Pregnancy Pillow Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

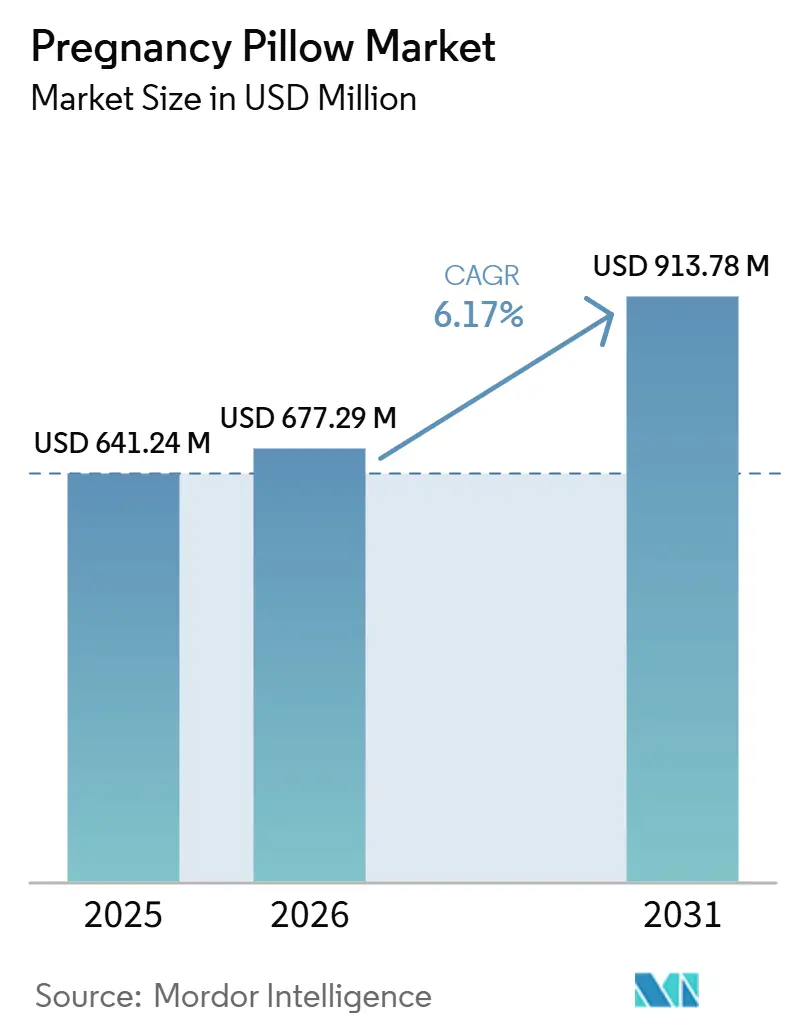

| Market Size (2026) | USD 677.29 Million |

| Market Size (2031) | USD 913.78 Million |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pregnancy Pillow Market Analysis by Mordor Intelligence

The Pregnancy Pillow Market size is projected to be USD 641.24 million in 2025, USD 677.29 million in 2026, and reach USD 913.78 million by 2031, growing at a CAGR of 6.17% from 2026 to 2031.

The pregnancy pillow market is benefiting from stronger medical acceptance because a randomized controlled study published in 2026 showed that third-trimester pillow use improved sleep quality and comfort outcomes for pregnant women. The pregnancy pillow market is also drawing support from the continued rise in older motherhood, since U.S. fertility rates for women aged 40 and older increased over the last decade, and that pattern continued into 2025. The pregnancy pillow market is becoming easier to scale because digital retail now shapes how expectant mothers discover, compare, and purchase prenatal comfort products. The pregnancy pillow market is also moving up the value chain as certified materials, stronger ergonomic positioning, and postpartum use cases support higher price realization. The pregnancy pillow market still faces trust pressure from counterfeit listings and unsafe products on open marketplaces, which makes clinician partnerships, verified materials, and direct brand control more important for long-term performance.

Key Report Takeaways

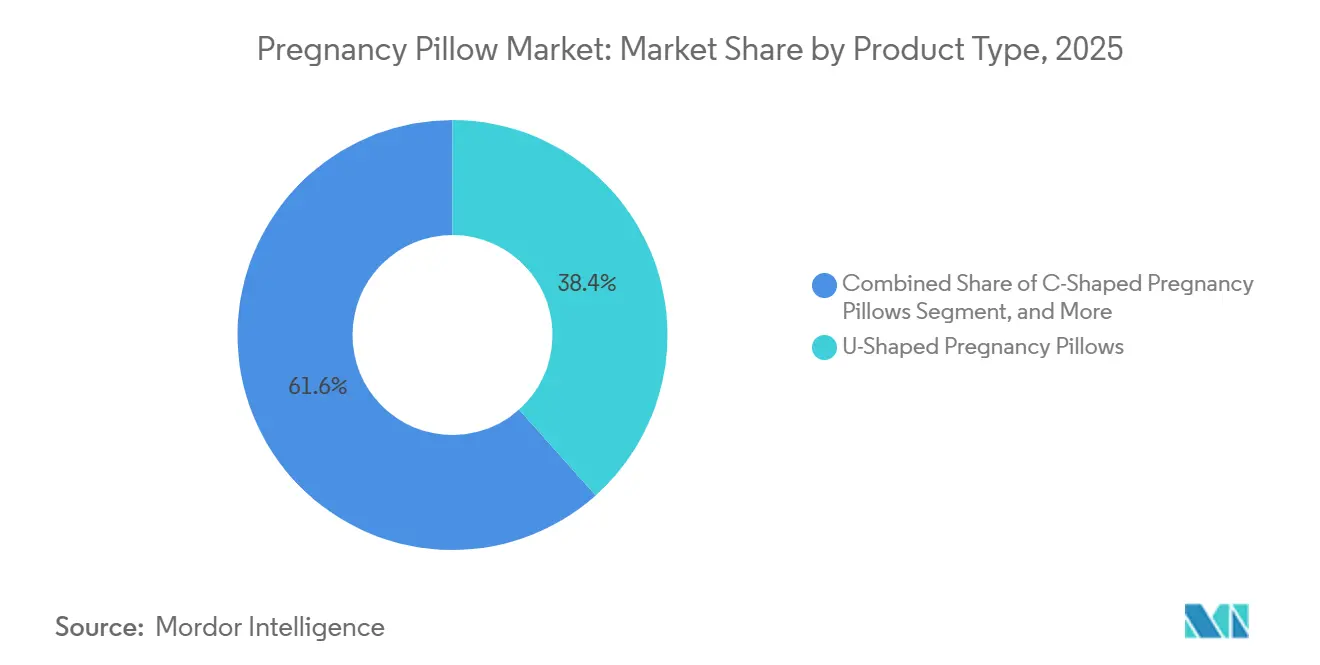

- By product type, U-shaped pillows held 38.43% share in 2025, while full body pillows are projected to expand at a 7.03% CAGR through 2031.

- By material type, memory foam held 42.82% share in 2025, while organic cotton and natural fill are forecast to grow at a 6.64% CAGR through 2031.

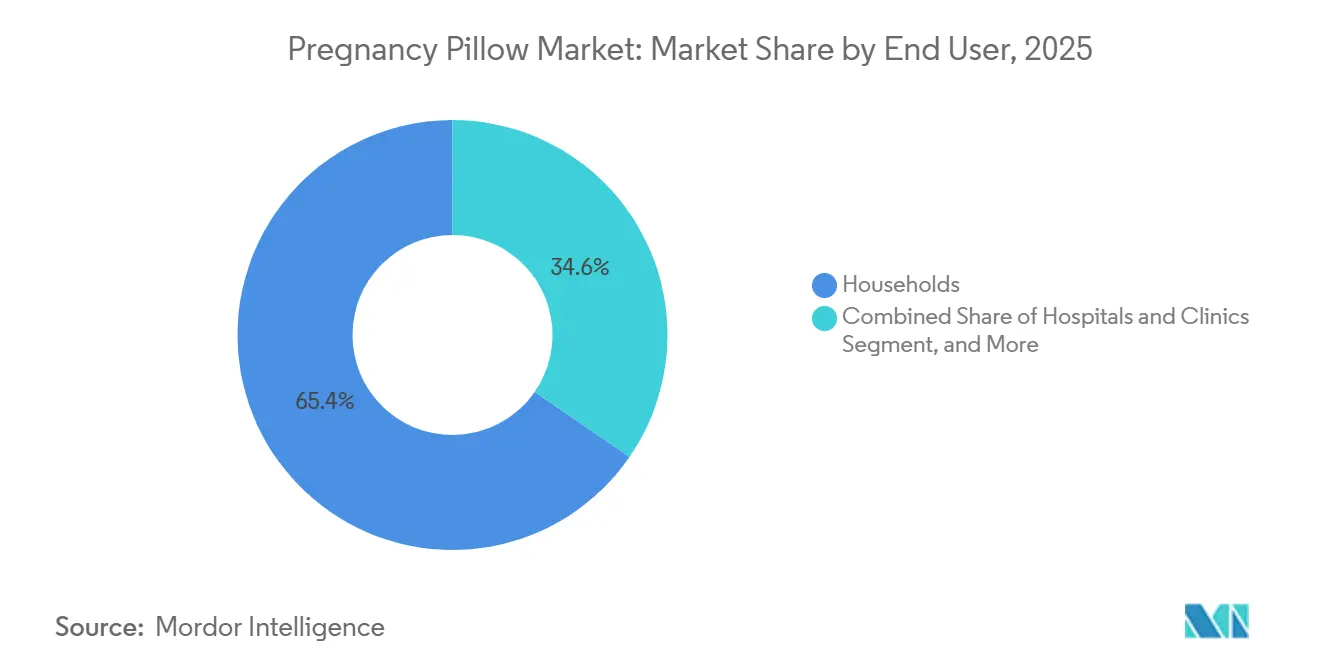

- By end user, households held 65.39% share in 2025, while maternity homes and birth centers are projected to record the highest CAGR at 7.44% through 2031.

- By distribution channel, online retail held 52.19% share in 2025, while specialty sleep stores are forecast to expand at a 6.82% CAGR through 2031.

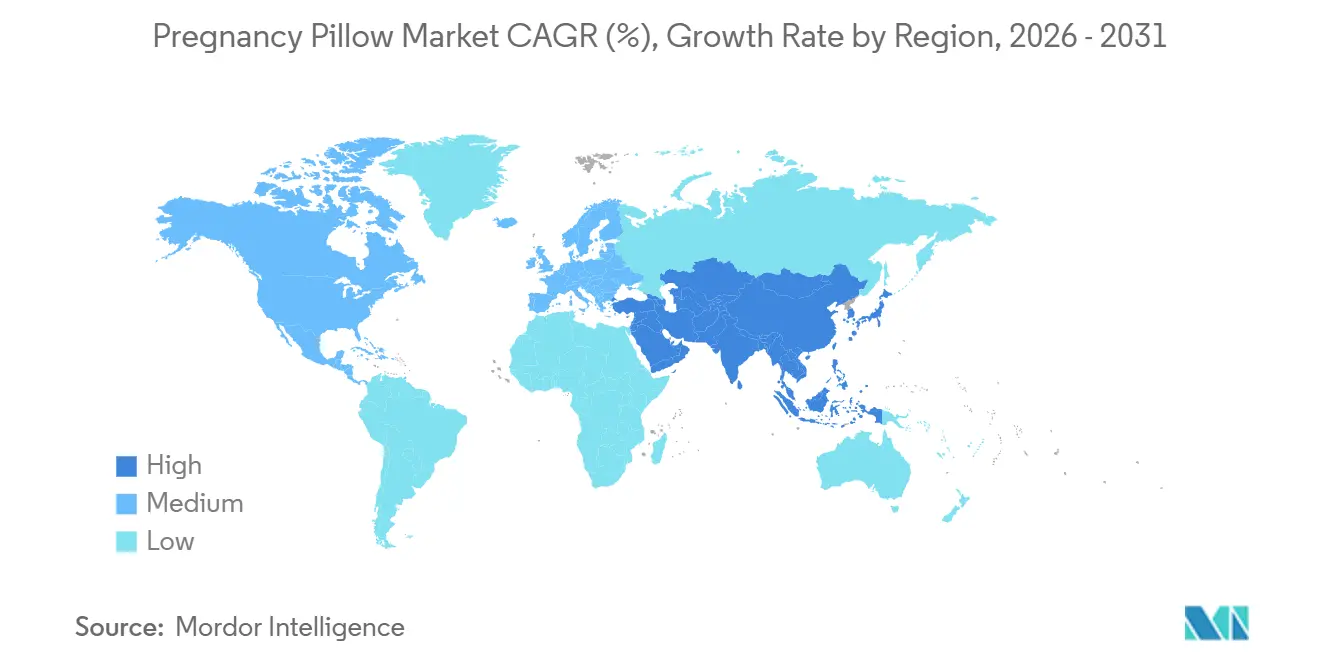

- By geography, North America held 42.24% of the pregnancy pillow market share in 2025, while Asia-Pacific is projected to grow at a 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pregnancy Pillow Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Maternal Age and Sleep Discomfort | +1.4% | Global, most pronounced in North America, Western Europe, and East Asia tier-1 cities | Long term (≥ 4 years) |

| Doctor-Backed Prenatal Sleep Guidance | +1.1% | North America, Europe including the UK, Germany, and France, with gradual spillover to APAC urban centers | Medium term (2-4 years) |

| E-Commerce Discovery and Trial-Based Purchasing | +1.2% | Global, with highest velocity in APAC, Latin America, and Eastern Europe | Short term (≤ 2 years) |

| Product Multipurpose Use Beyond Pregnancy | +0.8% | Global, particularly strong in North America and Northern Europe where postpartum wellness bundling is commercialized | Medium term (2-4 years) |

| Premiumization Through Materials and Ergonomics | +0.6% | North America, Germany, the UK, Australia, and Japan | Long term (≥ 4 years) |

| Under-Reported Postpartum Wellness Bundling | +0.5% | North America and Northern Europe, with early-stage adoption in APAC urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Maternal Age and Sleep Discomfort: Structurally Expanding the Buyer Base

Advanced maternal age remains one of the most durable demand supports for the pregnancy pillow market because sleep problems rise during pregnancy and become harder to manage in later gestation.[1]H. Chen et al., “Clinical Review: Maternal Sleep Disorders During Pregnancy,” Sleep Medicine, sciencedirect.com A 2025 meta-analysis reported a 45.7% incidence of sleep disorders during pregnancy, and the burden increased with gestational age and maternal BMI. U.S. fertility data also showed that births among older mothers kept rising, with the rate for women aged 40 and older increasing 24% from 2015 to 2024, while provisional 2025 data showed that this shift continued. This matters for the pregnancy pillow market because delayed childbearing usually overlaps with higher household income, stronger health awareness, and a greater willingness to pay for ergonomic sleep products. The pregnancy pillow market, therefore, gains not only a larger clinical need base, but also a buyer group that is more likely to trade up into better materials, fuller support designs, and products with stronger medical framing.

Doctor-Backed Prenatal Sleep Guidance: Clinical Endorsement as a Purchase Trigger

Clinical guidance is turning pregnancy sleep support from a discretionary item into a more deliberate purchase within the pregnancy pillow market.[2]National Institute for Health and Care Excellence, “Antenatal Care: Evidence Review W, Maternal Sleep Position During Pregnancy,” NICE, magicapp.org NICE recommends side sleeping after 28 weeks of gestation, and that advice gives positional support products a clearer place in prenatal care conversations. Advocate Health Care also advised pregnant women in 2025 to use a pillow to support side sleeping, which directly links clinical sleep advice to category demand. The pregnancy pillow market gained stronger evidence in support when a randomized controlled study found significant improvement in Pittsburgh Sleep Quality Index scores and pregnancy comfort outcomes among third-trimester users. The pregnancy pillow market is also moving closer to institutional adoption because Amenity Health began recruiting for a positional therapy study in 2026, which shows that device-grade positioning is becoming a live competitive dimension rather than a distant concept.

E-Commerce Discovery and Trial-Based Purchasing: The Channel That Builds the Market

Digital commerce remains central to the pregnancy pillow market because the importance of that channel goes beyond transaction volume, as it has become the main space where first-time mothers compare support shapes, fabric claims, and peer reviews. Momcozy’s June 2025 launch of a midwife-approved pillow series showed how the pregnancy pillow market now blends expert validation, direct-to-consumer selling, and creator-led awareness in one launch model. This structure reduces buyer hesitation because review systems and professional endorsements help replace the in-store trial that many shoppers no longer rely on. The pregnancy pillow market, therefore, grows faster when digital storefronts function as education, validation, and conversion tools at the same time.

Premiumization Through Materials and Ergonomics: The Durable Value Creation Story

The pregnancy pillow market is moving away from undifferentiated fill products and toward certified materials, cleaner inputs, and stronger ergonomic claims. Organic cotton and natural fill is the fastest-growing material segments, with a 6.6% CAGR through 2031. Obasan’s 2026 redesign of its organic latex pregnancy pillow showed how brands are using GOLS-certified latex and GOTS-certified cotton to support premium positioning with material traceability.[3]Obasan, “Obasan Organic Latex Pregnancy Pillow,” Obasan, obasan.com The pregnancy pillow market also benefits from the wider availability of certification frameworks because they make premium claims easier to verify during purchase comparison. This shifts value away from low-cost commodity offerings and toward brands that can combine shape retention, cleaner fabrics, lower chemical concern, and a more professional product story.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Price Versus Short Usage Window | -0.8% | Global, most pronounced in price-sensitive markets in South America, MEA, and APAC tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Bulky Form Factor and Storage Friction | -0.5% | Global, most acute in compact urban living markets including Japan, South Korea, Hong Kong, and dense EU cities | Medium term (2-4 years) |

| Comfort Subjectivity and Return Risk | -0.4% | Global, elevated in markets with advanced e-commerce return policies including North America, Germany, and Australia | Short term (≤ 2 years) |

| Counterfeit and Low-Trust Marketplace Listings | -0.6% | Global, concentrated in open marketplace-dependent markets including the United States, India, China, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Price Versus Short Usage Window: The Value Perception Gap

The pregnancy pillow market still faces a basic value hurdle because the item often carries a noticeable upfront price while its primary use period feels limited to later pregnancy. Premium full-body designs commonly retail between USD 60 and USD 150 in the user-supplied draft, and that creates a real purchase pause for price-sensitive households. The issue becomes stronger when buyers frame the product as a short-term solution rather than as a multi-stage support item for sleep, nursing, and recovery. The pregnancy pillow market performs better when brands explain postpartum and general back-support use clearly, because that extends perceived product life and improves value perception. That communication remains inconsistent across mass retail listings, which leaves part of the category exposed to hesitation even when the comfort need is clear.

Counterfeit and Low-Trust Marketplace Listings: Undermining the Digital Sales Engine

Counterfeit proliferation is a direct restraint on the pregnancy pillow market because it damages the same digital channels that currently drive discovery and volume. Amazon reported that it identified, seized, and disposed of more than 15 million counterfeit products globally in 2025, and the baby and sleep categories were among the most exposed groups. Which? also identified 150 unsafe baby and sleep products across major marketplaces in July 2026, which reinforced concerns around platform enforcement and buyer trust. In December 2025, the UK Office for Product Safety and Standards issued a safety alert covering baby sleep pillows marketed with misleading claims, which raised the compliance bar for related sleep product listings. The pregnancy pillow market therefore, rewards brands that can prove product safety, maintain verified listings, and move customers toward trusted direct or specialist channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: U-Shaped Leads, Full-Body Surging

U-shaped pregnancy pillows held 38.43% of the pregnancy pillow market share in 2025, which reflected their ability to support the back and abdomen at the same time. Their wraparound format reduces the need for repositioning during sleep, and that makes the design especially relevant in later pregnancy when movement becomes harder. The format also fits neatly with side-sleep guidance because it helps users maintain lateral positioning with fewer adjustments. C-shaped products remained important for buyers who wanted front and back support with a lighter physical footprint, while J-shaped, wedge, and inflatable options served entry-level, travel, or space-limited needs inside the pregnancy pillow market.

Full body pregnancy pillows are projected to expand at a 7.03% CAGR through 2031, giving them the fastest growth profile within this product mix. That pace reflects growing preference for designs that adapt to changing body geometry across trimesters without the need to switch pillows. The pregnancy pillow market also gained stronger support for this format after a 2026 randomized study showed better sleep quality and comfort outcomes for third-trimester users. Postpartum extension adds another layer of demand because many full-body models are marketed for nursing support, back relief, and longer household use after delivery. The main limit remains shelf practicality in physical retail, where bulky formats require more space and are harder to display than wedges or more compact shapes.

By Material Type: Foam Dominant, Organic Rising Fast

Memory foam held 42.82% of the global material share in 2025, which kept it at the center of the pregnancy pillow market because buyers associate it with pressure relief and adaptive support. The material is familiar to consumers, easier to compare across brands, and usually available across both mass and premium price tiers. Certification is also becoming more relevant in this category, as MedCline highlighted CertiPUR-US certified shredded memory foam in its maternity pillow positioning. Polyester and microfiber fill stayed commercially relevant because they support entry-level and mid-tier price points, while hypoallergenic fillings remained important in clinical or allergy-sensitive settings within the pregnancy pillow market.

Organic cotton and natural fill are forecast to grow at a 6.64% CAGR through 2031, which makes it the fastest-rising material group in the pregnancy pillow market size. That trend reflects a shift from broad comfort claims toward cleaner material provenance and more visible certification language. Obasan’s 2026 redesign used a GOLS-certified organic latex core and a GOTS-certified organic cotton cover, which showed how premium brands are turning source transparency into a purchase signal. As buyers compare inputs more closely, certification-backed products gain stronger credibility among health-conscious households and specialist retailers. This also increases pressure on undifferentiated polyester-fill products, since they face tighter pricing and weaker defensibility when premium alternatives become easier to verify.

By End User: Households Lead, Institutions Gaining Share

Households accounted for 65.39% of the global pregnancy pillow market in 2025, which made personal purchase the core demand base for the category. Most household decisions are shaped by review depth, perceived comfort, and confidence that the pillow will solve side-sleep or back-support problems quickly. Social proof matters heavily in this segment, and midwife, OB, or peer endorsements often shorten the evaluation window before purchase. Hospitals and clinics held a smaller but meaningful place in the pregnancy pillow market because their selection process depends more on evidence, hygiene, and product durability than on lifestyle branding.

Maternity homes and birth centers are projected to expand at a 7.44% CAGR through 2031, which gives them the strongest growth profile among end users. This shift shows that the pregnancy pillow market is moving beyond household convenience and into more structured care environments. Clinical validation supports that transition, since a 2026 randomized controlled study showed measurable gains in sleep quality and comfort among users in late pregnancy. Procurement in these settings will likely favor brands that can supply compliance documents, washable designs, and more consistent bulk availability. Consumer-oriented companies that build an institutional offer early stand to benefit as maternity settings treat positional support as a standard care aid rather than an optional amenity.

By Distribution Channel: Online Commands Share, Specialty Accelerates

Online retail held 52.19% of global distribution in 2025, which means the pregnancy pillow market is already led by a digitally native sales model. Many brands first build visibility through marketplaces and brand-owned sites, where search placement, reviews, and creator content play a larger role than physical shelf presence. This structure lowers the entry barrier for newer labels because buyers can compare support styles and proof points without an in-store visit. Offline retail still matters in the pregnancy pillow market because tactile checks on fabric feel, fill density, and overall size remain useful for buyers who are less comfortable purchasing a large sleep item unseen.

Specialty sleep stores are projected to expand at a 6.82% CAGR through 2031, which makes them the fastest-growing channel within the pregnancy pillow market. That pattern is commercially logical because premium pricing works better in environments where staff can explain ergonomic features and material claims in person. Pharmacies and maternity stores also support trust-sensitive purchases, especially where medical association itself acts as a soft quality filter. The pregnancy pillow market is therefore splitting into two clear channel roles, with e-commerce driving scale and discovery while specialty and pharmacy channels help protect margin on better-differentiated products. Brands that treat these routes as separate strategies rather than one blended channel plan are better placed to manage pricing, education, and product mix.

Geography Analysis

North America held 42.24% of the pregnancy pillow market size in 2025, and it remained the most commercially mature regional base for the category. The region benefits from high health spending, broad retail access, and a buyer group that is more likely to respond to medical advice on side sleeping and prenatal comfort. U.S. fertility trends also support demand because births among older mothers kept rising through 2024, and that direction continued in provisional 2025 data. The pregnancy pillow market in North America also shows elevated exposure to counterfeit risk because open marketplace dependence is high, and third-party seller density is strong.

Europe does not move as one unit in the pregnancy pillow market, and country-level execution matters more than broad regional messaging. Germany remains important because e-commerce and specialist retail both support premium ergonomic sleep products, while brands with strong direct-to-consumer positioning can build share without depending only on mass retail. Nordic and German-rooted labels also benefit from consumer familiarity with wellness-led design and cleaner material positioning. Southern and Eastern Europe form the next demand layer as urban maternal age rises and online shopping becomes more normalized for maternity products. The UK adds a sharper compliance lens to the pregnancy pillow market because safety scrutiny around baby sleep pillows has raised expectations for product claims and listing quality.

Asia-Pacific is forecast to grow at a 6.94% CAGR through 2031, which makes it the fastest-growing region in the pregnancy pillow market. Urban China and India are creating demand conditions that resemble earlier North American development, with rising maternal age, stronger digital retail use, and greater awareness of prenatal sleep ergonomics. Japan, South Korea, and Australia sit at the premium end of the regional spectrum, where higher-quality ergonomic sleep products already have an established consumer base. Middle East and Africa and South America remain earlier-stage parts of the pregnancy pillow market, but improving health infrastructure, stronger e-commerce access, and rising disposable incomes are opening room for category expansion, with GCC markets and Brazil leading within their respective regions.

Competitive Landscape

The pregnancy pillow market remains moderately fragmented, with specialist brands and large marketplace sellers competing across very different price and trust levels. Brands such as Leachco, Momcozy, MedCline, Boppy, and bbhugme hold stronger brand equity because they combine product identity with clearer positioning around comfort, safety, or clinical relevance. Momcozy used that playbook in June 2025 when it launched a midwife-approved pregnancy pillow series built around licensed professional review and sleep-care messaging. MedCline moved the category closer to medical framing with its December 2025 pregnancy body pillow launch and its 2026 positional therapy study activity, which together strengthen its credibility with healthcare-linked buyers. Boppy also reinforced its design moat in October 2025 when the U.S. Patent and Trademark Office granted a patent for a firm support pillow design.

A major white space in the pregnancy pillow market sits in institutional selling, since maternity homes and birth centers are growing faster than the wider category. Many brands still approach the business with a consumer-first model, even though institutional buyers require bulk pricing, hygiene documents, and evidence packages. Postpartum extension is another underused lever because products that move from pregnancy support into nursing and recovery can defend premium pricing more effectively. The pregnancy pillow market therefore offers the best upside to companies that connect clinical framing, longer product life, and operational readiness rather than relying only on consumer advertising.

Counterfeit pressure is also shaping competition in the pregnancy pillow market by pushing buyers toward better-known names and more controlled channels. When unsafe or misleading products stay visible on large marketplaces, smaller price-led sellers may gain short-term volume, but trust shifts toward brands that can prove compliance and origin. That gives an advantage to companies with clinician partnerships, certification-backed materials, and stronger listing governance. Even so, the pregnancy pillow market is not yet close to tight consolidation because private-label sellers and shape-level duplication still keep entry barriers relatively low across digital channels.

Pregnancy Pillow Industry Leaders

The Procter and Gamble Company

Boppy Company LLC

Noble Pillow

Theraline e.K.

Walmart Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Momcozy debuted multiple new maternal care innovations at ABC Kids Expo 2026 (Las Vegas), reaffirming its position as a global leader in wearable breast pumps and maternal care, including comfort-forward feeding and sleep solutions. The launches reflected a strategic commitment to covering the maternal care continuum from pregnancy through postpartum.

- March 2026: Amenity Health's MedCline division began recruiting participants for a clinical investigation (NCT07492420) evaluating the MedCline Sleep System for treatment of mild obstructive sleep apnea through positional therapy — a study with direct implications for the medical-grade positioning of pillow-based sleep interventions and their alignment with American Academy of Sleep Medicine guidelines.

Global Pregnancy Pillow Market Report Scope

The Pregnancy Pillow Market refers to the global industry involved in the design, manufacturing, distribution, and sale of pillows specifically created to provide comfort and support for pregnant individuals. These pillows are designed to alleviate pressure on the back, hips, abdomen, neck, and legs, helping improve sleep quality and reduce discomfort during pregnancy.

The Pregnancy Pillow Market is segmented based on product type, material type, end user, distribution channel, and geography. By product type, the market includes U-shaped pregnancy pillows, C-shaped pregnancy pillows, J-shaped pregnancy pillows, wedge pregnancy pillows, full body pregnancy pillows, and inflatable pregnancy pillows. Based on material type, the market is categorized into memory foam, polyester and microfiber fill, organic cotton and natural fill, and hypoallergenic fillings. By end user, the market is divided into households, hospitals and clinics, and maternity homes and birth centers.

Geographically, the Pregnancy Pillow Market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa, and South America. North America includes the United States, Canada, and Mexico. Europe comprises Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. Asia-Pacific covers China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific. The Middle East & Africa region includes the GCC, South Africa, and the Rest of Middle East & Africa, while South America consists of Brazil, Argentina, and the Rest of South America.

| U-Shaped Pregnancy Pillows |

| C-Shaped Pregnancy Pillows |

| J-Shaped Pregnancy Pillows |

| Wedge Pregnancy Pillows |

| Full Body Pregnancy Pillows |

| Inflatable Pregnancy Pillows |

| Memory Foam |

| Polyester and Microfiber Fill |

| Organic Cotton and Natural Fill |

| Hypoallergenic Fillings |

| Households |

| Hospitals and Clinics |

| Maternity Homes and Birth Centers |

| Online Retail |

| Offline Retail |

| Specialty Sleep Stores |

| Pharmacies and Maternity Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | U-Shaped Pregnancy Pillows | |

| C-Shaped Pregnancy Pillows | ||

| J-Shaped Pregnancy Pillows | ||

| Wedge Pregnancy Pillows | ||

| Full Body Pregnancy Pillows | ||

| Inflatable Pregnancy Pillows | ||

| By Material Type | Memory Foam | |

| Polyester and Microfiber Fill | ||

| Organic Cotton and Natural Fill | ||

| Hypoallergenic Fillings | ||

| By End User | Households | |

| Hospitals and Clinics | ||

| Maternity Homes and Birth Centers | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| Specialty Sleep Stores | ||

| Pharmacies and Maternity Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the pregnancy pillow market by 2031?

The pregnancy pillow market is forecast to reach USD 913.78 million by 2031, growing from USD 677.29 million in 2026 at a 6.17% CAGR.

Which product type leads demand today?

U-shaped pillows led the category in 2025 with 38.43% share because they support both the back and abdomen and fit side-sleep needs well.

Which product format is growing the fastest?

Full body pillows are projected to grow at a 7.03% CAGR through 2031 because they adapt across trimesters and extend into postpartum use.

Why are maternity homes and birth centers becoming more important?

This end-user group is expected to grow at a 7.44% CAGR through 2031 as clinical validation and procurement interest move pillows closer to routine maternity care.

How important is online retail for category expansion?

Online retail held 52.19% of distribution in 2025, making digital discovery, reviews, and direct-to-consumer selling central to brand growth.

Page last updated on: