Power Delivery Module (VRM) for GPU and AI Servers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

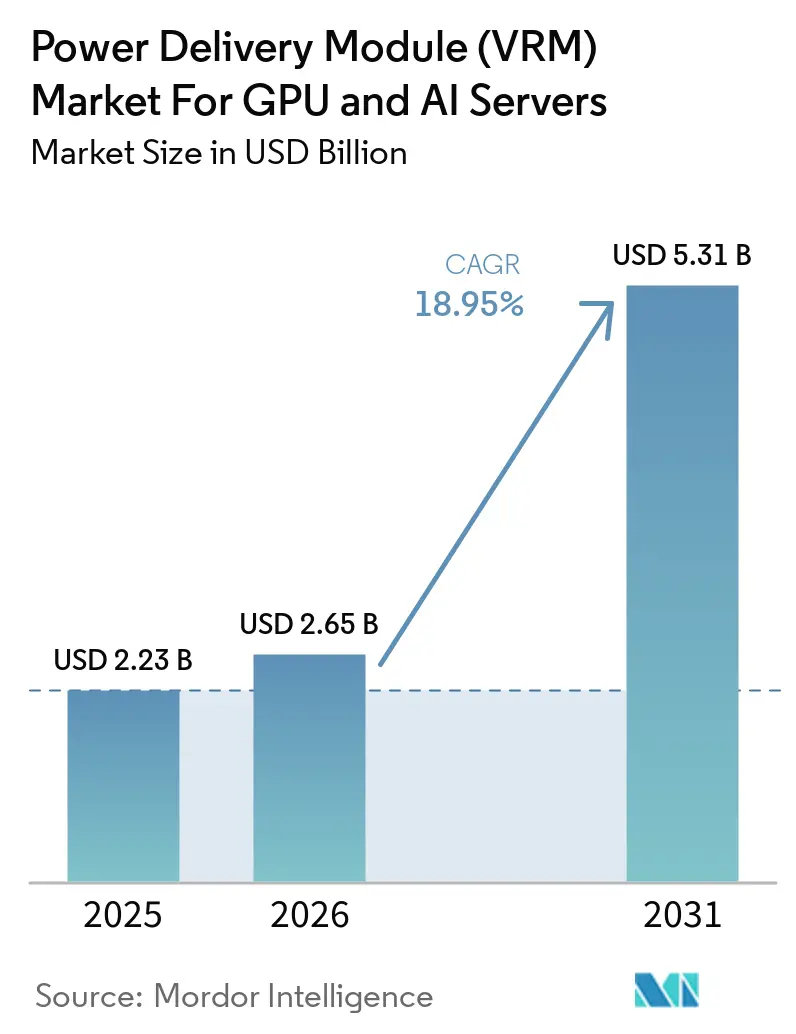

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 18.95% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Power Delivery Module (VRM) for GPU and AI Servers Market Analysis by Mordor Intelligence

The Power Delivery Module (VRM) market size is expected to increase from USD 1.78 billion in 2024 to USD 2.23 billion in 2025 and reach USD 5.31 billion by 2031, growing at an 18.95% CAGR over 2026-2031. A rapid pivot toward inference-optimized and training-intensive GPU workloads, coupled with sub-0.7-volt core rails on 3-nanometer silicon, is compressing impedance budgets and pulling phase counts above 20. Server builders are shifting to direct liquid cooling, 800-volt intermediate buses, and DrMOS power stages to attain rack densities above 100 kilowatts while meeting energy-efficiency clauses in hyperscaler procurement. The migration to high-bandwidth memory stacks is lifting transient load steps above 1,000 amperes per microsecond, accelerating the adoption of coupled inductors and vertically mounted modules that minimize loop inductance. At the same time, supply-chain constraints for advanced substrates are prompting dual-sourcing strategies and heightening interest in integrated power modules that encapsulate controller, power stages, and magnetics.

Key Report Takeaways

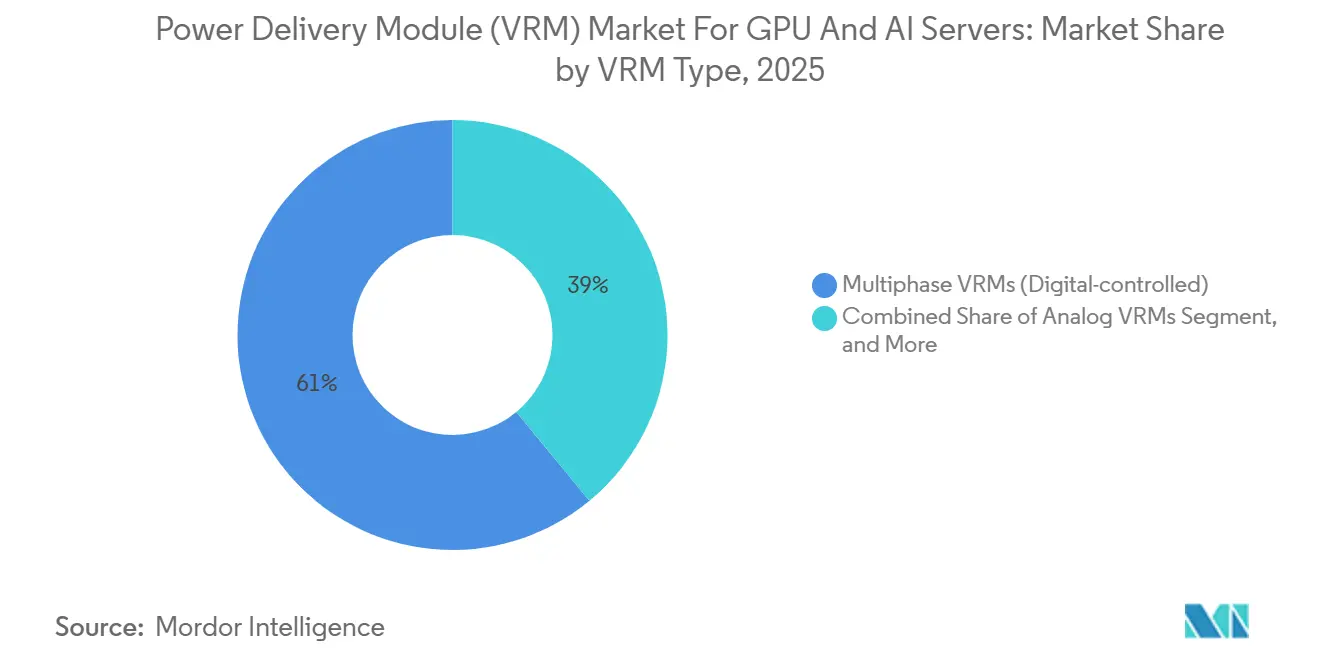

- By VRM type, multiphase digital-controlled designs accounted for 61% of revenue in 2025, while integrated power modules are forecast to expand at a 19.74% CAGR through 2031.

- By phase count, 13-20 phase solutions captured 43% of the market in 2025, and the 20-plus phase category is projected to post a 19.63% CAGR through 2031.

- By current capacity, high-power 300-800 A units accounted for 45% of the market share in 2025, whereas ultra-high-power designs above 800 A are set to advance at a 19.76% CAGR through 2031.

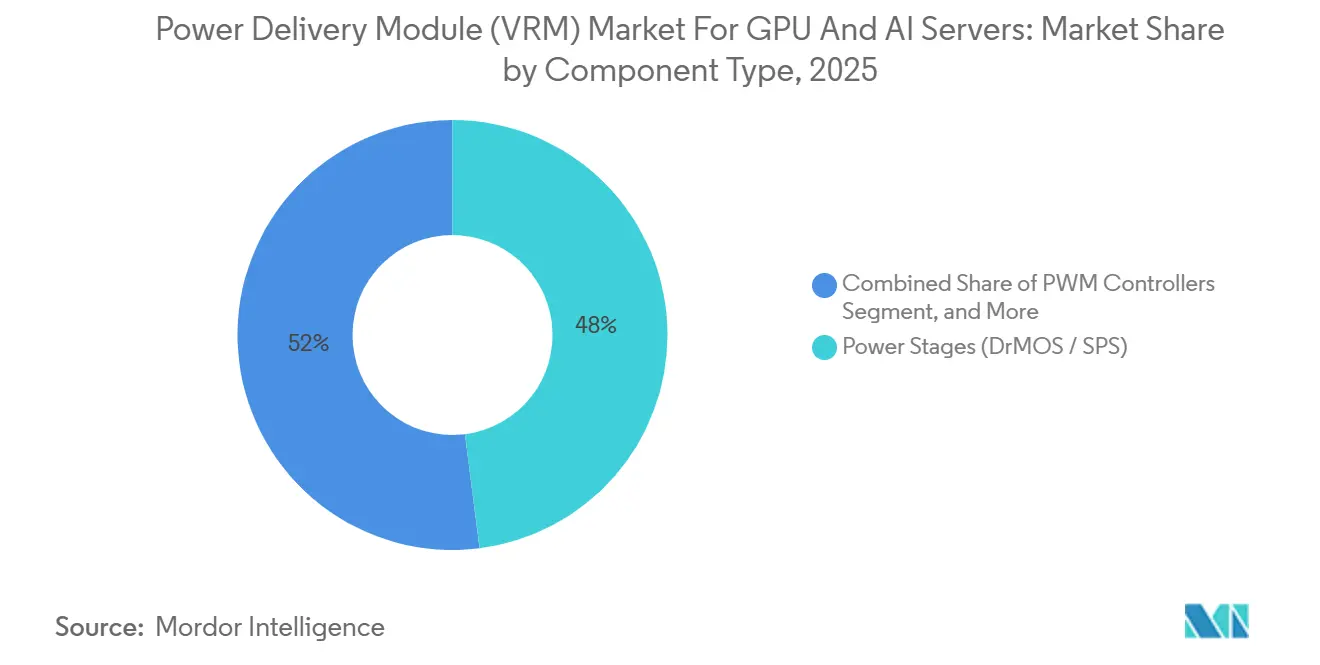

- By component, power stages accounted for 48% of 2025 revenue and are expected to grow at a 19.39% CAGR during 2026-2031.

- By end application, AI and HPC servers commanded 44% share in 2025, while AI training systems are on track for a 19.56% CAGR through 2031.

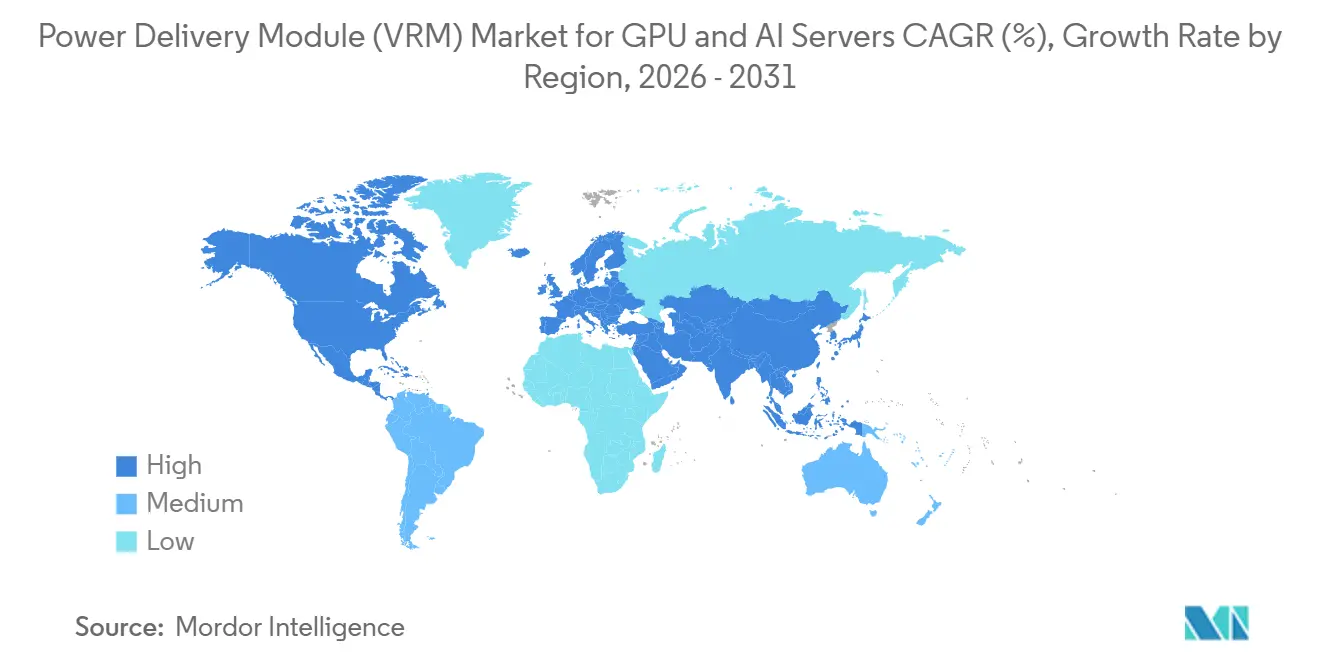

- By geography, Asia-Pacific led with 58% of 2025 revenue, yet North America is positioned to expand at a 20.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Power Delivery Module (VRM) for GPU and AI Servers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forcast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for GPU Accelerators in Hyperscale Data Centers | +5.2% | Global, concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Transition Toward 3D Stacked HBM Memory Raising Transient Load Requirements | +4.8% | Taiwan, South Korea, United States | Medium term (2-4 years) |

| Energy-Efficiency Mandates from Cloud Service Providers | +3.6% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Adoption of Advanced FinFET Nodes Lowering Core Voltages | +2.9% | Taiwan and South Korea fabs | Long term (≥ 4 years) |

| AI Inference at the Edge Driving Compact High-Current VRMs | +1.5% | North America, Europe, China | Medium term (2-4 years) |

| Government Incentives for Domestic Semiconductor Supply Chains | +1.0% | United States, European Union, Japan, South Korea, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for GPU Accelerators in Hyperscale Data Centers

Hyperscale operators deployed more than 3 million GPU accelerators in 2025 as compute fabrics shifted toward large language models and recommendation engines. Each NVIDIA H200 or AMD MI300X card draws up to 1,000 watts, forcing VRMs to deliver 1,200 amperes at sub-volt rails with ripple below 10 millivolts. Direct liquid-cooled racks enable power densities above 100 kilowatts, encouraging the use of integrated power modules that compress board footprint. Hyperscalers now require real-time telemetry for phase current, temperature, and efficiency, a specification that favors digital multiphase controllers. These operators increasingly co-develop application-specific modules under 24- to 36-month supply agreements, bypassing traditional distribution channels.

Transition Toward 3D Stacked HBM Memory Raising Transient Load Requirements

HBM3E, in volume since late 2024, introduces transient steps of 200 amperes per microsecond; HBM4 prototypes will push per-stack power past 50 watts by 2027. VRM suppliers respond with coupled inductors and adaptive voltage positioning, lowering output impedance by 40%.[1]IEEE, “Coupled Inductor Design for Multiphase VRMs,” ieee.org A Texas Instruments six-phase reference design achieved a 15-millivolt transient response at 500 amperes in March 2025. The vertical distance between the GPU die and the memory is shrinking, tightening impedance budgets and forcing VRM placement within 20 millimeters of the substrate. Vertical power modules mounted perpendicular to the board reduce loop inductance by 50%, but they demand custom mechanical fixtures and thermal interfaces.

Energy-Efficiency Mandates from Cloud Service Providers

Microsoft Azure stipulates ≥ 96% power-conversion efficiency at 50% load, while Google Cloud requires data-center PUE below 1.10 for facilities commissioned in 2026. These targets drive adoption of 800-volt intermediate buses that cut distribution losses by 75%. Texas Instruments and STMicroelectronics disclosed gallium nitride stages that switch above 1 megahertz to trim inductor volume by 60%. Washington State energy-disclosure rules, effective January 2025, triggered retrofits emphasizing digital controllers with dynamic phase shedding. The European Union’s amended directive sets a 2027 PUE ceiling of 1.20, accelerating replacement of analog VRMs.

Adoption of Advanced FinFET Nodes Lowering Core Voltages

Taiwan Semiconductor Manufacturing Company began high-volume 3-nanometer production in late 2024, and Intel 18A with backside power entered risk production in February 2025. Nominal voltages slid to 0.65-0.75 volts, doubling current draw for equal power and pushing phase counts past 16. Intel PowerVia reduces parasitic resistance by 30%, yet shifts the bottleneck to VRM capacitors. NVIDIA’s Blackwell GPU, sampling in 2025, is expected to exceed 1,000 watts, prompting the use of 24- and 32-phase controllers with adaptive dead-time control. As gate-all-around transistors emerge at 2 nanometers in 2027, designers explore switched-capacitor and hybrid buck-boost topologies to maintain efficiency below 0.6 volts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Tightness for High-Performance Power Stages | -2.1% | Asia-Pacific and North America | Short term (≤ 2 years) |

| Thermal Management Challenges Above 800 A Rails | -1.6% | High-density data centers globally | Medium term (2-4 years) |

| Board Space Constraints in Dense GPU Card Layouts | -0.9% | Global | Medium term (2-4 years) |

| Limited Standardization Across Server OEM VRM Specifications | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Tightness for High-Performance Power Stages

Lead times for DrMOS and smart power stages stretched to 26 weeks in early 2026 as substrate suppliers prioritized high-margin chiplets. Vishay reported 95% utilization and a backlog into late 2025. Onsemi’s October 2025 acquisition of Vcore secured gallium nitride wafer capacity, illustrating vertical integration moves to stabilize supply. Infineon earmarked EUR 800 million (USD 904 million) for additional silicon-carbide wafers, though new fabs will not reach full output until late 2027. Shortages are most acute above 100 amperes per phase, where copper-clip bonding is needed for thermal headroom. VRM designers must qualify alternate vendors and revise firmware, extending development cycles by up to 9 months.

Thermal Management Challenges Above 800 A Rails

VRMs delivering above 800 amperes dissipate 40-80 watts, exceeding conventional heatsinks and pushing the adoption of liquid-cooled cold plates. Accelsius demonstrated a microfluidic module that cut junction temperatures by 25 °C in January 2025.[2]Accelsius, “Microfluidic Cooling for High-Current VRMs,” accelsius.com Liquid loops add complexity in connectors, leak detection, and maintenance, limiting uptake outside hyperscale settings. Frore Systems’ solid-state AirJet entered production in 2025, providing localized airflow for edge servers where liquid cooling is impractical. Thermal cycling between idle and peak loads degrades solder joints, prompting a shift to sintered-silver die attach and high-temperature polymer capacitors to extend mean time between failures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By VRM Type: Digital Controllers Remain Anchor While Modules Surge

Multiphase, digitally controlled units led the Power Delivery Module (VRM) market share, accounting for 61% of revenue in 2025. These units are preferred due to their advanced features, including firmware-updatable control loops and PMBus telemetry, which are well-suited for hyperscaler fleet monitoring systems. The ability to update firmware ensures adaptability to evolving requirements, while PMBus telemetry provides real-time monitoring and control, making these units highly efficient and reliable for large-scale operations. Integrated power modules, although representing a smaller market share in 2025, are projected to experience the fastest CAGR of 19.74% during the forecast period. This growth is driven by server builders' increasing preference for compact, drop-in solutions that simplify design and reduce development time.

The market share of integrated modules in the Power Delivery Module (VRM) sector is steadily increasing, supported by advancements such as 48-volt intermediate buses and liquid-cooled racks, which enable tighter, more efficient layouts. Vendors like Vicor are at the forefront of this trend, offering innovative solutions that integrate controllers, power stages, and coupled inductors into a single package. This integration reduces board area by approximately 40%, providing significant space-saving benefits for manufacturers. While analog controllers remain cost-effective for edge devices, the long-term trend is shifting toward digital or hybrid designs. These advanced designs offer a balanced approach, combining low latency with enhanced telemetry capabilities, which are critical for modern applications requiring precise power management and monitoring.

By Phase Count: Ultra-High-Phase Designs Address Expanding GPU Budgets

Thirteen- to 20-phase solutions accounted for 43% of the revenue in 2025, establishing themselves as the standard for accelerators requiring up to 700 watts of power. These solutions are widely adopted because they meet the power demands of high-performance computing systems. However, the 20-plus phase tier is projected to grow at a compound annual growth rate (CAGR) of 19.63%, driven by the increasing power requirements of GPUs, which are expected to surpass 1,200 watts in the coming years.

The growth of the Power Delivery Module (VRM) market in this tier is supported by advancements in coupled inductors, which enable 12-phase performance within a compact six-phase footprint. This innovation allows for more efficient power delivery while optimizing space on circuit boards. Additionally, smart power stages with integrated current sensing technology help reduce routing congestion and streamline the design of 24- and 32-phase layouts. Suppliers who can effectively integrate high-phase controllers with vertical packaging solutions are well positioned to capitalize on demand for next-generation GPU launches, as these technologies align with evolving market requirements.

By Current Handling Capacity: Ultra-High-Power Leads Expansion Curve

High-power 300-800 A units accounted for 45% of 2025 revenue, primarily catering to mainstream H100 deployments. These units are critical for supporting the growing demand for high-performance computing applications, which require robust power-delivery solutions. Ultra-high-power units exceeding 800 A are projected to experience a compound annual growth rate (CAGR) of 19.76%, driven by the adoption of training clusters built around next-generation GPUs, such as the upcoming Blackwell and MI400 models. These GPUs are expected to push the boundaries of computational capabilities, further fueling the demand for ultra-high-power units.

The market share of ultra-high-power designs in the Power Delivery Module (VRM) segment is anticipated to grow significantly as advancements in liquid-cooled inductors and vertical module designs reach production. These innovations are expected to enhance efficiency and thermal management, making them ideal for next-generation GPU applications. Meanwhile, mid-power devices in the 100-300 A range are expected to grow in volume, though they may face price compression driven by increased competition and technological advancements. On the other hand, low-power devices below 100 A will continue to play a role in edge inference applications, where lower power requirements are sufficient. However, their overall market value is expected to decline as the focus shifts toward higher-power solutions.

By Component Type: Power Stages Command Value Pool

Power stages accounted for 48% of the revenue in 2025 and are expected to grow at a compound annual growth rate (CAGR) of 19.39%, driven by the increasing adoption of silicon carbide (SiC) and gallium nitride (GaN) devices. These advanced devices significantly enhance efficiency, pushing it above 96%, a critical factor in their growing demand. Furthermore, the integration of DrMOS (Driver MOSFET) technology has proven to be a game-changer, effectively reducing parasitic inductance by 30-40%. This reduction not only improves performance but also justifies the premium pricing associated with these solutions.

The Power Delivery Module (VRM) market size linked to power stages is poised to benefit from the ongoing capacity expansions by major industry players such as onsemi and Infineon. These expansions are expected to address supply chain challenges by reducing lead times and ensuring a more reliable supply of components. In addition, there is a parallel increase in investments in coupled inductors and high-voltage ceramic capacitors, which are essential to support the growing demand for power stages. Despite these developments, controllers continue to hold a strategically significant position in the market. This is because digital telemetry capabilities, which are integral to controllers, play a pivotal role in determining system qualifications and ensuring optimal performance across applications.

By End Application: AI Training Systems Outpace Mature Server Installations

AI and HPC servers accounted for 44% of the revenue in 2025, highlighting their significant role in supporting an installed base designed for mixed training and inference workloads. These servers are optimized to handle the demanding computational requirements of artificial intelligence (AI) and high-performance computing (HPC) applications. AI training systems, in particular, are expected to grow at a compound annual growth rate (CAGR) of 19.56%, driven by increased government investments in sovereign clusters across regions such as Europe, the Middle East, and Asia-Pacific. These investments aim to enhance regional capabilities in AI and HPC technologies.

Training nodes require highly synchronized power delivery systems capable of supporting 8-16 GPUs, necessitating voltage regulator modules (VRMs) with sub-microsecond response times and phase-locked telemetry. These advanced power delivery requirements ensure the efficient operation of training systems under heavy workloads. Meanwhile, GPU cards designed for inference tasks remain a stable mid-growth segment of the market. However, the price sensitivity of inference GPUs limits the potential for significant revenue growth in this niche, despite steady demand.

Geography Analysis

Asia-Pacific generated 58% of 2025 revenue, driven by Taiwan Semiconductor Manufacturing Company’s advancements in packaging technologies and China’s development of exascale training clusters. Japan’s Rapidus initiative secured JPY 920 billion (USD 6.2 billion) in funding to achieve 2-nanometer logic production by 2027, which is expected to create significant demand for sub-0.6-volt Voltage Regulator Modules (VRMs). South Korea’s K-Chips Act is channeling KRW 26 trillion (USD 19.5 billion) into domestic power-management IC production lines, facilitating expansions by major players such as SK hynix and Samsung. Meanwhile, India’s USD 15 billion subsidy program is attracting assembly investments; however, the majority of controller silicon is still sourced from Taiwan and the United States.

North America is anticipated to experience the fastest Compound Annual Growth Rate (CAGR) of 20.95% through 2031, primarily due to the CHIPS Act, which is incentivizing the localization of semiconductor manufacturing capacity. Intel’s USD 20 billion Arizona fabrication facility is set to include a power-management production line by late 2026, while Wolfspeed’s USD 6.5 billion silicon carbide (SiC) plant in North Carolina is expected to begin operations in 2026. Additionally, cloud service providers such as Microsoft Azure and Amazon Web Services are planning to deploy over 500,000 GPUs each by 2027, resulting in a projected VRM demand exceeding 500 megawatts.

Europe’s market share remains limited due to the region’s lack of GPU manufacturing capabilities. However, the EUR 43 billion (USD 48.6 billion) European Chips Act is actively funding the establishment of power-management design hubs in countries like Germany and the Netherlands.[3]European Commission, “European Chips Act Funding,” ec.europa.eu In contrast, the markets in the Middle East, Africa, and South America are still in their early stages of development, relying heavily on imported VRMs to support government-sponsored AI research clusters.

Competitive Landscape

The top five suppliers, Texas Instruments, Renesas Electronics, Infineon Technologies, Monolithic Power Systems, and Analog Devices, collectively accounted for approximately 55-60% of the total revenue in 2025, indicating a moderately concentrated market. The competitive landscape primarily revolves around digital multiphase controllers, which offer real-time telemetry and firmware flexibility. These features are critical for addressing end-users' evolving demands. Additionally, white-space opportunities exist in areas such as vertical power modules and liquid-cooled assemblies, where there is a notable lack of mechanical expertise, creating potential for innovation and market entry.

Strategic initiatives in the market highlight the growing importance of vertical integration and collaborative development. For instance, Onsemi acquired Vcore in October 2025 to ensure a stable supply of GaN wafers, a critical component for advanced power solutions. Similarly, Danfoss completed its acquisition of the remaining 50% stake in Semikron Danfoss in March 2026, strengthening its position in the liquid-cooled GPU cluster segment.[4]Danfoss, “Acquisition of Semikron Danfoss,” danfoss.com Texas Instruments, on the other hand, introduced a 30-kilowatt reference design in March 2025, which has significantly influenced procurement strategies during the Blackwell era. Meanwhile, the Open Compute Project continues to draft VRM guidelines. However, hyperscalers maintain proprietary pinouts, which perpetuate integration challenges and limit industry-wide standardization.

Smaller players, such as Vicor and Advanced Energy, are gaining market share by offering drop-in modules that significantly reduce design cycles, making them attractive to customers seeking faster time-to-market solutions. Additionally, fabless controller startups are leveraging advanced CMOS technology to integrate ADCs, gate drivers, and fault logic into a single die. This innovation reduces the number of external components required by approximately 20%, offering cost and efficiency advantages to manufacturers and end-users alike.

Power Delivery Module (VRM) for GPU and AI Servers Industry Leaders

-

Texas Instruments Incorporated

-

Renesas Electronics Corporation

-

Infineon Technologies AG

-

Semiconductor Components Industries, LLC

-

Analog Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Danfoss completed the acquisition of the remaining 50% stake in Semikron, consolidating its power module portfolio.

- October 2025: Onsemi finalized the Vcore acquisition, locking in GaN epi supply for next-gen power stages.

- September 2025: Wolfspeed’s USD 6.5 billion North Carolina SiC fab reached mechanical completion with ramp slated for Q2 2026.

- August 2025: Renesas introduced ISL91301B and ISL91302B multiphase controllers with 16-bit ADC telemetry.

Global Power Delivery Module (VRM) for GPU and AI Servers Market Report Scope

The Power Delivery Module (VRM) for GPU and AI Servers Market refers to the global ecosystem involved in the design, development, manufacturing, and commercialization of voltage regulation modules (VRMs) used to supply stable, efficient, and high-current power to GPUs and AI-focused computing systems. VRMs are critical components that convert and regulate power supply voltages to meet the precise requirements of high-performance processors in data centers, AI training systems, and accelerator cards.

The Power Delivery Module (VRM) for GPU and AI Servers Market Report is Segmented by VRM Type (Multiphase Digital, Analog, Integrated Power Modules, and Hybrid), Phase Count (≤6, 7-12, 13-20, and 20+), Current Capacity (Low <100A, Mid 100-300A, High 300-800A, and Ultra High 800A+), Component (Power Stages, PWM Controllers, Inductors, and Capacitors), End Application (GPU Cards, AI/HPC Servers, and Training Systems), and Geography (North America, Europe, Asia-Pacific, and Rest of World). Market Forecasts are Provided in Terms of Value (USD).

| Multiphase VRMs (Digital-controlled) |

| Analog VRMs |

| Integrated Power Modules |

| Hybrid VRMs |

| ≤6 Phases |

| 7-12 Phases |

| 13-20 Phases |

| 20+ Phases |

| Low Power (<100 A) |

| Mid Power (100-300 A) |

| High Power (300-800 A) |

| Ultra High Power (800 A+) |

| Power Stages (DrMOS / SPS) |

| PWM Controllers |

| Inductors (Chokes) |

| Capacitors |

| GPU Accelerator Cards |

| AI / HPC Servers |

| AI Training Systems |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By VRM Type | Multiphase VRMs (Digital-controlled) | |

| Analog VRMs | ||

| Integrated Power Modules | ||

| Hybrid VRMs | ||

| By Phase Count | ≤6 Phases | |

| 7-12 Phases | ||

| 13-20 Phases | ||

| 20+ Phases | ||

| By Current Handling Capacity | Low Power (<100 A) | |

| Mid Power (100-300 A) | ||

| High Power (300-800 A) | ||

| Ultra High Power (800 A+) | ||

| By Component Type | Power Stages (DrMOS / SPS) | |

| PWM Controllers | ||

| Inductors (Chokes) | ||

| Capacitors | ||

| By End Application | GPU Accelerator Cards | |

| AI / HPC Servers | ||

| AI Training Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the 2026 value of the Power Delivery Module (VRM) market and how large will it be by 2031?

The market is projected to reach USD 2.23 billion in 2025 and grow to USD 5.31 billion by 2031 at an 18.95% CAGR.

Which VRM type currently holds the largest revenue share?

Multiphase digital-controlled VRMs led with a 61% share in 2025.

Which geographic region will grow the fastest through 2031?

North America is expected to post the fastest regional CAGR of 20.95% through 2031.

Why are 800-volt intermediate buses gaining traction in VRM design?

They cut distribution losses by 75% and help meet strict energy-efficiency mandates set by cloud service providers.

What is driving demand for ultra-high-power VRMs above 800 amperes?

Next-generation GPUs for AI training are expected to surpass 1,000 watts each, necessitating VRMs capable of delivering sustained currents above 800 amperes.

How are suppliers mitigating supply-chain tightness for power stages?

Leading vendors are vertically integrating, expanding SiC and GaN wafer capacity, and qualifying alternative packaging partners to shorten lead times.

Page last updated on: