Portugal Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

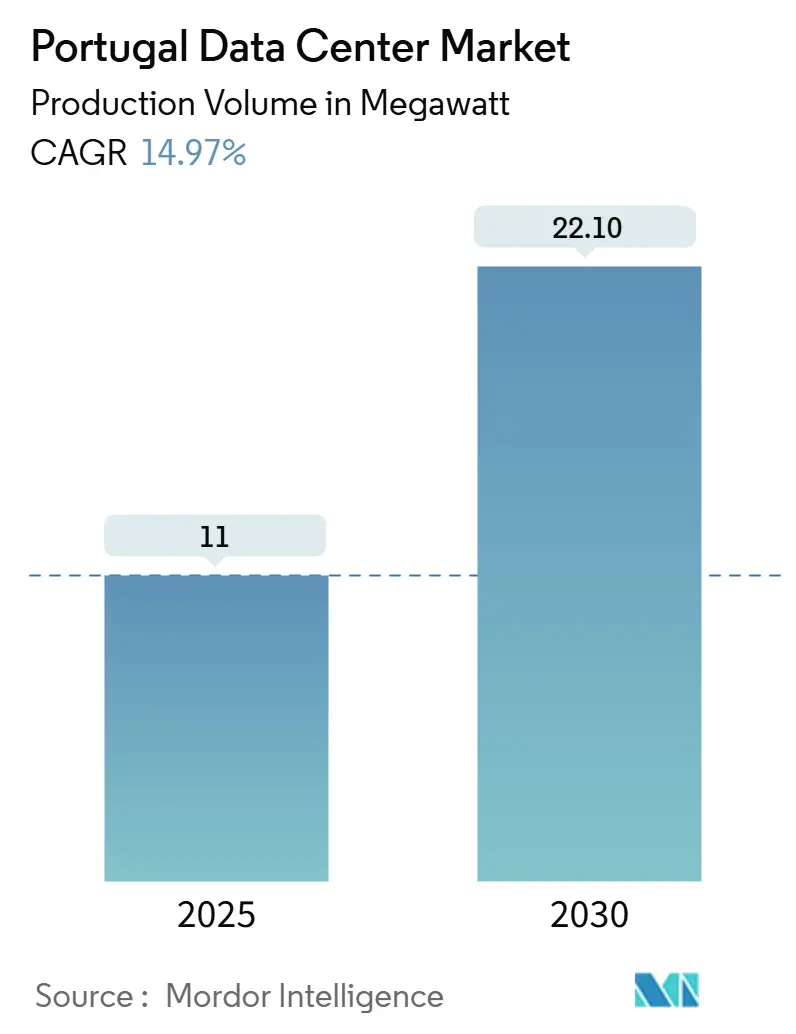

| Market Volume (2025) | 11 megawatt |

| Market Volume (2030) | 22.10 megawatt |

| Growth Rate (2025 - 2030) | 14.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Data Center Market Analysis by Mordor Intelligence

The Portugal data center market size stands at an installed IT load of 11 MW in 2025 and is projected to reach 22.1 MW by 2030, reflecting a 14.97% CAGR. Demand is fueled by hyperscale cloud regions, direct trans-Atlantic cables, and the country’s 87.4% renewable-power mix, which together lower latency and operating costs. Strategic positioning between Europe, the Americas, and Africa allows the Portugal data center market to capture traffic that once bypassed Southern Europe. Robust submarine routes have also prompted operators to shift from speculative builds to AI-ready campuses, creating strong pull-through for power-dense infrastructure. Financing momentum remains high, with EUR 12 billion (USD 13.0 billion) committed through 2030 to expand capacity, edge nodes, and grid-stabilizing renewables.

Key Report Takeaways

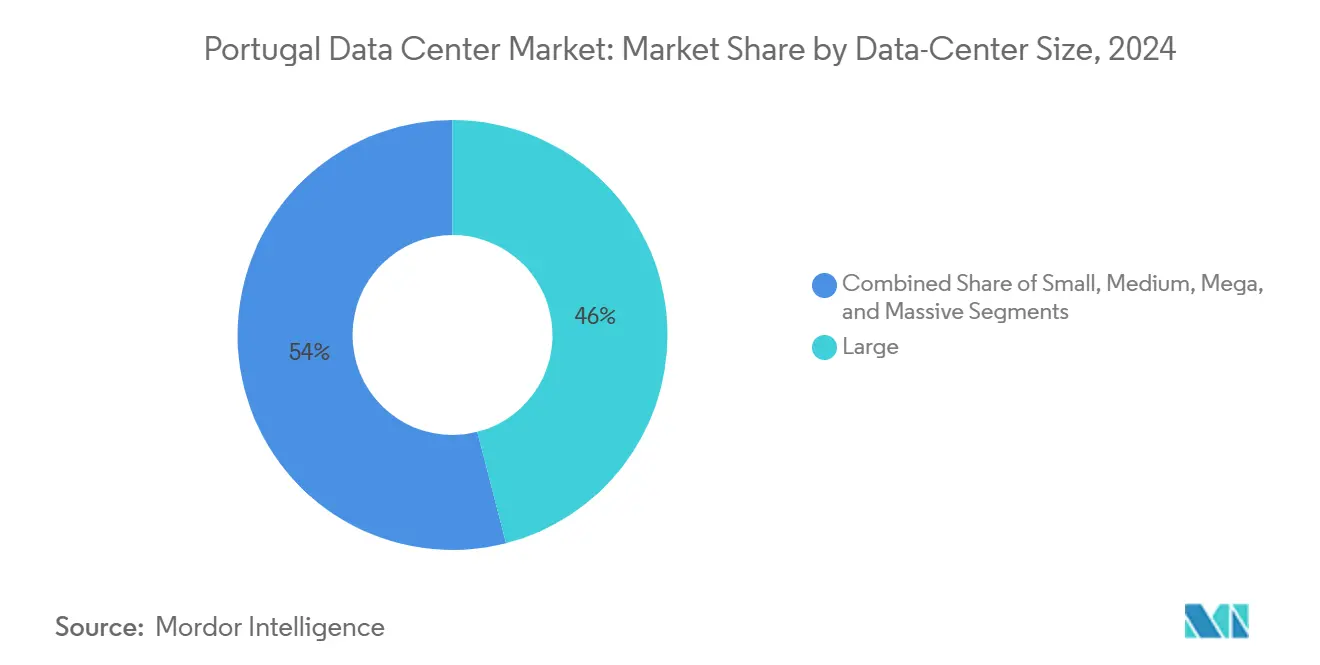

- By data center size, large facilities led with 46% of Portugal data center market share in 2024, while the Massive segment is forecast to expand at a 19.40% CAGR to 2030.

- By tier standard, Tier III captured 58% of deployments in 2024; Tier IV is projected to grow at a 15.70% CAGR through 2030.

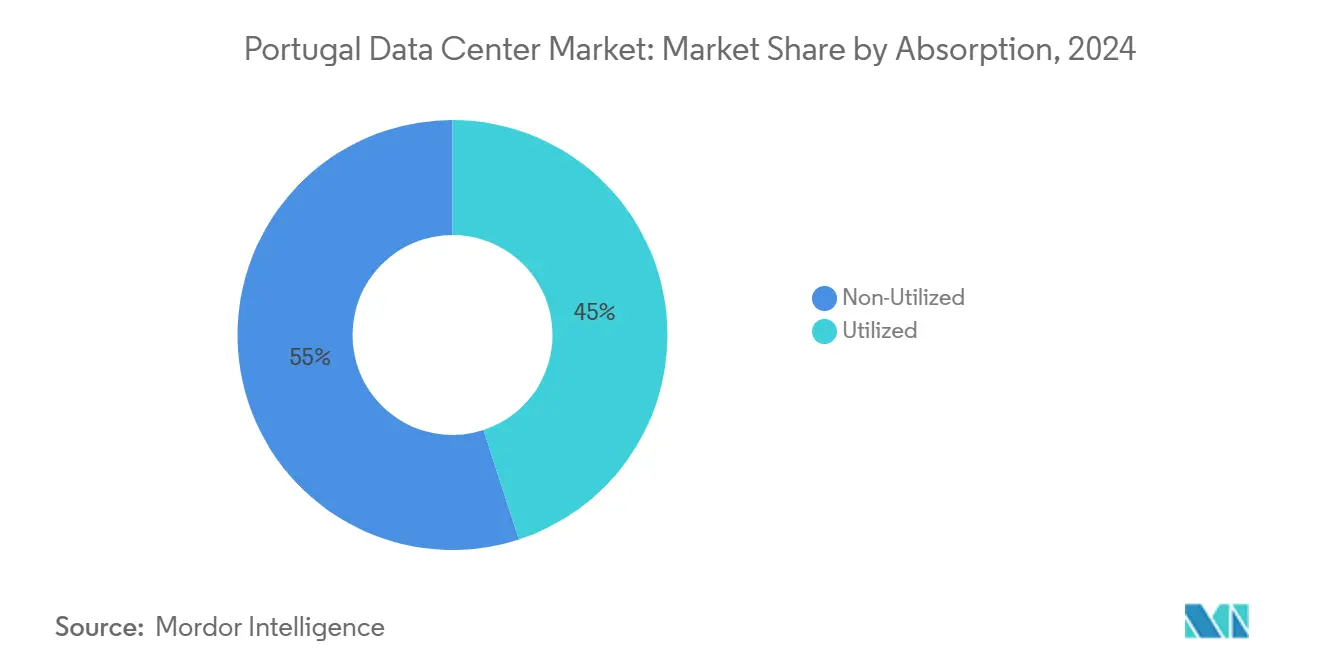

- By absorption, the utilized category accounted for 45% of the Portugal data center market size in 2024 and will rise at a 15.50% CAGR to 2030.

- By hotspot, Lisbon Metro held 52% of installed load in 2024, whereas Sines Coastal Hub is advancing at a 16.00% CAGR between 2025-2030.

Portugal Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud expansion | +3.20% | Lisbon Metro; national spillover | Medium term (2-4 years) |

| Submarine-cable Atlantic gateway | +2.80% | Sines and Lisbon | Long term (≥4 years) |

| Renewable-energy surplus | +2.10% | National; strongest coastal | Long term (≥4 years) |

| Sovereign-cloud localization mandates | +1.80% | National | Medium term (2-4 years) |

| AI/HPC workload spill-over | +1.50% | Lisbon; Sines | Short term (≤2 years) |

| Green-hydrogen PPAs | +1.30% | Coastal and industrial zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud Expansion Drives Infrastructure Transformation

Microsoft’s Lisbon Azure region and Google’s planned cloud zone confirm Portugal’s graduation to primary European destination status. The Portugal data center market benefits from EllaLink’s 50% latency reduction to Latin America, enabling single-region deployments for multinational workloads. Hyperscale footprints also lift demand for Massive buildings, whose 19.40% CAGR reflects economics favoring 50-100 MW blocks for AI clusters. Local EPC firms now pre-qualify equipment for 65 kW racks while utilities fast-track dual-feed substations to support ≥100 MVA connections. As hyperscale operators standardize on 100% renewable energy, campus-level power-purchase agreements deepen integration between the digital and energy sectors.

Submarine Cable Infrastructure Creates Atlantic Gateway Advantage

Portugal's transformation into an Atlantic connectivity hub stems from strategic investments in submarine cables, positioning the country as a critical interconnection point between three continents. The EllaLink system, with 100 Tbps capacity and landing points in both Sines and Lisbon, establishes Portugal as the primary European gateway to Latin America.[1]European Commission, “EllaLink – Connectivity Between Europe and Latin America,” ec.europa.eu Google's Equiano cable connects Portugal to South Africa with branches to multiple African countries, while the Nuvem cable extension to the Azores enhances network resilience and provides additional routing options for Submarine Networks. These infrastructure developments enable content delivery networks and financial services to establish single European locations serving global markets. The concentration of submarine cables also attracts internet exchange points, with DE-CIX expanding its presence to both Lisbon and Sines facilities.

Renewable Energy Surplus Enables Competitive Power Economics

Portugal's renewable energy generation rate of 87.4% creates structural cost advantages for data center operations, particularly as AI workloads drive power density increases across the industry.[2]Start Campus, “Start Campus Inaugurates SIN01 Data Center,” startcampus.ptThe country's National Plan for Energy and Climate targets 93% renewable electricity consumption by 2030, supported by competitive auctions for solar and wind capacity. EDP's exploration of data center sites with over 2 GW of quick network access demonstrates how energy companies are positioning Portugal as a destination for power-intensive computing workloads. Seawater cooling systems, implemented at facilities like Start Campus's Sines DC, achieve PUE ratings of 1.1 while eliminating freshwater consumption for cooling purposes. For instance, the EDP-MERLIN partnership near Lisbon features Portugal's largest decentralized solar project, which has the potential to reach a 100 MWp capacity, powering carbon-neutral data center operations.

Sovereign Cloud Mandates Accelerate Public Sector Adoption

European data sovereignty requirements, reinforced by GDPR and national cybersecurity frameworks, drive public sector demand for locally-operated cloud infrastructure. Portugal's implementation of Law 58/2019 establishes the Comissão Nacional de Proteção de Dados (CNPD) as the national supervisory authority, creating compliance requirements that favor domestic data center operations. The Portuguese National Cybersecurity Centre's framework requires organizations to implement security measures aligned with local regulations, particularly for critical infrastructure operators. Government digitalization initiatives, including the National Action Plan for Digital Transition, prioritize secure data processing capabilities within Portuguese borders. Banking sector compliance demonstrates this trend, with Millennium bcp implementing infrastructure solutions that reduce operational complexity while maintaining regulatory adherence. The cybersecurity job market's projected 8% annual growth through 2029 reflects increasing demand for local expertise in data protection and sovereign cloud operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Iberian grid congestion around Lisbon | -2.30% | Lisbon Metro, surrounding municipalities | Short term (≤ 2 years) |

| Scarcity of Tier III/IV certified O and M talent | -1.80% | National, acute in specialized roles | Medium term (2-4 years) |

| Slow permitting cycle for high-voltage interconnects | -1.20% | National, regulatory bottlenecks | Medium term (2-4 years) |

| Rising insurance premiums for coastal campuses | -0.90% | Coastal regions, seismic risk zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Infrastructure Constraints Limit Expansion Velocity

The April 2025 Iberian Peninsula blackout exposed critical vulnerabilities in Portugal's electrical grid that directly impact data center reliability and expansion plans. Internet traffic dropped by 90% during the outage, demonstrating the interdependence between power infrastructure and digital services. European data center operators face 5-8 year wait times for grid connections, with Portugal experiencing similar constraints despite renewable energy abundance. EDP acknowledges the need for 50% increases in electrical network investment between 2026-2030 to support growing data center demand, while current low returns on investment in Portugal complicate infrastructure financing. Grid instability concerns intensify with high renewable energy penetration, as the blackout analysis revealed challenges in managing frequency oscillations and voltage control during generation loss events.[3]Baker Institute, “The Iberian Peninsula Blackout — Causes, Consequences, and Challenges Ahead,” bakerinstitute.org

Talent Scarcity Constrains Operational Excellence

Portugal ranks as the 4th most difficult country globally for hiring technology talent, creating operational bottlenecks for data center expansion. The cybersecurity sector faces a 30% job vacancy rate despite government commitments to train 1,000 students by 2025, indicating structural mismatches between educational output and industry requirements. Tier III and Tier IV data center operations require specialized skills in critical systems management, power distribution, and cooling optimization that are scarce in the Portuguese market. For instance, Cloudflare's criticism of Portuguese bureaucracy and immigration processes reflects broader challenges in attracting international talent to support data center operations. The mismatch between educational curricula and market demands, combined with talent emigration to higher-paying European markets, constrains the availability of qualified operations and maintenance personnel for sophisticated data center environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Size: Massive Facilities Drive Hyperscale Adoption

Large data centers commanded 46% market share in 2024, reflecting the predominance of traditional enterprise and colocation facilities across Portugal's established markets. However, Massive data centers represent the fastest-growing segment at 19.40% CAGR through 2030, driven by hyperscale operators seeking economies of scale for AI and high-performance computing workloads. Start Campus's Sines DC exemplifies this trend, with 1.2 GW total capacity distributed across six buildings, positioning it as Europe's largest colocation campus. Medium facilities serve regional enterprise customers and edge computing applications, while Small deployments support local connectivity and content delivery requirements.

The shift toward Massive facilities reflects fundamental changes in data center economics and operational requirements. Hyperscale operators leverage larger deployments to optimize power distribution, cooling efficiency, and network interconnection costs, achieving operational advantages unavailable in smaller formats. For instance, Start Campus's seawater cooling system and 100% renewable energy sourcing become economically viable only at massive scale, delivering PUE ratings of 1.1 across the entire campus. The concentration of submarine cable landing points in Sines and Lisbon further advantages Massive facilities, as operators can justify the infrastructure investments required for direct fiber connectivity to multiple international cables.

By Tier Standard: Tier IV Expansion Reflects Mission-Critical Demands

Tier III facilities dominate the Portuguese market with 58% share in 2024, representing the standard for enterprise and cloud service provider deployments requiring high availability without the cost premium of Tier IV infrastructure. However, Tier IV facilities exhibit the strongest growth trajectory at 15.70% CAGR through 2030, driven by financial services, government agencies, and hyperscale operators with zero-tolerance downtime requirements. The growth in Tier IV deployments reflects Portugal's evolution from a secondary European market to a primary location for mission-critical workloads serving global customers.

Tier I and II facilities serve cost-sensitive applications and development environments, though their market share continues declining as operators standardize on higher resilience levels. The Portuguese government's sovereign cloud requirements and GDPR compliance mandates favor Tier III and IV facilities, as these standards provide the redundancy and security controls required for sensitive data processing. Digital Realty's focus on 99.999% uptime across its global portfolio demonstrates how international operators are raising baseline reliability standards, influencing local market expectations and driving Tier IV adoption.

By Absorption: Utilized Capacity Optimization Drives Efficiency

The Utilized segment represents 45% of total market absorption in 2024 and is projected to grow at a 15.50% CAGR through 2030, reflecting operators' focus on maximizing returns on infrastructure investments through improved capacity planning and deployment strategies. Non-utilized capacity serves as a strategic reserve for rapid expansion and disaster recovery requirements; however, operators are increasingly minimizing idle capacity through just-in-time provisioning and modular deployment approaches. The growth in utilized capacity reflects Portugal's maturation from a speculative market to an operational hub with predictable demand patterns.

Within the Utilized segment, Hyperscale colocation drives the highest growth rates as cloud service providers establish a presence in Portugal to serve European and Latin American markets simultaneously. Retail colocation serves traditional enterprise customers migrating from on-premises infrastructure, while Wholesale arrangements support large-scale deployments by telecommunications operators and content delivery networks. For instance, Equinix's Lisbon facility offers interconnection services to over 50 networksfacilitatingng efficient traffic exchange and reducing latency for content providers serving both Portuguese and international audiences. The concentration of submarine cables creates natural wholesale opportunities, as operators can offer direct access to international connectivity without intermediate network hops.

By Hotspot: Sines Emerges as Hyperscale Destination

Lisbon Metro maintains 52% market share in 2024, leveraging its position as Portugal's economic center and primary international connectivity hub with established fiber infrastructure and skilled workforce availability. However, Sines Coastal Hub represents the fastest-growing geographic segment at 16.00% CAGR through 2030, driven by purpose-built hyperscale facilities and direct submarine cable access. Rest of Portugal serves regional markets and edge computing applications, though growth remains constrained by limited fiber infrastructure and power availability outside major metropolitan areas.

Sines' emergence as a hyperscale destination reflects strategic advantages unavailable in traditional urban locations, including abundant land availability, seawater cooling access, and direct submarine cable landings without urban fiber routing constraints. The EllaLink cable system's primary landing point in Sines provides operators with direct access to Latin American markets, while the planned Sines-Lisbon fiber connection will enable seamless integration with existing Portuguese networks. Start Campus's EUR 8.5 billion (USD 9.83 billion) investment demonstrates the scale of commitment to Sines as a data center destination, with the first 26 MW facility operational and construction beginning on additional buildings. The Portuguese government's designation of the Sines project as a National Interest Project reflects official recognition of its strategic importance for the country's digital infrastructure development.

Geography Analysis

Lisbon Metro dominates the Portuguese data center market with 52% share in 2024, benefiting from its role as the country's primary economic and technological hub with established telecommunications infrastructure and proximity to international submarine cable landing points. The region's growth prospects remain strong through 2030, supported by continued enterprise digital transformation and the expansion of cloud service provider presence. Major developments include AtlasEdge's 20 MW facility development and Equinix's planned expansion in Alcochete, demonstrating sustained investor confidence in the metropolitan market. The concentration of Portugal's technology workforce in Lisbon provides operational advantages for data center operators, though rising real estate costs and grid congestion constraints may limit future expansion velocity. Cloudflare's establishment of its EMEA technical hub in Lisbon, expanding from 14 to over 350 employees since 2019, illustrates the region's attractiveness for international technology companies despite bureaucratic challenges.

Sines Coastal Hub emerges as the fastest-growing geographic segment at 16.00% CAGR through 2030, transforming from an industrial port into Portugal's primary hyperscale data center destination through strategic infrastructure investments and government support. Start Campus's EUR 8.5 billion (USD 9.83 million) investment in a 1.2 GW campus represents Europe's largest sustainable data center project, leveraging seawater cooling and 100% renewable energy to achieve industry-leading efficiency metrics. The region's advantages include direct submarine cable access through EllaLink and future systems, abundant land availability for large-scale development, and proximity to renewable energy generation without urban constraints. The Portuguese government's EUR 3.5 billion (USD 4.05 billion) foreign investment announcement for Sines reflects official recognition of the region's strategic importance for digital infrastructure development. DE-CIX's expansion to Sines demonstrates how internet exchange operators are following data center investments to provide interconnection services in emerging markets.

Rest of Portugal represents emerging opportunities for edge computing and regional data center deployments, though growth remains constrained by limited fiber infrastructure and power grid capacity outside major metropolitan areas. NOS's EUR 6 million (USD 6.94 million) investment in the Litoral Alentejano region, doubling fiber connectivity and increasing mobile network capacity by 150%, demonstrates how telecommunications operators are expanding infrastructure to support distributed computing requirements. The region's potential lies in supporting latency-sensitive applications for manufacturing and logistics operations, as demonstrated by Ericsson and Vodafone's private 5G deployment at CIMPOR's cement plant in Alhandra, enabling IoT sensors and autonomous device operation for industrial optimization. CTS Group and Eaton's strategic investment in Viana do Castelo for data center industry development signals growing recognition of regional opportunities beyond traditional metropolitan markets.

Competitive Landscape

The five largest operators command 58% of installed load, leaving room for niche entrants in sovereign cloud and edge hosting. Start Campus leads with a 1.2 GW masterplan and has signed liquid-cooling deals with JetCool for 100 kW racks. Equinix scales interconnection services in Alcochete, launching metro-edge fabrics that link 50+ carriers to hyperscale availability zones. Digital Realty secured “AI Data Centre of the Year” honors after deploying immersion-cooling suites that cut AI cluster energy use by 15%.

Local telcos NOS and Altice differentiate through managed networks and compliance hosting tailored to Portuguese-language workloads. NOS’s acquisition of Claranet strengthens cloud migration offerings for SMEs, while Altice leverages wholesale dark fiber to attract French OTT providers looking for EU-sovereign redundancy. The April 2025 power outage reordered buyer priorities toward diversified utility feeds and in-country megawatt-class battery farms, spurring investment in 4-hour lithium-iron-phosphate systems.

EDP partners with MERLIN Edged on a 100 MWp solar farm tied directly to a Tier IV campus near Vila Franca de Xira. Meanwhile, CTS Group and Eaton invest in prefab module production in Viana do Castelo, shortening lead times for power-skid assemblies by 20%. As AI cluster densities climb, suppliers of cold-plate manifolds, high-capacity busways, and 48 VDC power trains gain negotiating leverage.

Portugal Data Center Industry Leaders

Start Campus (SINES DC)

Equinix Portugal

Digital Realty / Interxion Lisbon

Colt Data Centre Services

Altice Portugal / Portugal Telecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: EDP announced its largest decentralized solar energy project partnership with MERLIN Edged to power Portugal's first carbon-neutral data center campus near Vila Franca de Xira, potentially reaching 100 MWp capacity with 24/7 renewable electricity supply.

- June 2025: Start Campus began construction of its second data center building (SIN02) in Sines, following the successful operation of SIN01 with 26 MW capacity and targeting completion by 2026 with up to 180 MW IT capacity.

- April 2025: Reuters reported Start Campus plans to invest USD 9.35 billion in Portugal data hub development, significantly expanding the original Sines DC project scope.

- April 2025: Colt Technology Services sold its European data centers to NorthC, indicating strategic portfolio optimization and potential market consolidation in the European data center sector.

- March 2025: NOS acquired Claranet Portugal, expanding its cloud and data analytics capabilities while reinforcing its position in the Portuguese enterprise market.

- February 2025: CTS Group and Eaton announced strategic investment in Viana do Castelo focusing on data center industry development, expanding infrastructure capabilities beyond traditional metropolitan markets.

Portugal Data Center Market Report Scope

Portugal Data Center Market is Segmented by Data-Center Size (Small, Medium, Large, Mega, Massive), Tier Standard (Tier I and II, Tier III, Tier IV), Absorption (Non-Utilized, Utilized (Colocation Type (Hyperscale, Retail, Wholesale), End-User (BFSI, Cloud Service Providers, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End-Users)), and Hotspot (Lisbon Metro, Sines Coastal Hub, Rest of Portugal). The Market Forecasts are Provided in Terms of Volume (MW).

| Small |

| Medium |

| Large |

| Mega |

| Massive |

| Tier I and II |

| Tier III |

| Tier IV |

| Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale |

| Retail | ||

| Wholesale | ||

| By End-User | BFSI | |

| Cloud Service Providers | ||

| E-Commerce | ||

| Government | ||

| Manufacturing | ||

| Media and Entertainment | ||

| Telecom | ||

| Other End-Users | ||

| Lisbon Metro |

| Sines Coastal Hub |

| Rest of Portugal |

| By Data-Center Size | Small | ||

| Medium | |||

| Large | |||

| Mega | |||

| Massive | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By Absorption | Non-Utilized | ||

| Utilized | By Colocation Type | Hyperscale | |

| Retail | |||

| Wholesale | |||

| By End-User | BFSI | ||

| Cloud Service Providers | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End-Users | |||

| By Hotspot | Lisbon Metro | ||

| Sines Coastal Hub | |||

| Rest of Portugal | |||

Key Questions Answered in the Report

How large is the Portugal data center market in 2025?

Installed IT load reaches 11 MW in 2025 and is projected to double to 22.1 MW by 2030.

What is driving new hyperscale builds in Portugal?

Direct trans-Atlantic cables, 87.4% renewable power, and Lisbon’s new Azure and Google regions attract 50 MW-plus campuses.

Which region is growing fastest for facilities?

Sines Coastal Hub leads with a 16.00% CAGR thanks to abundant land, seawater cooling, and immediate access to EllaLink and Equiano cables.

Why is Tier IV adoption accelerating?

Financial, public-sector, and AI workloads require 99.999% uptime and concurrently maintainable systems, pushing Tier IV to a 15.70% CAGR.

What challenges could slow expansion?

Grid congestion around Lisbon and a 30% cybersecurity talent gap raise costs and delay project timelines.

How sustainable are Portuguese data centers?

Operators leverage seawater cooling and sub-EUR 0.03/kWh solar PPAs, achieving PUE as low as 1.1 with 100% renewable energy feeds.

Page last updated on: