Power Sector Exhaust System Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 1.09 Billion |

| Market Size (2030) | USD 1.29 Billion |

| Growth Rate (2025 - 2030) | 3.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

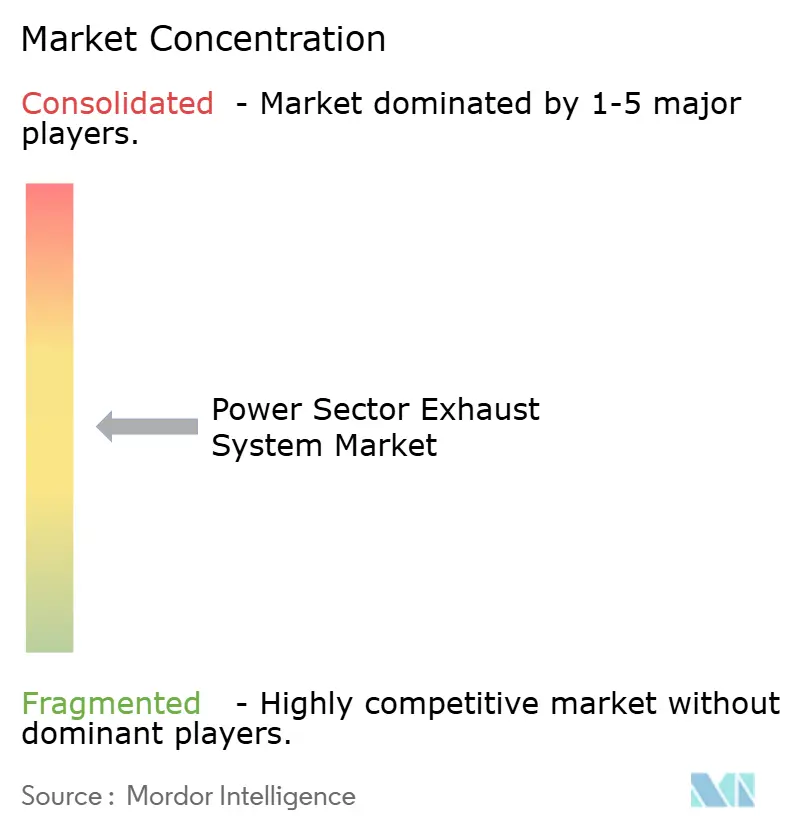

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Sector Exhaust System Market Analysis by Mordor Intelligence

The Power Sector Exhaust System Market size is estimated at USD 1.09 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 3.48% during the forecast period (2025-2030).

Behind this headline pace, spending is tilting away from new-build power plants toward retrofits that help existing thermal fleets meet ever-stricter NOx and particulate ceilings. Catalytic converters remained the largest component class thanks to their broad ability to oxidize carbon monoxide and unburned hydrocarbons, yet particulate filters are rising fastest as diesel-genset and industrial engine rules converge on on-road standards. Stainless steel maintained the biggest share of material demand, but composites and ceramics are taking hold where weight savings, thermal durability, and recyclability matter. Further momentum stems from distributed generation: urban microgrids, industrial CHP units, and data-center gensets create a dispersed order book of smaller systems that still need advanced emission and acoustic controls. At the same time, platinum-group-metal shortages and renewable displacement of baseload coal and gas curb growth in large, continuous-duty installations.

Key Report Takeaways

- By component, catalytic converters accounted for 33.3% of the power sector exhaust system market share in 2024, while particulate filters are forecast to expand at a 7.5% CAGR to 2030.

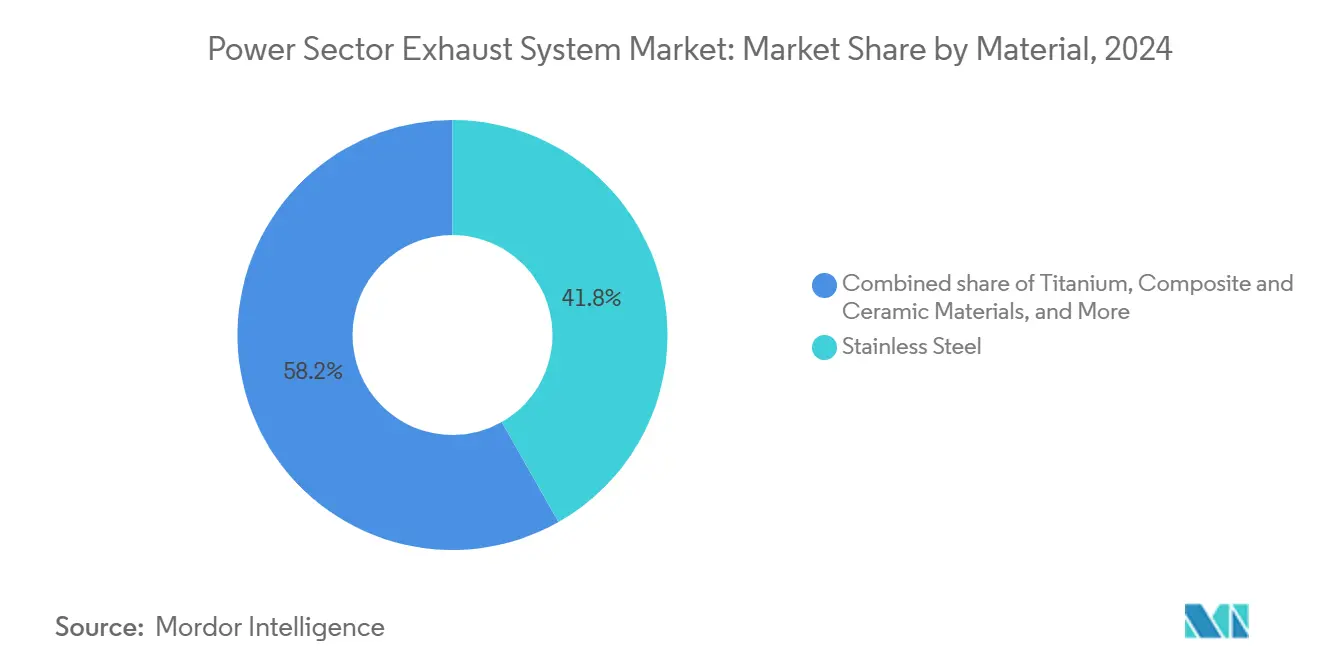

- By material, stainless steel held 41.8% of 2024 revenue; composites and ceramics are poised to grow at an 8.1% CAGR through 2030.

- By fuel type, diesel engines represented 53.5% of 2024 demand, yet the “others” category, including biogas, hydrogen blends, and dual-fuel units, is advancing at a 10.9% CAGR during the outlook period.

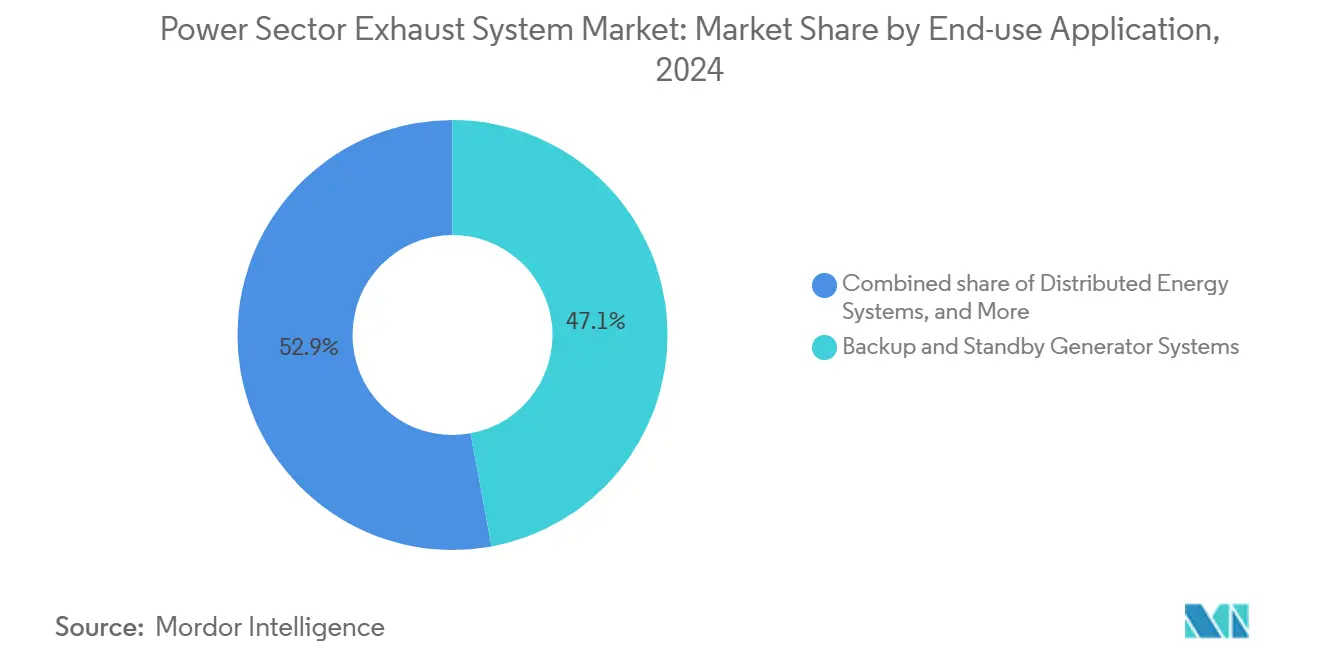

- By end use, backup and standby generator systems led with 47.1% of 2024 revenue, whereas distributed energy systems are projected to post a 10.4% CAGR through 2030.

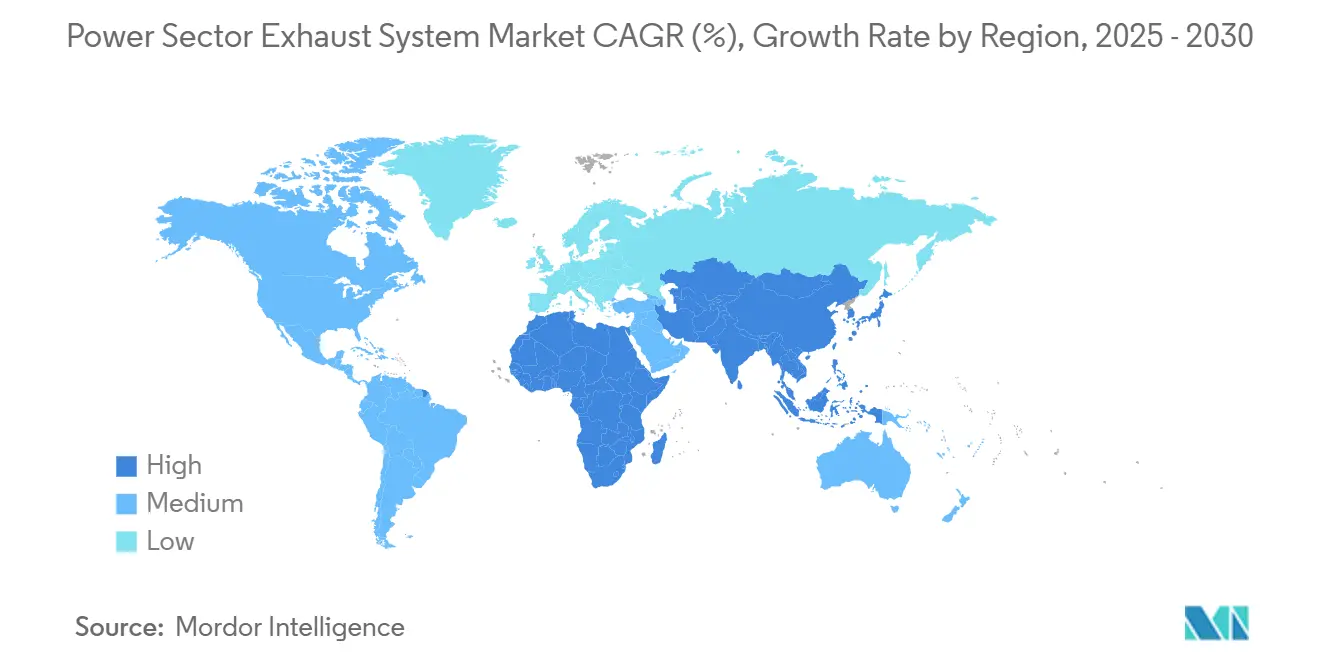

- By geography, Asia-Pacific captured 46.4% of 2024 sales and is projected to compound at 6.8% to 2030.

Global Power Sector Exhaust System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global emission regulations | 1.20% | EU, North America, China, India | Medium term (2-4 years) |

| Growth in gas-fired distributed generation | 0.80% | North America, Europe, APAC urban clusters | Medium term (2-4 years) |

| Data-center backup genset build-out | 0.60% | North America, Europe, APAC tier-one hubs | Short term (≤ 2 years) |

| Industrial CHP expansion | 0.40% | Europe, North America, China industrial zones | Long term (≥ 4 years) |

| Catalytic exhaust plus micro-carbon capture | 0.30% | EU, California, select APAC pilots | Long term (≥ 4 years) |

| Urban microgrid acoustic attenuation demand | 0.20% | Dense urban centers worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emission Regulations

New rules in the United States, China, India, and the European Union have pushed NOx and particulate limits for stationary engines to levels once reserved for on-road vehicles. U.S. Tier 4 caps, effective from 2024, cut NOx to 0.67 g/kWh and particulate to 0.03 g/kWh, forcing SCR-DPF combinations on engines above 560 kW.[1]U.S. Environmental Protection Agency, “Stationary Compression-Ignition Engines – Tier 4 Standards,” epa.gov China’s National VI and India’s Bharat Stage VI impose closed-loop urea dosing and particulate filtration across industrial engines, adding USD 80,000–150,000 per MW in hardware costs.[2]Reuters Staff, “China Implements National VI Emission Standards for Industrial Engines,” reuters.com Europe’s revised Industrial Emissions Directive lowers NOx for medium combustion plants to 100 mg/Nm³, making dual-stage SCR almost unavoidable. Suppliers with in-house test cells and proven formulations are winning business as operators race to certify engines within 24 months of rulemaking.

Growth in Gas-Fired Distributed Generation

Urban microgrids and industrial campuses are opting for 1-10 MW gas engines that ramp faster than turbines and supply usable heat for CHP. Global distributed gas capacity additions hit 12 GW in 2024, 60% in North America and Europe.[3]International Energy Agency, “Gas-Fired Distributed Generation Capacity Additions 2024,” iea.org Air districts in California and New York permit such projects only if NOx falls below 9 ppm, so three-way catalysts or lean-NOx traps are standard kit.[4]California Energy Commission, “NOx Emission Limits for Distributed Generation,” energy.ca.gov Japan’s feed-in tariff rewards CHP units that keep NOx under 25 ppm, stimulating demand for high-cell-density ceramic substrates. Each project orders several small SCR or oxidation-catalyst skids rather than a single large stack, reshaping supply logistics.

Data-Center Backup Genset Build-Out

Hyperscale operators deploy tens of 2-3 MW gensets at each campus for N+1 resiliency, collectively representing gigawatts of standby capacity. Amazon disclosed more than 1,200 units worldwide in 2024. Local permits often cap run time to 50 h/year yet set NOx limits as low as 0.5 g/bhp-h, so SCR systems are installed even on engines that rarely run. Renewable diesel initiatives by Microsoft and peers add another twist: catalysts must tolerate higher oxygen and variable sulfur content. Operators want remote monitoring for ammonia slip and catalyst temperature to avoid compliance failures.

Industrial CHP Expansion

Chemical, food, and pulp mills are adding reciprocal-engine CHP packages that harvest 40–50% of exhaust heat, lifting plant efficiency beyond 80%. The United States added 450 MW of such capacity in 2024. Germany approved 320 MW under decentralized-energy programs that also require NOx below 100 mg/Nm³. High-cell-density substrates (up to 600 cpsi) withstand thermal cycling and maintain pressure drop within 4 in. H₂O. Pilot projects blending 20% ammonia by energy content cut CO₂ but triple NOx, calling for oversized SCR reactors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable surge curbing thermal fleet | −0.9% | EU, California, Australia | Short term (≤ 2 years) |

| Costly retrofits in aging plants | −0.5% | North America, Europe, select APAC | Medium term (2-4 years) |

| Diesel-genset bans in Tier-1 cities | −0.3% | Beijing, Delhi, select EU metros | Short term (≤ 2 years) |

| Platinum-group-metal catalyst shortages | −0.4% | Global supply chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renewable Surge Curbing Thermal Fleet

Solar and wind additions of 473 GW in 2024 outpaced thermal retirements threefold, trimming baseload gas and coal runtime. California saw 15 days where midday solar eclipsed demand, relegating gas plants to cycling duty that degrades catalysts faster. Cold starts keep exhaust below 200 °C, allowing NOx slip until SCR beds light off. Electrically heated substrates solve this, but cost an extra USD 50,000-100,000 per MW. Where renewable penetration is high, operators may forego costly retrofits and instead accept shorter operating lives, dampening near-term orders.

Platinum-Group-Metal Catalyst Shortages

Rhodium averaged USD 4,800/oz in 2024 amid South African and Russian disruptions, hiking catalyst bills 25-40%. Suppliers diluted precious-metal loadings with base oxides, but low-temperature activity suffered. Three-way catalysts for stoichiometric gas engines are hardest hit because rhodium uniquely reduces NOx. Some OEMs shifted to lean-burn calibrations, replacing rhodium with downstream urea-SCR, which raises complexity. Secondary refining grew 30% to 180,000 oz, yet undersupplies persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Particulate Filters Capture New Diesel Rules

Particulate filters held 7.5% CAGR prospects between 2025 and 2030, eclipsing the 3.48% baseline for the power sector exhaust system market. Catalytic converters still owned 33.3% of the 2024 value, underscoring their role across diesel, natural-gas, and heavy-fuel applications. SCR arrays proliferate where sub-1 g/kWh NOx ceilings prevail, while EGR remains niche for large units that can accommodate coolers and fouling mitigation. Heat-recovery add-ons like 50-200 kW organic Rankine modules bolster efficiency, and combined muffler-catalyst units cut the footprint by 40% in budget-sensitive projects.

Early adoption of particulate filters accelerated as data-center, hospital, and telecom gensets fell under PM2.5 limits mirroring on-road Stage V. Europe now forces filters on stationary diesels above 560 kW, prompting cordierite-to-silicon-carbide upgrades that endure regeneration to 1,200 °C. Standby gensets need active regeneration because low runtime thwarts passive soot burn-off, adding USD 15,000-30,000 per unit. Such dynamics make particulate filters the fastest-growing slice of the power sector exhaust system market.

By Material: Composites and Ceramics Edge Out Metals

Composites and ceramics recorded an 8.1% CAGR outlook, twice the overall market pace, as operators value lightweight and thermal resilience. Stainless steel kept 41.8% of 2024 revenue but faces inherent limits above 450 °C. Titanium and nickel alloys fill marine and heavy-fuel niches yet remain costly. Ceramic honeycombs of cordierite or silicon carbide dominate catalyst supports; Corning’s silicon-carbide filter captures 99.9% of particles ≥0.1 µm and survives runaway regenerations up to 1,200 °C. Composite SCR substrates that fuse alumina fibers to stainless mesh cut mass 30% and pressure drop by 10%, appealing to retrofit projects with space constraints. Recycling economics further favor ceramics because extracting platinum-group metals from monoliths is simpler than from foil substrates.

By Fuel Type: Alternative Blends Accelerate “Others”

Diesel stayed the largest fuel class with 53.5% in 2024, yet hydrogen blends, renewable diesel, ammonia co-fires, and biogas lifted the “others” segment to a 10.9% CAGR. Natural-gas engines in CHP and microgrids broaden demand for three-way catalysts and lean-NOx traps. Hydrogen co-firing up to 20 % by volume requires re-timed injection and enhanced knock detection, while ammonia trials at 30 % energy share triple NOx, necessitating dual-stage SCR. Renewable diesel meets low-carbon fuel standards in California but carries a USD 0.30-0.90/L premium that only incentives can offset. Meticulous upstream gas cleaning for biogas, siloxanes, and H₂S removal adds USD 100,000-200,000 to each MW yet shields catalysts from poisoning.

By End-Use Application: Distributed Energy Surges

Distributed energy systems show a 10.4% CAGR through 2030, leveraging microgrids that couple gas reciprocating engines, heat recovery, and batteries for resilience in cities. Backup gensets dominate value today thanks to data centers, but face stricter run-hour and fuel regulations. Continuous-duty plant orders flatten as renewables displace baseload, shifting procurement to flexible peakers. Industrial CHP gains where carbon pricing and steam demand justify SCR investment. Marine and offshore niches require compact IMO Tier III-compliant SCR units that fit tight engine rooms. Real-time monitoring platforms, such as Cummins’ connected exhaust, let operators schedule catalyst changes based on degradation trends, trimming unplanned downtime by 20%.

Geography Analysis

Asia-Pacific contributed 46.4% of 2024 turnover and is set for a 6.8% CAGR as India and China extend Stage VI norms to industrial engines and retrofit coal peakers with tail-end SCR. India installs roughly 3 GW of gensets yearly; new Tier-4 rules push packaged oxidation-catalyst and filter solutions into this fleet.[5]Central Pollution Control Board of India, “Bharat Stage VI Norms for Gensets,” cpcb.nic.in China’s 14th Five-Year Plan allocates CNY 120 billion to industry retrofits, with SCR for engines above 1 MW forming a major tranche. Indonesia cleared 1.2 GW of gas-fired distributed schemes in 2024 that must hit 150 mg/Nm³ NOx, ensuring steady catalyst orders. Japan’s CHP tariff bonuses for ≤25 ppm NOx sustain demand for high-spec substrates, while Australia’s coal retirements spawn gas peakers that require SCR to comply with a 400 mg/Nm³ ceiling.[6]Government of New South Wales, “Peaking Plant NOx Limits,” nsw.gov.au

North America remains a retrofit stronghold. U.S. Tier 4 stationary rules force SCR-DPF combos on new engines above 560 kW, and California’s Rule 1110.2 drives dual-stage systems at 11 ppm NOx. Data-center hubs in Virginia and Oregon add genset farms but face NOx caps that mandate SCR even for standby duty. Europe shares similar dynamics; the Industrial Emissions Directive now binds 1-50 MW gas engines to 100 mg/Nm³ NOx. Germany’s decentralized energy push funnels 320 MW of CHP permits toward advanced exhaust kits.

Emerging regions trail but hold niche upsides. Brazil approved 800 MW of distributed generation, though weaker standards limit SCR penetration. Saudi Arabia earmarked USD 2.5 billion for gas-fired capacity in industrial cities, requiring 200 mg/Nm³ NOx, while South Africa pilots SCR on 7 GW of coal units, albeit hampered by budget and supply chain hurdles. The UAE enforces 150 mg/Nm³ on gensets above 1 MW in Abu Dhabi and Dubai, enough to justify oxidation catalysts.

Competitive Landscape

The power sector exhaust system market features moderate fragmentation. Engine OEMs, Caterpillar, Cummins, Wärtsilä, MAN, Rolls-Royce, bundle proprietary emission kits tuned to engine controls, securing service lock-in but simplifying compliance. Catalyst specialists Johnson Matthey, Haldor Topsoe, Tenneco, Donaldson, and Hug Engineering focus on formulation life and retrofit. Johnson Matthey’s Puraspec catalyst pushes high-sulfur life to 32,000 h via barium-promoted ceria-zirconia washcoats. Haldor Topsoe’s TopFrax silicon-carbide substrate hits 600 cpsi at <3 In. H₂O pressure drop. Smaller players, such as Eminox, carve urban-microgrid niches with combined acoustic-catalytic units.

Electrically heated catalysts answer cold-start NOx slip: Siemens Energy filed a European patent on a resistive heater embedded in ceramic SCR that halves light-off time. Micro-carbon-capture bolt-ons draw venture interest if carbon credits top USD 50/t. Consolidation continues: Caterpillar bought Weir’s oil-and-gas arm for USD 405 million, adding turbocharger tech that dovetails with high-pressure exhaust lines. Cummins is spending USD 150 million to expand ceramic-substrate capacity in the U.K. Wärtsilä secured EUR 85 million to supply integrated SCR-filter systems for a floating LNG terminal.

Power Sector Exhaust System Industry Leaders

Cummins Inc.

Caterpillar Inc.

Siemens Energy

Wartsila

MAN Energy Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: MIRATECH, a global frontrunner in emissions and acoustic control solutions for stationary engines, has inked a deal to acquire Exhaust Control Industries (ECI). ECI, hailing from Australia, specializes in industrial exhaust, power exhaust systems, and emissions solutions. This acquisition not only underscores MIRATECH's ambitious global growth strategy but also highlights its dedication to providing tailored solutions for clients throughout the Asia Pacific.

- September 2025: Rolls-Royce has unveiled a new line of compact and flexible power exhaust aftertreatment systems, designed to work seamlessly with its 16-cylinder mtu Series 4000 engine. These systems cater to a range of vessels, including yachts, tugs, and ferries. The latest innovations boast a 42% reduction in space requirements, a 40% decrease in weight, and a 15% cut in life cycle costs (LCC). Notably, these components offer versatile installation options: they can be positioned horizontally, vertically, upright, or even suspended within the engine room.

- April 2025: Hyundai Motor Group has introduced its next-generation hybrid powertrain system, setting a new benchmark for power and efficiency. The inaugural powertrain to feature this advanced hybrid system is a newly developed 2.5-litre turbo gasoline hybrid unit, which refines the design and control technology of the current 2.5 turbo gasoline engine to optimize efficiency. Additionally, the system incorporates an enhanced power exhaust system, further improving overall performance and fuel economy.

Global Power Sector Exhaust System Market Report Scope

Engineered to purify environments, a power sector exhaust system effectively eliminates contaminated air, fumes, smoke, and particles. Utilizing components such as hoods, fans, and ducts, the system captures pollutants at their source, transports them, and either filters or directly discharges them.

The global industrial exhaust systems market is segmented by component, material, fuel type, end-use application, and geography. By component, the market is segmented into mufflers, catalytic converters, particulate filters, selective catalytic reduction (SCR) systems, exhaust gas recirculation (EGR) systems, heat-recovery and energy-conversion systems, and others (combination and control modules). By material, the market is segmented into stainless steel, mild steel, titanium, nickel alloys, and composite and ceramic materials. By fuel type, the market is segmented into heavy fuel oil (HFO), diesel, natural gas, and others. By end-use application, the market is segmented into power-generation plants, backup and standby generator systems, industrial CHP systems, distributed energy systems, marine/offshore power support, and data centers and mission-critical. The market forecasts are provided in terms of value (USD).

| Mufflers |

| Catalytic Converters |

| Particulate Filters |

| Selective Catalytic Reduction (SCR) Systems |

| Exhaust Gas Recirculation (EGR) Systems |

| Heat-Recovery and Energy-Conversion Systems |

| Others (Combination and Control Modules) |

| Stainless Steel |

| Mild Steel |

| Titanium |

| Nickel Alloys |

| Composite and Ceramic Materials |

| Heavy Fuel Oil (HFO) |

| Diesel |

| Natural Gas |

| Others |

| Power-Generation Plants |

| Backup and Standby Generator Systems |

| Industrial CHP Systems |

| Distributed Energy Systems |

| Marine/Offshore Power Support |

| Data-Centers and Mission-Critical |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Mufflers | |

| Catalytic Converters | ||

| Particulate Filters | ||

| Selective Catalytic Reduction (SCR) Systems | ||

| Exhaust Gas Recirculation (EGR) Systems | ||

| Heat-Recovery and Energy-Conversion Systems | ||

| Others (Combination and Control Modules) | ||

| By Material | Stainless Steel | |

| Mild Steel | ||

| Titanium | ||

| Nickel Alloys | ||

| Composite and Ceramic Materials | ||

| By Fuel Type | Heavy Fuel Oil (HFO) | |

| Diesel | ||

| Natural Gas | ||

| Others | ||

| By End-use Application | Power-Generation Plants | |

| Backup and Standby Generator Systems | ||

| Industrial CHP Systems | ||

| Distributed Energy Systems | ||

| Marine/Offshore Power Support | ||

| Data-Centers and Mission-Critical | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the power sector exhaust system market?

It was valued at USD 1.04 billion in 2024 and is forecast to reach USD 1.29 billion by 2030.

Which component is growing fastest in power plant exhaust retrofits?

Particulate filters, propelled by diesel-genset PM rules, are projected to expand at 7.5% CAGR through 2030.

Why is Asia-Pacific dominant in exhaust-system demand?

Tight Stage VI engine norms in China and India, alongside distributed-generation build-outs in Southeast Asia, push the region to a 46.4% share and 6.8% CAGR.

How are data-center operators meeting strict NOx limits?

They install SCR units on standby gensets and increasingly burn renewable diesel to satisfy emerging sustainability mandates.

What materials are displacing stainless steel in catalyst substrates?

Ceramic honeycombs such as silicon carbide and composite alumina-fiber meshes are preferred for higher temperature stability and lower weight.

How will platinum-group-metal shortages affect catalyst pricing?

Rhodium and palladium volatility has already raised prices 25-40%, prompting suppliers to trim loadings and explore base-metal substitutes without sacrificing activity.

Page last updated on: