Polyethylene Terephthalate (PET) Fiber Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

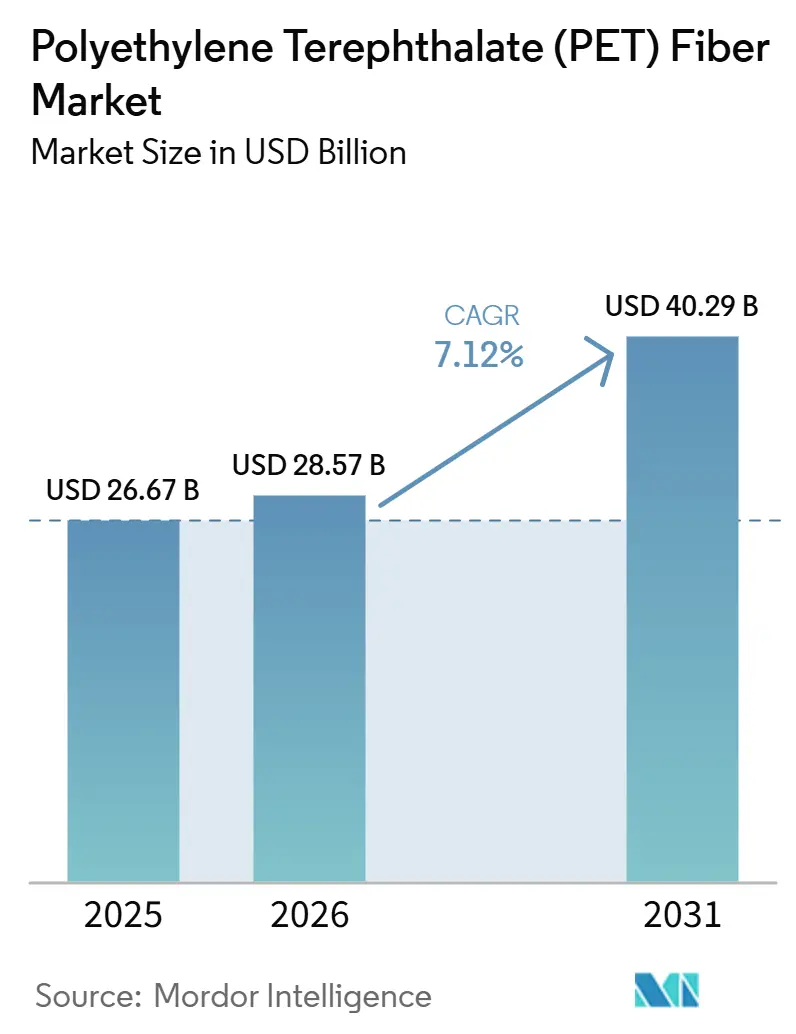

| Market Size (2026) | USD 28.57 Billion |

| Market Size (2031) | USD 40.29 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

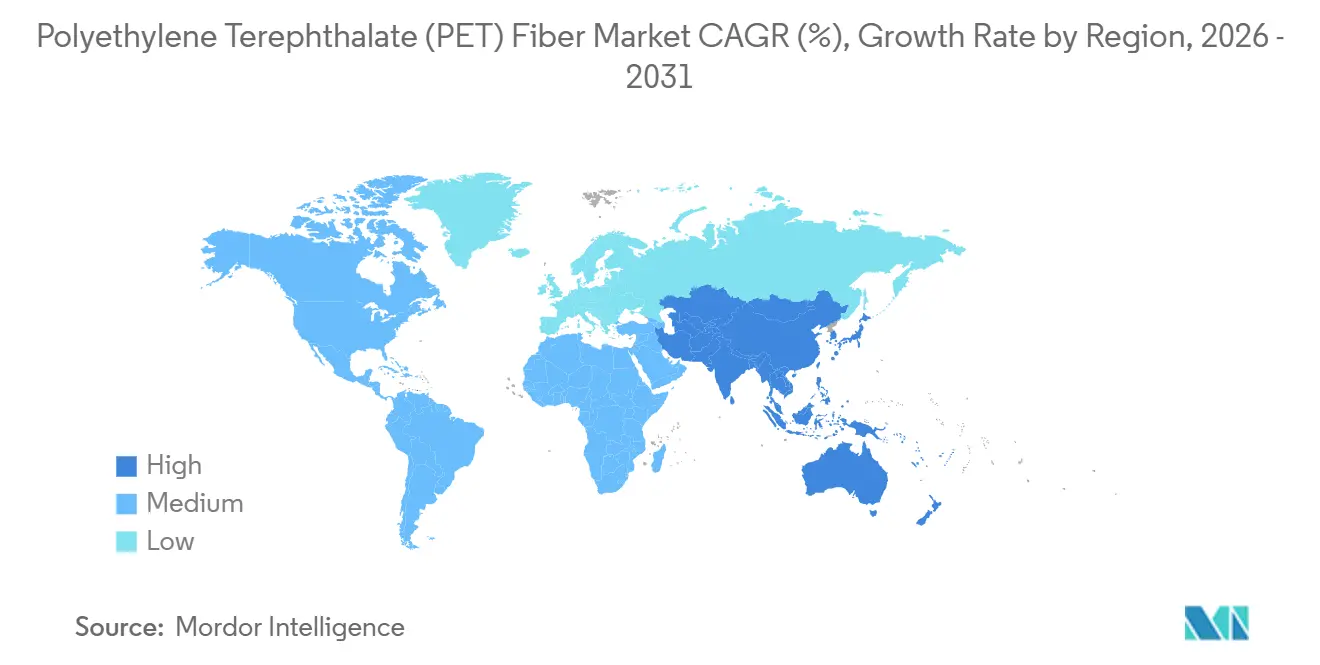

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyethylene Terephthalate (PET) Fiber Market Analysis by Mordor Intelligence

The Polyethylene Terephthalate Fiber Market size is expected to increase from USD 26.67 billion in 2025 to USD 28.57 billion in 2026 and reach USD 40.29 billion by 2031, growing at a CAGR of 7.12% over 2026-2031. As recycled-content rules steer PET flake towards fiber, demand surges. AI-driven spinning systems cut defect rates, and automakers are opting for lightweight PET nonwovens, enhancing electric vehicle ranges. While staple fiber remains a significant contributor to revenue, continuous-filament grades are witnessing a quicker expansion, driven by stringent tensile-strength demands in airbags, tire cords, and geotextiles. The Asia-Pacific region continues to dominate the market and leads capacity expansions. Meanwhile, North American mills are capitalizing on Inflation Reduction Act credits, narrowing the cost gap with Asian imports. Diverging regulations are disrupting trade flows, prompting vertically integrated companies to set up regional hubs. These hubs aim to meet local-content incentives and reduce tariff risks.

Key Report Takeaways

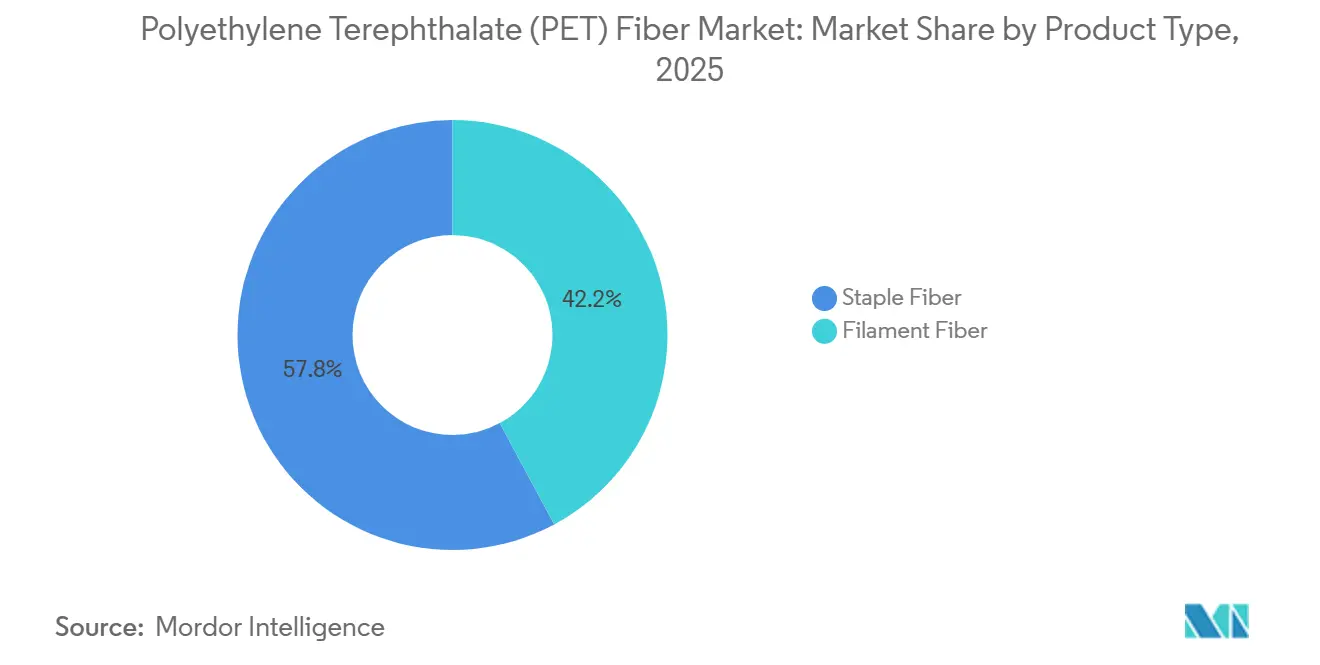

- By product type, staple fiber held 57.84% of the polyethylene terephthalate fiber market share in 2025, whereas filament fiber is poised to record a 7.62% CAGR during the forecast period (2026-2031).

- By application, textiles led with 48.26% revenue share in 2025, while automotive is forecast to expand at an 8.41% CAGR during the forecast period (2026-2031).

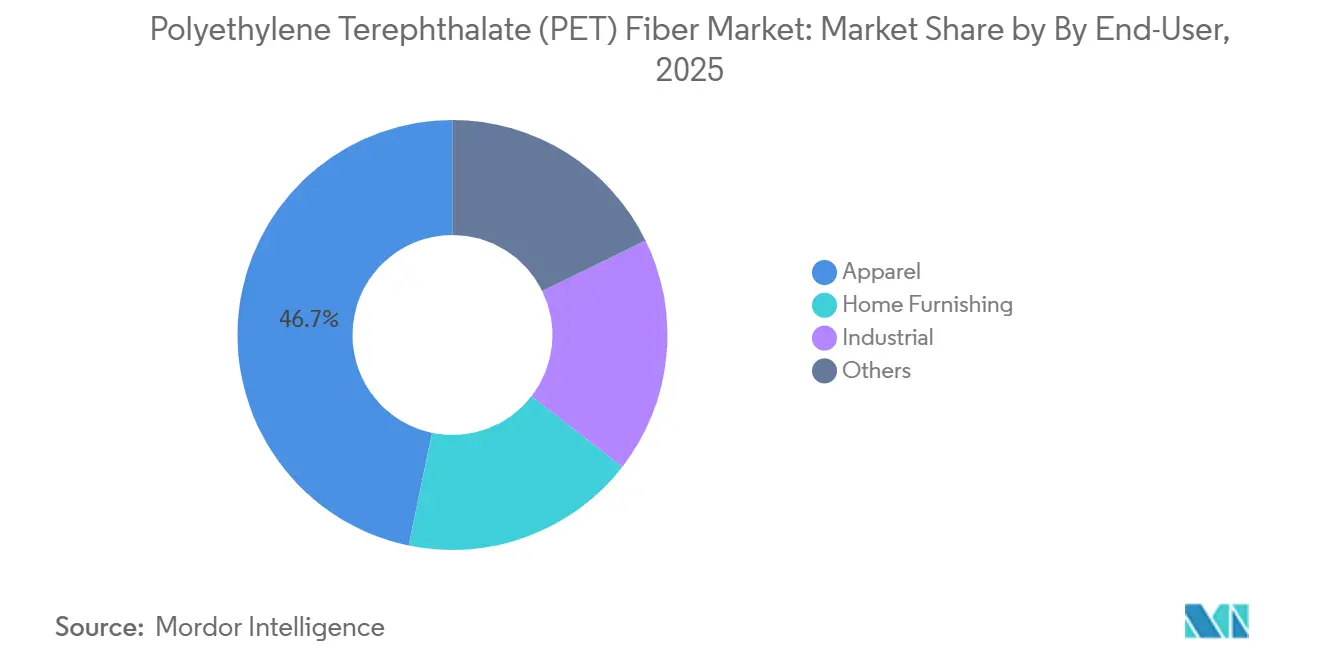

- By end-user, apparel commanded 46.73% of 2025 spending, but the industrial segment is projected to advance at an 8.08% CAGR between 2026 and 2031.

- By geography, Asia-Pacific accounted for 62.58% of 2025 revenue and is set to grow at a 7.94% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyethylene Terephthalate (PET) Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Advantage and Versatility of PET Fibers | +1.20% | Global | Long term (≥ 4 years) |

| Rising Demand for Performance Textiles and Activewear | +1.50% | North America and EU, Asia-Pacific spillover | Medium term (2-4 years) |

| Recycled-Content Mandates Boost Fiber Uptake | +1.80% | EU core, North America and Asia-Pacific adoption | Short term (≤ 2 years) |

| Expansion of Technical and Industrial Applications | +1.30% | Global, concentrated in Asia-Pacific and the Middle-East | Medium term (2-4 years) |

| AI-Enabled Spinning Control Enhancing Yield and Quality | +0.80% | Asia-Pacific core, early pilots in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Advantage and Versatility of PET Fibers

PET’s melt-spinning route circumvents water-intensive ginning and carding, lowering installed-capacity capex by roughly 40% versus cotton systems. Competitive delivered costs let converters price staple below cotton-polyester blends in furnishings and industrial cloth, while chemical inertness and UV stability widen use in geotextiles and filtration. Copolymer tweaks, adding isophthalic acid or diethylene glycol, shift glass-transition temperature and dye affinity without new hardware, enabling quick grade changes for diverse markets. Because the same extruders produce both staple and filament, plants flex capacity toward whichever grade commands better margins, further reinforcing PET’s cost moat[1]Journal of Applied Polymer Science "Artificial Neural Network and Genetic Algorithm Optimization for Polyester Yarn Quality" onlinelibrary.wiley.com.

Rising Demand for Performance Textiles and Activewear

Brands now mandate micro-denier filaments (1.0-1.5 denier per filament [dpf]) that create a softer hand and four-way stretch when co-knit with elastane. Hollow or channeled cross-sections in COOLMAX-type yarns supply moisture management with no weight penalty, prized by outdoor and military programs. Mechanically recycled REPREVE yarn already represented 31% of Unifi's FY 2025 sales and targeted more than 50% by 2030. EU Ecodesign rules entering into force in 2028 add further pull by requiring traceable recycled content, compelling mills to lock in recycled PET (rPET) supply.

Recycled-Content Mandates Boost Fiber Uptake

EU waste and packaging directives have split PET into a food-contact premium stream and a discounted colored stream. Apparel brands respond by signing tolling deals or taking equity stakes in depolymerization ventures such as Loop Industries’ 70 kilotons per year project in Gujarat, due in 2027[2]European Commission "EU Waste Framework Directive." environment.ec.europa.eu. China’s dual-carbon targets push Tongkun to invest CNY 5.6 billion (USD 0.77 billion) in differentiated fiber incorporating recycled inputs.

Expansion of Technical and Industrial Applications

Automotive trims, trunk liners, and acoustic components are transitioning from polypropylene to PET nonwovens. This change significantly reduces mass while meeting stringent Noise, Vibration, and Harshness (NVH) targets. Autoneum's Ultra-Silent Frunk, featuring a high percentage of recycled PET content, began volume production in 2025. Additionally, PET geotextiles, known for their superior tensile strength compared to polypropylene, are increasingly used for subgrade reinforcement in highway projects across Indonesia and the Middle-East. In industrial applications, dust filters and liquid cartridges are favoring PET spunbond for its chemical resistance at elevated temperatures, replacing nylon in cost-sensitive scenarios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-Linked Feedstock Price Volatility | -1.10% | Global | Short term (≤ 2 years) |

| Competition from Cotton and Bio-based Alternatives | -0.70% | Global, pronounced in North America and the EU | Medium term (2-4 years) |

| rPET Bottle-to-Bottle Demand Squeezing Fiber Feedstock | -0.90% | EU core, North America adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Crude-Linked Feedstock Price Volatility

Purified Terephthalic Acid (PTA) and Monoethylene Glycol (MEG) track with a lag, so Brent’s early-2025 rally squeezed Chinese filament margins to multi-year lows. PTA-paraxylene spreads collapsed to USD 80 per ton mid-2025 as new Asian capacity outpaced demand, forcing high-cost spinners into turnarounds. Futures hedges help, yet Brent-PTA basis swings of USD 30 per ton undermine perfect cover, pressing firms toward deeper integration.

Competition from Cotton and Bio-based Alternatives

When Intercontinental Exchange (ICE) cotton sinks below USD 0.70 per pound and Brent tops USD 90 per barrel, cotton-polyester parity surfaces, nudging mass-market T-shirt makers back to natural fiber. Simultaneously, bio-PET containing 30% renewable ethylene glycol from sugarcane attracts athletic brands angling for Scope 3 cuts. LanzaTech’s Carbon Smart route cuts greenhouse emissions by 52%, allowing the product to qualify for green-bond financing and eroding virgin-PET demand in premium sportswear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Filament Fiber Gains on Technical-Grade Demand

In 2025, staple fiber held a commanding 57.84% share of the market. Meanwhile, filament fiber is projected to grow at a 7.62% compound annual growth rate (CAGR) from 2026 to 2031, driven by its applications in airbags, seatbelts, and tire cords, all of which demand a failure tolerance of less than 1 part per million (ppm). In 2025, China introduced an additional 1.83 million tons per year (Mt/y) of partially oriented yarn (POY), primarily channeling it into draw-textured yarns for upholstery and technical fabrics. Concurrently, Filatex India is gearing up for 2026 with plans for 62 kilotons per year across its partially oriented yarn (POY), fully drawn yarn (FDY), and draw-textured yarn (DTY) lines. Filament fiber boasts lower conversion costs compared to staple fiber and minimizes cutting waste, enhancing its profit margins. On the downstream side, continuous-filament weavers are securing original equipment manufacturer (OEM) certifications, effectively sidelining competitors for contract durations of three to five years, bolstering their growth trajectory.

While staple fiber remains the go-to choice for apparel blends and home furnishings, thanks to ring and rotor systems fine-tuned for specific cuts, its growth rate is trailing behind that of filament fiber. This is particularly evident as cotton makes a comeback in leisurewear. Specialty staple varieties, including cationic-dyeable, flame-retardant, and hollow fibers, not only command a higher value but also underpin the limited new capacities emerging in the West. Beginning in 2028, the EU's Digital Product Passports mandate will enhance traceability for filament fibers, especially in contrast to multi-fiber staple yarns. Such a development is poised to channel more investments into continuous assets.

By Application: Automotive Outpaces Textiles on Lightweighting Mandates

Textiles supply 48.26% of the 2025 value, yet rise only at the market average, capped by cotton substitution in casualwear and mature-market saturation. Automotive end uses are advancing at an 8.41% CAGR from 2026 to 2031 as OEMs are replacing polypropylene with PET nonwovens to enhance EV range by reducing vehicle weight. The EU's updated mandate on End-of-Life Vehicles, requiring increased recycled content by 2030, further drives this transition. PET's compatibility with hot-melt adhesives makes it a preferred material for interior modules. While films and electronics experience steady growth, the bottle segment is focusing on lightweighting initiatives to minimize material usage per unit.

By End-User: Industrial Segment Leverages Infrastructure Tailwinds

Apparel still comprised 46.73% of 2025 spend, yet premium activewear and outdoor gear are the only robust sub-niches, underpinned by recycled filament adoption. Industrial users of geotextiles, filtration, and conveyor belts are tracking an 8.08% CAGR between 2026 and 2031, fueled by India's Bharatmala and ASEAN expressways that specify high-tenacity PET fabrics for subgrade reinforcement. Home furnishings in emerging Asia grow with urban housing but remain cyclical versus real-estate trends.

Geography Analysis

Asia-Pacific, accounting for 62.58% of 2025 revenue, is set to grow at a 7.94% CAGR from 2026 to 2031. China, with a significant share of the global filament capacity, stands as the dominant player. In a notable development, Tongkun is making a substantial investment to expand its production of green differentiated fiber. Meanwhile, India is advancing with Reliance's upcoming polyester-fiber line and Filatex's planned expansion of partially oriented yarn (POY), both expected to commence operations in 2026. Looking ahead to 2029, Brunei's Phase II aims to enhance its production of purified terephthalic acid (PTA) and polyethylene terephthalate (PET), leveraging its advantage of low-cost gas feedstock.

Despite facing high energy prices and regulatory costs, Europe and North America continue to attract niche investments. In early 2025, Alpek restarted a PET facility in the UK to enhance production capacity. On the Gulf Coast, credits from the Inflation Reduction Act are providing a modest boost to capacity. European mills are pivoting, now focusing on recycled filament and outsourcing virgin grades to Thailand. In a strategic expansion, Teijin increased its high-tenacity recycled capacity in Thailand in 2025. While South America and the Middle-East and Africa play minor roles currently, they are poised to benefit from Saudi infrastructure projects and Brazilian mining activities, both of which have a significant demand for PET geotextiles and conveyor belts.

Competitive Landscape

The Polyethylene Terephthalate (PET) Fiber Market is moderately fragmented. Commodity staple and Partially Oriented Yarn (POY) markets are fiercely price-driven, especially among Chinese mills running 75%-80% utilization. Technical-grade filament, destined for auto and industrial textiles, brings healthy premiums due to stringent Original Equipment Manufacturer (OEM) certifications.

Polyethylene Terephthalate (PET) Fiber Industry Leaders

-

Reliance Industries Limited

-

Alpek S.A.B. de C.V.

-

Far Eastern New Century Corporation

-

Indorama Ventures Public Company Limited

-

Toray Advanced Composites (Toray Industries, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UNIFI, Inc. announced its push for REPREVE recycled polyester is fueling a rising demand for sustainable PET fiber. In response, traditional producers are increasingly shifting towards circular models and adopting greener manufacturing methods.

- December 2025: Lotte Chemical and HD Hyundai invested KRW 800 billion (USD 545 million) into their Daesan joint venture to restructure their petrochemical operations and reduce ethylene and naphtha capacities. By cutting ethylene supplies, the availability of raw materials for PET fiber was tightened.

Global Polyethylene Terephthalate (PET) Fiber Market Report Scope

Polyethylene Terephthalate (PET) fiber is a strong, durable, and lightweight synthetic fiber made from polymerizing ethylene glycol and terephthalic acid. Commonly known as polyester, it is the world’s most used synthetic fiber, valued for being crease-resistant, quick-drying, and often created by recycling plastic bottles.

The Polyethylene Terephthalate (PET) Fiber market is segmented by product type, application, end-user, and geography. By product type, the market is segmented into staple fiber and filament fiber. By application, the market is segmented into textiles, bottles, films, automotive, electronics, and others. By end-user, the market is segmented into apparel, home furnishing, industrial, and others. The report also covers the market size and forecasts for PET fiber in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Staple Fiber |

| Filament Fiber |

| Textiles |

| Bottles |

| Films |

| Automotive |

| Electronics |

| Others |

| Apparel |

| Home Furnishing |

| Industrial |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Staple Fiber | |

| Filament Fiber | ||

| By Application | Textiles | |

| Bottles | ||

| Films | ||

| Automotive | ||

| Electronics | ||

| Others | ||

| By End-User | Apparel | |

| Home Furnishing | ||

| Industrial | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the Polyethylene Terephthalate (PET) Fiber Market?

The Polyethylene Terephthalate (PET) Fiber Market stands at USD 28.57 billion in 2026 and is forecast to reach USD 40.29 billion by 2031 at a 7.12% CAGR from 2026 to 2031.

Which region contributes the largest revenue today?

Asia-Pacific already accounts for about 62.58% of the value and continues to lead in new capacity.

Why is automotive demand growing faster than apparel?

Electric-vehicle lightweighting targets push automakers toward PET nonwovens that cut mass 40-50%, driving an 8.41% CAGR in automotive fiber.

What threatens fiber access to recycled PET?

EU bottle-to-bottle mandates divert clear flake into food-contact resin, tightening fiber feedstock and squeezing margins.

How are producers mitigating feedstock volatility?

Leading firms are backwardly integrating into PTA and MEG and entering chemical-recycling joint ventures to secure stable raw material flows.

Page last updated on: