Pregnancy Medication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 51.98 Billion |

| Market Size (2031) | USD 71.22 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

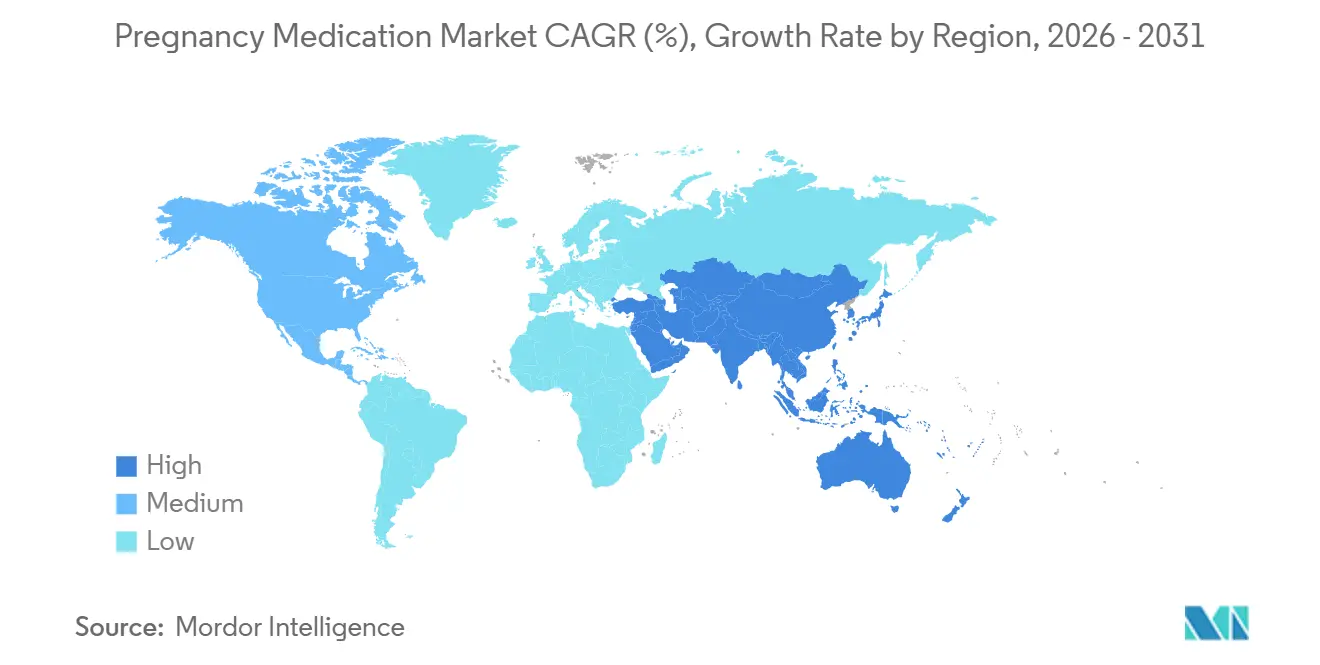

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pregnancy Medication Market Analysis by Mordor Intelligence

The Pregnancy Medication Market size was valued at USD 49.58 billion in 2025 and is estimated to grow from USD 51.98 billion in 2026 to reach USD 71.22 billion by 2031, at a CAGR of 6.5% during the forecast period (2026-2031).

This growth path reflects three structural changes that are now shaping product demand and clinical decision pathways, including the withdrawal of long-standing progesterone therapies for recurrent preterm birth prevention, the prioritization of biomarker-led triage for preeclampsia, and persistent shortages in plasma-derived immunoglobulins that are accelerating the shift to precision diagnostics instead of routine prophylaxis. Initial guidelines in 2026 emphasize targeted prophylaxis and stratified care, which channels volume toward therapies with proven maternal and neonatal benefits and away from maintenance regimens without demonstrable outcome gains. The pregnancy medication market is also redistributing usage across care settings as acute hypertension protocols and seizure prophylaxis shift more administrations into hospital pharmacies, while stable outpatient therapies remain anchored in retail channels. The most durable growth tailwind comes from rising metabolic complications of pregnancy, where evolving formularies and improved adherence strategies are lifting antidiabetic utilization and shaping payer criteria for continuation of therapy.

Key Report Takeaways

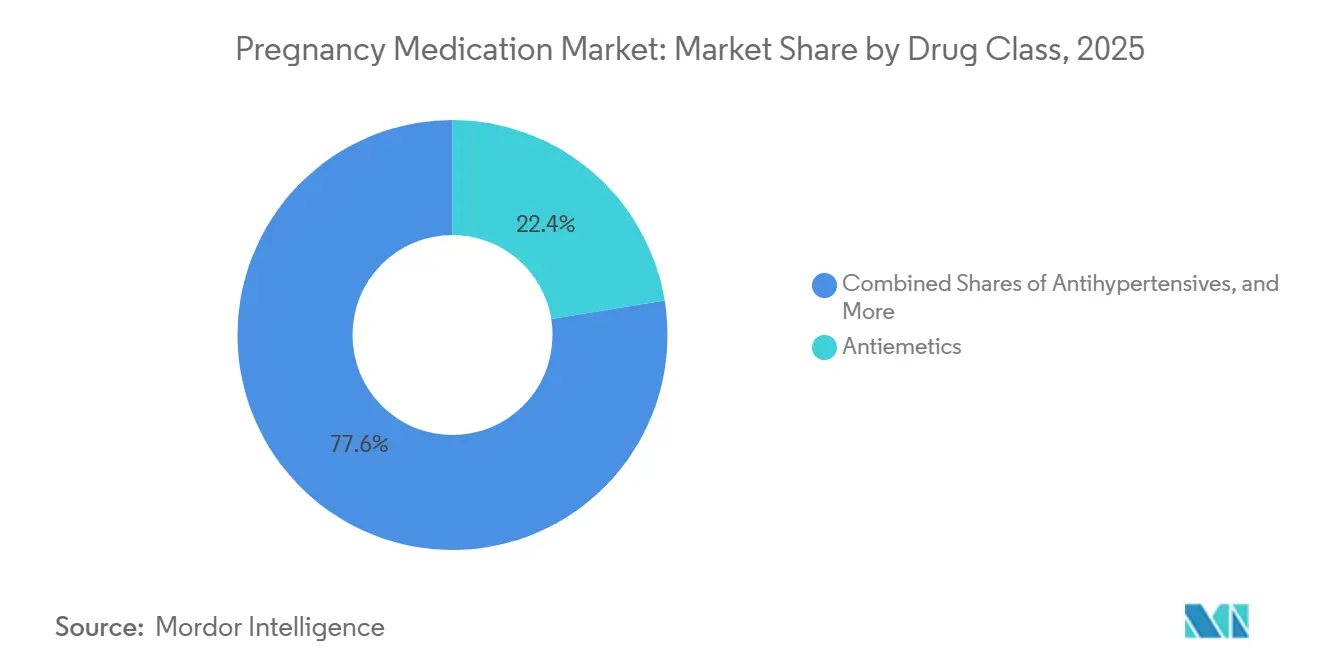

- By drug class, antiemetics led with 22.45% revenue share in 2025, while antidiabetics are forecast to expand at a 9.03% CAGR to 2031.

- By indication, nausea and vomiting of pregnancy accounted for a 24.32% share of the pregnancy medication market size in 2025, while gestational diabetes management is advancing at an 8.53% CAGR through 2031.

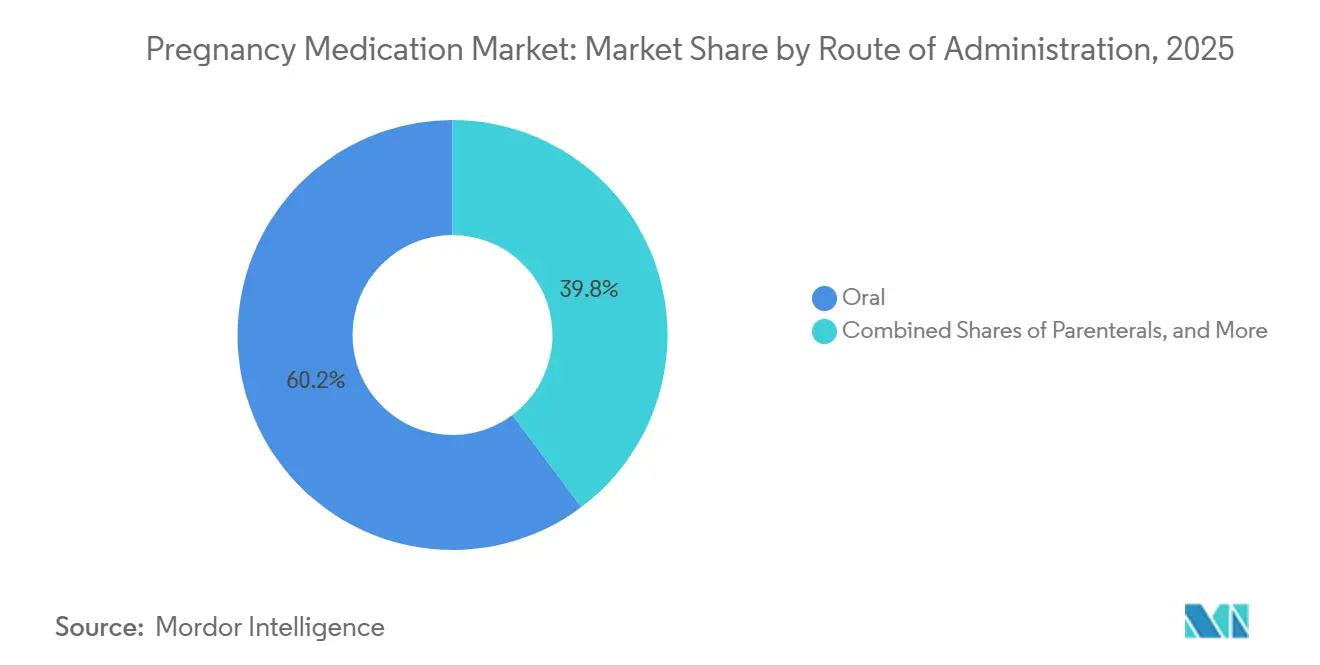

- By route of administration, oral formulations held 60.23% of 2025 volume, while parenteral administration is projected to grow at a 7.23% CAGR.

- By distribution channel, retail pharmacies accounted for 55.32% of 2025 distribution, while hospital pharmacies are projected to grow at a 7.22% CAGR.

- By geography, North America captured 32.45% of 2025 revenues, while Asia-Pacific is projected to expand at a 7.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pregnancy Medication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of nausea and vomiting of pregnancy | +1.2% | Global, with higher treatment uptake in North America and Western Europe | Medium term (2-4 years) |

| Persistent global burden of preterm birth and need for tocolysis and ACS | +0.9% | Global, acute in Sub-Saharan Africa and South Asia | Medium term (2-4 years) |

| Rising hyperglycemia in pregnancy driving insulin and antidiabetic use | +1.8% | APAC core (India, China, Southeast Asia), spill-over to Middle East | Long term (≥ 4 years) |

| Guideline-backed low-dose aspirin prophylaxis in high-risk pregnancies | +1.0% | North America, EU, Australia | Short term (≤ 2 years) |

| Growing use of antihypertensives in hypertensive disorders of pregnancy | +0.8% | National, with early gains in US, UK, Canada | Medium term (2-4 years) |

| Biomarker-led triage (e.g., PlGF) enabling earlier pharmacologic intervention | +0.7% | EU (especially UK, Germany, Netherlands), selective adoption in US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence Of Nausea And Vomiting Of Pregnancy

Between 70% and 80% of pregnant women experience nausea and vomiting of pregnancy, with a smaller subset progressing to hyperemesis gravidarum that requires hospital care. Doxylamine succinate combined with pyridoxine hydrochloride has extensive safety data without a teratogenic signal across very large exposed cohorts, which supports its first-line role in guidance updates. The entry of approved generics, including the Health Canada authorization of delayed-release doxylamine-pyridoxine 10 mg/10 mg by Apotex[1]Apotex/Health Canada, “Doxylamine succinate, Pyridoxine hydrochloride Delayed Release Tablets PM,” Health Canada, pdf.hres.ca, adds price competition and can expand access in cost-sensitive settings. The delayed-release pharmacokinetic profile that peaks after several hours enables evening dosing and better alignment with morning-predominant symptoms, which helps adherence in outpatient care. These factors keep antiemetics central to first-line management and sustain the foundation of the pregnancy medication market.

Persistent Global Burden Of Preterm Birth And Need For Tocolysis And Antenatal Corticosteroids

Preterm birth remains a leading driver of neonatal morbidity and mortality, and global standards have converged on time-limited tocolysis that creates a 48-hour window to administer antenatal corticosteroids and transfer mothers to higher-acuity centers. WHO guidance specifies evidence-backed steroid regimens, including betamethasone 12 mg intramuscularly in two doses 24 hours apart or dexamethasone 6 mg intramuscularly in four doses 12 hours apart, for women between 24 and 34 weeks when preterm delivery appears likely within seven days. Maintenance tocolysis is discouraged due to limited neonatal benefit and higher maternal risk, which restrains chronic tocolytic use in outpatient settings and focuses utilization on periods of clear neonatal benefit. The United States withdrawal of 17-hydroxyprogesterone caproate in 2023 removed the previously approved option for recurrent preterm birth risk reduction and shifted practice toward off-label alternatives or closer surveillance. Acute tocolysis often centers on short courses of nifedipine or indomethacin consistent with time-limited protocols, which aligns procurement with the inpatient windows that deliver the greatest impact on neonatal outcomes.

Rising Hyperglycemia In Pregnancy Driving Insulin And Antidiabetic Use

Gestational diabetes is rising in regions with genetic predisposition to insulin resistance and increased maternal age, which is driving higher use of basal insulin and metformin under updated care pathways[2]Australian Prescriber, “Gestational diabetes: update on screening, diagnosis and maternal management,” Australian Prescriber, australianprescriber.tg.org.au. Kaiser Permanente’s 2025 guidance endorses insulin glargine as the preferred basal insulin and shifts metformin toward extended-release dosing twice daily, which improves adherence by reducing gastrointestinal side effects in outpatient care. Professional recommendations advise against glyburide first line due to higher risks of neonatal hypoglycemia and macrosomia relative to insulin or metformin, which consolidates treatment around safer profiles in the pregnancy medication market.

Comparative evidence in type 1 diabetes pregnancies indicates insulin aspart can improve third-trimester glycemic control without worsening perinatal outcomes, which supports formulary preference for analog insulin[3]Novo Nordisk Science Hub, “Insulin aspart in pregnant women with type 1 diabetes,” Novo Nordisk, sciencehub.novonordisk.com. Expanded clinical use of continuous glucose monitoring supported by clinician guidance on automated insulin delivery algorithms can standardize glycemic targets across maternal-fetal programs and support steady growth in diabetes care corridors.

Guideline-Backed Low-Dose Aspirin Prophylaxis In High-Risk Pregnancies

Low-dose aspirin started early in pregnancy reduces the risk of preeclampsia, preterm birth, and intrauterine growth restriction in high-risk women, and this evidence base has led to broad support and ongoing implementation across systems[4]American Academy of Family Physicians, “Hypertensive Disorders of Pregnancy,” AAFP, aafp.org. Dosing varies by region, with 81 mg daily common in the United States and 150 mg endorsed in U.K. protocols, which reflects differing balances of bleeding risk and background cardiovascular risk. Success depends on initiation before 16 weeks, since later initiation reduces the likelihood of benefit, which underscores the role of first-trimester screening in prenatal care workflows. U.S. Preventive Services Task Force recommendations and primary care efforts continue to improve identification of risk factors, although adherence gaps persist when high-risk women are not seen early enough. As identification criteria and prescribing workflows become more consistent across systems, the pregnancy medication market benefits from reliable and early prophylaxis in the women most likely to gain from it.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA withdrawal of 17-OHPC (Makena) curtails progesterone use | -0.5% | United States, with EU suspension in 2024 | Short term (≤ 2 years) |

| Rh(D) immune globulin shortages constrain prophylaxis availability | -0.4% | Global, most acute in North America and EU | Medium term (2-4 years) |

| Non-invasive fetal RhD genotyping reducing unnecessary anti-D administration | -0.3% | EU (Finland, Norway, Netherlands, Denmark), emerging in North America | Long term (≥ 4 years) |

| WHO limits on maintenance tocolysis and restricted indications temper use | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FDA Withdrawal Of 17-OHPC (Makena) Curtails Progesterone Use For Recurrent PTB Prevention

The U.S. Food and Drug Administration finalized the withdrawal of Makena (17-hydroxyprogesterone caproate) and its generics in April 2023, which removed the only drug that had been approved in the United States for reducing the risk of recurrent preterm birth in women with a prior spontaneous preterm birth and a current singleton pregnancy. This decision erased a mature subcategory within the pregnancy medication market and led clinicians to rely on off-label alternatives or closer surveillance for high-risk patients. The change also signaled that pregnancy medications cleared on surrogate endpoints face ongoing regulatory scrutiny that can result in post-approval reversal if confirmatory evidence does not show clinical benefit, which may influence future development and payer reviews. The resulting coverage uncertainty for off-label progesterone formulations has limited scaled substitution, which leaves a therapeutic gap for recurrent preterm birth risk reduction. As health systems adapt, utilization has shifted toward evidence-supported acute protocols like time-limited tocolysis and antenatal corticosteroids for imminent preterm delivery, which constrains the longer-duration progesterone corridor within the pregnancy medication market.

Rh(D) Immune Globulin Shortages Constrain Prophylaxis Availability

Rh(D) immune globulin shortages identified in late 2023 persisted through 2026 in several regions, driven by shrinking RhD-negative donor pools, manufacturing deviations, and the long production lead times required for plasma-derived products. AABB guidance prioritizes postpartum prophylaxis during severe shortages over routine 28-week antepartum doses and endorses the use of cell-free fetal DNA testing to identify the estimated 40% of RhD-negative mothers who carry RhD-negative fetuses and can forgo prophylaxis. The European regulatory community has also urged targeted use through non-invasive prenatal screening and investment in research for recombinant anti-D, since plasma-derived supply depends on immunized donor pools that are structurally constrained. Investments in new plasma fractionation capacity are planned, but time frames stretch to the end of the decade, which limits near-term relief and keeps stewardship measures central to practice. These dynamics reweight demand toward precision diagnostics and inpatient prioritization, which shapes both channel mix and class-level performance in the pregnancy medication market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Antidiabetics Overtake Legacy Leaders on Metabolic Crisis

Antiemetics held 22.45% of the pregnancy medication market share in 2025, while antidiabetics are projected to grow at a 9.03% CAGR to 2031, outpacing the overall pregnancy medication market as metabolic complications rise with maternal age and obesity. Kaiser Permanente’s June 2025 guidance designated insulin glargine as the preferred basal insulin and moved metformin toward extended-release dosing twice daily, which improves adherence and aligns with formulary shifts in integrated health systems. Professional recommendations that advise against glyburide as first line have consolidated treatment around insulin and metformin, creating a more predictable uptake trajectory within the pregnancy medication market. Antihypertensives remain a durable and mature corridor anchored by labetalol and nifedipine, with use rising in the third trimester as preeclampsia prevalence increases and as targets tighten in inpatient settings. Tocolytics, in contrast, face restricted indications due to WHO guidance limiting use to a 48-hour window, which curbs maintenance therapy and aligns utilization with the periods of proven neonatal benefit.

The progesterone corridor contracted sharply after the 2023 United States withdrawal of hydroxyprogesterone caproate, which left off-label alternatives without consistent payer coverage and reduced scaled substitution in the pregnancy medication industry. Immunoglobulins, especially anti-D products, remain under supply strain due to donor demographics and concentrated manufacturing, which has accelerated targeted prophylaxis strategies using non-invasive fetal RhD genotyping to avoid unnecessary administration. Antenatal corticosteroids such as betamethasone and dexamethasone continue to track preterm birth exposures and are guided by WHO protocols that permit a single repeat course under specific conditions, which keeps demand stable in tertiary centers. Anticoagulants and anti-infectives focus on defined risk cohorts, and while they contribute steady baseline demand, they do not alter the aggregate growth profile of the pregnancy medication market in the current cycle.

By Indication: Gestational Diabetes Outpaces NVP on Epidemiologic Momentum

Nausea and vomiting of pregnancy accounted for a 24.32% share of the pregnancy medication market size in 2025, which reflects widespread prevalence and the entrenched first-line role of antiemetics in outpatient care. Gestational diabetes management is advancing at an 8.53% projected CAGR to 2031 on rising maternal BMI and delayed childbearing, and it benefits from clearer preferences that center on insulin glargine and extended-release metformin. The Australasian Diabetes in Pregnancy Society’s 2025 consensus refined screening and diagnostic thresholds to improve case identification while seeking to avoid overdiagnosis, but the prevalence trends in high-risk populations maintain upward pressure on treatment volumes. Hypertensive disorders of pregnancy continue to command significant pharmacologic attention, with biomarker-integrated triage in several European systems enabling earlier identification of cases that will benefit from antihypertensives and magnesium sulfate prophylaxis.

Rh immunoprophylaxis remains essential to prevent alloimmunization, but use is now being targeted through non-invasive fetal RhD genotyping in several European countries, which cuts unnecessary injections and helps steward supply. Preterm labor management revolves around tighter, evidence-based prescribing of tocolytics and antenatal corticosteroids, which shifts exposure into windows of highest neonatal benefit and contains maintenance use. Infection-related care such as Group B Streptococcus prophylaxis follows stable protocols and contributes steady baseline utilization with low volatility. Smaller indications such as threatened miscarriage and venous thromboembolism address focused risk cohorts, and while clinically important, they hold limited influence on the overall trajectory of the pregnancy medication market.

By Route of Administration: Parenteral Gains as Acute-Care Protocols Intensify

Oral formulations accounted for 60.23% of 2025 volume, reflecting the dominance of outpatient maintenance therapies, while parenteral therapies are projected to grow at 7.23% CAGR through 2031 as acute protocols for severe hypertension, seizure prophylaxis, and preterm labor concentrate use in hospital settings. Management of acute-onset severe hypertension favors intravenous labetalol or hydralazine and immediate-release oral nifedipine for rapid control, which emphasizes readiness of hospital pharmacies and utilization under medical benefits. Magnesium sulfate infusions remain the standard for seizure prophylaxis in preeclampsia with severe features, with peri- and postpartum monitoring that extends inpatient exposure. Subcutaneous insulin by pens and emerging automated insulin delivery systems are expanding evidence in high-risk ambulatory care, which adds a device-enabled layer to glycemic control in the pregnancy medication market.

Vaginal formulations support reproductiveogy and selected obstetric uses and remain sensitive to payer coverage and formulary controls, while generics may broaden access as approvals progress. Intramuscular betamethasone and dexamethasone courses continue to mitigate respiratory risk in imminent preterm delivery, guided by WHO protocols that depend on accurate dating and readiness for neonatal care. As hospital pathways refine timing criteria and observation standards, the pregnancy medication market continues to tilt toward settings that can deliver time-sensitive interventions consistently with measurable impact on outcomes.

By Distribution Channel: Hospital Pharmacies Capture Acute-Care Escalation

Retail pharmacies held 55.32% of 2025 distribution for oral maintenance therapies, while hospital pharmacies are projected to grow at 7.22% CAGR as acute, high-acuity care consolidates parenteral use under inpatient management with assured reimbursement. Allocation protocols during shortages have also favored inpatient prioritization, which has been especially clear in postpartum anti-D dosing when supply is constrained. Specialty maternal-fetal medicine clinics support intermediate-acuity use of antenatal corticosteroids and selected biologics and continue to shape local distribution even as hospital pharmacies expand share in severe disease pathways. Online channels remain limited for pregnancy-specific medications due to control status, cold-chain logistics, and time-sensitive use, which narrows e-commerce to select oral maintenance drugs with stable safety profiles.

Shortages and stewardship measures are central for plasma-derived products, and investments to expand fractionation capacity aim to ease bottlenecks over multi-year timelines, which informs procurement and contracting strategy across the pregnancy medication market. European guidance encourages targeted use and research into recombinant anti-D to reduce dependence on constrained donor pools, which could strengthen resilience of supply for obstetric programs.

Geography Analysis

North America captured 32.45% of 2025 revenues on the strength of high per-capita pharmaceutical spending, comprehensive prenatal screening, and broad access to guideline-based therapies within the pregnancy medication market. European systems continue to integrate biomarker-led triage for preeclampsia, which supports earlier targeted treatment and reduces unnecessary admissions in high-volume centers. Donor constraints for plasma-derived anti-D in Europe have driven prioritization guidance and a fresh interest in recombinant alternatives to build long-run supply resilience for obstetric care. Provider networks in the United States emphasize rapid-control hypertension protocols and magnesium sulfate prophylaxis, which sustain hospital pharmacy demand and align with tightened targets for maternal safety. Retail channels in both regions continue to anchor outpatient antiemetics, antihypertensives, and antidiabetics and maintain the largest distribution share in the pregnancy medication market.

Asia-Pacific is projected to expand at a 7.69% CAGR to 2031, led by rising gestational diabetes prevalence, improved maternal health infrastructure, and broader coverage for advanced diagnostics and therapies. National policies that back non-invasive prenatal testing and maternal screening build a foundation for earlier identification and targeted pharmacology in high-risk pregnancies, which supports steady class growth in the pregnancy medication market. Australia’s support for publicly funded fetal RhD genotyping illustrates a precision approach to maternal-fetal medicine and provides a model for resource stewardship in countries with similar payer structures. Southeast Asian health systems are adding diabetes and hypertension management capacity in ambulatory clinics and tertiary centers, which expands demand for antidiabetics, antihypertensives, and diagnostics. As coverage expands and clinical pathways standardize, the pregnancy medication market in the region is likely to sustain above-trend growth through 2031.

The Middle East is experiencing faster utilization growth in gestational diabetes therapy with clear recognition of elevated baseline risk, though reimbursement and formulary structures vary by country and payer mix. South America continues to adopt first-line obstetric pharmacology, while currency volatility challenges imported biologics procurement and nudges systems to support local manufacturing of essential oral therapies. Sub-Saharan Africa carries the highest preterm birth burden, and WHO guidance emphasizes that antenatal corticosteroids should be used where accurate gestational age dating and neonatal support are available to ensure net benefit. As infrastructure and workforce training improve, demand for time-sensitive maternal medications and monitoring is expected to grow in regional referral centers, reinforcing evidence-based pathways within the pregnancy medication market.

Competitive Landscape

The pregnancy medication market combines fragmented outpatient oral corridors with concentrated biologics corridors that rely on limited donor pools and capital-intensive manufacturing. Kedrion’s EUR 150 million investment to expand plasma fractionation capacity in Tuscany exemplifies the long timelines and high capital needs that shape immunoglobulin supply through the end of the decade. Company-reported revenues and EBITDA from 2024 indicate scaled operations across plasma-derived products and reinforce the connection between donor reliability and anti-D supply stability in obstetric care. Grifols and CSL face similar donor and capacity constraints, which is why stewardship guidance prioritizing postpartum prophylaxis remains essential during shortages. These supply realities support precision diagnostics and targeted dosing strategies that reduce waste and protect the highest-value use cases across the pregnancy medication market.

Analog insulin leaders reinforce their positions with comparative evidence that supports glycemic control without additional safety risk in pregnancy, which can guide formulary preference and payer alignment. Integrated care systems like Kaiser Permanente embed updated safety and adherence data into guidelines that favor insulin glargine

Pregnancy Medication Industry Leaders

Ferring

Abbott Laboratories

Besins Healthcare Monaco S.A.M

CSL

Kedrion

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Tandem Diabetes Care obtained expanded FDA clearance for its Control-IQ+ automated insulin delivery (AID) technology, enabling its application in managing pregnancies complicated by type 1 diabetes mellitus.

- December 2024: Accord Healthcare, Inc. launched clomiphene tablets, the generic equivalent of CLOMID (clomiphene citrate), further expanding its women’s health portfolio. The product is indicated for the treatment of ovulatory dysfunction in women seeking pregnancy.

Global Pregnancy Medication Market Report Scope

The pregnancy medication market refers to the segment of the pharmaceutical industry focused on drugs and therapies indicated for use during pregnancy to manage maternal conditions, pregnancy‑related complications, and fetal health.

The pregnancy medication market is segmented by drug class, indication, route of administration, and distribution channel. By drug class, the market includes antiemetics, antihypertensives, antidiabetics, anticoagulants, tocolytics, progesterone therapies, immunoglobulins, corticosteroids, and other drug classes, such as pregnancy‑compatible anti‑infectives and hematological agents. By indication, the market is categorized into nausea and vomiting of pregnancy (NVP), hypertensive disorders of pregnancy, Rh immunoprophylaxis (anti‑D therapy), preterm labor management, gestational diabetes management, infection management, and other indications, including threatened miscarriage and venous thromboembolism. Additionally, by route of administration, the market is segmented into oral, parenteral (intravenous, intramuscular, and subcutaneous), vaginal routes of administration, and others.

Furthermore, the distribution channel of the pregnancy medication market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Antiemetics |

| Antihypertensives |

| Antidiabetics |

| Anticoagulants |

| Tocolytics |

| Progesterone therapies |

| Immunoglobulins |

| Corticosteroids |

| Others (Anti-infectives, Hematological Agents) |

| Nausea & Vomiting of Pregnancy (NVP) |

| Hypertensive Disorders of Pregnancy |

| Rh Immunoprophylaxis (Anti-D) |

| Preterm Labor Management |

| Gestational Diabetes Management |

| Infection Management |

| Others (Threatened Miscarriage, Venous Thromboembolism) |

| Oral |

| Parenteral (IV/IM/Subcutaneous) |

| Vaginal |

| Other Route of Administrations |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Antiemetics | |

| Antihypertensives | ||

| Antidiabetics | ||

| Anticoagulants | ||

| Tocolytics | ||

| Progesterone therapies | ||

| Immunoglobulins | ||

| Corticosteroids | ||

| Others (Anti-infectives, Hematological Agents) | ||

| By Indication | Nausea & Vomiting of Pregnancy (NVP) | |

| Hypertensive Disorders of Pregnancy | ||

| Rh Immunoprophylaxis (Anti-D) | ||

| Preterm Labor Management | ||

| Gestational Diabetes Management | ||

| Infection Management | ||

| Others (Threatened Miscarriage, Venous Thromboembolism) | ||

| By Route of Administration | Oral | |

| Parenteral (IV/IM/Subcutaneous) | ||

| Vaginal | ||

| Other Route of Administrations | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the pregnancy medication market size and expected growth to 2031?

The pregnancy medication market size was USD 49.58 billion in 2025 and is projected to reach USD 71.22 billion by 2031 at a 6.5% CAGR over 2026-2031.

Which therapeutic classes are leading and which are growing fastest?

Antiemetics led with 22.45% revenue share in 2025, while antidiabetics are forecast to grow at 9.03% CAGR through 2031 as gestational diabetes prevalence rises.

How are guidelines reshaping demand in the pregnancy medication market?

WHO limits tocolysis to a 48-hour window, ACOG and others back low-dose aspirin for high-risk women, and biomarker-led triage with PlGF reduces unnecessary hospitalizations, concentrating use in proven pathways.

Which regions present the strongest growth prospects?

Asia-Pacific shows the fastest expansion at a 7.69% projected CAGR through 2031, driven by rising gestational diabetes prevalence and improving maternal health infrastructure.

How are supply constraints influencing product strategies?

Ongoing anti-D immunoglobulin shortages have encouraged targeted use via non-invasive fetal RhD genotyping and catalyzed capacity investments in plasma fractionation, shaping allocation and procurement.

What channel dynamics matter most near term?

Retail pharmacies remain the largest channel at 55.32% of 2025 distribution, but hospital pharmacies are growing at 7.22% CAGR through 2031 due to acute protocols for severe hypertension and preterm labor care.

Page last updated on: