Poultry Processing Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 8.96 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

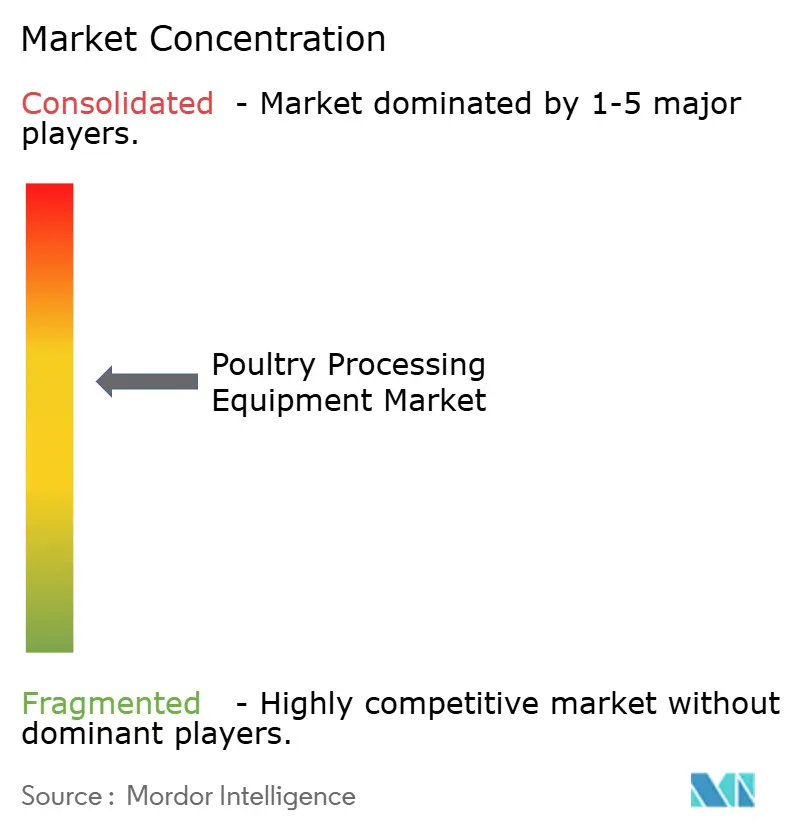

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Poultry Processing Equipment Market Analysis by Mordor Intelligence

The Poultry Processing Equipment Market size is projected to expand from USD 6.73 billion in 2025 and USD 7.06 billion in 2026 to USD 8.96 billion by 2031, registering a CAGR of 4.9% between 2026 to 2031. Demand remains linked to rising poultry consumption. The OECD and FAO expect poultry to account for the largest share of incremental global meat intake over the long term, keeping processing capacity expansion on the agenda for integrated producers. Equipment purchasing decisions are also becoming more financially disciplined, as even small yield losses per bird can accumulate quickly at high operating volumes. This trend makes investment in modern lines easier to justify when processors can directly link equipment performance to output recovery. Competitive intensity is expected to increase after the JBT Marel combination is completed in January 2025, with the combined company expected to report USD 3.8 billion in full-year 2025 revenue, supported by protein demand led by poultry. Food safety requirements and AI-enabled inspection are advancing together, prompting processors to view inline monitoring, vision grading, and automated inspection as core line components rather than optional add-ons. Brownfield upgrades remain a clear opportunity in the poultry processing equipment market, as processors can improve uptime and yield on existing high-speed assets without incurring the full cost of new plant construction.

Key Report Takeaways

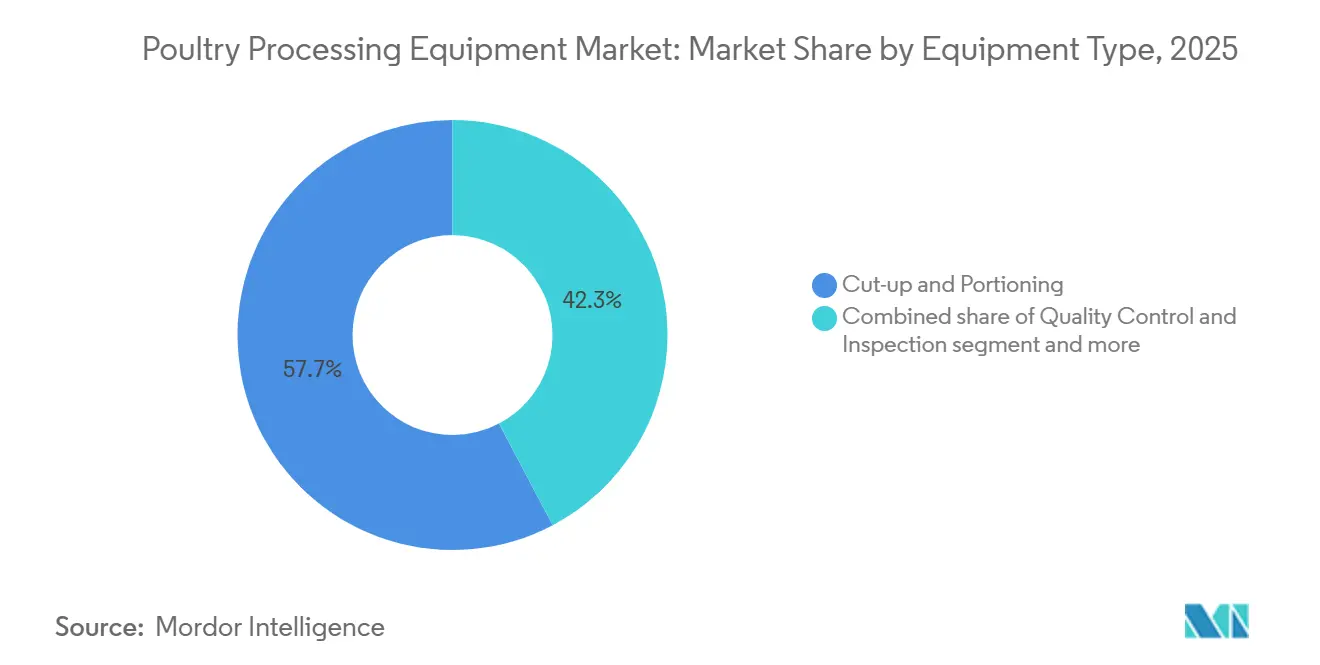

- By equipment type, Cut-up and Portioning accounted for the largest share of the poultry processing equipment market, at 22.89% in 2025, while Quality Control and Inspection is projected to grow at the fastest CAGR of 5.74% during 2026–2031.

- By automation level, Semi-Automated systems accounted for the largest share of the poultry processing equipment market, at 57.71% in 2025, while Fully Automated systems are projected to grow at the fastest CAGR of 6.21% during 2026–2031.

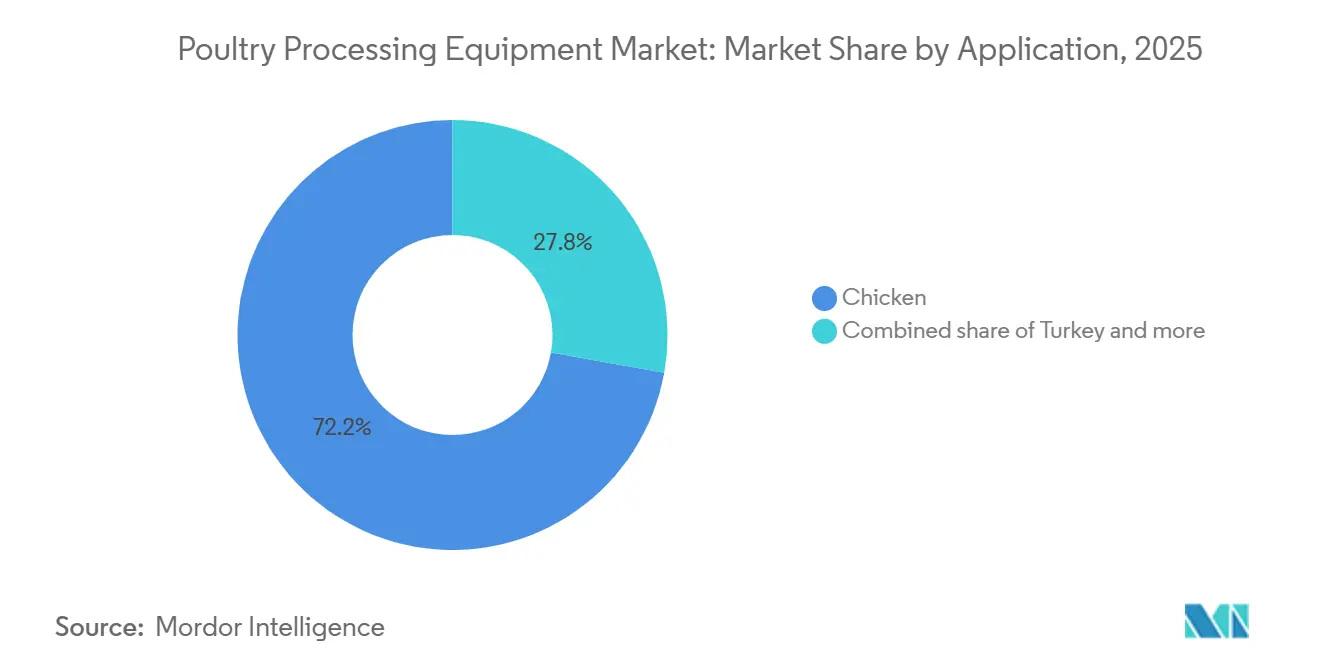

- By application, Chicken accounted for the largest share of the poultry processing equipment market, at 72.19% in 2025, while Turkey is projected to grow at the fastest CAGR of 5.84% during 2026–2031.

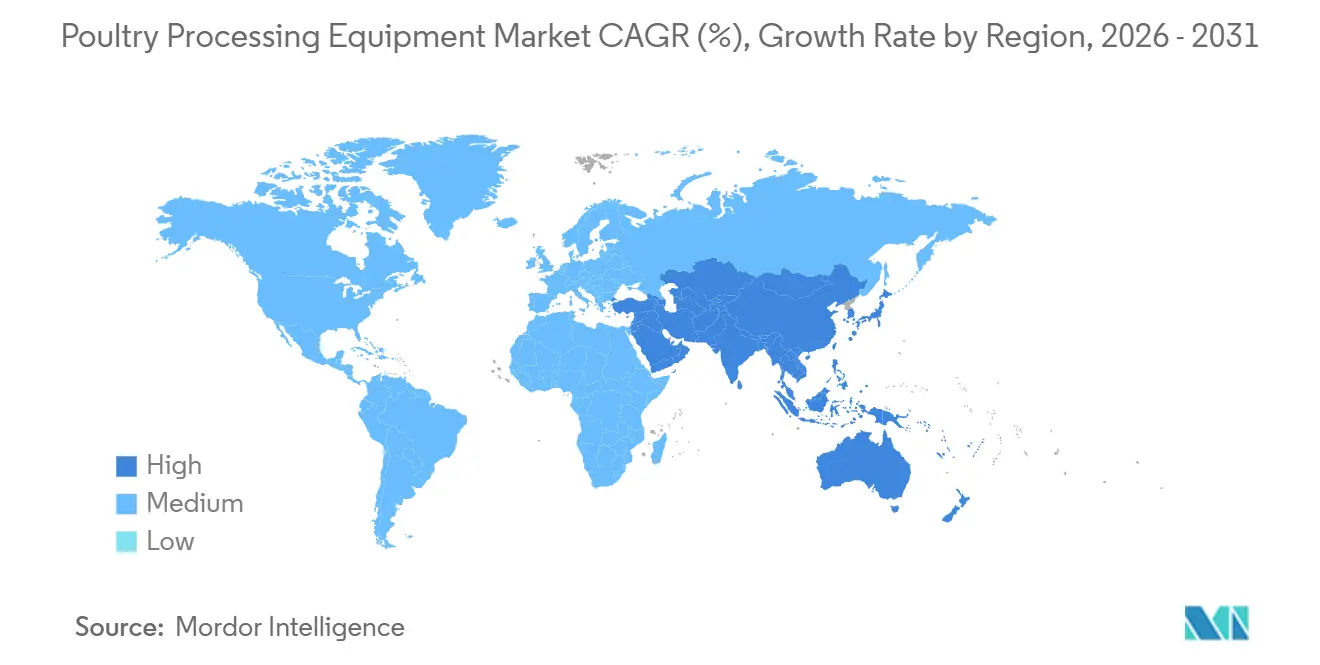

- By geography, Asia-Pacific accounted for the largest share of the poultry processing equipment market, at 29.57% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 7.42% during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Poultry Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for high throughput automated processing lines | +1.2% | Global, intensity highest in North America, EU, and Asia-Pacific core | Medium term (2-4 years) |

| Tightening food safety and hygiene compliance requirements | +0.8% | North America and EU, with influence on export-oriented Asia-Pacific processors | Short term (≤ 2 years) |

| Labor shortages and wage inflation in processing plants | +0.9% | North America, Western Europe, Australia, with spillover into Middle East and Africa | Medium term (2-4 years) |

| Expansion of ready-to-cook and ready-to-eat poultry formats | +0.7% | Asia-Pacific, Middle East, and emerging markets | Long term (≥ 4 years) |

| Ai-powered inspection, yield optimization, and vision grading adoption | +0.6% | Global, with fastest hardware uptake in Europe and North America | Medium term (2-4 years) |

| Retrofit demand from brownfield plants seeking uptime and yield gains | +0.5% | North America and Europe, with secondary demand in Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Throughput Automated Processing Lines

High throughput capacity has become a key procurement requirement for large poultry processors expanding or modernizing their facilities in the poultry processing equipment market. Marel’s work on De Heus’s greenfield plant in Tây Ninh, Vietnam, shows how manufacturers are engineering new lines to process 6,000 birds per hour at startup, with a built-in pathway to expand to 12,000 birds per hour without replacing core machinery. This phase-ready design reduces the risk of repeated civil work and supports processors planning gradual volume ramp-ups. Meyn also demonstrated the operational benefits of higher throughput with its Rapid Plus M5.0 breast deboner, which underwent 36,000 hours of engineering validation and delivered a 4 g per fillet yield gain during a two-year pilot with Norsk Kylling. As more processors benchmark performance based on yield per bird and hourly output, suppliers that cannot demonstrate measured results are likely to face greater pressure in line tenders.

Tightening Food Safety and Hygiene Compliance Requirements

Food safety regulations are directly shaping equipment specifications in the poultry processing equipment market, as processors increasingly need compliance, traceability, and contamination control built into processing lines[1]Source: Food Safety and Standards Authority of India, "FSSAI guidance document on poultry processing food safety", fssai.gov.in. The USDA Food Safety and Inspection Service is expected to update its retained water guidance in January 2025, with full label compliance set to take effect on January 1, 2026[2]Source: USDA Food Safety and Inspection Service,"FSIS to Modify Procedures to More Accurately Sample Raw Poultry Establishments", fsis.usda.gov. This timeline is pushing plants to revisit control procedures and documentation. In Europe, Regulation (EC) No. 853/2004 continues to impose strict requirements for evisceration, chilling, and hygiene performance, sustaining plant upgrade activity at mature facilities. India’s licensing framework is also encouraging smaller processors to formalize operations to access organized retail and export channels, supporting demand for certified equipment. As a result, inline microbial monitoring and vision-based inspection are shifting from premium options to baseline tools in the poultry processing equipment market.

Labor Shortages and Wage Inflation in Processing Plants

Labor scarcity remains a durable driver of automation in the poultry processing equipment market, as it changes the payback profile of deboning, conveying, inspection, and material handling systems. Large processors in major poultry corridors are expected to continue deploying robotic deboning lines, automated guided vehicles, and related upgrades through 2025 to reduce reliance on hard-to-fill production roles. This shift has not eliminated labor risk; instead, it has changed its nature, as plants now require fewer repetitive operators and more technicians to keep automated lines running. Purdue University research expected to be published in 2026 links workforce disruptions in U.S. poultry processing to higher hiring costs, increased separations, and more food safety inspection deficiencies at affected establishments, reinforcing the operational value of stable, automated processes. As a result, the Poultry Processing Equipment Market is benefiting not only from wage pressure but also from the need to reduce production volatility when labor availability remains uncertain.

Expansion of Ready-to-Cook and Ready-to-Eat Poultry Formats

The shift toward ready-to-cook and ready-to-eat poultry products is changing the equipment demand mix in the poultry processing equipment market, as value-added formats require more processing steps than commodity whole-bird lines. Portioning, deboning, marination, coating, thermal processing, and inspection become increasingly important as producers expand into retail meal formats, deli products, and foodservice specifications. GEA’s planned launch of the CookStar First compact spiral oven in February 2026 reflects this requirement, as the company designed it for small-to-mid-sized processors entering coated poultry and ready meal production without committing to full greenfield investment. This product strategy also supports brownfield sites that require compact equipment layouts and solutions for restricted ceiling clearance rather than full plant redesigns. As product mixes shift toward higher processing intensity, the Poultry Processing Equipment Market benefits from higher equipment content per unit of finished output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of fully automated processing lines | -0.8% | Global, most acute in South Asia, Sub-Saharan Africa, and smaller Asia-Pacific markets | Short term (≤ 2 years) |

| Complex maintenance and sanitation downtime requirements | -0.5% | Global | Medium term (2-4 years) |

| Integration friction with legacy slaughter and chilling assets | -0.4% | North America and Europe, especially older brownfield sites | Medium term (2-4 years) |

| Skilled technician shortage for advanced controls and robotics | -0.3% | Global, particularly acute in North America and parts of Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Fully Automated Processing Lines

Capital intensity remains a major barrier to full-line adoption in the Poultry Processing Equipment Market, particularly among processors outside the largest integrated companies. A fully automated evisceration, cut-up, and deboning line for a 6,000-bird-per-hour facility still requires multi-million-dollar investment before civil work, utilities, and commissioning costs are added. This cost burden keeps many mid-sized buyers focused on phased investments. This buying pattern helps explain why semi-automated systems are expected to account for a 57.71% share in 2025, as they allow plants to capture part of the efficiency gains without incurring the full cost of complete automation. Equipment suppliers are responding with modular formats, and GEA’s planned MultiJector 500 launch in April 2026 shows how vendors are targeting smaller and mid-capacity marination lines with scalable layouts. Despite modular design improvements, the poultry processing equipment market is expected to continue facing slower fully automated adoption in price-sensitive regions where financing depth and equipment collateral structures remain limited.

Skilled Technician Shortage for Advanced Controls and Robotics

The shortage of qualified technicians is creating a practical limit on how quickly companies in the poultry processing equipment market can use advanced systems to their full potential. Modern poultry processing lines integrate machine vision, PLC systems, AI-based inspection, sensors, and data platforms, requiring maintenance teams to manage mechanical, software, and hygiene-related functions. The challenge often becomes more significant after automation is installed, as downtime on a high-speed line can quickly offset the throughput and yield gains that justified the investment. Purdue University research published in 2026 supports this concern by linking labor disruptions in U.S. poultry processing to higher operating friction and food safety deficiencies, highlighting the importance of workforce stability and technical capability. Until vocational training and OEM-led certification programs expand more widely, the Poultry Processing Equipment Market is likely to experience a slower transition from equipment sales to full operating optimization across several mature regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Value-added Cuts Hold Scale While Inspection Systems Grow Faster

Cut-up and portioning is expected to hold 22.89% of the poultry processing equipment market share in 2025, making it the largest equipment category across the installed and new investment base. Its leadership reflects the significant role of portion-specific poultry supply for quick-service restaurants, foodservice buyers, and retail programs that require consistent breast, thigh, wing, and mixed-cut specifications. As a result, automated cut-up lines remain central to processor capital expenditure, as processors must balance accuracy, line speed, and yield. The category also benefits from upstream processes, including slaughtering, defeathering, chilling, deboning, and evisceration, which ultimately support downstream cut quality and usable portion recovery.

Quality control and inspection are projected to register a 5.74% CAGR through 2031, making it the fastest-growing equipment type in the poultry processing equipment market size. This growth is tied to the need to integrate compliance, defect detection, and yield optimization into a single line architecture, rather than relying on manual end-of-line checks. Meyn’s Asymmetric Rehanger with Multi Vision Quality Grading demonstrates how inspection functions are moving into high-speed conveying systems, while BAADER’s ClassifEYE platform adds inline deviation detection on evisceration lines before losses become more expensive. Academic work published in Foods in 2025 also supports this direction, as deep learning models are already demonstrating quality deviation detection at production-line speeds, giving commercial processors greater confidence in inspection-led upgrades.

By Automation Level: Semi-Automated Systems Lead While Fully Automated Lines Expand Faster

Semi-automated systems are expected to account for a 57.71% share in 2025, giving them the broadest installed base across the Poultry Processing Equipment Market. This segment remains a practical choice for many facilities because it allows operators to automate repetitive and high-speed processes, such as evisceration, chilling, and conveyance, while retaining manual labor in areas where anatomical variation and product grading still create handling complexity. This model also reduces capex risk, as processors can add automation in stages instead of replacing the entire line at once. Manual systems continue to operate in lower-volume or lower-wage environments, but investment remains concentrated in semi-automated configurations that balance cost and performance.

Fully automated systems are forecast to grow at a CAGR of 6.21% during 2026-2031, making them the fastest-growing automation category in the poultry processing equipment market. Growth is strongest among large integrators that have already captured most of the benefits from hybrid line designs and now aim to reduce their remaining labor dependence. Smart and AI-enabled features are becoming central to this shift, as they add continuous monitoring, yield tracking, and process intelligence to mechanical automation. BAADER’s Front Half Deboner 6630 and related AI-based vision capabilities illustrate how suppliers are reducing manual scrape tests and embedding quality checks directly into processing lines. In addition, academic research from Auburn University is expected to review a broader set of machine learning tools for postharvest poultry processing in 2026.

By Application: Chicken Keeps the Core Volume Base While Turkey Advances Faster

Chicken is expected to account for a 72.19% share in 2025, maintaining its position as the dominant application in the poultry processing equipment market. This position stems from chicken’s scale in global consumption, trade, and further processing, which keeps major OEM product development focused on chicken line productivity, hygiene, and cutting accuracy. JBT Marel’s fully automated evisceration line for retired laying hens in China indicates that even smaller application niches within chicken are attracting industrial-scale equipment investment as processors aim to formalize supply and increase throughput. Regulatory formalization also supports the segment, as licensing and pathogen-control requirements are pushing processors in major poultry-producing countries toward certified, enclosed, and more automated equipment platforms[3]Source: Food Safety and Standards Authority of India, "Safety and Quality of Meat and Poultry", fssai.gov.in.

Turkey is projected to grow at a CAGR of 5.84% through 2031, making it the fastest-growing application in the poultry processing equipment market. The segment benefits from stronger demand for deli meats, snack products, and ready-to-eat formats in North America and Europe, where value-added poultry portfolios remain important. Turkey processing also has a different technical profile than chicken processing, as larger bird size and more complex anatomy increase the equipment content required for deboning and precision cutting. Duck and other poultry types remain smaller niches. However, their presence broadens the application base of the Poultry Processing Equipment Market, as suppliers can use species-specific product extensions to capture emerging processing needs beyond chicken.

Geography Analysis

Asia-Pacific is expected to account for 29.57% of the poultry processing equipment market share in 2025, making it the largest regional block in current demand. Mechanization in China and India’s steady shift from wet-market dependence toward chilled and processed poultry formats support the region’s leadership. Regulatory formalization is also supporting growth, as processors serving organized retail or export channels require more controlled and certified equipment layouts. Vietnam, Indonesia, and Thailand are also gaining importance as integrated agri-food companies build export-oriented processing capacity. JBT Marel’s greenfield engagement with De Heus in Vietnam reflects this trend, as the line was designed for immediate operation and future expansion within the same processing platform.

Asia-Pacific is also forecast to register the fastest CAGR of 7.42% during 2026-2031, making it the fastest-expanding regional part of the poultry processing equipment market size. A combination of domestic protein demand, food safety formalization, and export preparation is driving growth, rather than a single factor. New plants in the region increasingly include provisions for future throughput expansion, indicating stronger confidence in future processed poultry demand. This positions the poultry processing equipment market with a strong regional growth engine that combines volume growth with rising technology intensity.

North America is expected to remain one of the most equipment-dense regions in 2025, with demand shaped by automation upgrades, brownfield retrofits, and a focus on labor reduction across large poultry processors. Europe is expected to remain a mature but highly technical market, where equipment innovation, hygiene compliance, and research and development concentration continue to influence product development before export to other regions. South America continues to offer scale potential through Brazil’s export-driven poultry market, although financing and foreign exchange conditions can slow new-unit purchases. The Middle East and Africa remain an emerging demand zone, where food security programs, self-sufficiency goals, and gradual formalization support integrated processing investment. Across these regions, retrofit economics, export compliance needs, and public or private investment in more formal poultry infrastructure are shaping the poultry processing equipment market.

Competitive Landscape

The Poultry Processing Equipment Market remains moderately concentrated. A small group of full-line multinational suppliers leads major plant builds and expansion projects, while a broader set of specialists serves retrofits, component systems, and regional service demand. The most significant competitive shift is expected in January 2025, when JBT Corporation completes its acquisition of Marel hf for approximately USD 4.27 billion, creating a stronger integrated supplier platform in protein equipment. The combined company is expected to report USD 3.8 billion in 2025 revenue and identify the recovery in poultry-led protein demand as an important performance support factor. This development raises the threshold for smaller competitors, as integrated hardware, software, and lifecycle support increasingly influence large tenders more than machine capability alone.

Other suppliers are responding with faster innovation cycles and sharper product positioning in thepoultry processing equipment market. Meyn is expected to use VIV Europe 2026 to introduce the Maestro M4.0 Pro Series, built around the Eviscerator Prime, with performance above 99% across birds with up to 20% weight variation. This strengthens its position in advanced evisceration systems. BAADER is expected to use the same event to highlight the Front Half Deboner 6630 and ClassifEYE, reinforcing its move into AI-supported deboning and inline vision inspection. GEA is expected to expand its presence in value-added processing with the MultiJector 500 and CookStar First launches during 2026, targeting flexible marination and thermal processing needs in small and mid-capacity facilities. Duravant’s Foodmate APEX world premiere also signals stronger competition, as challengers target the high-yield automated white meat segment with tightly integrated inline systems.

Competition in the poultry processing equipment market is also shifting toward recurring revenue, digital monitoring, and service-led retention. JBT Marel is expected to disclose that around 50% of its 2025 revenue comes from recurring sources, highlighting the growing importance of aftermarket service, consumables, and digital subscriptions in supplier strategies. This trend creates opportunities for large suppliers with broad installed bases. However, it also leaves room for regional and mid-market companies that can offer lower-cost solutions in smallholder formalization markets across South Asia and Africa. Overall, the Poultry Processing Equipment Market is likely to remain defined by a few broad-line leaders, active innovation from established challengers, and selective opportunities for specialized players that can address local cost and service constraints.

Poultry Processing Equipment Industry Leaders

-

Marel hf

-

John Bean Technologies Corporation

-

GEA Group AG

-

BAADER Group

-

Meyn Food Processing Technology B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Duravant/Foodmate to Unveil APEX White Meat Deboning System at VIV Europe: Duravant will present the Foodmate APEX, a fully automated, integrated, and synchronized inline white meat deboning system, at its world premiere at VIV Europe 2026 in Utrecht, Netherlands.

- June 2026: BAADER to Launch Front Half Deboner 6630 and ClassifEYE at VIV Europe: BAADER will demonstrate the new Front Half Deboner 6630 at VIV Europe. The system integrates AI-based vision technology to continuously monitor yield and detect residual meat without manual scrape tests. The company will also showcase the ClassifEYE vision system for inline evisceration deviation detection and introduce the new Leg Processor 6340 for high-precision anatomical cuts.

- April 2026: GEA Launches MultiJector 500 Brine Injection System: GEA expanded its injection portfolio with the MultiJector 500, a modular brine injection system designed for small-to-mid-capacity marination lines handling poultry, ham, and fish. Its ScreenFilter module specifically addresses clogged-needle downtime in poultry applications, where protein release into recirculated brine creates contamination risks.

- September 2025: JBT Marel Partners with De Heus on Vietnam Greenfield Plant: JBT Marel began fully equipping De Heus’s greenfield poultry processing plant in Tây Ninh, Vietnam. The facility is engineered to process 6,000 birds per hour, with back-end infrastructure pre-built to support expansion to 12,000 birds per hour. It is positioned as a regional reference facility for Southeast Asia.

Global Poultry Processing Equipment Market Report Scope

| Slaughtering and Defeathering |

| Cut-up and Portioning |

| Chilling and Cooling |

| Deboning |

| Evisceration |

| Quality Control and Inspection |

| Other Equipment Type |

| Fully Automated |

| Semi-automatic |

| Manual |

| Smart and Ai-Enabled |

| Chicken |

| Turkey |

| Duck |

| Other Poultry Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Morocco | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Equipment Type | Slaughtering and Defeathering | |

| Cut-up and Portioning | ||

| Chilling and Cooling | ||

| Deboning | ||

| Evisceration | ||

| Quality Control and Inspection | ||

| Other Equipment Type | ||

| By Automation Level | Fully Automated | |

| Semi-automatic | ||

| Manual | ||

| Smart and Ai-Enabled | ||

| By Application | Chicken | |

| Turkey | ||

| Duck | ||

| Other Poultry Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Morocco | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Poultry Processing Equipment Market?

The Poultry Processing Equipment Market stands at USD 7.06 billion in 2026 and is projected to reach USD 8.96 billion by 2031 at a 4.9% CAGR.

Which equipment category leads demand?

Cut-up and Portioning led with 22.89% share in 2025 because portion-specific supply for foodservice and retail keeps automated cutting lines central to processor capex.

Which automation level is growing the fastest?

Fully Automated systems are forecast to grow at 6.21% CAGR through 2031 as large processors in North America and Europe move further into full-line automation.

Why is inspection equipment gaining importance?

Quality Control and Inspection is growing at 5.74% CAGR because processors want one investment that supports compliance, defect detection, and yield recovery at the same time

Page last updated on: