 9.3% over the same period, reinforcing the focus on speed, consistency, and modular designs that integrate digital ordering and telemetry. In Asia-Pacific, multinational QSR chains entering India and Southeast Asia are adopting automated platforms with multilingual interfaces and centralized recipe control, enabling uniform execution of menus across their franchise portfolios. Manufacturers with connectivity stacks and service ecosystems benefit because chains increasingly tie equipment performance to uptime metrics and remote management capabilities. The global professional coffee machines market reflects these preferences, as operational throughput and repeatable quality become decisive purchase criteria for chains that process hundreds of transactions daily.

Super-Automatic Bean-to-Cup Platforms Address Persistent Labor Shortages

Operators continue to view staffing constraints and skill variability as critical risks to beverage quality and service times in multi-unit environments. Fully automatic bean-to-cup systems deliver programmable recipes and automated milk texturing that reduce the training burden for new hires and help retain service standards across locations. Post-2020 shifts in Australia and New Zealand showed how automation moved from convenience to necessity, with Übermilk ONE’s automatic milk solution helping shops maintain volume and quality amid staffing pressures. In North America, feature-rich systems that streamline milk and cleaning routines reduce waste and errors while simplifying daily workflows in busy dayparts. Company product data shows that on-demand grinding and optimized brewing cycles can meaningfully cut coffee and water waste, which compounds across fleets as operators scale. As a result, the global professional coffee machines market is realigning investment toward super-automatic platforms that maintain service continuity and beverage uniformity across dispersed operations.

Office Coffee Service Premiumization Accelerates Return-to-Office Strategies

Workplace strategies in 2026 position high-quality coffee programs as a core amenity to encourage office attendance and support employee well-being in hybrid models. Gallup tracking shows that 52% of the United States employees in remote-capable jobs were following hybrid schedules by early 2026, a stable foundation for amenity investments that emphasize the in-office experience. Corporate buyers respond by upgrading from drip brewers and pods to automated espresso platforms with fresh milk systems and specialty menus that emulate third-wave cafes inside the office. OCS providers increasingly lead with subscription models that bundle equipment, consumables, telemetry, and preventive maintenance, which reduces up-front capex exposure for mid-market clients. The global professional coffee machines market benefits from this shift because high-spec office installations rely on platform-level connectivity and service guarantees that align with building standards and HR objectives. As hybrid norms settle, OCS deployments focus on uptime, volume flexibility, and menu variety to sustain employee engagement across variable attendance patterns.

Telemetry and IoT Connectivity Transform Fleet Management Economics

Connected machines now ship with device-level telemetry that reports cleaning compliance, drink counts, and component wear to cloud dashboards for predictive maintenance and centralized control. Melitta’s IoT Hub, for example, monitors more than 145 attributes per machine across a large, connected base and supports remote recipe updates, reducing site visits when menus or extraction parameters need to be changed[2]INSIDE M2M https://inside-m2m.de/en/references/melitta. WMF CoffeeConnect delivers encrypted performance and sales data that helps operators track beverage volumes per unit, compare site performance, and schedule maintenance windows before failures disrupt service. For retailers and QSR chains, this shift from reactive to predictive service reduces downtime risks and makes uptime a contracted outcome rather than a best-effort result. Facilities data support the financial case, as lost beverage sales during espresso outages can materially impact daily margins in convenience formats where beverages drive a large portion of profit contribution. As these capabilities become standard, the global professional coffee machines market favors manufacturers that offer secure connectivity, scalable data platforms, and APIs that integrate with POS and loyalty systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and lifecycle maintenance/TCO for multi-group and super-automatic platforms | -1.1% | Global, particularly acute for independent cafes and SME buyers in price-sensitive markets | Short term (≤ 2 years) |

| Scarcity of certified service technicians and parts lead times | -0.8% | North America and Western Europe are the core, emerging in urban APAC as the installed base grows | Medium term (2-4 years) |

| Capsule waste scrutiny and policy pressures affecting pod-heavy OCS placements | -0.5% | Western Europe is leading due to EU PPWR, North America following as EPR schemes expand | Long term (≥ 4 years) |

| Power and water quality constraints in emerging markets raise TCO and downtime risk | -0.4% | Fragmented APAC, Middle East, and select Latin America regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Total Cost of Ownership Constrain Adoption

Upfront costs for commercial espresso and super-automatic machines are significant for independent cafes and smaller foodservice operators, and multi-year operating expenses add to the burden. Buyers often focus on sticker price and underweight the cost of water treatment, professional installation, consumables, and planned maintenance over the first three years. In this environment, leasing and managed-service models appeal because they convert a one-time investment into predictable monthly fees that include maintenance and consumables. Yet multi-year contracts reduce flexibility when operators want to pivot to new menus or equipment platforms, especially as consumer preferences evolve. These trade-offs slow adoption among price-sensitive buyers even as the operational case for automation gets stronger. The global professional coffee machines market, therefore, sees higher penetration first with larger chains and workplaces that can commit to service-level economics.

Certified Technician Scarcity and Extended Parts Lead Times Elevate Service Costs

The installed base is growing faster than the pool of certified coffee machine technicians, which creates response-time bottlenecks and higher service costs for complex fleets. Brands and their partners have begun strengthening parts distribution and training resources to reduce downtime; for example, Hemro’s expansion of its Parts Town and REPA partnership into new markets to improve grinder parts availability and support[3]HEMRO GROUP https://www.hemrogroup.com/en/news-and-events/hemro-group-appoints-parts-town-uk. Operators increasingly value vendors that guarantee replacement units during extended repairs and that offer telemetry-based maintenance plans aligned to actual usage. Without easy access to certified technicians, owners risk warranty issues and repeat failures stemming from improper repairs or delayed parts, particularly in machines with advanced electronics and dual-milk systems. The scarcity also pushes more buyers toward OCS and managed-service contracts where the provider holds service-level accountability. As a result, service depth, parts logistics, and training investment are becoming competitive differentiators in the global professional coffee machines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Automation Drives Super-Automatic Dominance While Manual Formats Retain Artisan Niches

Super-automatic bean-to-cup machines held 43.82% of the 2025 share and are projected to grow at 5.92% annually through 2031, widening their lead over traditional semi-automatic/manual espresso machines, drip/filter brewers, capsule/pod systems, and specialty beverage modules. The global professional coffee machines market continues to favor automation because it removes skill bottlenecks, standardizes extraction, and enables telemetry that supports predictive maintenance and remote recipe control across large fleets. Company product roadmaps mirror this shift, with Franke’s New A Line focusing on modularity, usability, energy savings, and hygiene features that match high-volume requirements. Thermoplan highlighted platform updates in 2025 targeting throughput, menu breadth, and fleet management for multi-site operators. The global professional coffee machines market rewards brands that integrate digital controls and milk systems for both dairy and plant-based beverages, as menu variety now plays a role in equipment selection.

Drip-and-filter brewers face substitution, while on-demand bean-to-cup platforms reduce waste and water use while providing a better cup experience for workplaces and convenience formats. Product data shows that on-demand grinding and optimized brew cycles can meaningfully reduce coffee waste and water use, which matters when replicated across large fleets[4]WILBUR CURTIS https://wilburcurtis.com/microsite/genesis/. Capsule/pod systems remain relevant in select OCS placements but face EU packaging rules that increase compliance complexity, motivating consideration of alternatives that avoid single-serve waste. Specialty modules, including nitro and rapid cold brew, are scaling from small bases as operators seek incremental traffic in the afternoon and evening periods with formats that do not require baristas.

By End User: Cafes Lead Share, but Offices Drive Fastest Marginal Growth Through Managed Services

Cafes and coffee shops accounted for 46.92% of 2025 revenue and are projected to grow at a 5.81% CAGR through 2031 as they anchor beverage-led foodservice across cities and suburbs. The segment bifurcates between artisan cafes that rely on manual equipment to differentiate brand identity and chain operators that prioritize speed, repeatability, and low training requirements through fully automated platforms. In the United States, drive-thru formats, rapid growth among chains like 7 Brew and Dutch Bros underlines the requirement for under-90-second service and high beverage consistency when handling high morning volumes. Hotels, restaurants, and QSR sites require stable throughput and easy operator interfaces to accommodate varied staffing, which supports investments in connected bean-to-cup systems. Offices and workplaces are a rising growth engine as employers use premium coffee programs to support hybrid work and recruit and retain talent.

Workplace coffee reflects shifting expectations as employees operating in hybrid patterns value in-office amenities that approximate cafe experiences. Hybrid adoption has stabilized in 2026, giving companies confidence to upgrade office beverage programs with fresh milk and specialty menus delivered through automated platforms. OCS providers address capex barriers through managed contracts that bundle equipment, consumables, telemetry, and maintenance with predictable monthly fees that align with facilities' budgets. Convenience retail and travel hubs also expand self-serve premium platforms that require robust uptime and cashless, touch-friendly interfaces that integrate with POS and loyalty ecosystems.

By Distribution Channel: OCS Providers Accelerate Through Managed Models While Traditional Dealers Face Margin Pressure

Authorized distributors and dealers accounted for 35.62% share in 2025, reflecting the value of local relationships, on-site installation expertise, and fast-response service for cafes and hospitality. Office coffee service providers are projected to grow at the fastest 5.66% CAGR through 2031 as subscription-based models convert capital expenditure into predictable operating fees and shift uptime responsibility to the provider. Telemetry-enabled service agreements allow providers to time preventive maintenance and deliver remote recipe updates, raising first-time fix rates and minimizing site disruption for clients. Direct-to-chains deal structures also carry strategic weight because large QSR and hospitality groups demand multi-country coverage, recipe governance, and uniform service-level terms. E-commerce and B2B portals continue to improve consumables replenishment and parts procurement, but remain a secondary path for complex machine purchases that require site surveys and professional installation.

Traditional dealers face pressure, while managed OCS contracts offer financing flexibility, telemetry analytics, and guaranteed replacement commitments that are hard to match without scale. In response, many dealers specialize in high-touch artisan cafes, boutique hotels, and local chains where consultative equipment configuration and rapid on-site support command a premium. Parts and service logistics are becoming a differentiator across channels, with partnerships that extend late cut-off times and enable same-day shipping, improving fleet support for grinders and machines. As these models mature, the global professional coffee machines market share for authorized distributors and dealers remains meaningful.

Geography Analysis

Europe retained the largest 2025 regional share at 34.24% on the back of dense cafe culture, strong hygiene norms, and sustainability mandates that reward energy-efficient equipment and automated cleaning. Buyers in Western Europe also consider compliance with the EU’s Packaging and Packaging Waste Regulation when evaluating capsule systems, which can favor bean-to-cup configurations that avoid single-serve waste. Feature roadmaps from leading manufacturers emphasize modularity, low standby consumption, and usage-based cleaning audits to meet procurement criteria tied to ESG disclosures.

Asia-Pacific is projected to grow fastest at a 6.13% CAGR through 2031 as urban specialty cafes proliferate and QSR coffee programs expand across China, India, and Southeast Asia. Franchise operators lean toward automated platforms with multilingual interfaces and touchscreen workflows to address staff turnover and training constraints. Manufacturers continue to invest in regional presence and training infrastructure to match the installed base’s growth, as evidenced by Franke’s Southeast Asia flagship showroom in Singapore, which serves as a hub for demonstrations, training, and collaboration. Australia and New Zealand maintain high standards for milk quality and workflow efficiency, spurring the adoption of automatic milk systems and connected diagnostics in hospitality and office settings.

North America combines mature cafe markets with rapid OCS expansion, aligning coffee programs with hybrid work patterns and employer amenity competition. Drive-thru growth among brands like 7 Brew and Dutch Bros reinforces the push toward under-90-second service windows and repeatable quality in early-day peaks. Convenience retail formats continue to roll out self-serve premium stations where beverage categories drive a significant share of margin dollars, and uptime is critical. In the Middle East and Africa, premium hospitality in GCC markets drives high-end placements while infrastructure variability in parts of Africa influences TCO and service strategies. Recycling partnerships that separate aluminum from grounds for compost and metal recovery illustrate maturing sustainability ecosystems that intersect with equipment choices in select markets.

Competitive Landscape

The competitive field includes scaled global manufacturers with multi-brand portfolios and specialized premium players that differentiate through engineering, connectivity, and service. SEB Professional sustains a portfolio approach that covers fully automatic and semi-automatic espresso systems for HoReCa, plus North American filter brewing via the Curtis line, which now includes a bean-to-cup platform focused on reducing waste and energy consumption. Franke underscores Swiss engineering with modular platforms, upgraded insulation, usage-based hygiene cycles, and native connectivity to enable centralized fleet management. Thermoplan updates focus on capacity, menu range, and digital tools that align with the needs of multi-location operators in foodservice and retail. These strategies show how the global professional coffee machines market rewards brands that integrate hardware advances with data, service, and sustainability value.

New solution categories spanning telemetry and digital workflow tools are reshaping the ecosystem around traditional hardware. Manufacturers that deliver secure data pipelines, recipe governance, and remote diagnostics provide operators with visibility into per-machine performance and product consistency. Producers are also expanding training and showroom footprints in high-growth regions to support integrators, distributors, and clients through hands-on demos and configuration workshops. For grinders and machine subcomponents, improved parts distribution via specialist partners shortens repair timelines and supports higher uptime across fleets. In this environment, the global professional coffee machines market favors OEMs that can deliver integrated value spanning equipment, digital services, training, and sustained parts availability.

Premium and artisan segments remain vibrant as brands showcase workflow innovations that combine manual craft with digital precision. La Marzocco’s connected ecosystem and telemetry platform illustrate how premium manufacturers are layering digital features onto traditional espresso workflows to retain high-end cafe customers who value hands-on extraction and precise reproducibility. In OCS and corporate environments, JURA’s professional line is designed for open-plan offices and self-serve areas, with device connectivity and cashless integration to support unattended operation. As equipment complexity rises, buyers seek suppliers who combine hardware reliability with straightforward maintenance, trustworthy connectivity, and clear sustainability credentials. The global professional coffee machines market, therefore, remains competitive on engineering, total cost of ownership, and digital service experience rather than hardware alone.

Professional Coffee Machines Industry Leaders

SEB Professional

Evoca Group

Franke Coffee Systems

Thermoplan AG

Gruppo Cimbali

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Franke Coffee Systems received the iF Design Award 2026 for its New A Line of professional coffee machines, highlighting modular scalability, HeatGuard boiler insulation that reduces energy loss by up to 44% compared with prior models, a new digital interface, and construction that uses high-quality steel and recycled materials.

- March 2026: Gruppo Cimbali announced a long-term strategic partnership with Mazzer and unveiled a Mazzer x Slayer grinder prototype to support high-volume cafés with grind-by-weight functionality and load-cell integration.

- February 2026: Hemro Group appointed Parts Town UK as its official spare parts distributor in the United Kingdom, expanding a global partnership to provide same-day shipping and support for Mahlkönig, Anfim, Ditting, and HeyCafé brands.

- February 2026: La Marzocco introduced Sistema, a connected platform for commercial espresso machines that offers real-time insights, usage-based servicing, continuous monitoring, and multi-tiered subscriptions for fleets of varying sizes.

Global Professional Coffee Machines Market Report Scope

| Super-automatic (bean-to-cup) |

| Traditional espresso (semi-automatic/manual) |

| Drip/Filter brewers |

| Capsule/Pod systems (professional) |

| Self-serve/Vending & OCS machines |

| Specialty beverage modules (e.g., cold brew/nitro) |

| Cafes & Coffee Shops |

| Hotels, Restaurants & QSR |

| Offices & Workplaces |

| Convenience & Retail |

| Travel & Leisure (Airports, Transport Hubs) |

| Others (Catering, Public Sector & Institutions (Education, Healthcare)) |

| Direct to Chains / Key Accounts |

| Authorized Distributors & Dealers |

| OCS Service Providers |

| E-commerce & B2B Digital |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Machine Type | Super-automatic (bean-to-cup) | |

| Traditional espresso (semi-automatic/manual) | ||

| Drip/Filter brewers | ||

| Capsule/Pod systems (professional) | ||

| Self-serve/Vending & OCS machines | ||

| Specialty beverage modules (e.g., cold brew/nitro) | ||

| By End User | Cafes & Coffee Shops | |

| Hotels, Restaurants & QSR | ||

| Offices & Workplaces | ||

| Convenience & Retail | ||

| Travel & Leisure (Airports, Transport Hubs) | ||

| Others (Catering, Public Sector & Institutions (Education, Healthcare)) | ||

| By Distribution / Channel | Direct to Chains / Key Accounts | |

| Authorized Distributors & Dealers | ||

| OCS Service Providers | ||

| E-commerce & B2B Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the outlook for the global professional coffee machines market through 2031?

The global professional coffee machines market size is projected to grow from USD 3.33 billion in 2025 to USD 4.48 billion by 2031, at a 5.21% CAGR, driven by automation, connectivity, and the adoption of managed services.

Which machine type is expected to lead growth over the forecast period?

Super-automatic bean-to-cup systems lead with 43.82% share in 2025 and are projected to grow at 5.92% annually through 2031, driven by consistency, uptime, and reduced training needs.

Where is regional growth the fastest in this space?

Asia-Pacific is projected to grow at a 6.13% CAGR through 2031 as specialty cafes, QSR programs, and modern office installations scale across major urban markets.

How are workplace trends influencing equipment purchases?

Stable hybrid work patterns are pushing employers to upgrade to premium office coffee with automated espresso platforms, telemetry, and service contracts to enhance the employee experience and reliability.

What role does connectivity play in fleet economics?

Telemetry platforms from OEMs and partners enable predictive maintenance, centralized recipe control, and faster issue resolution, reducing downtime and improving multi-site consistency.

How are regulations affecting equipment and capsule choices?

EU PPWR requirements on compostability and recycled content for capsules are prompting buyers to consider compliant packaging or bean-to-cup systems that avoid single-serve waste.

Page last updated on: