Print Advertising Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

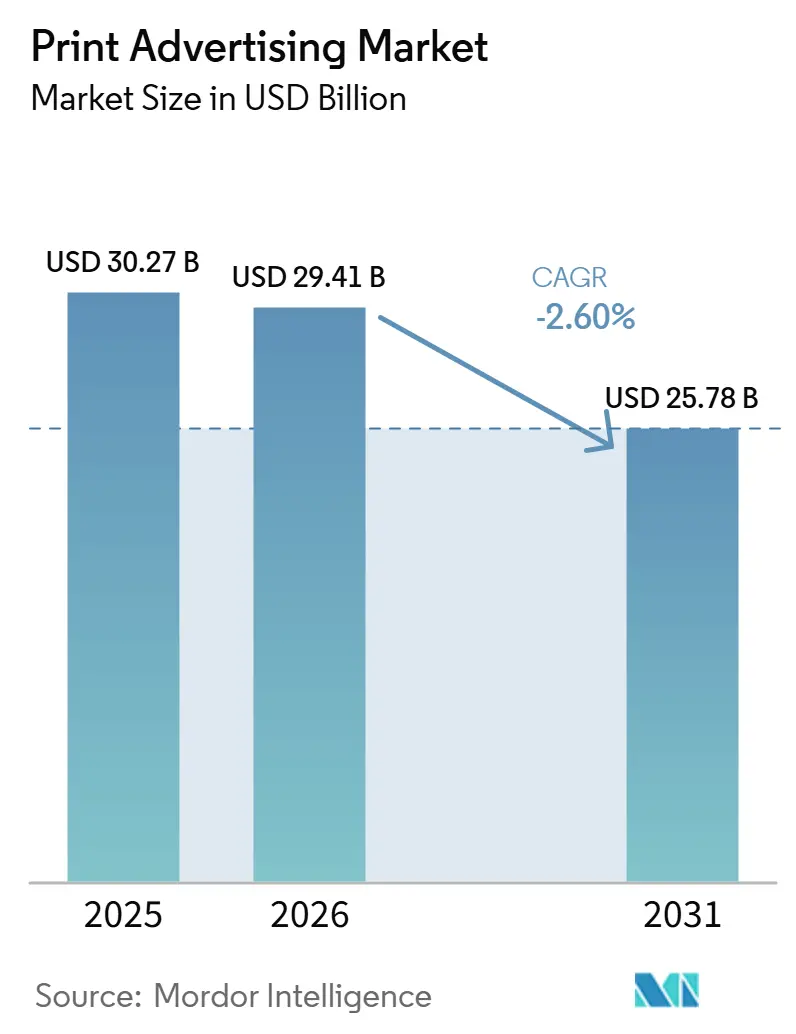

| Market Size (2026) | USD 29.41 Billion |

| Market Size (2031) | USD 25.78 Billion |

| Growth Rate (2026 - 2031) | -2.60% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Print Advertising Market Analysis by Mordor Intelligence

The print advertising market size is projected to expand from USD 30.27 billion in 2025 and USD 29.41 billion in 2026 to USD 25.78 billion by 2031, registering a CAGR of -2.60% between 2026 to 2031. The print advertising market is undergoing a structural reset as advertiser budgets continue to shift toward digital channels that offer faster measurement and more consistent optimization cycles. At the same time, print continues to play a defined role in areas where trust, physical presence, and response tracking are important, particularly in direct mail and premium local placements. Rising paper, ink, and postal fulfillment costs continued to pressure margins in 2025, making scale alone a less effective competitive advantage. As a result, larger providers in the print advertising market have expanded their service offerings to include production, audience data, creative support, and campaign execution. Consequently, the market has become increasingly divided, with broad-reach print formats continuing to decline, while measurable, personalized, and compliance-sensitive formats retain strategic budget relevance.

Key Report Takeaways

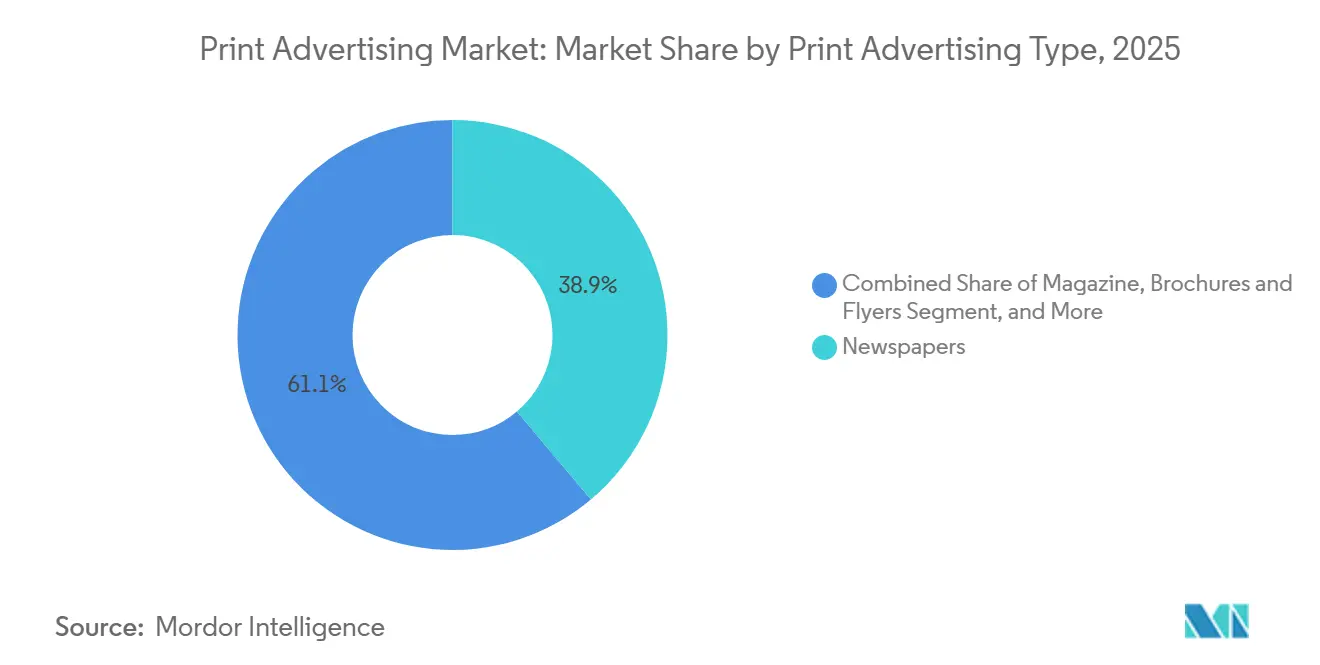

- By print advertising type, newspapers held 38.87% of print advertising market in 2025, while posters and billboards are projected to record the highest format CAGR at -1.78% through 2031.

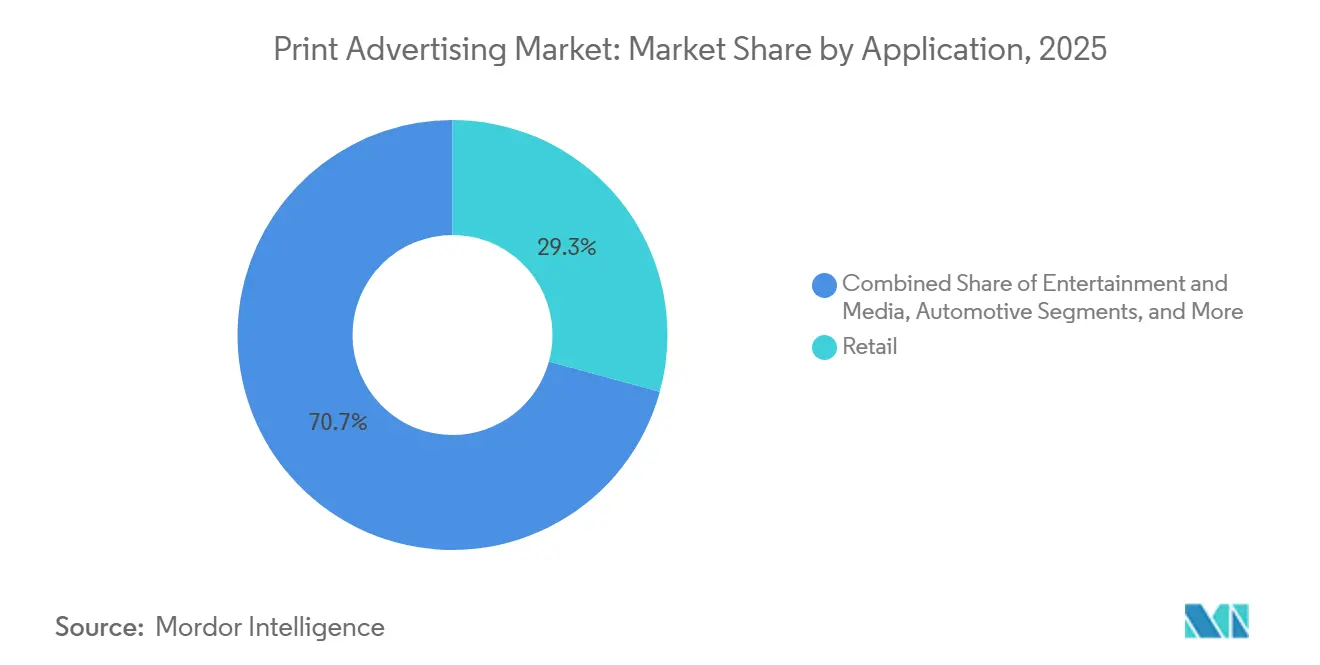

- By application, retail accounted for 29.26% of print advertising market in 2025, while healthcare is projected to post the strongest application CAGR at -1.98% through 2031.

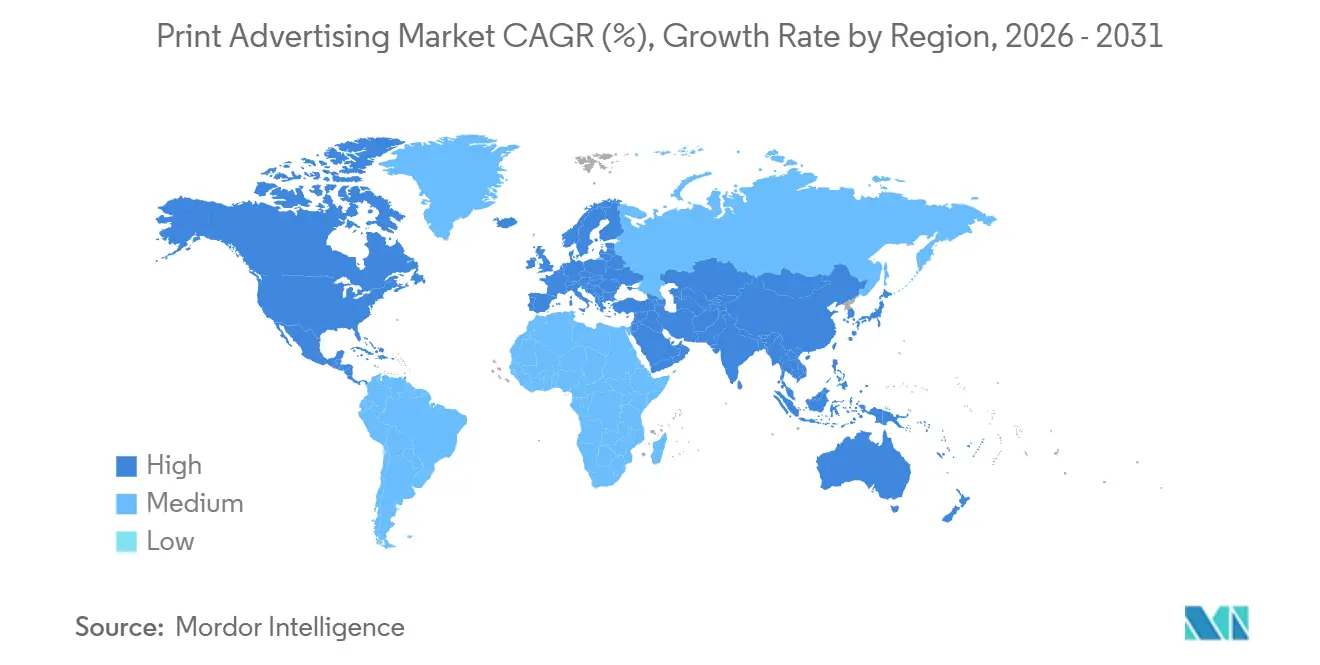

- By geography, Asia-Pacific held 33.22% of print advertising market in 2025, while the Middle East is projected to record the highest regional CAGR at -0.86% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Print Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Measurable Offline Response Channels | +0.5% | Global, concentrated impact in North America and Europe | Medium term (2-4 years) |

| Print-Plus-Digital QR Attribution in Direct Mail | +0.4% | Global, early adoption in North America and APAC core | Short term (≤ 2 years) |

| Variable-Data Printing for Micro-Segmented Mailings | +0.3% | North America and EU primary, spill-over to APAC and MENA | Medium term (2-4 years) |

| Retail Circulars and Coupon-Driven Footfall Recovery | +0.2% | North America and APAC core, early signs in Europe | Short term (≤ 2 years) |

| Premiumization of High-Impact Local Promotions | +0.2% | North America, Europe, and select APAC metropolitan markets | Medium term (2-4 years) |

| Postal Addressable Audience Access in Low-Data Penetration Markets | +0.1% | Africa, South Asia, and MENA, spill-over to rest of South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Measurable Offline Response Channels

The print advertising market is seeing renewed support in areas where advertisers can connect physical delivery with observable response behavior. According to a 2025 industry report, 79% of marketing executives ranked direct mail as their top-performing channel, while 82% planned to increase investment, indicating that print remains competitive when campaign response can be measured effectively. The same report identified an average direct mail response rate of 4.4%, helping explain why the print advertising market continues to attract investment in performance-driven campaigns rather than solely in brand-awareness initiatives. This shift is significant because print is increasingly being used not as a passive broadcast medium but as a tool for first-party customer engagement integrated within broader customer data strategies. As privacy restrictions make digital targeting less accessible in certain environments, postal channels become more valuable for campaigns requiring broad reach, stable consent frameworks, and measurable customer actions. Consequently, the print advertising market benefits most when marketers treat offline media as an integrated component of a connected customer response strategy rather than as a standalone legacy channel.

Print-Plus-Digital QR Attribution in Direct Mail

QR-enabled campaign design has addressed one of the longest-standing challenges in the print advertising market: the difficulty of linking print exposure to individual consumer actions. Printed materials can now direct users to a tracked destination, generating campaign, geographic, and conversion data that align with contemporary media planning practices. This capability makes print easier to compare with digital channels during budget evaluations because campaign performance is no longer assessed solely through broad circulation estimates. It also raises execution standards by making lower-performing placements easier to identify and eliminate from future campaigns. In practice, this trend favors high-quality direct mail, inserts, and premium print placements that support stronger audience intent. As a result, the print advertising market benefits from this development because measurable print campaigns are easier to justify within integrated, multi-channel marketing budgets.

Variable-Data Printing for Micro-Segmented Mailings

Variable data printing has become a more important support layer in the print advertising market because it allows each mail piece to reflect customer attributes, campaign triggers, or recent interactions. Franklin Madison reported in 2025 that 95% of direct mail marketers tested creative quarterly or more often, and more than half tested 11%-20% of mailing volume, which shows that print now follows a more iterative discipline than before.[1]Franklin Madison, “2025 Direct Mail Marketing Benchmark Report,” Franklin Madison Direct, franklinmadisondirect.com Dentsu Japan also noted that variable-data orders were increasingly cited by commercial print operators as a stabilizing revenue stream, even as mass-circulation advertising kept weakening. This changes the basis of competition because data handling and production flexibility become more important than volume capacity alone. It also gives the print advertising market a clearer role in campaigns that require personalization but still need physical delivery. For providers that can connect CRM inputs, creative variation, and print production, this part of the print advertising market offers better resilience than undifferentiated commodity print.

Retail Circulars and Coupon-Driven Footfall Recovery

Retail programs continue to support the print advertising market because of physical offers, local promotions, and store-led messaging function differently from digital impressions. Circulars, inserts, and coupon formats remain effective where retailers aim to drive store visits, promote weekly value, or reinforce local market presence through tangible communication. Their impact is particularly strong in categories characterized by habitual purchasing behavior, where printed materials act as prompts during household planning. In financial services and other conversion-driven sectors, direct mail continues to be used as part of customer acquisition and retention strategies, reflecting its ongoing role within response-oriented marketing programs. Within the print advertising market, this reinforces the relative durability of retail-linked formats compared with broad, non-targeted display placements. It also indicates that print continues to secure budget allocation when it is directly connected to measurable outcomes such as store traffic, household engagement, or redemption behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Structural Migration of Brand Budgets to Search and Social | -2.3% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) continuing through medium term |

| Declining Newspaper Readership and Magazine Ad Inventory | -1.2% | North America, Europe, and East Asia | Medium term (2-4 years) |

| Rising Paper, Ink, and Postal Fulfillment Costs | -0.6% | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| Shorter Campaign Cycles Favoring Always-On Digital Media | -0.4% | North America and EU primary, growing in APAC core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Structural Migration of Brand Budgets to Search and Social

The largest restraint on the print advertising market remains the steady migration of brand budgets toward search, social, and data-rich digital environments. This shift is reinforced by the way large agency groups continue to invest in data identity and collaboration tools that improve digital targeting precision and campaign optimization. WPP acquired InfoSum in April 2025 to strengthen privacy-safe data collaboration inside GroupM, which supports more refined audience planning across media channels.[2]WPP plc, “WPP Acquires InfoSum in Major Investment in Its AI-Driven Data Offer,” WPP, wpp.com Publicis Groupe also acquired Lotame in March 2025, adding independent identity and data capabilities that support more personalized media delivery across client campaigns. As these digital planning systems become more capable, the print advertising market faces a higher burden of proof during budget allocation. This makes broad print placements more exposed unless they can demonstrate either premium contextual value, addressable delivery, or compliance-led necessity.

Declining Newspaper Readership and Magazine Ad Inventory

The print advertising market also remains constrained by the continued decline in newspaper readership and the shrinking availability of standard magazine inventory. Dentsu reported that newspaper advertising expenditure in Japan fell 8.2% to JPY 313.6 billion (USD 2.06 billion). The same source reported that magazine advertising in Japan declined 3.7% to JPY 113.5 billion (USD 0.75 billion) on the same conversion basis.[3]Dentsu Inc., “2025 Japan Advertising Expenditures,” Dentsu Japan, dentsu.co.jp In Germany, ZAW reported that daily newspapers declined 9.0% in 2025, consumer magazines fell 14.7%, and specialist publications dropped 7.3%, while weekly and Sunday newspapers grew 12.1%. This pattern shows that surviving print inventory is becoming narrower, more selective, and more premium in nature. This limits recovery potential in the print advertising market because available volume contracts even before advertiser demand is fully tested.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Print Advertising Type: Newspapers Lead Despite Format-Level Divergence

Newspapers held 38.87% of print advertising market share in 2025, maintaining their position as the largest format even as readership erosion continued across mature markets. Posters and billboards are projected to record the strongest format CAGR at -1.78% through 2031, indicating that they are declining more slowly than the overall print advertising market. This relative resilience is driven by their continued use in brand-building programs where location, visibility, and environmental context remain important. Magazine formats remain under stronger pressure where digital substitution is deeper, and readership recovery has not materialized. In Germany, consumer magazine advertising fell 14.7%, and specialist titles declined 7.3% in 2025, underscoring the uneven nature of the print advertising market across format types.

Posters and billboards, with a projected CAGR of -1.78%, remain the most durable format segment within the print advertising industry because they continue to support high-visibility campaigns that are difficult to replicate through handheld digital screens alone. Brochures and flyers also retain value in event settings, B2B trade activity, and local promotional contexts where physical handoff supports attention and recall. The “Others” category, which includes direct mail, catalogs, and promotional inserts, is declining more slowly than flat-circulation newspaper formats because personalization and scan-based attribution have improved accountability. This is one of the few areas where the print advertising market is being partially supported at the segment level by improved targeting rather than broad audience scale. The industry is therefore separating into formats that can connect with response data and formats that continue to rely primarily on legacy reach.

By Application: Retail Commands Spend, Healthcare Outpaces Sector Decline

Retail accounted for 29.26% of the print advertising market size in 2025, making it the largest application segment across the print advertising market. Healthcare is projected to post the highest application CAGR at -1.98% through 2031, which still reflects decline but at a slower pace than the overall market. This segment stands out because healthcare communication often requires compliant, targeted, and documented outreach rather than open digital targeting. The U.S. Department of Health and Human Services continues to enforce HIPAA regulations governing the protection and handling of health information, which reinforces the practical role of postal outreach in patient communication, acquisition, and adherence programs.[4]U.S. Department of Health and Human Services, “HIPAA Security Rule,” HHS, hhs.gov This regulatory context supports the continued use of print in healthcare, contributing to its relative resilience within the print advertising market.

Financial services also demonstrate sustained application-level demand, with mailing volumes in some segments expected to increase significantly, reflecting the continued use of print for product launches, compliance communication, and customer acquisition. Automotive remains an important user of print for launch visibility and regional promotion programs, particularly where large-format displays and local newspaper presence retain influence. Entertainment and media, along with education, continue to use print more selectively for event-driven campaigns and regional audience reach. The “Others” category remains relevant as government, NGO, and B2B communications continue to rely on print in contexts where digital penetration or targeting flexibility is limited. Across the print advertising industry, application resilience is strongest where compliance requirements, local reach, or measurable conversion pathways give physical media a defined functional role.

Geography Analysis

Asia-Pacific held 33.22% of print advertising market share in 2025, making it the largest regional segment in the print advertising market. The region combines markets where print still retains local reach strength with others where digital substitution has advanced more rapidly. In Japan, newspaper advertising expenditure fell 8.2% to JPY 313.6 billion (USD 2.06 billion) in 2025, highlighting how sharply even historically print-oriented markets are adjusting. Magazine advertising in Japan also declined 3.7% to JPY 113.5 billion (USD 0.75 billion) on the same basis, reflecting continued pressure from digital news consumption and weakening print inventory conditions. Despite these declines, the print advertising market in Asia-Pacific remains large due to local-language publishing depth, continued use of promotional print formats, and a relatively broad print ecosystem compared with many Western markets.

Germany recorded EUR 6,741.94 million in print advertising revenue in 2025 (USD 7.28 billion), representing a 2.7% decline from the prior year. ZAW reported that daily newspapers declined 9.0% and consumer magazines fell 14.7%, while weekly and Sunday newspapers rose 12.1%, indicating that audience concentration and editorial frequency continue to influence performance in premium print environments. This suggests that the print advertising market in Europe is not declining uniformly, as niche and higher-quality segments continue to attract selective investment. North America follows a similar pattern, where structural decline persists but direct mail remains relatively more stable than broad print display due to stronger measurability of response. In this context, targeted print formats continue to retain relevance even as overall market volumes contract.

The Middle East is projected to post the highest regional CAGR at -0.5% to +1.0% through 2031, making it the least negative geography and the only region with a potential for marginal growth at the upper end of the range in the print advertising market. Demand in the region is supported by government communication requirements, luxury placements in Arabic-language publications, and high-visibility urban poster campaigns. Africa and South America remain smaller contributors to global value, although selected countries continue to sustain newspaper and promotional print demand across FMCG, telecom, public communication, and retail campaigns. Overall, this results in a geographically uneven print advertising market, with resilience concentrated in specific countries and use cases rather than consistent regional expansion.

Competitive Landscape

The print advertising market is moderately fragmented, with large print production groups, specialist providers, publishers, and media holding companies all influencing how budgets are planned and executed. Cimpress reported FY2025 revenue of USD 3.40 billion, up 3.38%, and stated that its PrintBrothers and The Print Group segments together exceeded USD 1 billion in annual revenue for the first time, indicating that scaled customization continues to generate demand. This is significant in the print advertising market because web-to-print and mass customization provide larger operators with a more flexible growth path compared to standard commercial print alone. Quad also reflects this shift, with its FY2025 Form 10-K noting that approximately 90% of U.S. clients purchased more than one service in 2025, indicating deeper integration across data, production, and execution. In the print advertising market, competitive advantage is now shaped less by print capacity alone and more by the ability to bundle targeting, creative support, analytics, and fulfillment.

RRD illustrated this transition through the launch of Iridio in April 2025, a unified platform combining print production, digital advertising, one-to-one marketing, data management, AI-driven creative development, and cloud-native technology. WPP also strengthened the data layer of omnichannel media planning by acquiring InfoSum in April 2025, expanding privacy-safe audience collaboration capabilities within GroupM. Publicis Groupe followed with its acquisition of Lotame in March 2025, adding identity and data infrastructure that supports more precise campaign delivery across media formats, including print-integrated programs within broader campaigns. These developments indicate that the print advertising market is increasingly being managed as part of a connected media ecosystem rather than as an isolated channel. They also highlight a widening gap between providers capable of integrating print into data-driven workflows and those competing primarily on cost and production scale.

Another strategic development came from Publicis Groupe in April 2026, when it expanded its partnership with Microsoft to develop a full-stack agentic marketing solution across its organization, supporting personalization and planning across channels. DNP also expanded its footprint in June 2026 through a formal offer for AUSTRIACARD HOLDINGS AG, extending its position in information security-related operations beyond traditional print activities. TOPPAN similarly advanced its adjacency strategy by completing the acquisition of Sonoco’s TFP business in April 2025, strengthening its packaging footprint across the Americas. The print advertising market therefore remains structurally fragmented, but leading companies are increasingly broader, more data-driven, and more diversified into adjacent services that help preserve value as traditional print volumes decline.

Print Advertising Industry Leaders

R.R. Donnelley & Sons Company

Cimpress plc

Dai Nippon Printing Co., Ltd.

Toppan Holdings Inc.

Quad/Graphics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Publicis Groupe and Microsoft expanded their strategic partnership to develop a full-stack agentic marketing solution, deploying Microsoft 365 Copilot across 114,000+ Publicis employees and selecting Microsoft Azure as preferred cloud provider. The collaboration is designed to accelerate personalization at scale across all channels, including integrated print and digital campaign planning and execution.

- April 2026: Publicis Groupe entered into a definitive agreement to acquire 160over90, a global sports and culture-first agency, for an undisclosed consideration, adding high-impact sports context print advertising capabilities to its cross-channel portfolio and expanding its sports-driven media investment practice.

- April 2025: WPP plc acquired InfoSum, the leading data collaboration platform, for approximately USD 150 million. InfoSum joined GroupM, WPP's media investment group, enabling privacy-safe data collaboration for audience targeting across print and digital campaigns, and representing a significant AI-driven enhancement to WPP's data infrastructure.

- April 2025: TOPPAN Holdings Inc. completed the acquisition of Sonoco Products Company's Thermoformed and Flexible Packaging business for approximately USD 1.8 billion, TOPPAN's largest acquisition to date, expanding the company's global sustainable packaging manufacturing footprint across North and South America.

Global Print Advertising Market Report Scope

The Print Advertising Market Report is Segmented by Print Advertising Type (Newspapers, Magazines, Brochures and Flyers, Posters and Billboards, and More), Application (Retail, Automotive, Healthcare, Financial Services, Entertainment and Media, Education, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Newspapers |

| Magazines |

| Brochures and Flyers |

| Posters and Billboards |

| Other Print Advertising Type |

| Retail |

| Automotive |

| Healthcare |

| Financial Services |

| Entertainment and Media |

| Education |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Print Advertising Type | Newspapers | |

| Magazines | ||

| Brochures and Flyers | ||

| Posters and Billboards | ||

| Other Print Advertising Type | ||

| By Application | Retail | |

| Automotive | ||

| Healthcare | ||

| Financial Services | ||

| Entertainment and Media | ||

| Education | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the print advertising market size through 2031?

The print advertising market size is projected to move from USD 30.27 billion in 2025 and USD 29.41 billion in 2026 to USD 25.78 billion by 2031, at a CAGR of -2.60% during 2026-2031.

Which print format holds the largest share of revenue?

Newspapers remained the largest format in 2025 with 38.87% of global value, even though the segment continues to face structural readership pressure.

Which application is holding up best in the forecast period?

Healthcare is projected to perform best on a relative basis, with a CAGR of -1.98%, because compliant patient communication still supports direct mail use.

Which region leads global demand for print advertising?

Asia-Pacific led in 2025 with 33.22% of global value, while the Middle East is expected to post the strongest regional growth range through 2031.

Why does direct mail still matter for advertisers?

Direct mail continues to matter because marketers can now track response more effectively through QR codes, personalized URLs, and attribution systems that link physical mail to digital actions.

How are major companies adapting to the decline in traditional print volumes?

Leading firms are moving toward broader service models through data, personalization, automation, and acquisitions, with examples including WPP’s InfoSum deal, Publicis’s Lotame deal, and RRD’s Iridio platform launch.

Page last updated on: