Prefilled Formalin Vials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 468.52 Million |

| Market Size (2031) | USD 582.78 Million |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prefilled Formalin Vials Market Analysis by Mordor Intelligence

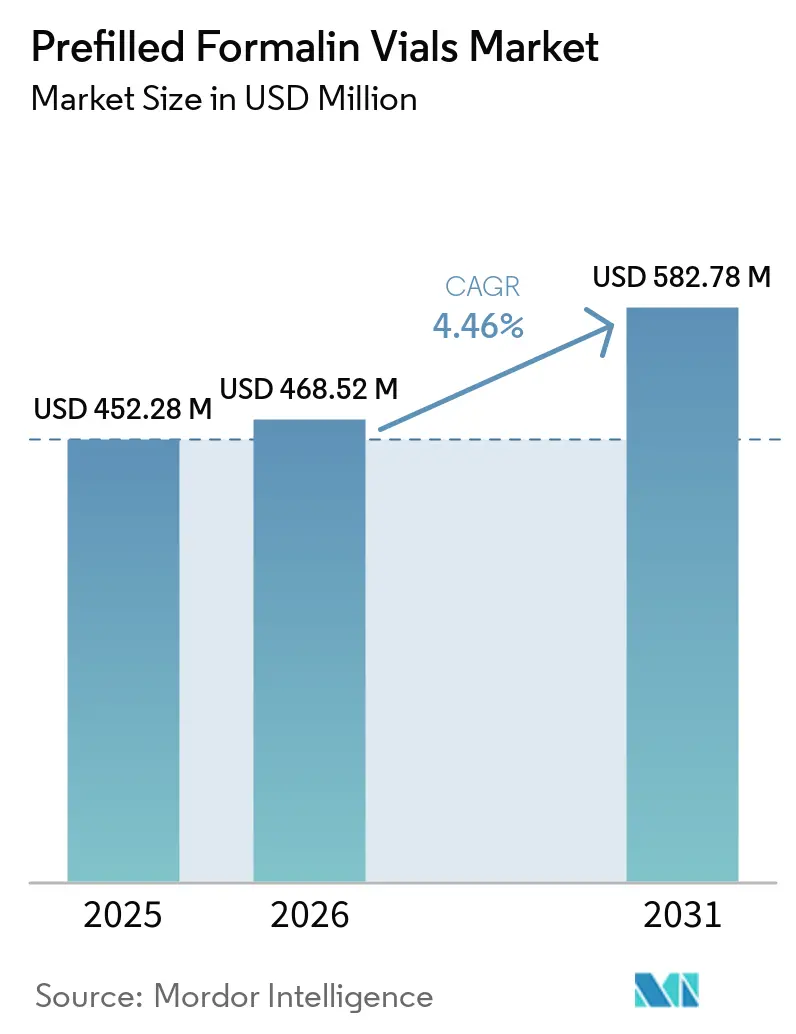

The Prefilled Formalin Vials Market size is expected to increase from USD 452.28 million in 2025 to USD 468.52 million in 2026 and reach USD 582.78 million by 2031, growing at a CAGR of 4.46% over 2026-2031.

Growth reflects steady expansion in diagnostic biopsy volumes, persistent use of 10% neutral buffered formalin in routine histopathology, and a higher premium on closed, compliant containers within digitized laboratories. The prefilled formalin vials market also aligns with pathology’s shift toward standardization and chain-of-custody improvements that reduce labeling risk across high-acuity oncology workflows. Intensifying exposure standards in the United States and the European Union are reinforcing the utility of sealed and pressure-tested vials that limit vapor release during handling and shipment. The prefilled formalin vials market is further supported by long-standing clinical validation of formalin-based fixation in regulated diagnostic settings, even as formalin-free options gain visibility in research environments that prioritize nucleic acid integrity. Long-term cancer incidence projections indicate that specimen volumes will continue to rise, which underpins durable demand for prefilled containers used at the point of tissue collection and transport

Key Report Takeaways

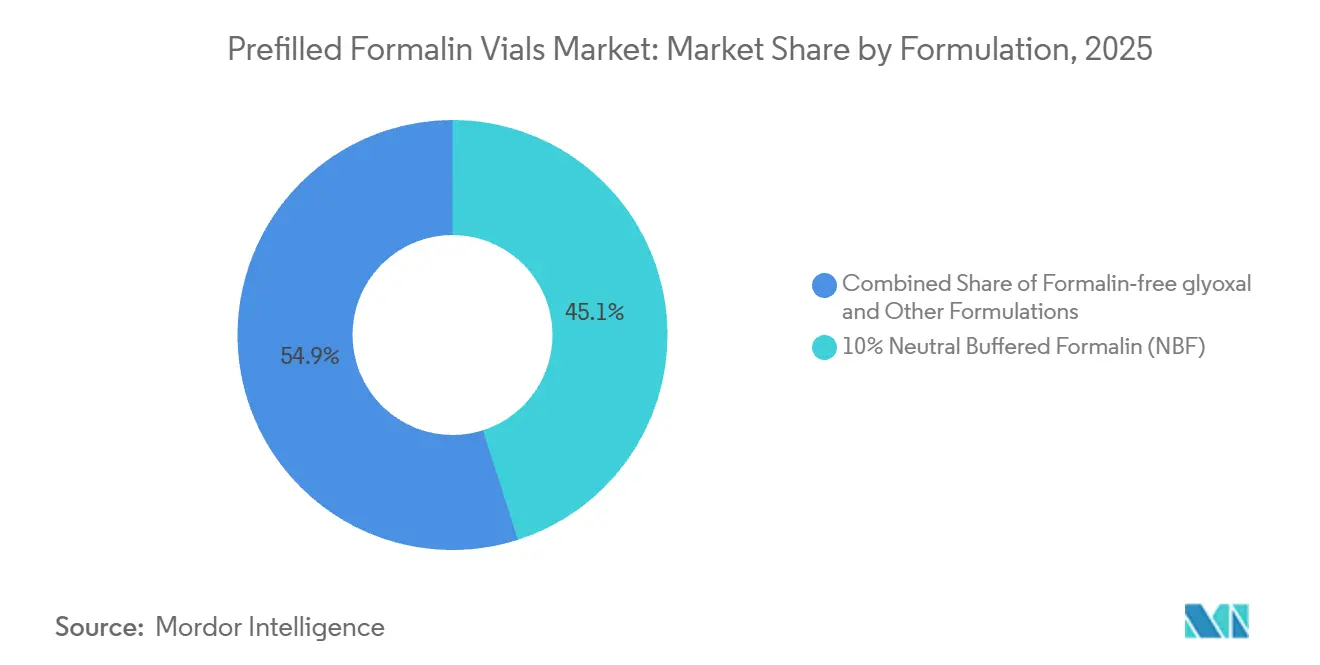

By formulation, 10% neutral buffered formalin held 68.24% of the prefilled formalin vials market share in 2025, while formalin-free glyoxal and alternative fixatives recorded the highest projected growth at 4.88% CAGR through 2031.

By volume, 20–40 mL vials accounted for 32% in 2025, and the 90–500 mL range is projected to expand at a 4.95% CAGR over 2026–2031.

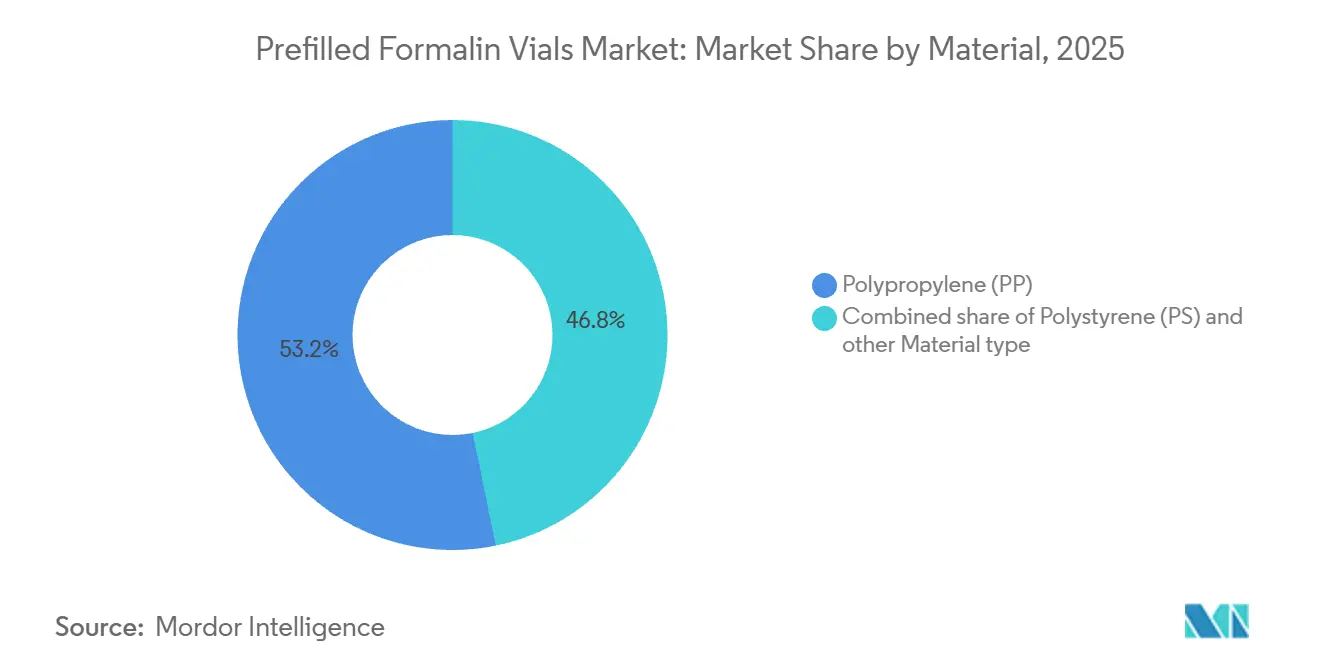

By material, polypropylene captured 53.23% in 2025, and polystyrene is forecast as the fastest growing at 4.76% CAGR through 2031.

By end user, hospitals and surgical centers held 44.65% in 2025, while diagnostic laboratories are expected to advance at 5.10% CAGR through 2031.

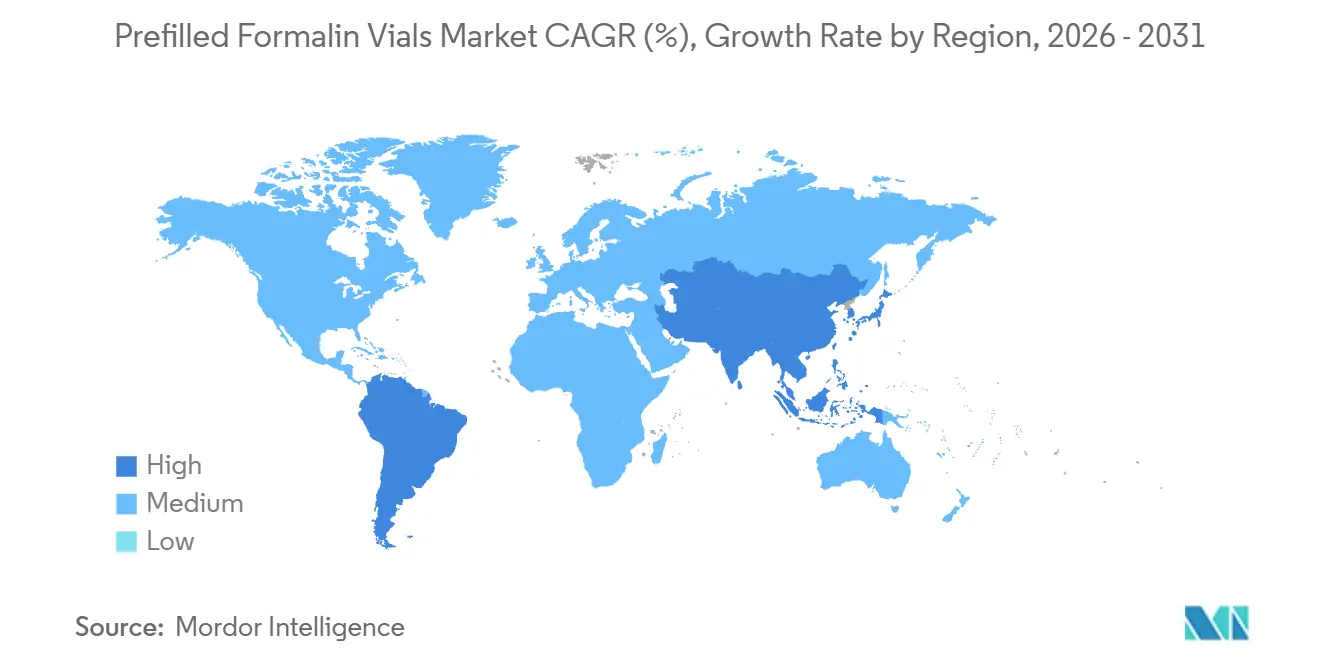

By geography, North America led with 41.13% in 2025, while the Asia Pacific is projected to grow at 5.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Prefilled Formalin Vials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising biopsy volumes and cancer incidence lift pre-analytical fixative demand | +1.8% | Global, with concentration in Asia Pacific, Europe, North America | Medium term (2-4 years) |

| Stricter formaldehyde exposure rules push adoption of closed, prefilled containers | +1.2% | North America, EU, Asia Pacific | Short term (≤ 2 years) |

| Standardized 10% NBF fixation reduces errors and rework in histopathology | +0.9% | Global; CAP-accredited and ISO 15189 facilities | Long term (≥ 4 years) |

| Hospital workflow digitization favors pre-barcoded, LIS-ready vials | +0.7% | North America core, Europe, and select Middle East systems | Medium term (2-4 years) |

| 95 kPa/air-transport and pneumatic tube compliance standardizes container specs | +0.6% | North America and Europe emphasize, Asia Pacific reference-lab networks | Short term (≤ 2 years) |

| Cold-chain resilience via alcoholic NBF variants expands use in colder regions | +0.4% | Northern Europe, Canada, northern China, and Russia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Biopsy Volumes and Cancer Incidence Lift Pre-Analytical Fixative Demand

Global cancer incidence is projected to reach 35 million annual diagnoses by 2050, which will sustain the need for reliable tissue fixation at the point of collection and transport[1]International Agency for Research on Cancer, “Global Cancer Burden Growing, Amidst Mounting Need for Services". Increased case complexity around precision oncology adds pressure on pre-analytical quality, reinforcing the entrenched use of 10% neutral buffered formalin and sealed primary containers that stabilize specimens during handoffs. The prefilled formalin vials market benefits from this demand because each biopsy must enter fixative rapidly to protect morphology and downstream testing performance under standardized timelines. Shifts in tumor subtype patterns, such as the broad prominence of lung adenocarcinoma, elevate the volume of slides and ancillary testing, which indirectly promotes higher vial throughput per case in busy centers. Rising breast cancer incidence adds further volume in core biopsy pathways and sentinel node protocols that favor consistent prefilled container formats across multi-site hospital systems by reducing labeling variability and handling steps. As incidence grows fastest in lower-resourced regions, large reference networks and public programs will likely standardize container SKUs to manage training and quality at scale, which supports continued growth in the prefilled formalin vials market.

Stricter Formaldehyde Exposure Rules Push Adoption of Closed, Prefilled Containers

In 2025, the United States Environmental Protection Agency updated its risk analysis for formaldehyde and lowered the acute inhalation point-of-departure to 0.3 ppm, narrowing the safety margin for indoor environments where specimen handling occurs. European policy continues to tighten as CLP amendments sharpen carcinogenic classification and labeling, which encourages laboratories to couple safer handling with digital documentation and compliance-ready packaging by the middle of the decade. These changes drive purchasing toward closed, prefilled containers that minimize pouring and reduce vapor peaks during accessioning and grossing, a trend most visible in larger systems that manage centralized quality processes. IATA packaging requirements for clinical specimens in transport reinforce a sealed-container default for inter-facility movement and regional send-outs, which consolidates buyers on pressure-rated options At the same time, hospitals using enterprise laboratory information systems align on pre-barcoded vials that integrate with scanning workflows to shrink open-container steps in specimen rooms, improving both exposure control and identification accuracy. The net effect is a steady shift toward premium, sealed, and transport-ready products that differentiate on compliance and integration rather than commodity pricing, which supports the long-run expansion of the prefilled formalin vials market.

Standardized 10% NBF Fixation Reduces Errors, and Rework in Histopathology

Updated College of American Pathologists materials and protocols maintain 10% neutral buffered formalin as the reference fixative for regulated oncology workflows, which anchors purchasing to the most validated chemistry in surgical pathology. Evidence-based guidance on DNA and RNA extraction from FFPE biospecimens sets practical limits for fixation durations that sustain downstream assay performance, which strengthens adherence to standard fixative and handling steps. CAP’s 2024 immunohistochemistry validation update requires separate analytic validation when labs change fixation methods, which raises the procedural bar for switching away from formalin and increases the value of quality-assured prefilled options that track fixation conditions cleanly. European biobanking recommendations to optimize fixation time for nucleic acid preservation are also catalyzing demand for time-aware workflows and labeled containers that document exposure intervals, which complement formalin’s role in core diagnostic pathways. Across routine oncology, consistent fixation chemistry supports predictable staining and molecular profiling, which lowers rework and fosters procurement patterns that emphasize barcode-native, closed vials that can be logged automatically into lab systems. These dynamics continue to reinforce the central position of formalin-based products inside the prefilled formalin vials market.

Hospital Workflow Digitization Favors Pre-Barcoded, LIS-Ready Vials

Large commercial and academic centers are scaling digital pathology platforms that integrate AI-enabled case triage and image management, which increases the operational value of pre-barcoded vials that reduce relabeling, scanning errors, and manual entry. Pre-barcoded and GS1-ready labels on primary containers link patient identifiers to downstream slides and images inside end-to-end systems, which streamlines case setup and throughput in high-volume settings. Purpose-built barcode tracking applications further reduce transcription errors in accessioning and cassetting, creating an ecosystem effect where LIS settings and container specifications evolve together. With image-based review scaling, the consistency of vial dimensions and transparency features matters for pre-scan visual checks and scanning automation, driving preference for container families that integrate with digital workflows. As these systems expand across multi-site networks and reference labs, procurement consolidates around containers that meet barcode, LIS, and transport standards together, which supports premiumization within the prefilled formalin vials market. These operational dependencies increase switching costs away from standardized, integrated containers that have already cleared validation inside digital pathology chains.

Restraints Impact Analysis*

| Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carcinogenic hazard classification of formaldehyde increases handling burdens | -0.8% | Global; stricter in EU, United States, Japan | Medium term (2-4 years) |

| Shift to formalin-free or low-formaldehyde fixatives in select labs | -0.5% | Europe, North America, limited Asia Pacific | Long term (≥ 4 years) |

| Hazardous waste fees and spill/liability risks raise lifecycle costs | -0.4% | North America, EU, select United States states | Medium term (2-4 years) |

| Fragmented procurement and GPO contracting limit premium pricing | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carcinogenic Hazard Classification of Formaldehyde Increases Handling Burdens

Formaldehyde’s Group 1 carcinogenic classification continues to shape labeling, storage, and exposure-control requirements that elevate compliance workloads in clinical laboratories. In the United States, evolving risk evaluations reflected in late 2025 updates raise attention on short-term and chronic exposure thresholds across healthcare facilities handling fixatives[2]United States Environmental Protection Agency, “Formaldehyde; Updated Draft Risk Calculation Memorandum” . In Europe, amendments to classification, labeling, and packaging rules codified tighter carcinogen and mutagen hazard statements with related documentation, which adds packaging and training steps for any product that contains formaldehyde. These requirements encourage moves to closed, clearly labeled, and digitally tracked primary containers that reduce ambient vapor peaks and simplify audits, but they also add cost for suppliers and customers that must validate new formats. As standards become more prescriptive, procurement teams scrutinize seal integrity, pressure ratings, and label content together, which can slow specification changes and temper near-term price realization. This creates a measured headwind for the prefilled formalin vials market, even as compliance-ready designs mitigate exposure risks in routine workflows.

Shift to Formalin-Free or Low-Formaldehyde Fixatives in Select Labs

Formalin-free pathways using supercritical CO2 show strong gains in nucleic acid integrity and avoid fixation-induced artifacts, which aligns with translational research and certain precision oncology workflows outside core clinical protocols. Follow-on studies in 2026 confirmed high success rates across histochemistry and immunohistochemistry panels using non-formalin tissue processing, which strengthens the technical case for targeted adoption in research and specialized labs. Glyoxal-based fixatives have also been evaluated, although specific tissue contexts, such as retina, raised challenges in maintaining structural integrity and signal quality across selected assays, which has limited diagnostic uptake so far. At the same time, CAP’s 2024 immunohistochemistry validation requirements add new steps when switching fixatives, which raises practical barriers for wholesale migrations in clinical environments that maintain large antibody menus. These trends indicate a dual-track reality where formalin-free processing scales within research and biobanking, while formalin-based fixation remains dominant inside regulated diagnostic chains. The result for the prefilled formalin vials market is a persistent substitution headwind in research tiers, counterbalanced by continued reliance on formalin in routine surgical pathology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Formulation: 10% NBF Remains Entrenched While Alternatives Gain Research Traction

10% neutral buffered formalin accounted for 45.08% in 2025 within the prefilled formalin vials market, reinforcing its role as the reference chemistry for regulated oncology workflows that rely on consistent morphology and validated IHC panels. The weight of accreditation practices and biospecimen guidance sustains demand for 10% NBF in hospitals and independent pathology groups that must meet repeatable diagnostic performance across high-volume case mixes. European biobanking recommendations to safeguard DNA for sequencing reinforce tighter control of fixation times, which increases the appeal of containers and labels that support time-aware logging and standardized processing. These operational needs keep prefilled, sealed options at the center of lab workflows where chain-of-custody accuracy is critical for oncology and transplant specimens. The prefilled formalin vials market therefore exhibits steady preference for established fixative chemistry and barcode-native packaging in clinical channels, even as procurement teams evaluate enhanced features like pressure testing for air and tube transport.

Formalin-free glyoxal and supercritical CO2 modalities are projected to grow at 4.88% CAGR through 2031, reflecting strong use cases in research and some translational pipelines that prioritize nucleic acid preservation and artifact-free sequencing. Studies demonstrate that non-formalin processing can deliver high-quality DNA with no fixation-induced artifacts while maintaining a wide panel of histochemical and IHC stains, which encourages adoption in biobanks and academic centers. Diagnostic settings continue to emphasize the reproducibility and validation depth associated with formalin-fixed tissue, especially under accreditation and proficiency-testing regimes where assay changes trigger new validation steps. As a result, alternative fixatives expand mostly in non-routine or research contexts, while 10% NBF remains embedded in core clinical use. This dynamic supports incremental growth at the innovative edges without displacing the large installed base that anchors the prefilled formalin vials market.

By Volume per Container: Larger Formats Track Complex Surgeries and Reference Send-Outs

20–40 mL vials captured 32% in 2025 due to alignment with common biopsy sizes and the long-standing 10:1 formalin to tissue ratio employed in routine surgical pathology. Standard operating procedures rely on this ratio to stabilize tissue consistently across a wide range of sample types, which makes 20–40 mL a versatile default in hospitals and integrated delivery networks. The prefilled formalin vials market remains balanced around these midrange capacities because they support common specimens while keeping shipping weight and volume manageable during inter-facility transfers. Demand for larger formats emerges from resections and transplant cases that require higher formalin volumes to achieve proper tissue penetration during initial fixation. This variety sustains a full line of SKUs across specimen sizes, which also assists quality teams in matching container choices to case complexity.

The 90–500 mL tier is projected to expand at 4.95% CAGR as reference centers and surgery programs process larger tissue blocks that benefit from container headspace and secure closures during transport. Air and pneumatic tube transport rules influence procurement of those larger containers since 95 kPa pressure performance and triple-packaging readiness enable safer movement without leakage. Studies on pneumatic tube systems highlight the importance of robust primary containers to minimize transport-induced specimen damage, which raises the value of pressure-capable designs. As hospitals step up regional send-outs for subspecialty second opinions, the preference for dual-purpose containers that satisfy both fixation and transport needs strengthens. This convergence supports premiumization inside the prefilled formalin vials market, where container performance and compliance matter as much as fixative chemistry.

By Material: PP Leads on Sterilization Durability While PS Supports Visual Checks in Digital Workflows

Polypropylene accounted for 53.23% in 2025 due to its sterilization tolerance, chemical resistance, and compatibility with common healthcare cleaning and reuse protocols in controlled training and teaching environments PP’s thermal properties allow reliable performance through typical decontamination cycles and align with medical-grade plastic guidelines followed by hospital buyers. Chemical resistance tables support the use of compatible polyolefins for aldehyde-containing solutions, which explains PP’s role in long-hold storage of formalin-based fixatives. This material’s resilience under handling stress also suits pneumatic tube transfer where container integrity is important to avoid leaks that could disrupt sample chains. Institutional preferences for reliable and durable substrates sustain PP’s lead position in the prefilled formalin vials market where total cost of ownership and error avoidance outweigh marginal material savings. These advantages underpin stable demand profiles across hospital and independent laboratory buyers that require consistent performance over long-term contracts.

Polystyrene is projected as the fastest-growing substrate at 4.76% CAGR, driven by use cases that favor higher optical clarity to support pre-scan specimen checks in digital workflows without breaching seals. Digital pathology adoption incentivizes uniform, transparent walls that allow staff to inspect tissue condition and position quickly at accessioning and before scanning, which reduces unnecessary handling. In parallel, container families that marry clarity with secure closures and barcode-ready surfaces appeal to enterprise LIS deployments that prize consistent dimensions and fast scanning. Facilities with high send-out volumes also segment material choice by use case, retaining PP for maximum ruggedness in transport pathways while leveraging PS for visibility in image-led review. The prefilled formalin vials market, therefore, accommodates both material paths, while procurement consolidates around suppliers able to offer full lines that pass transport and labeling requirements. Through 2031, adoption patterns reflect the expanding role of digital workflows in container selection and the persistent baseline need for rugged primary containment in specimen logistics.

By End User: Diagnostic Labs Scale Fast as Digital and CGP Volumes

Rise Hospitals and surgical centers held 44.65% in 2025 as the primary origination points for tissue specimens and as the largest adopters of standardized prefilled vials to streamline operating room to lab handoffs. Standard fixation and labeling across perioperative kits and pathology receiving improves traceability, which supports high compliance across inpatient and ambulatory surgery networks. Evidence-based practices for FFPE processing are widely implemented in hospital laboratories, which reinforces entrenched use of formalin and simple, labeled containers that fit existing workflows. Chain-of-custody options such as RFID and barcode systems further reduce identification risk, and they work best when primary containers integrate standard labels and surfaces designed for quick scanning. Hospitals continue to invest in digital pathology pilots, which encourages harmonized container specifications that align with slide scanners and LIS barcode settings, and that sustains the prefilled formalin vials market in core clinical channels.

Diagnostic laboratories are projected to grow at 5.10% CAGR through 2031 as large reference networks expand digital capabilities, automate triage, and integrate AI for artifact detection and expedited review. These labs favor pre-barcoded and sealed containers that reduce ambient exposure and standardize metadata capture when specimens arrive for processing in regional hubs. Integration with barcode tracking platforms and laboratory information management systems creates savings in time and rework, which justifies paying for premium, compliant vials over generic alternatives. As oncology testing volumes rise and comprehensive genomic profiling workflows demand controlled fixation windows, an emphasis on pre-analytical quality elevates container specification decisions. Together, these requirements uphold steady adoption in independent and hospital-affiliated diagnostics as digital pathology spreads, reinforcing the mid-single-digit expansion profile visible in the prefilled formalin vials market.

Geography Analysis

North America led with 41.13% in 2025, based on embedded formalin workflows inside accredited laboratories and fast adoption of digital pathology across commercial and academic networks. The prefilled formalin vials market benefits in this region from consistent fixation practices, routine use of pre-barcoded containers, and alignment with LIS settings that automate accessioning data. Commercial reference networks are scaling AI-enabled platforms that reinforce container standardization for scanning and case routing, which supports premium sealed vials that link to image management and reporting systems. Hospital systems emphasize chain-of-custody and error reduction during high-throughput case days, which favors RFID and barcode-ready designs linked to digital logs. IATA transport standards add another layer that encourages pressure-tested vials for inter-facility movement, including regional shipping to subspecialty consult services. Policy attention to exposure thresholds in the United States also sustains movement toward sealed, compliant primary containers that reduce vapor release in handling rooms, which in turn supports higher-value products inside the prefilled formalin vials market.

Asia Pacific is projected as the fastest-growing region at 5.55% CAGR due to expanding screening programs and rising oncology incidence, which translates into more biopsies moving through hospitals and reference labs. China had about 2.7 million new cancer cases were men and about 2.5 million were women in 2024, and rising volumes across populous countries create continuous demand for fixatives and compliant primary containers in point-of-care and centralized workflows. As networked labs scale operations across national systems, procurement tends to consolidate on validated SKUs that simplify training and supply management across distributed sites. Digitization initiatives across leading centers promote the adoption of pre-barcoded vials for accurate intake and linking to image pipelines. Transport standards and rising use of pneumatic tube systems inside large hospitals also elevate the value of pressure-capable containers that perform predictably during shipment and internal movement [3]Frontiers in Physiology, “Navigating Preanalytical Challenges: A Real World Study on Single Tube Pneumatic Tube Systems” . Combined with growing investment in oncology infrastructure, these forces support expanding demand for sealed and compliant products within the prefilled formalin vials market.

Europe maintains a significant share as labs adhere to ISO-driven quality systems, expand digital pathology capabilities, and respond to incremental policy tightening on hazard classification and labeling. Biobanking leaders are also testing non-formalin processing to improve nucleic acid preservation, which nudges research inventories toward alternative fixation pathways without altering clinical protocols at scale. IATA’s packaging requirements for biological specimens continue to align with hospital and reference lab practices across the region, which keeps pressure-tested and sealed primary containers top of mind in procurement. As digital adoption spreads and transport rules converge, buyers favor container families that reduce exposure, automate label capture, and pass inter-facility shipping checks. These conditions sustain broad demand for prefilled, sealed vials in clinical channels while research growth diversifies fixative mix at the margins of the prefilled formalin vials market.

Competitive Landscape

The prefilled formalin vials market remains moderately fragmented, with the top five suppliers holding an estimated 38–42% in 2025 based on consolidated hospital and reference lab procurement patterns. Competitive dynamics hinge on integration rather than commodity chemistry, as vendors differentiate through barcode-native surfaces, transport-ready seals, and links to specimen tracking platforms. Leica Biosystems’ CEREBRO ecosystem underscores a focus on chain-of-custody and identification accuracy that resonates with oncology centers seeking to minimize pre-analytical risk. Digital pathology is another lever for bundling and loyalty, where companies cross-sell scanners, software, cassettes, and vials to embed customers inside integrated platforms. Epredia’s award-winning digital scanner performance illustrates the momentum behind image-led workflows that reward vendors who can link consumables with instrumentation and software. Collectively, these moves increase the value of validated, closed vials that scan reliably and ship safely.

Vertical integration into tissue processors and embedding centers strengthens positions for suppliers that can pair equipment financing with long-term consumable commitments. StatLab’s United States launch of Diapath instruments demonstrates a portfolio approach that aligns capital equipment with daily-use plastics and reagents across the histology workflow. Transport-ready primary containers also differentiate on pressure performance and leakage prevention in shipping, which aligns with IATA’s packaging standards for biological specimens. Vendors that validate 95 kPa performance and triple-packaging compatibility gain an edge on compliance, especially for customers consolidating send-outs to regional subspecialty centers. Larger buyers prefer single-source kits and libraries that maintain consistent geometry and label read rates, which magnifies advantages for suppliers with depth across SKUs. These combined elements continue to shape competition in the prefilled formalin vials market as buyers lean into workflow reliability and audit-ready documentation.

Enterprise digital platforms shift case mix and throughput economics, prompting laboratories to pay premiums for containers that cut relabeling steps and improve scan-line flow. Large networks that deploy AI-assisted case triage rely on consistent primary container formats to stabilize image quality and support benchmarks around turnaround time. As reference labs scale, favored configurations encompass sealed, barcode-native vials with verified transport performance to reduce failure risk during inter-facility shipments and internal tube transport. Company portfolios that join these features with digital tracking stacks and LIS connectivity continue to gain traction in multi-site procurements. Across 2026, the prefilled formalin vials market reflects this pivot away from standalone commodities toward containers embedded in broader digital and regulatory compliance architectures.

Prefilled Formalin Vials Industry Leaders

Epredia (Richard‑Allan Scientific)

Leica Biosystems

StatLab Medical Products

Cardinal Health

Avantor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Labcorp expanded its collaboration with PathAI to deploy the FDA-cleared AISight Dx digital pathology platform across Labcorp's national anatomic pathology laboratory network and hospital partnerships. The cloud-based system integrates AI-powered tools such as TumorDetect and ArtifactDetect to accelerate case turnaround and support precision-medicine products, building on Labcorp's 2019 strategic investment in PathAI. This deployment is expected to process over 750,000 digital slides annually by Q4 2026, cementing Labcorp's position as the largest commercial digital-pathology operator in North America.

- September 2025: Epredia's E1000 Dx Digital Pathology Solution won three categories (Quality 20x, Quality and High Throughput 40x) in the 2025 International Scanner Benchmark Awards from the Ecosystem for Pathology Diagnostics with AI Assistance (EMPAIA). The awards, announced at the 37th European Congress of Pathology in Vienna, validated the scanner's ability to create high-resolution digital images of up to 1,500 tissue samples daily, a critical metric for laboratories transitioning to AI-assisted diagnostic workflows.

- September 2025: StatLab Medical Products announced the United States commercial launch of Diapath signature instruments, including the Donatello Automated Tissue Processor (Series 3), Galileo Precision-Engineered Microtome (Series 2), and Dante Ergonomic Embedding Center. This fulfills StatLab's strategic vision following its August 2024 acquisition of Italy-based Diapath S.p.A., extending the company's reach from consumables into capital equipment and positioning it to offer end-to-end anatomic pathology solutions in United States markets.

- February 2024: The College of American Pathologists published updated guidance on the analytic validation of immunohistochemical (IHC) assays, requiring separate validation for each new analyte and fixation method when IHC is performed on cytologic specimens not fixed identically to tissues used for initial assay validation. The guideline, effective March 2025 for CAP accreditation, mandates a minimum of 10 positive and 10 negative cases per validation, raising compliance costs for laboratories adopting formalin-free fixatives.

Global Prefilled Formalin Vials Market Report Scope

| 10% Neutral Buffered Formalin (NBF) | 68% |

| Zinc Formalin (10%) | |

| Alcoholic NBF (5�10% alcohol) | |

| Formalin?free glyoxal or alternative fixatives |

| 10 mL |

| 10-20 mL |

| 20-40 mL |

| 40-60 mL |

| 60-90 mL |

| 90-500 mL |

| 500 mL-1 L |

| More than 1 L |

| Polypropylene (PP) |

| High?density polyethylene (HDPE) |

| Polystyrene (PS) |

| Hospitals & Surgical Centers |

| Diagnostic Laboratories |

| Anatomic Pathology/Histology Labs |

| Others (Forensic Laboratories, Academic & Research Institutes, among others) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| APAC | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Concentration/Formulation | 10% Neutral Buffered Formalin (NBF) | 68% |

| Zinc Formalin (10%) | ||

| Alcoholic NBF (5�10% alcohol) | ||

| Formalin?free glyoxal or alternative fixatives | ||

| By Volume per Container | 10 mL | |

| 10-20 mL | ||

| 20-40 mL | ||

| 40-60 mL | ||

| 60-90 mL | ||

| 90-500 mL | ||

| 500 mL-1 L | ||

| More than 1 L | ||

| By Material | Polypropylene (PP) | |

| High?density polyethylene (HDPE) | ||

| Polystyrene (PS) | ||

| By End User | Hospitals & Surgical Centers | |

| Diagnostic Laboratories | ||

| Anatomic Pathology/Histology Labs | ||

| Others (Forensic Laboratories, Academic & Research Institutes, among others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| APAC | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the prefilled formalin vials market size in 2026 and its growth outlook to 2031?

The prefilled formalin vials market size reached USD 452.28 million in 2026 and is projected to reach USD 582.78 million by 2031 at a 4.46% CAGR.

Which formulation category currently leads in this space?

10% neutral buffered formalin leads with 68.24% share in 2025 due to entrenched validation in regulated diagnostic workflows.

Which region leads and which grows the fastest through 2031?

North America leads with 41.13% in 2025, while Asia Pacific is projected to grow at 5.55% CAGR through 2031.

How are regulations shaping container specifications?

Tightening exposure and transport standards drive adoption of sealed, pressure-rated, and barcode-native vials that reduce vapor release and meet IATAs 95 kPa packaging requirements.

What role does digital pathology play in procurement decisions?

Enterprise digital platforms favor pre-barcoded vials with consistent geometry and label readability to reduce relabeling and speed accessioning and image workflows.

Which materials are most used and why?

Polypropylene leads for sterilization durability and chemical resistance, while polystyrene is favored for transparency in visual checks linked to digital workflows.

Page last updated on: