PPG Biosensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

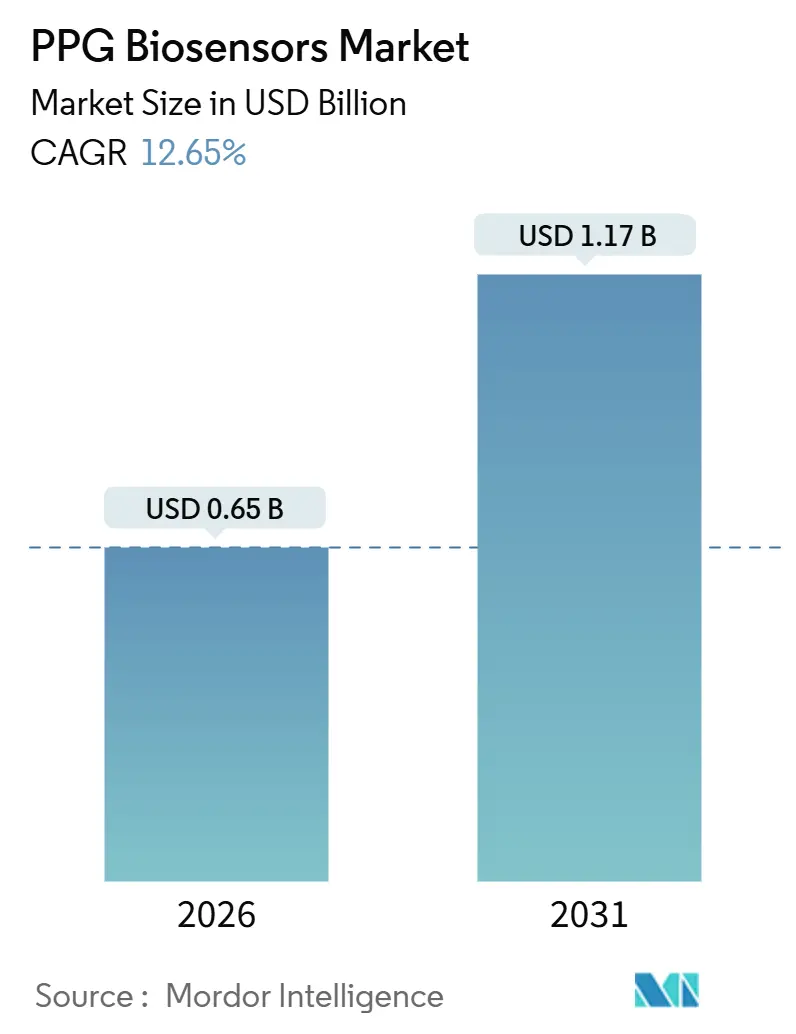

| Market Size (2026) | USD 0.65 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 12.65% CAGR |

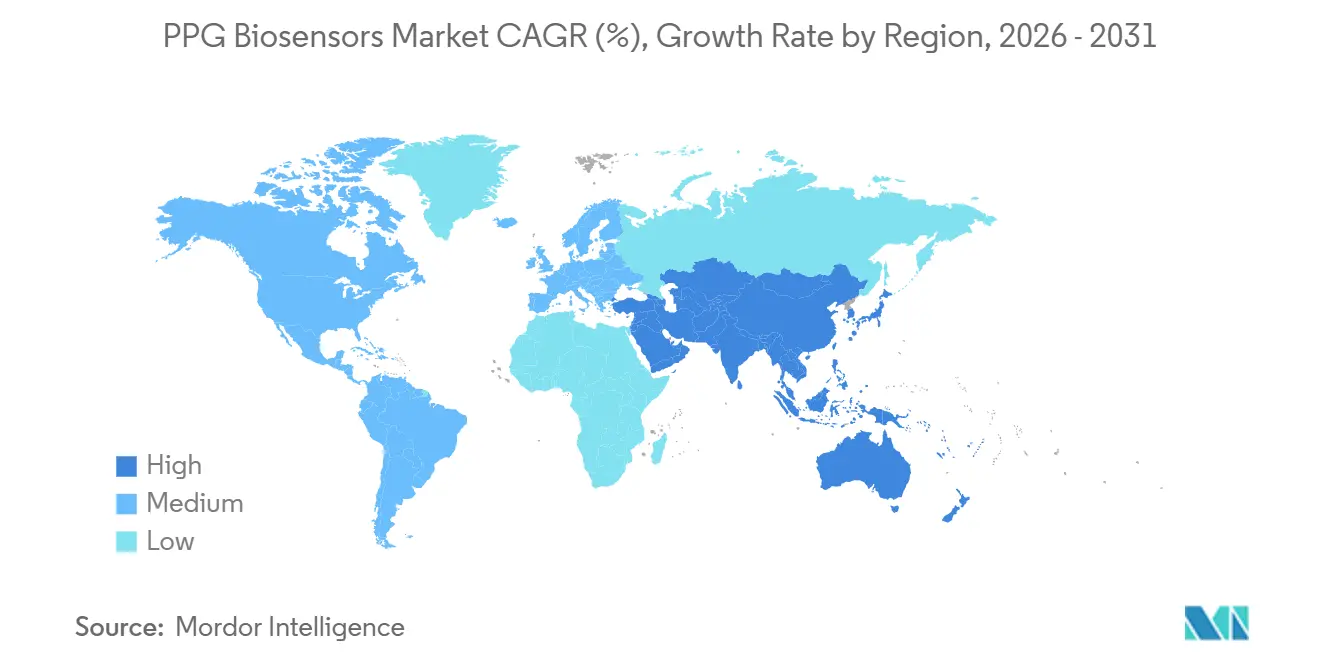

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

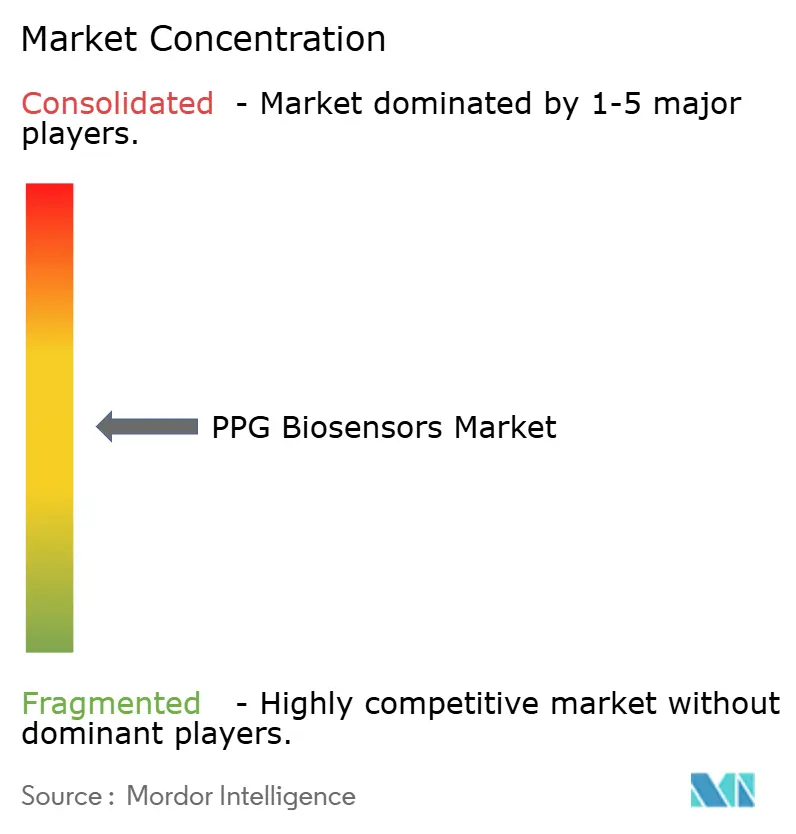

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

PPG Biosensors Market Analysis by Mordor Intelligence

The PPG Biosensors Market size is estimated at USD 0.65 billion in 2026, and is expected to reach USD 1.17 billion by 2031, at a CAGR of 12.65% during the forecast period (2026-2031).

Demand is being accelerated by fast-track regulatory clearance for digital therapeutics, cheaper ultra-low-power mixed-signal ASICs, and original-equipment installation of photoplethysmography modules in connected vehicles. Vendors that can combine sensor accuracy, seamless reimbursement workflows, and robust cybersecurity postures are positioned to capture share, while semiconductor design wins are consolidating around single-chip, multi-wavelength analog front-ends that cut bill-of-materials costs in half. Health-system adoption of remote patient-monitoring codes has locked in per-patient monthly reimbursement, creating predictable revenue for clinicians and sustained pull-through for device makers. Automotive tier-1 suppliers have begun embedding driver-wellness modules that feed telematics platforms, opening an ancillary channel for PPG Biosensors market penetration. Despite headwinds such as motion-artifact bias in darker skin tones and rising privacy-compliance costs, a virtuous cycle of longer battery life, richer longitudinal data, and more accurate AI algorithms continues to attract capital and talent.

Key Report Takeaways

- By product type, smart watches led with a 42.78% revenue share in 2025; smart wristbands are forecast to grow at a 13.64% CAGR to 2031.

- By application, heart-rate monitoring accounted for 46.07% of the PPG Biosensors market size in 2025, and blood pressure monitoring is advancing at a 13.88% CAGR through 2031.

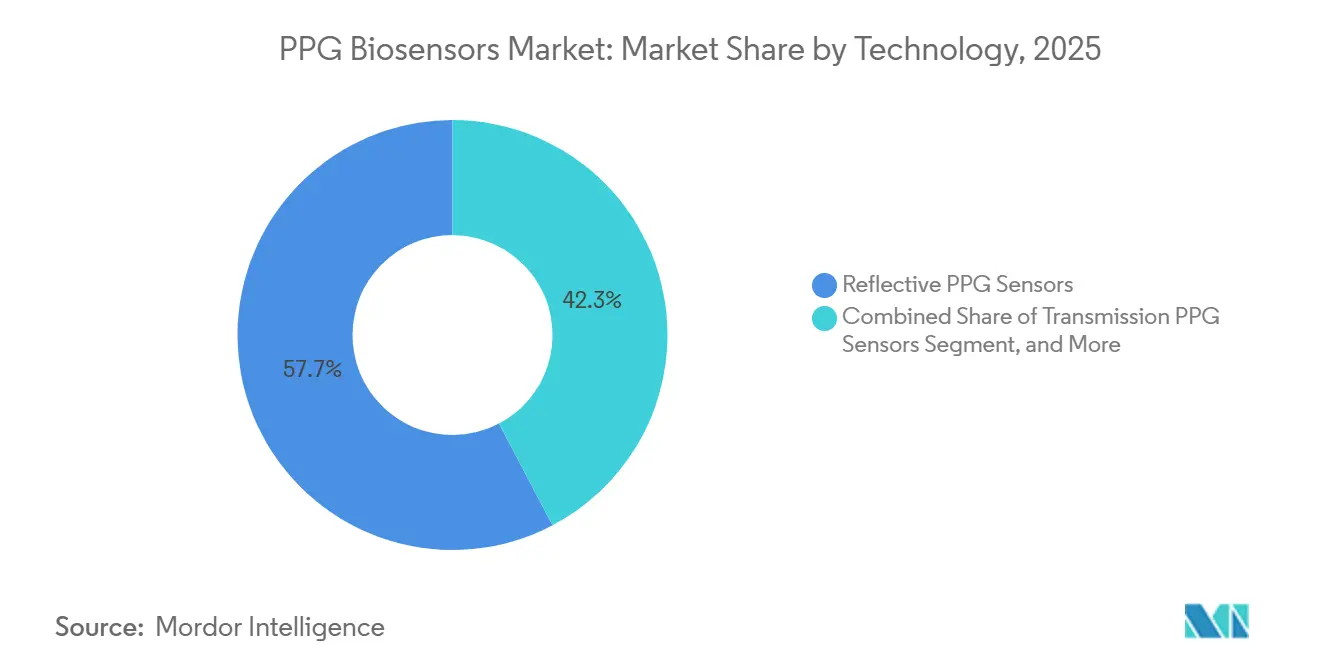

- By technology, reflective PPG sensors held 51.72% of the PPG Biosensors market share in 2025, while Multimodal PPG+ECG Sensors are expanding at a 15.28% CAGR to 2031.

- By geography, North America held a 38.89% share in 2025; Asia-Pacific is the fastest-growing region at a 16.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global PPG Biosensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Wearable Health-Monitoring Devices | +2.5% | Global, with highest penetration in North America and Western Europe | Medium term (2-4 years) |

| Growth of Remote-Patient-Monitoring Programs Post-COVID-19 | +2.0% | North America and EU, expanding to APAC urban centers | Short term (≤ 2 years) |

| Advancements in Multi-Wavelength & AI-Enabled PPG Algorithms | +1.8% | Global, led by R&D hubs in US, China, and Israel | Long term (≥ 4 years) |

| Regulatory Fast-Track Pathways for Digital Therapeutics | +1.5% | North America (FDA TEMPO pilot), EU (CE Mark streamlining) | Medium term (2-4 years) |

| Ultra-Low-Power ASICs Reducing BOM Cost | +1.2% | Global, with manufacturing concentrated in Taiwan, South Korea, and Germany | Short term (≤ 2 years) |

| Automotive In-Cabin PPG Modules for Safety & Insurance Telematics | +0.8% | North America, EU, and China (OEM adoption) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Wearable Health-Monitoring Devices

Consumer demand has broadened from fitness enthusiasts to chronic-disease patients, enlarging the addressable base for the PPG Biosensors market and lifting average selling prices. Samsung’s Galaxy Watch 7 received FDA clearance for atrial fibrillation detection in 2024, validating consumer hardware as an adjunctive diagnostic.[1]Samsung Electronics, “Galaxy Watch 7 Launch,” samsung.com Garmin’s Fenix 8 pushed PPG-derived VO₂ max metrics into expedition-grade devices favored by endurance athletes, proving that accuracy and ruggedization can coexist. Oura Ring 4 addressed earlier bias concerns by dynamically optimizing LED placement to maintain signal quality across diverse skin tones. The American Heart Association highlighted the need for diverse data sets in algorithm development, an impetus for vendors to scale real-world evidence collection. Masimo’s FDA-cleared W1 offers a parallel premium tier for clinicians who require medical-grade accuracy and are willing to pay a premium.

Growth of Remote-Patient-Monitoring Programs Post-COVID-19

Permanent reimbursement codes 99453-99458 now guarantee per-patient payments for PPG-derived physiological data, turning remote monitoring from a pilot initiative into standard care.[2]Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule,” cms.gov The FDA’s TEMPO pilot is shortening review times for devices that demonstrate FHIR interoperability, enabling vendors to iterate on hardware and software updates within a single fiscal year. Peerbridge’s Cor monitor pairs PPG sensors with multi-channel ECG to deliver QT interval data, and a Lenox Hill trial demonstrated performance equal to that of traditional Holter monitors, driving hospital procurement decisions. Senseonics’ 365-day implant shows how extended-wear optical sensors improve adherence and generate longitudinal datasets valued by payers.

Advancements in Multi-Wavelength & AI-Enabled PPG Algorithms

Single-chip designs now integrate 20-bit ADCs, 120 dB dynamic range, and five LED wavelengths, enabling simultaneous capture of heart rate, SpO₂, blood pressure, and hydration with minimal power draw. Texas Instruments’ AFE4432 consumes only 12 µA, extending the smartwatch's seven-day battery life even with continuous monitoring. Huawei’s TruSense algorithm, trained on 182 million monthly users, reaches 98% heart-rate accuracy and sub-2% SpO₂ error, proving the value of large training datasets. Rockley Photonics demonstrated 99% accuracy for dehydration prediction using integrated laser spectroscopy, hinting at wider biomarker coverage in future wearables. A 2025 peer-reviewed synthesis in Nature reported a mean absolute percentage error below 10% for heart rate and an area under the curve of 0.97 for atrial fibrillation detection, cementing PPG’s clinical utility.

Regulatory Fast-Track Pathways for Digital Therapeutics

The TEMPO pilot and Europe’s streamlined CE Mark process have reduced time-to-market for predicate devices from 18 months to under 12 months. Apple’s Hypertension Notification received clearance in 2025 without a cuff-based comparator, signaling the agency's openness to trend warnings rather than absolute measurements. WHOOP’s ECG function was cleared under a new adjunctive code, broadening the competitive set for sports-performance platforms. The new PPW product classification quantifies cardiovascular status by matching photoplethysmography waveforms, simplifying predicate navigation for startups. Cross-Atlantic regulatory alignment is improving, allowing companies to stagger launches and optimize evidence-generation budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Motion-Artifact Accuracy Limitations in Dark-Skin & High-Motion Users | -1.5% | Global, with disproportionate impact in Africa, South Asia, and underserved populations | Medium term (2-4 years) |

| Data-Privacy & Cybersecurity Compliance Costs | -1.2% | EU (GDPR), North America (HIPAA, state privacy laws), China (PIPL) | Short term (≤ 2 years) |

| Supply-Chain Risk for Specialty Optoelectronic Components | -0.8% | Global, with bottlenecks in Taiwan, South Korea, and Germany | Short term (≤ 2 years) |

| Tariff Volatility on Semiconductor Imports | -0.5% | North America, EU (China-sourced components) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Motion-Artifact Accuracy Limitations in Dark-Skin & High-Motion Users

Systematic reviews published in JMIR and npj Digital Medicine confirmed persistent bias in SpO₂ readings for darker skin tones, with oxygen saturation overestimated by 1-3 points, delaying critical interventions.[3]JMIR Publications, “Skin Tone Bias in Pulse Oximetry,” jmir.org A 2025 Scientific Reports study found that wristband tension miscalibration increases error, and users seldom adjust straps correctly. Exercise conditions exacerbate inaccuracies; laboratory ±5% heart-rate error widens in real-world activity, and derived VO₂ max can miss by 60%. Munich Re’s actuarial review quantified lower accuracy for obese and darker-skinned individuals, raising fairness concerns in insurance underwriting. Vendors are responding with adaptive LED intensity and multi-path sensor layouts, but these hardware upgrades raise costs and power draw, slowing adoption in price-sensitive segments.

Data-Privacy & Cybersecurity Compliance Costs

HHS’s proposed HIPAA Security Rule update mandates encryption, MFA, 72-hour data-restore, and annual penetration testing, pushing initial compliance costs to USD 500,000–2 million for smaller vendors. The FTC’s Health Breach Notification Rule widens liability for non-HIPAA personal health record providers, many of which power consumer wearables. The EU AI Act classifies health-monitoring algorithms as high-risk, requiring conformity assessment and post-market surveillance, thereby increasing market-entry costs. NIST’s SP 800-66 guides zero-trust architecture, yet implementing those controls demands skilled personnel in short supply. Compliance costs favor well-funded incumbents and could slow innovation among startups unless modular privacy-engineering toolkits mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wrist Bands Continue to Narrow the Gap

Smart Wrist Bands are on track to expand at a 13.64% CAGR, closing the gap with Smart Watches, which accounted for 42.78% of 2025 shipments. The PPG Biosensors market size for wristbands benefits from aggressive sub-USD 50 pricing and broad channel reach in emerging economies, where spending elasticity is high. Xiaomi’s Band 7 packs heart-rate, SpO₂, and sleep-breathing metrics into a slim form factor, delivering 80% of a smartwatch’s value at one-fifth the cost. Pulse oximeters maintain relevance for telehealth respiratory monitoring, anchoring clinical trust that filters down to consumer categories. Finger rings, such as Oura’s fourth-generation model, deliver higher capillary-density signals and appeal to users seeking unobtrusive overnight tracking.

Smart Watches remain the segment anchor thanks to converged sensors, cellular modules, and app ecosystems. Apple Watch 10 added sleep apnea notifications via respiratory rate modeling, broadening medical screening utility while maintaining consumer appeal. Samsung and Garmin are positioning their flagship models for both wellness and diagnostics, buttressed by multi-band GPS and week-long battery life, though longer replacement cycles temper annual shipment growth. Other form factors, including adhesive patches and in-ear devices, are likely to see niche adoption when specialized clinical metrics are needed. Still, they lack the broad-based app support that fuels smartwatch retention. Across form factors, margins depend on silicon integration that contains bill-of-materials while sustaining performance targets, a delicate balance that favors platform owners with in-house design teams.

By Application: Cuffless Blood Pressure Emerges as a Demand Catalyst

Blood pressure monitoring is advancing at a 13.88% CAGR as vendors chase the clinical holy grail of cuffless, continuous measurement. Apple’s Hypertension Notification, cleared in 2025, provides trend alerts without absolute systolic and diastolic values, marking a regulatory first step and raising consumer expectations. Omron’s oscillometric HeartGuide shows hybrid compromises, while Aktiia’s PPG-calibrated solution marches toward FDA submission after CE-Mark success. IEEE Standard 1708-2014 is under revision to acknowledge machine-learning-based calibration, a move that could unlock broader device approvals.

Heart-rate monitoring still accounts for 46.07% of 2025 revenue because its accuracy has been proven and its data are widely used across fitness, chronic-disease management, and digital therapeutics. A 2025 Nature synthesis affirmed less than 10% error rates in lab settings and high atrial-fibrillation detection capability, cementing clinician confidence. The COVID-driven surge in SpO₂ monitoring persists but faces biased scrutiny across diverse populations. Experimental uses such as hydration sensing and core-temperature estimation are moving from pilot to product in 2026 releases, powered by laser spectroscopy and machine-learning inference, but lack reimbursement pathways and remain speculative drivers of the PPG biosensors market.

By Technology: Multimodal Fusion Outpaces Legacy Architectures

Multimodal PPG+ECG sensors are growing fastest at 15.28% CAGR, powered by devices like Cardiosense’s CardioTag, which fuses PPG, ECG, and seismocardiography to derive left-ventricular ejection time and pulmonary-capillary-wedge pressure. A multicenter trial presented at AHA 2024 showed that wedge-pressure estimation was comparable to that of implantable hemodynamic monitors, hinting at hospital-grade diagnostics in consumer wearables. The technology stack leverages machine-learning models that integrate electrical, optical, and mechanical signals for richer phenotyping.

Reflective PPG Sensors hold 51.72% share because they balance cost, power, and acceptable accuracy for mass-market devices. ams-OSRAM’s 1.68-mm module exemplifies aggressive miniaturization critical for rings and earbuds. Transmission PPG remains dominant in fingertip oximeters, prized for higher signal quality in clinical spot checks. Future growth depends on AI-driven signal fusion and cloud analytics that translate multichannel waveforms into actionable insights, ensuring that added hardware complexity converts into reimbursable clinical endpoints, not just consumer curiosity.

Geography Analysis

Asia-Pacific will expand at a 16.31% CAGR through 2031, outstripping all other regions. The combination of smartphone saturation, rising middle-class incomes, and state-sponsored health digitization agendas is boosting the PPG Biosensors market in China, India, and Southeast Asia. Huawei’s TruSense platform uses economies of scale to lower per-sensor costs while leveraging a dataset of 182 million users to refine algorithms. Xiaomi’s sub-USD 50 Band 7 democratizes access, especially in India, where affordability dictates adoption patterns. Japan’s aging demographics drive home-monitor adoption, with Omron integrating PPG sensors into its widely trusted blood-pressure ecosystem. South Korean OEMs leverage strong semiconductor capabilities to innovate hardware for both consumer and clinical markets.

North America retained a 38.89% share in 2025, thanks to stable reimbursement and an FDA pipeline that provides clear guidance on digital health devices. The PPG Biosensors market benefits from ACO-driven adoption as Apple Watch and Masimo W1 align with value-based care incentives. The TEMPO pilot further accelerates innovation cycles by rewarding FHIR compliance, aligning with U.S. interoperability mandates, and reducing friction in vendor negotiations with health systems.

Europe faces stricter privacy regulations under GDPR and the EU AI Act, yet maintains solid demand. Withings’ BeamO combines PPG, ECG, a digital stethoscope, and contactless temperature sensing, aiming to enable telehealth integration into chronic-care pathways. Polar Electro leverages Precision Prime sensor fusion to sell HRV analytics to corporations looking to curb healthcare costs. The region’s regulatory rigor adds compliance overhead but favors vendors that can finance audits, thereby erecting competitive barriers. Motion-artifact bias in darker-skin populations poses an equity challenge in Middle East & Africa, while Latin America’s adoption follows mobile-penetration curves, constrained by economic volatility yet buoyed by public-sector telehealth pilots.

Competitive Landscape

Competition is moderate and centers on value-chain control. Apple integrates silicon, sensors, algorithms, and cloud storage, enabling rapid feature rollouts such as sleep-apnea screening while protecting data within its walled garden. Samsung leverages in-house ASIC fabrication to integrate PPG and ECG on the BioActive sensor, balancing cost and performance for mainstream price tiers. Huawei’s TruSense amplifies algorithm quality through a massive installed base, reinforcing a data network effect that smaller rivals struggle to match.

Medical-device incumbents push clinical-grade accuracy. Masimo’s W1 and Omron’s HeartGuide target regulated channels and professional endorsement, aided by existing distribution in hospitals and pharmacies. Semiconductor suppliers such as ams-OSRAM, Texas Instruments, and Analog Devices compete on signal-to-noise ratio, power efficiency, and integration density, often securing multiyear design wins that lock OEMs into their roadmaps.

Automotive and insurance entrants are creating adjacency plays. Bosch and Continental embed contactless PPG in cabins, expanding the PPG Biosensors market to vehicles. Munich Re and Vitality programs demonstrate actuarial relevance by linking daily step counts to mortality risk, thereby incentivizing users to wear sensors and share data. Disruptors like Rockley Photonics and Biobeat are betting on laser spectroscopy and chest-worn patches, respectively, to unlock new biomarkers and hospital-at-home use cases.

PPG Biosensors Industry Leaders

Omron Healthcare

Samsung Electronics

Medtronic

Masimo Corporation

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cardiosense gained FDA clearance for CardioTag, the first wearable combining PPG, ECG, and seismocardiogram sensing, with multicenter studies confirming implant-grade accuracy.

- December 2025: FDA launched the TEMPO pilot to streamline digital-health device reviews that meet FHIR and OMOP interoperability standards.

- November 2024: Dexcom invested USD 75 million in Oura to integrate glucose data with PPG sleep and recovery metrics, targeting metabolic-health programs.

- November 2024: Omron received FDA clearance for HeartGuide BP+AFib, merging oscillometric cuff accuracy with PPG-based atrial-fibrillation alerts.

Global PPG Biosensors Market Report Scope

PPG biosensors (Photoplethysmogram biosensors) are non-invasive optical sensors that measure changes in blood volume in peripheral tissues, enabling continuous monitoring of vital signs such as heart rate, blood oxygen saturation, and blood pressure. They are widely used in wearable devices like smartwatches, fitness trackers, and medical monitoring systems.

The PPG biosensors market report is segmented by product type (pulse oximeters, smart watches, smart wrist bands, other product types), application (heart-rate monitoring, blood-oxygen saturation, blood pressure monitoring, other applications), technology (reflective PPG sensors, transmission ppg sensors, multimodal ppg+ecg sensors), and geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The market forecasts are provided in terms of value (USD).

| Pulse Oximeters |

| Smart Watches |

| Smart Wrist Bands |

| Other Product Types |

| Heart-Rate Monitoring |

| Blood-Oxygen Saturation |

| Blood Pressure Monitoring |

| Other Applications |

| Reflective PPG Sensors |

| Transmission PPG Sensors |

| Multimodal PPG + ECG Sensors |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pulse Oximeters | |

| Smart Watches | ||

| Smart Wrist Bands | ||

| Other Product Types | ||

| By Application | Heart-Rate Monitoring | |

| Blood-Oxygen Saturation | ||

| Blood Pressure Monitoring | ||

| Other Applications | ||

| By Technology | Reflective PPG Sensors | |

| Transmission PPG Sensors | ||

| Multimodal PPG + ECG Sensors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the PPG Biosensors market expected to grow between 2026 and 2031?

It is projected to expand at a 12.65% CAGR, rising from USD 0.65 billion in 2026 to USD 1.17 billion by 2031.

Which product category is likely to post the highest growth by 2031?

Smart wrist bands, supported by sub-USD 50 price points in emerging economies, are forecast to grow at 13.64% CAGR.

Why is cuffless blood-pressure monitoring considered a pivotal application?

Eliminating inflatable cuffs enables continuous tracking, and FDA moves such as Apple’s Hypertension Notification show regulators now accept trend-based alerts.

Which region will lead growth in wearable PPG adoption over the forecast period?

Asia-Pacific, underpinned by smartphone saturation, expanding middle-class income, and large-scale rollouts from brands like Huawei and Xiaomi.

What are the principal barriers to accuracy in darker-skin users?

Motion artifact and differential light absorption introduce 1–3 point SpO₂ bias, prompting vendors to adopt adaptive LED intensity and multi-path sensor designs.

Page last updated on: